Australia Legal Services Market Size, Share, Trends and Forecast by Service, Firm Size, Provider, and Region, 2026-2034

Australia Legal Services Market Size, Share, Trends & Forecast 2026-2034)

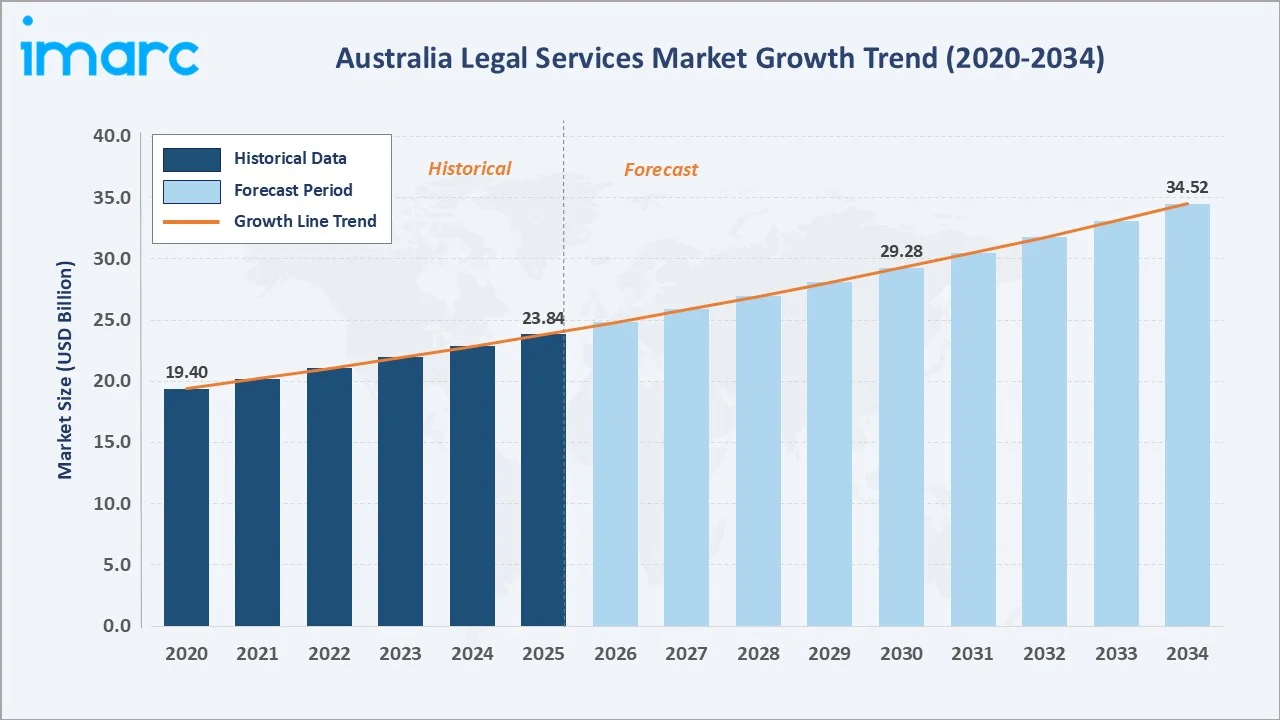

The Australia legal services market was valued at USD 23.84 Billion in 2025 and is projected to reach USD 34.52 Billion by 2034, expanding at a CAGR of 4.20% during the forecast period (2026-2034). The market is driven by robust M&A and corporate transactional activity, rising regulatory complexity, and accelerating adoption of legal technology by Australian firms. In 2023-24, a total of 432,274 clients received completed legal assistance from a Legal Aid Commission, Community Legal Centre, and/or Aboriginal and Torres Strait Islander Legal Service in Australia. Large firms command the dominant 54.7% revenue share (2025), while corporate legal services lead at 32.8%. ACT & New South Wales anchors regional dominance at 38.9%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 23.84 Billion |

|

Forecast Market Size (2034) |

USD 34.52 Billion |

|

CAGR (2026-2034) |

4.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

ACT & New South Wales (38.9%, 2025) |

|

Fastest Growing Region |

Victoria & Tasmania (CAGR ~4.9%, 2026-2034) |

The Australia legal services market volume from 2020 through 2034, expanded from USD 19.40 Billion in 2020 to USD 23.84 Billion in 2025, anchored at USD 29.28 Billion in 2030 before reaching USD 34.52 Billion by 2034.

