Australia Iron Ore Market Size, Share, Trends and Forecast by Type, End Use, and Region, 2026-2034

Australia Iron Ore Market Summary:

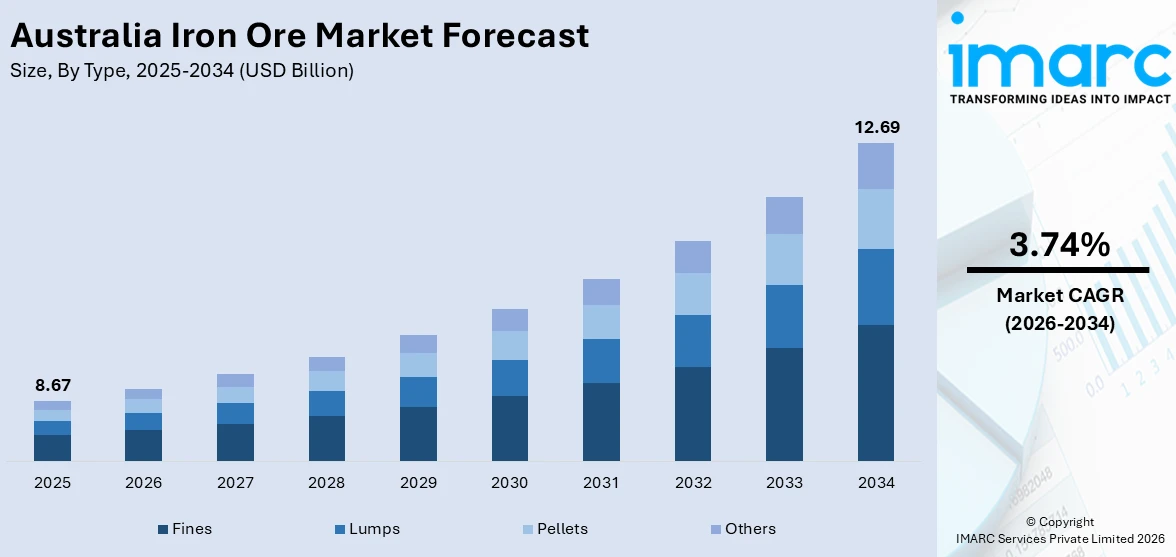

The Australia iron ore market size was valued at USD 8.67 Billion in 2025 and is projected to reach USD 12.69 Billion by 2034, growing at a compound annual growth rate of 3.74% from 2026-2034.

The Australia iron ore market is underpinned by the country’s position as the world’s largest iron ore producer and exporter, supplying a significant share of global seaborne trade. Sustained demand from Asian steelmakers, particularly in China and emerging markets such as India and Vietnam, continues to support production volumes. Ongoing investments in mining infrastructure, mine replacement projects across the Pilbara region, and growing interest in green iron and low-carbon steelmaking technologies are further strengthening the Australia iron ore market share.

Key Takeaways and Insights:

- By Type: Fines dominate the market with a share of 62.5% in 2025, driven by strong demand from Chinese blast furnaces that rely on sintered fines as their primary feedstock for large-scale steel production.

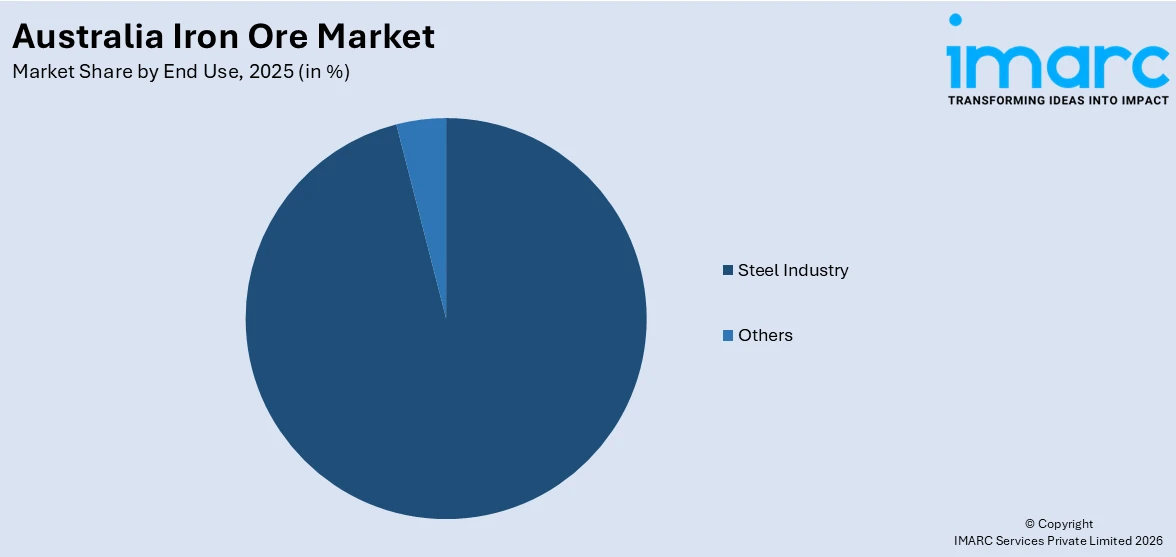

- By End Use: Steel industry leads the market with a share of 96.5% in 2025, reflecting iron ore’s essential role as the principal raw material input for blast furnace and basic oxygen furnace steelmaking processes globally.

- By Region: Western Australia represents the largest segment with a market share of 88.5% in 2025, owing to the vast Pilbara iron ore deposits and world-class export infrastructure including Port Hedland and Dampier.

- Key Players: The Australia iron ore market is highly concentrated, with a small number of large-scale integrated mining companies dominating production, export logistics, and global pricing. Strategic investments in mine replacement, technology innovation, and green iron initiatives are shaping competitive dynamics across the sector.

To get more information on this market Request Sample

Australia’s iron ore sector remains the backbone of the nation’s resource economy, contributing significantly to export earnings and employment. The country produced approximately 40% of global iron ore output in 2024, with nearly all production concentrated in Western Australia’s Pilbara region. The industry is navigating a structural transition as key producers invest in replacement mines to sustain output from maturing deposits. For instance, in June 2025, Rio Tinto’s $2 billion Western Range project commenced commercial production in the Pilbara, designed to produce 25 million tonnes per annum to offset depletion at the Paraburdoo mine. Simultaneously, the sector is pivoting toward green iron technologies to secure long-term demand as the global steel industry decarbonizes. Moreover, the NeoSmelt consortium, comprising five leading resources and manufacturing companies, received AU$19.8 million in ARENA funding for a pilot electric smelting furnace at Kwinana, targeting up to 80% reduction in CO₂ emission intensity from Pilbara iron ore processing.

Australia Iron Ore Market Trends:

Acceleration of Green Iron and Low-Carbon Steelmaking Technologies

Australia’s iron ore industry is increasingly focused on developing technologies that enable low-emission steelmaking using Pilbara-grade ores. The transition toward direct reduced iron and electric smelting furnace pathways is gaining momentum, supported by government funding and industry collaboration. For instance, in March 2025, the Australian Federal Government established a $1 billion Green Iron Investment Fund as part of the Future Made in Australia plan, signaling a strong policy commitment to positioning the country as a global hub for green iron production and supporting the Australia iron ore market growth.

Diversification of Export Destinations Beyond China

Although China continues to be the primary purchaser of Australian iron ore, demand from alternative markets is gradually increasing as emerging economies expand their steel production capabilities. India, as one of the world’s leading steel producers, is emerging as a strategically important destination for Australian exports. This diversification of trade flows reflects broader shifts in global steel demand and supports a more balanced export outlook for Australian iron ore suppliers. According to the industry reports, Australia’s iron ore exports will rise from 953 million metric tonnes in 2024 to approximately 971.9 million metric tonnes in 2025, with emerging Asian economies contributing to demand diversification.

Expansion of Autonomous Mining and Digital Technologies

Australian iron ore producers are adopting advanced automation and digital solutions to enhance operational efficiency, reduce costs, and improve safety across mining operations. The deployment of autonomous haulage systems, remote operations centers, and predictive maintenance technologies is transforming the sector. For instance, in October 2025, Rio Tinto, alongside Mitsui and Nippon Steel, committed a combined investment of $733 million, of which Rio Tinto will contribute $389 million, to advance the West Angelas Sustaining Project. The development forms part of the Robe River Joint Venture operations located in the Pilbara region of Western Australia, incorporating next-generation automated mining systems and digital monitoring platforms designed to optimize extraction rates and reduce operational downtime.

Market Outlook 2026-2034:

The Australia iron ore market outlook is shaped by sustained production volumes, ongoing mine replacement investments, and evolving demand dynamics across Asian steel markets. While traditional blast furnace demand from China is expected to moderate as the economy matures, growth in India and Southeast Asia provides long-term support. Australia’s investments in green iron technologies and value-added processing are expected to create new revenue streams as global steelmakers transition toward lower-carbon production methods. The market generated a revenue of USD 8.67 Billion in 2025 and is projected to reach a revenue of USD 12.69 Billion by 2034, growing at a compound annual growth rate of 3.74% from 2026-2034.

Australia Iron Ore Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

| Type | Fines | 62.5% |

| End Use | Steel Industry | 96.5% |

| Region | Western Australia | 88.5% |

Type Insights:

- Fines

- Lumps

- Pellets

- Others

Fines dominate with a market share of 62.5% of the total Australia iron ore market in 2025.

Iron ore fines represent the most produced and traded form of iron ore in Australia, serving as a key raw material for sintering plants that feed blast furnaces worldwide. The geological characteristics of the Pilbara region naturally result in a significant share of fines during mining and processing activities. Major producers maintain a product portfolio where fines account for a substantial proportion due to strong international demand. Their cost efficiency and compatibility with conventional sintering and blast furnace technologies make fines highly attractive to steelmakers, particularly across Asian markets.

Sustained demand for Australian iron ore fines is largely driven by their affordability and suitability for blending within established steelmaking processes. Many Asian steel producers favor mid-grade fines because they offer operational flexibility and cost advantages. As deposits mature and ore characteristics evolve, the quality profile of fines production is gradually shifting. This has prompted adjustments in market benchmarks and pricing references to better align with prevailing grade specifications and the broader supply landscape within the global iron ore market.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Steel Industry

- Others

Steel industry leads with a share of 96.5% of the total Australia iron ore market in 2025.

Iron ore’s primary use in steel manufacturing firmly establishes the steel industry as the dominant end-use segment in the Australian market. The majority of mined iron ore is directed toward steel production, with key global producers relying heavily on imports to sustain output. The blast furnace–basic oxygen furnace route remains the prevailing steelmaking method worldwide, requiring substantial volumes of iron ore as the main metallic raw material, thereby reinforcing consistent demand for Australian supply.

Rising demand from India’s expanding steel sector further strengthens this segment’s importance. As the country advances large-scale infrastructure and industrial development initiatives, steel consumption continues to grow. Limitations in domestic ore quality and production capacity are likely to encourage greater reliance on imported higher-grade material, supporting sustained long-term demand for Australian iron ore within the steel industry segment. The Australia steel market size reached USD 20.1 Billion in 2025. Looking forward, the market is expected to reach USD 26.2 Billion by 2034, exhibiting a growth rate (CAGR) of 2.91% during 2026-2034.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Western Australia represents the largest share at 88.5% of the total Australia iron ore market in 2025.

Western Australia’s overwhelming dominance is driven by the vast iron ore reserves of the Pilbara region, which hosts most of the nation’s production capacity and export infrastructure. The state is home to world-class operations and benefits from Port Hedland, the world’s largest bulk export terminal by tonnage, along with Dampier and Cape Lambert facilities. In 2025, the total estimated value of iron ore projects in Western Australia’s committed stage increased from AU$6.3 billion in 2024 to AU$9.6 billion, driven by major investments in replacement and expansion mines.

The region’s competitive strengths extend well beyond its rich geological resources, encompassing an extensive rail network, deep-water port infrastructure, a highly skilled workforce, and proximity to major Asian markets. These structural advantages support efficient large-scale mining, streamlined logistics, and reliable export operations. Leading producers continue to channel significant capital into the area, focusing on mine replacement projects, infrastructure modernization, and the integration of advanced technologies. Ongoing investment initiatives are aimed at sustaining long-term production capacity, enhancing operational efficiency, and maintaining the region’s global competitiveness in iron ore supply. The Onslow Iron project in West Pilbara, operated by Mineral Resources, achieved its 35 million metric tonnes per annum nameplate capacity in August 2025, further consolidating Western Australia’s position as the global epicenter of iron ore production.

Market Dynamics:

Growth Drivers:

Why is the Australia Iron Ore Market Growing?

Sustained Demand from China’s Blast Furnace Steelmaking

Despite gradual moderation in China’s overall steel output, the country’s continued reliance on blast furnace technology ensures robust demand for Australian iron ore imports. China remains the world’s largest steel producer and accounts for over 80% of Australia’s iron ore exports. The country has invested heavily in modern, high-quality blast furnaces over the past decade, which require consistent iron ore feedstock and are expected to remain operational for decades. While the proportion of electric arc furnace steelmaking is growing, industry analysts note that the target of 15% EAF production by 2025 has not been fully achieved, with actual EAF ratios remaining above 10%. This structural dependence on the blast furnace route sustains large-volume purchases of Australian fines and lump ore, providing a stable demand foundation for the market.

Significant Investments in Mine Replacement and Expansion Projects

Australia’s leading iron ore producers are committing substantial capital to develop replacement mines and expand production capacity, ensuring long-term supply continuity from the Pilbara region. These investments offset natural depletion at mature operations and support sustained export volumes. For instance, in March 2025, Rio Tinto announced a $1.8 billion investment in the Brockman Syncline 1 mine project, with first production expected in 2027. Such strategic developments reflect the industry’s proactive approach to maintaining stable output levels and reinforcing Australia’s position in the global iron ore trade.

Emerging Demand from India and Southeast Asian Steel Markets

Growing steel production capacity in India and Southeast Asian economies is creating new export opportunities for Australian iron ore producers, partially offsetting the anticipated moderation in Chinese demand. India’s accelerating industrialization and large-scale infrastructure development are fueling strong growth in steel consumption, as the country works toward significantly expanding its total steelmaking capacity. Over the long term, steel requirements are expected to rise substantially, reflecting sustained urbanization, manufacturing expansion, and public infrastructure programs. As domestic iron ore resources face quality and logistical constraints, demand for higher-grade imported material, including Australian supply, is likely to strengthen. At the same time, Southeast Asian economies such as Vietnam and Indonesia are increasing steel production capacity to support industrial growth, further reinforcing regional demand for iron ore.

Market Restraints:

What Challenges the Australia Iron Ore Market is Facing?

Declining Ore Grades at Mature Pilbara Deposits

As long-established mining operations in the Pilbara region approach depletion, the average quality of extracted iron ore is gradually declining. Lower iron content in mined ore reduces product premiums and increases processing costs, challenging the competitiveness of Australian exports against higher-grade competitors from Brazil and Africa’s emerging Simandou deposits.

Increasing Global Supply Competition from New Projects

The anticipated increase in the large international iron ore projects, especially the large-scale projects in Guinea like the Simandou mines, is likely to increase world supply. These projects should transform trade patterns, increase competition among manufacturers, and affect the overall market patterns in major market regions of imports and exports as they move to full-scale operations. Together with the Brazilian expansions, this incremental production promises to cause market oversupply and have a long-term negative effect on the price of iron ore.

Structural Shift in Chinese Steel Technology Toward Scrap Recycling

China’s growing adoption of electric arc furnace steelmaking using scrap steel reduces the country’s reliance on imported iron ore. The growing adoption of scrap-based electric arc furnace (EAF) steelmaking in China is expected to increase its share in overall steel production over the coming years. This structural shift toward greater scrap utilization could reduce reliance on imported iron ore, potentially affecting export volumes from major suppliers such as Australia and other leading producing nations.

Competitive Landscape:

The Australia iron ore market is characterized by a highly concentrated competitive structure, with a small number of vertically integrated mining companies controlling the majority of production, transportation, and export capacity. These leading producers benefit from significant scale advantages, low-cost operations on the global cost curve, and extensive infrastructure networks spanning mines, rail, and port facilities. Competition centers on operational efficiency, product quality differentiation, mine replacement strategies, and the ability to secure long-term offtake agreements with major Asian steelmakers. The industry is also witnessing growing competition around green iron and low-carbon steelmaking technology development, as major producers invest in pilot projects to future-proof their operations against evolving decarbonization requirements in global steel markets.

Recent Developments:

- In January 2026, Scientists confirmed that the Hamersley Province in Western Australia contains what is believed to be the largest known iron ore reserve globally, with an estimated 55 billion metric tons of high-grade ore. At prevailing market prices, the deposit is valued at more than $6.5 trillion. The discovery significantly enhances the strategic importance of the region, reinforcing its position as a cornerstone of global iron ore supply and marking a major geological and economic milestone for Australia’s mining sector.

- In January 2026, Rio Tinto and BHP entered two non-binding Memoranda of Understanding to assess a potential partnership aimed at extracting up to 200 million tonnes of iron ore from their adjacent Yandicoogina and Yandi operations in the Pilbara region. As part of the proposed collaboration, the companies will evaluate joint development opportunities at Rio Tinto’s Wunbye deposit. In addition, BHP may supply ore from its Yandi Lower Channel Deposit to Rio Tinto for processing through Rio’s existing wet plant facilities under mutually agreed commercial arrangements.

Australia Iron Ore Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Fines, Lumps, Pellets, Others |

| End Uses Covered | Steel Industry, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Iron Ore Market Report

The Australia iron ore market size was valued at USD 8.67 Billion in 2025.

The Australia iron ore market is expected to grow at a compound annual growth rate of 3.74% from 2026-2034 to reach USD 12.69 Billion by 2034.

Fines, holding the largest revenue share of 62.5% in 2025, dominate the Australia iron ore market due to their critical role as the primary feedstock for sintering and blast furnace steelmaking, driven by strong demand from Asian steel producers.

Key factors driving the Australia iron ore market include sustained demand from China’s blast furnace steelmaking, significant mine replacement and expansion investments in the Pilbara, emerging export demand from India and Southeast Asia, and growing investments in green iron technologies.

Major challenges include declining ore grades at mature Pilbara deposits, increasing global supply competition from Simandou and Brazilian projects, structural shifts in Chinese steelmaking toward scrap recycling, and downward pressure on iron ore prices.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade