Australia Head-Up Display Market Size, Share, Trends and Forecast by Product Type, Conventional and Augmented Reality, Technology, Application, and Region, 2026-2034

Australia Head-Up Display Market Summary:

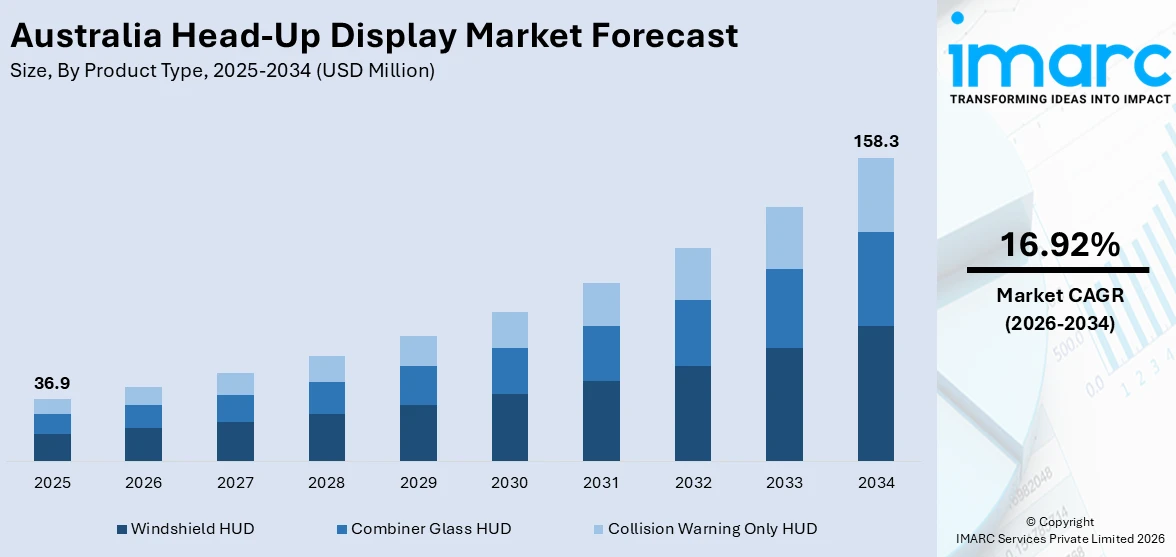

The Australia head-up display market size was valued at USD 36.9 Million in 2025 and is projected to reach USD 158.3 Million by 2034, growing at a compound annual growth rate of 16.92% from 2026-2034.

The market is driven by the increasing integration of advanced projection technologies that deliver critical real-time data within the driver's or pilot's line of sight, enhancing situational awareness and operational safety. Growing consumer demand for connected vehicle interiors, backed by rapid electric vehicle adoption and rising road safety compliance requirements, is accelerating HUD deployment across automotive and aviation segments. The expansion of augmented reality capabilities, alongside evolving digital cockpit ecosystems, continues to broaden the Australia head-up display market share.

Key Takeaways and Insights:

- By Product Type: Windshield HUD dominates the market with a share of 58.4% in 2025, driven by its wide forward projection field, ergonomic superiority over combination variants, and strong alignment with premium automotive design expectations.

- By Conventional and Augmented Reality: Conventional HUD leads the market with a share of 64.2% in 2025, owing to proven reliability, lower production costs, and widespread OEM adoption across mid-range and premium vehicle lines.

- By Technology: Digital HUD represents the largest segment with a market share of 66.8% in 2025, driven by superior image quality, energy efficiency, and scalability for augmented reality integration across automotive and aviation applications.

