Australia Mortgage Lending Market Size, Share, Trends and Forecast by Type of Mortgage Loan, Mortgage Loan Terms, Lender, Interest Rate, and Region, 2026-2034

Australia Mortgage Lending Market Summary:

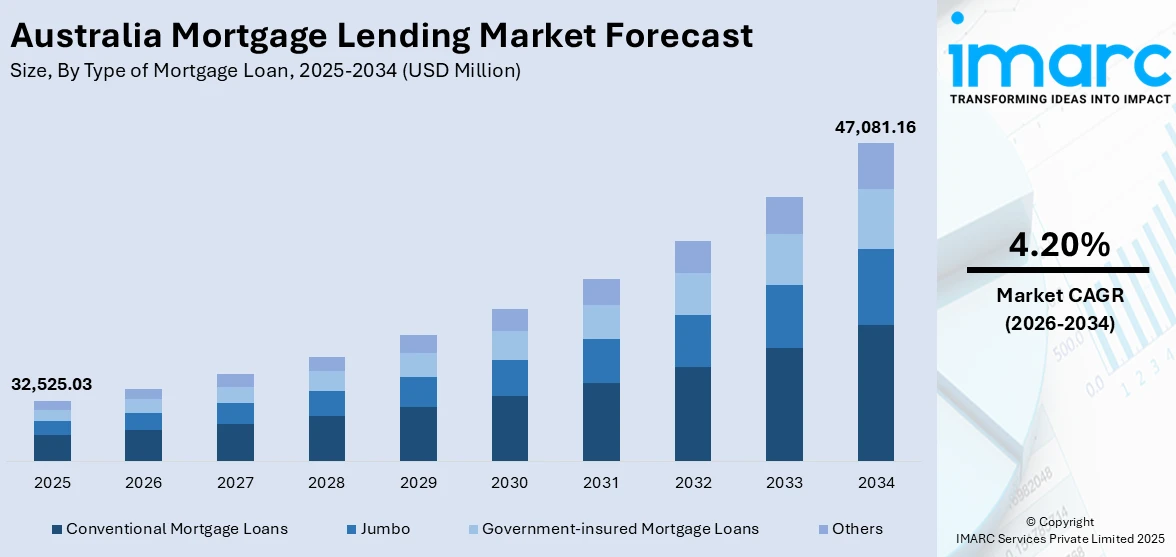

The Australia mortgage lending market size was valued at USD 32,525.03 Million in 2025 and is projected to reach USD 47,081.16 Million by 2034, growing at a compound annual growth rate of 4.20% from 2026-2034.

The Australia mortgage lending market is expanding steadily, underpinned by a resilient housing sector, favorable government homeownership initiatives, and evolving borrower preferences. Increasing demand from owner-occupiers and investors, coupled with ongoing digital transformation in lending processes and the growing adoption of sustainable financing solutions, continues to strengthen market fundamentals. Competitive lending conditions and improving mortgage accessibility across diverse borrower segments are further reinforcing positive momentum.

Key Takeaways and Insights:

- By Type of Mortgage Loan: Conventional mortgage loans dominate the market with a share of 62.9% in 2025, owing to their widespread accessibility, competitive interest rate structures, and strong borrower preference for standardized lending products backed by established financial institutions. Rising property acquisition activity among owner-occupiers is fueling the segment expansion.

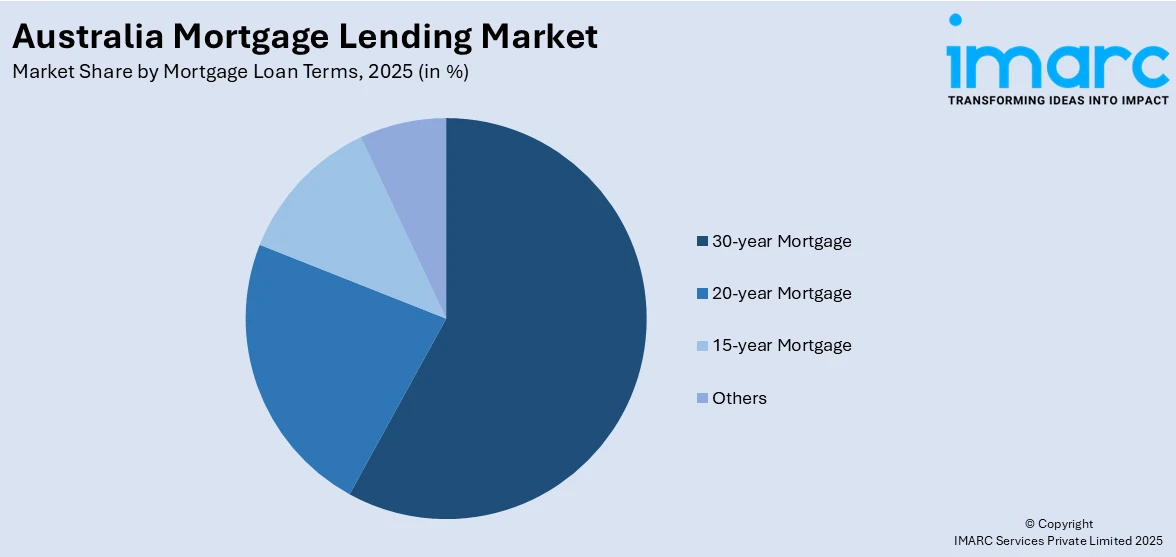

- By Mortgage Loan Terms: 30-year mortgage leads the market with a share of 57.6% in 2025, driven by lower monthly repayment obligations that enhance affordability for households, greater flexibility in budget management, and strong alignment with long-term wealth-building strategies among Australian homebuyers.

- By Lender: Primary mortgage lender comprises the largest segment with a market share of 71.2% in 2025, reflecting the entrenched dominance of authorized deposit-taking institutions that offer comprehensive loan portfolios, competitive pricing, and established customer trust built through decades of regulated lending operations.

- By Interest Rate: Fixed-rate mortgage loan exhibits a clear dominance in the market with 64.5% share in 2025, driven by borrower demand for payment certainty amid monetary policy fluctuations, enabling households to lock in favorable rates and shield themselves from potential future interest rate volatility.

- By Region: Australia Capital Territory & New South Wales represents the largest region with 39.8% share in 2025, driven by Sydney’s concentration of financial services, high property values generating larger loan commitments, robust population growth, fueled by interstate and overseas migration, and strong investor lending activity.

- Key players: Key players drive the Australia mortgage lending market by expanding digital platforms, diversifying product portfolios, offering competitive refinancing solutions, and strengthening broker partnerships to enhance customer acquisition, improve lending efficiency, and capture market share.

To get more information on this market Request Sample

The Australia mortgage lending market is witnessing sustained momentum, as multiple structural and cyclical factors converge to strengthen lending activity. Government homeownership programs, particularly the expanded Home Guarantee Scheme, which from October 2025 allowed all first home buyers to purchase with a 5% deposit without paying lenders mortgage insurance, are materially lowering entry barriers and broadening the addressable borrower base. Digital transformation across lending institutions is streamlining application processes and reducing approval timelines, while growing investor appetite for residential assets and persistent housing supply constraints continue to underpin mortgage origination volumes across all geographic segments of the market. In addition, easing monetary conditions and expectations of greater interest rate stability are improving borrower confidence and refinancing activity. Banks are also intensifying competition through tailored mortgage products, flexible repayment options, and data-driven credit assessments.

Australia Mortgage Lending Market Trends:

Accelerating Digital Transformation in Mortgage Origination

Australian lenders are rapidly embracing digital mortgage solutions to enhance customer experience and operational efficiency. Online application platforms, artificial intelligence (AI)-driven credit assessments, and automated document verification systems are streamlining the end-to-end lending process. Major banks are competing through digital-only home loan products offering lower interest rates exclusively to online applicants. These innovations are significantly reducing approval times and improving transparency for borrowers throughout the loan journey. Enhanced data analytics and open banking integration are also enabling more personalized loan offerings and faster refinancing decisions.

Rising Adoption of Green and Sustainable Home Loans

Sustainability-focused mortgage products are gaining traction, as environmental awareness among borrowers increases alongside regulatory encouragement for energy-efficient housing. Green home loans offer discounted interest rates and reduced lenders mortgage insurance premiums for properties meeting specific energy efficiency standards. Lenders are collaborating with developers and energy assessors to advance certified sustainable housing initiatives. These products incentivize investments in solar panels, efficient insulation, and low-emission building materials. As a result, green mortgages are emerging as a key differentiation strategy while supporting Australia’s broader climate and decarbonization objectives.

Surge in Mortgage Refinancing Activity

Mortgage refinancing has emerged as a dominant trend as borrowers actively seek better terms following successive interest rate reductions. According to data released by the Australian Bureau of Statistics, more than 640,000 homeowners refinanced their mortgages in 2025, reflecting heightened consumer awareness and competitive lender offers. External refinancing volumes have surged as lenders aggressively compete with cashback incentives, reduced fees, and lower variable rates to attract switchers. This refinancing wave is intensifying competition among lenders and reshaping portfolio compositions across Australia’s mortgage lending landscape.

Market Outlook 2026-2034:

The Australia mortgage lending market is positioned for robust expansion over the forecast period, supported by favorable monetary policy settings, strengthening housing demand, and ongoing government interventions to improve homeownership accessibility. The market generated a revenue of USD 32,525.03 Million in 2025 and is projected to reach a revenue of USD 47,081.16 Million by 2034, growing at a compound annual growth rate of 4.20% from 2026-2034. Persistent housing supply shortages, population growth, and rising average loan sizes will sustain credit demand. Digital innovation in lending processes, expanded broker distribution channels, and the continued evolution of product offerings, including green mortgages and flexible repayment structures, are expected to further broaden market participation and bolster sustained revenue growth.

Australia Mortgage Lending Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type of Mortgage Loan |

Conventional Mortgage Loans |

62.9% |

|

Mortgage Loan Terms |

30-year Mortgage |

57.6% |

|

Lender |

Primary Mortgage Lender |

71.2% |

|

Interest Rate |

Fixed-rate Mortgage Loan |

64.5% |

|

Region |

Australia Capital Territory & New South Wales |

39.8% |

Type of Mortgage Loan Insights:

- Conventional Mortgage Loans

- Jumbo

- Government-insured Mortgage Loans

- Others

Conventional mortgage loans dominate with a market share of 62.9% of the total Australia mortgage lending market in 2025.

Conventional mortgage loans maintain leading position in the market, owing to their broad accessibility through major banks and authorized deposit-taking institutions, competitive interest rate structures, and standardized underwriting criteria that streamline the approval process. These loans, which come with fixed and variable rate choices, are intended for borrowers who have established credit histories and adequate deposit savings. Their popularity among first-home buyers, owner-occupiers, and investors is further reinforced by their flexibility in loan tenure, repayment plans, and refinancing choices.

Conventional mortgage loans benefit from significant consumer familiarity and trust developed over decades of broad use. To accommodate a range of financial needs, lenders are constantly improving these products with features, including offset accounts, redraw capabilities, and adjustable repayment plans. Uptake is also supported by competitive pricing brought about by fierce interbank competition. Conventional loans are also appealing across economic cycles because they easily align with government incentives and refinancing plans.

Mortgage Loan Terms Insights:

Access the comprehensive market breakdown Request Sample

- 30-year Mortgage

- 20-year Mortgage

- 15-year Mortgage

- Others

30-year mortgage leads with a share of 57.6% of the total Australia mortgage lending market in 2025.

30-year mortgage remains the preferred mortgage loan term among Australian borrowers because it offers the lowest monthly repayment obligations, thereby enhancing affordability in a market characterized by elevated property prices. This extended tenure allows households to manage cash flow more effectively while maintaining capacity for other living expenses and savings. It is particularly attractive to first-home buyers seeking to maximize borrowing capacity without overstretching monthly budgets. Longer tenures also provide a buffer against short-term income volatility.

The sustained dominance of the 30-year mortgage tenure reflects the structural characteristics of Australian housing finance, where rising property values consistently outpace wage growth. Borrowers selecting this term benefit from greater financial flexibility, enabling them to allocate surplus funds towards offset accounts, redraw facilities, or investment opportunities. This structure supports faster interest reduction when extra repayments are made. As a result, borrowers can balance long-term affordability with strategic wealth-building goals.

Lender Insights:

- Primary Mortgage Lender

- Secondary Mortgage Lender

Primary mortgage lender prevails the market with a 71.2% share of the total Australia mortgage lending market in 2025.

Primary mortgage lender commands the Australia mortgage lending landscape through ability to originate loans directly and access lower-cost deposit funding. The competitive advantage of primary mortgage lenders stems from established regulatory frameworks, economies of scale, and comprehensive product portfolios spanning variable, fixed, and split-rate mortgages. Commonwealth Bank reported average home loan balances of USD 622 Billion during the second half of 2025, representing five percent year-on-year growth and demonstrating the sustained scale advantages that primary lenders maintain across the market.

