Australia Plant-Based Meat Market Size, Share, Trends and Forecast by Product Type, Source, Meat Type, Distribution Channel, and Region, 2026-2034

Australia Plant-Based Meat Market Size and Share:

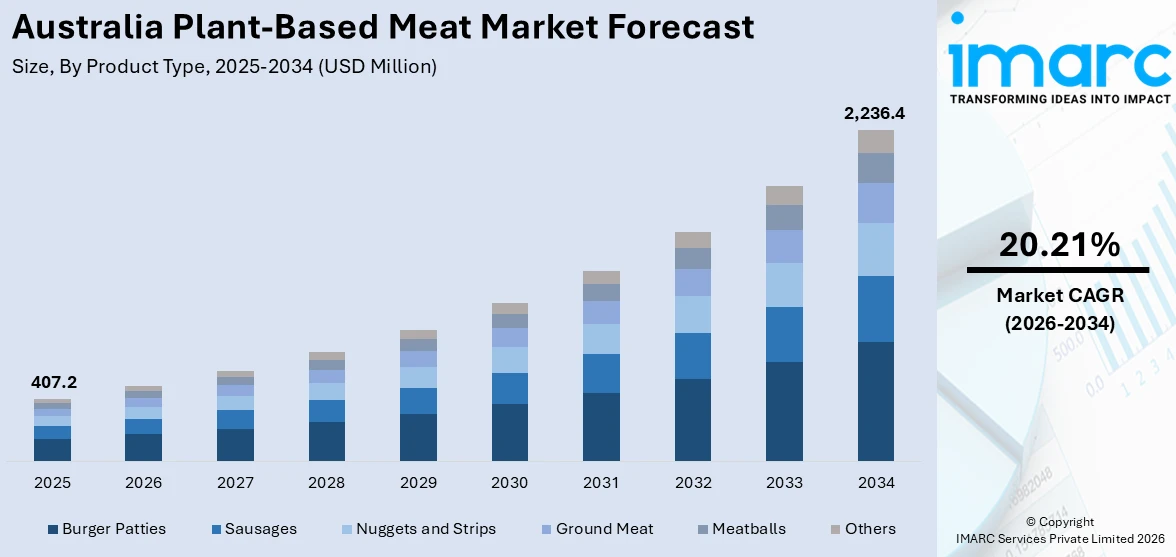

The Australia plant-based meat market size reached USD 407.2 Million in 2025. Looking forward, the market is expected to reach USD 2,236.4 Million by 2034, exhibiting a growth rate (CAGR) of 20.21% during 2026-2034. The growing health consciousness, increasing vegan and flexitarian populations, rising environmental concerns, continual advancements in food technology, expanding product availability, strong retail and foodservice adoption, implementation of supportive government initiatives, and shifting consumer preferences toward sustainable protein sources are some of the major factors augmenting Australia plant-based meat market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 407.2 Million |

| Market Forecast in 2034 | USD 2,236.4 Million |

| Market Growth Rate 2026-2034 | 20.21% |

Key Trends of Australia Plant-Based Meat Market:

Rising Consumer Demand for Health and Sustainability

The market is witnessing a rise in consumer demand driven by health consciousness and environmental concerns. Consumers in Australia are increasingly seeking healthier alternatives to traditional meat due to concerns over saturated fats, cholesterol, and the link between excessive red meat consumption and various health risks, including cardiovascular diseases and certain cancers. Industry reports highlight that one in six Australians are living with cardiovascular disease (CVD), affecting over 4.5 million people and accounting for nearly 18% of the population. As health awareness grows, many are turning to plant-based meat products as a nutritious alternative. These products, often fortified with essential nutrients like protein, iron, and vitamin B12, cater to health-conscious individuals looking for balanced diets without compromising nutritional value. This shift is propelling significant Australia plant-based meat market growth as consumers prioritize both personal well-being and sustainable food choices. In addition to this, environmental sustainability is another key factor supporting market expansion. The livestock industry significantly contributes to greenhouse gas emissions, water consumption, and deforestation. As climate awareness grows, more Australians are opting for plant-based alternatives to reduce their carbon footprint. Additionally, the demand for locally sourced, sustainable, and organic plant-based meat options is particularly strong, with consumers favoring brands that emphasize ethical sourcing and minimal environmental impact.

To get more information on this market Request Sample

Retail and Foodservice Sector Growth and Accessibility

The availability of plant-based meat in supermarkets, restaurants, and fast-food chains is expanding significantly, which is increasing the sales of plant-based meat and contributing to the market growth. According to an industry report, sales of plant-based meat increased by a remarkable 47% between 2020 and 2023 in Australia, reaching USD 272.5 Million in 2023. Major Australian retailers are increasing their plant-based meat offerings, dedicating more shelf space to these products. Moreover, private-label plant-based meat brands are also emerging, thereby making alternatives more affordable and accessible to a broader demographic. Supermarkets are strategically placing plant-based meats alongside traditional meat products rather than in separate vegan sections to encourage trial purchases from mainstream consumers, which is positively impacting the Australia plant-based meat market outlook. Apart from this, the food service industry is also capitalizing on the trend. Fast-food chains are introducing plant-based options, catering to the rising flexitarian and vegan populations. Furthermore, fine dining restaurants are incorporating gourmet plant-based meat dishes, appealing to sustainability-conscious consumers. The shift towards plant-based menus in public institutions, such as schools and hospitals, further demonstrates growing acceptance. Besides this, continual advancements in supply chain logistics have improved distribution efficiency, ensuring that plant-based meats remain competitively priced and widely available, further driving the Australia plant-based meat market demand.

Growth Factors of Australia Plant-Based Meat Market:

Climate-Driven Pressures and Eco-Friendly Shifts

One of the most powerful drivers of growth in Australia's plant-based meat sector is the heightened public consciousness of the environmental cost involved in conventional livestock production. Australians are increasingly aware of the connections between meat production and land degradation, methane release, and water consumption, especially as the country sees more severe droughts, bushfires, and volatile weather conditions. These pressures are not theoretical; they are lived experiences, particularly among rural communities who witness firsthand the pressure on Australia's ecosystems. Consumers are thus looking for food options that have a lower contribution to environmental strain, and plant-based meat alternatives present an attractive solution. This change is backed by mass environmental activism, increased integration of sustainability in school curricula, and significant media attention to Australia's exceptional climate issues. By framing plant-based meats as a direct response to environmental issues, businesses capitalize on an expanding market of environmentally oriented consumers intent on making a real impact through their daily diets.

Culinary Innovation Rooted in Aboriginal Australian Flavors

According to the Australia plant‑based meat market analysis, the industry is uniquely enhanced through culinary innovation based on indigenous ingredients that best represent the region’s rich natural diversity. Food manufacturers and chefs are now combining traditional Australian botanicals such as wattle seed, bush tomato, lemon myrtle, and macadamia to produce plant-based meat with unmistakable regional taste. Whether it is a burger patty flavored with indigenous spice profiles or a sausage substitute that achieves depth of savory through bush herbs, these products strike a chord with Australian consumers wanting something both comforting and new. This is hence an action that connects with national pride, honoring a relationship with the earth and indigenous cuisine expertise. This also distinguishes Australian plant‑based meat from others in the international market, giving them authenticity and geographic significance. Locally produced ingredients facilitate product character while also helping regional farmers, such as those in far-flung parts of Western Australia, the Outback, and Tasmania, which are regions where diversification of agriculture into native crops is creating new opportunities and anchoring plant-based meat products into place-based food stories.

Retail Accessibility and Strategic Partnerships across Supply Chains

Another significant growth driver for Australia's plant‑based meat industry is the manner in which accessibility and strategic collaboration are evolving through distribution channels and the food system more broadly. Large supermarket retailers and specialty food stores are increasing their offerings of plant‑based meat, making it readily accessible to homes across Australia's capital cities and rural towns. Parallel to this, local farmers and processing hubs along regional corridors like Riverina, Gippsland, and Queensland, are aligning with food startups to provide plant-based protein ingredients like pulses, native seeds, and legumes. These arrangements provide a reliable, locally based supply chain that supports product consistency as well as cost effectiveness. In addition, partnerships between food-tech entrepreneurs and education or agricultural research institutions are facilitating innovation of new plant-based meat products tuned to Australian flavor preferences and texture requirements. Through drawing on expertise in culinary, agricultural, and scientific fields, and anchoring production within local economies, Australia is establishing a robust network for supporting scale-up of plant‑based meat. This ecosystem enhances both market penetration and economic inclusion, catalyzing momentum for further growth in the domestic market and opening the way for export opportunities imbued with Australian identity.

Opportunities of Australia Plant-Based Meat Market:

Exclusive Native Ingredients and Indigenous Cooperation

Australia has an extraordinary diversity of indigenous botanicals that provide a compelling opportunity for plant-based meat innovation strongly linked to local culture. There are special ingredients like wattle seed, bush tomato, lemon myrtle, quandong, and macadamia that can be infused into plant-based meat substitutes to produce unmistakably Australian taste profiles. These indigenous flavors are thrilling for culinary explorers in urban centers such as Melbourne and Sydney while also appealing to rural foodies interested in honoring their respective terroir. Working alongside Indigenous people provides avenues for culturally sensitive sourcing and co-creation, allowing producers to develop authenticity-led products that respect traditional ecological knowledge. This strategy unlocks storytelling avenues that rise products from commodity goods to statements of place and heritage. Tourist destinations like the Byron Bay country, Tasmania's wilderness areas, or the remote Outback also offer platforms for displaying products celebrating indigenous flora, highlighting them through food experiences, food trails, and local markets. Such regionally rooted products can have the ability to get noticed in national retail channels and capture export markets searching for genuine, origin-rich plant-based developments.

Regional Supply Chains and Agricultural Diversification

The variety of Australia's geography offers a rich soil for agricultural diversification, with a robust support system for the plant-based meat industry. Much regional farm country that has traditionally specialized in cereal grains or conventional livestock can draw on production of pulses, legumes, and native grains appropriate for plant-based protein. Areas such as the Riverina, Gippsland, and western Queensland, with their strong farm infrastructure, are best positioned to diversify into lentils, chickpeas, lupins, and specialty native crops well suited to plant-based formulation. This reorientation towards agriculture can support rural community economic resilience and cut the link to traditional commodity cycles. In addition, local processing and packing hubs customized for such crops can increase supply reliability, minimize logistic gaps, and facilitate the freshness and traceability of plant-based meat ingredients. To consumers in regional Australia, where access to specialty food products is usually limited, localized production can enhance access and affordability, fostering increased acceptance. Collaborations amongst agritech clusters, universities, and startups reinforce innovation even more, enabling farmers to engage in a burgeoning industry and entwining rural economies in the developing plant-based foodscape.

Culinary Tourism and Regional Branding Potential

Australia's fertile landscapes and successful food tourism create strong channels to drive plant-based meat consumption via regional marketing and experiential food culture. Some of these regions, like Margaret River, the Fleurieu Peninsula, and the Daintree hinterland, already benefit from being gourmet destinations because of their local produce and food trails. Incorporating plant-based meat alternatives, such as wattle seed-infused sausage workshops, or pop-up dinners at local vineyards, can integrate such options into the regional culinary narrative, appealing to wellness-conscious tourists looking for ethical and sustainable dining. Plant-based options in farmer's markets, seafood festivals along the coast, and ALP-inspired beachside cafés leverage consumer curiosity, becoming brand ambassadors converting visitors into advocates beyond the local region. This approach can span the distance between novelty and conventional consumption and make plant-based meat familiar yet intriguing. When local producers and tourism operators co-promote these plant-based products, they promote trust and raise visibility in both physical stores and online platforms. Ultimately, culinary tourism becomes an effective lever for consumer trial, and for creating sustained demand while ingraining plant-based meats into Australia's rich gastronomic heritage.

Challenges of Australia Plant-Based Meat Market:

Climatic Extremes Stressing Ingredient Supply

Australia's plant‑based meat industry struggles with substantial issues that are based on the country's climate variability and environmental uncertainty. Places like New South Wales' Riverina or Western Australia's Wheatbelt, which are regions crucial to growing pulses and legumes key to plant‑based manufacturing, are oftentimes plagued by long‑duration droughts, variable rainfall patterns, and heatwaves. These become threats to crop viability, drive up costs, and deteriorate the quality and production of raw materials. Farmers in rural areas are not able to seasonally plan, hence destabilizing supply chains for plant‑based meat manufacturers. Bushfires also present a twofold threat: they not only destroy farms and interrupt transport routes but also contaminate air quality and soil that impinges on plant growth for years to come. The threats are especially severe for smaller growers who do not have the financial means of quickly bouncing back from shocks in the environment. In response to this, the sector needs to invest in robust supply structures like acquiring from many microclimates or incorporating indigenous drought-resistance crops, which requires time and calls for strategic planning through regions previously concentrating on conventional agriculture more than plant-based innovation.

Cultural Tastes and Meat-Focused Conventions

In Australia, strong cultural ties to meat culture and barbeque foods are a significant barrier to adopting plant‑based meat. At backyard barbeques to national celebrations, meals involving beef, lamb, or seafood are intertwined with community and identity symbols, particularly in rural and regional towns throughout Queensland, Tasmania, and South Australia. Meat continues to be at the core of daily meals and communal feast days for many families, making it challenging for alternatives to penetrate the mainstream without sacrificing valuable associations. Some consumers have a perception that plant-based meats can't match the robust textures, rich depths, or comforting familiarity of their animal-based counterparts. This tension represents a challenge for producers, who have to create plant-based alternatives with the power to deliver rich flavor and mouthfeel while having a distinctly Australian gastronomic hue. Transcending embedded habits entails not just product innovation but reframing culture, through domesticated marketing, tastings at public events, and partnerships with respected local chefs, to reframe attitudes without derogating nostalgic ties to conventional meals.

Complexity of Labeling and Regulatory Ambiguity

Navigating regulatory landscapes and product labeling presents another complex hurdle for Australia’s plant‑based meat industry. Without nationally harmonized definitions or guidelines for naming conventions such as using terms like “sausage,” “mince,” or “nugget”, companies face potential confusion among consumers and risk legal scrutiny. Local producers in regions with culinary identity, like South Australia's Barossa, and Victoria's Yarra Valley, will often rely heavily on locally branded names to differentiate their products; however, without well-defined rules, their communications can be confusing or misunderstood. This confusion makes marketing and packaging more difficult while it also hinders investment, as manufacturers might wait before bringing new products to market until the regulatory framework stabilizes. Smaller businesses and start-ups may not have legal or compliance infrastructure to adjust quickly, especially when entering into retail chains or exporting. Inconsistent state-by-state enforcement or changing tide of regulation can further add costs and impede growth. Stability and clarity in labeling regulations will be critical for the plant-based meat market to thrive throughout Australia, to ensure consumer confidence, allow for true differentiation, and foster ongoing innovation.

Australia Plant-Based Meat Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country level for 2026-2034. Our report has categorized the market based on product type, source, meat type, and distribution channel.

Product Type Insights:

- Burger Patties

- Sausages

- Nuggets and Strips

- Ground Meat

- Meatballs

- Others

The report has provided a detailed breakup and analysis of the market based on the product type. This includes burger patties, sausages, nuggets and strips, ground meat, meatballs, and others.

Source Insights:

- Soy

- Wheat

- Peas

- Others

A detailed breakup and analysis of the market based on the source have also been provided in the report. This includes soy, wheat, peas, and others.

Meat Type Insights:

- Chicken

- Beef

- Pork

- Others

The report has provided a detailed breakup and analysis of the market based on the meat type. This includes chicken, beef, pork, and others.

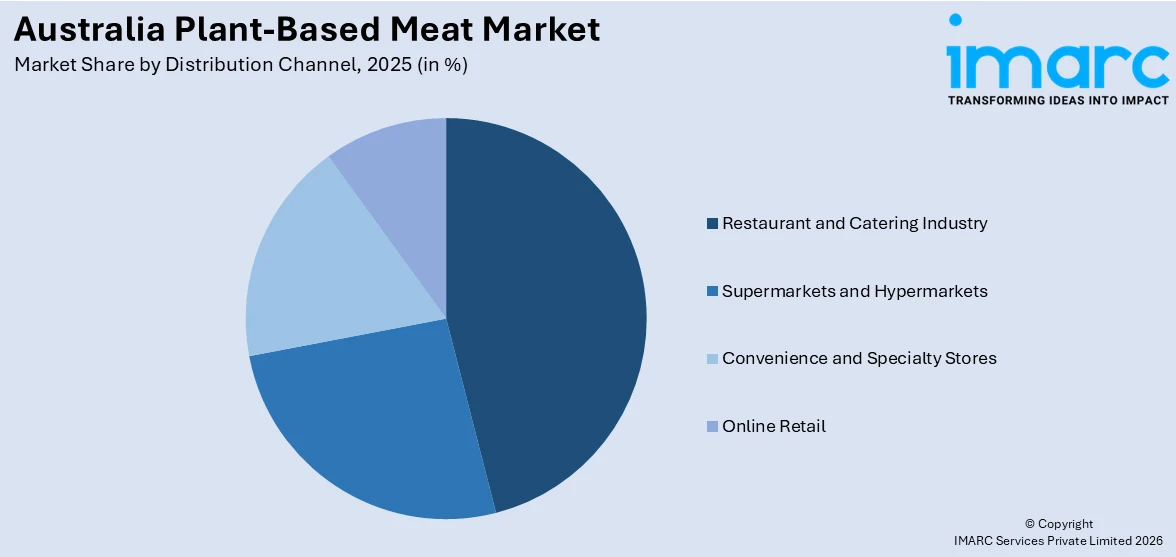

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Restaurant and Catering Industry

- Supermarkets and Hypermarkets

- Convenience and Specialty Stores

- Online Retail

A detailed breakup and analysis of the market based on the distribution channel have also been provided in the report. This includes restaurant and catering industry, supermarkets and hypermarkets, convenience and specialty stores, and online retail.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Plant-Based Meat Market News:

- On July 31, 2024, Australian plant-based meat brand Plantein announced the launch of its new product line in Woolworths supermarkets, featuring burgers, mince, and meatballs, each priced at USD 2.95. This initiative aims to provide consumers with affordable, nutritious alternatives to conventional meat, addressing rising living costs. The products are enriched with B vitamins, iron, fiber, and zinc, and are packaged in recyclable materials.

- On September 24, 2024, vEEF, an Australian plant-based meat business, unveiled four carbon-neutral products, including plant based beef mince, plant based classic sausages, plant based smokey sausages, and plant based chorizo sausages. The products are priced at or below animal-based equivalents. This strategic move aims to address the increasing consumer demand for sustainable and affordable meat alternatives.

Australia Plant-Based Meat Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Burger Patties, Sausages, Nuggets and Strips, Ground Meat, Meatballs, Others |

| Sources Covered | Soy, Wheat, Peas, Others |

| Meat Types Covered | Chicken, Beef, Pork, Others |

| Distribution Channels Covered | Restaurant and Catering Industry, Supermarkets and Hypermarkets, Convenience and Specialty Stores, Online Retail |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia plant-based meat market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia plant-based meat market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia plant-based meat industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Plant-Based Meat Market Report

The Australia plant-based meat market was valued at USD 407.2 Million in 2025.

The Australia plant-based meat market is projected to exhibit a CAGR of 20.21% during 2026-2034

The Australia plant-based meat market is expected to reach a value of USD 2,236.4 Million by 2034.

The Australia plant-based meat market trends include rising demand for products featuring native ingredients like wattle seed and bush tomato, increased availability in supermarkets and restaurants, and a focus on clean-label, minimally processed options. Consumers favor plant-based meats that offer familiar textures and flavors with sustainable, locally sourced ingredients, which further facilitate growth of the market.

The Australia plant-based meat market is driven by growing environmental awareness, increasing health consciousness, and demand for ethical food choices. Urban consumers and younger demographics are adopting flexitarian diets, while innovations using native ingredients and expanding retail availability make plant-based meats more accessible and appealing across diverse Australian regions.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)