Australia Offshore Wind Power Market Size, Share, Trends and Forecast by Installation, Water Depth, Capacity, and Region, 2026-2034

Australia Offshore Wind Power Market Summary:

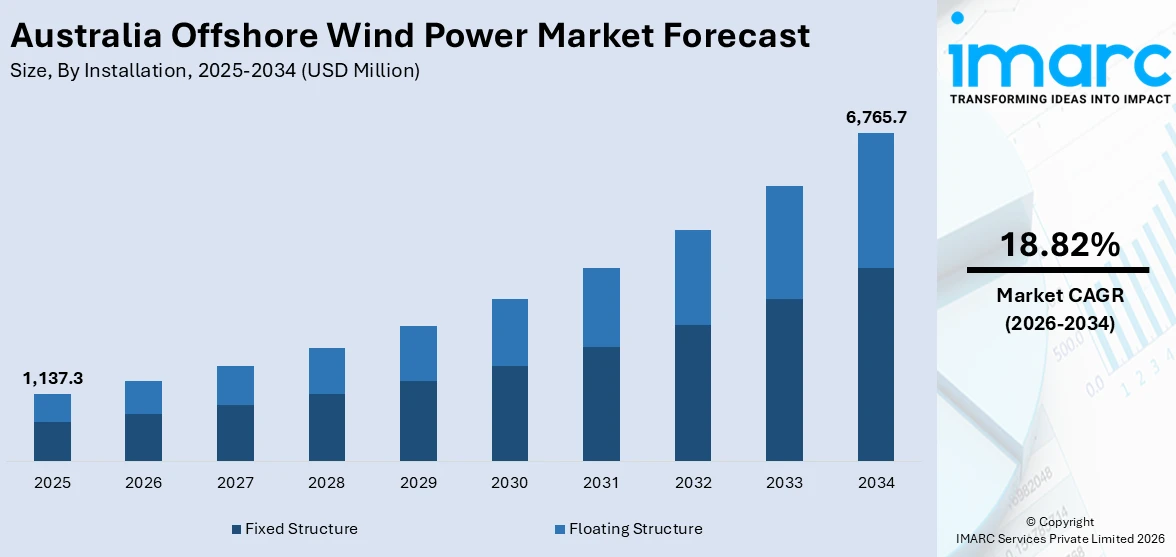

The Australia offshore wind power market size was valued at USD 1,137.3 Million in 2025 and is projected to reach USD 6,765.7 Million by 2034, growing at a compound annual growth rate of 18.82% from 2026-2034.

The Australia offshore wind power market is accelerating as the nation transitions toward cleaner energy sources and reduces reliance on aging coal-fired generation infrastructure. Supportive federal and state regulatory frameworks, expanding offshore wind zone declarations, and the growing investor confidence are collectively strengthening sector momentum. Advancements in turbine technology, favorable coastal wind resources, and increasing energy security priorities are reshaping the competitive landscape, positioning offshore wind as a transformative pillar of the national energy mix.

Key Takeaways and Insights:

- By Installation: Fixed structure dominates the market with a share of 89.0% in 2025, driven by the prevalence of shallow water sites across declared offshore wind zones, mature technology readiness, and significantly lower capital costs compared to floating alternatives.

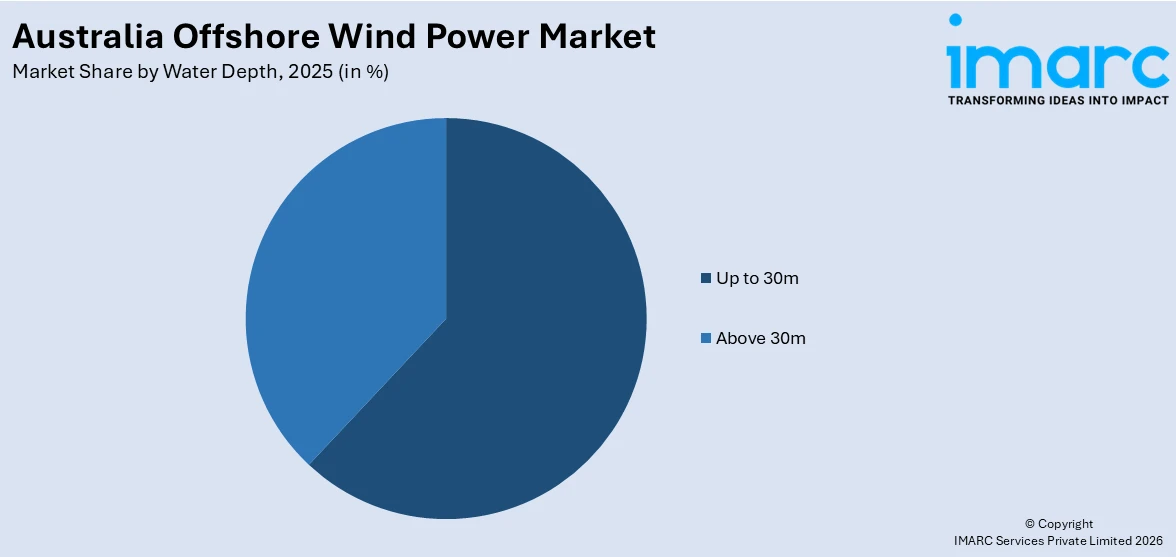

- By Water Depth: Up to 30m leads the market with a share of 62.5% in 2025, reflecting the favorable bathymetric conditions in key development zones where shallow continental shelves enable cost-effective fixed-bottom foundation deployment and simplified installation logistics.

- By Capacity: Above 5MW represents the largest segment with a market share of 78.5% in 2025, underscoring the industry preference for high-capacity turbines that maximize energy output per unit, reduce levelized cost of electricity, and improve overall project economics.

- By Region: Victoria & Tasmania dominate the market with a share of 52.5% in 2025, due to world-class wind resources in Bass Strait, legislated offshore wind targets, advanced regulatory frameworks, and the concentration of project development activity in the Gippsland zone.

- Key Players: The Australia offshore wind power market is increasingly competitive, with established global energy developers securing feasibility licenses, forming strategic joint ventures, investing in environmental assessments, and building local supply chain partnerships to capture emerging opportunities across declared offshore wind zones.

To get more information on this market Request Sample

The offshore wind power market in Australia is becoming a central pillar of the national energy transition, driven by formal renewable capacity targets and the establishment of a dedicated offshore regulatory regime. Clear licensing frameworks, declared offshore wind zones, and staged approval pathways are creating structured entry points for large-scale private investment. Momentum accelerated in 2024 when Australia awarded its first offshore wind feasibility licenses to six projects proposed offshore Gippsland, Victoria, representing a combined capacity of approximately 12 GW. Developers, including Ocean Winds, Ørsted, Copenhagen Infrastructure Partners, and Parkwind/JERA Nex, were able to undertake detailed environmental and technical studies before progressing toward commercial licenses. The government also signaled that up to six additional licenses may be granted, potentially expanding planned capacity in the zone to 25 GW. This measured yet ambitious rollout demonstrates policy-backed market formation, reinforcing offshore wind’s role in replacing retiring coal assets and supporting long-term energy security objectives.

Australia Offshore Wind Power Market Trends:

Precision-Led Resource Mapping to De-Risk Large-Scale Projects

A clear market trend is the growing reliance on advanced measurement technologies to reduce development risk before final investment decisions. Developers are prioritizing high-resolution wind and ocean data collection to optimize turbine configuration, foundation engineering, and grid connection design. In 2025, Ocean Winds launched Australia’s first offshore wind and metocean measurement campaign for the 1.3 GW High Sea Wind project in Gippsland, deploying a floating LiDAR buoy with TGS to capture wind, wave, and current data. This structured data-led approach strengthens energy yield modelling, supports environmental assessments, and improves lender confidence in large, capital-intensive offshore wind developments.

Stronger Federal Intervention to Accelerate Project Approvals

Another important trend is the increasing role of the federal government in fast-tracking strategically significant offshore wind developments. Enhanced coordination mechanisms are being used to help developers navigate complex environmental, maritime, and regulatory processes. In 2025, JERA Nex BP’s 1 GW Blue Mackerel project in Gippsland received Major Project Status, granting access to dedicated support from the Major Projects Facilitation Agency. This designation reflected a policy shift toward proactive approval management to reduce bottlenecks and provide greater certainty around timelines. Federal facilitation is strengthening investor confidence and signaling national commitment to accelerating offshore wind deployment.

Development of Multi-Gigawatt Offshore Clusters in Designated Zones

The emergence of large-scale project clustering within formally declared offshore wind areas is a crucial trend influencing the market growth in Australia. Developers are pursuing multi-gigawatt capacity portfolios in zones supported by state planning frameworks and future auction pathways. For example, in 2024, Ørsted secured a feasibility license and was progressing a second for two offshore wind projects off Gippsland with a combined potential capacity of 4.8 GW. Located between 56 and 100 kms offshore, the projects planned to undergo detailed site investigations and environmental studies before auction participation. This clustering strategy supports coordinated transmission planning and long-term capacity build-out in high-resource regions.

Market Outlook 2026-2034:

The Australia offshore wind power market demonstrates exceptional growth potential throughout the forecast period, supported by irreversible energy transition imperatives and strengthening policy frameworks. The market generated a revenue of USD 1,137.3 Million in 2025 and is projected to reach a revenue of USD 6,765.7 Million by 2034, growing at a compound annual growth rate of 18.82% from 2026-2034. The scheduled retirement of aging coal-fired power stations, ambitious state-level renewable energy targets, the maturation of feasibility assessments into construction-ready projects, and the anticipated first offshore wind auction in Victoria are expected to catalyze substantial capital deployment and revenue generation across the forecast horizon.

Australia Offshore Wind Power Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Installation |

Fixed Structure |

89.0% |

|

Water Depth |

Up to 30m |

62.5% |

|

Capacity |

Above 5MW |

78.5% |

|

Region |

Victoria and Tasmania |

52.5% |

Installation Insights:

- Fixed Structure

- Floating Structure

Fixed structure dominates with a market share of 89.0% of the total Australia offshore wind power market in 2025.

Fixed structure leads the market due to its suitability for shallow coastal waters where most early-stage projects are planned. Australia’s identified offshore wind zones, particularly along the southern coastline, offer seabed conditions that support monopile and jacket foundations. This installation structure provides strong stability and proven performance in established European markets, giving developers greater confidence during initial investments. Fixed installation also benefits from mature supply chains and standardized engineering practices, reducing technical uncertainty. Lower construction complexity compared to floating systems helps manage project timelines. This practicality makes fixed structure the preferred choice for current large-scale offshore developments.

Another factor supporting fixed structure dominance is cost efficiency at commercial scale. Developers can leverage existing global expertise, vessel availability, and installation methods refined over decades. Financing institutions often favor fixed-bottom projects due to its established track record and predictable performance metrics. Grid connection planning is also simpler for nearshore fixed installations, lowering transmission risks. Government feasibility studies are prioritizing zones with suitable depths for fixed foundations, accelerating regulatory approvals. As Australia builds its offshore wind industry from the ground up, early projects naturally align with technologies that offer reliability and clearer return visibility, reinforcing fixed structures as the leading installation type.

Water Depth Insights:

Access the comprehensive market breakdown Request Sample

- Up to 30m

- Above 30m

Up to 30m leads with a market share of 62.5% of the total Australia offshore wind power market in 2025.

Up to 30m represents the largest segment owing to the concentration of proposed project zones in relatively shallow coastal areas. Many designated offshore wind regions, particularly along Victoria and parts of South Australia, feature seabed depths within this range, making them technically suitable for fixed-bottom foundations. Shallow waters simplify installation processes, reduce foundation complexity, and limit reliance on specialized floating platforms. Developers can deploy monopile or jacket structures using established construction methods, which lowers engineering risk. Shorter distances from shore also ease grid connection planning and maintenance logistics. These practical advantages position shallow-water sites as the initial focus for project development.

Another reason for the dominance of the up to 30m segment is cost predictability during early market formation. Installation vessels, cranes, and support equipment are more readily available for shallow-water projects, helping control capital expenditure. Construction timelines are generally shorter compared to deeper sites, improving financing confidence. Environmental assessments and seabed surveys are also more straightforward in nearshore zones. Australia’s offshore wind sector is still emerging, so developers are prioritizing lower-risk depth categories to establish operational experience. As the industry scales and supply chains mature, deeper projects may expand, but current investment momentum remains concentrated in shallow waters within this depth range.

