Australia Unified Communications Market Size, Share, Trends and Forecast by Component, Deployment Mode, Organization Size, End User, and Region, 2026-2034

Australia Unified Communications Market Summary:

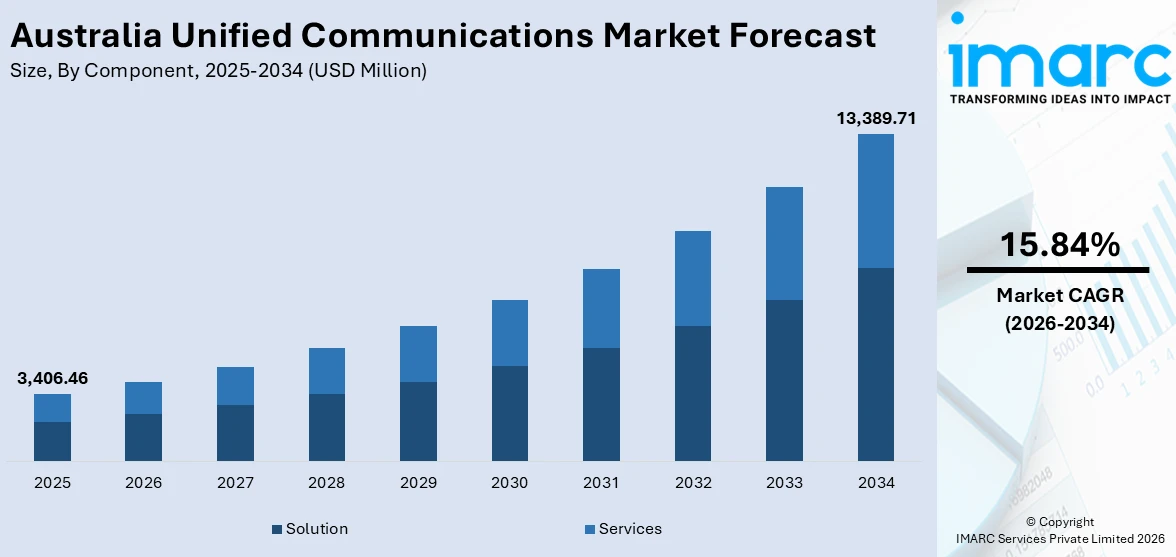

The Australia unified communications market size was valued at USD 3,406.46 Million in 2025 and is projected to reach USD 13,389.71 Million by 2034, growing at a compound annual growth rate of 15.84% from 2026-2034.

Australia's unified communications market is undergoing a transformative phase, driven by the rapid uptake of hybrid and remote work models across industries. Enterprises are increasingly investing in integrated platforms that unify voice, video, messaging, and collaboration functions under a single digital ecosystem, enabling seamless connectivity for distributed teams. The proliferation of cloud-based solutions and the ongoing rollout of high-speed 5G networks are further accelerating the pace of digital transformation across corporate and public sectors. The integration of artificial intelligence and automation in communication platforms is enhancing operational efficiency, enabling intelligent meeting management, real-time transcription, and predictive analytics. Growing demand from large enterprises, the education sector, and government agencies for secure, scalable, and interoperable communication infrastructure continues to expand the Australia unified communications market share.

Key Takeaways and Insights:

- By Component: Solution dominates the market with a share of 71.5% in 2025, driven by the high adoption of integrated software suites that address diverse communication needs, including messaging, conferencing, and telephony, across enterprises of all sizes.

- By Solution Sub-Segment: Audio and video conferencing leads the market with a share of 32.5% in 2025, owing to the growing prevalence of hybrid work arrangements and the demand for high-quality, real-time visual collaboration tools among distributed teams.

- By Deployment Mode: Hosted leads the market with a share of 52.5% in 2025, reflecting the strong preference for cloud-delivered communication solutions that offer scalability, reduced capital expenditure, and seamless access from any location.

- By Organization Size: Large enterprises dominate the market with a share of 56.8% in 2025, supported by their extensive IT budgets, complex communication requirements, and the need for enterprise-grade security, compliance, and multi-location connectivity.

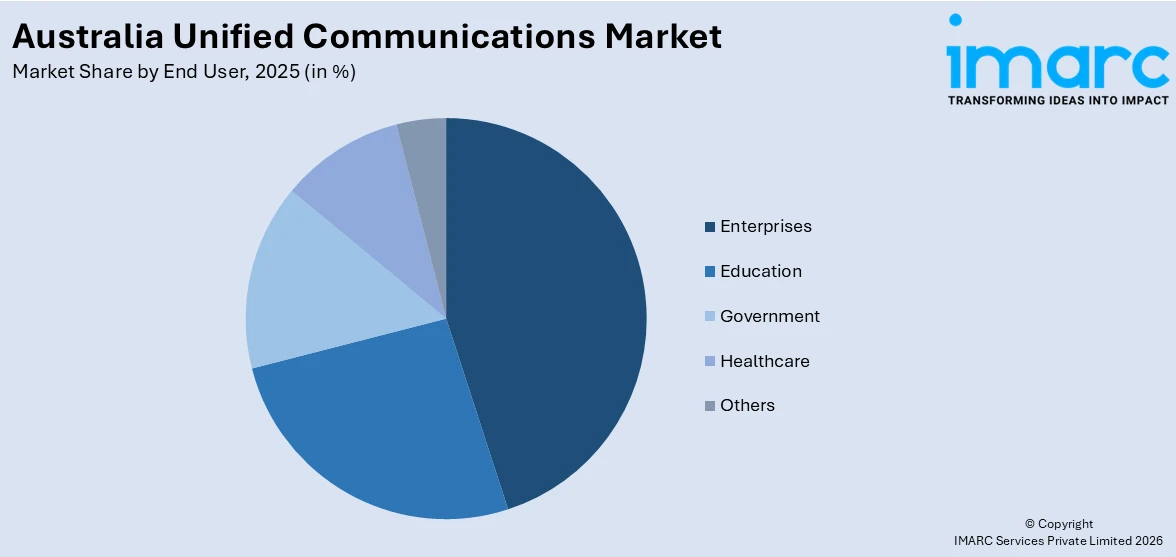

- By End User: Enterprises hold the leading segment with a share of 42.5% in 2025, reflecting the critical role unified communications plays in enhancing business productivity, enabling seamless internal collaboration, and supporting customer-facing communication workflows.

- By Region: Australia Capital Territory & New South Wales represents the largest region with a share of 34.8% in 2025, driven by the high concentration of large corporations and government agencies in Sydney and Canberra, both of which are major hubs for enterprise technology adoption and digital infrastructure investment.

- Key Players: Key players in the Australia unified communications market are advancing their competitive positions by developing AI-driven features, expanding cloud-hosted solution portfolios, and forging strategic partnerships with telecommunications providers. Their investments in security, interoperability, and managed services are strengthening enterprise adoption and broadening market reach across sectors.

To get more information on this market Request Sample

The Australian unified communications market shows strong and sustained growth, driven by a number of structural and technological growth drivers. Australian businesses are increasingly abandoning their fractured legacy communication systems in favor of fully integrated UC systems capable of integrating voice, video, instant messaging, and collaboration tools into a fully unified digital experience. This trend has been driven by the normalization of hybrid working arrangements, which has created a sustained demand for flexible, location-agnostic communication infrastructure in the enterprise space. Cloud-native solutions, such as Unified Communications as a Service, are also gaining traction due to scalability, flexible pricing, and ease of integration with existing productivity suites. Continuing government investment in national digital infrastructure is also supporting the growth of the fundamental connectivity infrastructure upon which advanced UC solutions rely, extending high-speed connectivity to businesses in both metropolitan and regional areas of the country. The growing integration of artificial intelligence within UC solutions is enabling intelligent meeting management, automated workflows, and real-time communication analytics, adding significant enterprise value. Together, these forces are creating a robust environment for continued market expansion across all major industry verticals and geographic regions throughout Australia.

