Australia Telehealth Market Size, Share, Trends and Forecast by Component, Communication Technology, Hosting Type, Application, End-User, and Region, 2026-2034

Australia Telehealth Market Summary:

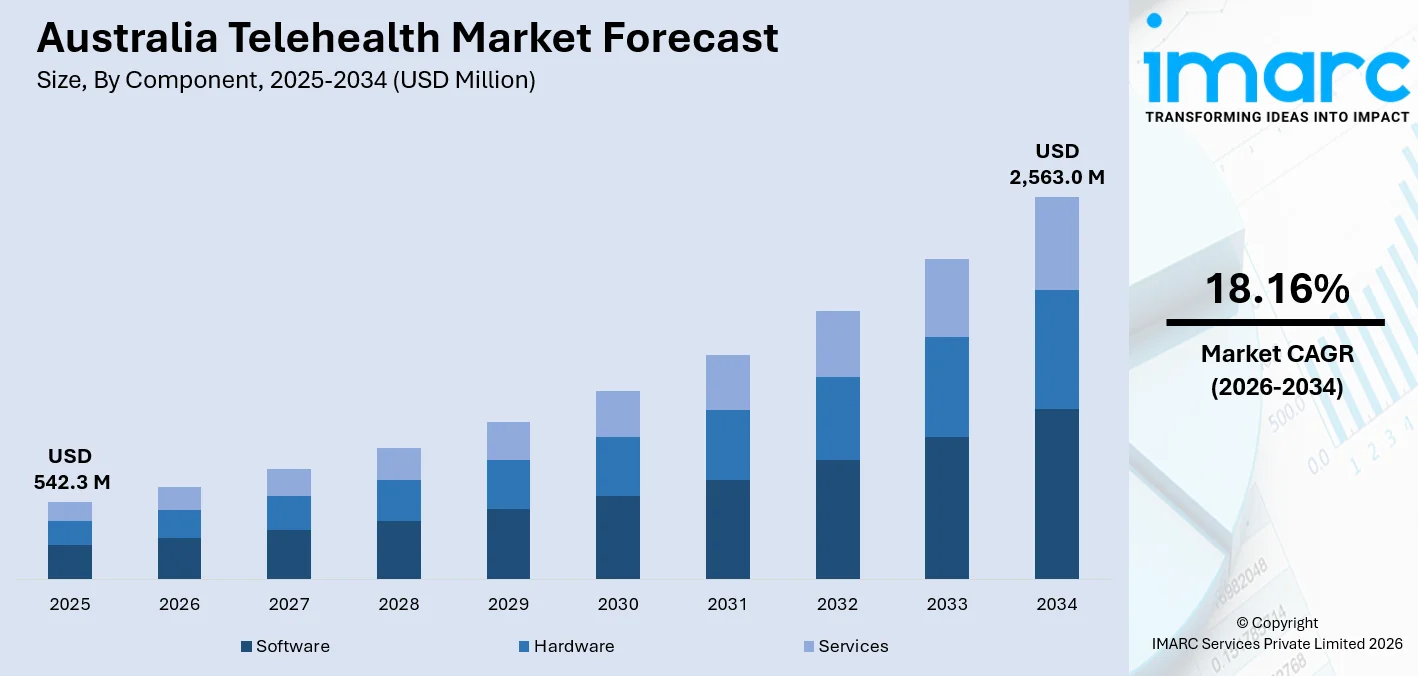

The Australia telehealth market size was valued at USD 542.3 Million in 2025 and is projected to reach USD 2,563.0 Million by 2034, growing at a compound annual growth rate of 18.16% from 2026-2034.

The Australia telehealth market is gaining strong momentum as the country accelerates digital transformation across healthcare delivery. Growing demand for remote care, particularly in rural and underserved areas, is driving widespread adoption. Expanding internet connectivity, a rising elderly population, and increasing prevalence of chronic conditions are compelling healthcare providers to embrace virtual consultation platforms, thereby strengthening the Australia telehealth market share.

Key Takeaways and Insights:

- By Component: Software dominates the market with a share of 42.3% in 2025, reflecting strong adoption of integrated virtual care platforms and clinical management tools across healthcare facilities and service providers nationwide.

- By Communication Technology: Video conferencing leads the market with a share of 48.5% in 2025, emerging as the preferred mode for real-time clinical interactions between patients and healthcare professionals across Australia.

