Australia Freight and Logistics Market Size, Share, Trends and Forecast by Logistics Function, End Use Industry, and Region 2026-2034

Australia Freight and Logistics Market Size & Forecast 2026-2034

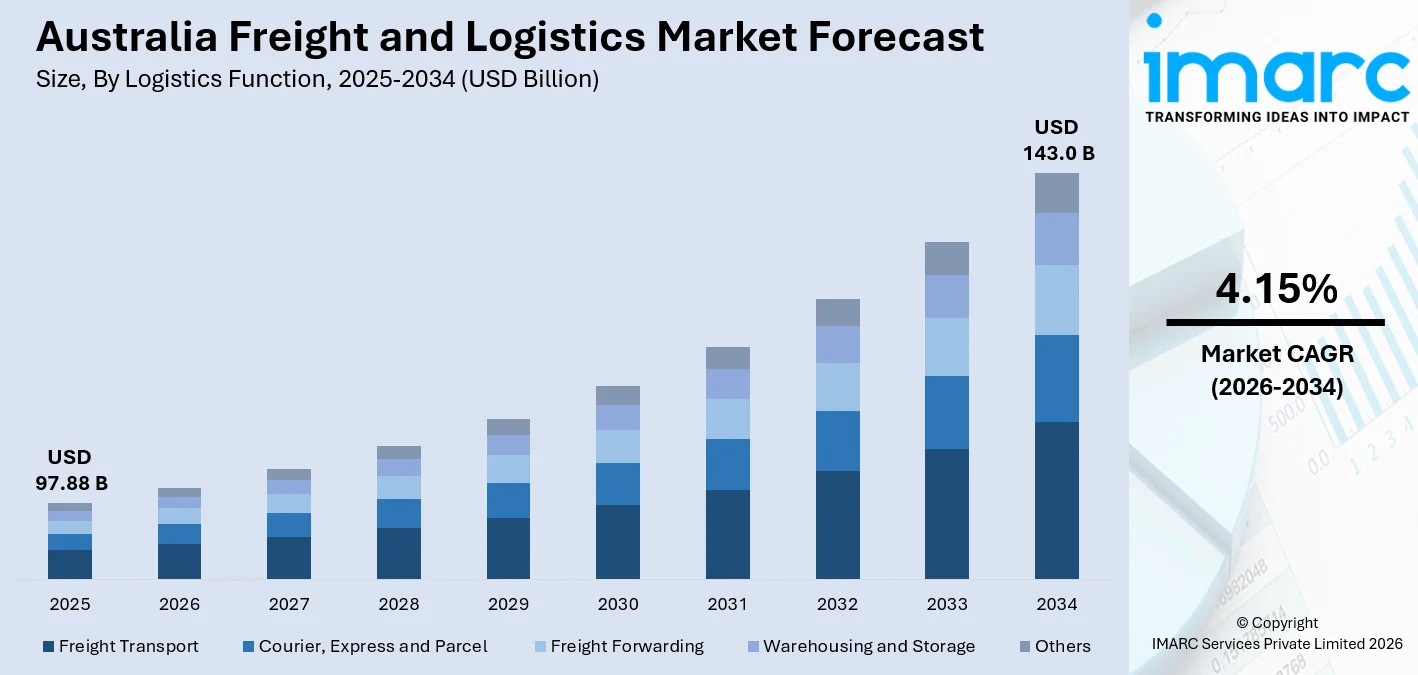

The Australia freight and logistics market size, valued at USD 97.88 Billion in 2025, is projected to reach USD 143.0 Billion by 2034, growing at a CAGR of 4.15% from 2026-2034, underpinned by the USD 31 billion Inland Rail program transforming east-coast freight economics, e-commerce-driven parcel infrastructure investment, and accelerating adoption of AI-based fleet automation and digital supply chain visibility platforms across road, rail, air, and sea modes shaping the Australia freight and logistics market share.

To get more information on this market Request Sample

Australia Freight and Logistics Industry Analysis - Key Insights

- Freight Transport commands 28% of the logistics function segment in 2025 - high-tonnage bulk commodity movements and interstate road replenishment routes anchor its lead position, with over 47,000 road freight operators serving Australia's dispersed industrial and consumer geography.

