Australia Medical Waste Management Market Size, Share, Trends and Forecast by Treatment Site, Treatment, and Region, 2026-2034

Australia Medical Waste Management Market Overview:

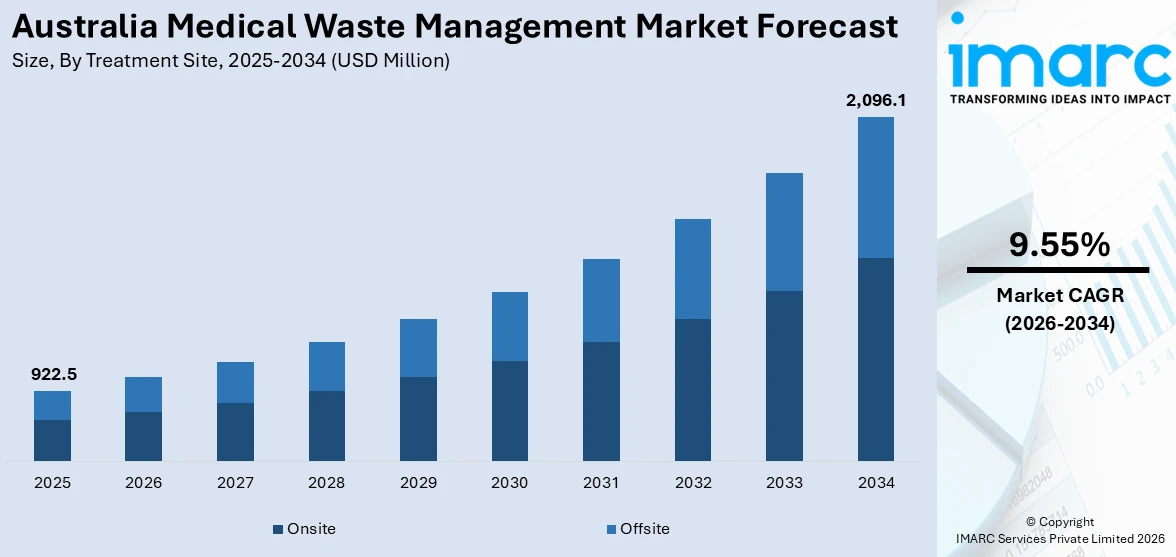

The Australia medical waste management market size reached USD 922.5 Million in 2025. Looking forward, IMARC Group expects the market to reach USD 2,096.1 Million by 2034, exhibiting a growth rate (CAGR) of 9.55% during 2026-2034. The market is driven by stringent environmental regulations mandating structured medical waste handling, alongside rapid expansion of healthcare infrastructure generating complex waste streams. Hospitals increasingly prefer digitalized, traceable, and scalable services aligned with safety and sustainability goals, thereby fueling the market. Technological upgrades and circular economy initiatives further augment the Australia medical waste management market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 922.5 Million |

| Market Forecast in 2034 | USD 2,096.1 Million |

| Market Growth Rate 2026-2034 | 9.55% |

Australia Medical Waste Management Market Trends:

Regulatory Compliance and Healthcare Sector Accountability

Australia’s robust environmental protection framework and healthcare safety regulations are central to the management of medical waste. The Environment Protection and Biodiversity Conservation Act and various state-level laws require hospitals, clinics, and laboratories to segregate, treat, and dispose of biomedical waste in accordance with public health standards. As healthcare institutions face legal consequences for improper handling, compliance has become a non-negotiable operational priority. This has intensified demand for specialized service providers capable of ensuring safe collection, transport, and disposal. The introduction of waste auditing programs and mandatory tracking systems in New South Wales, Victoria, and Queensland has driven investment in data-driven solutions and container-based tracking mechanisms. Additionally, increased awareness of infection control and cross-contamination risk, particularly in post-pandemic settings, has led healthcare providers to seek advanced waste sterilization and incineration systems. Partnerships between public hospitals and licensed waste handlers are also rising to meet capacity requirements. For instance, Nauru has implemented a new medical waste management system across the Pacific, where 85% of healthcare waste is general and non-hazardous, and 15% is hazardous. The innovative non-burning technology decontaminates all types of medical waste using electricity alone and produces no harmful emissions. This system, which replaces high-temperature burning, is environmentally friendly and managed by specially trained local staff. These developments are driving increased service uptake, operational optimization, and infrastructure upgrades, collectively supporting Australia medical waste management market growth.