- By Hosting Type: Cloud-based and web-based represents the largest segment with a market share of 62.4% in 2025, enabling scalable, flexible, and cost-efficient telehealth delivery across diverse healthcare settings and geographies.

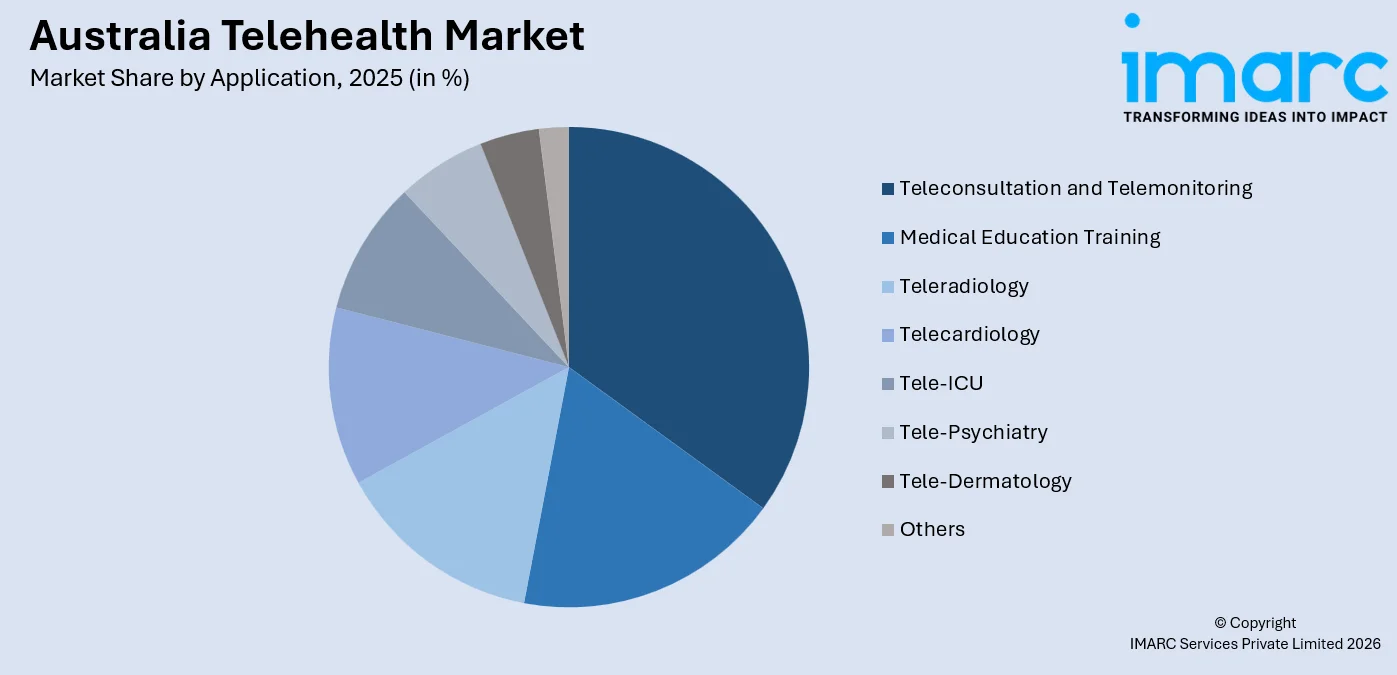

- By Application: Teleconsultation and telementoring dominates the market with a share of 35.2% in 2025, representing the most widely used telehealth application for connecting patients with specialists and primary care practitioners remotely.

- By End-User: Providers represents the largest segment with a market share of 45.3% in 2025, driven by growing adoption of virtual care tools to enhance care delivery efficiency and patient management capabilities.

- By Region: Australia Capital Territory & New South Wales leads the market with a share of 34.5% in 2025, supported by dense population, robust digital infrastructure, and strong healthcare network concentration.

- Key Players: The Australia telehealth market is moderately competitive, with a mix of domestic and international players expanding virtual care capabilities, investing in platform innovation, and forming strategic partnerships to strengthen market presence and enhance patient outcomes. Some of the key players operating in the market include, Coviu, Docto, Doctors on Demand, Eucalyptus, GP2U, Healthengine, Medmate Australia Pty Ltd, My Emergency Doctor, and Teledoc Australia.

To get more information on this market Request Sample

Australia’s telehealth market is undergoing a significant transformation driven by digital innovation, evolving patient expectations, and progressive healthcare policy reforms. The permanent inclusion of telehealth services within the national universal health insurance framework has shifted virtual care from an emergency response mechanism to a core component of mainstream healthcare. In June 2025, Telstra Health announced a strategic partnership with Salesforce and Snowflake to build a unified cloud-based healthcare platform aimed at improving patient access and integrating clinical data across systems. Heightened investment in digital health infrastructure, growing interoperability between electronic health records and virtual platforms, and widespread smartphone penetration are collectively accelerating adoption. Mental health services, chronic disease management, and specialist consultations are witnessing particularly strong uptake. As the country advances its national digital health strategy, integration of artificial intelligence, remote patient monitoring, and cloud-based platforms continues to elevate the scope and quality of telehealth services across Australia.

Australia Telehealth Market Trends:

Expansion of Mental Health Services via Telehealth

The growing demand for accessible mental health support is reshaping Australia’s telehealth landscape. Remote psychiatric consultations, digital therapy sessions, and telepsychiatry services are becoming mainstream components of mental healthcare. In August 2025, Teladoc Health acquired Australian virtual care provider Telecare, a platform with over 300 specialists delivering remote consultations, to expand access to specialist and mental health services across underserved regions. Greater acceptance of virtual mental health appointments is broadening service reach and addressing long-standing gaps in mental health access, particularly for individuals in regional and remote communities with limited proximity to specialist mental health professionals.

Integration of Artificial Intelligence in Virtual Care Platforms

Artificial intelligence is increasingly being embedded into telehealth platforms to enhance diagnostic accuracy, automate administrative workflows, and support clinical decision-making. AI-driven triage tools and symptom assessment systems are gaining prominence, enabling providers to deliver more targeted virtual consultations. In July 2025, Eucalyptus partnered with AI platform Amigo to integrate AI-powered health assistants into its telehealth services, supporting patient triage, care coordination, and virtual health coaching within its digital clinics. This technological integration is enhancing service quality and operational efficiency, supporting Australia telehealth market growth and positioning AI as a cornerstone of next-generation virtual care delivery.

Shift Toward Cloud-Based Platforms and Remote Patient Monitoring

The widespread transition to cloud-based telehealth platforms is enabling scalable and secure delivery of virtual healthcare services. Growing adoption of remote patient monitoring technologies and wearable health devices is facilitating continuous management for chronic disease patients. In September 2024, ResMed unveiled new digital and cloud-connected health solutions designed to deliver personalized insights and enable continuous remote monitoring, supporting collaboration between patients and healthcare providers in virtual care settings. This shift supports seamless data exchange between patients and providers, fundamentally transforming care delivery models and enabling more proactive, data-driven approaches to healthcare management across Australia’s expanding digital health sector.

Market Outlook 2026-2034:

The Australia telehealth market is gaining strong momentum as the country accelerates digital transformation across healthcare delivery. Growing demand for remote care, particularly in rural and underserved areas, is driving widespread adoption among providers and patients alike. Expanding internet connectivity, a rising elderly population, and increasing prevalence of chronic conditions are compelling healthcare organisations to embrace virtual consultation platforms. Supportive government policy frameworks and advancements in digital infrastructure continue to reinforce the Australia telehealth market share. The market generated a revenue of USD 542.3 Million in 2025 and is projected to reach a revenue of USD 2,563.0 Million by 2034, growing at a compound annual growth rate of 18.16% from 2026-2034.

Australia Telehealth Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Component |

Software |

42.3% |

|

Communication Technology |

Video Conferencing |

48.5% |

|

Hosting Type |

Cloud-Based and Web-Based |

62.4% |

|

Application |

Teleconsultation and Telementoring |

35.2% |

|

End-User |

Providers |

45.3% |

|

Region |

Australia Capital Territory & New South Wales |

34.5% |

Component Insights:

- Software

- Hardware

- Services

The software dominates with a market share of 42.3% of the total Australia telehealth market in 2025.

Software has emerged as the backbone of Australia's telehealth ecosystem, enabling seamless delivery of virtual consultations, clinical documentation, and patient engagement across diverse healthcare settings. Its ability to integrate with existing health information systems, support real-time communication between providers and patients, and automate administrative workflows has made it indispensable for healthcare organisations transitioning toward digital care models. Growing demand for interoperable, scalable platforms continues to reinforce software's central role in shaping the future of virtual healthcare delivery.

The rising adoption of software-driven telehealth solutions is being further accelerated by the need for platforms that can support chronic disease management, mental health services, and specialist referral coordination. Healthcare providers are increasingly prioritising software systems that offer robust data security, user-friendly interfaces, and compatibility with remote monitoring devices. As clinical confidence in virtual care grows and regulatory frameworks continue to mature, software investment is intensifying across both public and private healthcare sectors, cementing its position as the most strategically significant component within Australia's telehealth market.

Communication Technology Insights:

- Video Conferencing

- mHealth Solutions

- Others

The video conferencing leads with a share of 48.5% of the total Australia telehealth market in 2025.

Video conferencing has firmly established itself as the preferred communication modality for virtual healthcare consultations across Australia. Its capacity to replicate face-to-face clinical interactions through high-quality audio-visual connectivity makes it uniquely suited for general practice appointments, specialist referrals, and mental health sessions. Clinicians and patients alike have embraced video conferencing for its ability to convey visual clinical cues, build therapeutic rapport, and support accurate diagnoses in ways that telephone-based alternatives cannot adequately replicate, making it the most trusted real-time telehealth communication channel available.

Continued investment in broadband infrastructure and the widespread availability of compatible devices have further lowered barriers to video conferencing adoption across both metropolitan and regional communities. Healthcare providers are increasingly integrating video platforms directly into clinical management systems, enabling streamlined appointment scheduling, secure consultations, and seamless electronic record updates within a single workflow. As patient familiarity with virtual consultations deepens and provider confidence in remote examination techniques grows, video conferencing is expected to remain the dominant communication technology underpinning Australia's evolving telehealth landscape.

Hosting Type Insights:

- Cloud-Based and Web-Based

- On-Premises

The cloud-based and web-based dominates with a market share of 62.4% of the total Australia telehealth market in 2025.

Cloud-based and web-based hosting has become the infrastructure foundation of choice for telehealth service delivery across Australia. Its inherent scalability allows healthcare organisations to expand virtual care capabilities rapidly without significant upfront capital investment in physical infrastructure. The ability to support simultaneous access across multiple locations, enable real-time data sharing, and deliver automatic software updates makes cloud and web-based environments particularly well-suited to the dynamic and geographically dispersed nature of Australia's healthcare system, supporting both large hospital networks and smaller primary care practices.

Beyond scalability, cloud-based and web-based platforms offer meaningful advantages in terms of interoperability, disaster recovery, and regulatory compliance. Healthcare providers are drawn to these environments for their capacity to integrate with electronic health records, remote monitoring systems, and pharmacy platforms, enabling a more connected and coordinated care experience. As data governance frameworks evolve and provider confidence in cloud security strengthens, the preference for hosted digital infrastructure continues to grow, making cloud and web-based solutions the most strategically adopted hosting model within Australia's expanding telehealth sector.

Application Insights:

Access the comprehensive market breakdown Request Sample

- Teleconsultation and Telemonitoring

- Medical Education Training

- Teleradiology

- Telecardiology

- Tele-ICU

- Tele-Psychiatry

- Tele-Dermatology

- Others

The teleconsultation and telementoring leads with a share of 35.2% of the total Australia telehealth market in 2025.

Teleconsultation and telementoring has become the most widely adopted application within Australia's telehealth market, fundamentally transforming how patients access care and how clinicians deliver it. Virtual consultations enable patients to connect with general practitioners and specialists without the burden of travel, reducing wait times and improving care continuity for individuals managing ongoing health conditions. This application has proven particularly vital in extending specialist access to rural and remote communities, where geographic isolation has historically created significant barriers to timely medical care and clinical follow-up.

Telementoring adds a further dimension by facilitating knowledge transfer between experienced specialists and frontline clinicians operating in underserved areas. Through virtual supervision and real-time clinical guidance, providers in regional settings can deliver a higher standard of care without requiring specialist relocation. This collaborative model is strengthening clinical capability across Australia's healthcare workforce while improving patient outcomes in communities that were previously dependent on long-distance referrals. The combination of direct patient care and professional development makes this application uniquely valuable across the full spectrum of virtual healthcare delivery.

End-User Insights:

- Providers

- Patients

- Payers

- Others

The providers dominates with a market share of 45.3% of the total Australia telehealth market in 2025.

Healthcare providers represent the most significant end-user group driving telehealth adoption across Australia, as hospitals, general practices, and specialist clinics increasingly integrate virtual care platforms into their service delivery models. The transition toward telehealth has enabled providers to extend their reach beyond physical catchment areas, manage larger patient volumes with greater efficiency, and maintain care continuity for patients with chronic or complex health needs. Permanent reimbursement arrangements have removed the financial uncertainty that previously constrained provider investment in virtual care infrastructure and clinical workflows.

The depth of provider engagement with telehealth is expanding well beyond basic video consultations, encompassing remote patient monitoring, digital care coordination, and AI-assisted clinical decision support. Providers are investing in platforms that offer seamless integration with electronic health records and diagnostic systems, enabling more informed and responsive patient management. As workforce pressures mount and demand for specialist services grows, telehealth is increasingly positioned by providers not as a supplementary offering but as a core component of sustainable, high-quality healthcare delivery capable of meeting the evolving needs of Australia's patient population.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory and New South Wales exhibits a clear dominance with a 34.5% share of the total Australia telehealth market in 2025.

Australia Capital Territory and New South Wales leads Australia's telehealth market, underpinned by a concentration of major healthcare institutions, government health agencies, and technology providers that collectively drive innovation and adoption. The region's dense urban population, strong digital connectivity, and well-established healthcare workforce have created fertile conditions for widespread virtual care integration. Sydney's position as a national hub for health technology investment and the ACT's role as a centre for health policy development continue to reinforce this region's prominence within the national telehealth landscape.

Beyond metropolitan centres, this region also encompasses significant rural and peri-urban communities where telehealth is playing an increasingly vital role in bridging access gaps. Healthcare providers across New South Wales have been early adopters of virtual care programs targeting chronic disease management, mental health services, and aged care support. Strong collaboration between public health networks, private providers, and digital health innovators continues to generate new service models and platform capabilities, ensuring that this region maintains its leadership position as Australia's most active and progressive telehealth market.

Market Dynamics:

Growth Drivers:

Why is the Australia Telehealth Market Growing?

Government Policy Support and Medicare Reimbursement Frameworks

The sustained commitment of government bodies to embedding virtual care within the national healthcare framework is a primary driver of market growth. The permanent inclusion of telehealth services within the country’s universal health insurance program has legitimised virtual consultations as a standard, reimbursable component of medical practice, reducing financial barriers for both providers and patients. In May 2024, Australian telehealth startup Updoc secured a $20 million investment from Bailador Technology Investments to expand its digital consultation platform and enhance service accessibility, particularly for patients in regional areas. Federal investment in digital health strategies and national roadmaps has accelerated supporting infrastructure development, including interoperability standards and secure data exchange systems. Ongoing government collaboration with healthcare stakeholders to refine reimbursement models and expand eligible telehealth services continues to strengthen adoption and broaden virtual care delivery. This regulatory and financial foundation provides the stability required to attract long-term investment in telehealth technology and services across the country.

Rising Prevalence of Chronic Diseases and Demand for Continuous Care

The increasing burden of chronic conditions, including cardiovascular disease, diabetes, respiratory disorders, and mental health challenges, is a significant driver of telehealth adoption. Managing these conditions effectively requires consistent monitoring, regular clinical interactions, and timely specialist access, all of which telehealth platforms are uniquely positioned to facilitate. Patients benefit from remote monitoring tools, virtual check-ins, and digital care coordination, reducing the need for hospital visits and enabling proactive, preventive care approaches. Growing recognition among clinicians and healthcare administrators that virtual care can effectively complement traditional chronic disease management is driving sustained investment in telehealth solutions. As the population ages and chronic disease prevalence continues to rise, demand for accessible and continuous remote care models will further propel market expansion across Australia.

Technological Advancements and Expanding Digital Health Infrastructure

Rapid advances in digital technology are substantially expanding the capabilities of Australia’s telehealth ecosystem. High-speed broadband networks, growing smartphone penetration, and wearable health devices are enhancing the quality and reliability of virtual care delivery. Artificial intelligence integration is enabling smarter patient triage, automated health monitoring, and data-driven clinical decision support, elevating care well beyond simple video consultations. In March 2024, Microsoft introduced new AI and data capabilities within its healthcare solutions, including enhancements to Microsoft Cloud for Healthcare that enable unified data integration, advanced analytics, and improved clinical decision-making across care settings. Electronic health record interoperability is facilitating seamless data exchange between virtual and in-person care settings, supporting comprehensive and continuity-focused patient management. These technological developments are empowering providers to deliver sophisticated telehealth services, making virtual care a viable and attractive option across an expanding range of clinical disciplines and fundamentally transforming healthcare delivery throughout Australia.

Market Restraints:

What Challenges the Australia Telehealth Market is Facing?

Digital Literacy Barriers and Accessibility Challenges

Significant portions of Australia’s population, particularly elderly individuals and those from linguistically diverse communities, face challenges in accessing and effectively using telehealth services. Limited familiarity with digital devices, inadequate technical support structures, and language barriers restrict meaningful engagement with virtual care platforms. These accessibility gaps risk widening health disparities rather than addressing them, creating a persistent challenge for equitable telehealth expansion across all demographic segments of the population.

Data Privacy and Cybersecurity Concerns

Growing digitisation of healthcare intensifies concerns regarding patient data privacy, security vulnerabilities, and cyber threats targeting telehealth platforms. Providers must navigate complex regulatory obligations around data protection while implementing robust cybersecurity measures to safeguard sensitive health information. Patient hesitation to share health data digitally can limit telehealth uptake, particularly among those with heightened awareness of data breach risks or lower trust in online platforms, constraining broader market adoption.

Inconsistent Broadband Infrastructure in Remote and Rural Regions

Despite significant national investment in digital connectivity, broadband infrastructure quality remains uneven across Australia’s vast regional and remote areas. Unreliable internet access creates barriers to seamless telehealth consultations, limiting the platform’s effectiveness precisely in communities where remote care is most critically needed. The persistence of connectivity gaps constrains the transformative potential of telehealth in bridging healthcare access disparities between urban centres and rural populations.

Competitive Landscape:

The Australia telehealth market is characterised by a moderately competitive landscape, with a diverse mix of domestic and international players striving to capture share across various care segments. Market participants are actively investing in the development of more sophisticated virtual care platforms, incorporating features such as artificial intelligence-powered triage, integrated electronic health records, remote patient monitoring, and omni-channel patient engagement tools. Strategic partnerships between telehealth platform providers, healthcare networks, and health insurance organisations are reshaping competitive dynamics, enabling broader service reach and accelerated adoption. Mergers and acquisitions are emerging as a key competitive strategy, as established players seek to consolidate capabilities and expand specialist service networks. The growing emphasis on regulatory compliance, data security, and seamless system interoperability is influencing competitive positioning, as providers differentiate on clinical credibility, platform reliability, and the breadth of specialties supported through their virtual care ecosystems.

Some of the key players include:

- Coviu

- Docto

- Doctors on Demand

- Eucalyptus

- GP2U

- Healthengine

- Medmate Australia Pty Ltd

- My Emergency Doctor

- Teledoc Australia

Recent Developments:

- In February 2026: Hims & Hers Health announced the acquisition of Eucalyptus Health in a deal valued at up to $1.15–$1.6 billion. The transaction supports its expansion into Australia and Asia while enhancing personalized telehealth services and digital care capabilities.

Australia Telehealth Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Software, Hardware, Others |

| Communication Technologies Covered | Video Conferencing, mHealth Solutions, Others |

| Hosting Types Covered | Cloud-Based and Web-Based, On-Premises |

| Applications Covered | Teleconsultation and Telemonitoring, Medical Education Training, Teleradiology, Telecardiology, Tele-ICU, Tele-Psychiatry, Tele-Dermatology, Others |

| End-Users Covered | Providers, Patients, Payers, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Coviu, Docto, Doctors on Demand, Eucalyptus, GP2U, Healthengine, Medmate Australia Pty Ltd, My Emergency Doctor, Teledoc Australia, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Telehealth Market Report

The Australia telehealth market size was valued at USD 542.3 Million in 2025.

The Australia telehealth market is expected to grow at a compound annual growth rate of 18.16% from 2026-2034 to reach USD 2,563.0 Million by 2034.

Software, holding the largest revenue share of 42.3%, is central to Australia’s telehealth ecosystem, enabling seamless virtual consultations, electronic health record integration, and clinical workflow automation across diverse healthcare settings nationwide.

Key factors driving the Australia telehealth market include permanent Medicare reimbursement for telehealth services, expanding digital health infrastructure, rising chronic disease prevalence, growing mental health service demand, increasing artificial intelligence integration in virtual care platforms, and improving broadband access in regional areas.

Major challenges include digital literacy gaps among elderly and diverse communities, data privacy and cybersecurity concerns, inconsistent broadband access in remote areas, and workforce adaptation requirements for transitioning to virtual care delivery models.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)