Deposits, credit cards, and wealth products are parts of integrated banking ecosystems that give major mortgage lenders access to strong client relationships. Throughout the loan lifecycle, this facilitates more robust customer retention and efficient cross-selling. Proficient credit analytics, compliance infrastructure, and advanced risk management skills enable primary mortgage lenders to price risk competitively while adhering to regulatory standards. In addition to improving accessibility and service reach, their vast branch networks and digital platforms strengthen borrower confidence.

Interest Rate Insights:

- Fixed-rate Mortgage Loan

- Adjustable-rate Mortgage Loan

Fixed-rate mortgage loan comprises the largest segment with a 64.5% share of the total Australia mortgage lending market in 2025.

Fixed-rate mortgage loan maintains leading position, as Australian borrowers prioritize repayment certainty and protection against potential interest rate volatility. These products enable households to lock in a predetermined rate for periods typically ranging from one to five years, providing budgetary stability and shielding borrowers from market fluctuations. The competitive dynamics among lenders have further strengthened fixed-rate demand, with institutions aggressively pricing fixed-rate products to attract new borrowers and retain existing customers.

Features like offset accounts, partial prepayment options, and simplified rollover refinancing pathways are increasingly included in fixed-rate mortgage loan packages. In times of economic uncertainty, fixed-rate periods are frequently used by borrowers as a risk-management tool to match payback obligations with predictable income levels. Fixed-rate solutions help lenders with client retention and balance sheet planning. Fixed-rate mortgage loans continue to be attractive to risk-averse borrowers who want certainty while still having access to competitive pricing and flexible loan designs as long as interest rate forecasts are stable.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales represents the leading region with a 39.8% share of the total Australia mortgage lending market in 2025.

Australia Capital Territory & New South Wales commands the largest share of the Australia mortgage lending market, driven by Sydney’s position as the nation’s most populous city and primary financial center. The region’s elevated property values generate substantially larger individual loan commitments, with New South Wales recording the highest average mortgage size nationally at USD 828,000 as of September 2025. Strong population growth fueled by overseas migration, robust investor lending activity, and the concentration of high-income employment in financial services and professional sectors continue to underpin sustained mortgage demand across metropolitan and regional areas.

Strong lending activity across the region is supported by infrastructure investment, improved transport connectivity, and expanding employment hubs. Lifestyle-driven migration to regional centers is sustaining housing demand while maintaining relatively high loan sizes. A diversified borrower base, spanning first-home buyers, upgraders, and investors, supports consistent origination volumes. Additionally, the presence of major lenders’ headquarters and advanced credit assessment capabilities in the region enhances lending efficiency, reinforcing its leadership within Australia’s mortgage lending landscape.

Market Dynamics:

Growth Drivers:

Why is the Australia Mortgage Lending Market Growing?

Supportive Government Homeownership Initiatives and Policy Frameworks

The Australian government’s sustained commitment to expanding homeownership accessibility represents a foundational growth driver for the mortgage lending market. A comprehensive suite of demand-side interventions, including stamp duty concessions, collectively lowers entry barriers for aspiring homeowners and directly stimulates mortgage origination volumes. These policy frameworks create a sustained pipeline of new borrowers entering the mortgage market, reinforcing demand across all lending segments and geographic regions while supporting broader housing market stability. In addition, these initiatives improve borrower confidence by reducing upfront costs and improving loan serviceability outcomes. Continued policy continuity and periodic program expansions are expected to sustain first-home buyer participation and support steady growth in mortgage lending activity over the medium term. According to the Australian Bureau of Statistics, the total value of new home loan commitments for dwellings rose 9.5% in the December quarter of 2025, reflecting strengthening credit demand.

Digital Transformation and Innovation in Mortgage Lending

Rapid digitalization across Australia’s banking and financial services sector is significantly accelerating mortgage lending growth. Lenders are increasingly deploying end-to-end digital mortgage platforms, AI–driven credit assessments, and automated income and identity verification tools to simplify and shorten the loan approval process. These innovations reduce processing costs, improve risk assessment accuracy, and enhance customer experience through faster approvals and greater transparency. Open banking frameworks further support data-driven lending decisions, enabling more personalized pricing and product structuring. Digital-only mortgage products, often offered at competitive rates, are attracting younger and tech-savvy borrowers. Collectively, these advancements are lowering operational friction, increasing application volumes, and supporting higher conversion rates, thereby strengthening overall mortgage origination momentum across Australia. As digital capabilities continue to mature, lenders are also improving post-settlement servicing and retention through real-time account management, predictive analytics, and proactive refinancing offers, further reinforcing long-term lending growth.

Competitive Lending Environment and Product Diversification

Intensifying competition among major banks, non-bank lenders, and digital challengers is expanding access to mortgage credit and stimulating market growth. Lenders are differentiating through competitive pricing, flexible repayment features, offset and redraw facilities, and tailored loan products, targeting specific borrower segments. Growth in refinancing activity, supported by borrower willingness to shop for better rates and terms, is further boosting lending volumes. Non-bank lenders are playing a growing role by serving niche segments and offering faster approvals, while established banks leverage scale and funding advantages to defend market share. This dynamic and competitive landscape encourages continuous product innovation, improves affordability outcomes, and sustains robust mortgage lending activity across Australia. Ongoing marketing campaigns, cash-back offers, and fee waivers are also stimulating borrower switching and new loan origination across the market.

Market Restraints:

What Challenges the Australia Mortgage Lending Market is Facing?

Elevated Housing Affordability Pressures and Mortgage Stress

Despite recent easing in interest rate conditions, housing affordability continues to constrain mortgage market expansion in Australia. Persistently high property prices in major metropolitan areas are stretching household finances and limiting borrowing capacity. While mortgage stress has moderated from earlier peaks, it remains elevated, particularly among lower- and middle-income households. These pressures reduce the pool of eligible borrowers, dampen first-home buyer participation, and restrain overall mortgage demand across price-sensitive consumer segments.

Tightening Macroprudential Regulatory Environment

A more interventionist macroprudential stance by regulators is inhibiting the Australia mortgage lending growth. Stricter limits on borrower leverage and conservative serviceability assessments are reducing loan eligibility, especially for highly geared households and property investors. While these measures strengthen financial system resilience, they also restrict credit expansion and slow lending momentum. Banks face tighter compliance requirements, resulting in more cautious underwriting practices that temper mortgage origination volumes across the broader market.

Interest Rate Uncertainty and Economic Volatility

Ongoing economic uncertainty and shifting inflation dynamics are contributing to an unpredictable interest rate outlook, weighing on borrower sentiment. Concerns over potential policy changes and broader global economic risks are making households cautious about committing to long-term mortgage obligations. This hesitation can delay home purchase decisions, reduce refinancing activity, and suppress new loan demand.

Competitive Landscape:

The Australia mortgage lending market is characterized by intense competition among major banks, regional lenders, and emerging digital challengers. Regional banks and credit unions compete by offering personalized service, competitive rates, and strong local market presence. At the same time, non-bank and digital lenders are gaining traction by delivering faster approvals, flexible underwriting, and innovative, technology-driven mortgage products. This heightened competition is driving pricing pressure, accelerating product innovation, and encouraging lenders to enhance customer experience, ultimately benefiting borrowers through improved affordability and greater choice across the Australia mortgage lending market.

Australia Mortgage Lending Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types of Mortgage Loans Covered |

Conventional Mortgage Loans, Jumbo, Government-insured Mortgage Loans, Others |

|

Mortgage Loan Terms Covered |

30-year Mortgage, 20-year Mortgage, 15-year Mortgage, Others |

|

Lenders Covered |

Primary Mortgage Lender, Secondary Mortgage Lender |

|

Interest Rates Covered |

Fixed-rate Mortgage Loan, Adjustable-rate Mortgage Loan |

|

Regions Covered |

Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Mortgage Lending Market Report

The Australia mortgage lending market size was valued at USD 32,525.03 Million in 2025.

The Australia mortgage lending market is expected to grow at a compound annual growth rate of 4.20% from 2026-2034 to reach USD 47,081.16 Million by 2034.

Conventional mortgage loans dominated the market with a share of 62.9%, driven by widespread accessibility through major banking institutions, competitive pricing structures, and strong borrower preference for standardized loan products.

Key factors driving the Australia mortgage lending market include supportive government homeownership schemes, monetary policy easing, persistent housing supply shortages, rising property values, digital lending innovation, and expanding mortgage broker distribution networks.

Major challenges include elevated housing affordability pressures, tightening macroprudential regulations including debt-to-income lending limits, interest rate uncertainty, persistent mortgage stress among borrowers, and rising property prices that constrain first-time buyer access.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: sales@imarcgroup.com

Client Testimonials

.webp)