Australia Hydrogen Generation Market Size, Share, Trends and Forecast by Technology, Application, System Type, and Region, 2026-2034

Australia Hydrogen Generation Market Overview:

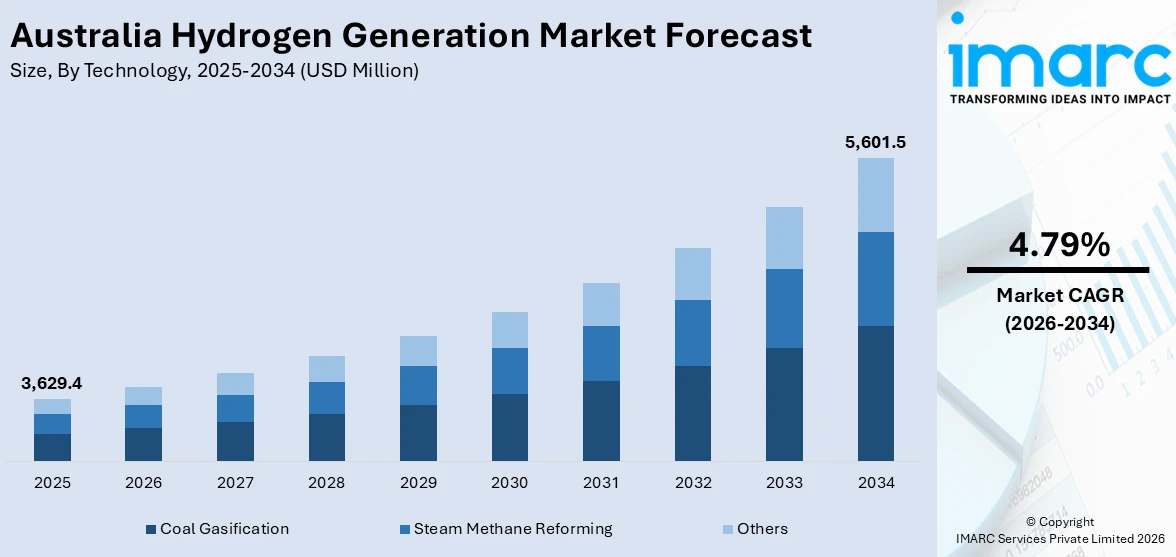

The Australia hydrogen generation market size reached USD 3,629.4 Million in 2025. Looking forward, the market is expected to reach USD 5,601.5 Million by 2034, exhibiting a growth rate (CAGR) of 4.79% during 2026-2034. A strong commitment to decarbonizing the energy sector, supported by regulations aimed at achieving net-zero emissions by 2050, is impelling the market growth. Government incentives, subsidies, and collaborations with international entities are fostering hydrogen as a key element in clean energy. Integration of hydrogen with renewable energy systems, especially solar and wind, enhances grid stability and energy reliability, addressing intermittency issues. These initiatives are expanding the Australia hydrogen generation market share, establishing it as a leader in renewable hydrogen production and export.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 3,629.4 Million |

| Market Forecast in 2034 | USD 5,601.5 Million |

| Market Growth Rate 2026-2034 | 4.79% |

Key Trends of Australia Hydrogen Generation Market:

Government Policy and Investment in Green Hydrogen Initiatives

The robust dedication of the governing authority in Australia to decarbonizing the energy sector significantly is strengthening the hydrogen production market, supported by various policy initiatives and strategies designed to reach net-zero emissions by 2050. In this transition, the governing body is implementing numerous incentives, subsidies, and collaborations with international entities to establish hydrogen as a vital element of Australia’s clean energy future. These efforts are not only encouraging research and development (R&D) but also advancing the commercialization of hydrogen technologies, especially green hydrogen, aligning with the nation's overarching sustainability objectives. The emphasis of the governing authority on developing a competitive hydrogen industry is clear in initiatives such as the Murchison Green Hydrogen Project in Western Australia. In 2025, the Australian Renewable Energy Agency (ARENA) granted $814 million to Copenhagen Infrastructure Partners for the 1,500 MW initiative, representing the initial funding from the Hydrogen Headstart Program. This initiative promotes the creation of extensive renewable hydrogen production, emphasizing the government's proactive involvement in advancing the market. Through these investments, Australia is establishing itself as a global frontrunner in hydrogen production and export, striving to satisfy internal energy requirements while taking advantage of the increasing international demand for clean energy. The funding and strategic policies illustrate how the government is utilizing financial backing and regulatory structures to hasten the creation of the hydrogen production industry.

To get more information on this market Request Sample

Technological Integration with Renewable Energy Systems

The combination of hydrogen manufacturing and renewable energy systems is a critical factor propelling the Australia hydrogen generation market growth. As the nation progresses in increasing its renewable energy capabilities, especially in solar and wind, hydrogen is essential for storing and transporting excess energy. Generating hydrogen when there is a surplus of renewable energy allows for its storage and later use, effectively addressing the intermittency challenges associated with renewable energy sources. The collaboration between renewable energy and hydrogen not only boosts grid stability but also increases energy reliability, positioning hydrogen as an essential element of Australia's clean energy transition. A notable instance of this integration is the introduction of Australia’s inaugural renewable hydrogen microgrid in Denham, Western Australia, set for 2024. Created in collaboration with Horizon Power, the system featured a 348-kW electrolyzer and a 100-kW fuel cell, which together reduced diesel utilization and supplied 20% of the town's energy requirements. This initiative directly aided Western Australia's objectives for a clean energy transition and demonstrates how hydrogen can enhance renewable energy production. The achievements of these projects encourage additional investment in hydrogen technologies, emphasizing the increasing importance of hydrogen in Australia's sustainable energy landscape and aiding in the overall expansion of the hydrogen generation market.

Growth Drivers of Australia Hydrogen Generation Market:

Abundant Natural Resources for Electrolysis

Australia is uniquely positioned for green hydrogen production due to its vast renewable energy resources. The country benefits from some of the world’s highest solar irradiance levels and consistent wind conditions, particularly in regions such as Western Australia, Queensland, and South Australia. These environmental advantages allow for the generation of low-cost, zero-emission electricity required for electrolysis. With renewable energy infrastructure expanding rapidly, Australia can ensure a reliable and scalable power supply for hydrogen generation. The abundance of open land also makes it easier to develop large-scale renewable and hydrogen projects simultaneously. These geographic and climatic factors provide Australia with a strategic advantage, enabling competitive production of green hydrogen at a global scale and strengthening its potential to become a clean energy superpower.

Rising Global Demand for Clean Hydrogen

The international market for clean hydrogen is expanding quickly as countries aim to decarbonize their energy systems. Nations such as Japan, South Korea, and members of the European Union are seeking reliable partners for long-term hydrogen supply, creating strong export opportunities. Australia’s proximity to key Asian markets and its reputation for being a stable, resource-rich exporter position it as a preferred supplier, which is expected to boost the Australia hydrogen generation market demand. As these regions implement aggressive net-zero targets and carbon pricing frameworks, the demand for green hydrogen is expected to surge. Australia’s early investments in hydrogen technology and infrastructure, combined with established trade channels, enhance its competitiveness. This rising global appetite for clean fuels is a powerful growth driver, incentivizing both public and private sector investment in Australia’s hydrogen generation capacity.

Private Sector Engagement and Innovation

Australia’s hydrogen sector is attracting increasing interest from private companies, ranging from global energy giants to domestic startups. These stakeholders are investing in various parts of the hydrogen value chain, including electrolysis technologies, hydrogen storage, transport systems, and end-use applications. This commercial momentum is accelerating innovation, reducing production costs, and enhancing project scalability. Collaborative pilot programs, public-private partnerships, and investment in demonstration projects are helping prove hydrogen’s technical and economic feasibility. The involvement of major industry players is also creating job opportunities, stimulating regional development, and fostering technology transfer. As competition grows, companies are striving to develop more efficient, lower-cost solutions that could accelerate Australia’s emergence as a global hydrogen leader. This dynamic business environment is a critical driver of long-term market growth.

Opportunities of Australia Hydrogen Generation Market:

Export-Oriented Hydrogen Hubs

Australia has a strategic opportunity to develop large-scale hydrogen export hubs by leveraging its extensive coastline and existing deepwater port infrastructure. Ports in regions like Western Australia, Queensland, and the Northern Territory are ideally located to support shipping routes to major Asian markets. Establishing dedicated hydrogen terminals, equipped for liquefaction or ammonia conversion, would facilitate efficient bulk transport of clean hydrogen overseas. These hubs could also serve as anchor points for integrated supply chains, linking generation, storage, and export operations. As international demand for green hydrogen surges, particularly from Japan and South Korea, export-oriented infrastructure can turn hydrogen into a long-term trade commodity. This would not only boost national revenue but also position Australia as a central player in the global clean energy transition.

Integration into Industrial Decarbonization

Hydrogen offers transformative potential for decarbonizing Australia’s emissions-intensive industrial sectors. Industries such as steel manufacturing, ammonia production, cement, and long-haul transport rely heavily on fossil fuels and face increasing pressure to reduce carbon emissions. Clean hydrogen can replace coal, natural gas, and other carbon-intensive feedstocks, enabling these sectors to meet climate goals without compromising productivity. For instance, green hydrogen can power direct reduced iron (DRI) steelmaking or serve as a key input for low-carbon ammonia. Government incentives and corporate net-zero targets are encouraging early investment in hydrogen-based technologies. Integration of hydrogen into industrial systems not only helps companies transition sustainably but also creates demand stability for hydrogen producers, ensuring a viable long-term domestic market alongside export opportunities.

First-Mover Advantage in the APAC Region

Australia’s early and active investment in hydrogen infrastructure provides a strategic first-mover advantage in the Asia-Pacific (APAC) region. By initiating pilot projects, building production capacity, and establishing research collaborations, Australia is ahead of several regional peers in the race to commercialize hydrogen. This leadership allows the country to influence the development of international safety standards, trade rules, and certification frameworks. It also strengthens Australia's negotiating power when forming long-term bilateral agreements with countries like Japan, Singapore, and South Korea. As clean energy demand accelerates, being among the first to market enables Australia to secure preferential trade deals and brand recognition as a reliable hydrogen supplier. This head start could deliver long-term economic and geopolitical benefits in the competitive APAC hydrogen economy.

Challenges of Australia Hydrogen Generation Market:

High Production and Delivery Costs

One of the most pressing challenges for Australia’s hydrogen generation market is the high cost associated with producing and delivering green hydrogen at scale. Electrolysis, the process used to generate hydrogen from water using renewable electricity, is still capital-intensive due to the high cost of electrolyzers and energy input. Additionally, hydrogen storage and transportation require specialized infrastructure, such as high-pressure tanks or cryogenic systems, which adds to the overall cost burden. These factors make green hydrogen significantly more expensive than traditional fossil fuel alternatives, reducing its competitiveness in price-sensitive markets. Without substantial reductions in equipment costs or financial support mechanisms, many projects may struggle to reach commercial viability. These economic constraints could slow down market development and limit the pace of hydrogen adoption in Australia.

Limited Domestic Demand Infrastructure

While Australia’s hydrogen export ambitions are strong, the domestic market remains underdeveloped. Key sectors such as transport, electricity generation, and heavy industry have yet to adopt hydrogen at scale due to a lack of infrastructure, technical readiness, or sufficient policy push. According to the Australia hydrogen generation market analysis, this limited domestic demand poses a risk to hydrogen producers, who require consistent and predictable consumption to justify investments in generation facilities. Without strong local offtake agreements or applications to absorb supply, project economics become uncertain. Additionally, the absence of refueling stations, hydrogen-ready power plants, and industrial-scale applications hinders broader market activation. A more integrated strategy to build domestic demand, through public procurement, fuel mandates, or blending requirements, will be essential to create a stable foundation that supports Australia’s hydrogen sector alongside its export aspirations.

Regulatory Uncertainty and Delayed Approvals

Australia’s hydrogen sector faces hurdles related to regulatory fragmentation and approval delays. Currently, there is no uniform national framework governing hydrogen safety, transport, environmental impact assessments, or certification. This regulatory ambiguity creates uncertainty for project developers, making it difficult to plan investments or secure funding with confidence. Land use approvals, water rights, and environmental clearances vary across states and territories, leading to inconsistent timelines and compliance requirements. These delays can add months or even years to project development cycles, discouraging private sector participation and raising project costs. Furthermore, the lack of clear standards for certifying hydrogen as “green” or “clean” complicates export agreements and investor decisions. Establishing a cohesive, transparent, and nationally aligned regulatory regime is crucial to accelerating growth and ensuring investor confidence in the hydrogen sector.

Government Support of Australia Hydrogen Generation Market:

Strategic National Hydrogen Roadmap

The Australian Government’s National Hydrogen Strategy serves as a foundational guide to establishing a globally competitive hydrogen industry. It outlines key milestones, investment priorities, and technological pathways needed to scale hydrogen production, infrastructure, and adoption. The roadmap emphasizes collaboration between federal, state, and territory governments, as well as coordination with industry, research institutions, and investors. It also highlights the importance of domestic use cases alongside export goals. By setting a long-term vision and defining areas for regulatory development and infrastructure investment, the roadmap brings structure to a rapidly evolving sector. This strategic framework enhances investor confidence, streamlines decision-making, and ensures that hydrogen development aligns with national energy, climate, and economic priorities. It acts as a vital reference for both public and private stakeholders.

Funding Through Key Initiatives

Australia’s hydrogen sector is being significantly supported by government funding programs that aim to reduce commercial risk and attract private investment. Notable initiatives include the Hydrogen Headstart program, which provides production credits to bridge the gap between high green hydrogen costs and market prices, and funding from the Clean Energy Finance Corporation (CEFC), which backs early-stage, scalable projects. These mechanisms are designed to accelerate the commercialization of hydrogen technologies, support large-scale electrolysis deployments, and enable storage and transport infrastructure. Additionally, funding is targeted toward feasibility studies, pilot projects, and industrial applications to validate business models and reduce technological uncertainty. By lowering upfront capital barriers and supporting long-term returns, these programs play a crucial role in enabling Australia to meet its hydrogen production and export goals.

International Collaboration and Trade Agreements

The Australian Government is actively strengthening its hydrogen industry through international collaboration with key trading partners such as Japan, Germany, Singapore, and South Korea. These partnerships are critical for establishing supply chain links, aligning technical standards, and supporting long-term offtake agreements for green hydrogen and its derivatives. Through bilateral agreements, Australia engages in joint feasibility studies, pilot projects, and infrastructure planning, ensuring that its hydrogen export ambitions are grounded in practical demand. These collaborations also support the co-development of certification frameworks, safety regulations, and maritime logistics for hydrogen trade. By participating in global alliances and forums, Australia is enhancing its reputation as a reliable and forward-looking clean energy exporter. Such international engagement not only facilitates technology exchange but also secures market access and investment confidence.

Australia Hydrogen Generation Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on technology, application, and system type.

Technology Insights:

- Coal Gasification

- Steam Methane Reforming

- Others

A detailed breakup and analysis of the market based on the technology have also been provided in the report. This includes coal gasification, steam methane reforming, and others.

Application Insights:

Access the comprehensive market breakdown Request Sample

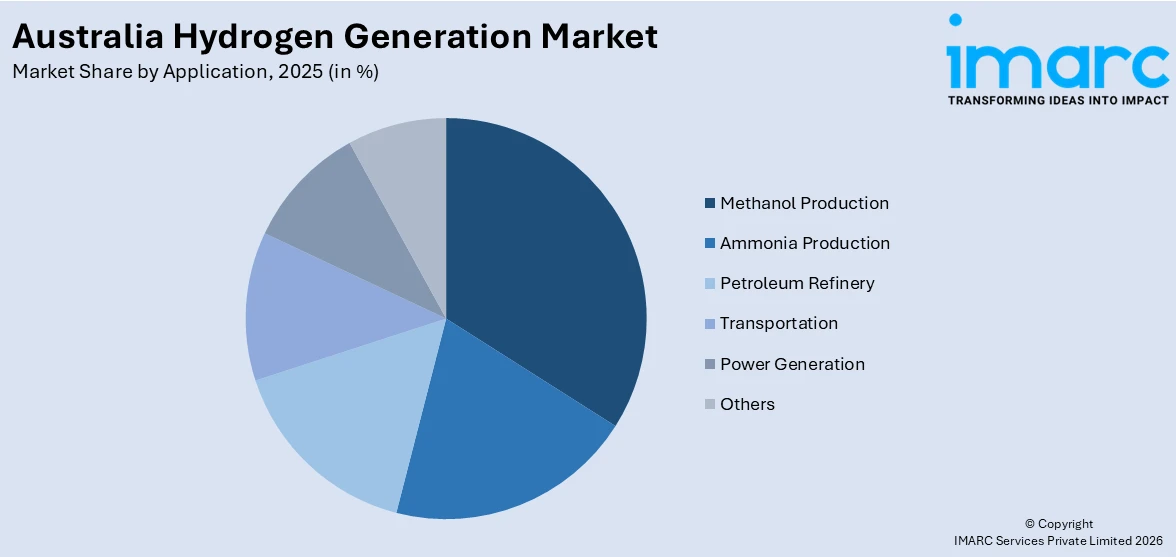

- Methanol Production

- Ammonia Production

- Petroleum Refinery

- Transportation

- Power Generation

- Others

The report has provided a detailed breakup and analysis of the market based on the application. This includes methanol production, ammonia production, petroleum refinery, transportation, power generation, and others.

System Type Insights:

- Merchant

- Captive

A detailed breakup and analysis of the market based on the system type have also been provided in the report. This includes merchant and captive.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Hydrogen Generation Market News:

- In March 2025, Blue Economy CRC launched Tasmania’s first green hydrogen production and research facility at BOC Australia's Lutana site in Hobart. The plant features a large electrolyser and a DC hydrogen microgrid to simulate renewable energy use. It supports both research and commercial-scale hydrogen production.

- In May 2024, Australia announced over A$8 billion (USD $5.3 billion) in investments to develop its clean hydrogen sector as part of the 2024–2025 federal budget. This included a Hydrogen Production Tax Incentive and support for large-scale renewable hydrogen projects.

Australia Hydrogen Generation Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Technologies Covered | Coal Gasification, Steam Methane Reforming, Others |

| Applications Covered | Methanol Production, Ammonia Production, Petroleum Refinery, Transportation, Power Generation, Others |

| System Types Covered | Merchant, Captive |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia hydrogen generation market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia hydrogen generation market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia hydrogen generation industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Hydrogen Generation Market Report

The hydrogen generation market in Australia was valued at USD 3,629.4 Million in 2025.

The Australia hydrogen generation market is projected to exhibit a CAGR of 4.79% during 2026-2034.

The Australia hydrogen generation market is projected to reach a value of USD 5,601.5 Million by 2034.

The Australia hydrogen generation market is shaped by strong government support and investment aimed at achieving net-zero emissions. Key trends include a focus on green hydrogen production from abundant renewable resources, significant private and public investment in large-scale projects, and the development of export capabilities to meet global demand, particularly from Asian markets.

Australia’s hydrogen generation market is growing rapidly, fueled by strong federal support, including funding programs and tax incentives under the Future Made in Australia strategy. Abundant renewable energy resources and rising export demand, particularly from Asia, position Australia as a key player in the global clean hydrogen supply chain.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)