Australia Prepaid Cards Market Size, Share, Trends and Forecast by Card Type, Purpose, Vertical, and Region, 2026-2034

Australia Prepaid Cards Market Summary:

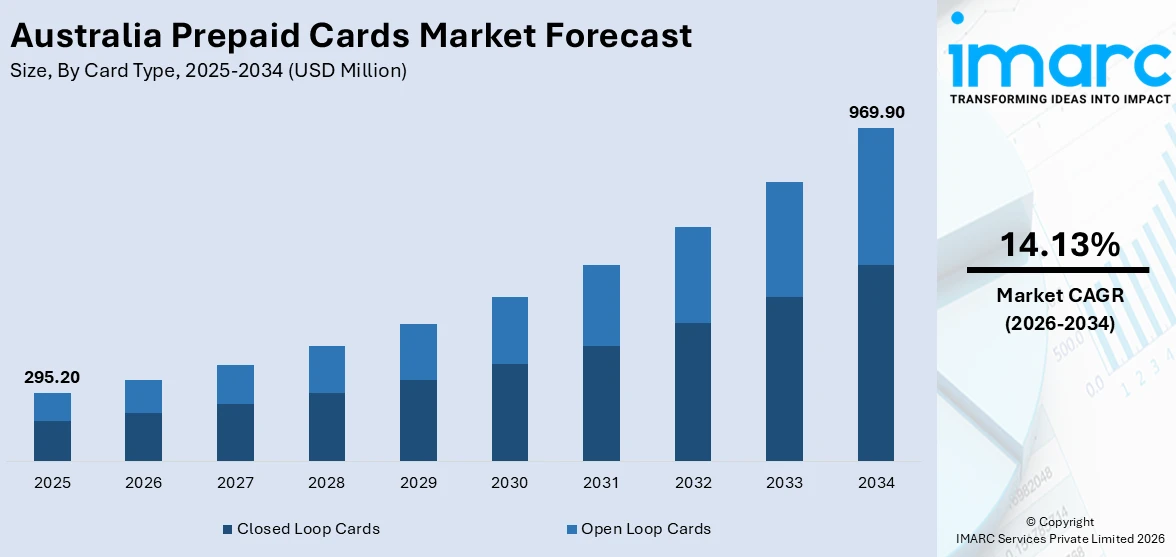

The Australia prepaid cards market size was valued at USD 295.20 Million in 2025 and is projected to reach USD 969.90 Million by 2034, growing at a compound annual growth rate of 14.13% from 2026-2034.

The Australia prepaid cards market is experiencing significant momentum driven by the accelerating transition from cash to digital payment methods and the growing integration of prepaid solutions into mobile wallet ecosystems. Rising consumer preference for flexible, convenient, and secure payment alternatives is strengthening adoption across retail and corporate segments, positioning the country as an evolving hub for next-generation prepaid payment solutions.

Key Takeaways and Insights:

- By Card Type: Closed loop cards dominate the market with a share of 62.0% in 2025, driven by their widespread adoption among Australian retailers for branded store programs, loyalty schemes, and gift card offerings that provide controlled spending environments and enhanced customer engagement.

- By Purpose: Gift cards lead the market with a share of 28.5% in 2025, owing to their growing popularity as convenient gifting solutions across retail and corporate segments, supported by digital integration with e-commerce platforms and mobile wallets that enhance accessibility and consumer convenience.

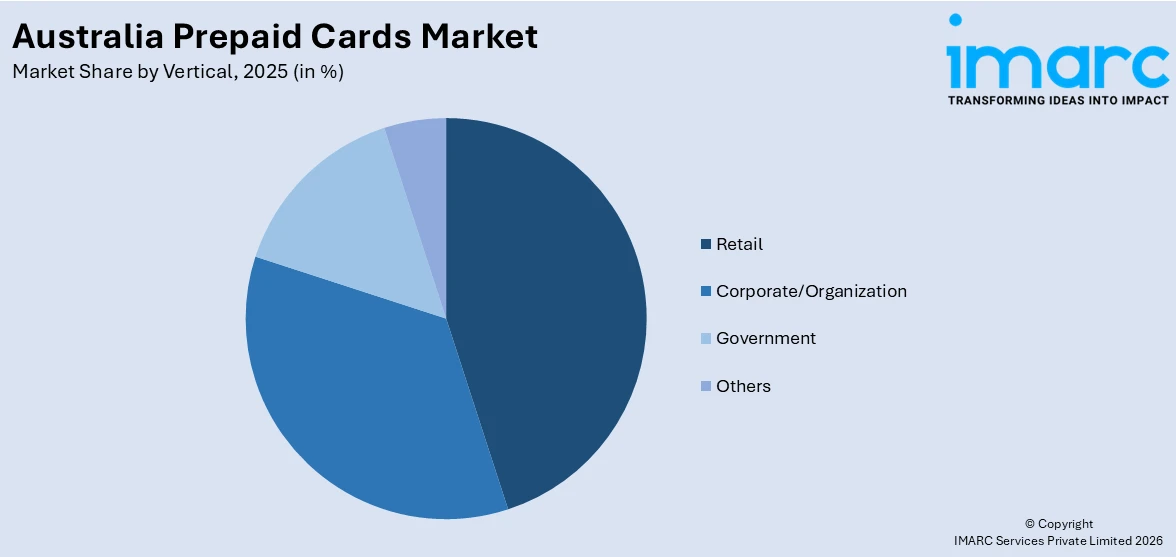

- By Vertical: Retail holds the largest segment with a market share of 42.5% in 2025, reflecting the strong consumer preference for prepaid card usage in everyday retail transactions, including in-store purchases, online shopping, and gift card redemptions across major retail chains.

- By Region: Australia Capital Territory & New South Wales represents the largest region with 34.8% share in 2025, driven by the concentration of Australia’s financial services industry, the country’s largest population base in Sydney, and a mature retail and e-commerce ecosystem that supports widespread prepaid card adoption.

- Key Players: Key players drive the Australia prepaid cards market by expanding digital payment integrations, enhancing card security technologies, strengthening partnerships with retailers, and investing in mobile wallet compatibility to boost adoption and market penetration across diverse consumer and corporate segments.

To get more information on this market Request Sample

The Australia prepaid cards market is advancing as consumers, businesses, and financial institutions increasingly embrace cashless payment solutions and digital-first financial tools. Growing smartphone penetration and the expansion of mobile wallet ecosystems, including Apple Pay and Google Pay, are enabling seamless integration of prepaid cards into daily payment routines. The corporate sector is emerging as a significant growth catalyst, with businesses leveraging prepaid instruments for employee rewards, wellness stipends, and customer incentive programs. Australia’s e-commerce sector is further strengthening the demand for digital and physical prepaid cards as preferred payment methods. Regulatory modernization, including the planned phase-out of cheques and enhanced payment system oversight, is reinforcing market expansion and encouraging innovation across the prepaid card ecosystem.

Australia Prepaid Cards Market Trends:

Integration of prepaid cards with digital wallets and mobile payment platforms

The integration of prepaid cards with digital wallets is reshaping payment experiences across Australia, as consumers increasingly link their prepaid instruments to platforms such as Apple Pay and Google Pay for seamless contactless transactions. In March 2025, Google Wallet introduced support for dual network debit cards in Australia, allowing transactions to be processed via the domestic eftpos network or international networks. This convergence of prepaid cards with mobile wallet infrastructure is expanding their utility beyond traditional point-of-sale use, driving the Australia prepaid cards market growth.

Expansion of corporate prepaid programs for employee incentives and rewards

Australian corporations are increasingly adopting prepaid card-based incentive programs to manage employee benefits, wellness stipends, retention bonuses, and customer rewards. Businesses recognize the tax efficiency, denomination flexibility, and seamless digital distribution that prepaid cards offer compared to traditional merchandise-based reward systems. In August 2024, Medibank’s Live Better platform, for example, has rewarded over 823,000 members through health-oriented gift card redemptions, illustrating the growing corporate appetite for prepaid solutions that enhance engagement and provide measurable return on investment across diverse workforce and customer segments.

Accelerated shift toward wallet-ready and tokenized prepaid solutions

Prepaid card programs in Australia are increasingly being designed as wallet-ready solutions with embedded tokenization capabilities, reducing reliance on physical card distribution and activation processes. In October 2025, CPI Card Group announced a strategic partnership with Karta, an Australian-born fintech backed by the Commonwealth Bank of Australia, to integrate its patent-pending SafeToBuy technology into prepaid card programs. This innovation embeds security data into EMV chips, eliminating printed card details and significantly reducing gift card fraud.

Market Outlook 2026-2034:

The Australia prepaid cards market is poised for sustained expansion over the forecast period, underpinned by the country’s accelerating shift toward a cashless economy, deepening digital wallet adoption, and growing corporate utilization of prepaid instruments for incentive and expense management programs. The ongoing phase-out of cheques, with issuance set to cease by June 2028 under the Australian Government’s Cheques Transition Plan, is expected to redirect transaction volumes toward prepaid and digital payment channels. Continued innovation in prepaid card security, including tokenization and EMV-based fraud prevention, alongside the expanding e-commerce landscape and rising consumer preference for flexible, controlled-spending payment solutions, are expected to sustain strong market momentum throughout the forecast period. The market generated a revenue of USD 295.20 Million in 2025 and is projected to reach a revenue of USD 969.9 Million by 2034, growing at a compound annual growth rate of 14.13% from 2026-2034.

Australia Prepaid Cards Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Card Type |

Closed Loop Cards |

62.0% |

|

Purpose |

Gift Cards |

28.5% |

|

Vertical |

Retail |

42.5% |

|

Region |

Australia Capital Territory & New South Wales |

34.8% |

Card Type Insights:

- Closed Loop Cards

- Open Loop Cards

Closed loop cards dominate with a market share of 62.0% of the total Australia prepaid cards market in 2025.

Closed loop cards maintain their leadership position in the Australia prepaid cards market owing to their extensive adoption by retailers for branded store-specific payment programs, loyalty reward schemes, and gift card platforms. These single-merchant or single-network cards offer businesses greater control over consumer spending patterns while providing customers with targeted promotional benefits. Major Australian retail chains continue to drive demand for closed loop instruments through comprehensive gift card ecosystems that serve as key customer engagement and retention tools.

The prominence of closed loop cards is further supported by the growing digital transformation of retail loyalty programs, where businesses are embedding prepaid card functionality into mobile applications and digital wallets. The accelerating shift from physical to digital closed loop instruments is reshaping distribution strategies across the retail sector. Leading Australian retailers continue to expand their branded prepaid card offerings, leveraging digital distribution channels to enhance customer convenience and drive repeat engagement across physical and online retail environments.

Purpose Insights:

- Payroll/Incentive Cards

- Travel Cards

- General Purpose Reloadable (GPR) Cards

- Remittance Cards

- Others

Gift cards lead with a share of 28.5% of the total Australia prepaid cards market in 2025.

Gift cards maintain their leading position in the purpose segment, driven by their growing acceptance as convenient and versatile gifting solutions across both individual consumer and corporate channels. The Australian gift card market is reflecting robust year-on-year growth fueled by the digital transformation of gifting practices and increasing retailer investments in branded gift card programs. The integration of gift cards with e-commerce platforms and mobile payment systems has significantly enhanced their accessibility, enabling seamless purchases and instant digital delivery across the country.

The corporate sector has emerged as a significant contributor to gift card demand, with businesses increasingly using them for employee recognition programs, wellness incentives, and customer acquisition campaigns. Australian companies expanded their employee experience allocations considerably after 2024, channeling substantial portions into wellness stipends and retention bonuses delivered via gift cards. The mandatory three-year expiry period introduced through regulatory reforms has further strengthened consumer trust and encouraged repeat purchases, while the expansion of third-party gift card distribution networks across supermarkets and convenience stores has broadened market reach.

Vertical Insights:

Access the comprehensive market breakdown Request Sample

- Corporate/Organization

- Retail

- Government

- Others

The retail exhibits a clear dominance with a 42.5% share of the total Australia prepaid cards market in 2025.

The retail vertical's leadership in the prepaid cards market is driven by the widespread use of gift cards, loyalty programs, and branded store-value cards across major retail chains. The continued expansion of e-commerce activity is accelerating the adoption of digital prepaid cards as preferred payment methods at checkout, with retailers integrating gift card redemption options directly into their online platforms to enhance convenience, streamline purchasing experiences, and drive sustained sales growth across diverse consumer segments.

Prominent Australian retailers have established comprehensive gift card and prepaid card ecosystems that serve as key customer engagement and retention tools. The growing integration of prepaid cards into in-store point-of-sale systems, self-checkout terminals, and online marketplaces has further solidified the retail vertical's dominance, as consumers increasingly prefer prepaid instruments for controlled budgeting, gift purchases, and promotional reward redemptions across both physical and digital retail environments throughout the country.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales represents the leading segment with a 34.8% share of the total Australia prepaid cards market in 2025.

The Australian Capital Territory & New South Wales command the largest share of the Australia prepaid cards market, driven by the region's concentrated financial services infrastructure and the presence of Sydney, Australia's largest metropolitan area. The region's strong retail ecosystem, high consumer spending power, and the concentration of corporate headquarters collectively drive enterprise-level prepaid card adoption, reinforcing its dominant position across both consumer and business segments within the national prepaid card landscape.

The region's advanced digital payment infrastructure and high e-commerce penetration further strengthen its leadership position in the prepaid cards market. New South Wales leads mobile wallet adoption owing to its highly urbanized population and tech-savvy consumer base, which accelerates demand for integrated prepaid card solutions. The continued expansion of fintech operations and digital banking services in Sydney reinforces the region's role as the primary growth driver for prepaid card innovation across Australia.

Market Dynamics:

Growth Drivers:

Why is the Australia Prepaid Cards Market Growing?

Rapid transition toward cashless payments and digital financial ecosystems

Australia's accelerating shift away from cash-based transactions is a fundamental driver of prepaid card market growth. The Reserve Bank of Australia's data confirms a significant and sustained decline in cash usage for retail transactions, reflecting the country's rapid transition toward digital payment methods. This transformation is being supported by the widespread adoption of contactless payment technologies, with mobile wallets such as Apple Pay, Google Pay, and Samsung Pay becoming increasingly prevalent across everyday consumer transactions. The Australian Government’s Strategic Plan for the payments system, which includes a phased cheque wind-down with issuance ceasing by June 2028 and acceptance ending by September 2029, is further channeling consumer and business payment volumes toward prepaid and digital card instruments. The rise of near-field communication technology, QR code-based payment solutions, and tap-and-go functionality has enhanced the practicality of prepaid cards in everyday commerce, accelerating their adoption among consumers seeking secure and convenient payment alternatives.

Expanding e-commerce sector driving demand for digital prepaid instruments

The robust growth of Australia's e-commerce sector is significantly boosting prepaid card demand, as online retailers increasingly integrate prepaid and gift card payment options into their checkout processes. Online shopping continues to account for a growing share of all retail spending in the country, creating substantial opportunities for digital gift cards and virtual prepaid solutions. Retailers are embedding gift card functionality within their online platforms, enabling instant digital delivery, personalized messaging, and seamless mobile wallet integration. The expansion of online marketplaces, subscription-based services, and cross-border e-commerce is further amplifying the use of prepaid instruments, as consumers seek flexible and budget-friendly payment tools for digital transactions.

Growing corporate adoption of prepaid cards for incentive and expense management

The corporate sector is emerging as a powerful growth engine for the prepaid cards market in Australia, with businesses across industries adopting prepaid solutions for employee rewards, expense management, vendor payments, and customer retention programs. Companies are recognizing the tax efficiency, budget control, and streamlined distribution capabilities offered by digital prepaid cards compared to traditional reward mechanisms. The substantial enterprise appetite for prepaid-based incentive programs continues to strengthen, as human resources departments integrate gift cards into wellness stipends, retention bonuses, and performance recognition initiatives, while finance teams appreciate the simplified reconciliation and reduced audit complexity associated with prepaid instruments. The growing availability of API-enabled digital card distribution platforms is enabling seamless program management and real-time tracking of redemption patterns across departments and geographies.

Market Restraints:

What Challenges the Australia Prepaid Cards Market is Facing?

Persistent fraud and security vulnerabilities in prepaid card programs

Prepaid cards, particularly gift cards, remain susceptible to various forms of fraud, including card draining, social engineering scams, and unauthorized activation exploits. The absence of printed cardholder verification on many prepaid instruments creates opportunities for criminal actors to target consumers and retailers. While technological countermeasures such as EMV chip integration and tokenization are advancing, the evolving nature of fraud techniques continues to pose significant security challenges that can erode consumer confidence and increase operational costs for issuers and program managers.

Regulatory complexity and compliance burdens across state and federal jurisdictions

The Australian regulatory environment for prepaid cards involves multiple layers of compliance requirements, including anti-money laundering and counter-terrorism financing obligations administered by AUSTRAC, consumer protection regulations, and varying state-level gift card expiry and disclosure rules. The evolving payment system regulatory framework, including proposed amendments to the Payment Systems Regulation Act and the expanding scope of Reserve Bank of Australia oversight to include digital wallet providers, is adding complexity for prepaid card issuers and program managers seeking to operate at national scale.

Intensifying competition from alternative payment methods

The prepaid cards market in Australia faces growing competitive pressure from alternative payment solutions, including buy now, pay later services, real-time account-to-account transfers through the New Payments Platform, and peer-to-peer payment applications. These alternatives offer consumers flexible spending options, instant fund transfers, and integrated shopping experiences that may reduce the perceived necessity of prepaid cards for certain use cases, particularly among younger demographics who are increasingly drawn to instalment-based payment models and digital-first financial tools.

Competitive Landscape:

The Australia prepaid cards market is characterized by a dynamic competitive environment where established financial institutions, major retailers, and emerging fintech companies are vying for market share through product innovation and strategic partnerships. Market participants are focusing on expanding digital card offerings, enhancing mobile wallet compatibility, and integrating advanced security features such as tokenization and biometric authentication to differentiate their products. The consolidation of payment platforms, including the proposed merger of BPAY, eftpos, and NPP into a single entity, reflects the industry’s drive toward streamlined payment infrastructure. Competitive intensity is further amplified by the entry of international fintech players and the development of cryptocurrency-based prepaid solutions, pushing incumbents to accelerate innovation cycles and forge collaborative partnerships.

Recent Developments:

- In February 2026, Vault Payment Solutions, Australia’s leading provider of secure card payments, selected Thredd as its strategic issuer processing partner to support the launch of new prepaid, debit, and private-label card programs in Australia and the United Kingdom on Mastercard’s global network. This partnership follows Vault’s appointment as a Mastercard Principal Issuing Partner.

- In October 2025, CPI Card Group announced a strategic partnership with and minority equity investment in Karta, an Australian-born fintech backed by the Commonwealth Bank of Australia. The collaboration integrates Karta’s patent-pending SafeToBuy technology with CPI’s prepaid solutions, embedding security data into EMV chips to mitigate fraudulent draining of prepaid cards.

Australia Prepaid Cards Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Card Types Covered | Closed Loop Cards, Open Loop Cards |

| Purposes Covered | Payroll/Incentive Cards, Travel Cards, General Purpose Reloadable (GPR) Cards, Remittance Cards, Others |

| Verticals Covered | Corporate/Organization, Retail, Government, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Prepaid Cards Market Report

The Australia prepaid cards market size was valued at USD 295.20 Million in 2025.

The Australia prepaid cards market is expected to grow at a compound annual growth rate of 14.13% from 2026-2034 to reach USD 969.9 Million by 2034.

Closed loop cards dominated the market with a share of 62.0%, driven by their extensive adoption among Australian retailers for branded store programs, loyalty reward schemes, and gift card platforms that provide controlled spending environments.

Key factors driving the Australia prepaid cards market include the rapid transition toward cashless payments, expanding e-commerce activity, growing corporate adoption of prepaid incentive programs, and supportive regulatory reforms modernizing the payment system.

Major challenges include persistent fraud and security vulnerabilities, regulatory complexity across state and federal jurisdictions, intensifying competition from alternative payment methods such as buy now pay later services, and evolving compliance requirements under AUSTRAC oversight.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)