Capacity Insights:

- Up to 3MW

- 3MW to 5MW

- Above 5MW

Above 5MW exhibits a clear dominance with a 78.5% share of the total Australia offshore wind power market in 2025.

Above 5MW holds the biggest market share driven by the industry’s focus on utility-scale generation. Offshore wind projects require high upfront investment, so developers prioritize larger turbines to maximize output per installation. Turbines above 5MW generate significantly more electricity per unit, reducing the number of foundations and grid connections needed for a given project size. This improves overall project economics and lowers maintenance intensity over the asset lifecycle. Australia’s strong coastal wind resources further support deployment of high-capacity turbines designed for higher efficiency. These performance advantages make larger capacity units the preferred choice for commercial offshore developments.

Another reason for the dominance of turbines above 5MW is the alignment with global technology trends. International manufacturers are increasingly producing high-capacity offshore turbines with improved blade design and enhanced reliability. Australian developers benefit from adopting these proven models, which offer better capacity factors and stronger returns on investment. Fewer turbines per project also simplify installation planning and reduce seabed disturbance. Grid infrastructure planning becomes more efficient when power is concentrated in higher-output units. As Australia builds large offshore wind farms to meet renewable energy targets, demand naturally concentrates in the above 5MW segment, securing its leading share in installed capacity.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Victoria and Tasmania dominate with a market share of 52.5% of the total Australia offshore wind power market in 2025.

Victoria and Tasmania command a leading share of the market because of superior wind conditions along the southern coastline and proactive state policy frameworks. Persistent Southern Ocean wind systems support strong and consistent generation potential, reinforcing project viability. Victoria has advanced regulatory clarity and procurement planning, attracting early developer participation. This leadership was reinforced in 2025 when the Victorian Government confirmed it will open the request for proposal stage in September 2025 for its first 2 GW offshore wind auction, with contracts expected before October 2026 under a contract-for-difference and availability payment structure. Tasmania benefits from established renewable integration and interconnection capacity, further strengthening regional prominence.

Another factor behind their leadership is proximity to industrial demand centers and established energy markets. Victoria’s large electricity usage base creates stable long-term offtake opportunities for offshore projects. Port infrastructure in cities, such as Geelong, supports potential assembly, staging, and maintenance operations. Tasmania’s experience with hydropower and renewable integration strengthens its capability to manage variable offshore wind generation. State-level renewable energy targets and investment facilitation programs have accelerated project pipelines. Developers seeking lower regulatory uncertainty and strong wind profiles naturally prioritize these regions. This concentration of planning, infrastructure readiness, and resource quality secures Victoria and Tasmania’s leading regional share.

Market Dynamics:

Growth Drivers:

Why is the Australia Offshore Wind Power Market Growing?

Entry of Global Renewable Majors into the Local Market

The participation of established international energy companies is shaping the competitive structure of Australia’s offshore wind sector. Large global developers are leveraging experience from mature offshore markets to secure early-stage licenses and position themselves for long-term growth. For example, in 2024, RWE obtained a seven-year feasibility license for the 2 GW Kent Offshore Wind Farm in the Bass Strait, marking its first offshore wind site in Australia. This move expanded RWE’s domestic renewable presence beyond solar and battery storage. The entry of such firms introduces technical depth, financing capacity, and execution expertise that support market credibility and pipeline expansion.

Rising Electricity Demand and Grid Replacement Needs

Australia’s electricity demand profile is evolving due to population growth, electrification of transport and industry, and the gradual retirement of ageing coal-fired power stations. Offshore wind offers large, stable generation capacity that can replace retiring baseload assets while supporting grid reliability. Coastal load centers, particularly in southeastern Australia, are located near high-quality offshore wind resources, reducing transmission congestion risks relative to remote onshore generation. The need to maintain energy security during the transition away from fossil fuels is accelerating procurement of long-duration, utility-scale renewable capacity, positioning offshore wind as a critical component of future generation portfolios.

