Australia Sports Betting Market Size, Share, Trends and Forecast by Platform, Betting Type, Sports Type, and Region, 2026-2034

Australia Sports Betting Market Summary:

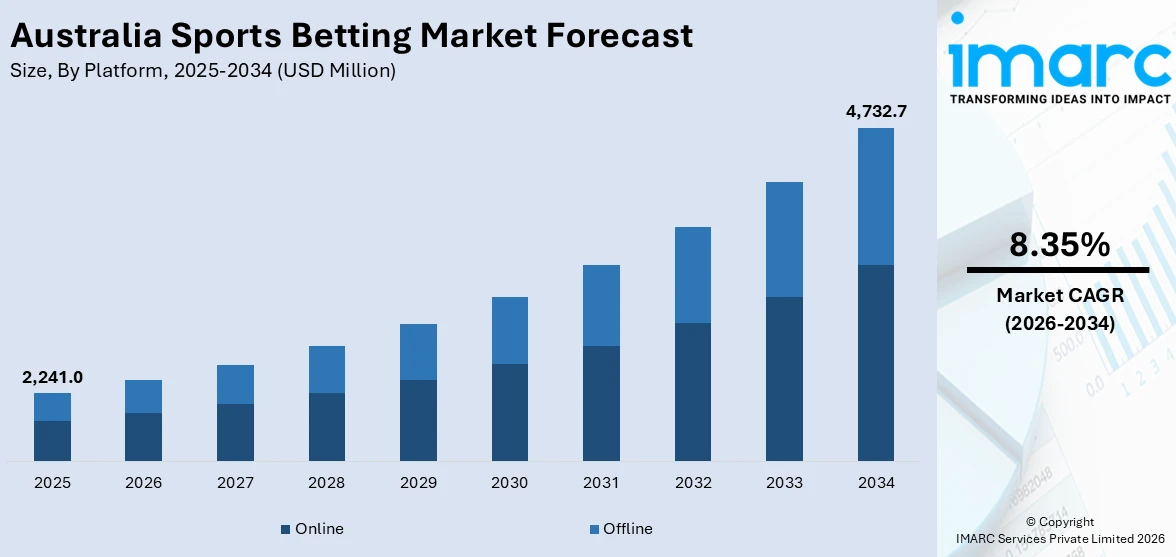

The Australia sports betting market size was valued at USD 2,241.0 Million in 2025 and is projected to reach USD 4,732.7 Million by 2034, growing at a compound annual growth rate of 8.35% from 2026-2034.

Australia’s sports betting market continues to grow steadily, supported by a deeply rooted wagering culture, increasing use of digital platforms, and a well-regulated environment that enhances consumer confidence. The rapid adoption of smartphones and seamless mobile betting experiences has transformed user engagement. At the same time, the integration of real-time data and analytics, along with a diverse and year-round sports calendar, is reshaping betting behavior.

Key Takeaways and Insights:

- By Platform: Online dominates the market with a share of 72.8% in 2025, driven by the rapid adoption of mobile applications, real-time in-play features, and seamless digital payment integrations that offer punters unmatched convenience.