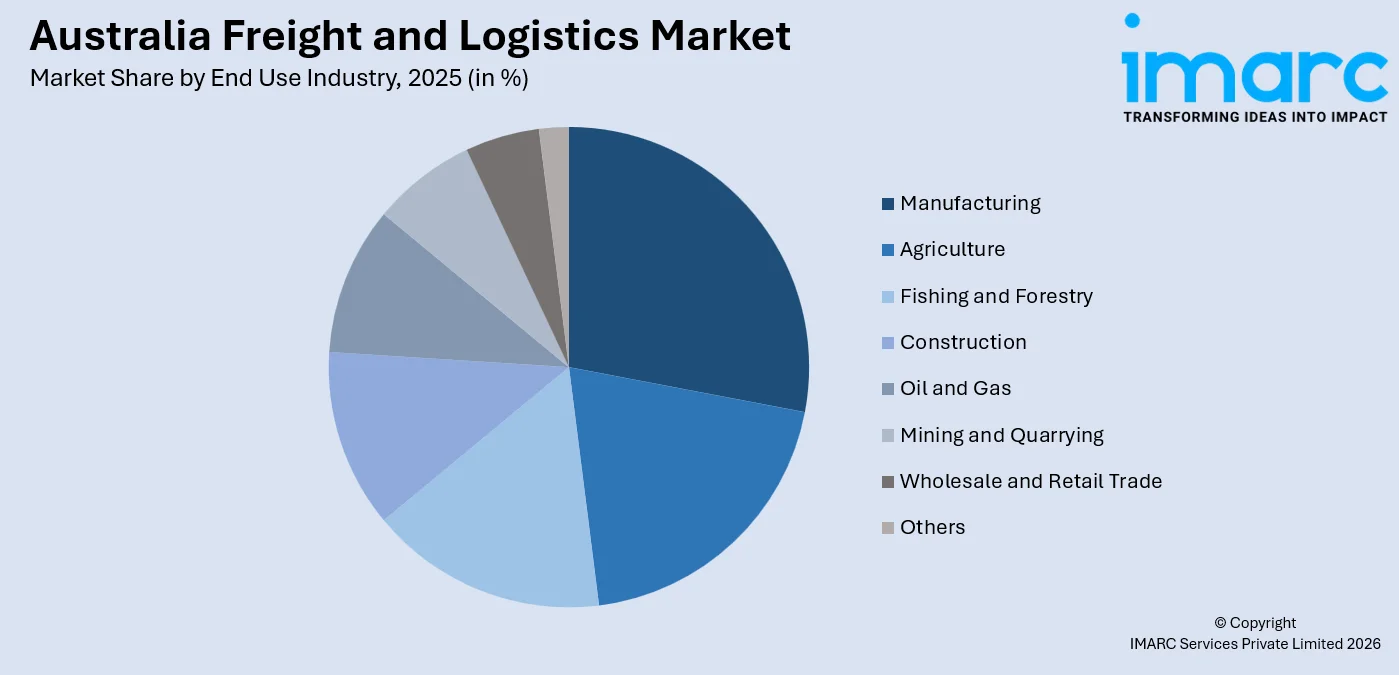

- Manufacturing holds 25% of the end use industry segment in 2025 - the sector generates demand for both inbound raw material transport and outbound distribution, making it the single largest driver of integrated multimodal freight solutions across the country.

- Australia Capital Territory & New South Wales leads regionally at 34% in 2025 - Port Botany's container throughput and the state's concentration of manufacturing, retail distribution, and e-commerce parcel activity make NSW & ACT the dominant freight market by both volume and value.

Australia Freight and Logistics Trends and Dynamic 2026

Market Trends

Growing Focus on Safety and Compliance

Australia's logistics companies are encouraged to update their fleets and improve safety procedures for workers. This comes in response to stricter rules regarding vehicle requirements, driver safety, and handling hazardous materials. The goals of these compliance initiatives are to improve operational reliability, reduce risk, and promote safer, stronger supply chain operations that include transportation and warehousing activities.

Electrification and Fleet Sustainability Investment Across Road Freight

With the adoption of electric heavy-duty vehicles and the expansion of urban charging infrastructure, Australia's freight industry is embracing low-emission transportation. Linfox ordered 30 Volvo FH and FM Electric trucks in May 2025, making it the largest order for electric trucks in the nation. These vehicles will be distributed throughout metropolitan operations with charging stations located in five major cities.

E-Commerce Driving Parcel Hub and Last-Mile Infrastructure Expansion

Rapid growth in online retail is driving demand for greater parcel processing capacity and last-mile delivery infrastructure across Australia. Logistics companies are expanding distribution networks and investing in automated parcel facilities to handle higher shipment volumes and meet faster delivery expectations. These efforts are strengthening nationwide fulfilment and improving efficiency in urban logistics.

- Digital Freight Visibility and TMS Platforms: Supply chain transparency across road, rail, and marine freight modes is being enhanced and booking-to-delivery processes are being shortened by real-time tracking and transport management systems.

- Cold Chain Expansion for Pharma and Agri Exports: The need for pharmaceutical sovereign stockpiles and the desire for premium fresh food and seafood exports to Asia-Pacific markets are driving the rapid advancement of refrigerated warehousing.

- The cargo precinct at Western Sydney Airport will open in 2026: Sydney now has a second major air cargo gateway thanks to the new airport, which also relieves capacity restrictions and builds new infrastructure for the delivery of expensive, urgent freight.

- Port Automation and On-Dock Rail Integration: To cut expenses associated with double handling and increase container throughput, Port Botany and major container terminals are implementing automated stacking cranes and twin on-dock rail sidings.

Growth Drivers

Mining and Commodity Export Volumes Sustaining Bulk Freight Demand

Strong demand for bulk freight across rail and port networks is fueled by Australia's position as the world's top exporter of iron ore and a major supplier of coal and LNG. A major investment in the nation's commodity logistics industry was made in November 2024 when Aurizon and BHP inked a USD 1.5 billion contract to combine autonomous rail with port automation, with a goal of 25% efficiency benefits.

Rise of Cross-Border E-Commerce Driving International Logistics Demand

Australia is seeing an increase in demand for effective international logistics due to growing cross-border e-commerce, which is driving providers to improve last-mile, shipping, and customs services. Long-term market expansion is highlighted by government programs including the National Freight and Supply Chain Strategy, port improvements, and Qantas Freight's 24,000 square meter facility in Western Sydney.

Manufacturing Reshoring and AUKUS Defence Logistics Growth

Freight transportation associated with industrial production and equipment logistics is growing as domestic manufacturing and defense supply networks expand. Within Australia's logistics ecosystem, investments associated with defense cooperation and supply chain resilience programs are promoting localized production and creating a steady need for inward raw materials and outbound delivery.

- E-Commerce package Volume Growth: Australian e-commerce parcel traffic grew 15% in 2024, expanding demand for micro-fulfillment centers, automated sortation hubs, and urban last-mile delivery infrastructure.

- Cross-Border Trade Under RCEP and FTAs: Trade agreements and regional economic partnerships are strengthening container freight activity at major east-coast ports, driving greater demand for international freight forwarding, customs handling, and integrated cross-border logistics services.

- Cold Chain and Pharmaceutical Logistics Demand: Temperature-controlled logistics experts and 3PL operators consistently earn premium revenue from high-value fresh food exports and sovereign pharmaceutical stockpile requirements.

- Warehouse Automation and Productivity Gains: By solving manpower shortages and accelerating fulfillment, automated storage and retrieval systems and AI-guided warehouse robotics are increasing throughput per square meter by up to 25%.

Market Restraints

Australia's Geographic Isolation and Vast Territory

Freight companies have inherent cost challenges due to Australia's vast size and distance from major international trading hubs. Long-haul distances between resource production zones and population centers result in consistently high logistical costs that are challenging to lower through operational savings alone. This limits competitive pricing in remote markets and restricts profitability in non-bulk segments.

Driver Shortage and Labor Cost Pressures

Road freight and distribution wage costs are rising, and capacity expansion is being hampered by a persistent lack of certified heavy truck drivers and experienced warehouse workers. Operators cannot rely solely on technology to alleviate the structural tension between network expansion goals and personnel availability, as the challenge of hiring logistics specialists in rural and regional growth areas persists.

Regulatory Fragmentation and Compliance Complexity

Vehicle access, mass restrictions, and environmental compliance are all governed by overlapping federal, state, and local regulatory frameworks in Australia's freight industry. Smaller carriers and cross-border operators negotiating multi-jurisdictional routes are disproportionately affected by the administrative complexity and compliance costs arising from varying interstate heavy vehicle access restrictions and variable permit conditions.

Australia Freight and Logistics Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Logistics Function | Freight Transport | 28% | 2025 |

| End Use Industry | Manufacturing | 25% | 2025 |

| Region | Australia Capital Territory & New South Wales | 34% | 2025 |

Logistics Function Insights

Freight Transport- 28% market share (2025) | Leading Logistics Function

Australia’s logistics sector is led by freight transport, fueled by its commodity exports and extensive road and rail networks connecting dispersed industrial and population centers. Strong demand from mining, agriculture, retail, and intercity trade drives national supply chains, with over 800 billion ton-kilometres moved annually. Around 47,162 road freight businesses operate nationwide, covering long-haul interstate and specialized regional services.

|

Segment Breakdown Freight Transport (28%) · Courier, Express and Parcel · Freight Forwarding · Warehousing and Storage · Others |

End Use Industry Insights

Access the comprehensive market breakdown Request Sample

Manufacturing- 25% market share (2025) | Leading End Use Industry

Australia’s manufacturing sector is the largest end-user of freight and logistics, relying on air, sea, rail, and road networks to move raw materials and finished goods. Continuous production cycles demand integrated supply chain solutions. In October 2024, Toll Group invested AUD 200 million to upgrade 25% of its trucking fleet, reflecting the scale of capacity required across key industrial corridors.

|

Segment Breakdown Manufacturing (25%) · Agriculture · Fishing and Forestry · Construction · Oil and Gas · Mining and Quarrying · Wholesale and Retail Trade · Others |

Regional Insights

Australia Capital Territory & New South Wales- 34% market share (2025) | Leading Region

New South Wales and the Australian Capital Territory anchor Australia’s freight and logistics market, supported by major port infrastructure, strong import and export activity, and concentrated economic operations. In October 2025, Australia Post planned six new parcel facilities, while Port Botany’s on-dock rail upgrade enhances ship-to-train container handling, reducing costs and improving distribution efficiency across regional logistics networks.

|

Metric

|

Details

|

|---|---|

|

Market Share in 2025

|

34%

|

|

Major Growth Drivers

|

Port Botany container volumes, e-commerce parcel infrastructure expansion, on-dock rail integration, Inland Rail corridor connectivity, Western Sydney Airport cargo precinct |

|

Outlook

|

Dominant logistics hub with accelerating parcel and intermodal capacity investment |

|

Regional Breakdown Australia Capital Territory & New South Wales (34%) · Victoria & Tasmania · Queensland · Northern Territory & Southern Australia· Western Australia |

Market Outlook 2026-2034

What is the future outlook of the Australia freight and logistics market?

The freight and logistics market in Australia has a bright future ahead of it thanks to growing freight volumes, modern infrastructure, digital transformation, and changing trade dynamics. Long-term forecasts show that the national freight challenge will continue to grow as trade, urbanization, and population growth boost the flow of products over air, sea, rail, and road networks. Over the ensuing decades, Australia's domestic freight demand is predicted to increase steadily, solidifying logistics' position as a vital pillar of economic activity.

Australia Freight and Logistics Market - Leading Key Players

The Australia freight and logistics market features a competitive mix of domestic champions and global multinationals, with consolidation accelerating as operators scale to meet e-commerce growth and automate operations. Australia Post, Toll Holdings, and Linfox lead the domestic landscape, while DHL, StarTrack Express, and Qantas Freight provide critical integration across air, express parcel, and international freight forwarding channels.

| Company | Leading Brands | Highlights |

|---|---|---|

| StarTrack Express | StarTrack Express, StarTrack Premium | Jointly owned by Australia Post and Qantas Freight; operates Australia's largest dedicated domestic freighter network; first fully integrated co-located facility with Australia Post confirmed at Elizabeth, SA |

| Qantas Freight | Qantas Freight, Express Freighters Australia | Operates dedicated freighter fleet; pre-committed to 24,000 m² cargo facility at Western Sydney International Airport (Oct 2024); major air freight partner to Australia Post under multi-year agreement |

| DHL Express (Australia) Pty Ltd | DHL Express, DHL Global Forwarding | Leading international express and freight forwarding operator in Australia; market leader in rail, air and sea freight forwarding by IBISWorld ranking; expanded Australian presence through 2022 Glen Cameron Group acquisition |

Some of the major players in the Australia freight and logistics market include Australia Post, Toll Holdings, Aurizon, Schenker Australia, FedEx Australia, Linfox, etc.

Latest Development & News

- In October 2025, Australia Post announced its largest-ever investment in the state, spending A$500 million to build a new parcel super hub at the former Holden manufacturing site in Elizabeth, South Australia. When it is finished in 2028, the 83,000-square-meter building will be the biggest in the country's network and the first fully integrated Australia Post and StarTrack co-located location. The hub will aim for a 5-star Green Star environmental rating and act as the model for Australia Post's next-generation automated facility deployment. It can process up to 400,000 packages per day, which is twice the capacity of Adelaide Airport.

- In May 2025, 30 Volvo battery-electric heavy-duty vehicles, comprising 29 FH Electric and one FM Electric type, were ordered by Linfox for use in metropolitan logistical operations, making it Australia's largest single commercial electric truck order. The historic order is the largest commercial EV commitment in Australia's road freight industry, and it directly addresses retailer sustainability mandates influencing procurement decisions for significant 3PL contracts. It is accompanied by investments in charging infrastructure across five Australian capital cities.

- In February 2025, At Melbourne Airport, Rohlig Logistics erected a brand-new 19,000 m² warehouse with 17,500 pallet positions and sustainable energy systems. As a result of ongoing private investment in logistics capacity close to important aviation gateways, the facility enhances Rohlig's air freight integration capabilities in Victoria and offers high-capacity logistics infrastructure for pharmaceutical, technology, and time-sensitive cargo at one of Australia's busiest air cargo hubs.

Australia Freight and Logistics Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Logistics Functions Covered |

|

| End Use Industries Covered | Agriculture, Fishing and Forestry, Construction, Manufacturing, Oil and Gas, Mining and Quarrying, Wholesale and Retail Trade, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, Australia freight and logistics market forecast, and dynamics of the market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia freight and logistics market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia freight and logistics industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Freight and Logistics Market Report

The Australia freight and logistics market was valued at USD 97.88 Billion in 2025.

The Australia freight and logistics market is anticipated to reach a value of USD 143.0 Billion by 2034.

Freight transport dominates the market with a share of 28%, driven by Australia's extensive bulk commodity export economy and the nationwide road freight network serving the country's dispersed industrial zones and population centers across long interstate and regional corridors.

Manufacturing commands the market with a share of 25%, reflecting the sector's substantial demand for integrated inbound raw material and outbound finished-goods freight services across road, rail, and sea transport modes connecting production facilities to domestic distribution networks and export ports.

Some of the major players in the Australia freight and logistics market include Australia Post, Toll Holdings, Linfox, StarTrack Express, Qantas Freight, DHL Express (Australia) Pty Ltd, etc.

Key trends include the transformative impact of the USD 31 billion Inland Rail program reducing east-coast freight costs by approximately 20%, accelerating fleet electrification with Linfox's landmark 30-unit Volvo EV order, Australia Post's A$500 million parcel super hub investment responding to e-commerce demand, port automation and on-dock rail integration at Port Botany, and the 2026 opening of Western Sydney International Airport's cargo precinct creating a second major air freight gateway.

With a 34% market share, Australia Capital Territory & New South Wales presently dominates the country's freight and logistics industry. Sydney's concentration of manufacturing and retail distribution activity, Port Botany's status as Australia's busiest container terminal, and the highest e-commerce parcel volume density in the country all benefit the area.

The mining industry's structurally high bulk commodity export volumes, federal government infrastructure investment through the National Freight and Supply Chain Strategy, e-commerce parcel demand multiplying last-mile and warehouse capacity requirements, the AUKUS defense program creating specialized logistics activity in South Australia, and the expansion of cross-border trade under RCEP and bilateral free trade agreements with major Asia-Pacific trading partners are all factors driving growth.

Australia's large geographic area and remote location impose high structural logistics costs that are challenging to lower through operational efficiencies; capacity growth in regional corridors is hampered by a persistent lack of skilled warehouse workers and qualified heavy vehicle drivers; and regulatory fragmentation across federal and state jurisdictions creates complicated compliance requirements for operators managing cross-border heavy vehicle operations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)