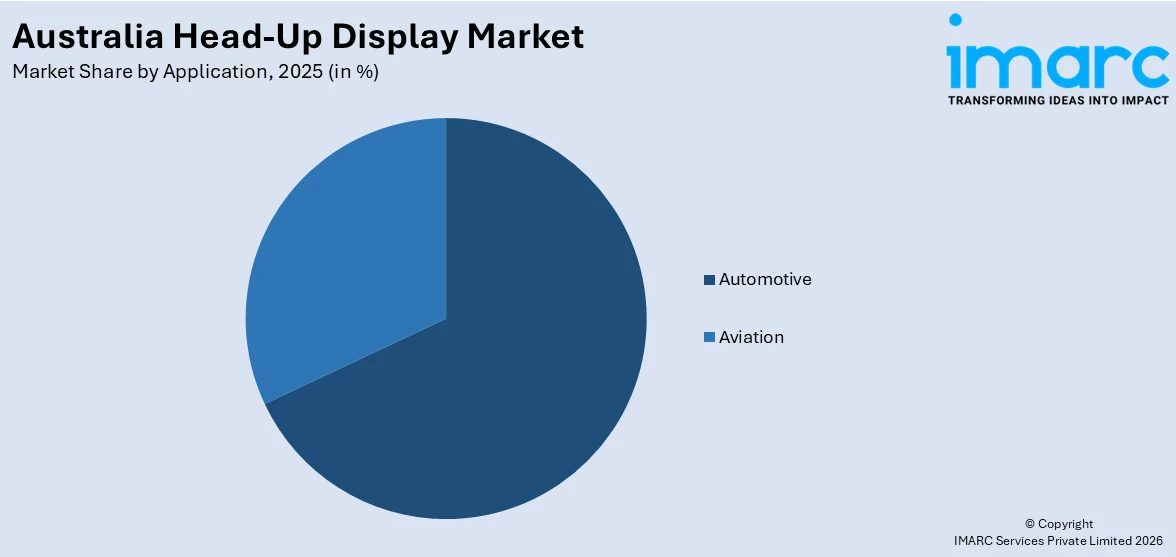

- By Application: Automotive dominates the market with a share of 67.3% in 2025, owing to rising vehicle sales, mandatory ADAS integration requirements, and the accelerating electric vehicle transition pushing automakers toward standardizing HUD systems.

- By Region: Australia Capital Territory & New South Wales leads the market with a share of 36.5% in 2025, driven by the highest premium vehicle concentration, a technologically progressive consumer base, and robust automotive retail infrastructure.

- Key Players: The Australia head-up display market is moderately competitive, with global automotive technology suppliers and specialized display innovators competing through continuous product innovation, augmented reality integration capabilities, strategic OEM partnerships, and supply chain alignment with domestic vehicle manufacturers and commercial aviation operators across key segments.

To get more information on this market Request Sample

The Australia head-up display market is experiencing sustained momentum, underpinned by the convergence of road safety imperatives, consumer appetite for advanced in-vehicle technology, and the accelerating shift toward electric and connected vehicles. Automakers operating in Australia are increasingly standardizing head-up displays across mid-range and premium segments, driven by regulatory pressure around distracted driving and heightened consumer awareness of ADAS benefits. In January 2025, BMW unveiled its Panoramic Vision head-up display at CES, featuring a windshield-spanning projection with integrated navigation and driving data, reinforcing next-generation HUD innovation trends influencing global automotive markets. The growing sophistication of digital cockpit ecosystems is further embedding HUD as a foundational component of modern vehicle design, enabling seamless integration of navigation, collision alerts, and augmented reality overlays within the driver's natural line of sight. In aviation, ongoing fleet modernization programs and sustained infrastructure investment are reinforcing adoption across both commercial and defense applications.

Australia Head-Up Display Market Trends:

Integration of Augmented Reality into Automotive Head-Up Display Systems

Australia is undergoing a structural transition toward augmented reality-enhanced head-up displays in passenger vehicles, as automakers and technology suppliers move beyond basic speed and navigation projections toward immersive, context-aware overlays. AR-HUDs are now capable of projecting lane guidance, hazard markers, and intersection alerts directly onto the windshield at real-world scale, dramatically improving driver cognition and situational awareness. In August 2025, Austroads launched an ADAS Guidance Service to improve driver understanding and safe use of advanced in-vehicle technologies, supporting wider adoption of systems that integrate with HUD-based interfaces.

Windshield HUD Replacing Combiner-Based Systems as the Preferred Format

The transition from combiner glass HUDs to full windshield projection systems is accelerating across Australia's automotive landscape, as manufacturers respond to consumer preference for a wider, more integrated field of view. Windshield HUDs project information at a greater virtual distance, reducing eye refocus time and promoting continuous road awareness, directly aligning with evolving ADAS safety standards. In June 2025, the Australian Automotive Aftermarket Association reported that advanced driver assistance systems are already embedded in all new passenger vehicles sold in Australia, reinforcing the ecosystem supporting advanced display technologies like windshield HUDs.

Rising Adoption of Digital HUD Technologies Across Aviation and Automotive Sectors

Beyond passenger vehicles, Australia's aviation and defense industries are progressively adopting advanced digital HUD platforms to enhance pilot situational awareness and operational performance. Commercial carriers modernizing their fleets are increasingly specifying HUD as standard cockpit equipment, while defense aviation programs have deepened the country's integration of high-performance head-up guidance systems across frontline aircraft. As per sources, Thales Group confirmed that its avionics solutions, including cockpit HUD systems, were selected for new Airbus aircraft deliveries, reinforcing the growing role of HUD-enabled flight decks in modern commercial aviation.

Market Outlook 2026-2034:

The Australia head-up display market is poised for robust expansion across the forecast period, driven by the deepening integration of digital cockpit ecosystems, rising electric vehicle penetration, and the progressive standardization of advanced driver assistance technologies across vehicle lines. Augmented reality-based HUDs are anticipated to gain increasing traction as production costs decline, and OEM adoption broadens from premium to mid-segment vehicles. Sustained aviation fleet modernization and growing road safety imperatives further reinforce the market's long-term structural growth trajectory throughout the outlook period. The market generated a revenue of USD 36.9 Million in 2025 and is projected to reach a revenue of USD 158.3 Million by 2034, growing at a compound annual growth rate of 16.92% from 2026-2034.

Australia Head-Up Display Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Windshield HUD |

58.4% |

|

Conventional and Augmented Reality |

Conventional HUD |

64.2% |

|

Technology |

Digital HUD |

66.8% |

|

Application |

Automotive |

67.3% |

|

Region |

Australia Capital Territory & New South Wales |

36.5% |

Product Type Insights:

- Windshield HUD

- Combiner Glass HUD

- Collision Warning Only HUD

Windshield HUD dominates with a market share of 58.4% of the total Australia head-up display market in 2025.

Windshield HUD leads the Australia head-up display market, projecting critical navigational and safety data directly onto the vehicle's windshield within the driver's natural forward field of vision. This format offers a significantly larger image area compared to combiner solutions, enabling richer data overlays including speed, navigation arrows, lane-departure alerts, and augmented reality hazard markers. The preference for windshield HUDs is growing in direct correlation with the increasing complexity of digital cockpit systems and the accelerating shift toward electric vehicles across Australia.

Windshield HUD's dominance is further reinforced by its superior ergonomic performance, as it substantially reduces the eye movement required to access critical driving information, keeping the driver's attention anchored to the road environment. Original equipment manufacturers are increasingly standardizing windshield projection systems across premium and mid-range vehicle lines, driven by consumer expectations for immersive in-vehicle technology experiences. The format's compatibility with augmented reality integration positions it as the preferred long-term platform for next-generation HUD deployment across Australia's evolving automotive landscape.

Conventional and Augmented Reality Insights:

- Conventional HUD

- Augmented Reality Based HUD

Conventional HUD leads with a share of 64.2% of the total Australia head-up display market in 2025.

Conventional HUD dominates Australia's head-up display market, delivering core driving information including speed, navigation guidance, and warning alerts through established optical projection technologies. Its dominance stems from proven manufacturing scalability, broad OEM integration across vehicle price tiers, and lower per-unit costs relative to augmented reality-based alternatives. In Australia, conventional systems are embedded across a wide range of vehicle lines, where their reliability and standardized calibration requirements make them the preferred choice for volume production across both passenger and commercial vehicle segments.

The sustained leadership of conventional HUD reflects the automotive industry's preference for technologies that balance performance, cost-efficiency, and deployment simplicity at scale. As Australian automakers progressively expand their model ranges to incorporate ADAS features, conventional HUD serves as the accessible entry point for head-up display integration without the engineering complexity associated with augmented reality systems. This positions conventional HUD as the foundational technology underpinning current market volumes, even as AR-based alternatives gradually gain traction in premium vehicle categories.

Technology Insights:

- CRT Based HUD

- Digital HUD

- Optical Waveguide HUD

- Digital Micromirror Device (DMD) HUD

- Light Emitting Diode (LED) HUD

- Others

Digital HUD exhibits a clear dominance with a 66.8% share of the total Australia head-up display market in 2025.

Digital HUD accounts for the largest technology share in Australia's head-up display market, leveraging advanced display technologies such as LED, DMD, and optical waveguide projection to deliver high-resolution, brightness-adaptive imagery across diverse ambient lighting conditions. The scalability of digital architectures makes them inherently compatible with augmented reality overlay integration, allowing manufacturers to upgrade software functionality without overhauling hardware. As per sources, Australia mandated under ADR 98/00 that all new vehicles sold must include autonomous emergency braking systems, reinforcing the nationwide adoption of advanced digital safety ecosystems that directly integrate with HUD-based driver information displays.

Digital HUD's leadership is further underpinned by its energy efficiency advantages relative to legacy CRT-based systems, making it particularly well-suited to electric vehicle platforms where power consumption optimization is a primary engineering priority. Optical waveguide variants are gaining traction for augmented reality applications due to their compact form factor and wide-angle projection capability, while DMD-based systems deliver precision brightness performance suited to large windshield displays. Together, these digital sub-technologies are collectively reshaping Australia's HUD supply landscape toward higher-performance, software-upgradeable display ecosystems.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Aviation

- Automotive

Automotive leads with a market share of 67.3% of the total Australia head-up display market in 2025.

Automotive holds the largest application share in Australia's head-up display market, propelled by sustained growth in new vehicle registrations, the increasing prevalence of ADAS-equipped models, and strong consumer preference for technologically advanced in-vehicle experiences. The electric vehicle transition is a particularly powerful enabler, as leading EV brands sold in Australia standardize advanced digital cockpit features across their lineups, with HUD increasingly positioned as a core component. Growing regulatory emphasis on driver safety and distraction reduction further accelerates HUD standardization across the automotive segment.

The automotive segment's dominance is reinforced by the expanding middle market for HUD-equipped vehicles, as original equipment manufacturers progressively extend display technologies beyond luxury tiers into mainstream price categories. Consumer familiarity with heads-up information interfaces, driven by smartphone navigation and wearable technology adoption, is lowering the perceived complexity of in-vehicle HUDs and broadening the addressable buyer base. Fleet operators, logistics companies, and rideshare platforms are also emerging as meaningful demand contributors, deploying HUD-equipped vehicles to enhance driver safety and operational efficiency across Australia's commercial road transport sector.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales dominates with a market share of 36.5% of the total Australia head-up display market in 2025.

Australia Capital Territory & New South Wales leads the regional market, driven by the ACT's position as Australia's foremost electric vehicle adoption hub and New South Wales's concentration of premium vehicle retail and fleet infrastructure. The region’s proactive EV incentive framework, including stamp duty exemptions and zero-interest loan schemes, has established the highest per-capita EV sales rate in the country, directly expanding the installed base of HUD-equipped vehicles. Sydney's role as the country's primary commercial aviation hub further reinforces HUD demand across the aviation application segment.

New South Wales strengthens the region's leadership through its dense network of automotive dealerships, corporate fleet operators, and technology-forward consumer demographics concentrated in the Greater Sydney metropolitan area. The region also hosts significant aviation infrastructure investment, with Sydney Airport executing a major domestic terminal transformation that will accommodate more advanced, HUD-equipped aircraft generations. Combined, these automotive and aviation demand dynamics position Australia Capital Territory & New South Wales as the enduring epicenter of head-up display adoption and revenue generation throughout the forecast period.

Market Dynamics:

Growth Drivers:

Why is the Australia Head-Up Display Market Growing?

Expanding Road Safety Regulations and ADAS Mandates

Australia's intensifying road safety regulatory environment is a fundamental growth driver for the head-up display market, as government bodies and transport authorities progressively mandate advanced driver assistance technologies across new vehicle categories. Head-up displays directly address distracted driving by maintaining critical information within the driver's forward line of sight, eliminating the need to divert attention to dashboard instruments. According to reports, in May 2024, the Australian Parliament passed the New Vehicle Efficiency Standard (NVES), introducing legally binding emissions regulations for all new vehicles to accelerate adoption of advanced automotive technologies nationwide.

