Australia Organic Food Market Size, Share, Trends and Forecast by Product Type, Distribution Channel, and Region, 2026-2034

Australia Organic Food Market Summary:

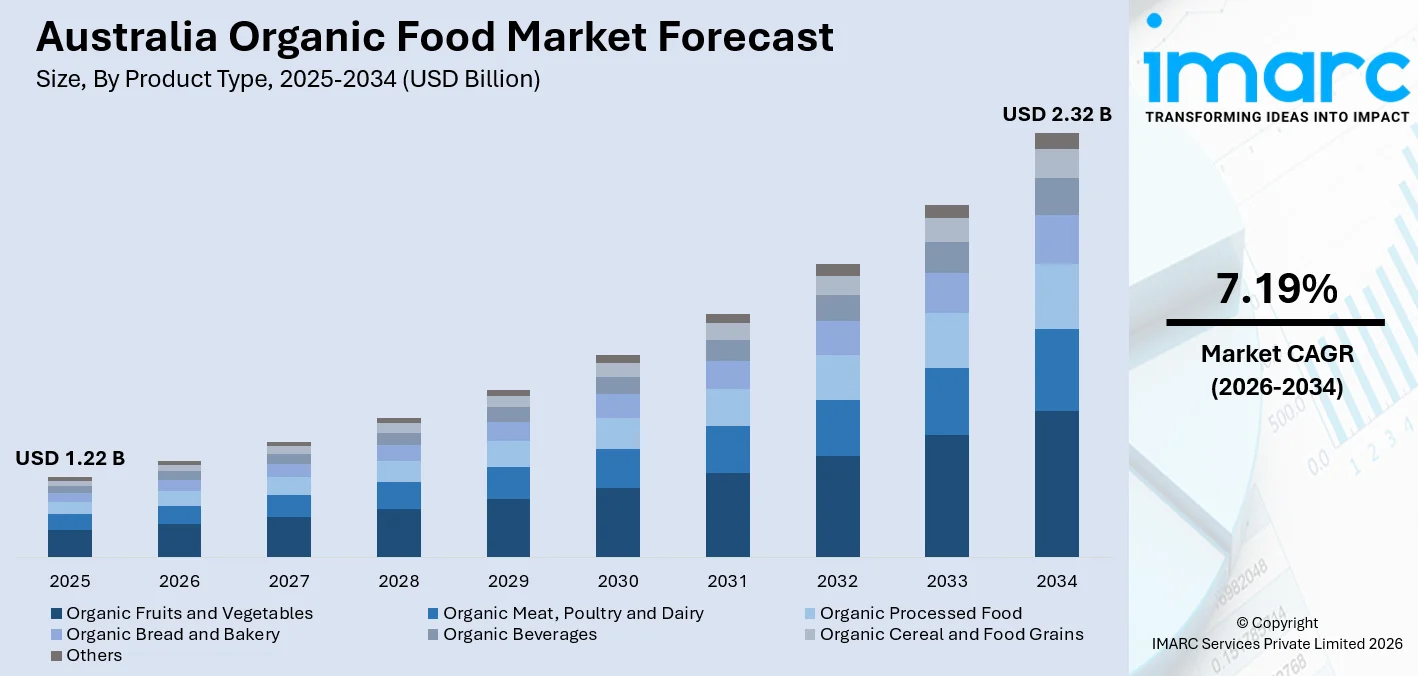

The Australia organic food market size was valued at USD 1.22 Billion in 2025 and is projected to reach USD 2.32 Billion by 2034, growing at a compound annual growth rate of 7.19% from 2026-2034.

The market is driven by the increasing awareness of consumers about the significance of chemical-free and nutritionally superior food products, as well as the overall shift in the culture of consumers towards responsible consumption. The increasing trend of consuming organic food by consumers of different ages, along with the availability of certified organic products, is further boosting the market share of the Australian organic food market.

Key Takeaways and Insights:

- By Product Type: Organic fruits and vegetables dominate the market with a share of 32.4% in 2025, driven by strong consumer preference for fresh, pesticide-free produce and its positioning as the most accessible entry point into organic eating.

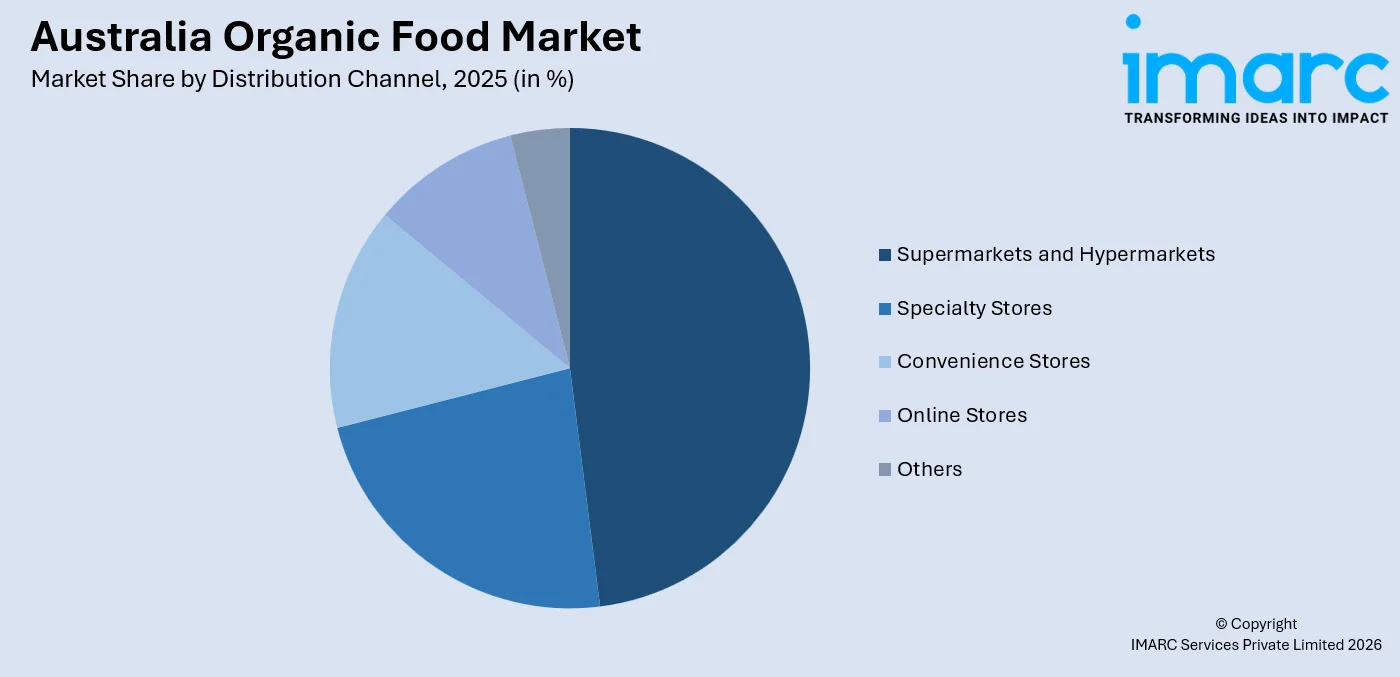

- By Distribution Channel: Supermarkets and hypermarkets lead the market with a share of 48.2% in 2025, owing to the extensive organic product range offered by mainstream retailers and widespread consumer familiarity with these shopping channels.

- By Region: Australia Capital Territory & New South Wales represents the largest region with a share of 34.5% in 2025, supported by a highly health-conscious urban population and a concentrated network of certified organic retailers and specialty outlets.

- Key Players: The Australia organic food market is moderately competitive, with participation from established domestic producers, certified organic brands, and major retail chains that collectively address evolving consumer preferences across quality, pricing, and sustainability.

To get more information on this market Request Sample

Australia’s organic food landscape is shaped by a convergence of health awareness, environmental responsibility, and demand for transparency in food production. Consumers increasingly prioritize food that is free from synthetic pesticides, herbicides, and genetically modified organisms, viewing organic choices as an investment in long-term personal wellbeing. The growing influence of lifestyle-driven dietary movements such as clean eating, plant-based nutrition, and mindful consumption has drawn a broader demographic into the organic segment. Reinforcing the importance of regulatory clarity, in November 2024 Australia introduced the National Organic Standard Bill 2024 to Parliament, aiming to establish a mandatory national certification standard for products labelled as organic and strengthen consumer protection against misleading claims. Mainstream retail integration has removed traditional barriers to access, allowing organic products to reach households across income levels and geographic locations. Regulatory efforts around certification labeling further underpin consumer trust, while Australia’s natural agricultural advantages continue to support diversified organic production. Together, these factors create a self-reinforcing cycle of demand that sustains the market’s steady forward trajectory.

Australia Organic Food Market Trends:

Rising Demand for Clean-Label and Minimally Processed Organic Products

Consumers across Australia are increasingly gravitating toward organic food products that carry clean-label credentials, specifically those with recognizable, minimal ingredients and no artificial additives or preservatives. This preference reflects a deeper awareness of processing methods and ingredient sourcing, with shoppers actively scrutinizing packaging for transparency markers. Reflecting this shift at the company level, Byron Bay-based organic chocolate brand Loco Love expanded its presence across more than 1,000 retail outlets in Australia by 2025 while introducing new product lines made with organic, fair-trade ingredients and natural sweeteners, highlighting rising demand for clean-label indulgence products. Organic options in categories such as snacks, cereals, and packaged goods are benefiting as buyers seek assurance that their food aligns with personal health and wellness values.

Expansion of Organic E-Commerce and Direct-to-Consumer Channels

Digital retail platforms are transforming how Australians access organic food, with online stores and subscription-based delivery services gaining substantial traction. This trend is particularly relevant for consumers in regional or semi-urban areas where physical specialty retail is limited. For instance, in August 2025, Australian startup VLOO reported that its vegan food-waste subscription box sold out within its first month of launch, highlighting strong consumer demand for online, subscription-based organic and sustainable food delivery models. The convenience of curated organic boxes, recurring deliveries, and personalized product discovery has unlocked new purchasing behaviors, enabling organic brands to build loyal customer relationships and progressively reduce dependence on traditional brick-and-mortar distribution networks.

Growing Integration of Organic Offerings in Foodservice and Hospitality

The organic food trend has extended beyond household consumption into the foodservice sector, as cafes, restaurants, and catering providers incorporate certified organic ingredients into their menus. This shift responds to growing diner expectations for ethically sourced, health-conscious meals, particularly among urban and millennial demographics. For instance, in 2024, The Sustainable Restaurant Association expanded its Food Made Good Standard into Australia, with restaurants such as Brae adopting rigorous sustainability and organic sourcing practices to differentiate themselves within the hospitality sector. Establishments that highlight organic sourcing are increasingly using it as a brand differentiator, fostering consumer trust and commanding premium pricing while reinforcing the broader visibility of organic food culture across Australia.

Market Outlook 2026-2034:

The organic food market in Australia is likely to exhibit robust growth over the upcoming forecast period, driven by underlying changes in consumer trends, retail models, and farming techniques. Increasing health awareness, rising environmental knowledge, and the need for certified products are likely to remain key factors that support the development of the organic food market across the country. Developments in organic farming infrastructure are also likely to support the development of the organic food market in the country over the upcoming forecast period. The market generated a revenue of USD 1.22 Billion in 2025 and is projected to reach a revenue of USD 2.32 Billion by 2034, growing at a compound annual growth rate of 7.19% from 2026-2034.

Australia Organic Food Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Product Type |

Organic Fruits and Vegetables |

32.4% |

|

Distribution Channel |

Supermarkets and Hypermarkets |

48.2% |

|

Region |

Australia Capital Territory & New South Wales |

34.5% |

Product Type Insights:

- Organic Fruits and Vegetables

- Organic Meat, Poultry and Dairy

- Organic Processed Food

- Organic Bread and Bakery

- Organic Beverages

- Organic Cereal and Food Grains

- Others

The organic fruits and vegetables dominates with a market share of 32.4% of the total Australia organic food market in 2025.

Organic fruits and vegetables are the most basic and widely accepted form of the organic food market in Australia. The reason is that consumers consider fresh fruits and vegetables the epitome of chemical-free, untainted, and pure nutrition, making them the most appropriate entry point for consumers looking to enter the market of organic foods. The category is well-supported across the market, with health-conscious households as the major drivers of demand for pesticide-free products suitable for day-to-day cooking and meal preparation.

The increased realization of the interrelation of pesticide exposure and health has also increased the requirement for organic fresh produce. Fruit and vegetable purchases are an everyday, high-frequency decision, and hence the segment where organic switching happens most naturally. The segment's high visibility in the mainstream retail space, its direct association with the concepts of nutrition and food safety, and its alignment with the concepts of seasonality and local sourcing continue to reinforce its position as the segment that generates the highest revenue and has the highest consumer recognition in the market.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Supermarkets and Hypermarkets

- Specialty Stores

- Convenience Stores

- Online Stores

- Others

The supermarkets and hypermarkets leads with a share of 48.2% of the total Australia organic food market in 2025.

Supermarkets and hypermarkets have emerged as the key access point for organic foods in Australia, using their existing store network, trust levels, and product variety to bring organic foods into the mainstream. These stores have strategically invested in expanding their product offerings of organic and natural foods by adding specific section space and premium private label brands to tap into the health-conscious shopper category. The ability of these stores to offer competitive prices through bulk purchase also adds to their ability to promote organic foods.

Apart from physical space, modern grocery stores such as supermarkets and hypermarkets have sought to improve the shopping experience for organic food buyers by incorporating digital media, loyalty programs, and certification signage. This diversification of marketing channels aligns with the values of modern consumers who desire convenience and assurance when purchasing organic food products. The dominance of this channel is further supported by the ability to carry all types of organic products, ranging from fresh food to packaged food, thus providing the most comprehensive shopping experience for organic buyers.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales exhibits a clear dominance with a 34.5% share of the total Australia organic food market in 2025.

New South Wales and the Australian Capital Territory collectively form the largest organic food region, driven by dense urban populations with above-average disposable incomes and high health literacy. Sydney's metropolitan area hosts a well-developed ecosystem of specialty organic retailers, farmers' markets, and health-focused foodservice establishments, creating both strong consumer demand and robust supply chain infrastructure. The ACT's policy-oriented demographic and proximity to certified organic farming regions further reinforce high per-capita organic spending throughout the combined territory.

The region also benefits from a mature certification and traceability ecosystem, with a high concentration of accredited organic producers and processors supporting consistent product quality and availability. Consumer awareness of organic labeling standards is particularly elevated among the region's educated and environmentally engaged population. The growing foodservice sector in Sydney and Canberra, including organic-focused cafes, premium restaurants, and institutional buyers, creates additional demand beyond household consumption, reinforcing the region's position as Australia's leading organic food market.

Market Dynamics:

Growth Drivers:

Why is the Australia Organic Food Market Growing?

Rising Consumer Health Consciousness and Preference for Chemical-Free Nutrition

The increasing prioritization of personal health and long-term dietary wellness among Australian consumers has fundamentally reshaped food purchasing behavior. As awareness of health implications associated with synthetic pesticides, artificial preservatives, and genetically modified organisms deepens, organic food is perceived as a safer and more nutritionally aligned alternative. Reflecting this shift, in January 2026, Australian Organic Limited was selected to participate in the Australian Government’s $50 million Trade Diversification Network initiative, aimed at expanding global demand for certified organic products and strengthening export capabilities. This perspective is particularly pronounced among families with young children and health-conscious adults. The organic segment benefits from a broad perception that its products contain higher levels of beneficial nutrients, antioxidants, and natural compounds.

Growing Environmental Awareness and Alignment with Sustainable Consumption

Environmental consciousness has emerged as a significant and increasingly influential force shaping organic food demand across Australia. Consumers are becoming progressively aware of the ecological impact of conventional agricultural practices, including soil degradation, water contamination through chemical runoff, and biodiversity loss. Organic farming methods that emphasize natural soil enrichment, crop rotation, and integrated pest management resonate deeply with environmentally motivated buyers. This shift is further reinforced by policy-level developments; for instance, in September 2025, the Australian government signed a Mutual Recognition Arrangement (MRA) on organic products with India, enabling certified organic goods to be traded more seamlessly and strengthening trust in organic standards across international markets. This alignment between organic purchasing and sustainable values is particularly prominent among urban demographics and younger consumer cohorts who prioritize environmental responsibility in everyday lifestyle decisions.

Retail Expansion and Mainstream Accessibility of Organic Products

The progressive mainstreaming of organic food through expanded retail availability has been one of the most transformative growth drivers in Australia. Major supermarket chains and hypermarkets have systematically increased the breadth of their organic product ranges, dedicating shelf space to certified items across all major food categories, substantially lowering the accessibility barrier that once confined organic purchasing to specialty health stores. This trend is further reinforced by corporate investment in organic supply chains; for example, Woolworths Group announced increased sourcing commitments toward sustainably and organically produced fresh food, alongside efforts to improve transparency and traceability across its supply network to meet rising consumer expectations for ethical and environmentally responsible products. The growth of online grocery platforms and organic food delivery services has further extended reach to time-pressed households and consumers in areas with limited physical retail options.

Market Restraints:

What Challenges the Australia Organic Food Market is Facing?

Premium Pricing and Affordability Constraints

Organic food consistently commands a significant price premium over conventionally produced alternatives, reflecting the higher labor intensity, extended growing cycles, and certification costs associated with organic farming. For many Australian households experiencing cost-of-living pressures, this pricing differential acts as a deterrent to frequent or comprehensive organic purchasing. While health-conscious consumers may willingly pay more for specific high-priority items, broader household adoption remains constrained when organic options are perceived as financially unsustainable as a complete dietary transition.

Limited Domestic Supply Capacity and Certification Barriers

Australia’s certified organic farming sector, while growing, faces structural limitations in scaling supply to match rising consumer demand. The transition from conventional to organic farming requires a multi-year certification process during which producers cannot command organic price premiums, creating a financial disincentive that slows the rate of new organic farm entrants. Geographic remoteness, water resource constraints, and limited access to organic farming expertise in rural areas further restrict the sector’s capacity to expand domestic production efficiently.

Fragmented Regulatory Framework and Consumer Confusion Around Labeling

Australia remains one of the few developed economies without a nationally legislated standard defining organic products, creating inconsistencies in how organic claims are made and verified across the market. This regulatory ambiguity can undermine consumer confidence, particularly for shoppers who encounter varying certification logos, terminology, and standards without clear guidance on their comparative integrity. The resulting label confusion reduces purchase decision confidence and may diminish the trust premium that underpins willingness to pay for certified organic products.

Competitive Landscape:

Australia’s organic food market is characterized by a moderately fragmented competitive structure, featuring a mix of large-scale national distributors, certified organic specialist brands, and regional producers catering to diverse consumer segments. Competitive dynamics are shaped by factors including certification credibility, supply chain transparency, retail partnerships, and the ability to deliver consistent product quality at accessible price points. Premium branding and authentic organic credentials serve as meaningful differentiation tools, particularly as mainstream retailers expand their own-label organic ranges that compete with established specialist brands. The growing prominence of e-commerce and direct-to-consumer models has enabled smaller, mission-driven organic producers to build national reach without relying solely on traditional retail intermediaries. In parallel, large-format supermarket chains continue to leverage their procurement scale and consumer touchpoints to consolidate category leadership. The competitive environment rewards organizations that can balance authenticity, affordability, and product innovation to meet the evolving expectations of Australia’s health-conscious consumer base.

Recent Developments:

- In February 2026, Australian organic chocolate company Loco Love reported strong growth, reaching about $12.8 million in revenue by 2025 and expanding its product range with new flavors and a maple-sweetened line.

Australia Organic Food Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Organic Fruits and Vegetables, Organic Meat, Poultry and Dairy, Organic Processed Food, Organic Bread and Bakery, Organic Beverages, Organic Cereal and Food Grains, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, Convenience Stores, Online Stores, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Organic Food Market Report

The Australia organic food market size was valued at USD 1.22 Billion in 2025.

The Australia organic food market is expected to grow at a compound annual growth rate of 7.19% from 2026-2034 to reach USD 2.32 Billion by 2034.

Organic fruits and vegetables dominated the product type segment with a share of 32.4%, driven by consistent consumer preference for fresh, pesticide-free produce and widespread availability across all major retail formats.

Key factors driving the Australia organic food market include rising health consciousness among consumers, growing environmental awareness and preference for sustainable farming practices, and the mainstream retail expansion of certified organic product ranges across all major food categories.

Major challenges include the premium pricing of organic products relative to conventional alternatives, limited domestic supply capacity and lengthy certification timelines for new organic farms, and the absence of a nationally legislated organic standard contributing to consumer confusion around labeling and certification.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)