Australia Polyethylene Terephthalate Market Size, Share, Trends and Forecast by Type, Application, and Region, 2026-2034

Australia Polyethylene Terephthalate Market Summary:

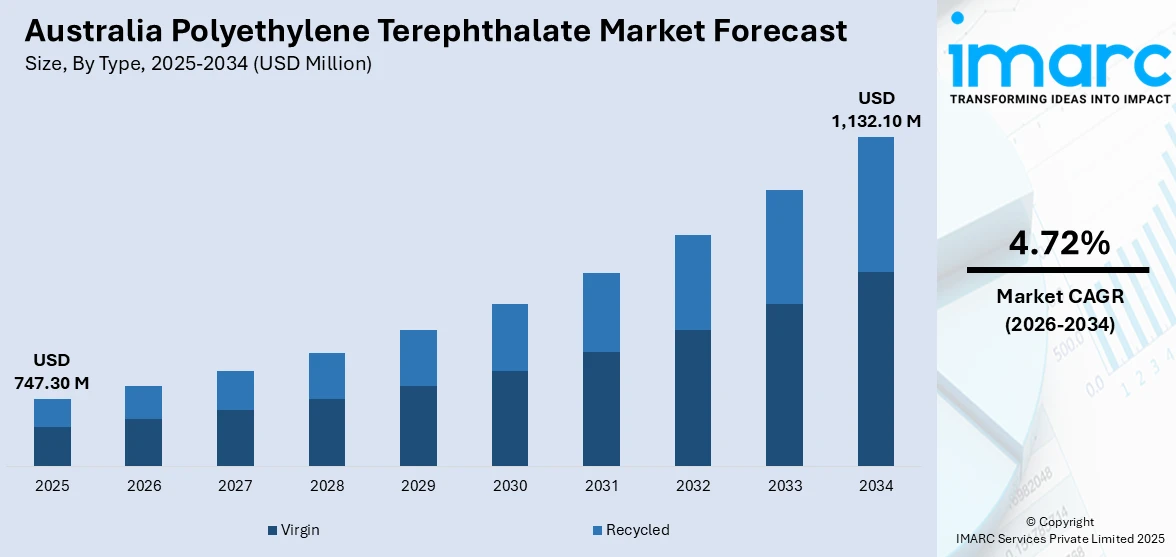

The Australia polyethylene terephthalate market size was valued at USD 747.30 Million in 2025 and is projected to reach USD 1,132.10 Million by 2034, growing at a compound annual growth rate of 4.72% from 2026-2034.

The Australia polyethylene terephthalate market is experiencing robust growth, driven by escalating demand for sustainable packaging solutions and strengthening recycling infrastructure nationwide. Government-mandated container deposit schemes, expanding food and beverage (F&B) manufacturing, and increasing adoption of recycled polyethylene terephthalate (PET) resin are accelerating market expansion. Technological advancements in PET processing, growing consumer preferences for lightweight and recyclable packaging materials, and industry-wide commitments to circular economy principles are fueling the market expansion.

Key Takeaways and Insights:

- By Type: Virgin dominates the market with a share of 63.8% in 2025, owing to its superior clarity, strength, and compliance with stringent food-grade safety standards essential for beverage bottles and premium packaging applications across Australia.

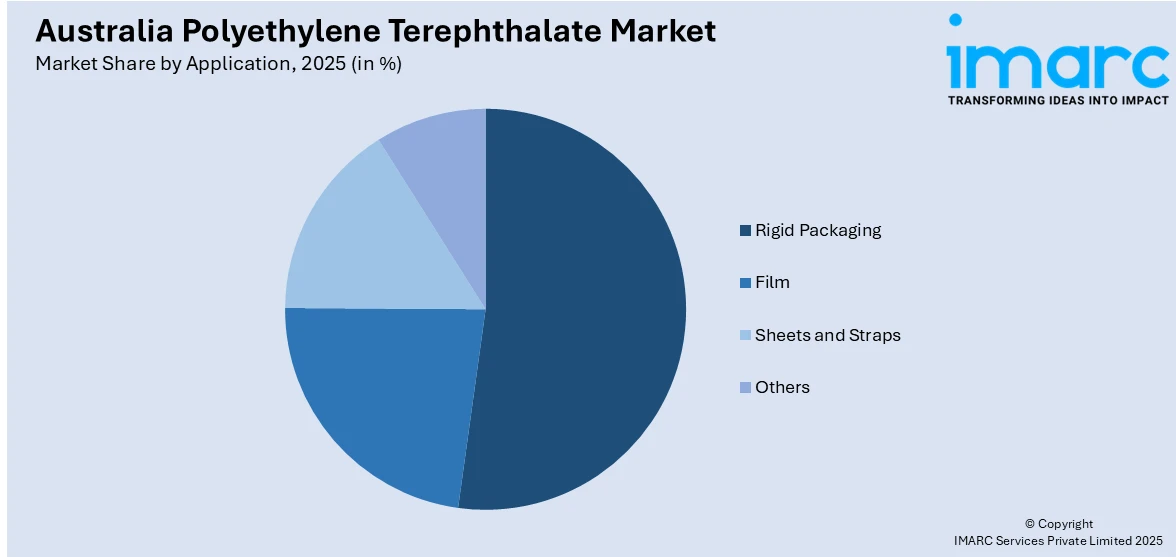

- By Application: Rigid packaging leads the market with a share of 52.4% in 2025, driven by widespread use in beverage bottles, food containers, and personal care product packaging, supported by growing consumer preferences for durable and recyclable materials.

- By Region: Australia Capital Territory & New South Wales represents the largest region with 34.9% share in 2025, supported by the concentration of major manufacturing facilities, robust container deposit infrastructure, and significant government investment in recycling modernization programs.

- Key Players: Key players drive the market growth by investing in advanced recycling technologies, expanding food-grade recycled PET production capacity, forming cross-industry partnerships, and strengthening closed-loop packaging systems to enhance sustainability credentials and maintain competitive positioning across domestic and export markets.

To get more information on this market Request Sample

The Australia polyethylene terephthalate market is advancing as regulatory frameworks, corporate sustainability commitments, and consumer awareness converge to create favorable conditions for sustained expansion. A critical factor underpinning this growth is the nationwide rollout of Container Deposit Schemes, which have dramatically improved PET collection and recycling rates across all states and territories. For example, Victoria’s Container Deposit Scheme, implemented in November 2023, collected 1 Billion eligible drink containers in the first year, resulting in AUD 950,000 being donated to community organizations. These deposit return programs provide a reliable and high-quality supply of post-consumer PET feedstock for domestic recycling facilities, supporting the broader transition towards a circular economy. Simultaneously, augmenting local recycling capabilities, rising use of recycled PET in F&B packaging, and increasing investments in sophisticated sorting and decontamination technologies are enhancing the entire value chain.

Australia Polyethylene Terephthalate Market Trends:

Expansion of Domestic PET Recycling Infrastructure

Australia is rapidly scaling its PET recycling capacity through purpose-built facilities designed to process post-consumer plastic waste into food-grade resin. In November 2023, the Circular Plastics Australia (PET) plant, a facility worth USD 50 Million that can recycle the equivalent of up to one billion 600ml PET plastic beverage bottles annually, began operations in Melbourne. It will transform used beverage bottles into high-quality food-grade resin, which is then utilized to produce new recycled PET beverage bottles and food packaging like meat trays and fruit punnets. These investments are reducing reliance on imported virgin resin and supporting the Australia polyethylene terephthalate market growth.

Lightweighting and Material Efficiency Innovations

Manufacturers are actively investing in lightweighting technologies to reduce material usage while maintaining packaging performance and safety standards. Advancements in resin formulation, bottle design, and preform engineering enable thinner PET packaging with comparable strength and durability. These innovations lower production costs, reduce transportation emissions, and support sustainability targets without compromising shelf life or product protection. Lightweight PET solutions are particularly attractive to beverage producers seeking cost efficiencies at scale. Continuous improvements in material efficiency enhance PET’s competitiveness against alternative packaging materials, reinforcing its role in Australia’s evolving packaging landscape.

Rising Adoption in Non-Packaging Applications

Beyond packaging, PET demand in Australia is increasing across textile fibers, automotive components, and construction materials. Recycled PET is increasingly used in polyester fibers for clothing, carpets, and industrial fabrics, supporting waste reduction objectives. In automotive and industrial applications, PET offers durability, chemical resistance, and lightweight properties. This diversification of end use applications reduces market reliance on packaging alone and enhances overall PET consumption stability, contributing to long-term market resilience.

Market Outlook 2026-2034:

The Australia polyethylene terephthalate market is positioned for sustained growth over the forecast period, underpinned by expanding recycling infrastructure, tightening environmental regulations, and rising demand for sustainable packaging solutions. The market generated a revenue of USD 747.30 Million in 2025 and is projected to reach a revenue of USD 1,132.10 Million by 2034, growing at a compound annual growth rate of 4.72% from 2026-2034. Growing corporate commitments to incorporate higher percentages of recycled PET content, combined with government-backed investment in advanced recycling technologies and circular economy initiatives, will create a more resilient and self-sufficient supply chain. Additionally, Australia’s F&B sector growth, alongside increasing pharmaceutical and personal care packaging requirements, will sustain strong underlying demand for both virgin and recycled PET products throughout the forecast period.

Australia Polyethylene Terephthalate Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Type |

Virgin |

63.8% |

|

Application |

Rigid Packaging |

52.4% |

|

Region |

Australia Capital Territory & New South Wales |

34.9% |

Type Insights:

- Virgin

- Recycled

Virgin dominates the Australia polyethylene terephthalate market with a share of 63.8% in 2025.

Virgin maintains its commanding position in Australia, owing to its unmatched optical clarity, mechanical strength, and ability to meet the stringent food-contact safety standards required across the beverage, dairy, and ready-to-eat (RTE) food sectors. As per IMARC Group, the Australia dairy market size was valued at USD 6.7 Billion in 2024. In Australia's vast logistics networks, where lowering transit weight immediately reduces carbon emissions and freight costs, the resin's lightweight qualities are especially advantageous.

Additionally, virgin PET plays vital roles in fresh produce trays, personal care containers, and pharmaceutical packaging, where contamination-free material integrity is essential for customer safety. Manufacturers are depending more on virgin PET's uniform processing properties and predictable molecular structure to preserve packaging quality across high-speed manufacturing lines, as food safety rules tighten and shelf-life requirements increase. This dependability reduces quality fluctuations in crucial consumer packaging applications and enables continuous large-scale production.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Rigid Packaging

- Film

- Sheets and Straps

- Others

Rigid packaging leads the Australia polyethylene terephthalate market with a share of 52.4% in 2025.

Rigid packaging encompasses bottles, jars, clamshells, and trays that are essential across Australia’s F&B, pharmaceutical, and personal care industries. PET is the material of choice for carbonated drinks, bottled water, fruit juices, and dairy goods due to its outstanding transparency, impact resistance, and economical lightweight construction. Its superior barrier qualities prolong the shelf life of delicate F&B categories by shielding products from oxygen and moisture. Furthermore, rigid PET packaging facilitates rapid labeling and filling processes, increasing productivity for large-scale manufacturers.

Rigid packaging is becoming able to reach new product categories, including kombucha, plant-based beverages, and functional health drinks, which require certain filling techniques to preserve product stability. This is made feasible by the development of aseptic PET containers and hot-fill technologies. Australia's growing e-commerce sector is driving the demand for robust PET containers that can withstand handling during transport while maintaining product integrity throughout the distribution chain. Because of the country's active outdoor lifestyle culture and the expansion of single-serve and portable consumption forms, rigid PET packaging is the most popular application segment in the market.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales represents the largest region with a 34.9% share of the total Australia polyethylene terephthalate market in 2025.

Australia Capital Territory & New South Wales commands the largest share of the market, driven by the concentration of major manufacturing facilities, F&B processing plants, and advanced recycling infrastructure. Sydney’s status as Australia’s largest consumer market generates substantial demand for PET-packaged beverages, food products, and personal care items. The presence of key industry players, research institutions, and logistics hubs creates a concentrated ecosystem that supports innovation in PET production, recycling, and packaging design across the value chain.

Strong policy support for waste reduction and environmental activities benefit the region, which promotes a greater use of recycled PET in packaging applications. Circular economy practices are strengthened by well-established collection and sorting systems that increase the availability of feedstock for recycling facilities. PET demand is further sustained throughout retail and e-commerce channels by high urban population density and growing packaged goods consumption. Furthermore, being close to important ports improves export capabilities, allowing firms to effectively service both domestic and foreign markets while preserving supply chain resilience and cost competitiveness.

Market Dynamics:

Growth Drivers:

Why is the Australia Polyethylene Terephthalate Market Growing?

Government-Led Regulatory Support

The market is being heavily driven by the collective federal and state government policies that have sustainability as the central tenet of packaging and waste management strategies. The government’s agenda is that packaging needs to be reusable, recyclable, or compostable within set time frames, which is pressuring the industry to focus on PET because of its proven recyclability. The ban on the export of mixed plastic waste has led to a massive amount of post-consumer waste being processed domestically, which is pressuring the industry to set up local recycling capacity. Barriers to entry have been reduced by financial support for large-scale recycling projects, which is encouraging the private sector to participate. This is being aided by tougher compliance standards that are discouraging the practice of landfilling and unsustainable waste management. As a result, the PET packaging industry is increasingly falling in line with the principles of a circular economy.

Rising Demand from F&B Packaging

In Australia, the polyethylene terephthalate market is expanding steadily due to strong and sustained demand from the F&B sector. As per IMARC Group, the Australia F&B market size reached USD 154.2 Billion in 2025. PET is widely favored for bottled water, carbonated drinks, juices, dairy products, and RTE foods because it combines lightweight properties with durability and excellent clarity. Changing consumer lifestyles, including on-the-go consumption and preference for convenient packaging formats, are increasing the use of single-serve and resealable containers made from PET. The material’s ability to preserve freshness and extend shelf life makes it especially suitable for temperature-sensitive products. As F&B producers continue to expand product ranges and distribution reach, PET remains a reliable packaging solution supporting consistent market growth.

Technological Advancements in PET Processing and Design

By increasing productivity, quality, and design flexibility, ongoing advancements in PET processing technologies are significantly contributing to market expansion. Modern molding techniques enable producers to use less material while still meeting safety and strength requirements. Better heat resistance and durability are made possible by improved resin formulas, which create chances for new applications, including specialty packaging and hot-fill beverages. PET packaging is becoming more competitive because of the use of automation and precision manufacturing, which lower waste and production costs. These technology advancements allow manufacturers to react swiftly to changing consumer demands for personalization. Additionally, high-speed production lines are becoming more consistent due to smart manufacturing technology and digital quality monitoring. Rapid prototyping made possible by improved design tools enables brand owners to introduce novel packaging formats and shorten product development cycles.

Market Restraints:

What Challenges the Australia Polyethylene Terephthalate Market is Facing?

Volatility in Petroleum-Based Raw Material Prices

PET production depends heavily on petroleum-derived feedstocks, including purified terephthalic acid and monoethylene glycol, whose prices are subject to significant fluctuations driven by global crude oil market dynamics. These cost variations directly impact manufacturing margins and can lead to unpredictable pricing for downstream converters and end users. The absence of domestic petrochemical feedstock production in Australia amplifies this vulnerability, as manufacturers must rely entirely on imported raw materials, exposing the supply chain to international trade disruptions and currency exchange volatility.

Complexity of Evolving Regulatory Compliance Requirements

Manufacturers operating in Australia’s PET market face an increasingly complex regulatory environment, spanning environmental impact assessments, recycled content mandates, material safety certifications, and extended producer responsibility obligations. Compliance with these evolving requirements demands significant investment in testing, documentation, and process modification, particularly for smaller producers who may lack the resources of multinational competitors. The ongoing revision of national packaging targets and introduction of eco-modulation fee structures add further uncertainty to long-term planning and capital allocation decisions.

Competition from Alternative Packaging Materials

PET faces growing competition from alternative materials, such as aluminum, glass, paper-based packaging, and bio-based plastics. Brand owners seeking differentiation or sustainability credentials may experiment with these alternatives, particularly in premium or niche product segments. While PET offers strong performance advantages, competing materials often benefit from favorable consumer perception or regulatory preferences. This competitive pressure can slow PET adoption in certain applications and force manufacturers to invest more heavily in innovation, branding, and sustainability messaging.

Competitive Landscape:

The Australia polyethylene terephthalate market features a moderately consolidated competitive landscape, characterized by a mix of established multinational packaging corporations and specialized domestic manufacturers. Companies are differentiating through investments in recycled PET processing capabilities, food-grade certification technologies, and closed-loop partnership models. Strategic emphasis on sustainability credentials, lightweight packaging innovation, and regional supply chain optimization is intensifying as brand owners demand higher recycled content and traceable material sourcing. Industry collaborations between waste management operators, resin producers, and beverage companies are reshaping competitive dynamics, with joint ventures and long-term offtake agreements becoming critical strategic tools for securing market positioning.

Australia Polyethylene Terephthalate Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Types Covered |

Virgin, Recycled |

|

Applications Covered |

Rigid Packaging, Film, Sheets and Straps, Others |

|

Regions Covered |

Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Polyethylene Terephthalate Market Report

The Australia polyethylene terephthalate market size was valued at USD 747.30 Million in 2025.

The Australia polyethylene terephthalate market is expected to grow at a compound annual growth rate of 4.72% from 2026-2034 to reach USD 1,132.10 Million by 2034.

Virgin dominated the market with a share of 63.8%, owing to its exceptional clarity, mechanical strength, and consistent quality. Its suitability for food-contact applications, lightweight properties, and reliability in high-speed production lines make it the preferred choice across industries.

Key factors driving the Australia polyethylene terephthalate market include government regulatory support, nationwide container deposit scheme coverage, expanding domestic recycling infrastructure, growing adoption of recycled PET, and rising demand for sustainable packaging.

Major challenges include volatile petroleum-based raw material prices, insufficient domestic recycling infrastructure relative to waste volumes, complex regulatory compliance requirements, and limited availability of food-grade recycled PET resin.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)