Australia Unified Communications Market Trends:

Rising Integration of Artificial Intelligence in Communication Platforms

Artificial intelligence is becoming deeply embedded in Australian UC platforms, enabling features such as real-time meeting transcription, automated task generation, and sentiment analysis. Enterprises are leveraging AI to reduce administrative burdens and enhance the quality of virtual interactions. Intelligent virtual assistants are now capable of scheduling meetings, summarising decisions, and routing communications based on contextual priorities. As AI capabilities within UC tools become more sophisticated, organisations across finance, healthcare, and government sectors are adopting these platforms to drive productivity gains and deliver more responsive internal and external communication experiences.

Accelerating Shift Toward Cloud-Based Unified Communications as a Service

The transition from on-premises legacy telephony infrastructure to cloud-hosted UCaaS platforms is a defining trend in the Australian market. Organisations are increasingly drawn to hosted deployment models for their ability to eliminate large capital expenditures, simplify system management, and support rapid scalability. The convergence of cloud computing with UC tools has enabled businesses to access enterprise-grade communication capabilities through subscription models, making advanced features available to organisations regardless of size. The growing availability of local data hosting options is also addressing data sovereignty and compliance concerns, further encouraging cloud migration among regulated industries.

Growing Adoption of Multi-Platform Interoperability and API Integration

Australian enterprises are increasingly prioritising UC solutions that can interoperate seamlessly across diverse platforms and integrate with core business applications such as customer relationship management and enterprise resource planning systems. The demand for API-driven communication integration is enabling businesses to embed voice, video, and messaging capabilities directly into workflows, improving the speed and coherence of business operations. Multi-platform compatibility is also becoming a competitive differentiator among UC providers, with enterprises seeking solutions that allow teams to collaborate effectively regardless of the communication tools preferred by individual departments or partner organisations.

Market Outlook 2026-2034:

The Australia unified communications market is poised for considerable growth in the coming years, owing to the continued trend of enterprise digitisation, increasing penetration of hybrid work concepts, and the growing trend of embedding AI-powered features in communication solutions. Enterprises in both the public and private sectors are likely to increase their pace in transitioning from traditional communication solutions to cloud-based unified communication solutions. The continued rollout of 5G networks in metropolitan and rural areas is also likely to positively influence the use of mobile-based unified communication solutions in Australia, in addition to the continued influence of government-led digitisation plans in the public administration and healthcare sectors. The increasing trend of embedding cybersecurity features in unified communication solutions is also likely to positively influence the market’s long-term growth trajectory. The market generated a revenue of USD 3,406.46 Million in 2025 and is projected to reach a revenue of USD 13,389.71 Million by 2034, growing at a compound annual growth rate of 15.84% from 2026-2034.

Australia Unified Communications Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Component |

Solution |

71.5% |

|

Solution Sub-Segment |

Audio and Video Conferencing |

32.5% |

|

Deployment Mode |

Hosted |

52.5% |

|

Organization Size |

Large Enterprises |

56.8% |

|

End User |

Enterprises |

42.5% |

|

Region |

Australia Capital Territory & New South Wales |

34.8% |

Component Insights:

- Solution

- Instant and Unified Messaging

- Audio and Video Conferencing

- IP Telephony

- Others

- Services

- Professional Services

- Managed Services

Solution dominates with a market share of 71.5% of the total Australia unified communications market in 2025.

The solution segment commands a dominant position in the Australia unified communications market owing to the breadth and depth of integrated software capabilities it encompasses, including instant messaging, audio and video conferencing, and IP telephony. Enterprises across all verticals are prioritising unified solution platforms that consolidate multiple communication functions into a single interface, reducing IT complexity and enabling consistent user experiences across devices and locations. The rapid evolution of cloud-native UC solution suites, bundled with AI-powered features such as smart transcription, virtual assistants, and advanced analytics, is making solution-based offerings increasingly attractive to organisations pursuing digital workplace transformation.

Within the solution segment, audio and video conferencing holds a sub-segment share of 32.5%, reflecting its centrality to modern enterprise communication workflows. The normalisation of hybrid working arrangements in Australia has significantly elevated the role of high-definition video conferencing tools in enabling cohesive team collaboration across distributed environments. Organisations are investing in enterprise-grade video conferencing capabilities that integrate directly into broader UC platforms, supporting functions such as screen sharing, breakout rooms, and meeting intelligence. The education sector has also been a significant driver, deploying video conferencing infrastructure to support blended and online learning models that have become standard across Australian universities and schools.

Deployment Mode Insights:

- On-premises

- Hosted

Hosted leads with a share of 52.5% of the total Australia unified communications market in 2025.

The hosted deployment model has emerged as the preferred mode for delivering unified communications in Australia, reflecting a broader enterprise shift toward cloud-first IT strategies. Hosted UC solutions eliminate the need for organisations to invest in and maintain physical infrastructure, offering instead a subscription-based model that provides flexibility, predictable costs, and the ability to scale capacity in alignment with business growth. The operational simplicity of hosted platforms, combined with automatic software updates, remote access capabilities, and built-in redundancy, makes them especially appealing to organisations managing distributed workforces across metropolitan and regional locations.

The hosted model's dominance is further reinforced by the increasing availability of locally hosted cloud environments that address data residency and regulatory compliance requirements. Australian enterprises in regulated sectors, including financial services and government, are increasingly able to adopt hosted UC solutions that guarantee data sovereignty without sacrificing the operational benefits of cloud delivery. This evolution has expanded the addressable market for hosted platforms beyond technology-forward enterprises to include compliance-sensitive organisations that previously favoured on-premises deployments. The on-premises segment continues to serve organisations with highly specialised security requirements or complex legacy integration needs, but its share is expected to gradually decline as cloud offerings become more capable.

Organization Size Insights:

- Small and Medium-sized Enterprises

- Large Enterprises

Large enterprises exhibit a clear dominance in the market with a 56.8% share of the total Australia unified communications market in 2025.

Large enterprises lead adoption of unified communications solutions in Australia, driven by the complexity of their communication environments, the scale of their distributed operations, and the significant IT budgets they allocate toward digital transformation. These organisations typically require enterprise-grade UC platforms that can support thousands of users across multiple offices, integrate with existing enterprise software ecosystems, and meet strict security, compliance, and audit requirements. Leading corporations in sectors such as financial services, mining, retail, and professional services have made substantial investments in UC infrastructure to enable seamless collaboration between head offices, branch networks, and remote workforces.

The dominance of large enterprises also reflects the increasing trend toward centralised communication management, where IT departments seek single-vendor UC platforms that provide full visibility, control, and analytics across the organisation. Large enterprises are among the earliest and most enthusiastic adopters of AI-powered UC features, leveraging predictive analytics, intelligent call routing, and automated meeting summaries to extract greater operational value from their communication investments. The SME segment, while smaller in current share, is growing rapidly as the affordability and accessibility of hosted UC platforms continues to improve, lowering the barriers to adoption for businesses with limited IT resources.

End User Insights:

Access the comprehensive market breakdown Request Sample

- Enterprises

- Education

- Government

- Healthcare

- Others

Enterprises represent the leading segment with a share of 42.5% of the total Australia Unified Communications market in 2025.

The enterprise end-user segment commands the largest share of the Australia unified communications market, underpinned by the broad adoption of UC platforms across corporate environments spanning financial services, professional services, retail, and information technology. Australian enterprises have prioritised the deployment of unified communication tools to address the challenges of managing geographically dispersed teams while maintaining high standards of operational efficiency and employee productivity. The growing sophistication of enterprise UC platforms, featuring integrated contact centre capabilities, real-time collaboration tools, and advanced security architecture, has elevated their role from supplementary IT infrastructure to a core component of business operations strategy.

Beyond the enterprise segment, education and healthcare are growing end-user categories reflecting Australia's public sector digitisation agenda. Educational institutions across Australia have adopted video conferencing and unified messaging platforms to support blended learning and remote student engagement. Meanwhile, healthcare organisations are deploying UC tools to facilitate secure clinical communications, teleconsultation services, and cross-departmental coordination, particularly in multi-site hospital environments. Government adoption remains significant, driven by federal and state digital transformation initiatives that mandate modernisation of public sector communication infrastructure. The others category includes SMEs and retail businesses increasingly engaging with hosted UC solutions.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australian Capital Territory & New South Wales represents the largest region with a 34.8% share of the total Australia unified communications market in 2025.

The Australian Capital Territory and New South Wales region takes the lead in this market, driven by the pre-eminent position of Sydney as Australia's largest financial and commercial hub, as well as Canberra, which houses federal government agencies and defense organizations. Sydney is home to the headquarters of all major financial institutions, insurance companies, law firms, and multinational technology companies, which are all major consumers of enterprise-grade UC solutions. The high concentration of large enterprises in this region creates disproportionate demand for advanced UC solutions that offer scalability, security, and interconnectivity between sites. The presence of regional headquarters of major UC vendors in Sydney also facilitates faster adoption and deployment of technology solutions.

The Canberra part of the region also adds to the demand side, with government institutions and organizations seeking to implement secure and compliant solutions for their UC environments, which are aligned to national cybersecurity policies. The ongoing digital transformation initiatives of the New South Wales state government and the Australian federal government also provide ongoing demand for UC solutions in the region. Additionally, the region’s advanced digital infrastructure, which includes high-speed broadband and 5G access, also facilitates the adoption of advanced hosted unified communications solutions, thus making it the leading region in the Australian unified communications market.

Market Dynamics:

Growth Drivers:

Why is the Australia Unified Communications Market Growing?

Widespread Adoption of Hybrid and Remote Work Models

The sustained normalisation of hybrid and remote working arrangements across Australian organisations has become one of the most powerful drivers of unified communications market growth. As businesses across sectors continue to support flexible work models, the demand for communication platforms that enable seamless collaboration regardless of employee location has intensified significantly. Organisations are moving away from traditional on-premises telephony and meeting systems toward integrated UC platforms that unify voice, video, messaging, and presence data in a single digital workspace. This shift is particularly pronounced in professional services, information technology, and financial services sectors, where distributed team structures have become standard operating practice. The ability of UC platforms to support real-time collaboration, virtual project management, and cross-functional communication across time zones is enabling Australian enterprises to maintain productivity while offering employees the flexibility they increasingly expect as a baseline workplace condition.

Rapid Expansion of Cloud Infrastructure and 5G Network Deployment

The accelerating expansion of cloud infrastructure and the ongoing nationwide deployment of 5G networks are creating the technical foundation necessary for next-generation unified communications adoption across Australia. Cloud-hosted UC platforms are benefiting from growing data centre investments in major Australian cities, improving the performance, reliability, and data sovereignty of hosted communication services. Simultaneously, the rollout of 5G services by major Australian telecommunications operators is unlocking new capabilities for mobile UC deployments, enabling low-latency video conferencing, real-time collaboration, and high-definition voice communications from mobile devices. Together, these infrastructure advancements are expanding the addressable market for UC solutions and reducing the technical barriers that previously limited adoption in bandwidth-constrained environments.

Integration of Artificial Intelligence and Automation in Communication Workflows

The integration of artificial intelligence and automation capabilities within unified communications platforms is driving a new wave of enterprise adoption across Australia. AI-powered features, including automated meeting transcription, intelligent virtual assistants, real-time sentiment analysis, and predictive communication routing, are delivering measurable productivity benefits that accelerate return on investment for UC deployments. Australian enterprises in sectors such as financial services, legal, and healthcare are adopting AI-enabled UC platforms to automate repetitive administrative tasks, improve the quality of decision-making in virtual meetings, and enhance the experience of both internal teams and external customers. The growing availability of generative AI tools embedded natively within major UC platforms is further elevating the value proposition of modern communication solutions. As AI capabilities continue to mature, the expectation among Australian businesses that their UC platforms deliver intelligent, context-aware communication experiences is becoming a standard procurement requirement.

Market Restraints:

What Challenges the Australia Unified Communications Market is Facing?

Cybersecurity Risks and Data Privacy Compliance Concerns

The growing reliance on cloud-hosted UC platforms introduces significant cybersecurity and data privacy challenges for Australian organisations. As communication platforms consolidate sensitive business data, voice recordings, and confidential video interactions in cloud environments, the attack surface for cyber threats expands considerably. Organisations operating in regulated industries, including healthcare and financial services, must navigate complex compliance obligations under Australian privacy legislation and sector-specific regulatory frameworks. The cost and complexity of implementing end-to-end encryption, multi-factor authentication, and continuous threat monitoring across enterprise UC deployments remain substantial barriers, particularly for mid-sized organisations with limited dedicated cybersecurity resources.

High Total Cost of Ownership and Integration Complexity

Despite the cost advantages associated with cloud-based UC delivery models, the total cost of ownership for enterprise unified communications deployments can present a significant restraint for Australian organisations, particularly in the public sector and among small and medium-sized enterprises. The integration of UC platforms with legacy communication infrastructure, existing enterprise software systems, and custom business applications requires substantial technical investment and expertise. Organisations facing complex multi-vendor environments may encounter interoperability challenges that increase both project timelines and implementation costs. Ongoing licensing, customisation, and managed service fees can further compound the financial commitment, tempering adoption among cost-sensitive segments of the market.

Limited Digital Literacy and Change Management Challenges

The successful adoption of unified communications platforms is contingent not only on technical deployment but on effective user adoption, which remains a persistent challenge across many Australian organisations. Workforce segments with limited digital literacy, including older employees and those in traditionally non-digital roles, may struggle to adopt new UC interfaces and workflows, reducing the realised productivity benefits of platform investments. Change management initiatives required to drive meaningful adoption, including training programmes, user support resources, and cultural transformation efforts, represent an additional overhead that organisations must absorb. In the absence of comprehensive change management strategies, UC deployments risk underutilisation, resistance from end users, and failure to achieve the collaboration improvements that motivated initial investment.

Competitive Landscape:

The unified communications market in Australia is highly competitive, with global technology leaders as well as regional providers of specialized solutions for unified communications. These players are differentiated on the basis of their ability to integrate platforms, feature sets of artificial intelligence, security certifications, and their professional and managed services networks in local markets. Competition in this market is becoming increasingly fierce, with providers looking to increase their share of this market by forging partnerships with telecommunication companies, investing in channel partner ecosystems, and continually enhancing their portfolios of cloud-delivered unified communications solutions. Providers of unified communications as a service solution with built-in contact centers, artificial intelligence, and security are seeing increased competitive advantage, particularly in large enterprises and government organizations with complex unified communications requirements.

Recent Developments:

- In December 2025, Macquarie Telecom expanded its partnership with Fortinet to launch a unified secure networking solution designed specifically for Australian organisations. The platform, delivered entirely within Australia by Macquarie Telecom's engineering teams, integrates consistent security policies and full network visibility across hybrid environments, helping organisations reduce communication infrastructure complexity while meeting local regulatory compliance requirements, including the Australian Government's Essential Eight framework.

- In July 2024, Vodafone Business, in partnership with RingCentral, added Australia and New Zealand to the coverage footprint of its cloud-based UCaaS platform, combining voice calling, video conferencing, and instant messaging capabilities. The expansion provided Australian multinational businesses with access to a single unified communications partner capable of managing services across more than 30 global markets, simplifying communication management for enterprises with international operations.

Australia Unified Communications Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered |

|

| Deployment Modes Covered | On-premises, Hosted |

| Organization Sizes Covered | Small and Medium-sized Enterprises, Large Enterprises |

| End Users Covered | Enterprises, Education, Government, Healthcare, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Unified Communications Market Report

The Australia unified communications market size was valued at USD 3,406.46 Million in 2025.

The Australia unified communications market is expected to grow at a compound annual growth rate of 15.84% from 2026-2034 to reach USD 13,389.71 Million by 2034.

Solution dominated the market with a share of 71.5%, owing to the broad adoption of integrated software platforms that consolidate messaging, conferencing, and telephony capabilities to support enterprise digital communication strategies.

Key factors driving the Australia unified communications market include the widespread adoption of hybrid and remote work models, rapid expansion of cloud infrastructure and 5G networks, and the integration of artificial intelligence and automation in enterprise communication platforms.

Major challenges include escalating cybersecurity and data privacy compliance requirements, high total cost of ownership and integration complexity for legacy system transitions, and limited digital literacy and change management challenges that can inhibit user adoption and reduce the realised productivity benefits of UC deployments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)