Australia Plastics and Rubber Market Report by Type (Rubber Products, Plastic Products), End-User (Automotive and Transportation, Electrical and Electronics, Medical Construction, and Others), and Region 2026-2034

Australia Plastics and Rubber Market Overview:

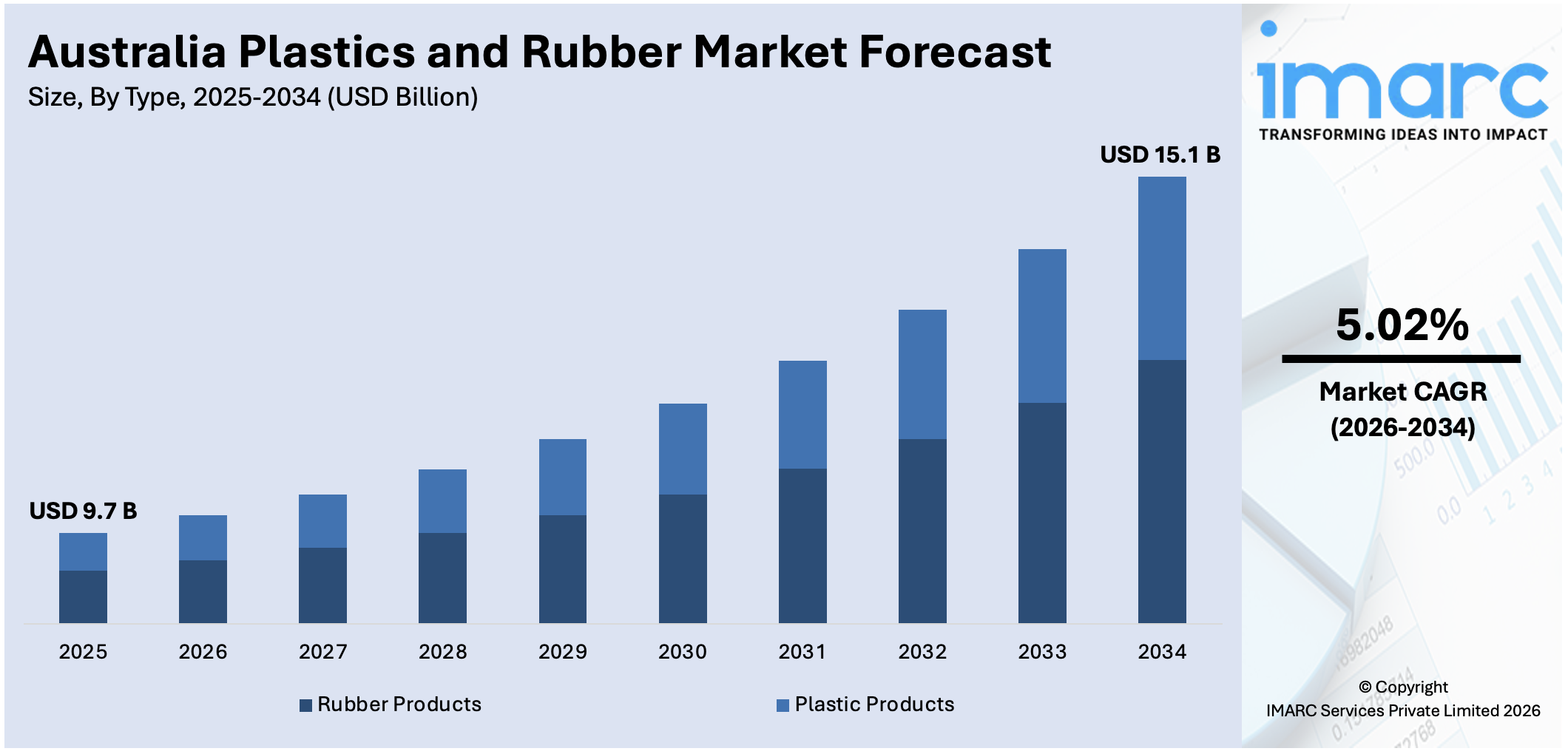

The Australia plastics and rubber market size reached USD 9.7 Billion in 2025. Looking forward, the market is expected to reach USD 15.1 Billion by 2034, exhibiting a growth rate (CAGR) of 5.02% during 2026-2034. The growing demand from key sectors such as automotive, packaging, and construction, improvements in polymer technology, rapid urbanization, the trend for greener materials, and increasing demand from end-use industries that require lightweight, durable, and eco-friendly materials are key factors bolstering the market growth.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 9.7 Billion |

| Market Forecast in 2034 | USD 15.1 Billion |

| Market Growth Rate 2026-2034 | 5.02% |

Key Trends of Australia Plastics and Rubber Market:

Increasing demand in the automotive sector

One of the major trends is the growing demand for plastics and rubber in the automotive industry. These materials are being used to reduce vehicle weight, which in turn improves fuel efficiency and lowers emissions. Plastics are extensively used in the manufacturing of automotive components such as dashboards, bumpers, and fuel systems, replacing heavier materials like metal. Rubber is used in tires, seals, gaskets, and hoses, essential for vehicle performance and durability. The demand for electric vehicles (EVs) has also driven the need for lightweight materials, such as the use of advanced plastics, which further boosts battery efficiency and the overall range of the vehicle. As a result, the demand for specialized, durable plastic and rubber products in the automotive industry is rising, as the industry continues to grow and evolve, thus contributing to the Australia plastics and rubber market growth.

To get more information on this market Request Sample

Rising focus on sustainable and eco-friendly materials

Another key trend is the increasing focus on sustainability and eco-friendly materials. With growing environmental concerns and stringent regulations aimed at reducing carbon footprints and waste, the market has seen a surge in demand for bioplastics and recycled materials. Consumers and industries alike are leaning toward eco-conscious solutions, driving the development and adoption of biodegradable plastics and rubber alternatives. The trend of phasing out traditional plastics that are non-recyclable in the packaging and construction sectors has been very strong, resulting in the use of materials that can either be recycled or degraded without causing harm to the environment. Besides this, numerous manufacturers have integrated recycling activities into their value chains, further giving credence to this growth in sustainability within the Australian plastics and rubber industry and aiding in Australia plastics and rubber market demand.

Advancements in polymer technology

Advancements in polymer technology also play a critical role in shaping the Australian plastics and rubber market. Innovations in materials science have led to the development of high-performance polymers that offer superior durability, flexibility, and heat resistance. These advanced polymers are being increasingly adopted across various industries, including construction, electronics, and healthcare, for applications that require materials capable of withstanding extreme conditions. The development of thermoplastic elastomers (TPEs), which combine the elasticity of rubber with the recyclability of plastics, is a notable innovation that has gained traction in the market. These advancements are driving product innovation and expanding the potential applications for plastics and rubber in the Australian market.

Growth Drivers of Australia Plastics and Rubber Market:

Rapid Infrastructure Development and Urbanization

Australia’s growing infrastructure and urban development efforts are fueling strong demand for plastics and rubber products across the construction sector. The government’s continued focus on large-scale development projects has increased the need for polymer-based materials such as pipes, fittings, insulation, and other essential components. Rapid urbanization in major cities like Sydney and Melbourne further accelerates the use of plastic products in both residential and commercial buildings. Additionally, national initiatives aimed at strengthening domestic manufacturing are supporting local production of construction-grade plastics and rubber, reducing reliance on imports and enhancing the overall resilience of the country’s supply chain.

Expansion of Electric Vehicle Manufacturing and Components

The accelerating transition toward electric vehicles in Australia is driving specialized demand for advanced plastics and rubber components optimized for EV applications, further fueling the Australia plastics and rubber market share. Electric vehicles require lightweight, high-performance materials to maximize battery efficiency and extend driving range, creating opportunities for polymer manufacturers to develop innovative solutions. Specialized rubber compounds for EV tires, plastic components for battery housings, and lightweight interior materials are experiencing increasing adoption. Government incentives for electric vehicle adoption, combined with major automakers' commitments to electrification, are establishing long-term growth trajectories for plastics and rubber suppliers serving the automotive sector. This transformation represents a strategic opportunity for manufacturers to develop high-value, specialized products that command premium pricing.

Growing Packaging Industry and E-commerce Growth

Australia's expanding packaging sector, fueled by robust e-commerce growth and evolving consumer preferences, continues to drive substantial demand for plastic materials. The packaging segment dominates engineering plastics applications, with increasing requirements for protective packaging, food-grade containers, and sustainable packaging solutions. E-commerce delivery requirements have accelerated demand for durable, lightweight packaging materials that protect products during transportation while minimizing shipping costs. Consumer preference shifts toward convenience packaging, portion-controlled products, and ready-to-eat meals further support packaging plastics consumption. Simultaneously, the packaging industry's commitment to achieving 70% recycling or composting of plastic packaging by 2025 under the Australian Packaging Covenant is driving innovation in recyclable and compostable plastic materials, creating opportunities for manufacturers developing sustainable packaging solutions.

Opportunities of Australia Plastics and Rubber Market:

Advanced Recycling Technologies and Circular Economy Development

The emergence of advanced recycling technologies, particularly chemical recycling and enzymatic processes, presents significant market opportunities for plastics and rubber manufacturers. Companies investing in breakthrough technologies like Samsara Eco's enzymatic recycling platform and various chemical recycling facilities are positioning themselves to capture value from the growing circular economy. These technologies enable processing of previously non-recyclable plastics, including multi-layered packaging and contaminated materials, converting them into virgin-quality raw materials. Government funding through initiatives like the Recycling Modernization Fund provides financial support for facility development, reducing investment risks. Manufacturers that establish capabilities in producing high-quality recycled materials can access premium markets, meet corporate sustainability commitments, and benefit from increasing regulatory requirements for recycled content in packaging and products.

Bioplastics and Sustainable Material Innovation

The growing demand for bioplastics and biodegradable materials creates substantial opportunities for manufacturers developing sustainable alternatives to conventional plastics. Environmental consciousness among consumers and corporations, combined with regulatory pressures to reduce plastic waste, is driving the adoption of bio-based polymers derived from renewable resources. Innovations in biodegradable plastics that maintain performance characteristics while offering end-of-life disposal advantages are attracting investment from brands seeking to enhance their environmental credentials. The development of specialty bioplastics for applications in packaging, agriculture, and consumer products enables manufacturers to differentiate their offerings and capture emerging market segments. Companies successfully commercializing economically viable bioplastic solutions can establish competitive advantages in sustainability-focused markets.

Medical and Healthcare Applications Expansion

Australia's healthcare sector presents expanding opportunities for specialized plastic and rubber products, driven by aging demographics, increasing healthcare spending, and medical technology advancement. Demand for medical-grade polymers used in devices, diagnostic equipment, pharmaceutical packaging, and personal protective equipment continues to grow. The COVID-19 pandemic highlighted the critical importance of healthcare supply chain resilience, creating opportunities for domestic manufacturers to establish capabilities in medical plastics production. Specialized applications requiring biocompatibility, sterilization resistance, and regulatory compliance command premium pricing and offer stable demand characteristics. Manufacturers developing expertise in medical-grade materials can access high-value market segments with strong growth trajectories and defensible competitive positions.

Challenges of Australia Plastics and Rubber Market:

Dependence on Imported Raw Materials and Price Volatility

Australia's plastics industry faces significant challenges due to heavy reliance on imported raw materials, with approximately 80% of plastic products currently sourced from overseas suppliers. This import dependence creates vulnerability to global supply chain disruptions, currency fluctuations, and international price volatility in petrochemical feedstocks. Rubber and crude oil price fluctuations directly impact production costs, constraining manufacturers' ability to maintain consistent pricing and profitability margins. The limited domestic production capacity for virgin resins necessitates substantial imports from Asia-Pacific manufacturing hubs, exposing Australian producers to geopolitical risks and shipping disruptions. Manufacturers must navigate these supply chain complexities while competing with imported finished goods that benefit from economies of scale in larger manufacturing markets.

Stringent Environmental Regulations and Compliance Costs

Increasingly stringent environmental regulations addressing plastic waste, microplastic pollution, and single-use plastic elimination present significant operational and financial challenges for industry participants. State and federal governments are implementing bans on various plastic products, including shopping bags, straws, and food packaging items, requiring manufacturers to reformulate products and invest in alternative materials. Compliance with extended producer responsibility schemes, recycled content mandates, and packaging recovery targets necessitates substantial investments in collection, sorting, and recycling infrastructure. New South Wales' impending microplastic bans and Victoria's progressive single-use plastic restrictions require ongoing product innovation and manufacturing process modifications. According to the Australia plastics and rubber market analysis, these regulatory pressures increase operational costs while potentially reducing addressable markets for conventional plastic products.

Infrastructure Limitations for Recycling and Circular Economy

Despite growing policy support for circular economy development, Australia's recycling infrastructure remains inadequate to process the diverse range of plastic materials generated domestically. Current mechanical recycling facilities struggle to handle soft plastics, multi-layered packaging, and contaminated materials, resulting in low national recycling rates of approximately 13% for plastics. The collapse of high-profile recycling programs like REDcycle highlighted systemic infrastructure gaps and processing capacity limitations. Geographic challenges in a vast country with dispersed population centers complicate efficient collection and processing of plastic waste. Substantial capital investment is required to develop advanced sorting, cleaning, and reprocessing facilities capable of producing high-quality recyclate suitable for manufacturing applications. Until comprehensive infrastructure is established, manufacturers face difficulties sourcing consistent supplies of recycled materials to meet sustainability commitments.

Australia Plastics and Rubber Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country level for 2026-2034. Our report has categorized the market based on type and end-user.

Type Insights:

- Rubber Products

- Tire

- Hoses and Belting

- Others

- Plastic Products

- Plastic Packaging Materials and Unlaminated Film and Sheet

- Plastic Pipes and Shapes

- Laminated Plastics Plate, Sheet, and Shape

- Plastics Bottle

- Urethane and Other Foam Product

- Polystyrene Foam Products

- Others

The report has provided a detailed breakup and analysis of the market based on the type. This includes rubber products (tire, hoses and belting, and others) and plastic products (plastics packaging materials and unlaminated film and sheet, plastic pipes and shapes, laminated plastics plate, sheet, and shape, plastics bottle, urethane and other foam product, polystyrene foam products, and others).

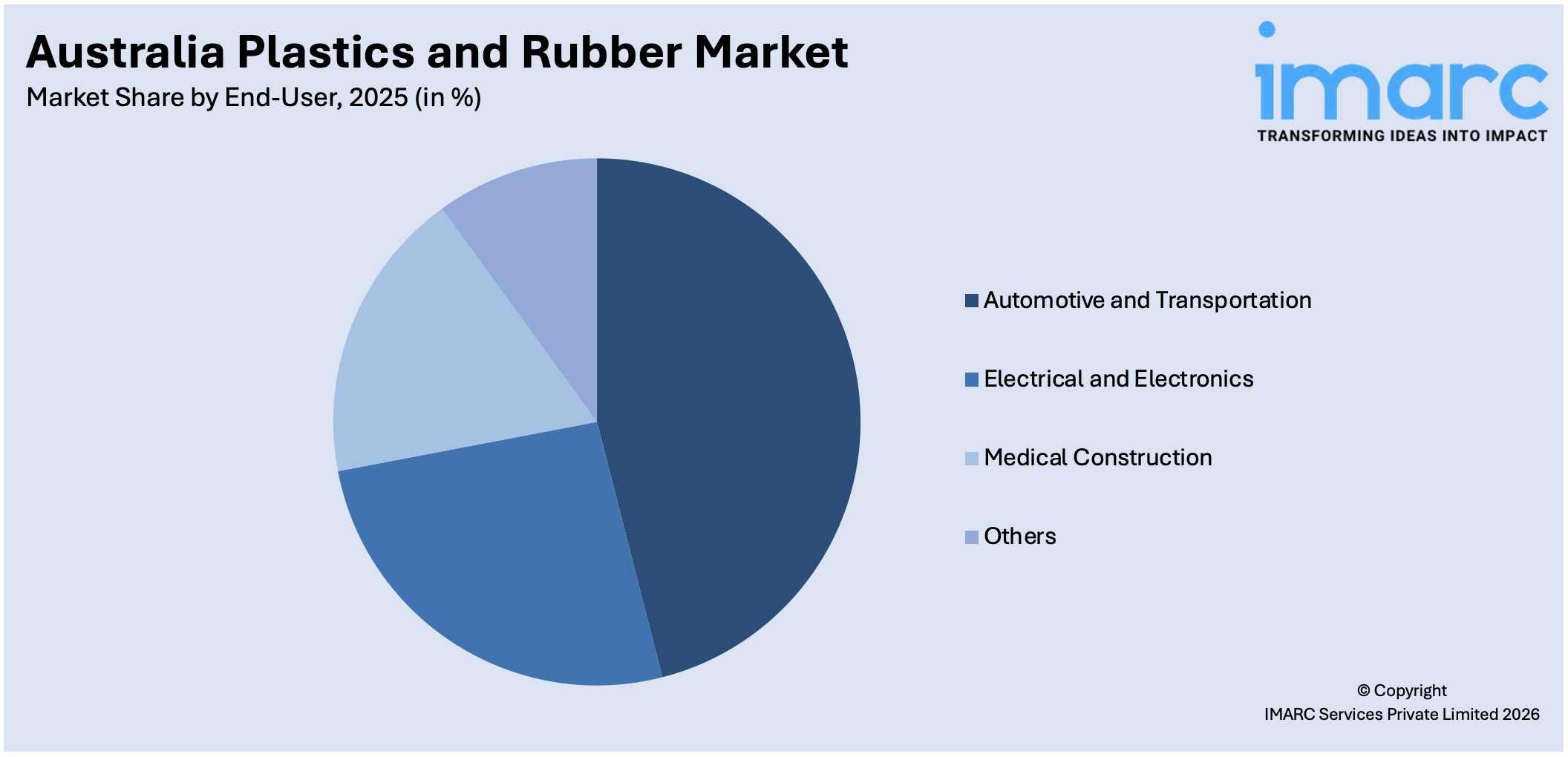

End-User Insights:

Access the comprehensive market breakdown Request Sample

- Automotive and Transportation

- Electrical and Electronics

- Medical Construction

- Others

A detailed breakup and analysis of the market based on the end-user have also been provided in the report. This includes automotive and transportation, electrical and electronics, medical construction, and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Plastics and Rubber Market News:

- In September 2025, Samsara Eco officially opened its first commercial-scale enzymatic plastics recycling plant in Jerrabomberra, New South Wales, marking a significant advancement in circular plastics manufacturing. The facility utilizes AI-designed enzymes to break down mixed plastics into raw materials for producing virgin-identical recycled nylon and polyester for apparel, packaging, and automotive applications.

- In August 2025, the Australian and New South Wales governments jointly invested $11.2 million in regional plastics recycling infrastructure projects. iQRenew received $9.1 million to upgrade its Mid North Coast facility to repurpose 10,000 tonnes of household soft plastic packaging annually into resin for manufacturing applications. The initiative supports the transition toward a circular economy for plastic waste management.

- In July 2024, the Australian Government invested $20 million in Recycling Plastics Australia's advanced recycling technology facility in Kilburn, South Australia. The project will annually divert over 14,000 tonnes of soft plastics from landfills, creating 45 jobs while developing supply chains to transform soft plastic waste into new packaging materials.

- In August 2024, the Australian Government invested A$15.6m ($10.5m) in soft plastics recycling in Victoria, aiming to divert over 43,000 tonnes of soft plastics annually. Pro-Pac Group will receive over A$6m to boost its facility's capacity to produce 11,000t of Australian soft plastic packaging annually.

- In December 2023, Victoria's largest PET plastic bottle recycling plant, the Circular Plastics Australia (PET) facility opened in Melbourne. The $50 million facility will convert used PET bottles into high-quality food-grade resin, which will be used to create new recycled PET beverage bottles and food packaging.

Australia Plastics and Rubber Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Types Covered |

|

| End-Users Covered | Automotive and Transportation, Electrical and Electronics, Medical Construction, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia plastics and rubber market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia plastics and rubber market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia plastics and rubber industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Plastics and Rubber Market Report

The plastics and rubber market in Australia was valued at USD 9.7 Billion in 2025.

The Australia plastics and rubber market is projected to exhibit a CAGR of 5.02% during 2026-2034.

The Australia plastics and rubber market is projected to reach a value of USD 15.1 Billion by 2034.

The Australia plastics and rubber market is witnessing trends such as growing adoption of bio-based materials, increased recycling initiatives, and technological innovations in polymer production. Rising demand from automotive, construction, and packaging sectors, along with sustainability-driven manufacturing practices, is reshaping industry dynamics and promoting circular economy principles.

The Australia plastics and rubber market is driven by expanding industrial applications, infrastructure modernization, and rising demand for lightweight materials. Supportive government policies, advancements in material science, and increasing use in healthcare and electronics sectors further enhance market expansion, encouraging domestic production and boosting export competitiveness across multiple end-use industries.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)