Australia Over The Counter (OTC) Drugs Market Size, Share, Trends and Forecast by Product Type, Route of Administration, Dosage Form, Distribution Channel, and Region, 2026-2034

Australia Over The Counter (OTC) Drugs Market Overview:

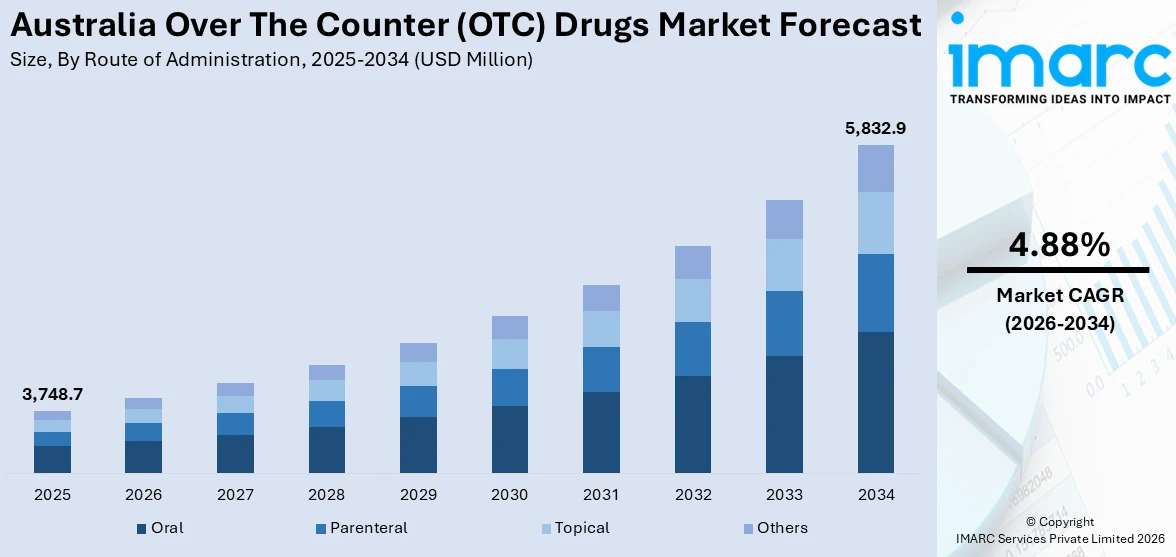

The Australia over the counter (OTC) drugs market size reached USD 3,748.7 Million in 2025. Looking forward, the market is expected to reach USD 5,832.9 Million by 2034, exhibiting a growth rate (CAGR) of 4.88% during 2026-2034. The market is growing steadily, supported by rising self-medication habits, wider product availability, and increasing demand for wellness solutions. Expansion of e-pharmacies and awareness around preventive care continue to influence buyer preferences across urban and rural regions.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 3,748.7 Million |

| Market Forecast in 2034 | USD 5,832.9 Million |

| Market Growth Rate 2026-2034 | 4.88% |

Key Trends of Australia Over the Counter (OTC) Drugs Market:

Rising Consumer Preference for Self-Care

The growing interest in self-care and minor ailment management is shaping demand for over-the-counter medications across Australia. Consumers increasingly rely on non-prescription treatments for everyday issues like colds, allergies, digestive concerns, and mild pain relief. This shift is partly influenced by time constraints and the desire to avoid clinic visits for manageable symptoms. An aging population and rising health awareness also play a role in encouraging people to manage recurring conditions without doctor supervision proactively. Pharmacists are becoming trusted first points of contact, often guiding choices of OTC products. Additionally, media exposure and digital health platforms are helping people make informed purchase decisions, increasing confidence in non-prescription options. A key factor contributing to over the counter (OTC) drugs market growth is the expansion of retail chains and pharmacies, which are diversifying their product ranges to include a mix of branded and generic OTC drugs. In 2023, leading pharmacy chains like Chemist Warehouse reported higher foot traffic driven by demand for cold and flu tablets, sleep aids, and vitamins. Market players are also investing in point-of-sale education to drive product awareness. These trends indicate that consumer autonomy in healthcare is becoming a major influence on the market’s direction.

To get more information on this market Request Sample

Digital Access and Product Availability

Digitalization and improved logistics are making OTC medications more accessible across Australian regions. E-commerce channels, including pharmacy apps and online drugstores, are growing rapidly, offering doorstep delivery and subscription-based purchase models. This ease of access supports the recurring use of OTC products for daily health concerns, particularly in remote or underserved areas. A wide range of categories, including skincare treatments, antacids, and anti-allergy drugs, are now readily available through both physical and digital shelves. Younger buyers are especially comfortable browsing and comparing product reviews online, adding momentum to digital sales. Towards the end of this trend, major players are optimizing supply chain routes and using AI tools for demand prediction. This has reduced stockouts and ensured the timely availability of seasonal medicines. For instance, in early 2024, several pharmacy chains introduced faster reordering systems in preparation for winter flu season, addressing previous gaps in cold relief product availability. The increase in shelf variety and consistent delivery timelines is reinforcing consumer trust, supporting steady market expansion. Based on these advancements, the over the counter (OTC) drugs market forecast suggests continued growth, with digital platforms and smart logistics playing a central role in shaping future distribution and consumer engagement strategies across Australia.

Growth Drivers of Australia Over the Counter (OTC) Drugs Market:

Increasing Incidence of Minor Ailments

Australia faces a continual rise in everyday health issues such as colds, mild allergies, digestive disturbances, and headaches, prompting consumers to opt for fast-acting OTC remedies rather than arranging doctor appointments. This self-care approach reduces healthcare expenses and offers quick relief, making OTC products the preferred first step for treating common conditions. The consistent need for effective, easily accessible solutions fuels steady market expansion across both urban and rural regions. Manufacturers are responding to this sustained demand by broadening their product portfolios, introducing innovative formulations, and enhancing availability to meet consumer expectations for convenience and reliability. As minor ailments remain prevalent, the role of OTC medicines as an immediate and cost-efficient treatment option continues to strengthen their market presence.

Expanding Retail and Pharmacy Networks

The Australia over the counter (OTC) drugs market growth benefits greatly from the extensive presence of pharmacies, supermarkets, and health-focused retail chains that make these products readily accessible. Strategic store locations in urban centers, suburban neighborhoods, and rural areas, combined with long operating hours, provide unmatched purchasing convenience. These broad distribution networks increase product visibility, allowing consumers to easily find and purchase OTC medications without delay. Enhanced retail penetration also encourages impulse buying and reinforces the availability of both traditional and specialized products. Consistent supply chains and strong relationships between manufacturers and retailers further support dependable product delivery, ensuring customers have timely access to trusted medications. According to the Australia over the counter (OTC) drugs market analysis, this robust and far-reaching retail infrastructure significantly contributes to the market’s consistent growth nationwide.

Growing Interest in Natural and Preventive Healthcare

Australian consumers are increasingly embracing natural and preventive healthcare solutions, favoring herbal remedies, vitamins, and nutritional supplements to maintain wellness and ward off illness. This growing preference for chemical-free and plant-based products aligns closely with rising health consciousness and eco-friendly lifestyles. Manufacturers and pharmaceutical companies are responding by introducing clean-label, sustainably sourced offerings that appeal to environmentally aware shoppers seeking holistic options. The trend supports innovation in product development, encouraging companies to diversify their OTC portfolios with alternative treatments and wellness-focused solutions. As more consumers prioritize preventive care and natural ingredients, the demand for these products strengthens, creating long-term opportunities for market expansion and establishing OTC medicines as essential components of proactive, health-oriented living across Australia.

Government Regulation of Australia Over the Counter (OTC) Drugs Market:

Stringent Safety and Quality Standards

Australia’s Therapeutic Goods Administration (TGA) upholds rigorous safety and quality benchmarks for all over-the-counter (OTC) medicines through extensive testing, clinical evaluations, and strict approval procedures. Every OTC product must demonstrate proven efficacy, accurate dosage, and consistent manufacturing practices before reaching consumers. These robust measures protect public health and prevent substandard or counterfeit products from entering the market. By demanding adherence to Good Manufacturing Practices (GMP), the TGA ensures manufacturers maintain superior production standards and regular quality audits. This regulatory discipline fosters consumer trust, reassures healthcare professionals, and creates a stable marketplace where only reliable, high-quality OTC medicines thrive. The result is a well-regulated environment that supports responsible growth and safeguards Australians who rely on accessible, effective self-care treatments, which is further fueling the Australia over the counter (OTC) drugs market share.

Clear Labeling and Consumer Education

Australian regulations require OTC medicines to feature comprehensive labeling that includes precise dosage instructions, active and inactive ingredient lists, expiration dates, and potential side effects. This transparent communication empowers consumers to make informed health decisions and minimizes the risk of misuse or accidental overdose. Clear guidance supports self-care by helping individuals treat common ailments confidently without professional supervision. Educational materials, such as patient information leaflets and online resources, further reinforce safe usage and encourage responsible purchasing habits. By mandating straightforward, easy-to-understand information, regulators strengthen public confidence in OTC products and reduce preventable health incidents. This commitment to consumer education promotes a culture of safe self-medication and reinforces the overall credibility of the Australia’s competitive OTC pharmaceutical market.

Controlled Advertising and Marketing Practices

The Australian government strictly regulates advertising for OTC medicines to ensure that all promotional content remains accurate, ethical, and evidence-based, which is further driving the Australia over the counter (OTC) drugs market demand. Marketing campaigns must avoid exaggerated claims or misleading statements, focusing instead on verified benefits and correct usage instructions. Regulatory agencies review advertisements across television, print, and digital platforms to maintain transparency and protect public health. These guidelines not only safeguard consumers from false or harmful information but also foster fair competition among pharmaceutical companies. By maintaining clear boundaries for endorsements, discounts, and comparative claims, regulators uphold industry integrity while allowing businesses to market responsibly. This balanced oversight supports market growth, builds consumer trust, and ensures that promotional activities complement the safe and effective use of OTC products throughout Australia.

Australia Over The Counter (OTC) Drugs Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional level for 2026-2034. Our report has categorized the market based on product type, route of administration, dosage form, and distribution channel.

Product Type Insights:

- Cough,Cold and Flu Products

- Analgesics

- Dermatology Products

- Gastrointestinal Products

- Vitamins,Minerals and Supplements (VMS)

- Weight-loss/Dietary Products

- Ophthalmic Products

- Sleeping Aids

- Others

The report has provided a detailed breakup and analysis of the market based on the product type. This includes cough, cold and flu products, analgesics, dermatology products, gastrointestinal products, vitamins, minerals and supplements (VMS), weight-loss/dietary products, ophthalmic products, sleeping aids, and others.

Route of Administration Insights:

- Oral

- Parenteral

- Topical

- Others

As per the over the counter (OTC) drugs market outlook, a detailed breakup and analysis of the market based on the route of administration have also been provided in the report. This includes oral, parenteral, topical, and others.

Dosage Form Insights:

- Tablets and Capsules

- Liquid

- Ointments

- Others

A detailed breakup and analysis of the market based on the dosage form have also been provided in the report. This includes tablets and capsules, liquid, ointments, and others.

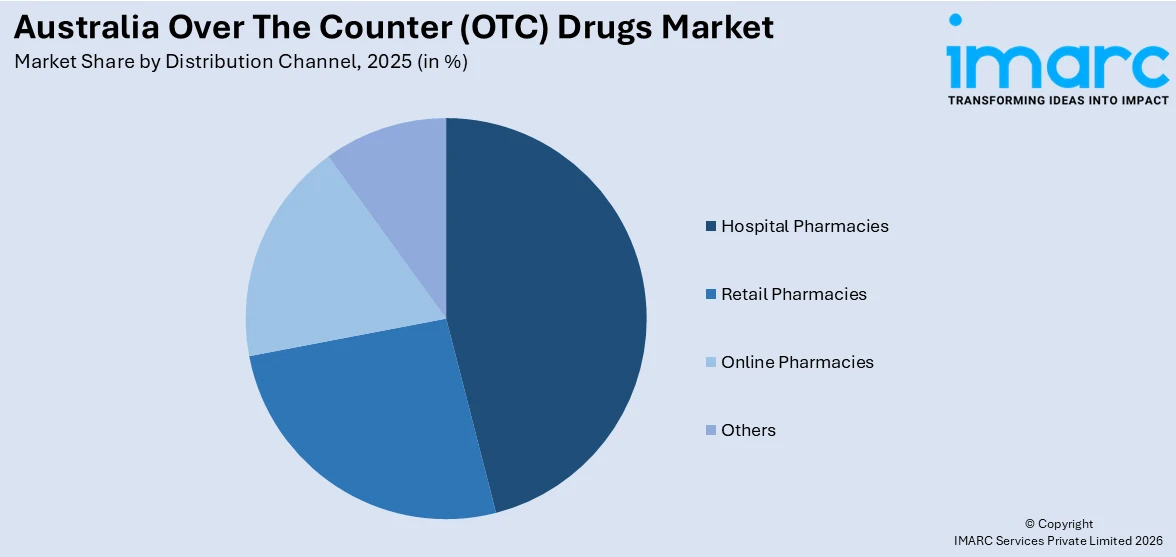

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Others

A detailed breakup and analysis of the market based on the distribution channel have also been provided in the report. This includes hospital pharmacies, retail pharmacies, online pharmacies, and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Over The Counter (OTC) Drugs Market News:

- March 2025: Avecho and Sandoz signed a ten-year deal to commercialize a CBD capsule for insomnia in Australia as an OTC product. This move marked progress toward TGA registration and expanded consumer access, strengthening the country’s emerging OTC cannabidiol market for sleep disorders.

- June 2024: Sigma’s proposed merger with Chemist Warehouse raised competition concerns in Australia’s OTC drugs market. The ACCC warned the merger could limit wholesale options, reduce retail competition, and affect product access, potentially raising prices and weakening service quality in pharmacy-sold OTC product segments.

Australia Over The Counter (OTC) Drugs Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Cough, Cold and Flu Products, Analgesics, Dermatology Products, Gastrointestinal Products, Vitamins, Minerals and Supplements (VMS), Weight-Loss/Dietary Products, Ophthalmic Products, Sleeping Aids, Others |

| Route of Administrations Covered | Oral, Parenteral, Topical, Others |

| Dosage Forms Covered | Tablets and Capsules, Liquids, Ointments, Others |

| Distribution Channels Covered | Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia over the counter (OTC) drugs market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia over the counter (OTC) drugs market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia over the counter (OTC) drugs industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Over The Counter (OTC) Drugs Market Report

The Australia over the counter (OTC) drugs market was valued at USD 3,748.7 Million in 2025.

The Australia over the counter (OTC) drugs market is projected to exhibit a CAGR of 4.88% during 2026-2034.

The Australia over the counter (OTC) drugs market is projected to reach a value of USD 5,832.9 Million by 2034.

The Australia OTC drugs market is shaped by rising self-medication, strong pharmacy channel growth, increased demand for natural and herbal products, digital health integration, aging population needs, deregulation expanding product accessibility, and consumers prioritizing wellness, convenience, and cost-effective treatment options.

Growth in Australia’s OTC drugs market is driven by rising healthcare costs pushing self-medication, wider pharmacy and retail penetration, government support for deregulation, increasing awareness about preventive care, demand for natural remedies, aging demographics with chronic conditions, and expanding e-commerce channels that enhance consumer access and product availability.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)