Electric Vehicle Transition Accelerating Digital Cockpit Standardization

Australia's accelerating transition toward electric vehicles is fundamentally reshaping the automotive technology landscape, creating natural demand for head-up display systems as a standard digital cockpit component. Electric vehicle platforms are architecturally designed around centralized computing and software-defined interiors, making HUD integration technically straightforward and commercially compelling for original equipment manufacturers. According to reports, in July 2025, the Australian Government expanded the Driving the Nation Fund to support nationwide EV charging infrastructure and fleet electrification, accelerating adoption of digitally advanced vehicle platforms. As EV adoption expands to mainstream consumers, demand for digital cockpits rises, making head-up displays a standard feature in Australia’s evolving vehicle market.

Growing Consumer Preference for Connected and Immersive Driving Experiences

Australian consumers are increasingly prioritizing connected, technology-rich in-vehicle experiences when making new vehicle purchase decisions, creating powerful demand-side momentum for head-up display adoption. Familiarity with digital interfaces through smartphones, wearables, and navigation applications has raised consumer expectations for intuitive, real-time information delivery within the driving environment. Automakers are responding by positioning HUD as a differentiating feature across both premium and emerging mid-range vehicle categories. This consumer-driven demand dynamic is encouraging original equipment manufacturers to accelerate HUD integration timelines and broaden availability across a wider spectrum of vehicle price points in the Australian market.

Market Restraints:

What Challenges the Australia Head-Up Display Market is Facing?

High Integration and Development Costs

Advanced head-up display systems, particularly augmented reality variants, involve substantial hardware and software integration costs that constrain widespread adoption beyond premium vehicle segments. Windshield preparation, waveguide optics, and real-time rendering processors require significant per-unit investment and extended OEM development cycles, creating meaningful adoption barriers for mid-range and economy vehicle categories where cost sensitivity among manufacturers and consumers remains pronounced.

Windshield Compatibility and Calibration Complexity

HUD performance is highly dependent on windshield geometry, curvature, and glass treatment specifications, creating compatibility challenges for both OEM installations and aftermarket retrofit programs. Achieving precise image registration and parallax correction across varying vehicle architectures requires custom optical calibration, increasing engineering complexity and extending deployment timelines for manufacturers integrating head-up display systems across diverse vehicle platforms and model variants.

Display Visibility Limitations Under Varied Lighting Conditions

Australia's high ambient light intensity, particularly in regional and outback environments, can degrade HUD display visibility for drivers under direct sunlight exposure or when using polarized eyewear. This reliability limitation reduces HUD's effectiveness as a primary information channel in specific geographic and environmental conditions, requiring manufacturers to invest in adaptive brightness and anti-glare technologies that add to overall system cost.

Competitive Landscape:

The Australia head-up display market features a moderately consolidated competitive environment, where global automotive technology specialists dominate through OEM-integrated supply agreements with leading vehicle manufacturers operating across the country. Competition is primarily driven by product differentiation in augmented reality integration capability, display resolution, field-of-view width, and software ecosystem compatibility with digital cockpit platforms. Leading suppliers are investing in co-development partnerships with vehicle OEMs and cockpit domain controller providers to accelerate next-generation windshield and AR-HUD deployment. In aviation, suppliers compete on avionics interoperability, modular retrofitability, and certification speed, as commercial airlines and defense operators prioritize system upgrades that minimize aircraft downtime and operational disruption.

Australia Head-Up Display Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Windshield HUD, Combiner Glass HUD, Collison Warning Only HUD |

| Conventional and Augmented Realities Covered | Conventional HUD, Augmented Reality Based HUD |

| Technologies Covered |

|

| Applications Covered | Aviation, Automotive |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Head-Up Display Market Report

The Australia head-up display market size was valued at USD 36.9 Million in 2025.

The Australia head-up display market is expected to grow at a compound annual growth rate of 16.92% from 2026-2034 to reach USD 158.3 Million by 2034.

Windshield HUD held the largest Australia head-up display market share, driven by its superior field of view, strong alignment with premium vehicle design standards, and growing integration within electric vehicle digital cockpit platforms across the market.

Key factors driving the Australia head-up display market include escalating road safety regulations and ADAS integration mandates, the accelerating electric vehicle transition driving digital cockpit demand, growing consumer preference for connected in-vehicle technology, and sustained aviation fleet modernization and infrastructure investment across commercial and defense sectors.

Major challenges include high integration costs for AR-based HUD systems, complex windshield calibration and compatibility requirements across diverse vehicle platforms, and display visibility limitations under Australia's high ambient light conditions, particularly for drivers using polarized eyewear.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)