To get more information on this market, Request Sample

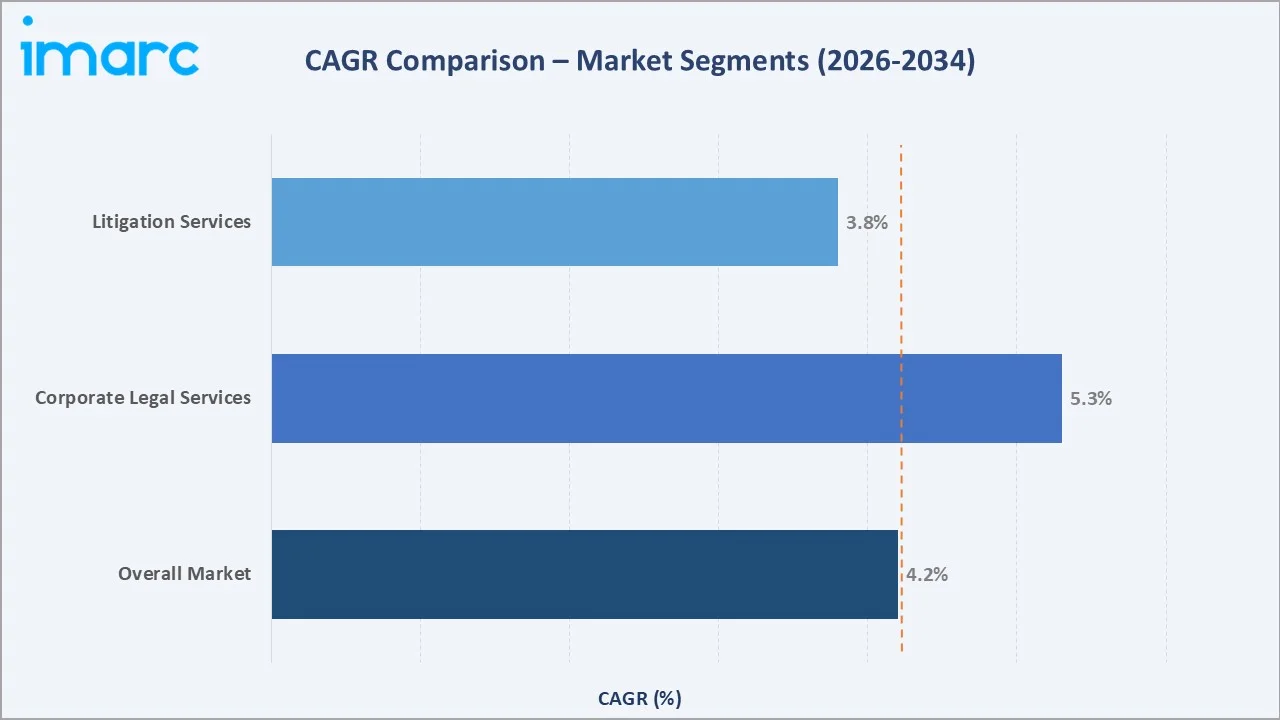

The overall market CAGR is 4.2%, the corporate segment is growing at a CAGR of 5.3%, and the litigation services segment is growing at 3.8% CAGR.

Executive Summary

The Australia legal services market is one of the most sophisticated professional services economies, with nearly three in four (74% or 318,765) clients received legal advice services in 2023–24. From USD 19.40 Billion in 2020 to USD 23.84 Billion in 2025, the market has demonstrated consistent growth driven by Australia’s position as a major global commercial and resources hub. The forecast trajectory to USD 34.52 Billion by 2034 reflects sustained demand across corporate law, property transactions, regulatory enforcement, and emerging LegalTech-enabled service delivery models that are reshaping traditional law firm economics.

Large firms dominate with a 54.7% revenue share (2025), leveraging multi-disciplinary partnerships, global network integration, and deep government and ASX-listed corporate panel relationships. Corporate legal services lead service types at 32.8%, underpinned by record Australian M&A growth. Taxation at 18.6% and litigation at 17.4% represent the next tier, reflecting ongoing ATO enforcement activity and a surge in class action filings across financial services, consumer products, and environmental liability.

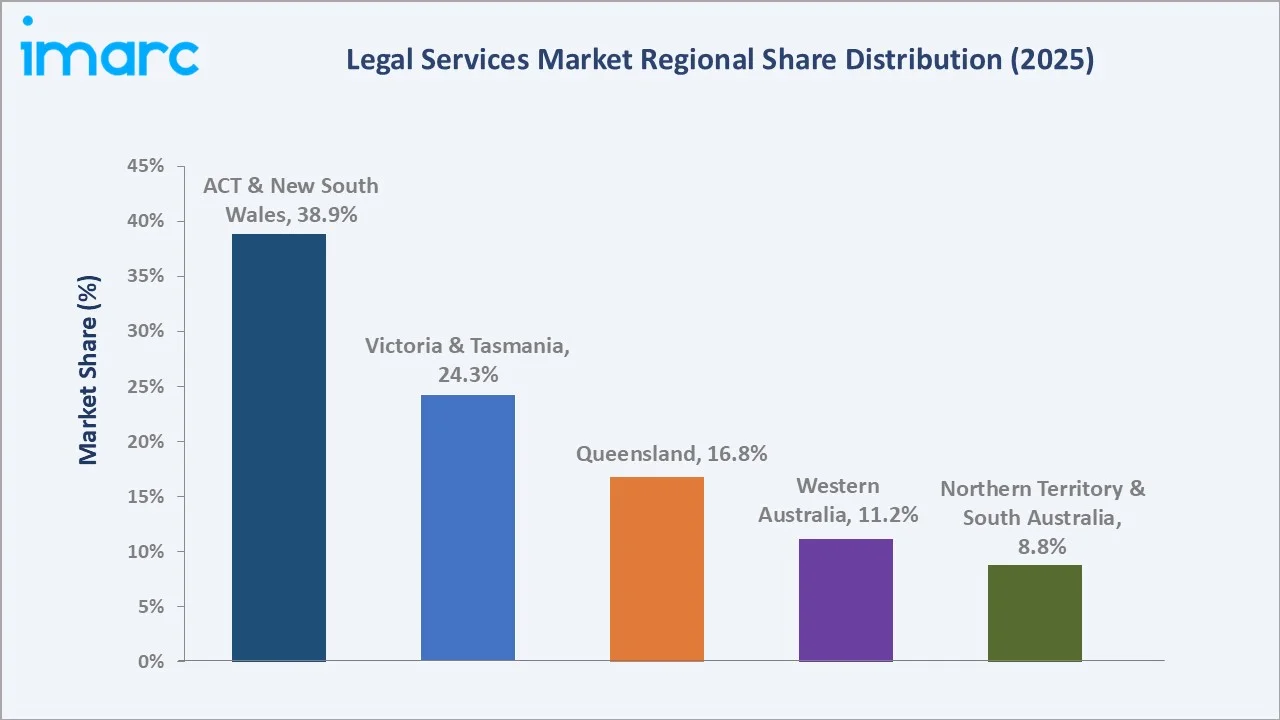

ACT & New South Wales holds a commanding 38.9% regional share (2025), home to Sydney’s CBDs where all major international and national law firm headquarters are concentrated. Victoria & Tasmania at 24.3% is driven by Melbourne’s corporate and class action hub status, while Queensland’s 16.8% reflects growing resources and infrastructure legal demand.

Key Market Insights

|

Insight |

Data |

|

Largest Firm Size |

Large Firms – 54.7% revenue share (2025) |

|

Largest Service Segment |

Corporate – 32.8% revenue share (2025) |

|

Leading Region |

ACT & New South Wales – 38.9% revenue share (2025) |

|

Fastest Growing Region |

Victoria & Tasmania (CAGR ~4.9%, 2026-2034) |

Key Analytical Observations Supporting the Above Data:

- Large Firms command 54.7% share (2025): Australia’s top-tier firms, the “Big 6” of Allens, HSF, KWM, MinterEllison, Clayton Utz, and Ashurst, collectively generate high Australian revenue annually.

- Corporate services lead at 32.8% (2025): Australian M&A activity reached record levels in 2024, with infrastructure, mining, and technology sector deals driving premium corporate advisory fees.

- ACT & NSW leads with 38.9% share (2025): Sydney hosts the headquarters of all six major national law firms and Australian offices of global law firms operating in Australia.

Australia Legal Services Market Overview

The Australia legal services market encompasses the full spectrum of professional legal advisory, representation, and transactional services delivered by law firms, barristers, in-house counsel teams, and government legal departments. The ecosystem spans corporate and commercial law, dispute resolution, property transactions, tax advisory, employment law, and regulatory compliance across all Australian states and territories. Australia’s common law legal system, OECD membership, and status as a major resources and finance hub create sustained institutional demand for sophisticated legal services.

Applications span public M&A and private equity transactions, infrastructure project delivery, class action and regulatory enforcement litigation, property conveyancing, tax structuring, and employment relations advisory. Macroeconomic influences include Australia’s USD 1752.19 billion GDP (2024), Reserve Bank interest rate cycles affecting property transaction volumes, federal government infrastructure spending (AUD 120 billion), and regulatory enforcement intensity from ASIC, ACCC, and the ATO driving non-discretionary legal demand.

