Australia Halal Food Market Size, Share, Trends and Forecast by Product, Distribution Channel, and Region 2026-2034

Australia Halal Food Market Summary:

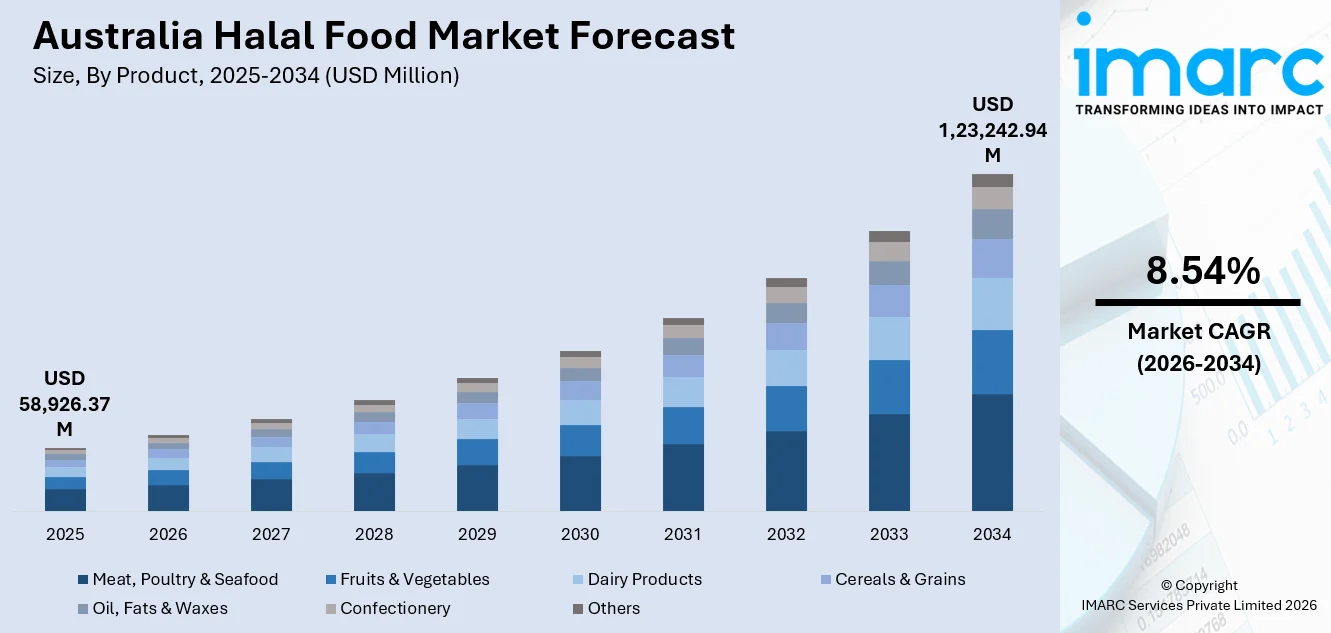

The Australia halal food market size was valued at USD 58,926.37 Million in 2025 and is projected to reach USD 1,23,242.94 Million by 2034, growing at a compound annual growth rate of 8.54% from 2026-2034.

The Australia halal food market is experiencing robust growth, driven by increasing Muslim population, rising consumer awareness, and demand for certified, ethically sourced products, supported by stringent regulatory compliance, expanding retail and e-commerce distribution, and adoption across diverse categories such as meat, processed foods, and beverages, while competitive dynamics, certification standards, and supply chain transparency continue to shape market development nationwide.

Key Takeaways and Insights:

- By Product: Meat, Poultry & Seafood dominates the market with a share of 48.5% in 2025, driven by high demand for protein-rich, certified halal products among Australian consumers.