To get more information on this market Request Sample

Sustainability Goals and Technological Integration in Waste Handling

Sustainability has become a strategic focus in Australia’s medical waste handling ecosystem. Healthcare contributes 4% to 5% of global greenhouse gas emissions, with Australia’s sector producing 35.8 million tonnes annually, or 7% of the country’s total emissions. Plastic production, responsible for 4% of global emissions in 2015, is expected to rise to 15% by 2050, with only 9% of plastics recycled. Hospitals and laboratories are under increasing pressure to meet waste diversion and recycling targets set by environmental agencies and green procurement frameworks. The Australian healthcare sector aims for net zero emissions by 2040, with an 80% reduction in emissions by 2030. As a result, institutions are adopting energy-efficient sterilization technologies, closed-loop recycling systems, and biodegradable packaging alternatives. Innovations such as smart bins, IoT-enabled tracking, and automated sorting platforms have gained traction, helping providers monitor disposal efficiency in real time. Waste-to-energy (WtE) methods are also being piloted in metropolitan regions to reduce landfill reliance. In addition, service providers are integrating lifecycle analysis (LCA) tools and sustainability reporting into their service models, making waste management part of institutional ESG frameworks. Stakeholders, including large hospital groups, diagnostic chains, and pharmaceutical manufacturers, prefer vendors who align with long-term carbon neutrality targets and circular economy principles. These green initiatives are reshaping procurement decisions and increasing adoption of cleaner and smarter disposal solutions across the healthcare value chain.

Australia Medical Waste Management Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on treatment site and treatment.

Treatment Site Insights:

- Onsite

- Collection

- Treatment and Disposal

- Recycling

- Others

- Offsite

- Collection

- Treatment and Disposal

- Recycling

- Others

The report has provided a detailed breakup and analysis of the market based on the treatment site. This includes onsite (collection, treatment and disposal, recycling, and others) and offsite (collection, treatment and disposal, recycling, and others).

Treatment Insights:

Access the comprehensive market breakdown Request Sample

- Incineration

- Autoclaving

- Chemical Treatment

- Others

The report has provided a detailed breakup and analysis of the market based on the treatment. This includes incineration, autoclaving, chemical treatment, and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all major regional markets. This includes Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Medical Waste Management Market News:

- On December 6, 2024, students from the University of Sydney, in collaboration with REMONDIS Australia, tackled the challenge of sustainable medical waste management. The initiative addresses the environmental impact of Australia's 42,000 tons of clinical waste produced annually, aiming to reduce greenhouse gas emissions from traditional disposal methods such as incineration. This project provides students with practical experience while contributing to the development of scalable solutions for waste management in hospitals, clinics, and other healthcare facilities.

Australia Medical Waste Management Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Treatment Sites Covered |

|

| Treatments Covered | Incineration, Autoclaving, Chemical Treatment, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Australia medical waste management market performed so far and how will it perform in the coming years?

- What is the breakup of the Australia medical waste management market on the basis of treatment site?

- What is the breakup of the Australia medical waste management market on the basis of treatment?

- What is the breakup of the Australia medical waste management market on the basis of region?

- What are the various stages in the value chain of the Australia medical waste management market?

- What are the key driving factors and challenges in the Australia medical waste management market?

- What is the structure of the Australia medical waste management market and who are the key players?

- What is the degree of competition in the Australia medical waste management market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia medical waste management market from 2020-2034.

- The research report provides the- latest information on the market drivers, challenges, and opportunities in the Australia medical waste management market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia medical waste management industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)