Australia Geopolymer Market Size, Share, Trends and Forecast by Application, End-Use Industry, and Region, 2026-2034

Australia Geopolymer Market Overview:

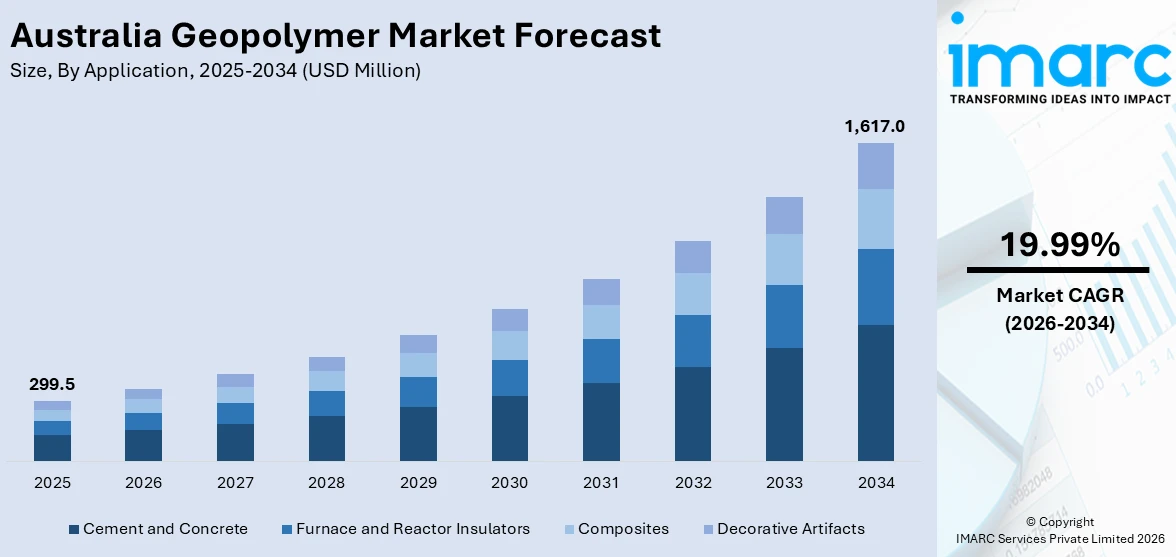

The Australia geopolymer market size reached USD 299.5 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 1,617.0 Million by 2034, exhibiting a growth rate (CAGR) of 19.99% during 2026-2034. The market share is expanding, driven by increasing investments in large-scale construction projects, which is creating the need for efficient alternatives to traditional cement, along with the growing government support for circular economy models.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025 |

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 299.5 Million |

| Market Forecast in 2034 | USD 1,617.0 Million |

| Market Growth Rate 2026-2034 | 19.99% |

Australia Geopolymer Market Trends:

Rising need to reduce carbon emissions

The growing need to reduce carbon emissions is offering a favorable Australia geopolymer market outlook. With ongoing investments in large-scale construction projects, the demand for low-emission alternatives to traditional cement is increasing. In September 2024, SA Water teamed up with five major construction firms to execute its USD 3.3 Billion capital initiative over the next four years. The plan featured USD 1.5 Billion in funding, which was a crucial element of the ‘Housing Roadmap’. It was intended to enhance the capacity of the water and sewer systems by upgrading pipes, pump stations, and tanks throughout South Australia. Geopolymers, made from industrial by-products like fly ash and slag, offer a much smaller carbon footprint compared to conventional cement, making them an attractive choice. Construction companies are starting to adopt geopolymers in infrastructure, residential, and commercial projects to align with environmental regulations and green building standards. These materials offer strong durability, fire resistance, and long-term performance, which adds value beyond their environmental benefits. As the awareness among the masses about climate change and sustainable development goals continues to grow, the demand for eco-friendly construction solutions is rising. Research institutions and manufacturers are working to improve the properties and scalability of geopolymer products, further supporting their employment. With the building industry being a major contributor to carbon emissions, geopolymers present a smart and responsible solution, helping Australia move towards a greener future.

To get more information on this market Request Sample

Increasing mining activities

The rising mining activities are impelling the Australia geopolymer market growth. As mining operations expand across the country to meet worldwide demand for minerals and metals, more of these waste materials are generated, creating a steady and cost-effective supply for geopolymer manufacturing. In December 2024, the Australian Government unveiled a USD 75 Million (AD 117.28 Million) investment designed to boost the availability of essential minerals required for the transition to renewable energy. The Clean Energy Finance Corporation (CEFC), an expert in Australia’s shift to net-zero emissions, partnered with Resource Capital Funds (RCF) to advance decarbonization in the Australian critical minerals mining industry. These projects are increasing the availability of industrial by-products like fly ash, red mud, and slag, which are key raw materials for producing geopolymers. These materials made from mining waste not only offer a sustainable option but also help to reduce landfill loads. Their durability, thermal resistance, and low carbon footprint make them suitable for various industrial applications, especially in areas close to mining zones. The government’s support for circular economy models is further positively influencing the market.

Australia Geopolymer Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the regional level for 2026-2034. Our report has categorized the market based on application and end-use industry.

Application Insights:

- Cement and Concrete

- Furnace and Reactor Insulators

- Composites

- Decorative Artifacts

The report has provided a detailed breakup and analysis of the market based on the application. This includes cement and concrete, furnace and reactor insulators, composites, and decorative artifacts.

End-Use Industry Insights:

Access the comprehensive market breakdown Request Sample

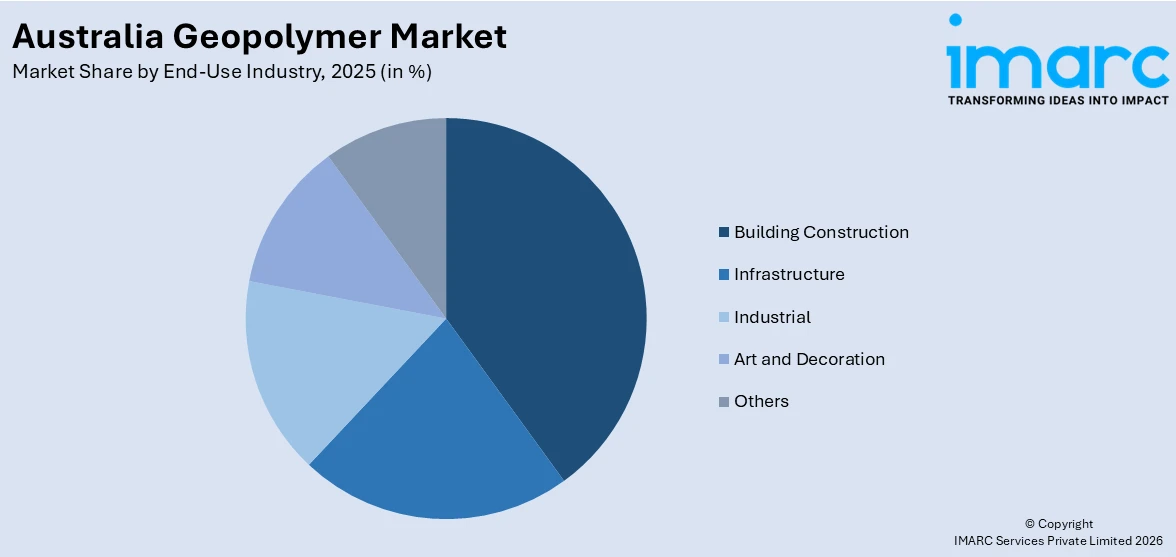

- Building Construction

- Infrastructure

- Industrial

- Art and Decoration

- Others

A detailed breakup and analysis of the market based on the end-use industry have also been provided in the report. This includes building construction, infrastructure, industrial, art and decoration, and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Geopolymer Market News:

- In November 2024, the University of Western Australia launched the RiverLab Project. Under the initiative, a new high-performance geopolymer concrete without cement was to be created, featuring strong resistance to corrosion caused by sulphates and chlorides found in the Swan River.

- In May 2024, Suvo, a prominent green cement manufacturer operational in Australia, teamed up with PERMAcast to create low-carbon geopolymer concrete solutions. These geopolymers were created from waste-sourced materials. PERMAcast CEO Darren Hedley stated that the new partnership represented an important advancement in developing more sustainable construction solutions by tackling the necessity to lower carbon emissions.

Australia Geopolymer Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Applications Covered | Cement and Concrete, Furnace and Reactor Insulators, Composites, Decorative Artifacts |

| End-Use Industries Covered | Building Construction, Infrastructure, Industrial, Art and Decoration, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Australia geopolymer market performed so far and how will it perform in the coming years?

- What is the breakup of the Australia geopolymer market on the basis of application?

- What is the breakup of the Australia geopolymer market on the basis of end-use industry?

- What is the breakup of the Australia geopolymer market on the basis of region?

- What are the various stages in the value chain of the Australia geopolymer market?

- What are the key driving factors and challenges in the Australia geopolymer market?

- What is the structure of the Australia geopolymer market and who are the key players?

- What is the degree of competition in the Australia geopolymer market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia geopolymer market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia geopolymer market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia geopolymer industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)