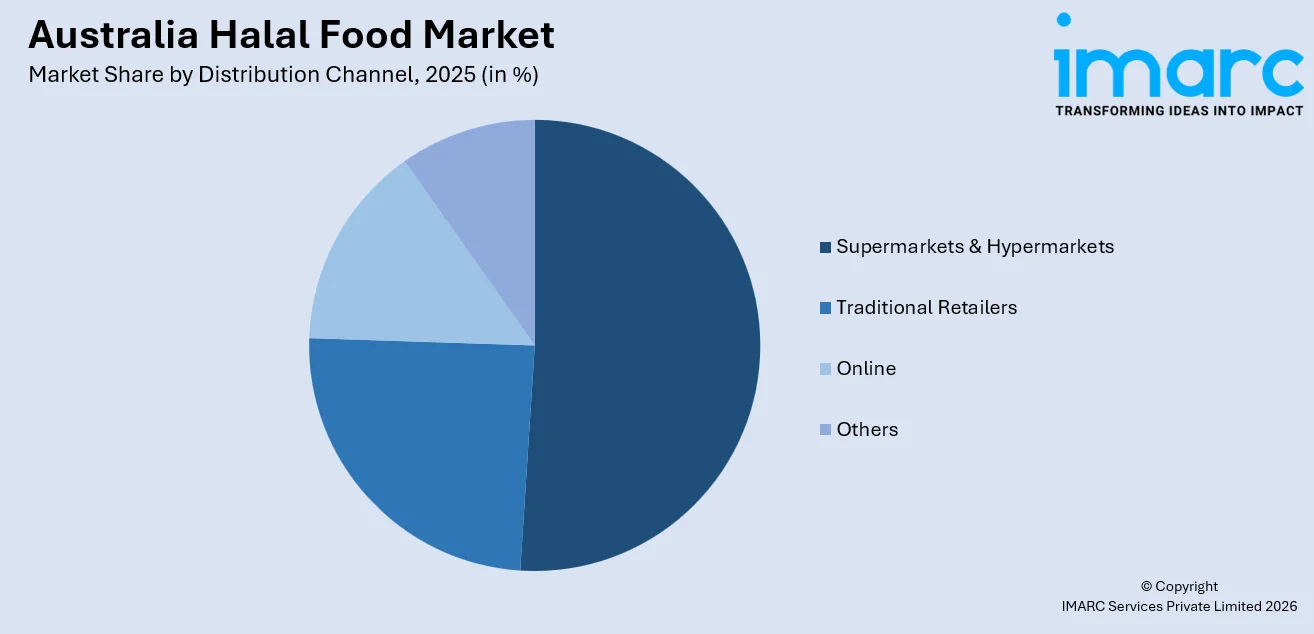

- By Distribution Channel: Supermarkets & Hypermarkets dominates the market with a share of 52.1% in 2025, benefiting from convenience, wide product availability, and strong consumer trust in halal-certified offerings.

- By Region: Australia Capital Territory New South Wales held the largest market segment in 2025, capturing 34.7% share, due to population density and strong demand for halal foods.

- Key Players: Leading market participants focus on product diversification, halal certification compliance, supply chain efficiency, and strategic retail partnerships, intensifying competition while expanding regional presence and meeting evolving consumer preferences.

To get more information on this market Request Sample

The Australia halal food market is witnessing steady expansion, fueled by increasing multicultural populations and heightened consumer awareness regarding ethically sourced, certified products. Australia’s population expanded from 3.8 million in 1901 to 25.7 million in 2021, according to the Australian Bureau of Statistics, while the proportion of people living in urban areas increased from 58% in 1911 to 90% by 2021. In line with this, rising demand extends beyond traditional meat and poultry to include processed foods, dairy, confectionery, and ready-to-eat meals, reflecting broader adoption across mainstream retail and foodservice channels. Retailers and manufacturers are further investing in advanced traceability systems, cold chain management, and stringent certification processes to ensure compliance with halal standards and maintain consumer trust. Likewise, the rise of e-commerce platforms and online grocery delivery services is driving greater market accessibility and convenience. Additionally, strategic collaborations between domestic producers and international suppliers are enhancing product variety and quality. With government support for food safety and labeling regulations, the market is poised for sustainable growth while emphasizing transparency, quality assurance, and diversified product offerings.