Technological Advancements and Cost Reductions

Advances in turbine size, floating foundation technology, digital monitoring systems, and installation techniques are improving project efficiency and lowering lifecycle costs. Larger turbines increase energy output per unit, reducing the number of installations required and optimizing seabed utilization. Improvements in subsea cabling, grid connection design, and predictive maintenance systems enhance operational reliability and reduce downtime. As global deployment expands, knowledge transfer and standardization are supporting cost efficiencies across procurement and construction phases. These technological improvements are strengthening project bankability and making offshore wind increasingly competitive within Australia’s evolving electricity generation mix.

Market Restraints:

What Challenges the Australia Offshore Wind Power Market is Facing?

High Upfront Capital Costs and Financing Complexity

Offshore wind projects require substantial capital investment, with individual projects potentially requiring multi-billion dollar commitments. The complexity of structuring project finance for a nascent industry without established local track records creates additional barriers, as lenders and investors require proven revenue certainty mechanisms before committing large-scale capital deployment.

Inadequate Port Infrastructure and Supply Chain Gaps

Most Australian ports lack the deep-water berths, heavy-lift capacity, and specialized facilities required for offshore wind turbine assembly, component staging, and operational maintenance. The absence of a mature domestic manufacturing supply chain for turbine foundations, towers, and blades increases dependency on imports and elevates logistics costs across the value chain.

Regulatory and Approval Process Complexity

Navigating overlapping federal, state, and local government approval processes creates lengthy development timelines and regulatory uncertainty for offshore wind project proponents. Environmental assessment requirements, indigenous heritage consultation obligations, and evolving legislative frameworks add procedural complexity that can delay project progression from feasibility through to final investment decision and construction commencement.

Competitive Landscape:

The Australia offshore wind power market features a competitive landscape dominated by international energy developers and renewable energy specialists establishing positions through feasibility license acquisitions and strategic partnerships. Market dynamics are characterized by developers leveraging global offshore wind experience to navigate the emerging regulatory framework, with competition intensifying around securing optimal project sites, supply chain partnerships, and future government revenue support mechanisms. The anticipated first offshore wind auction in Victoria is expected to significantly shape competitive positioning, as developers compete on project economics, local content commitments, and delivery capability. Strategic joint ventures between international expertise holders and domestic partners with local market knowledge are emerging as the preferred approach for managing development complexity and risk across this evolving market landscape.

Recent Developments:

- January 2026: Australia’s Department of Climate Change, Energy, the Environment and Water awarded final feasibility licenses to three offshore wind projects in the Bunbury zone off Western Australia. The projects, including Bunbury Offshore Wind South, Bunbury Offshore Wind North, and Westward Wind, could deliver around 4 GW of installed capacity within a zone capable of generating up to 11.4 GW. The move enables detailed site investigations and consultation, advancing large-scale offshore wind development in the region.

- December 2025: Star of the South lodged Australia’s first offshore wind Environmental Impact Statement under the EPBC Act, marking a key step toward federal approval. The project also secured a 120-hectare shore crossing site in Gippsland, renewed Major Project Status, and formalized an agreement with GLaWAC. Planned at up to 2.2 GW, the development aims to power 1.2 million homes and invest $7 billion into the Australian economy.

Australia Offshore Wind Power Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Installations Covered | Fixed Structure, Floating Structure |

| Water Depths Covered | Up to 30m, Above 30m |

| Capacities Covered | Up to 3MW, 3MW to 5MW, Above 5MW |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Offshore Wind Power Market Report

The Australia offshore wind power market size was valued at USD 1,137.3 Million in 2025.

The Australia offshore wind power market is expected to grow at a compound annual growth rate of 18.82% from 2026-2034 to reach USD 6,765.7 Million by 2034.

Fixed structure dominates the market with 89.0% revenue share in 2025, driven by the prevalence of shallow water development sites, mature technology readiness, and lower capital costs compared to floating platform alternatives.

Key factors driving the Australia offshore wind power market include stronger federal involvement in accelerating approvals for nationally significant projects. In 2025, JERA Nex BP’s 1 GW Blue Mackerel project received Major Project Status, enabling dedicated facilitation support to streamline environmental and regulatory processes and improve timeline certainty.

Major challenges include high upfront capital investment requirements, inadequate port infrastructure for turbine assembly and staging, regulatory and approval process complexity across multiple government jurisdictions, supply chain gaps, and financing uncertainty for a nascent domestic industry.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade