Australia Oxygen Concentrator Market Size, Share, Trends and Forecast by Type, Technology, Application, End User, and Region, 2026-2034

Australia Oxygen Concentrator Market Overview:

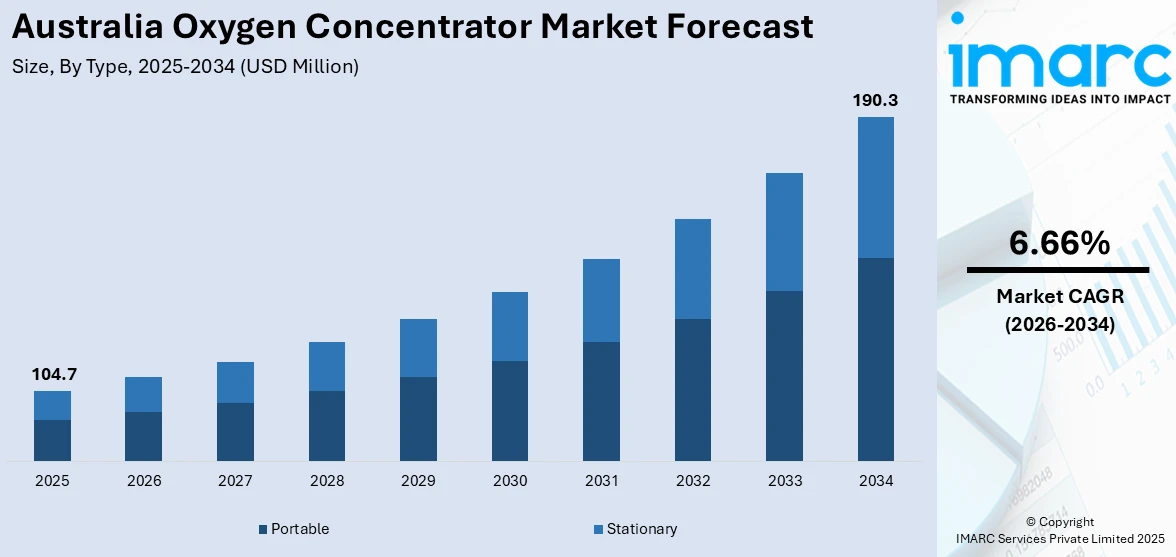

The Australia oxygen concentrator market size reached USD 104.7 Million in 2025. Looking forward, the market is expected to reach USD 190.3 Million by 2034, exhibiting a growth rate (CAGR) of 6.66% during 2026-2034. The market is witnessing significant growth due to the increasing prevalence of respiratory diseases, advancements in oxygen therapy technologies and growing awareness about the advantages of oxygen therapy at home care settings. Government initiatives, geriatric population opting for reliable oxygen therapy solutions and improved healthcare infrastructure are some other factors further increasing the Australia oxygen concentrator market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 104.7 Million |

| Market Forecast in 2034 | USD 190.3 Million |

| Market Growth Rate (2026-2034) | 6.66% |

Key Trends of Australia Oxygen Concentrator Market:

Increasing Prevalence of Respiratory Diseases

The rising prevalence of chronic respiratory diseases, particularly Chronic Obstructive Pulmonary Disease (COPD) and asthma, is a key factor driving the demand for oxygen concentrators in Australia. The AIHW's 2024 Burden of Disease Study reveals asthma's burden rose by 8.5% since 2003, ranking 8th highest overall. In 2023-2024, it accounted for 11.9% of the total disease burden in children 5-14, with 12.8% for males and 10.7% for females, highlighting urgent needs for improved management. These conditions, often worsened by factors such as smoking, pollution, and the aging process, require long-term management, such as oxygen therapy. With increasing numbers of cases of COPD and asthma, patients increasingly turn to oxygen concentrators to achieve ideal oxygen levels and improve their overall quality of life. Oxygen therapy is essential for patients suffering from serious respiratory diseases, as it controls the symptoms, curbs hospitalizations, and improves overall health conditions. With increased awareness about such ailments and advantages of oxygen therapy at home, more patients are preferring portable and stationary oxygen concentrators. This is playing a major role in spurring growth of the Australia oxygen concentrator market demand.

To get more information on this market, Request Sample

Rising Geriatric Population

Australia's aging population is a significant factor contributing to the growth of the oxygen concentrator market. According to the data published by the Centre for Population, by 2064–65, nearly 25% of the population will be aged 65 and over. The Government is implementing reforms to improve aged care and support Indigenous Australians, addressing disparities in life expectancy. As the proportion of elderly individuals increases, so does the prevalence of age-related respiratory conditions like COPD, emphysema, and other chronic illnesses, which often require long-term oxygen therapy. Oxygen concentrators are crucial for elderly patients, enabling them to manage their conditions at home, thereby reducing hospital visits and enhancing their quality of life. This demographic shift has led to an increased demand for portable and stationary oxygen concentrators, as elderly patients prefer home-based therapy for convenience and comfort. The government's healthcare initiatives and the rising availability of affordable oxygen concentrators are further driving the market's growth. As a result, the demand for oxygen concentrators continues to rise, significantly contributing to Australia oxygen concentrator market growth.

Growth Drivers of Australia Oxygen Concentrator Market:

Environmental Factors and Regional Vulnerabilities

One of the key drivers of growth in Australia's oxygen concentrator industry is Australia's exposure to environmental conditions that heighten respiratory health risks. Australia consistently faces occurrences like bushfires, dust storms, and high pollen seasons, especially within regions such as New South Wales, Victoria, and Western Australia regions, potentially causing adverse effects on air quality and worsening respiratory problems. These environmental risks have caused peaks in hospitalizations and have generated increased awareness about the necessity of at-home respiratory therapy. Portable oxygen concentrators become an important ally for patients with chronic respiratory illnesses and for susceptible populations suffering from brief exposure to poor air, like the elderly or those with underlying heart or lung diseases. Also, the isolation of much of Australia's communities means individuals could be far from access to hospital-based care when environmental conditions induce respiratory distress. Consequently, there is increasing demand for oxygen concentrators that can deliver stable, timely therapy in home and community environments where climate-related respiratory hazards are a constant presence.

Technological Advancements and Product Innovation

According to the Australia oxygen concentrator market analysis, another significant impetus is the fast pace of technological development in concentrator technology, which is reducing device size, energy consumption, noise levels, and handiness. Australian consumers are increasingly demanding convenient products like lightweight portable units with extended battery life, reduced noise, remote monitoring, and efficient continuous or pulse dose modes. To meet these demands, companies are utilizing newer membrane or zeolite materials, enhancing airflow quality, and integrating smart features enabling monitoring or alarms. These innovations reduce user barriers: to older users, to users with mobility constraints, and to remote area users who may experience constraints in power supply as well as device maintenance, better device design makes it easier to embrace concentrators. Additionally, concentrator design that meets Australia's regulatory and safety standards, yet still offers user friendliness, is attractive to healthcare providers and patients. Furthermore, equipment specially designed for home care is well suited to Australia's direction toward decentralized healthcare and ageing-in-place models, contributing to drive up market adoption.

Government Policy and Funding of Healthcare Toward Home Care

One of the key drivers of the market for oxygen concentrators in Australia is rising government and healthcare system support for home-based care supported by funding structures, subsidies or reimbursement policies that render home oxygen therapy more affordable. Since hospital beds and acute care are expensive, there is more incentive at both state and federal levels to decrease their burden through homecare options. Aged care, disability support service, and chronic disease management programs are increasingly adopting home oxygen solutions as a cost-saving means for enhancing quality of life. Improvements in healthcare infrastructure, regulatory clearance, safety standards, and quality control under agencies like the Therapeutic Goods Administration (TGA) also facilitate adoption by boosting consumer trust. In Australia, the governmental desire to provide better healthcare for remote and Indigenous populations also propels demand for home-usable oxygen devices, as these communities tend to have lesser access to large hospital facilities. As broader recognition on the part of clinicians and patients increases that home use of concentrators can decrease rehospitalization and enhance outcomes, payers and providers alike become more likely to cover or subsidize them, generating additional momentum for growth.

Australia Oxygen Concentrator Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on type, technology, application, and end user.

Type Insights:

- Portable

- Stationary

The report has provided a detailed breakup and analysis of the market based on the type. This includes portable and stationary.

Technology Insights:

- Continuous Flow

- Pulse Flow

A detailed breakup and analysis of the market based on the technology have also been provided in the report. This includes continuous flow and pulse flow.

Application Insights:

Access the comprehensive market breakdown Request Sample

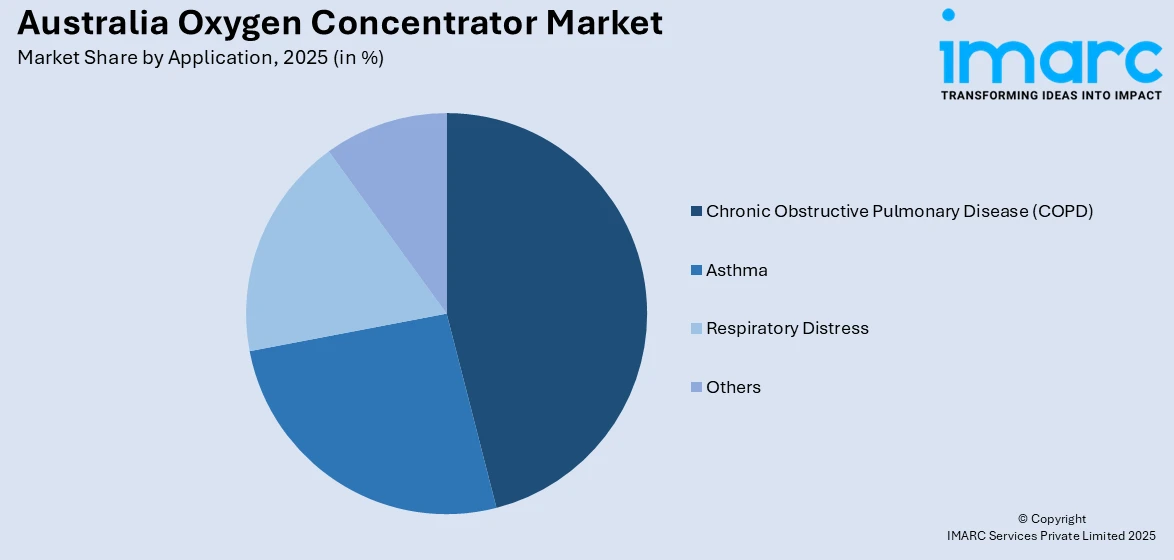

- Chronic Obstructive Pulmonary Disease (COPD)

- Asthma

- Respiratory Distress

- Others

A detailed breakup and analysis of the market based on the application have also been provided in the report. This includes chronic obstructive pulmonary disease (COPD), asthma, respiratory distress, and others.

End User Insights:

- Hospitals and Clinics

- Home Care Settings

- Ambulatory Surgical Centers and Physician Offices

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes hospitals and clinics, home care settings, and ambulatory surgical centers and physician offices.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Oxygen Concentrator Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered | Portable, Stationary |

| Technologies Covered | Continuous Flow, Pulse Flow |

| Applications Covered | Chronic Obstructive Pulmonary Disease (COPD), Asthma, Respiratory Distress, Others |

| End Users Covered | Hospitals and Clinics, Home Care Settings, Ambulatory Surgical Centers and Physician Offices |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia oxygen concentrator market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia oxygen concentrator market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia oxygen concentrator industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Oxygen Concentrator Market Report

The Australia oxygen concentrator market was valued at USD 104.7 Million in 2025.

The Australia oxygen concentrator market is projected to exhibit a CAGR of 6.66% during 2026-2034.

The Australia oxygen concentrator market is expected to reach a value of USD 190.3 Million by 2034.

Key trends in the Australia oxygen concentrator market include rising adoption of portable and user-friendly devices, integration of smart monitoring features, and a shift toward home-based respiratory care. Demand is growing in regional areas, driven by environmental factors and limited hospital access, while consumers increasingly seek discreet, travel-compatible oxygen solutions.

The Australia oxygen concentrator market is driven by increasing respiratory illnesses, frequent environmental hazards like bushfires, and the need for accessible care in remote regions. Advancements in portable device technology and strong government support for home-based healthcare also contribute to rising demand, especially among ageing and chronically ill populations.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)