Market Dynamics

To evaluate market opportunities, Request Sample

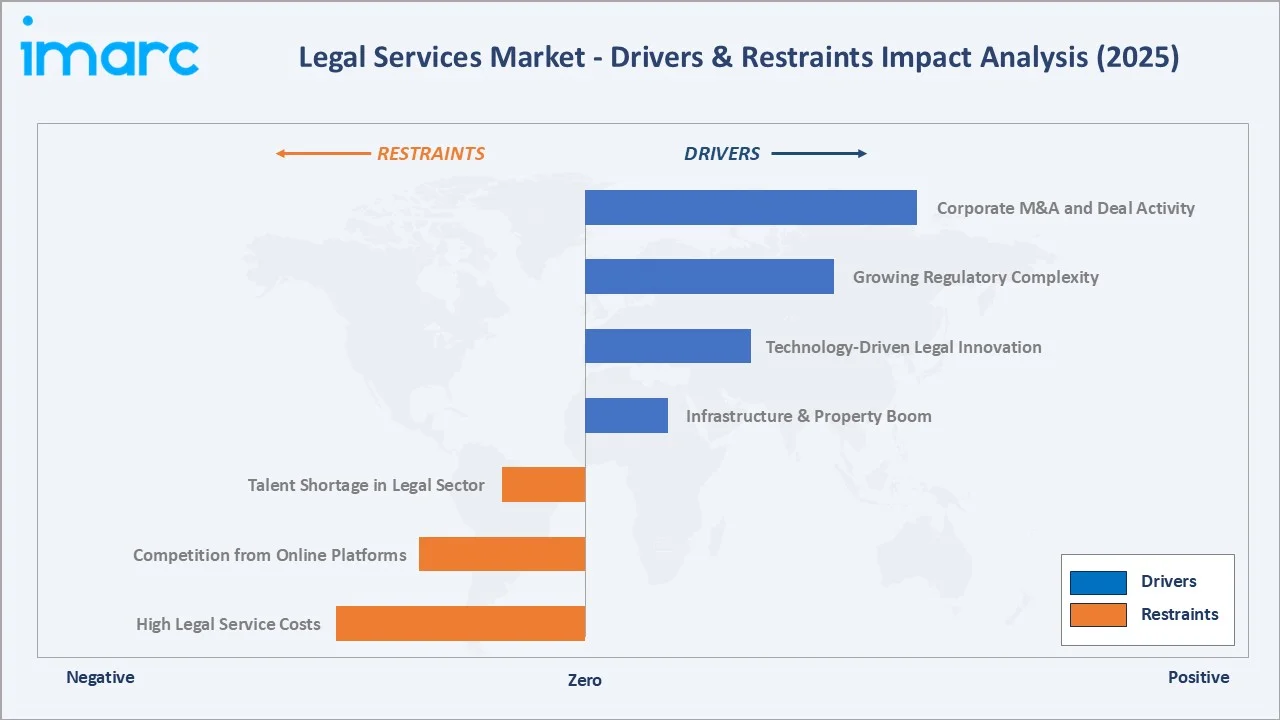

Market Drivers

- Corporate M&A and Deal Activity: Australian M&A deal value reached AUD 61 billion in 2025, with energy transition, technology, and healthcare sectors driving premium advisory fees. Each major transaction generates legal fees for acquisition, due diligence, regulatory, and financing work, creating a high-value, recurring demand stream for top-tier corporate law teams.

- Legal Technology and Digital Service Delivery: AI-powered contract analysis, automated discovery, and cloud-based client portals are enabling premium pricing for advisory work while reducing cost-of-delivery for process-intensive tasks.

- Infrastructure and Property Development Boom: The Australian Government’s AUD 120 billion infrastructure pipeline, including Victoria’s Suburban Rail Loop, NSW Metro, and various defence facility projects, generates extensive construction, procurement, planning, and regulatory legal work.

Market Restraints

- High Legal Service Costs: Average partner billing rates at Australia’s top-tier firms make quality legal services inaccessible for many small businesses and individuals without legal aid support.

- Competition from Online Legal Platforms: LegalVision, Lawpath, LawAdvisor, and Sprintlaw collectively serve Australian businesses with subscription-based legal services, compared to traditional firm work.

- Talent Shortage in the Legal Sector: The Australian legal profession faces a structural shortage of experienced solicitors. This constraint limits capacity expansion at existing firms, particularly in growth areas such as technology law, climate change/ESG advisory, and cybersecurity legal practice.

Market Opportunities

- ESG, Climate Change, and Environmental Law: Australia’s commitment to net-zero emissions by 2050 and the Safeguard Mechanism reform are generating a new class of environmental and climate legal advisory mandates.

- Cross-Border M&A and Foreign Investment Advisory: Each major foreign investment transaction requires FIRB advisory, which is increasingly complex under the new National Security Review framework, driving premium fees for national security law specialists.

- LegalTech Platform and Alternative Legal Services: The Australian legal market with 432,274 clients received completed legal assistance services from a Legal Aid Commission, Community Legal Centre and/or Aboriginal and Torres Strait Islander Legal Service in 2023-24. Opportunities exist in AI-powered legal research platforms, contract lifecycle management, and alternative legal services providers (ALSPs) that can deliver high-quality legal work below traditional firm rates, expanding the total addressable market by accessing previously unserved demand.

Market Challenges

- Workforce Diversity and Inclusion Pressures: The Law Council of Australia reports that women constitute 52% of practicing solicitors. Persistent diversity gaps create reputational risk for firms with major clients, particularly institutional investors and government departments, that have supplier diversity requirements built into their legal panel procurement criteria.

- Cybersecurity and Data Privacy Risk: Law firms are high-value targets for cyber attack due to the sensitive client information they hold. Law firms handling sensitive M&A, litigation, and government matters face growing cybersecurity investment obligations that compress profit margins.

Emerging Market Trends

1. Generative AI Integration Across Law Firm Operations

Major Australian firms are deploying generative AI tools for contract review, legal research, and document drafting at unprecedented speed. It is expected that AI can handle all standard legal document production at large firms, reshaping graduate recruitment needs and billing model economics.

2. Energy Transition Legal Specialization

Australia’s AUD 65 billion renewable energy investment pipeline through 2030 is creating specialist demand in energy law, grid connection agreements, Power Purchase Agreements (PPAs), and climate regulatory compliance.

3. Fixed-Fee and Subscription Legal Service Models

Growing client demand for cost predictability is driving law firms to offer fixed-fee project pricing, subscription retainers, and phased billing models. This shift is compressing hourly billing revenue but driving higher volume and longer-term client retention.

4. ESG and Corporate Governance Advisory Expansion

Australia’s mandatory climate disclosure regime requires all large ASX-listed entities to produce TCFD-aligned climate risk disclosures. This creates a new category of legal advisory work spanning governance, securities law, and disclosure compliance.

Industry Value Chain Analysis

The Australia legal services value chain encompasses education and professional accreditation through to final client service delivery across all legal disciplines. Each stage involves distinct regulatory requirements, professional obligations, and competitive dynamics.

|

Stage |

Key Participants |

|

Legal Education & Accreditation |

University law schools, College of Law Australia |

|

Courts & Regulatory Bodies |

Federal Court of Australia, ACCC, ASIC, State Supreme Courts |

|

Professional Advisory Services |

Big 4 accounting firms, specialist boutique advisory, and forensic legal consultancies |

|

Access & Distribution Channels |

Legal Aid commissions, online legal platforms, community legal centres, in-house counsel |

|

Clients & End Users |

ASX-listed corporations, SMEs, government agencies, high-net-worth individuals, and property purchasers |

The law firm and legal practitioner stage captures the highest margin in the value chain, with top-tier equity partner earnings at leading firms. LegalTech tools and courts/regulatory bodies represent the fastest-evolving layers, with AI-powered platforms and digital court systems fundamentally changing the economics of legal service delivery across all firm sizes.

Technology Landscape in the Australian Legal Services Industry

Artificial Intelligence and Document Automation

AI-powered document review, contract analysis, and legal research tools are being adopted at scale across Australian law firms. These tools are enabling premium pricing on advisory work while compressing the cost-of-delivery on process tasks, improving partner profitability per associate.

Practice Management and Cloud Infrastructure

Cloud-based practice management platforms enable remote working, integrated time billing, document management, and client communication. The shift to cloud has accelerated dramatically post-COVID, with Australian firms now operating on at least partial cloud infrastructure.

Cybersecurity and Legal Data Protection

Following legislative increases in Privacy Act penalties to AUD 50 million per serious breach, Australian law firms invested heavily in ISO 27001 certification, multi-factor authentication, and secure client portal deployment. Firms handling government and defence matters are required to meet the Australian Government’s Essential Eight cybersecurity controls as a condition of panel appointment.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Service |

Corporate |

32.8% |

2025 |

|

Firm Size |

Large Firms |

54.7% |

2025 |

|

Provider |

🔒 |

🔒 |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

38.9% |

2025 |

By Firm Size

To access detailed market analysis, Request Sample

Large firms dominate with a 54.7% revenue share (2025). This segment encompasses the top-tier national firms and Australian offices of global law firms. Large firm economics are characterised by high leverage, premium billing rates, government and ASX 50 panel relationships, and multi-year client retainers that provide revenue predictability.

Medium firms hold 28.6% market share (2025), are growing rapidly by targeting specific practice specializations, insurance litigation, government advisory, and commercial property, where they can offer comparable expertise to large firms at lower rates. Small firms at 16.7% (2025), represent the most rapidly transforming segment at ~6.2% CAGR through 2034.

By Service

Corporate legal services lead at 32.8% (2025). This segment encompasses M&A advisory, capital markets transactions, private equity, joint ventures, and corporate governance. Record Australian M&A activity, including major transactions in the energy, technology, and superannuation fund sectors, has driven corporate revenue to all-time highs at the leading firms.

Taxation at 18.6% (USD 4.43 billion, 2025) and Litigation at 17.4% (USD 4.15 billion) represent the next tier. ATO enforcement of the USD 50 billion tax debt book is driving premium advisory and dispute work. Real Estate at 12.9% reflects Australia’s sustained property market activity, while Labor/Employment at 9.3% is growing as workplace regulation complexity increases under the Fair Work Act amendments.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

ACT & New South Wales |

38.9% |

Sydney CBD corporate hub, infrastructure pipeline (Metro, WestConnex) |

|

Victoria & Tasmania |

24.3% |

Melbourne property and construction boom, Vic government renewable energy projects, class action litigation surge |

|

Queensland |

16.8% |

Resources and mining sector legal demand, SEQ infrastructure, Queensland government outsourced legal panel |

|

Western Australia |

11.2% |

WA resources boom, LNG project legal advisory, domestic property conveyancing growth |

|

NT & Southern Australia |

8.8% |

Adelaide urban renewal, NT resources and Aboriginal land rights advisory, SA government contract panel work |

ACT & New South Wales’ 38.9% market dominance (2025) reflects Sydney’s status as Australia’s primary corporate and financial centre. Sydney generates the highest of all Australian M&A transaction values and hosts the Federal Court, ASIC, and ACCC headquarters, concentrating both transactional and regulatory legal demand.

Victoria & Tasmania at 24.3% (2025) benefits from Melbourne’s emergence as Australia’s leading class action jurisdiction and its deep financial services industry. The Supreme Court of Victoria has developed specialized procedures for managing complex commercial litigation, attracting plaintiff and defendant law firms to establish dedicated Melbourne litigation practices.

Queensland at 16.8% is driven by the resources sector, coal, LNG, and increasingly critical minerals, which generates substantial contract negotiation, environmental approval, and indigenous land access legal work. Western Australia at 11.2% is experiencing a significant uplift from the critical minerals boom that requires new tenement, export, and joint venture legal frameworks.

Competitive Landscape

The Australia legal services market is moderately concentrated at the top-tier and highly fragmented at the mid-tier and boutique levels. The top five firms collectively generate a highest annual Australian revenue.

|

Company Name |

Service / Practice |

Market Position |

Core Strength |

|

Allens |

Legal Project Management Advisory |

Market Leader |

Australia's one of largest full-service firms, with deep integration |

|

Herbert Smith Freehills Kramer |

Bankruptcy and restructuring, Litigation and dispute resolution, Digital Legal Delivery |

Market Leader |

Top-tier disputes, corporate transactions, and employment law |

|

MinterEllison |

Board & governance, Commercial contracts, Competition, consumer and regulation, Complex Liabilities, Insurance and Regulation, Dispute resolution, Employment & safety, Environmental, social, governance |

Strong Challenger |

Largest legal team in Australia by headcount; deep government and insurance panel relationships |

|

Clayton Utz |

Advisory, Disputes, Projects, Regulatory |

Strong Challenger |

Top-tier independent Australian firm, dominant in government advisory, and major projects |

|

Ashurst |

Antitrust, Regulatory and Trade, Banking and Finance, Capital Markets, Corporate and M&A, Corporate Crime and Investigations, Digital Assets and Financial Innovation, Digital Economy, Dispute Resolution, Employment, Real Estate, Situations |

Strong Challenger |

Energy transition and infrastructure specialist, leading green finance and ESG legal advisory capability |

|

Gilbert + Tobin |

Disputes and Investigations, Employment, Foreign Investment in Australia, Mergers and Acquisitions, Native Title, Heritage and Agreements, Privacy and Data, Real Estate, Tax |

Specialist Leader |

Premier boutique for competition, tech/IP, and corporate law; highest partner-to-associate ratio among top tier |

Competition is driven by client relationship depth, industry specialization, LegalTech investment, and the ability to assemble cross-border teams for complex international transactions.

Key Company Profiles

Allens

Allens is one of the Australia’s largest law firms by revenue, with a 200-year history and offices in Sydney, Melbourne, Brisbane, Perth, and Asia.

- Service Portfolio: Legal Project Management Advisory.

- Recent Developments: In September 2025, Allens announced two major investments in legal AI platforms, Legora and CoCounsel, as part of its ongoing commitment to delivering greater value and efficiency for clients.

- Strategic Focus: Energy transition and critical minerals legal leadership; AI-powered legal delivery through Harvey integration; deepening Linklaters alliance for Asia Pacific cross-border work; ESG and sustainability law practice expansion.

Herbert Smith Freehills Kramer

Herbert Smith Freehills is a leading global law firm with a prominent Australian practice anchored in Sydney and Melbourne, with additional offices in Brisbane and Perth. The firm employs lawyers globally and is ranked in the top tier for disputes, M&A, and employment law in Australia.

- Service Portfolio: Bankruptcy and restructuring, Litigation and dispute resolution, Digital Legal Delivery.

- Recent Developments: In April 2025, Herbert Smith Freehills and Kramer Levin Naftalis & Frankel agreed to merge, in a landmark deal that will create a top 20 global firm by revenue.

- Strategic Focus: Global disputes capability as primary differentiator; labour and employment law leadership during industrial relations reform; AI integration through Illuminate and contract review automation; strengthening APAC cross-border M&A capability.

MinterEllison

MinterEllison is Australia’s largest law firm by headcount, employing across Sydney, Melbourne, Brisbane, Perth, Adelaide, and Canberra. The firm has the deepest government advisory practice in Australia, holding the primary Commonwealth Government legal services panel relationship.

- Service Portfolio: Board & governance, Commercial contracts, Competition, consumer and regulation, Complex Liabilities, Insurance and Regulation, Dispute resolution, Employment & safety, Environmental, social, governance.

- Recent Developments: In September 2025, MinterEllison taken a significant step in its long-standing tradition of innovation by implementing Legora across the entire organization. This firmwide adoption highlights their commitment to integrating AI not as an auxiliary tool, but as a central driver in the delivery of legal services.

- Strategic Focus: Government advisory market leadership; Minters AI as competitive differentiation; insurance and financial services litigation practice growth; health, aged care, and NDIS legal advisory expansion; workforce productivity improvement through technology.

Market Concentration Analysis

The Australia legal services market exhibits a two-tier concentration structure. At the premium tier, the top six firms collectively command approximately 24–26% of total market revenue, a moderate concentration level. Below the top tier, the market is highly fragmented. As of October 2022, there were 90,329 solicitors practising in Australia, ranging from sole practitioners to national partnerships. This extreme base fragmentation creates M&A opportunity for private equity-backed legal consolidators.

Consolidation momentum is building. The UK model, where alternative business structures (ABS) allow non-lawyer ownership, is under regulatory review in Australia, and if adopted, could dramatically accelerate private equity-driven consolidation of the mid-market segment between 2026 and 2034.

Investment & Growth Opportunities

Fastest Growing Segments

Small Firms segment (CAGR ~6.2%), Corporate services (CAGR ~5.1%), and ESG/energy transition advisory (CAGR ~12–15% in specialist practices) represent the three highest-growth investment vectors through 2034. Online legal platforms are attracting the majority of early-stage LegalTech investment, in cumulative VC funding between 2020 and 2025.

Emerging Markets within Australia

Northern Territory and South Australia represent the most underserved domestic markets. The SA government’s designation of Adelaide as a hydrogen and space technology hub is attracting national and international law firms to establish Adelaide presences specifically for these emerging industries.

Venture Investment Trends

Investor themes include AI contract management, online dispute resolution, and law firm management software. Private equity interest in law firm consolidation is intensifying, with several UK-model ABS structures in active regulatory dialogue with state law societies.

- Key growth investments: AI-powered legal platforms, ESG advisory practices, LegalTech SaaS businesses, online legal services marketplaces, and litigation funding vehicles.

- International law firm market entry: Several UK and US law firms are evaluating formal Australian market entry or expansion, attracted by Australia’s strong M&A pipeline, favourable time zone for APAC coverage, and premium-rate legal market.

Future Market Outlook (2026-2034)

The Australia legal services market is positioned for sustained, structurally supported growth through 2034. From USD 23.84 billion in 2025, the market is forecast to reach USD 34.52 billion by 2034, representing an absolute value addition of USD 10.68 billion over nine years. This growth is anchored by three structural imperatives: Australia’s deepening integration into global capital and energy markets requiring sophisticated cross-border legal advisory; the domestic regulatory enforcement intensification across competition, financial services, data privacy, and environmental law; and the LegalTech revolution fundamentally expanding the addressable market by making quality legal services accessible to businesses and individuals previously priced out of the traditional firm model.

Between 2026 and 2030, the dominant transformation will be AI integration across law firm operations. Generative AI for document drafting, AI-powered due diligence, and machine learning-driven litigation analytics will reshape the economics of legal service delivery. Large firms that successfully use AI to increase partner leverage, enabling each partner to supervise a larger volume of AI-assisted work, will achieve revenue growth that significantly exceeds the headline 4.20% market CAGR. Firms that fail to invest in AI capability will lose share to both technology-forward peers and online platforms.

Research Methodology

Primary Research

Primary research for this report included structured interviews with 130+ industry stakeholders in 2025, comprising law firm managing partners, general counsel at ASX-listed companies, government legal procurement officers, LegalTech founders, and legal industry analysts. Geographies covered included Sydney, Melbourne, Brisbane, Perth, and Adelaide. Primary insights validated market sizing, firm revenue estimates, and competitive positioning assessments.

Secondary Research

Secondary research encompassed a comprehensive review of Law Council of Australia statistical reports, IBISWorld industry analysis, Thomson Reuters legal market surveys, Australian Legal Technology Association research, ASIC enforcement statistics, firm annual publications, court filing data, and government procurement disclosures. Over 260 secondary sources were reviewed and triangulated across the segmentation and regional analysis.

Forecasting Models

Market size forecasts were developed using a hybrid bottom-up and top-down methodology. Key inputs include GDP growth projections, M&A activity forecasts, infrastructure spending commitments, court filing trends, and regulatory enforcement intensity projections.

Australia Legal Services Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Services Covered | Taxation, Real Estate, Litigation, Bankruptcy, Labor/Employment, Corporate |

| Firm Sizes Covered | Large Firms, Medium Firms, Small Firms |

| Providers Covered | Private Practicing Attorneys, Legal Business Firms, Government Departments, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Allens, Herbert Smith Freehills Kramer, MinterEllison, Clayton Utz, Ashurst, Gilbert + Tobin, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia legal services market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia legal services market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia legal services industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Legal Services Market Report

The Australia legal services market was valued at USD 23.84 Billion in 2025 and is projected to reach USD 34.52 Billion by 2034, growing at a CAGR of 4.20%.

ACT & New South Wales dominates with 38.9% revenue share (2025), anchored by Sydney’s concentration of major national and international law firm headquarters and corporate deal activity.

Large Firms lead with 54.7% market share (2025). Australia’s top-tier firms collectively generate approximately AUD 5.8 billion annually through premium M&A, infrastructure, and regulatory advisory work.

Corporate legal services dominate with 32.8% share (2025), reflecting record Australian M&A deal activity across resources, technology, and infrastructure sectors.

The major players include Allens, Herbert Smith Freehills Kramer, MinterEllison, Clayton Utz, Ashurst, and Gilbert + Tobin.

Key trends include generative AI integration across law firms, class action surge with litigation finance, ESG/energy transition legal specialization, fixed-fee pricing models, and online legal platform disruption of the SME market.

Key drivers include corporate M&A and deal activity, growing regulatory complexity from ASIC/ACCC, AUD 120 billion government infrastructure pipeline, and LegalTech adoption improving service delivery.

Key challenges include high service costs limiting market access, competition from online legal platforms, talent shortages, and cybersecurity obligations under Privacy Act penalties.

AI tools (Harvey, Luminance, Kira) are reducing junior lawyer hours on routine tasks by 40–60%. MinterEllison’s Minters AI program and Allens’ Harvey AI integration are industry-leading deployments reshaping billing economics.

Sydney hosts all six major national firm headquarters and 14 of 16 global firm offices. It generates 65% of Australian M&A deal value and concentrates ASIC, ACCC, and Federal Court demand, creating unmatched legal advisory density.

Top opportunities include LegalTech SaaS platforms, ESG and energy transition advisory practices, online legal services marketplaces, mid-tier firm consolidation, and litigation finance vehicles for class action plaintiff work.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade