Australia Railway System Market Size, Share, Trends and Forecast by Transit Type, System Type, Application, and Region, 2026-2034

Australia Railway System Market Size, Share, Trends & Forecast (2026-2034)

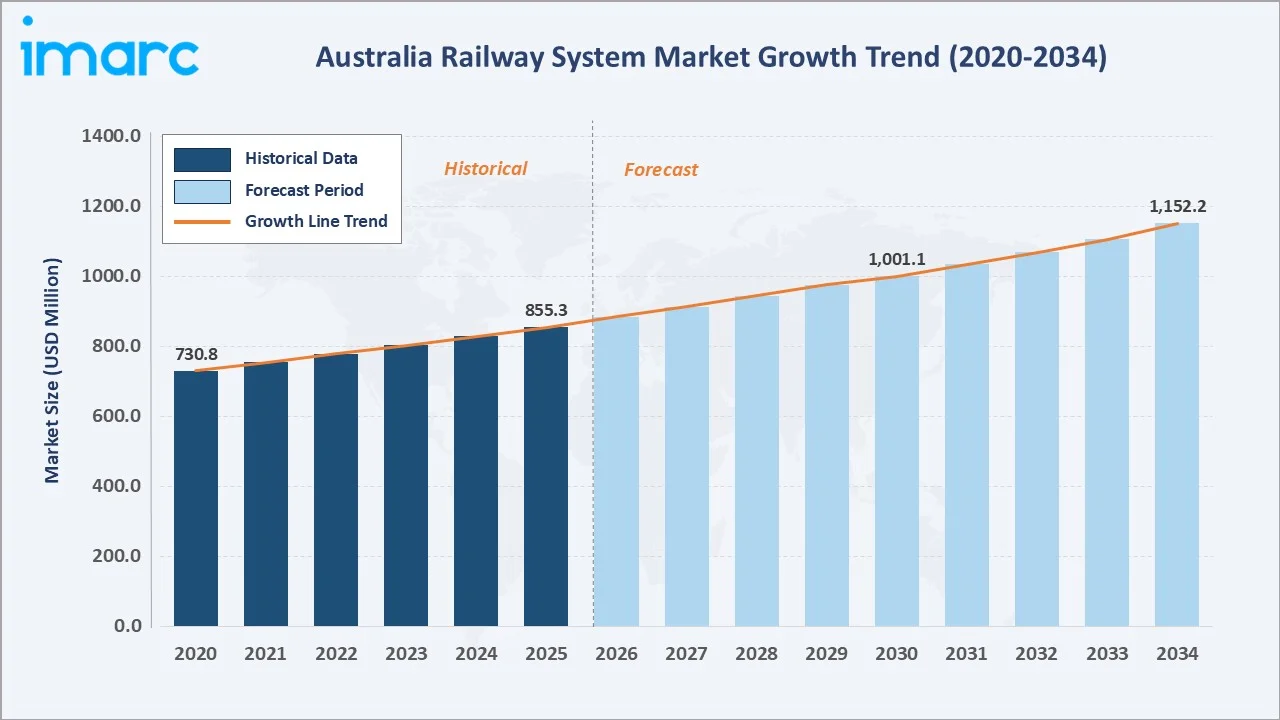

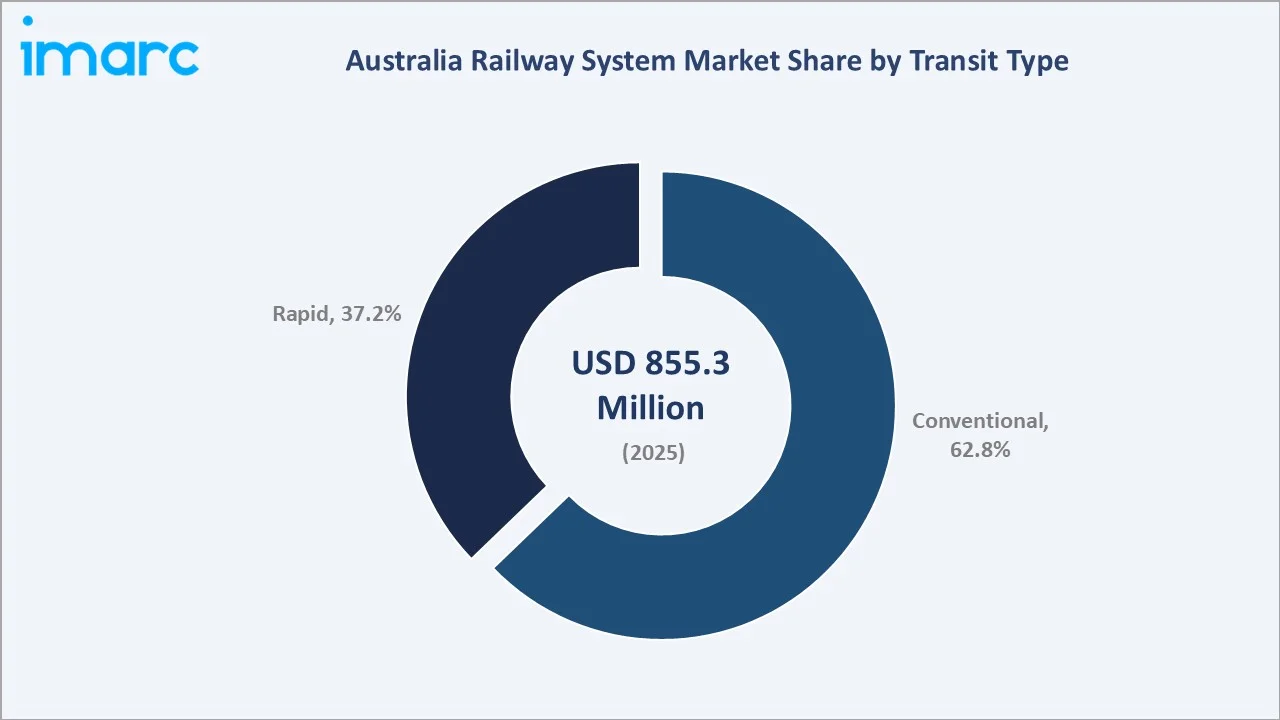

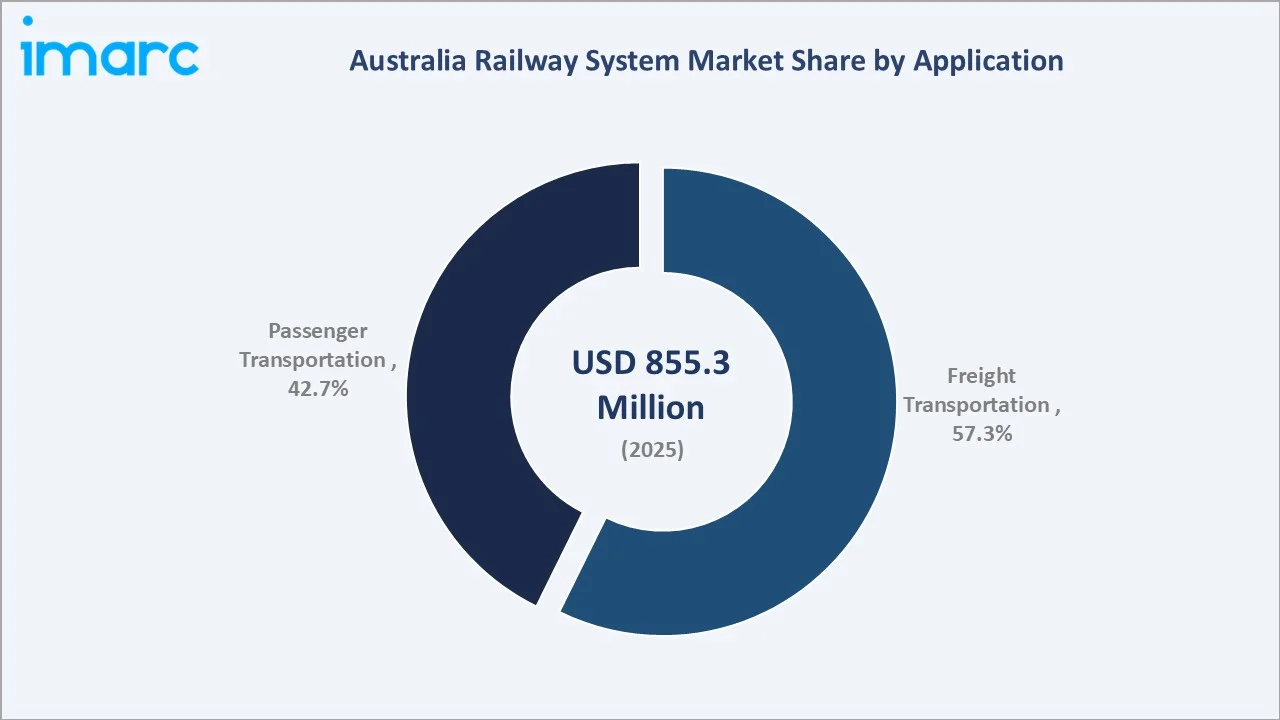

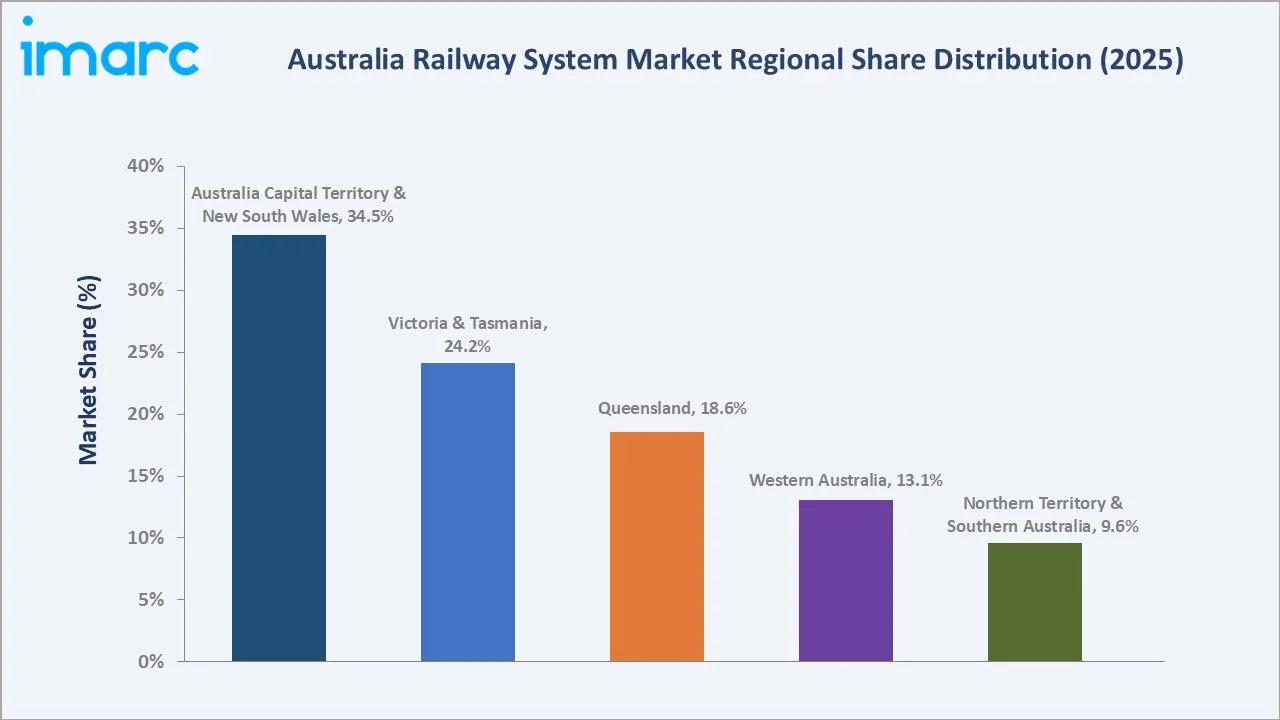

The Australia railway system market size was valued at USD 855.3 Million in 2025 and is projected to reach USD 1,152.2 Million by 2034, exhibiting a CAGR of 3.20% during the forecast period 2026-2034. Sustained government infrastructure investment, strong freight demand from Australia's resource-rich mining economy, and accelerating urban metro expansion are driving the Australia railway system market growth. Conventional leads transit type at 62.8% in 2025, while Freight Transportation dominates the application segment at 57.3%. Australia Capital Territory & New South Wales account for 34.5% of national revenue in 2025, the country's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 855.3 Million |

|

Forecast Market Size (2034) |

USD 1,152.2 Million |

|

CAGR (2026-2034) |

3.20% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Australia Capital Territory & New South Wales (34.5% share, 2025) |

|

Fastest Growing Region |

Queensland |

|

Leading Transit Type |

Conventional (62.8%, 2025) |

|

Leading Application |

Freight Transportation (57.3%, 2025) |

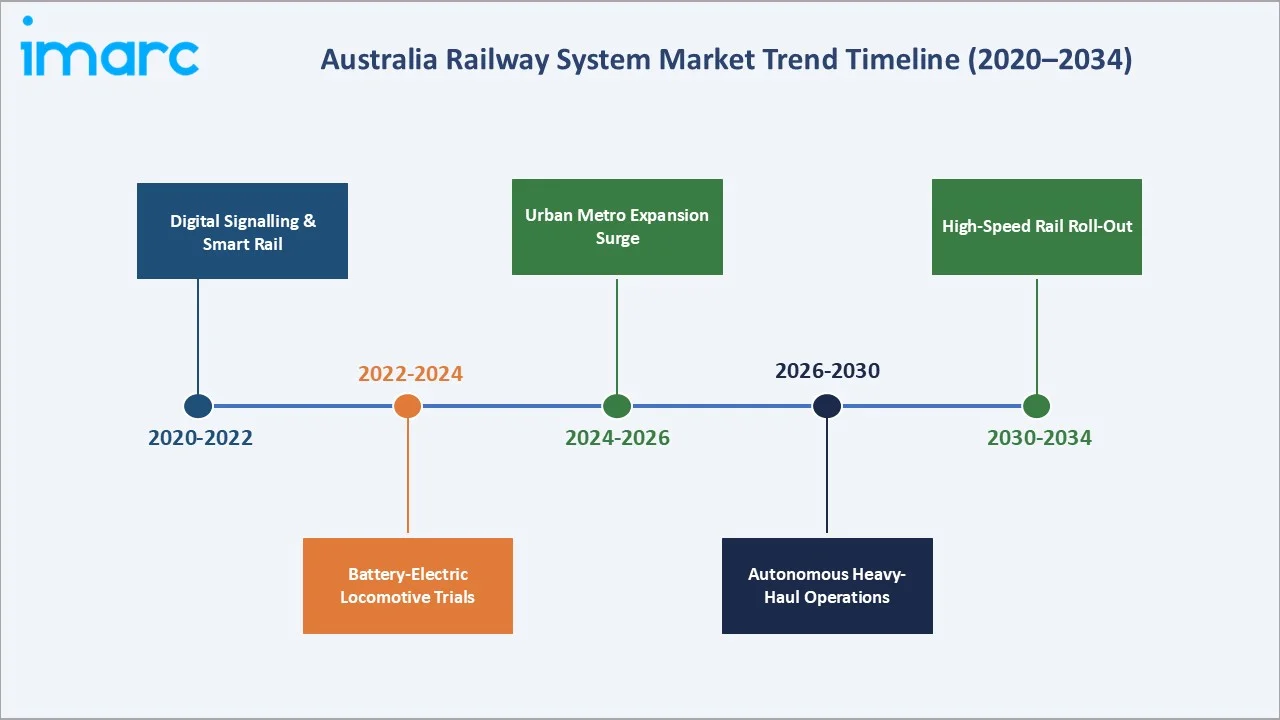

The Australia railway system market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by urban metro investment, heavy-haul freight modernisation, and progressive electrification of rolling stock across Australia's national rail corridors.

To get more information on this market, Request Sample

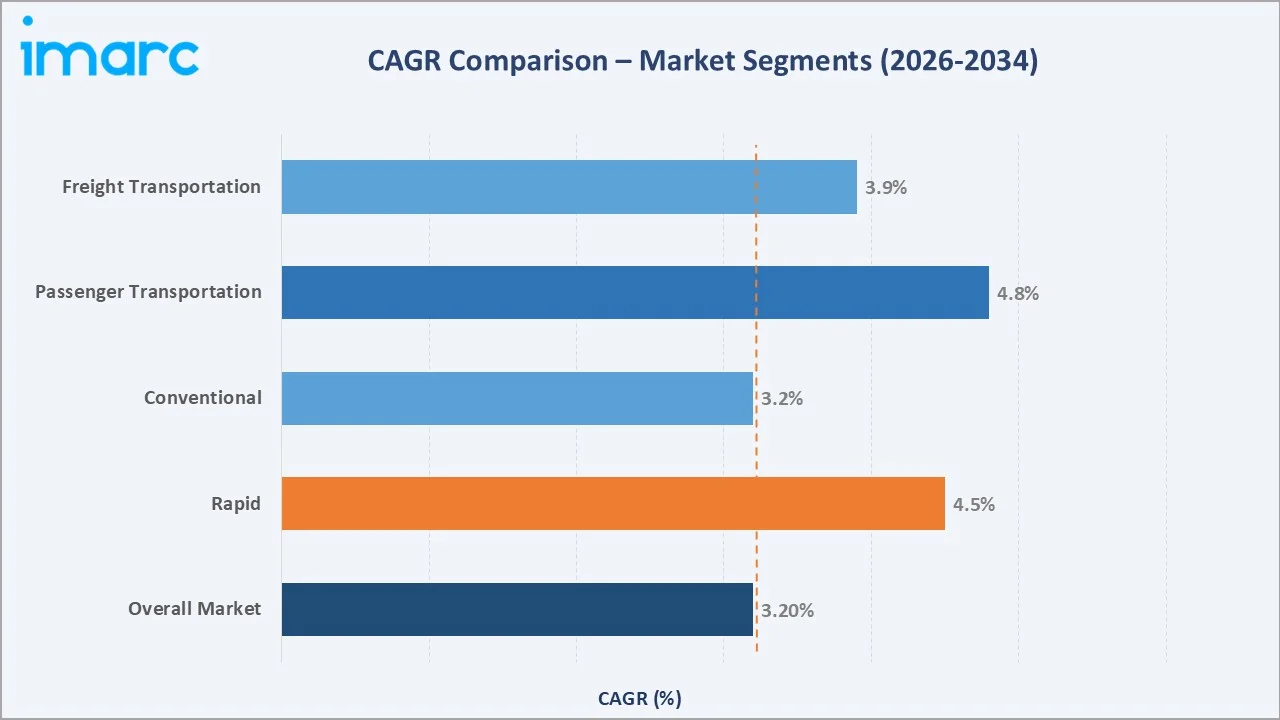

Segment-level share comparisons highlighting Conventional and Freight Transportation as the two dominant sub-categories within the Australia railway system market, alongside the faster-growing Rapid transit and Passenger Transportation segments through 2034.

Executive Summary

The Australia railway system market is undergoing a structural transformation driven by the convergence of urban population growth, decarbonisation commitments, and digital technology integration across both freight and passenger networks. Valued at USD 855.3 Million in 2025, the market is forecast to reach USD 1,152.2 Million by 2034 at a CAGR of 3.20%.

Conventional commands the dominant transit type share at 62.8% in 2025, driven by heavy-haul freight networks in the Pilbara region of Western Australia and extensive mainline passenger services across New South Wales, Victoria, and Queensland. BHP and Rio Tinto operate some of the world's most advanced autonomous heavy-haul rail systems, with axle loads among the highest recorded globally. Rapid at 37.2% is the fastest-growing segment, fuelled by urban metro expansion in Sydney, Melbourne, and Brisbane.

Australia Capital Territory & New South Wales dominate regional revenue with 34.5% in 2025, anchored by Sydney Metro and the Hunter Valley coal corridor. Victoria & Tasmania holds 24.2%, elevated by Melbourne Metro Tunnel and the Suburban Rail Loop. Queensland represents 18.6%, driven by Cross River Rail and Queensland Train Manufacturing Programme (QTMP). Western Australia, at 13.1%, is characterised by Pilbara heavy-haul intensity and Alstom's EUR 1 billion Urbalis CBTC signalling deployment. Northern Territory & Southern Australia account for 9.6%, serving the Adelaide-Darwin corridor and Eyre Peninsula freight logistics.

Key Market Insights

|

Insight |

Data |

|

Largest Transit Type |

Conventional — 62.8% share (2025) |

|

Leading Application |

Freight Transportation — 57.3% share (2025) |

|

Leading Region |

Australia Capital Territory & New South Wales — 34.5% revenue share (2025) |

|

Second Region |

Victoria & Tasmania — 24.2% revenue share (2025) |

|

Top Companies |

Aurizon, Pacific National, Alstom, Downer Group |

Key Analytical Observations Supporting the Above Data:

- Conventional with 62.8% dominance in 2025 reflects Australia's dependence on heavy-haul freight for bulk commodity export. The Pilbara iron ore network alone constitutes one of the world's highest-capacity freight rail systems by annual ton-kilometre volume.

- Freight Transportation's 57.3% share underscores Australia's status as one of the world's largest exporters of iron ore, coal, and grain — all commodity groups transported primarily by rail to coastal export ports.

- Australia Capital Territory & New South Wales's 34.5% regional dominance reflects Sydney Metro's status as Australia's largest public transport project, alongside the Hunter Valley coal corridor and ongoing intercity rolling stock modernisation programmes.

Australia Railway System Market Overview

Railway systems in Australia encompass the integrated ensemble of propulsion, signalling, safety, auxiliary power, train information, HVAC, and on-board vehicle control technologies that enable both freight and passenger trains to operate safely and efficiently across the national network. Australia's main line rail network spans approximately 35,000 kilometres — comparable to Germany's entire rail network — yet serves a vastly larger and more climatically diverse geography. System-level components are deployed across conventional diesel and electric mainline networks as well as urban rapid transit metro, light rail, and tram systems in all major capital cities.

Applications span Australia's full economic spectrum: heavy-haul freight systems serving iron ore, coal, and copper concentrate mining operations; intermodal and containerised freight connecting capital cities and port logistics hubs; intercity passenger services on the east coast; and high-frequency urban metro services in Sydney, Melbourne, Brisbane, Perth, and Adelaide. Macroeconomic enablers include Australia's export-oriented resource economy, sustained metropolitan population growth, and national decarbonisation commitments requiring rail to substitute for road freight on long-distance corridors where rail generates 16 times lower carbon intensity than road transport.

Australia’s rail market spans digital signalling, electrification, battery and hydrogen propulsion, autonomous operations, predictive maintenance, and passenger systems. Federal and state programs create a competitive environment where global Tier‑1 and local specialist firms vie for long-term, full-system contracts.

Market Dynamics

To evaluate market opportunities, Request Sample

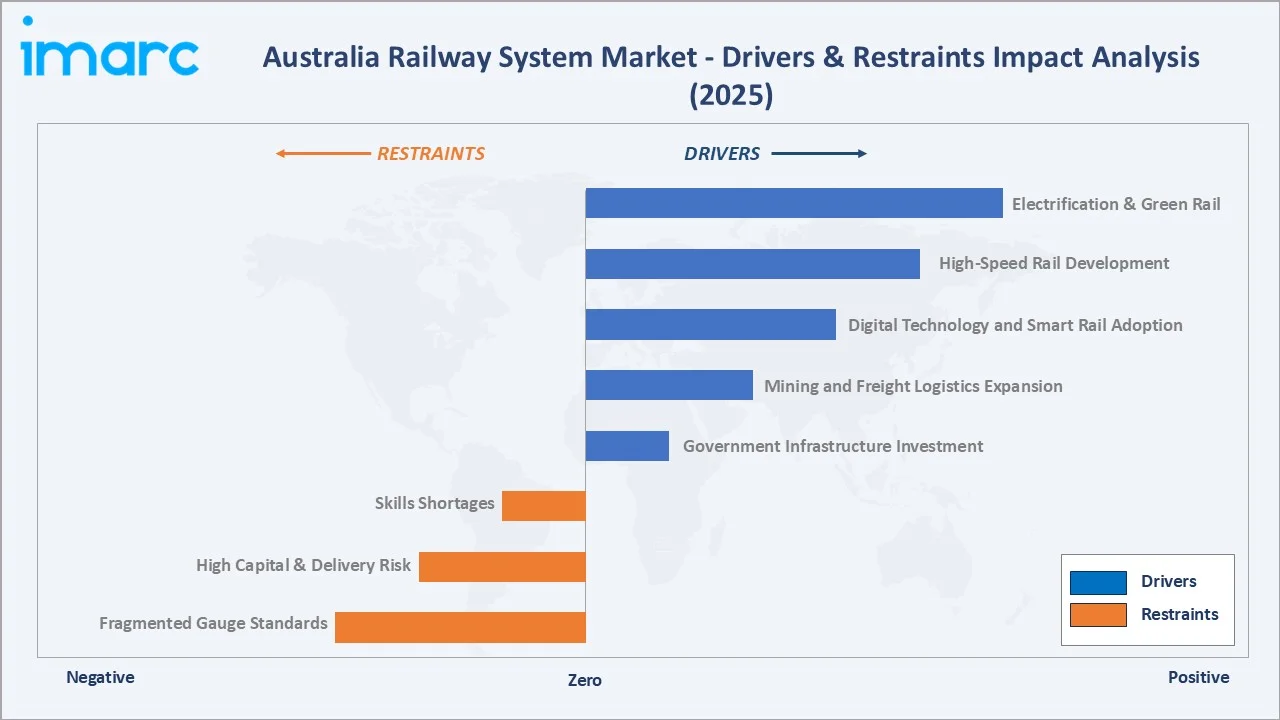

Market Drivers

- Government Infrastructure Investment: The Australian Government committed USD 670.4 million to the ARTC rail network in May 2024 as part of its four-year Infrastructure Investment Program. AUD 14.5 billion has been committed to Inland Rail alone, and the ARA confirmed AUD 132 billion in total rail construction and maintenance activity over the decade to 2025, creating sustained demand for railway system components and services.

- Mining and Freight Logistics Expansion: Australia's status as the world's leading iron ore exporter and a top-three metallurgical coal supplier sustains structural freight rail demand. The Inland Rail project will add capacity for 2 million tonnes of agricultural freight annually.

- Digital Technology and Smart Rail Adoption: Deployment of IoT-enabled predictive maintenance, autonomous train monitoring, and digital CBTC signalling systems is improving network efficiency at scale. In July 2024, Alstom and DT Infrastructure signed a EUR 1 billion Urbalis CBTC contract for Western Australia — the largest digital signalling programme in Australian railway history.

Market Restraints

- Fragmented Gauge Standards: Multiple track gauges (standard, broad, narrow) limit interoperability, increase maintenance costs, and reduce network efficiency.

- High Capital & Delivery Risk: Large-scale projects face cost overruns and delays—evidenced by the Cross River Rail three-year delay due to budget pressures and industrial action.

- Skills Shortages: Ongoing gaps in engineering, signalling, and project management talent (per Australasian Railway Association) are constraining project delivery amid peak construction demand.

Market Opportunities

- High-Speed Rail Development: The Federal Government has committed ~AUD 660 million (2026) to advance high-speed rail, with the High Speed Rail Authority initiating early-stage corridor planning—unlocking a long-term pipeline for advanced rail systems.

- Electrification & Green Rail: Australia’s 43% emissions reduction target by 2030 is accelerating rail electrification. Investments by Aurizon (low-emission traction) and Fortescue (battery-electric locomotives) are driving demand for sustainable rail technologies.

- Brisbane 2032 Olympics: The 2032 Brisbane Olympic and Paralympic Games are catalysing major rail upgrades, including Cross River Rail, faster intercity links, and new EMU fleet deployments, supporting multi-billion-dollar transit investment.

Market Challenges

- Interoperability and Standardisation: The absence of uniform national railway system standards for signalling, communications, and rolling stock specifications complicates multi-state project delivery and limits scale economies in procurement and maintenance contract structuring.

- Construction Cost Inflation: Rising input costs for steel, labour, and specialised components have increased project capital requirements, challenging budget assumptions in programmes approved before the 2021-2024 inflationary cycle and causing delays and scope revisions in several state rail projects.

Emerging Market Trends

1. Digital Signalling and Communications-Based Train Control (CBTC) Deployment

Australia is moving from legacy fixed-block signalling to CBTC and ETCS, boosting train frequency, safety, and real-time control. Major Alstom programs and Sydney’s FRMCS upgrade are driving large-scale digital modernisation of urban rail networks.

2. Battery-Electric and Hydrogen Propulsion Replacing Diesel on Freight Corridors

Decarbonisation of rail is accelerating, particularly on non-electrified freight corridors where diesel has traditionally dominated. Fortescue has introduced battery-electric heavy-haul locomotives in partnership with Progress Rail, demonstrating the viability of large-scale energy storage in rail applications. Meanwhile, Aurizon is investing approximately AUD 350 million in low-emission traction technologies to reduce fleet emissions. Hydrogen-powered train trials are also underway in New South Wales, supported by global manufacturers such as CAF and Alstom, signalling a broader shift toward alternative propulsion technologies.

3. Autonomous Train Operation Expansion in Heavy-Haul Freight

Australia leads in autonomous freight rail, especially in mining regions. Rio Tinto and BHP are advancing driverless operations, while autonomous and AI-enabled logistics are being explored on major corridors like Inland Rail to boost efficiency and competitiveness.

4. Urban Metro Expansion and Transit-Oriented Development

Large-scale metro and rail infrastructure projects are transforming Australia’s urban transport landscape. The Melbourne Metro Tunnel, opened in November 2025, has significantly increased cross-city capacity and operational efficiency. Concurrently, projects such as Sydney Metro West and Brisbane’s Cross River Rail are advancing, alongside broader Faster Rail initiatives. Collectively, New South Wales, Victoria, and Queensland account for the vast majority of public rail investment through 2030, underscoring strong government commitment to expanding high-capacity urban transit systems and supporting transit-oriented development.

5. Predictive Maintenance and Digital Twin Integration

Rail operators in Australia are increasingly deploying IoT-based predictive maintenance and digital twins to improve reliability and reduce downtime. The Australian Rail Track Corporation uses condition monitoring for early fault detection, while Queensland Rail is piloting AI-driven asset analytics. Adelaide has adopted IVU.rail for fully digital operations, and industry platforms like AusRAIL PLUS highlight a growing focus on ETCS and predictive maintenance, with Hitachi Rail actively expanding in this space.

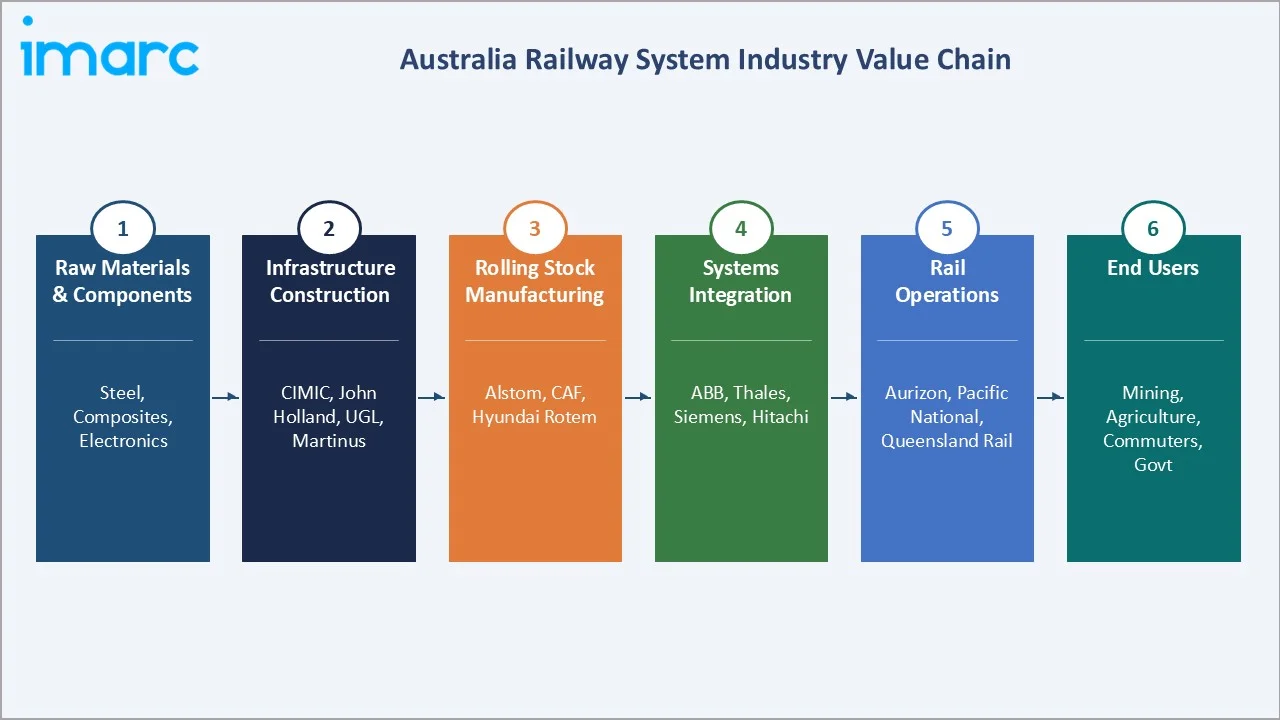

Industry Value Chain Analysis

The Australia railway system value chain spans five integrated stages from raw materials supply through end-user service delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements aligned with Australia's unique geographic and operational demands.

|

Stage |

Key Players / Examples |

Primary Function |

|

Raw Materials & Components |

BlueScope Steel, Boral, Wabtec, Knorr-Bremse |

Rails, sleepers, wheels, brakes, electronics |

|

Infrastructure Construction |

CIMIC Group, John Holland, CPB Contractors, Martinus |

Civil works, tunnelling, track laying, viaducts |

|

Rolling Stock & Systems Manufacturing |

Alstom, Hyundai Rotem, CAF, ABB, Thales, Siemens |

Trains, CBTC signalling, traction, control systems |

|

Rail Operations & Maintenance |

Aurizon, Pacific National, Progress Rail |

Freight haulage, passenger services, rolling stock O&M |

|

End Users |

BHP, Rio Tinto, Glencore, State Govts, Commuters |

Mining logistics, passenger travel, freight shippers |

Tier-1 rolling stock and systems manufacturers lead the value chain by delivering integrated, turnkey train solutions across propulsion, signalling, and safety systems. However, rising local content mandates are shifting value toward domestic manufacturing—evidenced by ABB’s traction facility in Maryborough and Vossloh’s turnout plant in Bendigo—thereby increasing entry barriers for import-dependent players.

Technology Landscape in the Australia Railway System Industry

Signalling and Train Control Systems

Australia’s rail signalling is split between legacy relay-based systems and modern CBTC/ETCS deployments on urban and mainline networks. Major programmes like Alstom’s Urbalis CBTC in Western Australia and Sydney Trains’ transition to FRMCS are driving a widespread digital upgrade.

Propulsion and Electrification

Rail propulsion spans diesel, electric, battery-electric, and hydrogen. Alstom and ABB lead conventional electric and EMU deployments, while battery-electric locomotives from Aurizon and Fortescue are shaping the next generation of freight traction.

Autonomous Operations and AI-Driven Analytics

Australia is a global leader in autonomous freight operations, exemplified by Rio Tinto’s AutoHaul network. AI-driven predictive maintenance and digital twins are increasingly deployed by ARTC, Queensland Rail, and system suppliers like Siemens, Thales, and Hitachi Rail, reflecting a shift toward data-driven, automated network management.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Transit Type |

Conventional |

62.8% |

2025 |

|

System Type |

🔒 |

🔒 |

2025 |

|

Application |

Freight Transportation |

57.3% |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

34.5% |

2025 |

By Transit Type

To access detailed market analysis, Request Sample

Conventional commands a 62.8% majority share in 2025, reflecting the structural dominance of heavy-haul freight and mainline intercity passenger services across Australia's vast network. The segment encompasses diesel, electric, and electro-diesel locomotive traction, as well as standard passenger coaches on intercity and regional services.

Rapid at 37.2% in 2025 is the fastest-growing sub-segment, driven by urban metro expansion across Sydney, Melbourne, Brisbane, and Perth.

By Application

Freight Transportation accounts for 57.3% of the Australia railway system market in 2025, underpinned by Australia's resource export economy and the structural cost advantage of rail over road for bulk long-distance haulage.

Passenger Transportation at 42.7% in 2025 is receiving disproportionate capital investment relative to its current revenue share, as governments prioritise urban congestion reduction and decarbonisation. In March 2024, ABB secured a USD 150 million traction contract with Hyundai Rotem for 65 new Queensland passenger trains, with service commencement targeted for the Brisbane 2032 Olympics.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Australia Capital Territory & New South Wales |

34.5% |

Sydney Metro, Hunter Valley coal rail, New South Wales intercity rolling stock renewal |

|

Victoria & Tasmania |

24.2% |

Melbourne Metro Tunnel, Suburban Rail Loop, Alstom G Class tram fleet |

|

Queensland |

18.6% |

Cross River Rail, QTMP rolling stock, Logan & Gold Coast Faster Rail, 2032 Olympics |

|

Western Australia |

13.1% |

Pilbara heavy-haul, Alstom C-series EMU, EUR 1B Urbalis CBTC programme |

|

Northern Territory & Southern Australia |

9.6% |

Adelaide-Darwin corridor, Eyre Peninsula freight, regional rail investment |

Australia Capital Territory & New South Wales lead all regional markets with a 34.5% share in 2025. This is driven by Sydney Metro, the country’s largest automated rail project, expanding network capacity and enabling modal shift. Vossloh has supplied key track components, while SYSTRA is supporting Sydney’s transition to FRMCS-based communications, modernising train-ground systems across the network.

Victoria & Tasmania holds 24.2%, elevated by Melbourne Metro Tunnel's November 2025 opening — creating a new cross-city underground backbone enabling trains every minute on the Sunbury-Cranbourne/Pakenham axis. Queensland at 18.6% is driven by the Brisbane 2032 Olympic catalyst: Cross River Rail (Pimpama station opened October 2025), Logan & Gold Coast Faster Rail (construction commenced March 2026), and QTMP's 65 new six-car EMUs. Western Australia, at 13.1%, is defined by Pilbara heavy-haul intensity and the EUR 1 billion Urbalis CBTC deployment. Northern Territory & Southern Australia (9.6%) serves the Adelaide-Darwin corridor and Eyre Peninsula grain freight, with targeted federal investment in regional rail upgrades under the Infrastructure Investment Program.

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Aurizon Holdings Limited |

Aurizon Freight / AutoHaul |

Leader |

Largest ASX-listed rail freight operator; coal, iron ore, intermodal |

|

Pacific National Group |

Pacific National Freight |

Leader |

Largest private freight operator; 30% of national freight by rail |

|

Alstom SA |

Urbalis CBTC |

Leader |

Rolling stock, signalling; EUR 1B WA CBTC contract |

|

Downer Group |

Downer Rail |

Challenger |

Infrastructure maintenance; QLD Rail rolling stock contracts |

|

CIMIC Group |

CPB Contractors |

Challenger |

Civil rail construction, tunnelling, and station development |

|

SCT Opco Pty Ltd. |

SCT Logistics Rail |

Challenger |

Intermodal: Melbourne-Perth and Melbourne-Brisbane corridors |

|

Progress Rail |

EMD Locomotives / Heavy‑Haul Solutions |

Challenger |

Global rolling stock OEM with Australian operations for heavy‑haul locomotives, fleet maintenance, and overhaul. |

The Australia railway system competitive landscape is characterised by a concentrated freight operations duopoly (Aurizon and Pacific National), state-owned passenger operators, and internationally competitive rolling stock and systems supply. Multinationals such as Alstom, ABB, Siemens, Thales, and Hitachi Rail compete with local firms for major contracts. Australian Industry Participation (AIP) mandates are increasingly shifting the advantage toward players with local manufacturing footprints, raising barriers for import-only suppliers.

Key Company Profiles

Aurizon Holdings Limited

Aurizon is Australia’s largest rail freight operator, moving coal, iron ore, grain, and intermodal cargo nationwide. Established as QR National in 2010 and rebranded in 2012, it combines below-rail infrastructure in Queensland with extensive above-rail haulage operations.

- Product & Service Portfolio: Coal haulage (Bowen Basin, Hunter Valley), iron ore transport, intermodal containerised freight, bulk commodity logistics (grain, fertiliser, minerals), freight terminal operations, and below-rail infrastructure management in Queensland.

- Recent Developments: In November 2025, Aurizon signed a three-year agreement with SCT Logistics to increase containerised freight frequency on the Brisbane–Sydney–Melbourne corridor.

- Strategic Focus: Aurizon’s strategy focuses on defending bulk haulage contracts, expanding intermodal market share, and decarbonising its freight fleet with battery-electric and alternative-fuel locomotives, positioning itself as the preferred partner for ESG-focused mining clients.

Alstom SA

Alstom is a leading global rolling stock and signalling provider, headquartered in France. In Australia, it has a strong local presence, supplying metro trains, light rail vehicles, and CBTC systems across multiple states, supported by extensive manufacturing, delivery, and maintenance operations employing thousands locally.

- Product & Platform Portfolio: C-series electric multiple units (Western Australia), Urbalis CBTC signalling system, X'Trapolis metro trains, Citadis tram series (Melbourne's G Class trams), Coradia regional trains, Healthhub predictive maintenance platform.

- Recent Developments: In April 2024, Alstom delivered its first locally built C-series EMU to Western Australia under a major rolling stock contract.

- Strategic Focus: Alstom’s Australian strategy focuses on CBTC and digital signalling leadership, localising rolling stock to meet government content requirements, and securing long-term maintenance contracts for lifecycle revenue.

Downer Group

Downer Group delivers end-to-end rail services in Australia, spanning design, construction, rolling stock, and maintenance across the full asset lifecycle.

- Product & Service Portfolio: Rail infrastructure construction and maintenance, rolling stock engineering and refurbishment, asset management services, digital maintenance diagnostics, hybrid locomotive solutions, and technical advisory services for rail operators.

- Recent Developments: In June 2023, Downer was awarded the contract to deliver the Queensland Train Manufacturing Program (QTMP).

- Strategic Focus: Downer’s rail strategy targets long-term public-sector maintenance contracts for stable revenue, complemented by rolling stock supply and engineering services, with diesel hybridisation and digital maintenance as key differentiators.

Market Concentration Analysis

Australia’s rail market shows moderate to high concentration. Freight operations are dominated by a duopoly—Aurizon and Pacific National—with strong entry barriers from long-term haulage contracts, specialised fleets, and network access rights.

In contrast, the systems and technology segment is globally competitive and fragmented, with players like Alstom, Siemens, Thales, ABB, and Hitachi Rail competing for large contracts. Local content mandates (AIP) are increasingly shifting the advantage toward firms with Australian manufacturing footprints, raising barriers for import-only suppliers.

Investment & Growth Opportunities

Fastest-Growing Segments

Urban metro and light rail are the fastest-growing segments, driven by multi-billion-dollar projects across major cities. Digital signalling and CBTC lead technology growth, while battery-electric and hydrogen propulsion are emerging, supported by funding from the Australian Renewable Energy Agency and industry decarbonisation goals.

Emerging Market Expansion

High-speed rail (HSR) is the largest future opportunity, backed by federal development funding and long-term procurement plans. Additionally, critical minerals logistics is driving new heavy-haul rail demand across resource-rich regions.

Venture & Government Investment Trends

Governments have committed ~AUD 132B to rail over the past decade, with increasing use of PPP models (e.g., Suburban Rail Loop, Inland Rail). Investment is also rising in battery-electric traction and digital analytics, creating a parallel rail-tech innovation ecosystem.

Future Market Outlook (2026-2034)

The Australia railway system market forecast projects steady value expansion from USD 855.3 Million in 2025 to USD 1,152.2 Million by 2034 at a CAGR of 3.20% — a market value increase of USD 296.9 Million underpinned by continued government infrastructure commitment, fleet electrification, and digital technology adoption across both freight and passenger rail.

Three key technology shifts will reshape Australia’s rail market through 2034. First, the transition from diesel to electric and battery-electric propulsion will drive demand for electrification and power systems. Second, large-scale adoption of CBTC and ETCS signalling will trigger a multi-billion-dollar upgrade cycle from legacy systems. Third, the rollout of high-speed rail in New South Wales, backed by federal development funding, will create a new market segment for specialised rail systems.

By 2034, the market will be more digital, electrified, and automated, with a competitive advantage favouring suppliers that localise manufacturing, secure long-term maintenance contracts, and align with both freight and urban transit demand driven by population growth, decarbonisation, and resource exports.

Research Methodology

Primary Research

Primary research included interviews with state rail project directors, transport agency procurement managers, Tier-1 supplier engineers, mining freight managers, and industry association representatives, validating market size, segment shares, investment trends, and competitive dynamics for 2020–2025 and 2026–2034.

Secondary Research

Secondary sources include the Australasian Railway Association (ARA) Annual Procurement Pipeline Report 2025, Infrastructure Australia investment programme data, ARTC annual reports, Australian Bureau of Statistics transport statistics, Department of Infrastructure Transport and Regional Development publications, company annual reports (Aurizon Holdings, Pacific National, Downer Group, Alstom SA), Railway Gazette International, Global Railway Review, AusRAIL PLUS 2025 conference proceedings, and state government transport capital budget papers from New South Wales, Victoria, Queensland, Western Australia, and South Australia.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models incorporating infrastructure investment pipeline data, historical market evolution patterns, GDP growth correlations, urbanisation indices, and commodity export volume forecasts from major Australian resource producers. Scenario analysis across base, optimistic, and conservative cases was performed to account for project delivery timing risk, commodity price sensitivity, and macroeconomic uncertainty over the 2026-2034 forecast horizon.

Australia Railway System Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Transit Types Covered |

|

| System Types Covered | Auxiliary Power System, Train Information System, Propulsion System, Train Safety System, HVAC System, On-Board Vehicle Control |

| Applications Covered | Freight Transportation, Passenger Transportation |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Aurizon Holdings Limited, Pacific National Group, Alstom SA, Downer Group, CIMIC Group, SCT Opco Pty Ltd., Progress Rail, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia railway system market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia railway system market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia railway system industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Railway System Market Report

The Australia railway system market was valued at USD 855.3 Million in 2025, driven by sustained government infrastructure investment and strong freight rail demand from Australia's resource export economy.

The market is projected to reach USD 1,152.2 Million by 2034, growing at a CAGR of 3.20% during 2026-2034, driven by urban metro expansion, Inland Rail freight corridor completion, digital CBTC signalling deployment, and rolling stock electrification programmes.

Conventional leads with a 62.8% share in 2025, driven by extensive heavy-haul freight networks in Western Australia and Queensland, as well as mainline intercity and regional passenger services across New South Wales and Victoria.

Freight Transportation accounts for 57.3% of the market in 2025, reflecting Australia's role as one of the world's largest exporters of iron ore, metallurgical coal, and agricultural bulk commodities — all reliant on rail for cost-effective long-distance haulage to coastal export ports.

Australia Capital Territory & New South Wales lead with 34.5% of the market in 2025, anchored by Sydney Metro — Australia's largest public transport project — alongside the Hunter Valley coal haulage corridor and the New South Wales intercity rolling stock renewal programme.

Key drivers include government infrastructure investment (USD 670.4 million ARTC commitment, May 2024), mining and freight logistics expansion (81 critical minerals projects valued at USD 30-42 billion), and digital technology adoption, including CBTC signalling, autonomous train operation, and predictive maintenance analytics deployment at network scale.

Leading companies include Aurizon Holdings Limited, Pacific National Group, Alstom SA, Downer Group, CIMIC Group, SCT Opco Pty Ltd., and Progress Rail.

Inland Rail is a 1,700-kilometre double-stack freight corridor connecting Melbourne and Brisbane, with AUD 14.5 billion in committed federal funding. It will remove 108 B-double trucks per train journey from national roads and add 2 million tonnes of agricultural freight capacity annually, generating sustained demand for railway system components and services along its entire corridor.

Electrification is reshaping rolling stock procurement and railway power systems demand. Alstom's C-series EMU delivery (USD 845 million, April 2024), Aurizon's AUD 350 million low-emission traction programme, and Fortescue's 14.5 MWh battery-electric heavy-haul locomotive commissioning exemplify the propulsion technology transition underway across both passenger and freight railway networks.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)