Australia Sodium Cyanide Market Size, Share, Trends and Forecast by Product Type, Industry, Sales Channel, Form, and Region, 2026-2034

Australia Sodium Cyanide Market Summary:

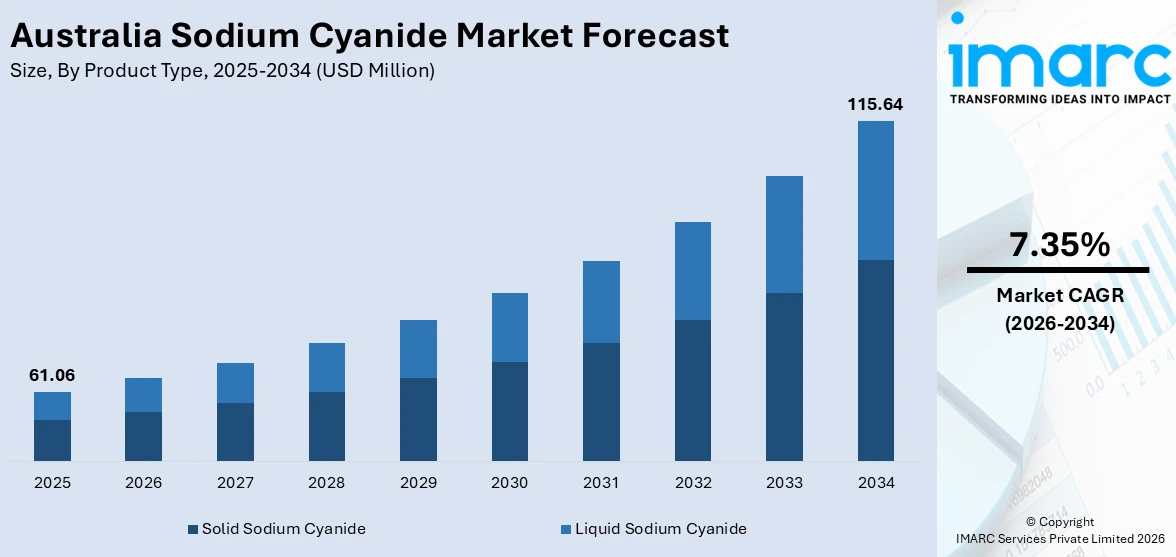

The Australia sodium cyanide market size was valued at USD 61.06 Million in 2025 and is projected to reach USD 115.64 Million by 2034, growing at a compound annual growth rate of 7.35% from 2026-2034.

The Australia sodium cyanide market is expanding steadily, underpinned by robust gold mining operations, rising precious metal prices, and growing industrial demand across chemical and pharmaceutical sectors. Increasing investments in production capacity, advancements in sustainable cyanide handling technologies, and strengthening export channels are reinforcing supply chain resilience. Government-supported mining exploration programs, coupled with heightened global demand for gold as a safe-haven asset, are accelerating consumption. These factors are collectively shaping the Australia sodium cyanide market share.

Key Takeaways and Insights:

- By Product Type: Solid sodium cyanide dominates the market with a share of 58.7% in 2025, owing to its superior stability during transportation, ease of storage in remote mining regions, and consistent dissolution properties that enable precise dosage control in gold extraction processes across Australia.

- By Industry: Mining leads the market with a share of 72.4% in 2025, driven by Australia’s position as the second-largest gold producer globally, extensive mining operations in Western Australia, and continued reliance on cyanidation as the primary gold extraction methodology.

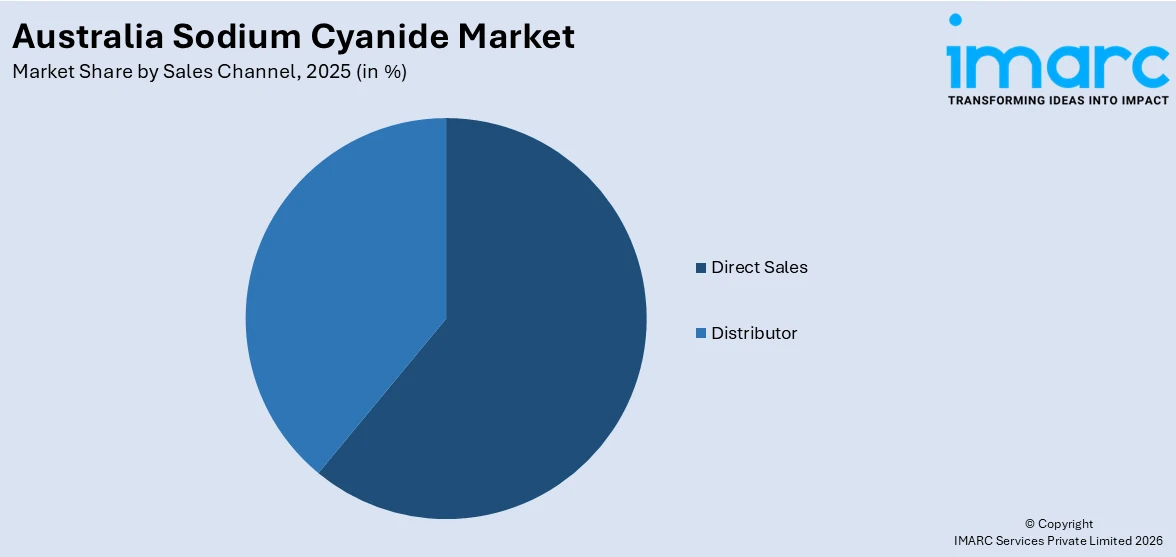

- By Sales Channel: Direct sales hold the largest segment with a market share of 61.2% in 2025, reflecting the preference of large-scale mining operators for direct procurement arrangements that ensure supply security, competitive pricing, and tailored logistics for sodium cyanide delivery.

- By Form: Solid exhibits a clear dominance in the market with 59.3% share in 2025, owing to its reduced leakage risk during handling, suitability for long-distance transport to remote mine sites, and compatibility with established gold leaching infrastructure throughout Australia.

- By Region: Western Australia represents the leading region with 41.8% share in 2025, driven by the concentration of major gold mining operations including Boddington, Super Pit, and Jundee mines, combined with proximity to key sodium cyanide manufacturing facilities in Kwinana.

- Key Players: Leading market participants drive Australia’s sodium cyanide sector by expanding production capacities, enhancing safety and environmental standards, investing in sustainable manufacturing technologies, and strengthening global distribution networks to ensure reliable supply for domestic and international gold mining operations.

To get more information on this market Request Sample

The Australia sodium cyanide market is advancing as gold mining activities intensify and industrial applications expand across the country. A major factor supporting this growth is the unprecedented rise in gold prices, which has motivated miners to increase output and invest in efficient extraction processes. For instance, Australia’s gold export earnings rose 42% to AUD 47 Billion in 2024–25, with forecasts projecting earnings to reach AUD 69 Billion in 2025–26, according to the Department of Industry, Science and Resources. This surge in gold production directly stimulates demand for sodium cyanide, the primary reagent used in cyanidation-based gold recovery. Expanding domestic manufacturing capacity, growing chemical sector applications, and rising global demand for Australian-produced sodium cyanide are further reinforcing market momentum. Strengthened regulatory frameworks for safe cyanide handling and investments in sustainable production technologies are also contributing to a more resilient and environmentally responsible market environment, supporting long-term growth across all end-use sectors.

Australia Sodium Cyanide Market Trends:

Rising Gold Prices Fueling Extraction Activity

Australia’s sodium cyanide consumption is being propelled by surging gold prices that have incentivized expanded mining operations nationwide. According to the Department of Industry, Science and Resources, gold prices reached a record above USD 4,300 per ounce in the October quarter of 2025, driven by geopolitical uncertainty and investor demand for safe-haven assets. This price environment is encouraging miners to process lower-grade ores and reopen marginal deposits, both of which require higher volumes of sodium cyanide for effective gold recovery and are supporting Australia sodium cyanide market growth.

Advancements in Sustainable Cyanide Management Technologies

Innovation in cyanide recycling and detoxification is reshaping operational practices across Australian gold mines. Research institutions and industry participants are developing advanced processes that improve gold recovery while enabling the recycling of toxic cyanide, reducing the volume of reagent that would otherwise be destroyed after use. Such advancements are enabling mining operators to reduce reagent consumption, lower environmental risks associated with tailings storage, and decrease transport requirements, all while maintaining extraction efficiency and supporting more sustainable mining practices across the country.

Expansion of Domestic Sodium Cyanide Production Capacity

Australian manufacturers are scaling up sodium cyanide production to meet growing domestic and export demand from the gold mining sector. Key producers are undertaking significant facility expansions to increase both solution and solid sodium cyanide output, positioning themselves among the largest global suppliers. These expansion programs incorporate low-emissions technologies and sustainable waste management infrastructure, highlighting the industry's commitment to combining capacity growth with environmental responsibility. Enhanced production capabilities are strengthening supply chain resilience for mining operations across Australia and international markets.

Market Outlook 2026-2034:

Australia’s sodium cyanide market, with its positive outlook for a sustained future expansion trend, is pointing towards a promising period with a tripling factor of escalating gold mining operations, consistent precious metal price trends, and surging usage within the national industry base. Furthermore, capacity expansion by indigenous companies like AGR with its Kwinana facility enhancement project and Orica with its reinforced global distribution capabilities following the acquisition of Cyanco is looking to enhance flexibility within the sodium cyanide supply chain for end-users. Advances in green technology for cyanide management, recycling, and environmentally friendly formulation will promote operational efficiency and sustainability within the sodium cyanide market. The market generated a revenue of USD 61.06 Million in 2025 and is projected to reach a revenue of USD 115.64 Million by 2034, growing at a compound annual growth rate of 7.35% from 2026-2034.

Australia Sodium Cyanide Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Solid Sodium Cyanide |

58.7% |

|

Industry |

Mining |

72.4% |

|

Sales Channel |

Direct Sales |

61.2% |

|

Form |

Solid |

59.3% |

|

Region |

Western Australia |

41.8% |

Product Type Insights:

- Solid Sodium Cyanide

- Liquid Sodium Cyanide

Solid sodium cyanide dominates with a market share of 58.7% of the total Australia sodium cyanide market in 2025.

Solid sodium cyanide, commonly supplied in briquette and pellet forms, is widely favored in Australia’s gold mining industry due to its stability and safer handling during transport to distant mining locations. Its solid form minimizes spillage concerns and supports secure storage and use at mine sites. Additionally, it dissolves consistently, enabling accurate dosage management in cyanidation processes and helping maintain efficient and controlled gold recovery operations.

The preference for solid sodium cyanide in Australia is further supported by the country’s vast geographic distances between manufacturing plants and mine sites, particularly in Western Australia and Queensland. Solid form minimizes hazardous material exposure during long-distance road and rail transport, complying with stringent safety protocols under Australia’s dangerous goods regulations. Domestic production hubs, including the AGR facility in Kwinana, which is expanding its solids production capacity as part of its 2025 expansion program, are ensuring a steady supply pipeline to meet the growing requirements of both domestic miners and international export markets.

Industry Insights:

- Mining

- Chemical

- Dye and Textile

- Pharmaceutical

Mining leads with a share of 72.4% of the total Australia sodium cyanide market in 2025.

The mining sector is the predominant consumer of sodium cyanide in Australia, driven by the country's standing as one of the largest gold producers globally. Cyanidation remains the most efficient and cost-effective method for gold extraction, making sodium cyanide an indispensable reagent across mining operations. The sector's dominance is reinforced by continued exploration activity, new project developments, processing of increasingly complex and lower-grade ore bodies, and sustained investment in gold recovery infrastructure nationwide.

Gold mining operations in Western Australia, which account for a significant majority of national output, are key drivers of sodium cyanide demand within the mining industry. The concentration of large-scale open-pit and underground mines across the Goldfields, Pilbara, and Murchison regions sustains substantial reagent consumption throughout the year. Adherence to internationally recognized cyanide management standards ensures safe handling, storage, and detoxification practices, reinforcing the sector's continued reliance on this essential extraction chemical.

Sales Channel Insights:

Access the comprehensive market breakdown Request Sample

- Direct Sales

- Distributor

Direct sales hold the largest share at 61.2% of the total Australia sodium cyanide market in 2025.

Direct sales dominate the sodium cyanide distribution landscape in Australia, reflecting the purchasing preferences of large-scale mining corporations that require assured supply, customized delivery logistics, and competitive pricing structures. Major gold mining operators typically enter into long-term procurement contracts directly with sodium cyanide manufacturers, ensuring supply security for operations in remote and geographically challenging locations. The direct sales model also facilitates comprehensive technical support, safety training, and storage management services that are critical for handling such a highly regulated hazardous chemical.

Australia’s direct sales channel for sodium cyanide is supported by the close location of major producers to key mining hubs, enabling efficient and reliable supply to gold operations. Facilities in Western Australia and Queensland help reduce transport complexity and ensure consistent delivery. Manufacturers often use specialized containers to improve safety during handling and shipment directly to mine storage sites. This well-developed direct distribution network plays an important role in maintaining steady reagent availability for mining activities.

Form Insights:

- Solid

- Liquid

Solid represents the largest segment with a 59.3% share of the total Australia sodium cyanide market in 2025.

The solid form of sodium cyanide dominates consumption in Australia due to its practical advantages in storage, transportation, and handling across the country’s expansive mining landscape. Solid sodium cyanide in briquette form is particularly suited for Australia’s remote mining operations, where logistical challenges and long transport distances require stable, low-risk chemical delivery solutions. The solid form also supports automated and controlled dosing systems at mine sites, enabling efficient and safe integration into established carbon-in-leach and carbon-in-pulp processing circuits widely used in Australian gold extraction.

The continued preference for solid form sodium cyanide is bolstered by ongoing manufacturing investments aimed at increasing solids production capacity within Australia. Major domestic producers are expanding their facilities to accommodate growing export demand alongside rising domestic requirements. Solid sodium cyanide represents the dominant form of global consumption, with Australia's remote mining regions in the Pilbara, Goldfields, and North Queensland ranking among the primary end-use markets due to their geographic isolation, challenging logistics corridors, and stringent transport safety requirements governing hazardous chemical movement.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Western Australia exhibits a clear dominance with a 41.8% share of the total Australia sodium cyanide market in 2025.

Western Australia continues to be the major region in terms of the consumption of sodium cyanide; this follows the dominance of gold mining activities in this region. There are many gold mines in this region where gold is processed using cyanide compounds as reagents in the gold retrieval process. These activities ensure there is consistent demand for sodium cyanide in gold mining activities, thereby ensuring the region remains dominant in gold mining activities within Australia.

This is supported by the fact that this region is also advantageous due to its proximity to important sodium cyanide manufacturing plant infrastructure within the state. A large sodium cyanide manufacturing plant is situated within the Kwinana industrial zone, implying a more efficient supply chain for the product to the mines within this state. Increased exploration within well-established mining regions is consistent with a national market for sodium cyanide, further validating the state’s significance within the country’s market for the product.

Market Dynamics:

Growth Drivers:

Why is the Australia Sodium Cyanide Market Growing?

Booming Gold Mining Sector and Record Precious Metal Prices

Australia’s gold mining industry is experiencing a significant upsurge, propelled by record-setting gold prices that have incentivized expanded production and exploration across the country. As the world’s second-largest gold producer, Australia’s mining sector directly drives sodium cyanide demand, given the chemical’s indispensable role in the cyanidation process for gold extraction. This price-driven expansion is encouraging miners to process lower-grade and complex ore bodies that require higher concentrations of sodium cyanide for effective gold recovery. New mining projects are advancing across Western Australia, Queensland, and New South Wales, further broadening the consumption base. The combination of favorable gold prices, expanding mine output, and intensified exploration activity is creating sustained and growing demand for sodium cyanide throughout the forecast period, positioning the gold mining sector as the primary engine of market growth.

Expansion of Domestic Production Capacities

Major sodium cyanide manufacturers in Australia are undertaking substantial capacity expansions to meet rising domestic and international demand. In February 2025, Australian Gold Reagents (AGR) made a final investment decision to expand its Kwinana production facility by over 30%, increasing total sodium cyanide solution capacity to approximately 130,000 tonnes per annum along with enhanced solids production for export markets. This expansion positions AGR as one of the world’s largest sodium cyanide producers. The growth in manufacturing capacity is complemented by strategic global consolidation within the industry. In February 2024, Australia-based Orica completed the USD 640 Million acquisition of US-based Cyanco, more than doubling its sodium cyanide production capacity to approximately 240,000 tonnes per year and creating an integrated global manufacturing and distribution network. These investments are improving supply chain reliability, reducing logistics costs, and enabling Australian producers to capitalize on expanding gold mining activity both domestically and across key international markets in Asia, Africa, and the Americas.

Innovation in Sustainable Cyanide Processing Technologies

Australia is at the forefront of research and development into sustainable sodium cyanide management, recycling, and alternative processing technologies that are enhancing the efficiency and environmental profile of gold extraction. The growing adoption of the International Cyanide Management Code (ICMC) across Australian mining operations is also driving investments in closed-loop processing systems, automated monitoring equipment, and advanced detoxification infrastructure. As mining companies face increasing scrutiny over environmental performance and sustainability metrics, the development and adoption of cleaner cyanide processing technologies are enabling continued industry growth while addressing regulatory and community expectations.

Market Restraints:

What Challenges the Australia Sodium Cyanide Market is Facing?

Stringent Environmental and Safety Regulations

The highly toxic nature of sodium cyanide subjects the market to rigorous environmental and safety regulations across all Australian states and territories. Compliance with federal environmental protection legislation, state-level mining safety regulations, and international standards such as the ICMC requires substantial ongoing investment in specialized handling equipment, monitoring systems, emergency response infrastructure, and personnel training. These regulatory requirements increase operational costs for both manufacturers and end-users, particularly smaller mining operations that may lack the capital to implement comprehensive cyanide management programs.

Development of Alternative Gold Extraction Technologies

Emerging cyanide-free gold extraction methods, including thiosulfate-based and glycine-based leaching processes, present a potential long-term challenge to sodium cyanide demand. CSIRO’s cyanide-free thiosulfate technology, commercialized through Clean Mining in Western Australia, and glycine-based pilot programs at international gold operations demonstrate the viability of alternative reagents. While these alternatives currently face limitations in cost-effectiveness and gold recovery efficiency compared to cyanidation, continued technological advancement could gradually reduce the mining industry’s dependence on sodium cyanide.

Rising Logistics and Hazardous Freight Costs

The transportation of sodium cyanide as a classified dangerous good incurs significant logistical costs and operational complexities, particularly for mine sites in remote areas of Western Australia, Queensland, and the Northern Territory. Specialized containment vessels, dedicated transport routes, comprehensive insurance requirements, and strict regulatory compliance protocols contribute to elevated supply chain expenses. Recent increases in hazardous-cargo freight premiums and insurance recalibrations have further compounded these costs, placing pressure on market participants and potentially influencing procurement decisions by smaller mining operators.

Competitive Landscape:

The Australia sodium cyanide market is highly concentrated with regard to competition wherein only a few large-scale players represent a high market presence. The manufacturers compete based on production capacities, consistent supply, safety, and technical assistance services required for the mining sector. Strategic market moves such as expansions of production capacities, eco-friendly production facilities, and supply contracts with large-scale gold mining corporations represent the market competition strategy. The consolidation drive within the global market, widely represented through acquisitions within the sodium cyanide market, is further driving competition within the market. The manufacturers have started differentiating themselves on the basis of investments in low-carbon footprint production mechanisms, logistical services, and cyanide handling services.

Australia Sodium Cyanide Market Report Coverage:

|

Report Features |

Details |

|

Base Year of the Analysis |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Units |

Million USD |

|

Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

|

Product Types Covered |

Solid Sodium Cyanide, Liquid Sodium Cyanide |

|

Industries Covered |

Mining, Chemical, Dye and Textile, Pharmaceutical |

|

Sales Channels Covered |

Direct Sales, Distributor |

|

Forms Covered |

Solid, Liquid |

|

Regions Covered |

Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

|

Customization Scope |

10% Free Customization |

|

Post-Sale Analyst Support |

10-12 Weeks |

|

Delivery Format |

PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Sodium Cyanide Market Report

The Australia sodium cyanide market size was valued at USD 61.06 Million in 2025.

The Australia sodium cyanide market is expected to grow at a compound annual growth rate of 7.35% from 2026-2034 to reach USD 115.64 Million by 2034.

Solid sodium cyanide dominated the market with a share of 58.7%, driven by its superior stability in transport, ease of storage in remote mining areas, and consistent dissolution properties that enable precise dosage in gold cyanidation processes.

Key factors driving the Australia sodium cyanide market include record gold prices boosting mining activity, expansion of domestic production capacities, growing export demand, technological advancements in sustainable cyanide management, and continued gold exploration across key mining regions.

Major challenges include stringent environmental and safety regulations, rising logistics and hazardous freight costs, development of alternative gold extraction technologies, supply chain complexities for remote mine sites, and increasing community scrutiny over cyanide management practices.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)