Australia Organic Beverages Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

Australia Organic Beverages Market Summary:

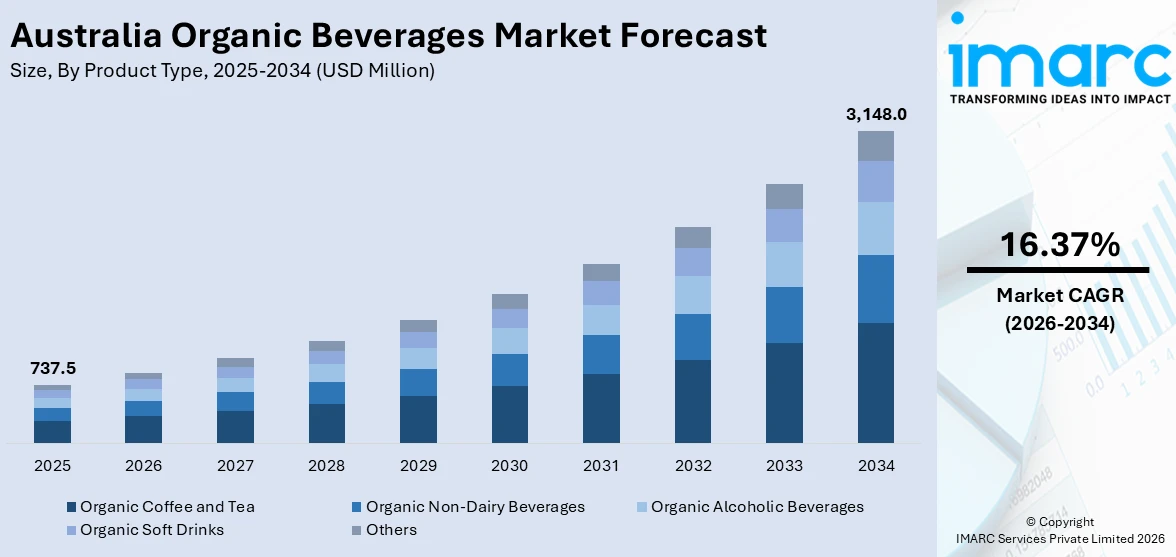

The Australia organic beverages market size was valued at USD 737.5 Million in 2025 and is projected to reach USD 3,148.0 Million by 2034, growing at a compound annual growth rate of 16.37% from 2026-2034.

The market for organic beverages in Australia is expanding rapidly as consumers place a higher value on clean-label, sustainably produced, and health-conscious drink options. Consumption patterns are changing due to the growing demand for functional beverages that provide benefits for immunity, digestive health, and wellness. The market for organic beverages in Australia is poised for continuous expansion due to factors such growing plant-based dietary consumption, expanding retail availability, and more environmental awareness.

Key Takeaways and Insights:

- By Product Type: Organic coffee and tea dominates the market with a share of 31.4% in 2025, owing to deep-rooted coffee culture, rising demand for specialty blends, and growing interest in herbal and functional teas that support wellness and digestive health.

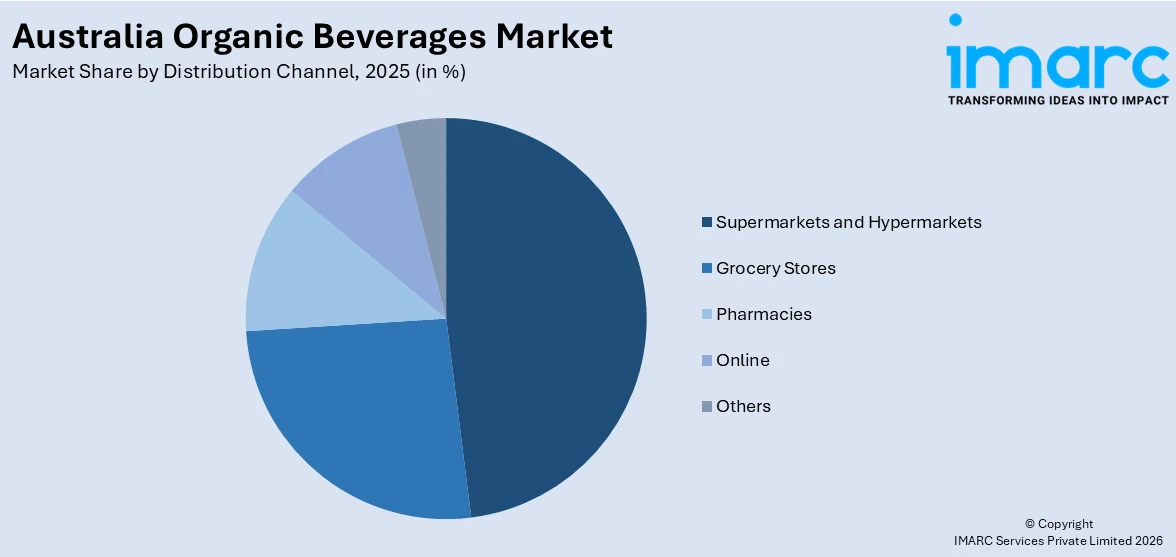

- By Distribution Channel: Supermarkets and hypermarkets lead the market with a share of 47.8% in 2025. This domination is driven by a wide range of products, organic shelf space, and the ease of one-stop shopping, which promotes organic beverage sampling and recurring business.

- By Region: Australia Capital Territory and New South Wales represent the largest region with 35.2% share in 2025, driven by a dense network of upscale retail establishments that encourage the accessibility of organic beverages, higher disposable incomes, and the concentration of health-conscious metropolitan residents in Sydney and Canberra.

- Key Players: The market for organic beverages in Australia is driven by major companies who enhance formulation technology, broaden product offerings, and fortify statewide distribution. They increase awareness, speed up adoption, and guarantee steady product availability through their marketing, sustainability, and retail chain connections. Some of the key players operating in the market include Byron Bay Coffee Company, Montville Coffee, Ovvio Organics, Planet Organic, República Organic, Tea Gardens Kombucha, and Tea Tonic.

To get more information on this market Request Sample

As consumers, retailers, and manufacturers all seek cleaner, more transparent beverage options that are in line with current wellness concerns, the Australian organic beverage market is growing. Growing consumer knowledge of the negative health consequences of artificial additives, preservatives, and genetically modified ingredients is causing consumers to choose organic products in a variety of categories, such as teas, kombuchas, plant-based milks, and cold-pressed juices. Products that boost intestinal health, strengthen the immune system, and improve cognition are drawing younger consumers and fitness enthusiasts to the functional beverage market, which is seeing significant growth. In July 2024, Sanitarium launched its Plantwell range of functional plant-based milks with clinically proven superfood ingredients at Woolworths stores across Australia, reflecting growing manufacturer investment in science-backed organic formulations. Consumer access is being further expanded by the growing retail infrastructure, which is bolstered by the establishment of specialty health food stores and organic sections within large supermarket chains. Furthermore, direct-to-consumer organic beverage sales, subscription models, and individualized product discovery are made possible by the quick development of e-commerce platforms, which supports the expansion of the organic beverages market in Australia.

Australia Organic Beverages Market Trends:

Rising Demand for Functional and Wellness-Oriented Organic Beverages

Organic beverages that offer specific health advantages beyond simple hydration are becoming more and more popular among Australian consumers. Probiotic-rich kombuchas, adaptogenic teas, and drinks with a gut health focus are examples of functional products that are becoming increasingly popular with wellness-conscious consumers. This change reflects a wider consumer preference for drinks made with natural, organic ingredients that promote brain clarity, digestive health, and immunity. Demand for the organic functional beverage category is rising as a result of manufacturers being encouraged to create novel formulations that cater to particular wellness requirements, such as stress reduction, increased metabolism, and improved cognitive function, by the growing intersection of beverage consumption and preventive health management.

Expansion of Organic Plant-Based Beverage Alternatives

As consumer dietary choices shift toward dairy-free, vegan, and allergy-friendly products, Australia's organic plant-based beverage market is expanding rapidly. Products made from organic oats, almonds, soy, and coconut milk are quickly becoming commonplace in food service and retail settings. The consumer base is being greatly increased by the increasing use of plant-based milks in cafés, especially organic oat milk for barista-grade applications. In response, producers are offering a variety of products, such as flavored, functional, and fortified plant-based substitutes that mimic the flavor and texture of traditional dairy while offering better nutritional profiles and sustainability credentials.

Growing Influence of Clean-Label Transparency and Organic Certification

When choosing beverages, Australian consumers are giving greater weight to ingredient clarity, clear labeling, and confirmed organic certification. Growing awareness of greenwashing tactics and consumer demand for products with identifiable, natural ingredients are the main drivers of this movement. The ecology of organic beverages as a whole is being strengthened by the legislative push for regulatory certainty. Younger consumers in particular prefer brands that exhibit genuine commitment to organic integrity, traceable supply chains, and environmentally responsible manufacturing processes across their whole product portfolios. Consumers are actively reading labels and looking for clarity on sourcing and production practices.

Market Outlook 2026-2034:

Underpinned by shifting consumer health concerns, expanding retail accessibility, and ongoing product innovation across functional and plant-based categories, the Australian organic beverages market is expected to grow significantly and sustainably over the course of the forecast period. Consistent demand increase is anticipated due to growing urbanization, rising disposable incomes, and the growing presence of organic beverage options in mainstream grocery chains. The market generated a revenue of USD 737.5 Million in 2025 and is projected to reach a revenue of USD 3,148.0 Million by 2034, growing at a compound annual growth rate of 16.37% from 2026-2034. The market is expected to gain speed because to the growing e-commerce distribution, the growing acceptance of functional beverages, and the ongoing transition to plant-based dairy substitutes. Furthermore, it is anticipated that manufacturers' growing investments in sustainable production methods and the continuous regulatory changes pertaining to domestic organic certification criteria would boost consumer confidence and market penetration throughout Australia.

Australia Organic Beverages Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Organic Coffee and Tea |

31.4% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

47.8% |

|

Region |

Australia Capital Territory and New South Wales |

35.2% |

Product Type Insights:

- Organic Coffee and Tea

- Organic Non-Dairy Beverages

- Organic Alcoholic Beverages

- Organic Soft Drinks

- Others

Organic coffee and tea dominates with a market share of 31.4% of the total Australia organic beverages market in 2025.

Organic coffee and tea hold the leading position in Australia's organic beverages market, supported by the country's deeply entrenched café culture and a rapidly expanding base of health-conscious tea drinkers. Australian consumers are increasingly willing to pay a premium for organically certified coffee sourced without synthetic pesticides, valuing both the perceived health benefits and the ethical production credentials. Major roasters and specialty café chains have accelerated their integration of organic single-origin coffees, while herbal and botanical organic teas, including those formulated with indigenous lemon myrtle and eucalyptus, are growing in popularity across both retail and hospitality channels.

The hospitality industry's growing emphasis on organic and premium beverage offerings has been a key amplifier for this segment. High-end hotels, wellness retreats, and specialty café chains are increasingly featuring certified organic teas as premium menu additions that signal sustainability and quality. Additionally, social media health influencers have played a significant role; a 2024 Hoozu Trust in Influencer Marketing Report revealed that 59% of Australian consumers expressed trust in sponsored posts from celebrities, driving organic tea adoption among younger demographics.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Grocery Stores

- Pharmacies

- Online

- Others

Supermarkets and hypermarkets lead with a share of 47.8% of the total Australia organic beverages market in 2025.

In Australia, supermarkets and hypermarkets are the main distribution channels for organic beverages. They use large store networks, special sections for organic products, and thoughtful shelf placement to encourage customer interaction and experimentation. The existence of large retail chains across the country, which have aggressively increased their organic product assortments, including private-label organic beverage lines, to satisfy growing consumer demand for clean-label substitutes, is the foundation of this channel's supremacy. Organic beverage acceptance among mainstream customers looking for accessible and reasonably priced wellness-oriented options is encouraged by the ease of one-stop shopping, competitive pricing methods, and loyalty incentive programs.

With the addition of special health and wellness aisles, in-store promotional activities, and digital integration through click-and-collect and home delivery options, the supermarket chain is still developing its organic beverage merchandising strategy. Large stores are increasingly collaborating with organic beverage companies to create unique product lines and marketing initiatives that increase awareness of organic beverages among budget-conscious consumers. While expanding online grocery usage complements traditional in-store distribution, the growth of smaller-format convenience stores with a health-focused product assortment further expands the accessibility of organic beverages in metropolitan areas.

Regional Insights:

- Australia Capital Territory and New South Wales

- Victoria and Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory and New South Wales hold the largest share with 35.2% of the total Australia organic beverages market in 2025.

Due to the concentration of health-conscious urban consumers in Sydney and Canberra, their high levels of disposable income, and the abundance of upscale retail establishments and specialty health food stores, the Australia Capital Territory and New South Wales hold the top regional position in the country's organic beverage market. Sustained demand growth across organic beverage categories is further supported by the region's well-established cafe culture, which actively supports organic and plant-based beverage options. Furthermore, the existence of a well-educated and health-conscious population base increases customer readiness to spend money on high-end organic goods.

The existence of large retail headquarters and distribution facilities that give priority to organic product listings, guaranteeing widespread availability and promotional awareness for organic beverages, further solidifies the region's dominance. In addition to complementing conventional retail channels, the increasing use of online grocery platforms in urban areas has increased customer access to a wider variety of organic beverage options. The region's organic beverage consumption patterns are further strengthened by strong institutional demand from eateries, wellness centers, and hospitality organizations; additional distribution channels are provided by flourishing farmers markets and specialty organic merchants.

Market Dynamics:

Growth Drivers:

Why is the Australia Organic Beverages Market Growing?

Escalating Health Consciousness and Demand for Chemical-Free Beverages

Rising health awareness among Australian consumers represents a primary catalyst for organic beverages market expansion. Increasing prevalence of lifestyle-related conditions including obesity, diabetes, and cardiovascular diseases has prompted consumers to critically evaluate their dietary choices, driving a pronounced shift away from conventionally produced beverages containing synthetic additives, preservatives, and artificial flavoring compounds. The perception that organic beverages offer superior nutritional profiles and reduced exposure to harmful chemicals is particularly resonant among health-conscious demographics spanning millennials, young families, and wellness-focused individuals. This behavioral shift is reinforced by growing scientific evidence and media coverage highlighting the potential health risks of long-term consumption of synthetic ingredients in conventional beverages. Public health campaigns and widespread reporting on lifestyle-related health disorders have further heightened interest in nutrition-based consumption, strengthening the consumer imperative for healthier beverage alternatives including organic options that support holistic wellness goals across diverse age groups and dietary preferences.

Expanding Retail Infrastructure and Mainstreaming of Organic Beverages

The broadening distribution and increased shelf presence of organic beverages across retail and e-commerce platforms have been instrumental in scaling market growth in Australia. Major supermarket chains have integrated dedicated organic sections into their store layouts, normalizing organic beverage purchases within routine grocery shopping and enabling easier product discovery for mainstream consumers. The proliferation of specialty health food stores, organic-focused retailers, and farmers markets has further diversified the channels through which consumers access organic beverages. Simultaneously, the rapid expansion of digital grocery platforms has enabled manufacturers to reach consumers through subscription models, personalized recommendations, and convenient home delivery options. The continued technological innovation in retail channels, including advanced in-store navigation tools and AI-driven product recommendation systems, is enhancing the consumer shopping experience and supporting organic product discovery across distribution networks. These developments collectively lower barriers to entry for new organic beverage brands while strengthening accessibility for existing producers throughout the country.

Growing Environmental Awareness and Sustainability-Driven Consumer Preferences

Environmental sustainability has emerged as a significant driver of organic beverage adoption in Australia, as consumers increasingly align their purchasing decisions with ecological values. Organic farming practices, which minimize synthetic chemical usage, promote biodiversity, reduce soil degradation, and lower greenhouse gas emissions, resonate strongly with environmentally conscious Australian consumers. The growing awareness of the environmental impact of conventional agriculture, particularly concerning water consumption, land use, and chemical runoff, is motivating consumers to seek sustainably produced alternatives. Plant-based organic beverages, especially oat and almond milk, are increasingly perceived as more environmentally responsible options compared to conventional dairy. This sustainability orientation extends to packaging preferences, with consumers favoring brands that adopt recyclable, biodegradable, or plant-based packaging solutions. Australia's extensive certified organic farmland base, one of the largest globally, provides a strong agricultural foundation that supports the continued scaling of organic beverage production while reinforcing the country's position as a leader in sustainable farming practices.

Market Restraints:

What Challenges the Australia Organic Beverages Market is Facing?

Premium Pricing Barrier Limiting Mass-Market Adoption

Organic beverages typically command higher retail prices compared to conventional alternatives, reflecting the elevated costs associated with organic ingredient sourcing, certification compliance, and smaller-scale production processes. This pricing premium creates a significant barrier for price-sensitive consumers, particularly during periods of economic uncertainty and cost-of-living pressures affecting Australian households. While long-term health benefits are widely acknowledged, many consumers remain hesitant to consistently pay premium prices for organic beverages, limiting broader market penetration beyond affluent demographics and urban centers.

Absence of Mandatory Domestic Organic Regulation

Australia remains the only OECD country without a legislated domestic definition for organic products, creating significant regulatory ambiguity that undermines consumer trust and market integrity. Products can currently be labeled as organic with minimal certified organic content, enabling greenwashing practices that erode the credibility of genuinely certified organic beverage manufacturers. This regulatory gap limits consumer confidence in organic claims, creates an uneven competitive landscape between certified and uncertified producers, and restricts export market access for Australian organic beverage producers.

Supply Chain Fragility and Organic Ingredient Sourcing Constraints

Organic beverage manufacturers face persistent challenges related to supply chain vulnerabilities, including limited availability of certified organic raw materials, seasonal production variability, and climate-related disruptions affecting crop yields across agricultural regions. The reliance on smaller, decentralized supply chains that lack the infrastructure necessary for large-scale production expansion constrains the ability of organic beverage producers to maintain consistent product availability. These factors are particularly impactful for beverages dependent on fresh, seasonal organic ingredients.

Competitive Landscape:

The Australia organic beverages market features a dynamic competitive landscape characterized by the presence of both established domestic producers and emerging niche brands competing across diverse product categories. Companies are increasingly differentiating through product innovation, functional ingredient integration, and sustainability credentials to attract health-conscious consumers. Strategic investments in production capacity, retail partnerships, and brand marketing are intensifying as manufacturers seek to strengthen their positions. The competitive environment is further shaped by expanding private-label organic offerings from major retailers, e-commerce channel development, and the entry of international organic beverage brands, driving continuous innovation and product diversification across the market.

Some of the key players include:

- Byron Bay Coffee Company

- Montville Coffee

- Ovvio Organics

- Planet Organic

- República Organic

- Tea Gardens Kombucha

- Tea Tonic

Australia Organic Beverages Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Type Covered | Organic Coffee and Tea, Organic Non-Dairy Beverages, Organic Alcoholic Beverages, Organic Soft Drinks, Others |

| Distribution Channel Covered | Supermarkets and Hypermarkets, Grocery Stores, Pharmacies, Online, Others |

| Region Covered | Australia Capital Territory and New South Wales, Victoria and Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Byron Bay Coffee Company, Montville Coffee, Ovvio Organics, Planet Organic, República Organic, Tea Gardens Kombucha, Tea Tonic, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Organic Beverages Market Report

The Australia organic beverages market size was valued at USD 737.5 Million in 2025.

The Australia organic beverages market is expected to grow at a compound annual growth rate of 16.37% from 2026-2034 to reach USD 3,148.0 Million by 2034.

Organic coffee and tea dominated the market with a share of 31.4%, driven by Australia's strong café culture, rising demand for organic specialty blends, and growing interest in herbal and functional teas among health-conscious consumers seeking clean-label wellness beverages.

Key factors driving the Australia organic beverages market include escalating health consciousness, expanding retail distribution across supermarkets and e-commerce platforms, growing environmental awareness, rising demand for functional wellness beverages, and increasing adoption of plant-based dietary patterns.

Major challenges include premium pricing limiting mass-market adoption, absence of mandatory domestic organic certification regulation, supply chain fragility for organic ingredients, seasonal production variability, and consumer confusion stemming from unregulated organic labeling practices.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)