Australia Halal Food Market Trends:

Expansion of Halal Ready‑to‑Eat and Convenience Foods

The Australia halal food market is experiencing notable growth in ready‑to‑eat and convenience food categories as consumers increasingly seek time‑saving, high‑quality meal solutions. This trend reflects changing lifestyles, urbanization, and greater participation of working professionals who favor quick, nutritious halal options. As per the Australian Bureau of Statistics, the population of Australia grew to 25.7 million by 2021, up from 3.8 million in 1901, with the urban population rising from 58% in 1911 to 90% over the same period. Manufacturers are also responding with diversified product portfolios, including microwaveable meals and pre‑prepared dishes, while ensuring strict adherence to halal certification and food safety standards. Moreover, retailers are expanding shelf space accordingly to meet changing consumer preferences, thereby providing an impetus to the market.

Rapid Technological Integration for Traceability and Transparency

Improved supply chain transparency is emerging as a key trend in the Australia halal food market, driven by both regulatory expectations and consumer demand for verifiable product origins. In parallel, companies are investing in digital traceability technologies such as blockchain and enhanced labeling systems to document sourcing, processing, and certification steps. As such, in November 2025, the Albanese Government introduced the Corporations Amendment (Digital Assets Framework) Bill, which regulates blockchain-based digital assets, unlocking USD 24 Billion in annual innovation potential, enhancing consumer protections, and supporting secure, licensed digital asset platforms. These innovations reinforce consumer trust, reduce risks of non‑compliance, and support brand differentiation in a competitive landscape, ultimately bolstering market credibility and long‑term growth.

Diversification of Halal Product Categories

The Australian halal food market is witnessing diversification beyond traditional meat products, with increased offerings in bakery, confectionery, plant‑based alternatives, and gourmet segments. This trend corresponds to evolving dietary preferences, including vegetarianism and health‑oriented consumption, encouraging producers to innovate while maintaining halal compliance. Retailers are showcasing broader product assortments, catering to both Muslim and non‑Muslim consumers seeking quality halal options. As a result, category expansion is strengthening market penetration and stimulating cross‑segment demand.

Market Outlook 2026-2034:

The Australia halal food market is projected to grow robustly, supported by increasing multicultural demographics, rising health consciousness, and expanding global trade opportunities. In 2025, industry research found that 45.9% of Australians committed to a healthier lifestyle, up 2.6% from 2024, with Gen Z taking the lead at 54.2%, followed by Millennials at 52.8%, Gen X at 46.3%, and Baby Boomers at 35%. Growth will also be driven by ongoing innovations in product formulation, enhanced cold‑chain logistics, and broader retail and online distribution networks. Furthermore, heightened regulatory emphasis on stringent certification and food safety will bolster consumer confidence, while strategic partnerships between domestic and international stakeholders are expected to diversify offerings. In addition, continued investment in quality assurance and marketing will further strengthen market penetration. The market generated a revenue of USD 58,926.37 Million in 2025 and is projected to reach a revenue of USD 1,23,242.94 Million by 2034, growing at a compound annual growth rate of 8.54% from 2026-2034.

Australia Halal Food Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product |

Meat, Poultry & Seafood |

48.5% |

|

Distribution Channel |

Supermarkets & Hypermarkets |

52.1% |

|

Region |

Australia Capital Territory & New South Wales |

34.7% |

Product Insights:

- Meat, Poultry & Seafood

- Fruits & Vegetables

- Dairy Products

- Cereals & Grains

- Oil, Fats & Waxes

- Confectionery

- Others

Meat, Poultry & Seafood dominate the total Australian halal food market with a 48.5% market share in 2025.

The dominance is reflected by strong consumer demand for high-quality, protein-rich, and certified halal products. These categories benefit from widespread cultural acceptance and frequent consumption patterns among Muslim households. Producers focus on sourcing ethically raised livestock and ensuring strict compliance with halal slaughter and processing standards, enhancing trust and reliability.

The segment’s leadership is reinforced by innovations in product variety, including value-added cuts, ready-to-cook portions, and processed seafood options. Retailers emphasize freshness, packaging, and labeling to attract both Muslim and non-Muslim consumers seeking quality and convenience. Moreover, strategic partnerships with suppliers and investment in cold-chain logistics further support consistent market dominance in the meat, poultry, and seafood categories. As such, Stonepeak launched Peregrine Cold Logistics, a Singapore-based platform expanding cold-chain infrastructure across Asia Pacific and the GCC. With a leadership team boasting 30+ years’ experience, it strengthens Australia’s strategic position, modernises facilities, and supports sustainable, high-quality food logistics.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Traditional Retailers

- Supermarkets & Hypermarkets

- Online

- Others

Supermarkets & Hypermarkets dominates with a market share of 52.1% of the total Australia halal food market in 2025.

The segment is preferred in the market, driven by wide product availability, convenient locations, and strong consumer trust. Similarly, large retail chains often feature certified halal sections and promotional campaigns, augmenting product visibility and adoption.

Their leadership is further supported by extensive cold-chain infrastructure, ensuring the quality and freshness of perishable items such as meat and poultry. Retailers also enhance customer engagement through loyalty programs and in-store sampling initiatives. With a broad regional presence, supermarkets consistently achieve market penetration, solidifying their position as the preferred distribution channel for halal food products.

Region Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales exhibits a clear dominance with a 34.7% share of the total Australia halal food market in 2025.

The region accounted for the largest share, driven by high population density and strong multicultural communities. These regions feature significant demand for certified halal food across the retail, hospitality, and institutional sectors, driving sustained market growth.

The regional leadership is further supported by advanced distribution networks, including major wholesalers and modern retail outlets, which facilitate accessibility and consistent supply. The Australian Bureau of Statistics (ABS) reported that retail sales in April 2025 rose 3.8% year-on-year, reaching USD 37.2 Billion. New South Wales saw a 1.7% increase, while the Australian Capital Territory recorded a 1.5% rise. Additionally, the concentration of foodservice businesses and cultural diversity encourages greater adoption of halal-certified products, cementing these states as the key growth hubs for the Australia halal food market.

Market Dynamics:

Growth Drivers:

Why is the Australia Halal Food Market Growing?

Rapid Integration of Digital Marketing and Consumer Engagement

Australian halal food brands are increasingly leveraging digital marketing and social media platforms to enhance consumer engagement and broaden market reach. IAB Australia reported that the Australian internet advertising market reached USD 4.2 Billion in the March 2025 quarter, up 11.6% year-on-year. Search advertising grew 10% to USD 1.896 Billion. Facebook remains the top platform, while TikTok is rapidly gaining traction among younger, highly engaged users. Companies are deploying targeted campaigns, influencer partnerships, and interactive content to educate consumers about halal certification, product benefits, and ethical sourcing practices. These efforts improve brand visibility and foster stronger customer loyalty. Additionally, brands are using online feedback and analytics to refine product offerings and tailor promotional strategies, aligning more closely with evolving consumer preferences and purchase behaviours.

Expansion of Halal Foodservice and Catering Services

The halal foodservice segment in Australia is witnessing significant growth, driven by rising demand from multicultural communities, tourism, and corporate catering contracts. According to the ABS Census, Australia’s Muslim population exceeds 800,000 and continues to grow, becoming increasingly visible in mainstream society and fueling rising demand for convenient, high-quality halal products. In tandem, restaurants, cafes, and institutional foodservice providers are expanding halal menu options to accommodate diverse dietary needs, while certified catering services are securing contracts for events, educational institutions, and healthcare facilities. This trend highlights broader acceptance of halal cuisine and reflects strategic efforts by service providers to capture incremental revenue by meeting specific cultural food requirements.

Heightened Adoption of Sustainable and Ethical Sourcing Practices

Sustainability and ethical sourcing are increasingly shaping the Australia halal food market, with producers prioritizing eco‑friendly farming methods, reduced carbon footprint practices, and animal welfare standards that complement halal compliance. Retailers and manufacturers are promoting transparency in supply chains, emphasizing traceability from farm to fork. Apart from this, certifications beyond halal, such as grass‑fed, free‑range, and organic labels, are gaining traction, appealing to environmentally conscious consumers and enhancing competitive differentiation in a crowded marketplace.

Market Restraints:

What Challenges the Australia Halal Food Market is Facing?

Stringent Halal Certification and Compliance Requirements

Ensuring compliance with rigorous halal certification standards remains a significant challenge for Australian food producers. Companies must adhere to specific slaughtering, processing, and handling procedures, often requiring audits and re-certifications. Maintaining these standards across large-scale operations and supply chains increases operational complexity and costs. Smaller producers, in particular, may face resource constraints to meet compliance consistently. Any lapses can damage brand reputation, reduce consumer trust, and limit access to both domestic and international halal food markets.

High Production and Operational Costs

The Australia halal food market faces pressure from elevated production and operational costs, including sourcing certified livestock, specialized processing, and maintaining segregation of halal and non-halal products. Investment in cold-chain logistics, packaging, and quality assurance further increases expenses. These costs can limit profitability, especially for smaller manufacturers, and may translate to higher consumer prices. Balancing cost efficiency with strict adherence to halal standards presents an ongoing challenge, impacting market competitiveness and slowing expansion into price-sensitive segments.

Limited Consumer Awareness in Non-Muslim Segments

Although halal food consumption is growing, limited awareness and understanding of halal certification among non-Muslim consumers can constrain market expansion. Misconceptions regarding religious requirements, quality, or taste may reduce broader adoption in mainstream retail and foodservice channels. This restricts potential growth outside traditional consumer bases and limits cross-market opportunities. Companies must invest in educational campaigns, labeling transparency, and marketing initiatives to address knowledge gaps and foster acceptance among diverse demographic groups.

Competitive Landscape:

The Australian halal food sector competes with established local manufacturers who face competition from regional distributors and international companies which aim to satisfy the rising demand for certified premium products. Companies compete on product variety, quality assurance, and strict compliance with halal certification standards, while leveraging strong distribution networks across supermarkets, hypermarkets, and e-commerce platforms. Brands create unique identities through their commitment to sustainable sourcing and ethical operations which they combine with innovative products that include ready-to-eat meals and special items. The market environment experiences constant transformation because companies establish competitive strength through their strategic partnerships and mergers with retail and supply partners.

Recent Developments:

- In November 2025, The Australian Halal Authority granted Halal certification to Aquna Sustainable Murray Cod, which enables their premium caviar product to access the UAE luxury dining sector. The product achieves its highest potential for international expansion because King Charles and Gordon Ramsay and Heston Blumenthal all favor the product.

- In July 2025, Indonesia and Australia held bilateral talks in Melbourne, to augment halal trade. With Indonesia needing 650,000 metric tons of halal meat annually, Australia’s 140,000-ton supply highlights growth opportunities. Both nations agreed to streamline certification, support food security, and enhance sustainable halal trade cooperation.

Australia Halal Food Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Products Covered |

Meat, Poultry & Seafood, Fruits & Vegetables, Dairy Products, Cereals & Grains, Oil, Fats & Waxes, Confectionery, Others |

|

Distribution Channels Covered |

Traditional Retailers, Supermarkets & Hypermarkets, Online, Others |

|

Regions Covered |

Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Halal Food Market Report

The Australia halal food market size was valued at USD 58,926.37 Million in 2025.

The Australia halal food market is expected to grow at a compound annual growth rate of 8.54% from 2026-2034 to reach USD 1,23,242.94 Million by 2034.

Meat, Poultry & Seafood dominated the market with 48.5% share in 2025, driven by high consumer demand, staple dietary preferences, and wide availability across retail and foodservice channels.

Key factors driving the Australia halal food market include a rising Muslim population, increasing awareness of halal certification, expanding distribution through supermarkets and online channels, higher disposable incomes, and a growing preference for ethical, safe, and high-quality food products.

Major challenges in the Australia halal food market include limited local halal-certified suppliers, high production and certification costs, inconsistent regulatory standards, supply chain complexities, and competition from imported products, which can impact pricing, availability, and consumer trust in the Australian halal food market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade