Australia Respiratory Syncytial Virus Diagnostics Market Size, Share, Trends and Forecast by Product, End Use, and Region, 2026-2034

Australia Respiratory Syncytial Virus Diagnostics Market Summary:

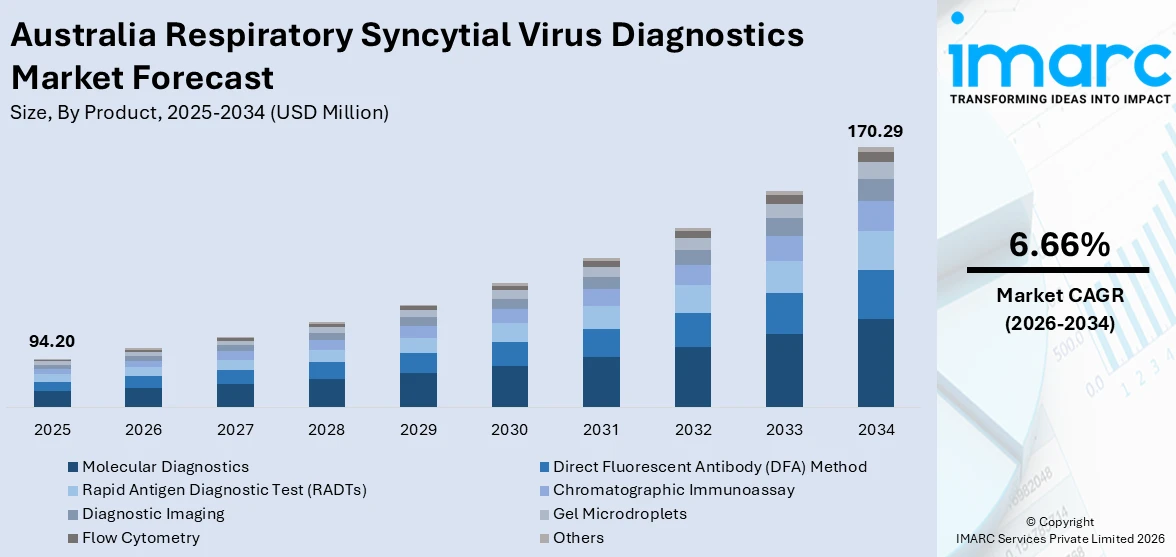

The Australia respiratory syncytial virus diagnostics market size was valued at USD 94.20 Million in 2025 and is projected to reach USD 170.29 Million by 2034, growing at a compound annual growth rate of 6.66% from 2026-2034.

The market expansion reflects heightened clinical emphasis on accurate respiratory pathogen identification amid increased seasonal RSV burden across Australian healthcare facilities. Molecular diagnostic platforms continue gaining preference among tertiary care centers and pediatric units due to superior sensitivity and rapid turnaround capabilities. Public health initiatives promoting early RSV detection in vulnerable infant populations and immunocompromised adults further accelerate testing volumes nationwide. Growing integration of multiplex assay technologies within laboratory workflows and emergency departments enhances operational efficiency while supporting timely clinical intervention and infection control protocols across Australia respiratory syncytial virus diagnostics market share.

Key Takeaways and Insights:

- By Product: Molecular diagnostics dominates the market with a share of 39.8% in 2025, owing to superior sensitivity and specificity in detecting RSV nucleic acids, widespread adoption in hospital laboratories for definitive pathogen identification, and ability to differentiate RSV subtypes for enhanced clinical decision-making.