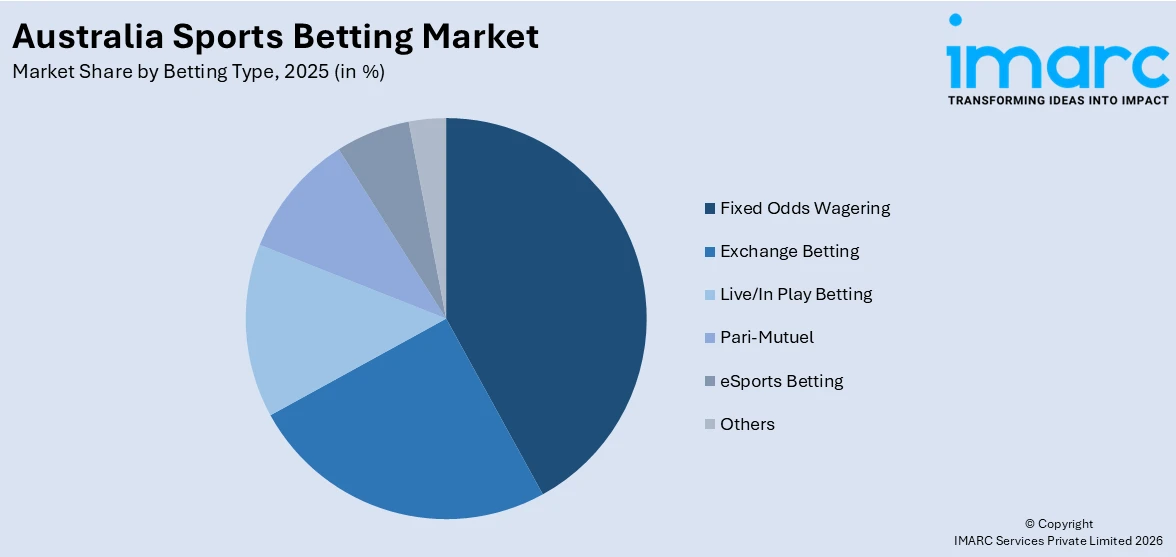

- By Betting Type: Fixed odds wagering leads with a market share of 41.6% in 2025, owing to its predictable payout structure, broad applicability across sports and racing events, and deep familiarity among Australian bettors.

- By Sports Type: Horse racing represents the largest segment with a market share of 37.9% in 2025, reflecting Australia's deeply rooted racing culture, year-round race calendar, and premium events such as the Melbourne Cup and Sydney Autumn Racing Carnival.

- By Region: Australia Capital Territory & New South Wales dominates the market with a share of 36.4% in 2025, supported by the concentration of sports infrastructure, high population density, and the headquarters of leading wagering operators.

- Key Players: The Australia sports betting market is highly competitive, characterized by a mix of established domestic operators and digital-first platforms, with competition spanning both retail outlets and rapidly expanding online and mobile betting channels.

To get more information on this market Request Sample

The Australia sports betting market is undergoing a structural transformation as consumers increasingly shift from physical retail outlets to digital and mobile platforms. This transition has redefined the competitive dynamics, with online-first operators capturing significant market share from traditional wagering businesses. The integration of advanced technologies including artificial intelligence-driven odds modeling, personalized marketing tools, and live-streaming capabilities has elevated user engagement across sporting codes. Australia's strong participation in events such as the AFL, NRL, Horse Racing Carnivals, and Big Bash Cricket League continues to generate sustained wagering activity. For instance, in May 2025, regulatory clearance was granted by Liquor & Gaming NSW for a pilot program enabling in-play betting within licensed pubs and clubs. This initiative represented a significant advancement in expanding interactive wagering access across the country’s largest betting region, highlighting a progressive shift toward modernizing traditional retail betting environments.

Australia Sports Betting Market Trends:

Accelerating Shift Toward Mobile-First Online Wagering

The migration of Australian punters from physical betting outlets to mobile platforms represents one of the most significant structural shifts in the market. Mobile devices now account for most online wagers, reflecting the convenience of placing bets anywhere and at any time. Operators have responded by investing heavily in intuitive app design, push notification features, and exclusive mobile-only promotions that enhance user retention and drive Australia sports betting market growth. Smartphone penetration combined with widespread broadband connectivity has made mobile the primary access point for wagering activity nationally.

Rising Adoption of Data Analytics and AI-Powered Personalization

Betting operators are increasingly leveraging machine learning algorithms and real-time data analytics to deliver personalized wagering experiences. Predictive modeling, behavior-based odds customization, and intelligent recommendation engines are transforming how consumers interact with sports betting platforms. These technologies enable operators to tailor promotional offers and market suggestions to individual betting histories, improving satisfaction and session depth. The growing use of data partnerships with sporting bodies further enriches the analytics ecosystem, providing detailed player and game statistics that underpin sophisticated wagering products.

Growing Appetite for Exotic and Multi-Sport Betting Markets

Australian punters are demonstrating a broadening appetite beyond traditional racing and football wagers toward exotic betting formats, including same-game multi-bets and accumulator products. The expansion of wagering options across international sports such as the English Premier League, NBA, and global cricket events has attracted new demographic segments. Operators are capitalizing on major international tournaments to introduce specialized markets and competitive odds. This diversification of sports coverage and bet types is deepening market participation and increasing average transaction values across both established and emerging sports wagering segments.

Market Outlook 2026-2034:

The Australia sports betting market is expected to experience sustained growth over the coming years, driven by continued digital adoption, an evolving regulatory landscape, and rising consumer engagement across a broader mix of sports and betting formats. Advancements in mobile platforms and user experience are enhancing accessibility and participation. At the same time, ongoing innovation in live betting features, responsible gambling technologies, and secure payment solutions is influencing how operators design their offerings, positioning the market for steady expansion and transformation. The market generated a revenue of USD 2,241.0 Million in 2025 and is projected to reach a revenue of USD 4,732.7 Million by 2034, growing at a compound annual growth rate of 8.35% from 2026-2034.

Australia Sports Betting Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Platform |

Online |

72.8% |

|

Betting Type |

Fixed Odds Wagering |

41.6% |

|

Sports Type |

Horse Racing |

37.9% |

|

Region |

Australia Capital Territory & New South Wales |

36.4% |

Platform Insights:

- Offline

- Online

Online dominates the market with a share of 72.8% of total of the Australia sports betting market in 2025.

The online platform segment has established itself as the primary channel through which Australian bettors engage with sports wagering. The proliferation of licensed digital operators offering feature-rich mobile applications, live streaming, and real-time odds updates has fundamentally displaced traditional physical betting venues as the preferred wagering interface. Enhanced user interfaces, seamless registration processes, and a broad array of deposit options including digital wallets have lowered friction for new entrants, expanding the overall wagering population. The convenience of placing bets from any location at any time has proven particularly compelling for younger demographic cohorts who are at the forefront of online adoption in Australia.

Operators in the online segment have made substantial investments in proprietary technology platforms that integrate real-time data feeds, personalization tools, and secure payment systems. The introduction of hybrid models that combine digital interactivity with physical retail environments reflects efforts to meet evolving consumer expectations for seamless, real-time wagering experiences while remaining compliant with regulatory requirements. Intense competition within the online space continues to drive innovation in product features and promotional strategies, helping operators maintain high levels of user engagement and differentiation in a rapidly evolving market.

Betting Type Insights:

Access the comprehensive market breakdown Request Sample

- Fixed Odds Wagering

- Exchange Betting

- Live/In Play Betting

- Pari-Mutuel

- eSports Betting

- Others

Fixed odds wagering represents the largest share of 41.6% of the total of Australia sports betting market in 2025.

Fixed odds wagering dominates the Australia sports betting market because it offers clarity, predictability, and ease of understanding for bettors. Users know their exact potential return at the time of placing a bet, which reduces uncertainty compared to variable payout models. This transparency appeals to both casual and experienced bettors, making it widely accessible. Additionally, fixed odds are heavily integrated into digital platforms, allowing seamless placement across a wide range of sports and events, further strengthening its popularity and consistent usage.

Another key driver is the flexibility and product innovation associated with fixed odds betting. Operators offer features such as live betting, cash-out options, and customized multi-bet combinations, enhancing user engagement and control. The format also supports competitive pricing and promotional strategies, encouraging frequent participation. Its compatibility with real-time data and mobile interfaces enables dynamic odds updates, aligning with modern betting preferences. Together, these advantages make fixed odds wagering the preferred and most dominant segment in the Australian sports betting landscape.

Sports Type Insights:

- Football

- Basketball

- Baseball

- Horse Racing

- Cricket

- Hockey

- Others

Horse racing represents the highest revenue share of 37.9% of the total of the Australia sports betting market in 2025.

Horse racing dominates the Australia sports betting market largely due to its deep cultural roots and long-standing integration with the country’s wagering ecosystem. It has historically been one of the most popular and widely followed betting sports, supported by frequent race schedules across multiple states. Unlike seasonal sports, horse racing events occur year-round, offering continuous betting opportunities. This consistent availability, combined with established pari-mutuel betting systems and widespread familiarity among bettors, ensures strong and stable wagering volumes compared to other sports.

Another key factor is the extensive retail wagering infrastructure built around horse racing, including licensed venues, on-course betting, and broadcast coverage that enhances accessibility and engagement. The sport benefits from detailed form guides, statistical data, and expert analysis, which encourage informed betting and repeat participation. Additionally, strong industry support, including sponsorships and partnerships, sustains visibility and interest. Together, these factors reinforce horse racing’s dominant position by combining tradition, accessibility, and consistent betting activity across both retail and digital channels.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales leads the market with a share of 36.4% of total of the Australia sports betting market in 2025.

The Australian Capital Territory and New South Wales lead the sports betting market due to their well-established regulatory frameworks and concentration of licensed wagering infrastructure. These regions host a large number of betting venues, including pubs, clubs, and dedicated outlets, supported by strong oversight that fosters consumer trust. High population density, particularly in New South Wales, contributes to a larger and more active betting base. Additionally, the presence of major sporting events and racing activities ensures consistent engagement and betting opportunities throughout the year.

Another key factor is the advanced digital adoption and seamless integration of online and retail betting channels in these regions. Consumers benefit from widespread access to mobile platforms, real-time betting features, and convenient payment systems. Strong transport connectivity and urban development further support accessibility to betting venues and events. Moreover, proactive regulatory bodies in these regions continue to enable controlled innovation while maintaining responsible gambling standards, reinforcing their leading position in the overall market.

Market Dynamics:

Growth Drivers:

Why is the Australia Sports Betting Market Growing?

Deeply Rooted Sports Culture and Expanding Sports Calendar

Australia possesses one of the world's most deeply embedded sports betting cultures, where wagering on racing and sporting events is a widely accepted recreational activity spanning multiple generations. The country's year-round sporting calendar, encompassing horse racing, AFL, NRL, cricket, tennis, and basketball, provides a continuous pipeline of wagering opportunities that sustains consumer engagement across all seasons. Major international events broadcast into Australian prime time further amplify betting activity, particularly for soccer, golf, and combat sports. The integration of betting operators as official partners of major sporting codes has normalized wagering within sports media consumption, reinforcing participation across both experienced and new punters. This cultural affinity for sports engagement and prediction has historically underpinned the market's resilience and formed the foundational basis for ongoing demand growth in the Australia sports betting market.

Technological Innovation and Smartphone-Led Digital Adoption

The prevalence of smartphones and high-speed mobile internet has essentially changed the way Australians make sports bets and set the stage for a continuing shift to digital sports betting platforms. Licensed operator mobile applications now allow real-time odds, live streaming, push alerts, and one-second bet placement, duplicating and exceeding the experience of traditional betting outlets. The growth of same-game multi-betting and the recommendation and exploration of personalization based on algorithms have greatly increased the level of user interaction, making betting more frequent and increasing the time spent on digital platforms. Meanwhile, the introduction of hybrid types of wagering that incorporate mobile betting into the physical venue settings indicates that there should be a transition toward integrating digital convenience into the traditional retail networks. This strategy emphasizes how technological innovation is closing the offline and online ecosystems and how more users in Australia can have a seamless and interactive betting experience.

Regulatory Framework Supporting Licensed and Responsible Wagering

Australia’s multi-layered regulatory framework, led federally by the Interactive Gambling Act 2001 and supported by state-level wagering authorities, creates a structured environment that promotes investment while ensuring strong consumer protection. Initiatives such as the BetStop National Self-Exclusion Register and the National Consumer Protection Framework establish consistent responsible gambling standards across the market. Active enforcement by the Australian Communications and Media Authority against illegal offshore operators further safeguards market integrity. Additionally, state-based licensing systems encourage competition and ongoing investment in advanced wagering technologies.

Market Restraints:

What Challenges the Australia Sports Betting Market is Facing?

Tightening Gambling Advertising Regulations

Australia's regulatory environment for gambling advertising is undergoing significant scrutiny, with both federal and state authorities advancing restrictions on when and how betting operators can advertise during live sporting events. New South Wales has implemented a complete ban on gambling advertising on public transport, while federal legislators are actively considering a phased prohibition on sports betting advertisements across broadcast and digital platforms. These restrictions threaten operators' ability to acquire new customers and sustain brand visibility during peak wagering periods, particularly around major sporting codes.

Escalating Point-of-Consumption Taxes and Compliance Costs

State and territory governments have progressively increased point-of-consumption taxes on wagering turnover, materially raising the cost burden on licensed bookmakers. The Northern Territory government's plans to further increase wagering taxes have drawn criticism from operators who cite shrinking margins. Simultaneously, expanding compliance obligations under Anti-Money Laundering reforms and stricter customer due diligence requirements are adding operational costs for wagering providers. These cumulative fiscal and regulatory pressures constrain profitability and may discourage new market entrants.

Consumer Spending Pressures and Responsible Gambling Obligations

Rising cost-of-living pressures in Australia have constrained discretionary spending, leading to softer engagement across leisure activities such as sports betting. At the same time, tighter regulatory measures, including pre-commitment requirements, restrictions on credit-based betting, and enhanced harm minimisation frameworks, are reshaping user behavior. These changes are encouraging more controlled wagering patterns while increasing compliance obligations for operators and potentially limiting overall spending per user.

Competitive Landscape:

The Australia sports betting market is characterized by a highly competitive landscape comprising established domestic operators and well-funded international digital platforms. Competition spans both retail wagering networks and rapidly expanding online channels, with operators leveraging extensive venue presence and advanced mobile platforms. Market dynamics are driven by aggressive promotional strategies, continuous product innovation, and the integration of real-time data analytics to enhance user engagement. Increasing focus on responsible gambling compliance also shapes competitive positioning. Additionally, ongoing consolidation through mergers and acquisitions continues to influence market structure and intensify competition across the industry.

Recent Developments:

- In February 2026, the Australian Communications and Media Authority (ACMA) imposed a penalty of AUD 158,000 on Tabcorp Holdings for accepting online in-play sports bets, in breach of the Interactive Gambling Act's prohibition on digital in-play wagering. The enforcement action highlighted ongoing regulatory scrutiny of how licensed operators navigate the boundary between lawful telephone-based in-play services and restricted online channels. The ACMA simultaneously requested Australian internet service providers to block additional illegal offshore gambling websites, reinforcing the country's effort to protect consumers and direct wagering activity toward licensed domestic operators.

- In February 2025, Tabcorp secured regulatory approval from Liquor & Gaming NSW to pilot in-play betting via mobile app terminals in licensed pub and club venues in New South Wales, in a first for Australia's physical wagering network. An initial two-venue trial at Cheers Sports Bar and Grill Sydney and Canterbury-Hurlstone Park RSL, in Hurlstone Park, was launched with plans to expand to 20 venues within weeks. Newly appointed CEO Gillon McLachlan described the tap-in-play initiative as the future of retail wagering, aiming to modernize Tabcorp's network of approximately 3,800 licensed venues by enabling live sport betting through digital terminals while remaining compliant with existing gambling regulations.

Australia Sports Betting Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Platform Covered | Offline, Online |

| Betting Types Covered | Fixed Odds Wagering, Exchange Betting, Live/In Play Betting, Pari-Mutuel, eSports Betting, Others |

| Sports Types Covered | Football, Basketball, Baseball, Horse Racing, Cricket, Hockey, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Sports Betting Market Report

The Australia sports betting market size was valued at USD 2,241.0 Million in 2025.

The Australia sports betting market is expected to grow at a compound annual growth rate of 8.35% from 2026-2034 to reach USD 4,732.7 Million by 2034.

Online platforms hold the largest market share at 72.8% in 2025, reflecting widespread mobile adoption, the convenience of real-time wagering access, and the competitive digital product offerings of Australia's major licensed bookmakers, which have successfully transitioned punters from physical venues to digital channels.

Key factors driving the Australia sports betting market include a deeply embedded sports wagering culture, rapid smartphone and mobile internet penetration, technological innovations in live and in-play betting, year-round racing and sports event calendars, and a structured regulatory framework that supports licensed operator activity and consumer confidence.

Major challenges include tightening gambling advertising regulations at federal and state levels, escalating point-of-consumption taxes and compliance costs, growing mandatory responsible gambling obligations, consumer spending pressures reducing discretionary wagering budgets, and increasing regulatory enforcement actions that constrain product and marketing flexibility for licensed operators.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade