Australia Kraft Paper Market Size, Share, Trends and Forecast by Product Type, Packaging, Application, Distribution Channel, and Region 2026-2034

Australia Kraft Paper Market Summary:

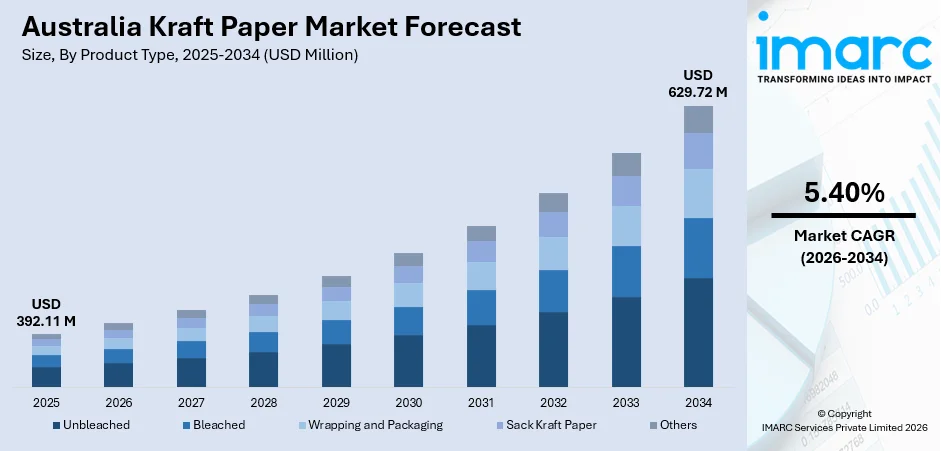

The Australia kraft paper market size was valued at USD 392.11 Million in 2025 and is projected to reach USD 629.72 Million by 2034, growing at a compound annual growth rate of 5.40% from 2026-2034.

The Australia kraft paper market is characterized by steady growth driven by rising demand from packaging, construction, and food industries, supported by sustainability regulations, expanding e-commerce, and preference for recyclable materials, while domestic production, import dependence, price volatility of pulp, and investments in lightweight, high-strength paper influence competitive dynamics and long-term market outlook across diverse end-use sectors nationwide consistently increasingly.

Key Takeaways and Insights:

- By Product Type: Unbleached dominates the market with a share of 52.6% in 2025, due to cost efficiency, strength, and high recyclability.

- By Packaging: Corrugated Box dominates the market with a share of 44.3% in 2025, driven by e-commerce growth and transport packaging demand.

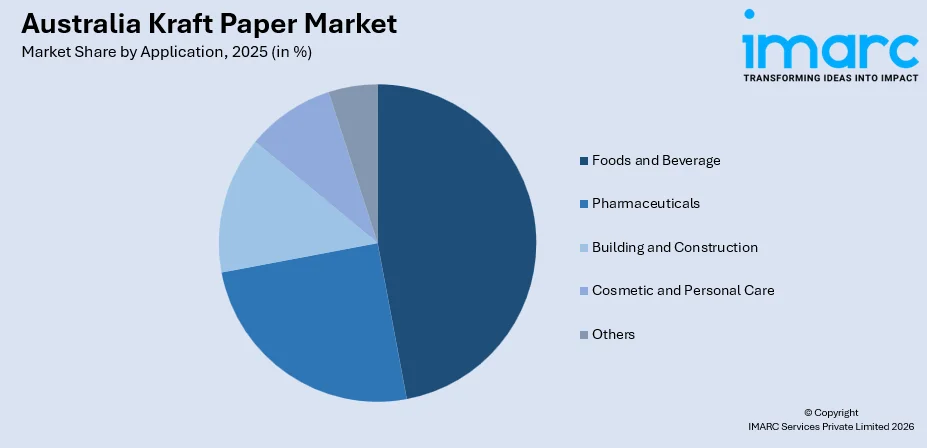

- By Application: In 2025, Foods and Beverage accounted for the highest market share of 47.1%, supported by sustainable food packaging requirements.

- By Distribution Channel: Offline dominates the market with a share of 61.2% in 2025, owing to established supplier networks and bulk purchasing.

- By Region: The Australian Capital Territory and New South Wales held the largest market segment in 2025, capturing 35.0% share, preferred for industrial density and demand.

- Key Players: The competitive landscape features domestic manufacturers and international suppliers focusing on sustainable sourcing, capacity expansion, and product innovation, while competition is shaped by pricing strategies, long-term contracts with packaging companies, and investments in lightweight, high-strength kraft paper to meet evolving regulatory and environmental standards.

To get more information on this market Request Sample

The Australia kraft paper market is experiencing steady growth, fueled by increasing environmental awareness and demand for eco-friendly packaging solutions across multiple industries. Industry reports indicate Australian consumers are highly environmentally conscious, with 96% adopting sustainable practices and 40–62% willing to pay more for eco-friendly packaging. In line with this, rising e-commerce activity and expanding logistics networks are intensifying the need for durable, lightweight, and recyclable paper materials, thereby propelling market growth. Technological advancements in kraft paper production, including improved fiber treatments and enhanced tensile strength, are enabling manufacturers to meet diverse industrial requirements. Furthermore, heightened regulatory emphasis on sustainable materials and reduced plastic usage further supports market expansion. Moreover, small and medium-sized enterprises are increasingly adopting kraft paper for branding and protective packaging. While domestic production remains significant, imports supplement supply to meet high-volume demands. The market is also witnessing growing investments in research and development to enhance product quality, recyclability, and cost efficiency, ensuring long-term competitiveness and sustainability in Australia.

Australia Kraft Paper Market Trends:

Rising Demand for Custom Packaging Solutions

Australian businesses are increasingly seeking customized kraft paper packaging to enhance brand identity and consumer engagement. Companies are adopting tailored sizes, designs, and finishes to meet specific product requirements, particularly in niche food, beverage, and luxury segments. This trend is driving innovation in printing techniques, surface coatings, and structural design, allowing kraft paper to serve both functional and marketing purposes. Manufacturers are also responding by offering flexible production runs and value-added services to capture changing customer demands.

Rapid Integration with E-commerce and Logistics Expansion

The growth of e-commerce in Australia is elevating the importance of kraft paper for protective, lightweight packaging. An industry report highlights that Australians spent a record $69 billion online, up 12% year on year. Online marketplaces accounted for 39% of total online spending growth, while Millennials led eCommerce activity in 2024, contributing 36% of overall online spend. Similarly, retailers and logistics companies are relying on corrugated and kraft-based materials to ensure safe transit, reduce shipping costs, and meet sustainability targets. The trend emphasizes compatibility with automated packing systems, dimensional efficiency, and durability under various handling conditions, making kraft paper a preferred solution for online order fulfillment, warehousing, and last-mile delivery operations.

Heightened Focus on Lightweight, High-Performance Grades

Manufacturers are increasingly producing lightweight yet strong kraft paper to optimize material usage and reduce transportation costs. In tandem, advanced pulping techniques and fiber treatments are being utilized to improve tensile strength, tear resistance, and printability while maintaining recyclability. This trend addresses both environmental regulations and operational efficiency, enabling packaging that is both sustainable and cost-effective. The ongoing development of specialized high-performance grades also expands opportunities across industrial, food, and beverage packaging applications in Australia. For example, Close the Loop Packaging introduced sustainable kraft paper pouches that combine natural aesthetics with high-barrier performance, customisation options, and recyclable or compostable materials, targeting food, beverage, pet care, and wellness brands seeking eco-friendly packaging solutions.

Market Outlook 2026-2034:

The Australia kraft paper market is projected to expand steadily, driven by growing industrial packaging requirements and rising adoption in institutional sectors such as healthcare and pharmaceuticals. In line with this, growing emphasis on lightweight, durable, and moisture-resistant paper grades is expected to enhance product versatility. Likewise, increasing investments in automated manufacturing, digital quality control, and supply chain optimization will support efficiency and market competitiveness. August 2025, Mondi launched Ad/Vantage Smooth Brown Semi Extensible, a next-gen kraft paper particularly designed to meet escalating industrial and packaging requirements. This innovative paper provides a unique combination of superior strength and flexibility, aiding it to withstand significant mechanical stress along with maintaining structural integrity. Additionally, favorable policy incentives promoting sustainable materials and circular economy practices are likely to bolster market demand, ensuring resilient long-term growth across diverse applications. The market generated a revenue of USD 392.11 Million in 2025 and is projected to reach a revenue of USD 629.72 Million by 2034, growing at a compound annual growth rate of 5.40% from 2026-2034.

Australia Kraft Paper Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Unbleached |

52.6% |

|

Packaging |

Corrugated Box |

44.3% |

|

Application |

Foods and Beverage |

47.1% |

|

Distribution Channel |

Offline |

61.2% |

|

Region |

Australia Capital Territory & New South Wales |

35.0% |

Product Type Insights:

- Unbleached

- Bleached

- Wrapping and Packaging

- Sack Kraft Paper

- Others

Unbleached dominates with a market share of 52.6% of the total Australia kraft paper market in 2025.

It is widely preferred in industrial and packaging applications where high tear and tensile resistance are required. The minimal chemical processing involved also aligns with evolving environmental regulations, making it a sustainable choice for manufacturers and end users alike. Its versatility across multiple sectors continues to reinforce its market leadership.

The popularity of unbleached kraft paper is further supported by its recyclability and suitability for both corrugated and flexible packaging formats. Manufacturers benefit from its adaptability to various production techniques, including lamination and coating, allowing for specialized applications. Additionally, businesses increasingly prefer unbleached paper for eco-conscious branding, as it provides a natural, brown appearance without additional chemical treatments.

Packaging Insights:

- Corrugated Box

- Grocery Bags

- Industrial Bags

- Wraps

- Pouches

- Others

Corrugated Box dominates with a market share of 44.3% of the total Australia kraft paper market in 2025.

The durability, cushioning properties, and stackability of corrugated box are ideal for transporting goods safely, particularly in retail and industrial supply chains. For instance, in October 2025, Abbe Group acquired Oji Fibre Solutions Australia, effective 1 November, expanding corrugated packaging capabilities across Victoria, NSW, and Queensland, strengthening regional distribution, and extending its family-owned business’s national reach and customer service offerings. The ability to customize box dimensions and printing further enhances their appeal, enabling businesses to combine functional packaging with branding opportunities.

The demand for corrugated boxes is also influenced by sustainability trends, as they are highly recyclable and increasingly manufactured using eco-friendly materials. Companies are also investing in lightweight corrugated designs to optimize shipping costs while maintaining strength. This combination of versatility, environmental compliance, and cost efficiency ensures that corrugated boxes remain the most utilized packaging segment in the Australian kraft paper market.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Foods and Beverage

- Pharmaceuticals

- Building and Construction

- Cosmetic and Personal Care

- Others

Foods and beverage leads with a share of 47.1% of the total Australia kraft paper market in 2025.

Kraft paper is widely used for packaging bakery items, beverages, and ready-to-eat products due to its strength, moisture resistance, and food-grade compatibility. Similarly, increasing consumer preference for eco-friendly packaging is accelerating the adoption of kraft paper in this sector.

Manufacturers are investing in specialized coatings and barrier treatments to enhance the protective properties of kraft paper while maintaining recyclability. The sector also benefits from regulatory support for sustainable materials in food packaging. With growing demand from both retail and institutional food suppliers, the food and Beverage application remains the primary driver of kraft paper consumption in Australia.

Distribution Channel Insights:

- Offline

- Online

Offline dominates with a market share of 61.2% of the total Australia kraft paper market in 2025.

The segment's leadership stems from longstanding relationships among manufacturers, distributors, and industrial clients. Bulk purchasing through wholesalers and retailers remains a preferred method for businesses seeking consistent supply and lower unit costs. Offline channels also allow for direct consultation, enabling buyers to select suitable grades, sizes, and specifications for specialized applications.

The offline dominance is further supported by established logistics networks, regional warehouses, and dedicated service teams that provide timely delivery and technical guidance. For sectors such as food, beverage, and industrial packaging, offline procurement ensures predictable supply and quality control, thereby sustaining its leading position in the distribution landscape.

Region Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales exhibits a clear dominance with a 35.0% share of the total Australia kraft paper market in 2025.

The region’s concentration of food, beverage, and logistics companies generates strong demand for kraft paper across multiple packaging formats, particularly corrugated boxes. Additionally, the presence of major manufacturing hubs enhances supply chain efficiency, reducing transportation costs and ensuring timely delivery to key end users. According to an industry report, New South Wales and Brisbane have the highest concentration of Industrial, Manufacturing and Resources sites, with 33,528 locations in NSW and 5,534 in Brisbane.

Economic growth and rapid urbanization in these regions continue to support demand for innovative, high-performance packaging materials. The combination of industrial infrastructure, regulatory support, and market accessibility positions Australia Capital Territory & New South Wales as the most influential regional market, driving both domestic production and import reliance for kraft paper solutions.

Market Dynamics:

Growth Drivers:

Why is the Australia Kraft Paper Market Growing?

Growth in Sustainable Packaging Innovation

In the Australia kraft paper market, there is a pronounced shift toward sustainable packaging innovation as manufacturers develop products with enhanced recyclability, biodegradable coatings, and reduced environmental impact. For instance, in August 2025, BioPak acquired Queensland-based Bygreen, combining complementary sustainable packaging products and expertise to expand market reach, strengthen innovation, and advance their shared mission of reducing environmental impact and promoting a circular, plastic-free economy. Businesses increasingly integrate eco‑friendly features to align with stringent environmental policies and consumer demand for greener solutions. This trend fosters research into renewable raw materials, process efficiencies, and lifecycle optimization, positioning kraft paper as a preferred alternative to conventional plastics across diverse packaging applications.

Expansion of Specialty and Technical Grades

The Australian market is experiencing growth in specialty and technical kraft paper grades designed for specific industrial applications. Producers are focusing on high‑strength variants, moisture‑resistant grades, and reinforced materials tailored to logistics, heavy‑duty packaging, and multi‑layer constructions. These advanced offerings address performance requirements previously met by synthetic alternatives, expanding the utility of kraft paper in sectors such as automotive components, machinery parts packaging, and protective industrial wraps.

Enhanced Integration with Circular Economy Practices

Circular economy principles are increasingly influencing the Australian kraft paper market, with stakeholders adopting recycling programs and closed‑loop systems to minimize waste. Accordingly, at TRANSFORM 2025, Australia’s Circular Economy Framework showcased opportunities to double material reuse by 2035, unlocking USD 26 Billion in GDP, cutting emissions 14%, diverting 26 million tonnes from landfill, and driving sustainable growth and innovation nationwide. Furthermore, strategic collaboration between manufacturers, waste management firms, and end‑users supports improved collection, repulping, and reuse of kraft paper products. The favorable government initiatives and industry commitments further encourage resource efficiency and material recovery. This trend not only bolsters sustainability credentials but also reduces raw material costs and reinforces long‑term supply resilience.

Market Restraints:

What Challenges the Australia Kraft Paper Market is Facing?

Volatility in Raw Material Prices

One significant challenge facing the Australia kraft paper market is the volatility in raw material prices, particularly pulp and recycled fiber. Fluctuating global commodity costs impact production expenses and profitability for manufacturers, making cost forecasting difficult. These price swings can lead to inconsistent pricing for end‑users and may deter investment in capacity expansion. Additionally, reliance on imported pulp exacerbates vulnerability to exchange rate shifts and supply chain disruptions, increasing operational risk across the value chain.

Infrastructure and Logistics Constraints

The Australia kraft paper market is constrained by infrastructure and logistics challenges, including limited regional transportation networks and higher freight costs for remote areas. Inefficiencies in storage, handling, and distribution elevate delivery times and overall operational expenses for producers and distributors. These constraints are especially pronounced for bulk shipments and exports, affecting competitiveness. Furthermore, inadequate logistics integration can hinder the timely fulfillment of large orders, reducing customer satisfaction and constraining market scalability.

Regulatory Compliance and Environmental Standards

Compliance with evolving regulatory requirements and environmental standards poses a challenge for kraft paper manufacturers in Australia. Stricter emissions controls, waste management mandates, and sustainability reporting obligations necessitate ongoing investments in cleaner technologies and process upgrades. Smaller producers, in particular, may face financial strain adapting facilities to meet compliance expectations. Additionally, navigating overlapping federal and state regulations increases administrative burdens, complicating strategic planning and potentially slowing market entry for new players.

Competitive Landscape:

The competitive landscape of the Australia kraft paper market is characterized by a mix of established domestic manufacturers and global suppliers striving to differentiate through product quality, sustainability, and service integration. Firms are increasingly investing in advanced manufacturing technologies, strategic partnerships, and supply chain optimization to enhance cost efficiency and responsiveness. Competition centers on meeting diverse industry needs, such as high‑strength grades and eco‑friendly solutions, while navigating raw material price volatility and regulatory compliance. Additionally, companies leverage value‑added services, long‑term contracts with end‑users, and regional distribution networks to strengthen market presence and capitalize on growth opportunities across packaging, industrial, and consumer segments.

Recent Developments:

- In September 2025, Visy completed a USD 30 Million upgrade to its 100% recycled paper mill, producing new corrugated box grades, boosting local jobs, and supporting Queensland’s farmers and food and beverage industries.

- In August 2025, SIG launched Australia’s first recycle-ready bag-in-box wine packaging, made at its Adelaide facility, featuring fully recyclable components, reducing carbon footprint, and supporting local recycling infrastructure with winery partners.

Australia Kraft Paper Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Product Types Covered |

Unbleached, Bleached, Wrapping and Packaging, Sack Kraft Paper, Others |

|

Packaging Covered |

Corrugated Box, Grocery Bags, Industrial Bags, Wraps, Pouches, Others |

|

Applications Covered |

Foods and Beverage, Pharmaceuticals, Building and Construction, Cosmetic and Personal Care, Others |

|

Distribution Channels Covered |

Offline, Online |

|

Regions Covered |

Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Kraft Paper Market Report

The Australia kraft paper market size was valued at USD 392.11 Million in 2025.

The Australia kraft paper market is expected to grow at a compound annual growth rate of 5.40% from 2026-2034 to reach USD 629.72 Million by 2034.

Unbleached dominated the market with 52.6% share in 2025. Its popularity stems from cost-effectiveness, durability, and widespread use in packaging, shipping, and industrial applications, making it the preferred choice among manufacturers and end-users.

Key factors driving the Australia kraft paper market include rising demand for sustainable and recyclable packaging, increased e-commerce activity, environmental regulations favoring eco-friendly materials, expansion of food and beverage sectors, and growing awareness among consumers and businesses about reducing plastic usage.

Major challenges in the Australia kraft paper market include fluctuating raw material costs, competition from alternative packaging materials like plastics and corrugated boards, limited domestic production capacity, supply chain disruptions, and the need for technological advancements to enhance paper strength and eco-friendly processing methods.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)