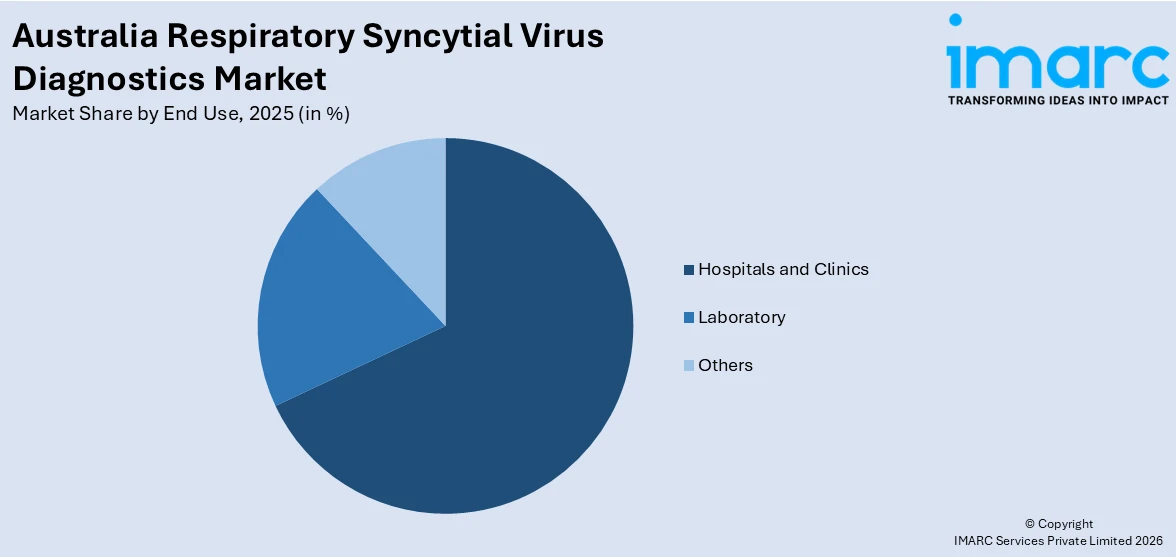

- By End Use: Hospitals and clinics lead the market with a share of 68.2% in 2025, driven by high RSV-associated hospitalization rates among infants and elderly populations requiring immediate diagnostic confirmation, comprehensive laboratory infrastructure supporting high-volume testing workflows, and integration with electronic medical record systems facilitating coordinated patient management.

- By Region: Australia Capital Territory & New South Wales is the largest region with 34.6% share in 2025, reflecting substantial population concentration across Sydney metropolitan and regional health districts, extensive tertiary pediatric hospital networks with specialized respiratory diagnostic capabilities, and established public health surveillance systems monitoring seasonal RSV epidemiology.

- Key Players: Key players drive the Australia respiratory syncytial virus diagnostics market by introducing innovative multiplex molecular assay platforms, expanding point-of-care testing solutions for emergency departments, and strengthening partnerships with pathology networks. Their investments in regulatory compliance, quality assurance programs, and clinical validation studies enhance product credibility while supporting widespread adoption across public and private healthcare sectors.

To get more information on this market Request Sample

The Australian diagnostic landscape increasingly prioritizes rapid molecular platforms capable of concurrent respiratory pathogen detection, driven by evolving clinical guidelines emphasizing early RSV identification in high-risk demographics. Government-funded immunization programs targeting infants through monoclonal antibody prophylaxis and maternal vaccination initiatives amplify diagnostic testing demand as clinicians seek to differentiate vaccine-preventable RSV disease from other respiratory infections. Healthcare facilities nationwide are expanding point-of-care molecular testing capabilities within emergency departments to expedite triage decisions and reduce unnecessary antibiotic prescribing. The integration of automated nucleic acid extraction systems and real-time PCR technology within hospital laboratory workflows continues enhancing operational efficiency while supporting Australia's broader respiratory surveillance infrastructure.

Australia Respiratory Syncytial Virus Diagnostics Market Trends:

Multiplex Molecular Diagnostic Platforms Gaining Dominance

Healthcare facilities across Australia are increasingly adopting multiplex molecular diagnostic platforms capable of simultaneously detecting multiple respiratory pathogens including RSV, influenza viruses, and SARS-CoV-2 from single patient specimens. These syndromic testing panels reduce diagnostic uncertainty during seasonal respiratory illness peaks while optimizing laboratory workflow efficiency through consolidated sample processing. In June 2024, Roche Diagnostics received FDA Emergency Use Authorization for its cobas liat SARS-CoV-2, Influenza A/B & RSV nucleic acid test, an automated multiplex real-time PCR assay producing results in just 20 minutes using a single nasopharyngeal or anterior nasal-swab sample. The technology's integration within emergency departments and urgent care facilities enables rapid clinical decision-making whilst minimizing patient waiting times.

Expansion of Point-of-Care Testing in Emergency and Urgent Care Settings

Point-of-care molecular diagnostic solutions are experiencing widespread deployment across Australian emergency departments and urgent care centers, driven by clinical demand for rapid RSV detection supporting immediate treatment decisions and infection control measures. These compact, user-friendly platforms eliminate central laboratory dependencies whilst delivering molecular-grade accuracy within near-patient care environments. In September 2024, Roche launched the Cobas Respiratory Flex test using proprietary TAGS technology to detect up to 15 pathogens including SARS-CoV-2, influenza A/B, and RSV in a single PCR test. The technology facilitates early RSV identification in vulnerable populations whilst supporting antimicrobial stewardship initiatives through definitive viral pathogen confirmation.

Rising Integration of Artificial Intelligence in Diagnostic Workflows

Australian pathology laboratories are incorporating artificial intelligence-enabled diagnostic software to enhance RSV test result interpretation accuracy whilst accelerating analytical workflows through automated quality control and anomaly detection capabilities. AI-driven platforms analyze molecular assay data patterns, flag potential interferences, and provide decision support for complex cases requiring specialist review. Advanced diagnostic software systems streamline result validation processes, enabling higher daily testing throughput whilst maintaining rigorous quality assurance standards across laboratory operations. These technological advancements support Australia's expanding respiratory surveillance programs whilst addressing workforce capacity constraints affecting public pathology networks during peak seasonal demand periods, facilitating sustained diagnostic service delivery.

Market Outlook 2026-2034:

The Australia respiratory syncytial virus diagnostics market demonstrates robust growth trajectory driven by expanding molecular testing infrastructure across metropolitan and regional healthcare facilities, sustained RSV disease burden necessitating enhanced diagnostic capabilities, and ongoing government investment in respiratory pathogen surveillance systems. The market generated a revenue of USD 94.20 Million in 2025 and is projected to reach a revenue of USD 170.29 Million by 2034, growing at a compound annual growth rate of 6.66% from 2026-2034. Healthcare sector focus on reducing pediatric RSV hospitalization rates through earlier diagnostic intervention, coupled with advancing point-of-care molecular technologies offering rapid turnaround capabilities, positions the market for sustained expansion throughout the forecast period. Integration of comprehensive respiratory panels within emergency medicine protocols and growing emphasis on antimicrobial stewardship through definitive viral pathogen identification further support positive market dynamics.

Australia Respiratory Syncytial Virus Diagnostics Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product |

Molecular Diagnostics |

39.8% |

|

End Use |

Hospitals and Clinics |

68.2% |

|

Region |

Australia Capital Territory & New South Wales |

34.6% |

Product Insights:

- Direct Fluorescent Antibody (DFA) Method

- Rapid Antigen Diagnostic Test (RADTs)

- Molecular Diagnostics

- Chromatographic Immunoassay

- Diagnostic Imaging

- Gel Microdroplets

- Flow Cytometry

- Others

Molecular diagnostics dominates with a market share of 39.8% of the total Australia respiratory syncytial virus diagnostics market in 2025.

Molecular diagnostic platforms represent the gold standard for RSV detection across Australian healthcare facilities due to exceptional analytical sensitivity capable of identifying minimal viral nucleic acid quantities in clinical specimens. These assays utilize real-time polymerase chain reaction technology to amplify and detect RSV-specific genetic sequences, providing definitive pathogen identification within hours rather than days required by traditional culture methods. The platforms' ability to differentiate RSV subtypes supports enhanced epidemiological surveillance while enabling clinicians to correlate specific viral strains with disease severity patterns. Leading manufacturers continue introducing fully automated RSV detection systems and multiplex PCR platforms integrating simultaneous multi-pathogen analysis capabilities.

Advanced molecular diagnostic systems increasingly incorporate automated nucleic acid extraction modules eliminating manual specimen processing steps while reducing contamination risks and operator-dependent variability. These integrated platforms streamline laboratory workflows from sample introduction through result reporting, enabling high-volume testing capacity essential during peak RSV seasonal activity when Australian pediatric facilities experience substantial diagnostic demand surges. Quantitative molecular assays additionally provide viral load measurements supporting clinical prognosis assessment and treatment monitoring in severe RSV cases requiring intensive care management. The technology's compatibility with comprehensive respiratory pathogen panels allows simultaneous detection of multiple viral and bacterial respiratory pathogens, facilitating differential diagnosis in complex clinical presentations while optimizing antimicrobial therapy selection through definitive etiological identification.

End Use Insights:

Access the comprehensive market breakdown Request Sample

- Hospitals and Clinics

- Laboratory

- Others

Hospitals and clinics lead with a share of 68.2% of the total Australia respiratory syncytial virus diagnostics market in 2025.

Australian hospitals and clinics constitute the primary RSV diagnostic testing venues driven by substantial pediatric and geriatric inpatient populations experiencing severe respiratory complications requiring immediate pathogen identification for appropriate clinical management. Emergency departments across major metropolitan teaching hospitals maintain comprehensive respiratory diagnostic capabilities including rapid molecular testing platforms supporting urgent triage decisions and infection control implementation. National health surveillance data highlights the significant disease burden associated with RSV hospitalizations, particularly among infant populations, necessitating robust hospital-based diagnostic infrastructure. Tertiary pediatric centers implement specialized RSV testing protocols for immunocompromised patients and neonatal intensive care units where early detection critically influences isolation procedures and targeted antiviral consideration.

Hospital laboratory services provide comprehensive RSV diagnostic portfolios encompassing rapid antigen detection for initial screening, confirmatory molecular assays for definitive identification, and specialized serology testing supporting retrospective diagnosis and epidemiological investigations. These facilities maintain rigorous quality assurance programs aligned with national accreditation standards while participating in respiratory surveillance networks coordinated through government health initiatives. General practice clinics increasingly deploy point-of-care RSV testing solutions enabling same-visit diagnosis and treatment planning, particularly beneficial for regional and remote communities with limited pathology service accessibility. Integration of electronic medical record systems facilitates seamless test ordering, result reporting, and clinical decision support across hospital networks while supporting population health analytics identifying geographic and temporal RSV transmission patterns.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales exhibits a clear dominance with a 34.6% share of the total Australia respiratory syncytial virus diagnostics market in 2025.

Australia Capital Territory & New South Wales maintains substantial RSV diagnostic market presence reflecting extensive metropolitan health infrastructure concentrated across Sydney metropolitan area and surrounding regional health districts serving Australia's most populous state. Major tertiary pediatric facilities operate specialized respiratory diagnostic laboratories with advanced molecular testing capabilities supporting high-volume RSV surveillance programs. The region's dense concentration of teaching hospitals, research institutions, and diagnostic pathology networks creates comprehensive testing infrastructure addressing diverse clinical needs across urban and regional populations. State government health departments implement coordinated respiratory illness monitoring systems requiring standardized diagnostic protocols, driving consistent testing demand throughout seasonal activity periods. Well-established referral pathways connecting primary care providers with specialist diagnostic services facilitate timely pathogen identification supporting clinical decision-making.

The combined territories benefit from substantial healthcare funding allocations supporting diagnostic service expansion, workforce development programs, and technology acquisition initiatives enhancing laboratory capabilities. Academic medical centers within the region conduct extensive clinical research requiring robust diagnostic infrastructure for patient recruitment, disease surveillance, and treatment outcome monitoring. Geographic positioning encompasses diverse demographic profiles including high birth rates in metropolitan suburbs generating significant pediatric diagnostic demand, alongside aging populations in coastal regions requiring geriatric respiratory illness management. Comprehensive public health surveillance networks coordinated through state health authorities maintain continuous RSV epidemiological monitoring, necessitating sustained diagnostic testing capacity across hospital, community, and reference laboratory settings supporting population health management objectives.

Market Dynamics:

Growth Drivers:

Why is the Australia Respiratory Syncytial Virus Diagnostics Market Growing?

Escalating RSV Infection Burden Across Vulnerable Demographics

Australia experienced unprecedented RSV disease burden during recent years driven by post-pandemic immune debt phenomena following reduced viral circulation during COVID-19 public health measures implementation. The nation recorded substantial increases in annual RSV cases, representing the highest totals since RSV became nationally notifiable, with significant proportions occurring among young children. This substantial increase in pediatric RSV infections overwhelmed hospital emergency departments and pediatric wards nationwide, necessitating enhanced diagnostic capacity to support clinical triage decisions and infection control protocols. Infant hospitalization rates associated with RSV remained significantly elevated compared to pre-pandemic baseline levels, with intensive care admissions requiring mechanical ventilation support placing considerable strain on tertiary pediatric facilities. National health surveillance data highlights persistent disease burden driving sustained diagnostic testing demand across neonatal and pediatric care settings. Elderly populations experienced dramatic increases in RSV-associated hospitalization rates over recent years, reflecting improved diagnostic recognition and expanded testing practices in geriatric medicine.

Government-Funded RSV Prevention Programs Amplifying Diagnostic Requirements

Australian federal and state governments implemented comprehensive RSV prevention strategies incorporating maternal vaccination programs and infant monoclonal antibody prophylaxis, creating substantial diagnostic testing demand for program eligibility assessment and efficacy monitoring purposes. The Australian Government announced that maternal RSV vaccine would be available to all pregnant women for free under the National Immunization Program, alongside targeted RSV monoclonal antibody programs offered at no cost to high-risk or unvaccinated newborns across jurisdictional health services. Several states committed substantial funding to establish comprehensive universal prophylaxis programs covering all infants entering their first RSV season, while other jurisdictions implemented more targeted approaches focusing specifically on infants at increased risk, requiring robust diagnostic infrastructure to identify eligible populations through standardized clinical assessment protocols. These government-funded prevention initiatives necessitate coordinated diagnostic testing to differentiate vaccine-preventable RSV disease from other respiratory infections, monitor program effectiveness through ongoing surveillance, and identify breakthrough infections requiring enhanced clinical management strategies. Public health agencies utilize diagnostic testing data to track RSV transmission patterns, inform seasonal program timing adjustments, and evaluate population-level immunization impact on hospitalization rates.

Technological Advancements Enhancing Diagnostic Accessibility and Performance

Rapid evolution of molecular diagnostic technologies delivers increasingly accessible, accurate, and efficient RSV detection solutions suitable for diverse healthcare settings ranging from tertiary hospital laboratories to regional urgent care facilities. Regulatory authorities continue approving multiplex PCR tests detecting and differentiating multiple respiratory viruses including SARS-CoV-2, influenza, and respiratory syncytial virus in single samples, streamlining diagnostic workflows and assisting clinical decision-making during respiratory illness season. Point-of-care molecular platforms achieve laboratory-grade sensitivity while delivering results rapidly, enabling emergency department clinicians to make immediate treatment and admission decisions without central laboratory dependencies. Automated nucleic acid extraction systems integrated within molecular testing platforms reduce manual specimen processing requirements while enhancing workflow standardization and reducing operator-dependent variability affecting result accuracy. Multiplex syndromic panels capable of simultaneously detecting comprehensive respiratory pathogen panels provide definitive etiological diagnosis in complex clinical presentations where multiple pathogens may contribute to patient symptomatology. These technological capabilities support Australia's antimicrobial stewardship initiatives by enabling definitive viral pathogen identification, reducing inappropriate antibiotic prescribing in RSV-positive cases while facilitating targeted antiviral therapy consideration in severe infections requiring intensive care management.

Market Restraints:

What Challenges the Australia Respiratory Syncytial Virus Diagnostics Market is Facing?

High Capital Investment Requirements for Advanced Molecular Platforms

Sophisticated molecular diagnostic systems require substantial upfront capital expenditure for equipment procurement, laboratory infrastructure modifications, and staff training programs, creating financial barriers particularly challenging for smaller regional healthcare facilities operating under constrained budgetary allocations. Automated molecular platforms with integrated nucleic acid extraction and real-time PCR capabilities typically cost several hundred thousand dollars per unit, whilst ongoing reagent consumption, maintenance contracts, and quality control materials generate significant recurrent operational expenses.

Limited Public Awareness Regarding RSV Disease Severity and Diagnostic Importance

General population understanding of RSV as distinct pathogen requiring specific diagnostic identification remains limited compared to more widely recognized respiratory viruses like influenza, resulting in suboptimal healthcare-seeking behavior and delayed presentation to medical facilities. Many parents and caregivers perceive RSV symptoms as common cold manifestations not warranting medical consultation or diagnostic testing, leading to missed opportunities for early intervention in vulnerable infant populations.

Stringent Regulatory Requirements Governing Diagnostic Product Registration

Therapeutic Goods Administration regulatory pathways for in vitro diagnostic devices necessitate comprehensive clinical validation studies demonstrating analytical and clinical performance characteristics, creating extended timelines and substantial resource requirements for manufacturers seeking Australian market entry. Point-of-care devices additionally require evidence supporting use by non-laboratory personnel in near-patient settings, demanding extensive usability studies and quality management system documentation.

Competitive Landscape:

The Australia respiratory syncytial virus diagnostics market demonstrates competitive intensity characterized by established multinational diagnostic manufacturers and specialized molecular testing companies competing through technological innovation, clinical validation partnerships, and distribution network expansion. Leading players focus on developing multiplex respiratory panels integrating RSV detection alongside other common respiratory pathogens, addressing clinical demand for comprehensive aetiological diagnosis from single patient specimens. Companies invest substantially in regulatory compliance, quality assurance programs, and post-market surveillance to maintain Therapeutic Goods Administration approvals whilst supporting healthcare provider confidence in diagnostic accuracy and reliability. Strategic partnerships with major pathology networks, hospital procurement groups, and primary care organizations facilitate market penetration whilst ensuring consistent product availability across metropolitan and regional healthcare settings.

Australia Respiratory Syncytial Virus Diagnostics Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Products Covered |

Direct Fluorescent Antibody (DFA) Method, Rapid Antigen Diagnostic Test (RADTs), Molecular Diagnostics, Chromatographic Immunoassay, Diagnostic Imaging, Gel Microdroplets, Flow Cytometry, Others |

|

End Uses Covered |

Hospitals and Clinics, Laboratory, Others |

|

Regions Covered |

Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Respiratory Syncytial Virus Diagnostics Market Report

The Australia respiratory syncytial virus diagnostics market size was valued at USD 94.20 Million in 2025.

The Australia respiratory syncytial virus diagnostics market is expected to grow at a compound annual growth rate of 6.66% from 2026-2034 to reach USD 170.29 Million by 2034.

Molecular diagnostics dominated the market with a share of 39.8%, driven by superior analytical sensitivity for detecting minimal viral nucleic acid quantities, widespread adoption across hospital laboratory networks for definitive pathogen identification, and compatibility with automated high-throughput testing platforms supporting peak seasonal demand management.

Key factors driving the Australia respiratory syncytial virus diagnostics market include escalating RSV infection burden with record-breaking case numbers exceeding 175,000 in 2024, comprehensive government-funded prevention programs requiring coordinated diagnostic infrastructure, and rapid technological advancement delivering accessible point-of-care molecular platforms.

Major challenges include substantial capital investment requirements for advanced molecular diagnostic equipment constraining smaller regional facility adoption, limited general population awareness regarding RSV disease severity reducing proactive healthcare-seeking behavior, stringent Therapeutic Goods Administration regulatory pathways extending product registration timelines, and ongoing operational costs associated with quality assurance programs and staff competency maintenance.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade