Australia Semiconductor Market Size, Share, Trends and Forecast by Components, Material Used, End User, and Region, 2026-2034

Australia Semiconductor Market Size, Share, Trends & Forecast (2026-2034)

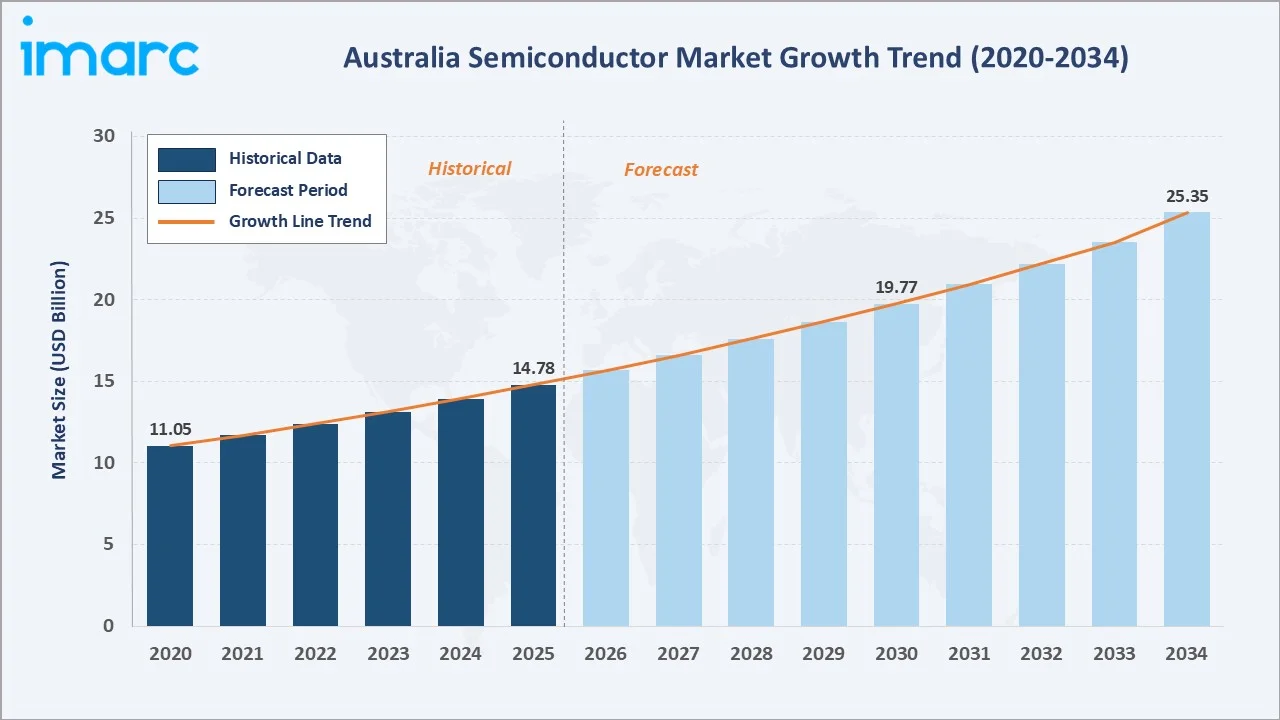

The Australia semiconductor market size reached USD 14.78 Billion in 2025 and is projected to reach USD 25.35 Billion by 2034, exhibiting a CAGR of 5.99% during 2026-2034. Strong government incentives, rising IoT and consumer electronics demand, proximity to Asia-Pacific supply chains, and cross-sector innovation culture are the primary growth drivers.

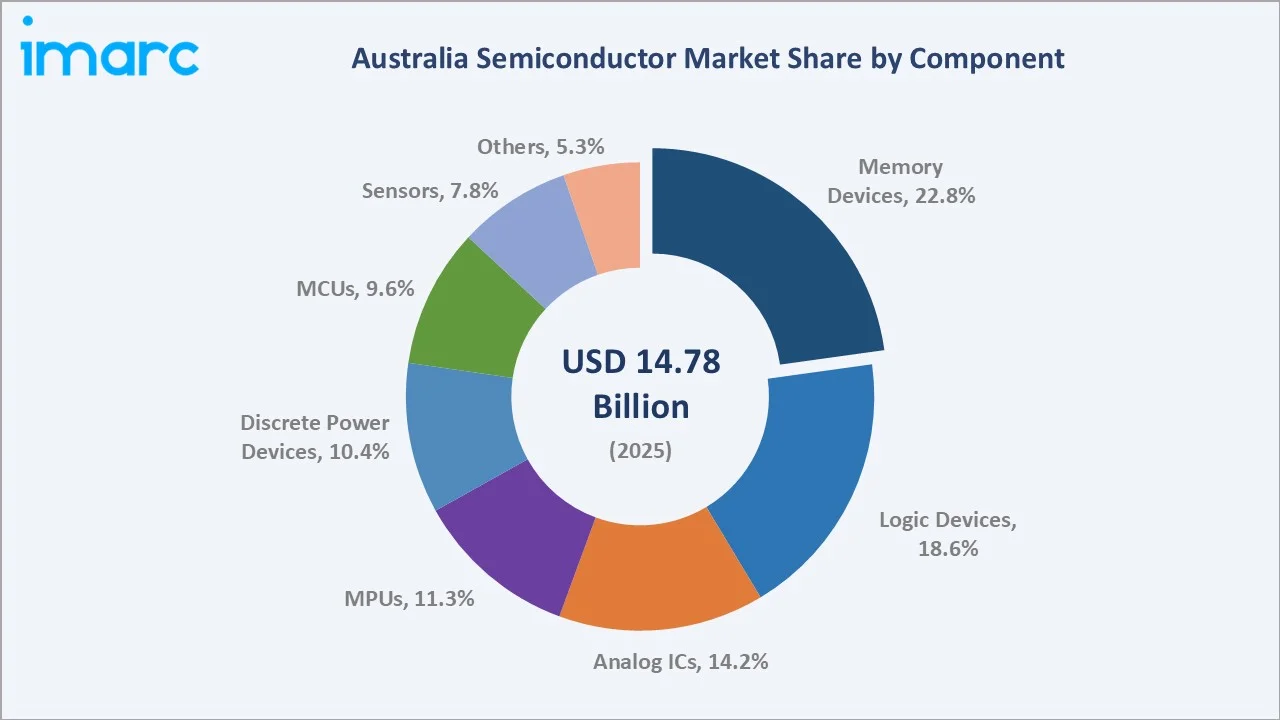

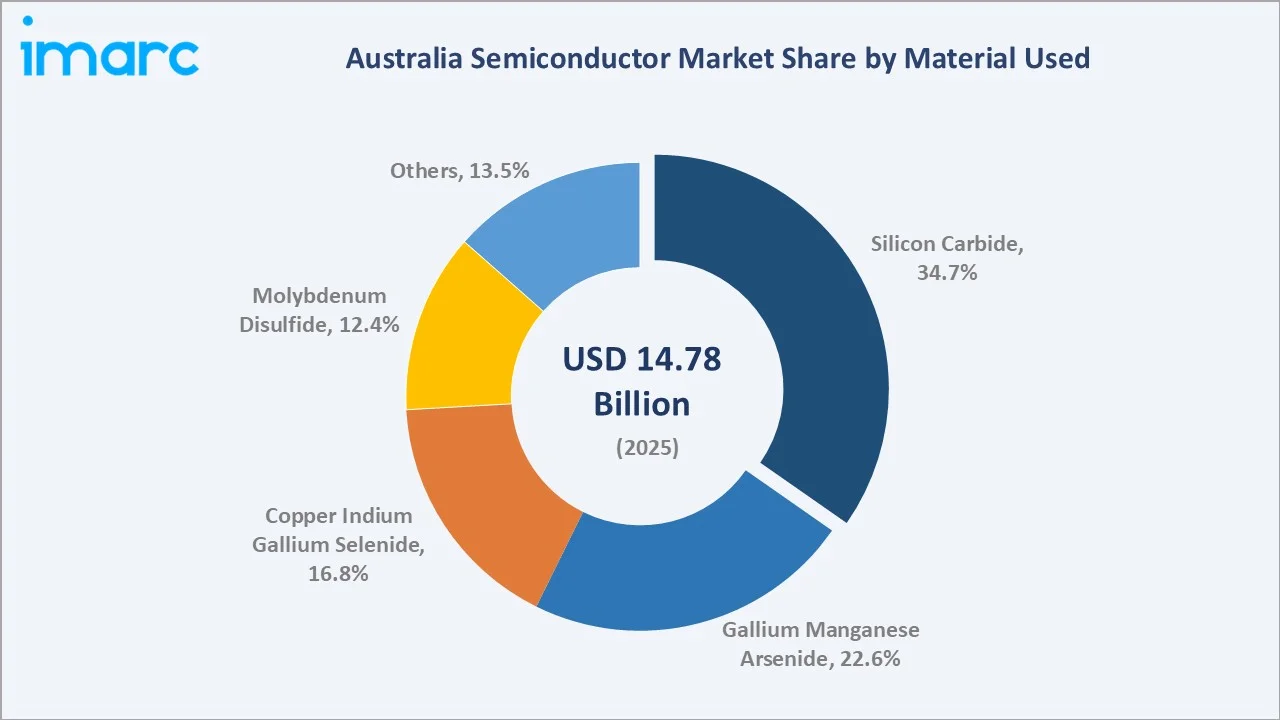

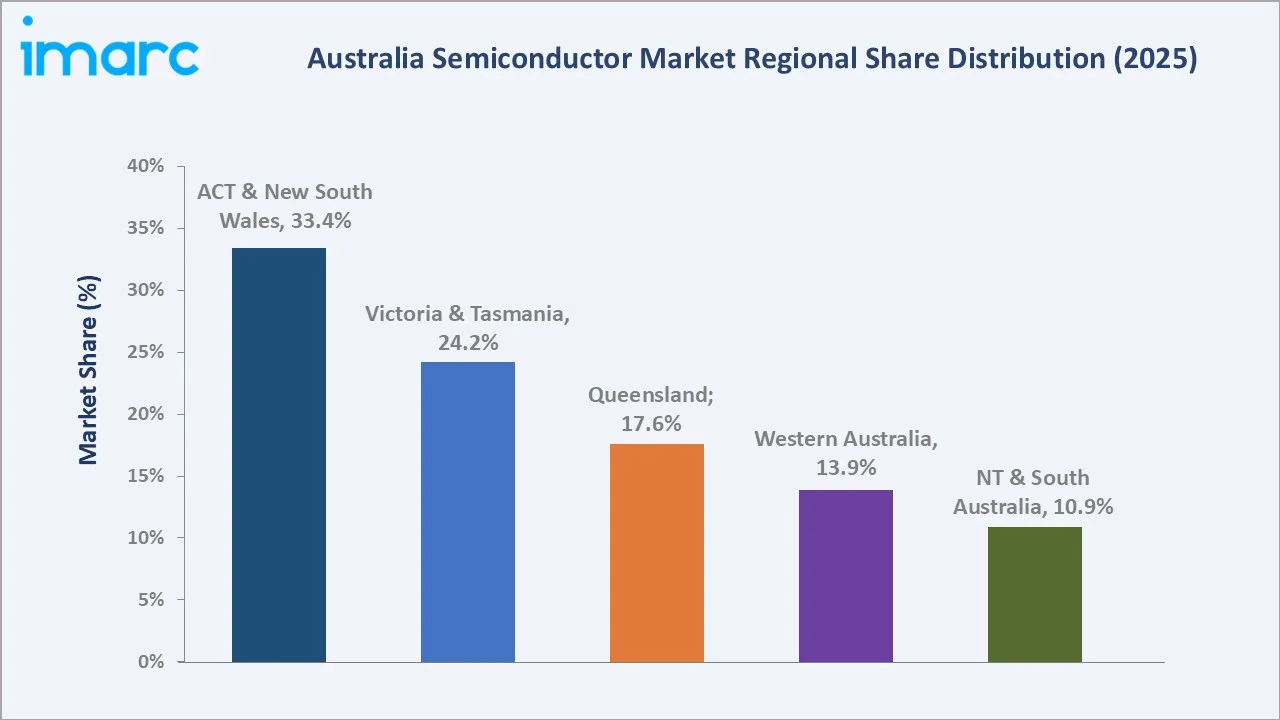

Memory Devices lead the component mix at 22.8%, Silicon Carbide dominates materials at 34.7%, and ACT & New South Wales commands 33.4% regional share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 14.78 Billion |

|

Forecast Market Size (2034) |

USD 25.35 Billion |

|

CAGR (2026-2034) |

5.99% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

ACT & New South Wales (33.4% share, 2025) |

|

Second Largest Region |

Victoria & Tasmania (24.2% share, 2025) |

|

Leading Component |

Memory Devices (22.8%, 2025) |

|

Leading Material |

Silicon Carbide (34.7%, 2025) |

The growth trajectory from 2020 through 2034, with the historical expansion to USD 14.78 Billion in 2025, reflects consistent government-driven and innovation-led demand, while the forecast to USD 25.35 Billion captures accelerating domestic manufacturing, quantum technology investment, and IoT-driven chip demand.

To get more information on this market, Request Sample

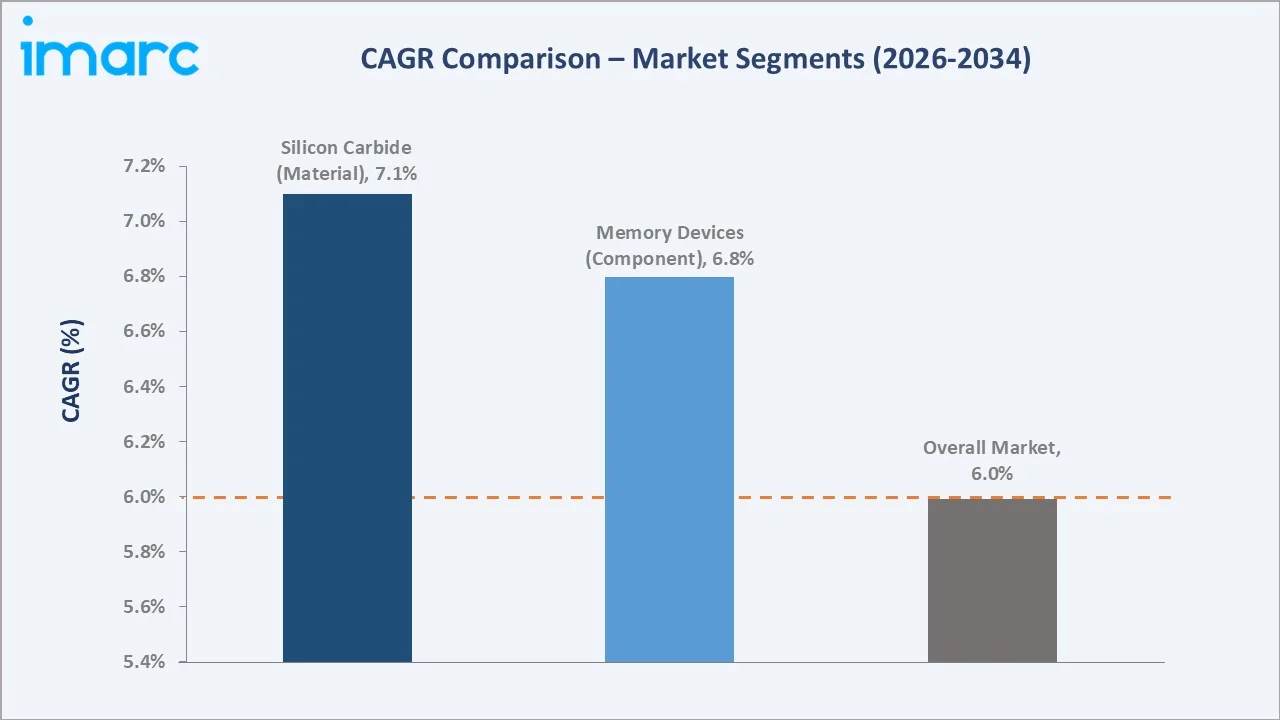

CAGR trajectories across key component, material, and regional sub-segments, with Silicon Carbide at ~7.1% CAGR and Memory Devices at ~6.8% CAGR, are the fastest-growing categories within the Australia semiconductor industry through 2034.

Executive Summary

The Australia semiconductor market is on a sustained growth trajectory from USD 14.78 Billion in 2025 to USD 25.35 Billion by 2034. Semiconductors underpin Australia's defence, telecommunications, mining, clean energy, and quantum computing sectors, creating non-discretionary demand for diverse chip architectures.

Memory Devices dominate the component mix at 22.8% in 2025, driven by data centre expansion and consumer electronics growth. Logic Devices (18.6%) and Analog ICs (14.2%) follow, reflecting rising embedded intelligence across industrial and automotive applications nationwide.

Silicon Carbide leads the material segment at 34.7% in 2025, benefiting from Australia's clean energy transition and power electronics demand. ACT & New South Wales commands 33.4% regional share, hosting the country's leading universities, defence precincts, and innovation hubs.

Key Market Insights

|

Insight |

Data |

|

Largest Component |

Memory Devices – 22.8% share (2025) |

|

Leading Material |

Silicon Carbide – 34.7% share (2025) |

|

Leading Region |

ACT & New South Wales – 33.4% share (2025) |

|

Second Largest Region |

Victoria & Tasmania – 24.2% share (2025) |

|

Top Companies |

Intel Corporation, Qualcomm Incorporated, Samsung, Texas Instruments Incorporated, Infineon Technologies AG, NXP Semiconductors |

Key Analytical Observations Expanding on the Above Data:

- Memory Devices, with 22.8% in 2025, dominate because Australia's data centre buildout, cloud adoption, and consumer electronics proliferation generate sustained demand for DRAM, NAND flash, and high-bandwidth memory components.

- Silicon Carbide, with 34.7% in 2025, leads materials because Australia's rapid solar, battery storage, and EV charging infrastructure rollout drives demand for high-efficiency SiC power devices that outperform silicon at high voltages.

- ACT & New South Wales, with 33.4% in 2025, dominate due to the concentration of federal government agencies, defence establishments, and leading semiconductor-linked universities that anchor research and commercialisation activity.

- Victoria & Tasmania, with 24.2% in 2025, benefits from Melbourne's advanced manufacturing ecosystem, strong university research, and proximity to defence and aerospace industry clusters across metropolitan and regional Victoria.

Australia Semiconductor Market Overview

Semiconductors are the foundational electronic components enabling computing, communication, sensing, power conversion, and memory storage. The Australian ecosystem spans chip designers, EDA software providers, test and measurement companies, packaging partners, foundry collaborations, and diverse end-use industries spanning defence, mining, clean energy, healthcare, and telecommunications.

The national ecosystem integrates university research centres, government-funded innovation hubs, international semiconductor companies with local design and sales offices, and a growing cohort of semiconductor startups targeting niche applications in quantum, IoT, and defence electronics.

Market Dynamics

To evaluate market opportunities, Request Sample

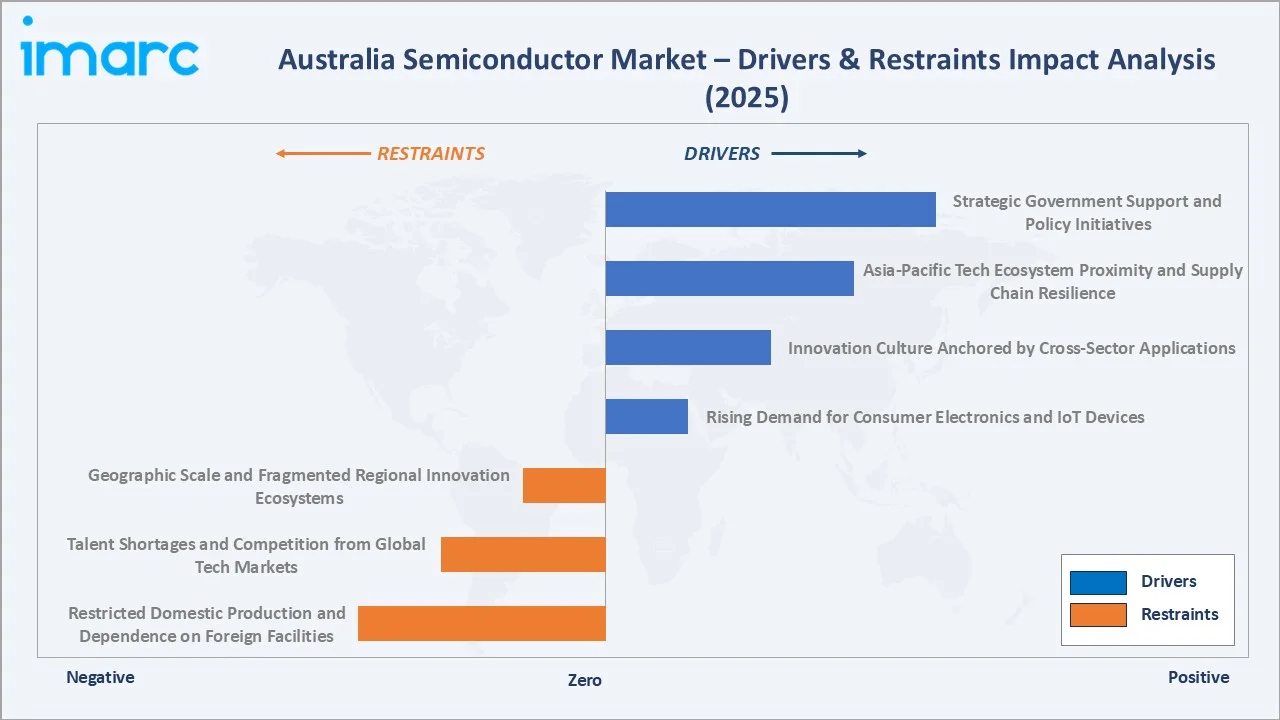

Market Drivers

- Strategic Government Support and Policy Initiatives: Australian federal and state governments have deployed coordinated incentive frameworks, including national semiconductor R&D grants, the National Semiconductor Manufacturing Hub initiative, and targeted university-industry co-investment programs that have created a virtuous cycle of talent development and private sector investment.

- Asia-Pacific Tech Ecosystem Proximity and Supply Chain Resilience: Australia's geographic proximity to key semiconductor production centres in Taiwan, South Korea, Singapore, and Japan enables just-in-time procurement and design collaboration. Its stable political environment and advanced logistics infrastructure attract international semiconductor firms seeking diversified supply chain nodes.

- Rising Demand for Consumer Electronics and IoT Devices: Expanding 5G network coverage, smart home device proliferation, connected mining equipment, precision agriculture sensors, and digital health monitoring devices are generating substantial incremental semiconductor demand across all component categories, particularly memory, sensors, and microcontrollers.

- Innovation Culture Anchored by Cross-Sector Applications: Australia's unique cross-sector application landscape, ruggedised mining electronics, outback remote sensing, offshore environmental monitoring, and clean energy power management, drives custom semiconductor IP development that serves both domestic and global markets with differentiated, application-specific solutions.

Market Restraints

- Restricted Domestic Production and Dependence on Foreign Facilities: Australia lacks advanced-node semiconductor fabrication facilities, compelling even locally designed chips to rely on overseas foundries for high-volume production, creating extended lead times, supply vulnerability, and limited opportunity to build ancillary manufacturing industries domestically.

- Talent Shortages and Competition from Global Tech Markets: Despite strong graduate output in electrical engineering and materials science, Australia faces significant attrition of semiconductor professionals to international hubs where ecosystem concentration, compensation packages, and career trajectories are comparatively more established and attractive.

- Geographic Scale and Fragmented Regional Innovation Ecosystems: Australia's vast geography disperses semiconductor capabilities across multiple cities and states, creating inter-jurisdictional coordination complexity, fragmented funding cycles, and logistical barriers that impede the formation of dense, integrated semiconductor clusters capable of competing with global innovation hubs.

Market Opportunities

- Growth of Local Design Hubs and Indigenous Innovation: Australia's world-class universities can anchor domestic semiconductor design centres focused on ASICs for deep-space exploration, mineral detection hardware, and high-performance computing for climate modelling, creating globally exportable IP from distinctly Australian innovation challenges and scientific strengths.

- Supply Chain Diversification and Domestic Manufacturing: Australia's stable regulatory framework and advanced port infrastructure position it to develop pilot packaging, testing, and niche wafer fabrication lines, serving mining, healthcare, and renewable energy customers with accelerated delivery and enhanced supply security against global disruptions.

Market Challenges

- Skilled Semiconductor Workforce Shortage: The semiconductor workforce deficit extends beyond graduate supply to hands-on fabrication process engineers, industrial testing specialists, and layout designers. Filling this gap demands not only expanded university programs but targeted industry-university fellowships linked to real Australian semiconductor applications.

- Technology Transition and Capital Intensity: Transitioning from import-dependent design to domestic pilot fabrication requires substantial capital expenditure in cleanrooms, lithography tools, and process chemicals. Coordinating government, university, and private co-investment across jurisdictional boundaries remains a complex, time-intensive organisational challenge.

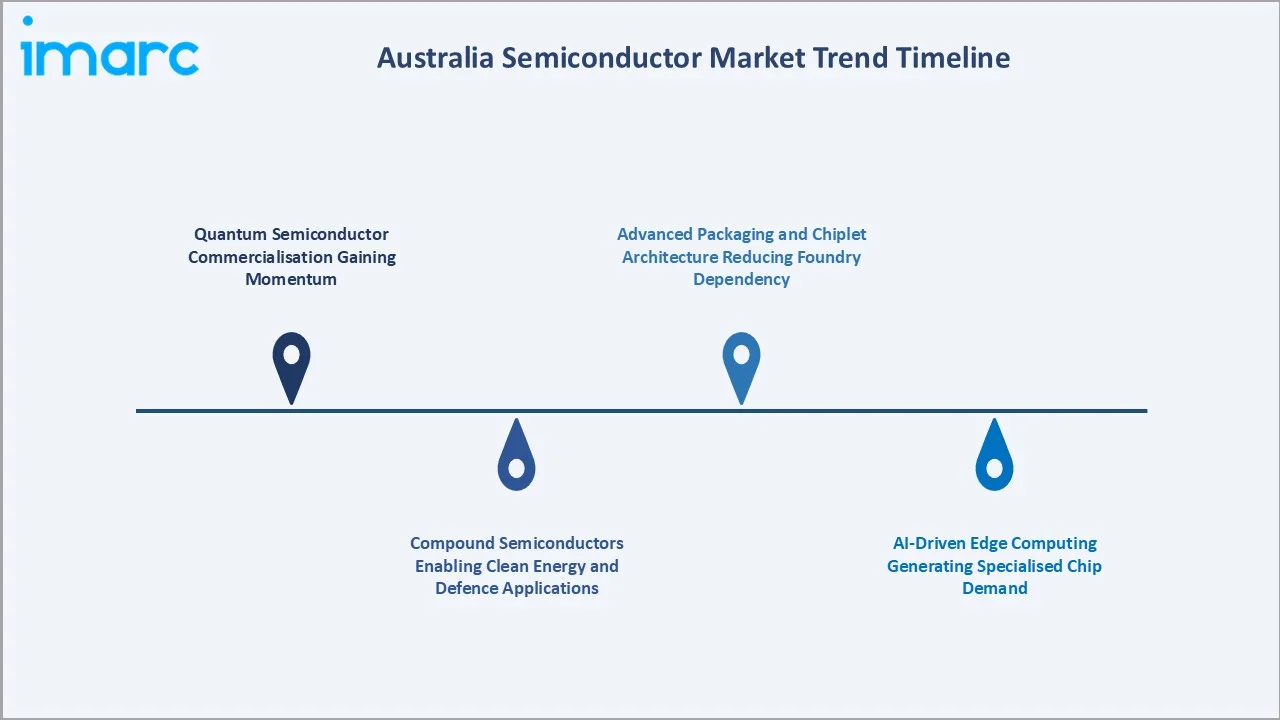

Emerging Market Trends

1. Quantum Semiconductor Commercialisation Gaining Momentum

Australia's significant quantum technology investments, including a large-scale fault-tolerant silicon quantum computer facility under construction in Brisbane, combined with private sector quantum ventures raising substantial funding in 2024, are establishing Australia as a global quantum semiconductor commercialisation leader through 2034.

2. Compound Semiconductors Enabling Clean Energy and Defence Applications

Silicon Carbide and Gallium Nitride compound semiconductor devices are enabling Australia's solar inverters, EV charging infrastructure, and defence radar systems to achieve superior switching efficiency and thermal performance, driving above-market growth in the materials and discrete power device segments throughout the forecast period.

3. AI-Driven Edge Computing Generating Specialised Chip Demand

Industrial AI applications in Australian mining automation, precision agriculture, and predictive healthcare are driving demand for edge AI inference chips optimised for low power consumption and harsh environmental conditions, creating differentiated opportunities for local semiconductor design startups focused on uniquely Australian challenges.

4. Advanced Packaging and Chiplet Architecture Reducing Foundry Dependency

Advanced packaging technologies including 2.5D interposers, fan-out wafer-level packaging, and chiplet integration enable Australian designers to combine best-of-breed chips from multiple foundries, reducing single-source dependency and creating local value-add in assembly and integration services.

Industry Value Chain Analysis

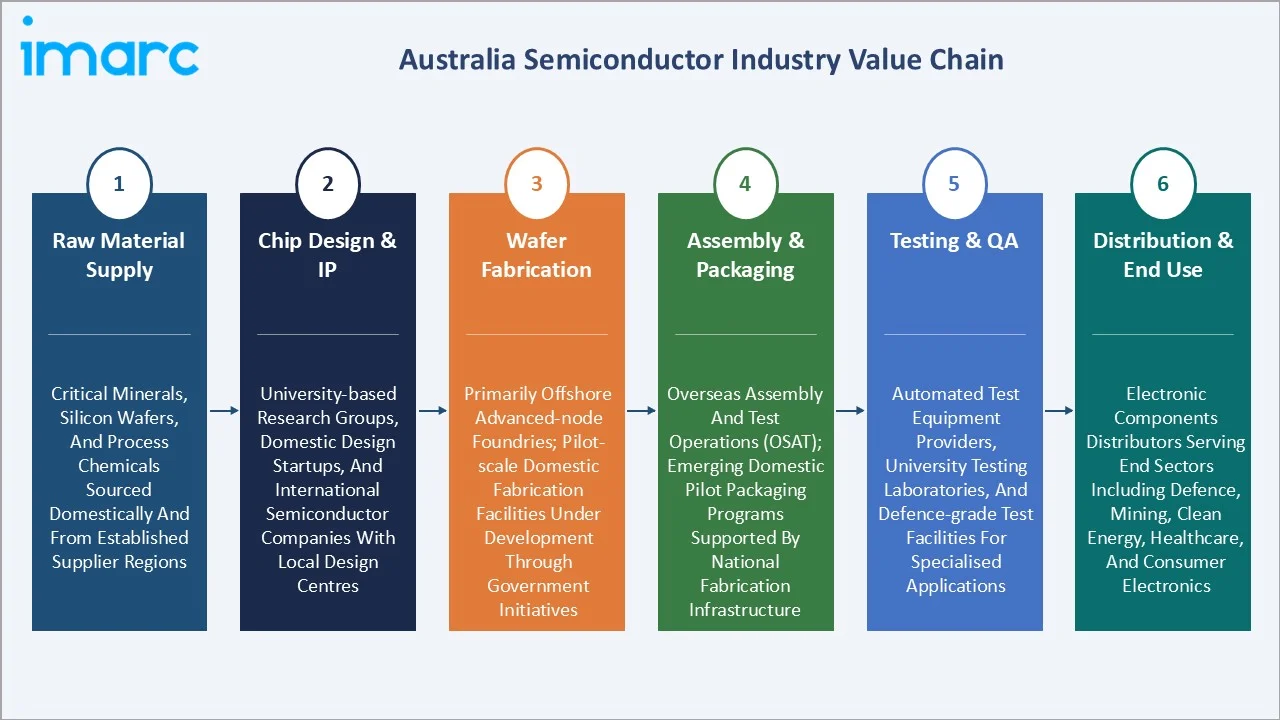

The Australian semiconductor value chain spans six stages from raw material supply through end-use industries. Chip design and IP development, alongside advanced packaging and testing, capture the highest value-add margins and represent the most accessible entry points for Australian companies and research institutions seeking to participate in global semiconductor supply chains.

|

Stage |

Description |

|

Raw Material Supply |

Critical minerals, silicon wafers, and process chemicals are sourced domestically and imported from established supplier regions |

|

Chip Design & IP |

University-based research groups, domestic design startups, and international semiconductor companies with local design centres |

|

Wafer Fabrication |

Primarily offshore advanced-node foundries; pilot-scale domestic fabrication facilities under development through government initiatives |

|

Assembly & Packaging |

Overseas assembly and test operations (OSAT); emerging domestic pilot packaging programs supported by national fabrication infrastructure |

|

Testing & QA |

Automated test equipment providers, university testing laboratories, and defence-grade test facilities for specialised applications |

|

Distribution & End Use |

Electronic components distributors serving end sectors including defence, mining, clean energy, healthcare, and consumer electronics |

Technology Landscape in the Australian Semiconductor Industry

Silicon Photonics and Quantum Device Technologies

Australia leads globally in silicon-spin qubit research, with leading university groups demonstrating record-fidelity two-qubit gates in silicon. These advances are translating into commercial quantum chip development through local ventures, positioning Australia at the frontier of next-generation semiconductor architectures with significant global commercialisation potential.

Wide Bandgap Semiconductor Materials: SiC and GaN

Silicon Carbide devices achieve blocking voltages above 3.3 kV and switching frequencies beyond 100 kHz, enabling compact, efficient power converters for utility-scale solar farms and battery storage systems. University research groups and government research bodies are actively researching SiC epitaxy process improvements targeted at local clean energy applications.

Advanced Node Design and EDA Toolchain Adoption

Australian semiconductor design houses are adopting advanced-node design rules via cloud-based EDA platforms, enabling globally competitive chip design without requiring on-shore advanced-node fabrication. This cloud EDA model lowers capital barriers for startups and university spinouts targeting niche markets in defence, quantum, and industrial IoT.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

Memory Devices |

22.8% |

2025 |

|

Material Used |

Silicon Carbide |

34.7% |

2025 |

|

End User |

🔒 |

🔒 |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

33.4% |

2025 |

By Component

Memory Devices command a 22.8% majority share in 2025 owing to Australia's accelerating data centre buildout, cloud services adoption, and consumer electronics demand. DRAM and NAND flash components serve enterprise computing, mobile devices, and automotive infotainment systems across the country.

To access detailed market analysis, Request Sample

Logic Devices at 18.6% in 2025 reflect the expanding embedded processing requirements of industrial automation, telecommunications infrastructure, and defence systems, with programmable and application-specific integrated circuits delivering intelligent processing across Australia's critical technology sectors.

Analog ICs (14.2%), MPUs (11.3%), and Discrete Power Devices (10.4%) collectively serve industrial control, computing, and power management applications. MCUs (9.6%) and Sensors (7.8%) address the rapidly expanding IoT and smart infrastructure segments across mining, agriculture, and smart cities.

By Material Used

Silicon Carbide dominates the material mix at 34.7% in 2025, driven by Australia's clean energy transition agenda, electric vehicle charging infrastructure rollout, and power electronics demand from renewable energy installations, where SiC's superior efficiency over silicon justifies its premium pricing and growing adoption.

Gallium Manganese Arsenide at 22.6% in 2025 serves high-frequency RF and microwave applications in telecommunications, defence radar, and satellite communications, where its superior electron mobility enables performance levels unachievable with silicon or SiC alternatives.

Copper Indium Gallium Selenide (16.8%) addresses photovoltaic and optoelectronic applications, benefiting from Australia's extensive solar energy sector. Molybdenum Disulfide (12.4%) is gaining traction in next-generation transistor research and flexible electronics development at leading Australian research institutions.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

ACT & New South Wales |

33.4% |

Highest concentration of government R&D investment, research institutions, defence precincts, and technology innovation hubs |

|

Victoria & Tasmania |

24.2% |

Advanced manufacturing ecosystem, strong university research output, defence aerospace industry, and technology startup activity |

|

Queensland |

17.6% |

Quantum technology investment, university research and development, mining electronics, and defence technology programs |

|

Western Australia |

13.9% |

Mining ruggedised electronics, remote sensing applications, port logistics infrastructure, and resources sector technology demand |

|

NT & South Australia |

10.9% |

Defence industry presence, autonomous systems development, remote connectivity semiconductor demand, and government technology programs |

ACT & New South Wales' 33.4% dominance in 2025 is driven by the highest concentration of semiconductor-linked research institutions, federal government procurement, defence facilities, and technology startup density in Australia. University quantum computing research groups and national fabrication facilities anchor regional market leadership.

Queensland, with 17.6% growth in 2025, is experiencing the most dynamic growth inflection, anchored by large-scale quantum computing facility investments in Brisbane, which are expected to catalyse downstream semiconductor supply chain investment and talent cluster formation through the forecast period.

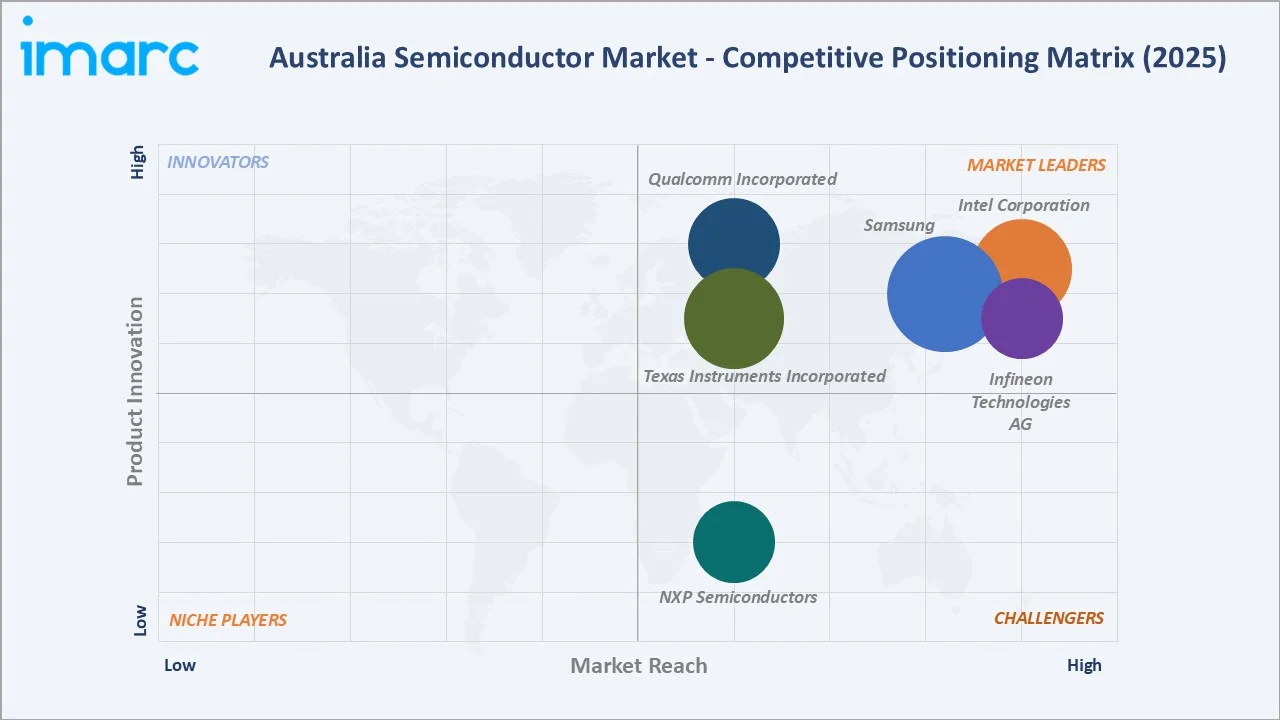

Competitive Landscape

The Australian semiconductor market is served primarily by subsidiaries, design centres, and distribution operations of major global semiconductor corporations, alongside a growing cohort of domestically founded design startups targeting niche quantum, mining, and clean energy applications.

|

Company Name |

Key Products |

Market Position |

Strategic Focus |

|

Intel Corporation |

Xeon 6, Core Ultra, Agilex FPGA |

Leader |

Data centres, AI compute, defense HPC, local design, and government technology partnerships |

|

Qualcomm Incorporated |

Snapdragon |

Leader |

Mobile, IoT, 5G chipsets; 5G network infrastructure and carrier partnerships |

|

Samsung |

DRAM, NAND Flash, Exynos |

Leader |

Memory supply; consumer electronics and enterprise storage |

|

Texas Instruments Incorporated |

Analog ICs, MCUs, DSPs |

Leader |

Industrial, automotive, clean energy, power management; broad distributor network |

|

Infineon Technologies AG |

SiC, IGBT, Security ICs |

Leader |

Power electronics, automotive, clean energy; SiC growth in the renewable energy segment |

|

NXP Semiconductors |

Automotive ICs, i.MX, RF |

Challenger |

Automotive, industrial IoT, secure connectivity, and smart infrastructure applications |

Key players include Intel Corporation, Qualcomm Incorporated, Samsung, Texas Instruments Incorporated, Infineon Technologies AG, NXP Semiconductors, and others.

Key Company Profiles

Intel Corporation

Intel Corporation is one of the world's largest semiconductor companies, headquartered in USA. Intel maintains a significant Australian presence through commercial, government, and defence technology operations, with strategic partnerships with Australian defence agencies and data centre operators across Sydney, Melbourne, and Canberra.

- Product Portfolio: Xeon 6, Core Ultra, Agilex FPGA

- Strategic Focus: Intel's Australian strategy leverages its data centre CPU and FPGA portfolio to capture growing government AI infrastructure investment while expanding into defence-grade compute requirements under Australia's strategic technology sharing and sovereign capability frameworks.

Qualcomm Incorporated

Qualcomm is a global leader in wireless semiconductor technology, headquartered in USA. Qualcomm's mobile platforms power the majority of smartphones sold in Australia, while its RF front-end modules underpin Australia's 5G network infrastructure deployment by major telecommunications carriers.

- Product Portfolio: Snapdragon

- Strategic Focus: Qualcomm's Australian strategy focuses on 5G network densification, IoT device proliferation, and automotive connectivity, targeting operators and equipment manufacturers adopting intelligent connectivity solutions across mining, logistics, and smart city applications.

Infineon Technologies AG

Infineon Technologies AG is a leading semiconductor company headquartered in Neubiberg, Germany, specialising in power semiconductors, automotive ICs, and security solutions. Infineon's Silicon Carbide and IGBT power devices are integral to Australia's solar inverter, battery energy storage, and EV charging infrastructure deployments.

- Product Portfolio: SiC, IGBT, Security ICs

- Strategic Focus: Infineon's Australian strategy centres on SiC power semiconductor supply to renewable energy, EV infrastructure, and industrial automation sectors, reinforced by its commitment to decarbonisation technology partnerships aligned with Australia's clean energy investment pipeline.

Market Concentration Analysis

The Australia semiconductor market is moderately concentrated at the distribution level, with global leaders holding strong positions, while the domestic design and startup ecosystem remains fragmented. No single company holds more than 10–12% of total Australian semiconductor market revenue, reflecting the market's diverse end-use base and the absence of a dominant domestic manufacturer.

Consolidation is occurring through global M&A activity filtering into Australian operations, with emerging domestic semiconductor companies targeting niche quantum, AI chip design, and data centre applications. Strategic acquisitions in early 2025 signal growing private sector interest in building Australian semiconductor IP assets for data centre and cybersecurity applications.

Investment & Growth Opportunities

Fastest-Growing Segments

Silicon Carbide at ~7.1% CAGR through 2034 is the highest-growth material segment, driven by renewable energy infrastructure and EV adoption. Memory Devices at ~6.8% CAGR reflect data centre expansion and AI computing infrastructure investment across Australia's hyperscale operators and enterprise sector.

Emerging Markets and Applications

Queensland's quantum technology ecosystem, anchored by large-scale quantum computing facility investment in Brisbane, represents the most strategically significant emerging semiconductor market in Australia. Cryogenic control electronics, photonic interconnects, and quantum error correction chips create novel semiconductor demand categories beyond 2028.

Venture and Investment Trends

Private sector semiconductor investment in Australia reached record levels in 2024, with quantum computing ventures and AI chip design companies raising substantial capital. Government co-investment frameworks including national R&D grant programs are catalysing additional private capital deployment into semiconductor design, testing, and packaging capabilities.

Future Market Outlook (2026-2034)

The Australia semiconductor market is forecast to expand from USD 14.78 Billion in 2025 to USD 25.35 Billion by 2034 at a CAGR of 5.99%, adding USD 10.57 Billion in incremental annual market value over the forecast period, representing the most sustained technology sector growth cycle in Australia's history.

Three technological forces will most significantly shape the Australian semiconductor landscape through 2034: quantum semiconductor commercialisation creating entirely new chip categories, SiC and GaN compound semiconductor adoption across clean energy sustaining above-market growth, and AI-driven edge computing generating specialised demand across mining and industrial automation applications.

Australia's National Semiconductor Manufacturing Hub, targeting pilot fabrication scale-up by 2027, will catalyse downstream ecosystem formation, reduce import dependency for niche applications, and anchor talent retention through competitive local career pathways in advanced semiconductor manufacturing.

Research Methodology

Primary Research

Primary research encompassed structured interviews with Australian semiconductor industry stakeholders, including university research directors, government agency technology officers, semiconductor distribution executives, and clean energy equipment manufacturers. Primary data validated market sizing, segment shares, regional breakdowns, and technology adoption timelines.

Secondary Research

Key secondary sources include government agency reports on semiconductor applications, national fabrication facility annual reports, official statistics on electronics imports and exports, Semiconductor Industry Association global reports, WSTS market statistics, IEA energy technology reports, and publicly available company disclosures for listed semiconductor-adjacent firms.

Forecasting Models

Market size estimations and growth projections were derived using top-down and bottom-up forecasting models incorporating GDP growth rates, technology adoption curves, government investment timelines, and historical market evolution patterns. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty.

Australia Semiconductor Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Memory Devices, Logic Devices, Analog IC, MPU, Discrete Power Devices, MCU, Sensors, Others |

| Materials Used Covered | Silicon Carbide, Gallium Manganese Arsenide, Copper Indium Gallium Selenide, Molybdenum Disulfide, Others |

| End Users Covered | Automotive, Industrial, Data Centre, Telecommunication, Consumer Electronics, Aerospace and Defense, Healthcare, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Intel Corporation, Qualcomm Incorporated, Samsung, Texas Instruments Incorporated, Infineon Technologies AG, NXP Semiconductors, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia semiconductor market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia semiconductor market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia semiconductor industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Semiconductor Market Report

The Australia semiconductor market reached USD 14.78 Billion in 2025, driven by government investment, rising IoT demand, and proximity to Asia-Pacific semiconductor supply chains.

The market is projected to reach USD 25.35 Billion by 2034, growing at a CAGR of 5.99% during 2026-2034, supported by quantum technology investment, clean energy semiconductor demand, and data centre expansion.

Memory Devices lead with 22.8% component share in 2025, driven by data centre buildout, consumer electronics proliferation, and enterprise cloud computing adoption across Australian organisations.

Silicon Carbide dominates at 34.7% in 2025, valued for its superior power conversion efficiency in solar inverters, battery storage systems, and EV charging infrastructure across Australia's energy transition.

ACT & New South Wales commands a dominant 33.4% market share in 2025, driven by federal R&D investment, national fabrication facilities, defence precincts, and leading semiconductor-linked universities.

Silicon Carbide is the fastest-growing material at ~7.1% CAGR through 2034, driven by renewable energy infrastructure and electric vehicle charging adoption across Australia's rapidly decarbonising economy.

Leading companies include Intel Corporation, Qualcomm Incorporated, Samsung, Texas Instruments Incorporated, Infineon Technologies AG, and NXP Semiconductors, among others.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade