Australia Venture Capital Market Size, Share, Trends and Forecast by Sector, Fund Size, Funding Type, and Region, 2026-2034

Australia Venture Capital Market Summary:

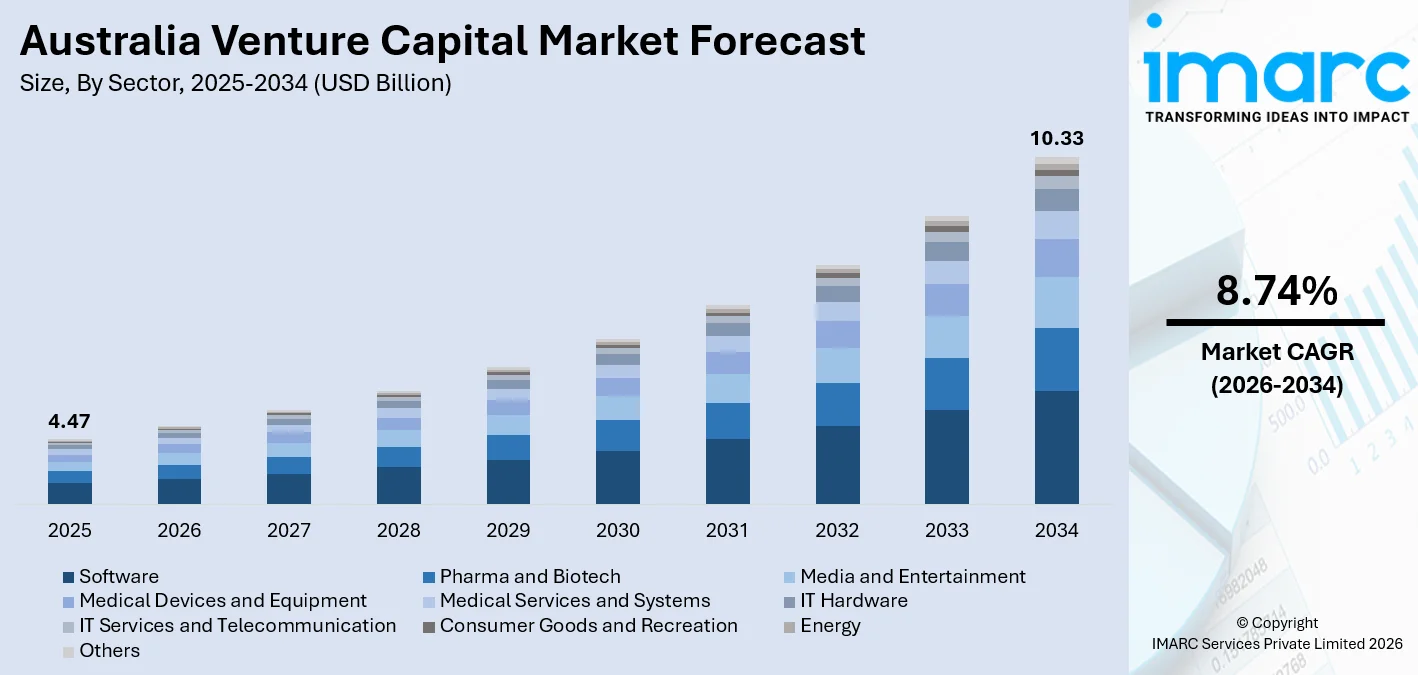

The Australia venture capital market size was valued at USD 4.47 Billion in 2025 and is projected to reach USD 10.33 Billion by 2034, growing at a compound annual growth rate of 8.74% from 2026-2034.

Australia's venture capital market is driven by a thriving startup ecosystem, expanding government-backed innovation programs, and rapidly growing investor appetite for technology, healthtech, and clean energy sectors. As digital transformation accelerates across industries, both domestic and international venture capital funds are increasing their exposure to high-growth Australian startups. The deepening engagement of institutional investors, corporate venture arms, and university spin-outs continues to diversify deal pipelines and strengthen the Australia venture capital market share.

Key Takeaways and Insights:

- By Sector: Software dominates the market with a share of 38.5% in 2025, owing to strong enterprise SaaS adoption, accelerating digital transformation across industries, and high investor confidence in scalable, recurring-revenue technology business models.

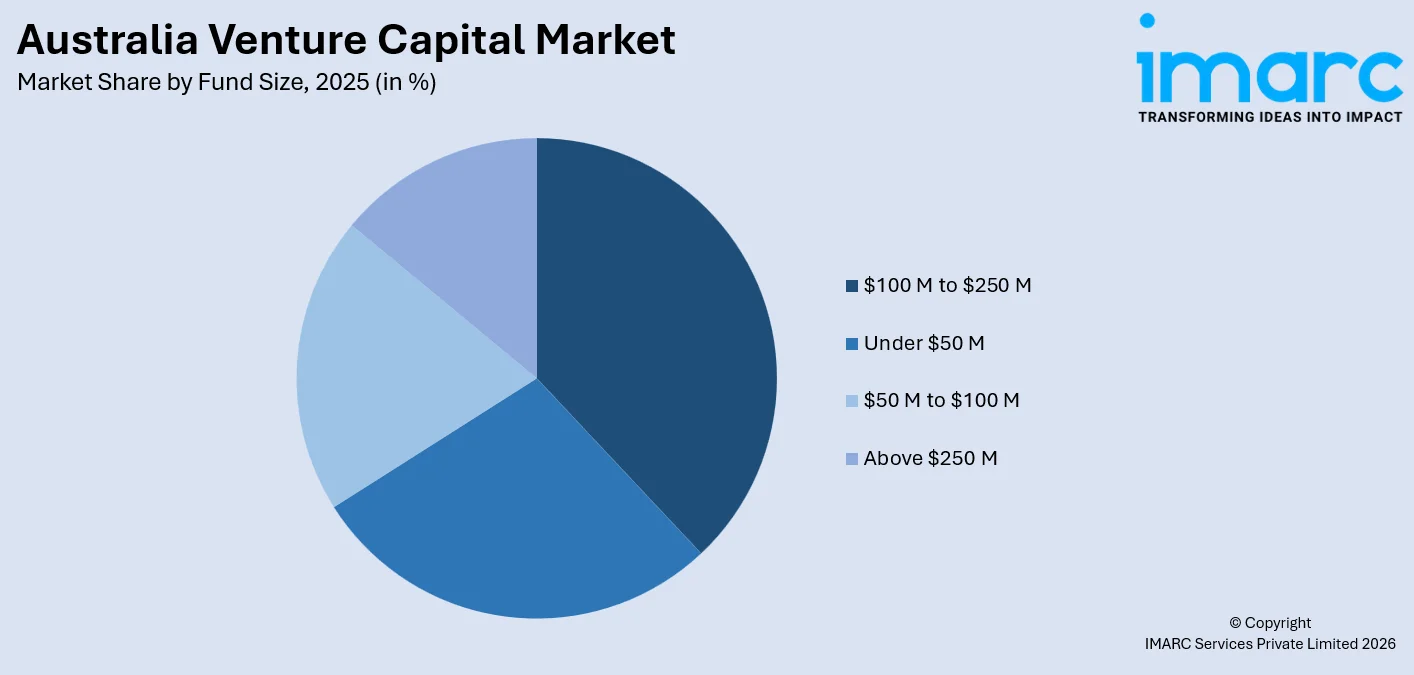

- By Fund Size: $100 M to $250 M leads with a share of 32.7% in 2025, reflecting institutional investors' preference for mid-sized funds that balance portfolio diversification with concentrated sector expertise and meaningful ticket sizes.

- By Funding Type: Follow-on venture funding holds the largest segment with a market share of 61.8% in 2025, driven by investors' strong preference for backing portfolio companies with demonstrated market traction and proven growth trajectories.

- By Region: Australia Capital Territory & New South Wales represents the largest region with 36.9% share in 2025, supported by Sydney's deep venture capital networks, concentration of technology sector activity, and proximity to established financial markets and enterprise customers.

- Key Players: Key players drive the Australia venture capital market by expanding fund sizes, strengthening sector-specific expertise, and building cross-border investment networks. Their strategic focus on software, healthtech, and clean energy, combined with co-investment initiatives and accelerator partnerships, accelerates deal flow, enhances portfolio performance, and deepens market access across diverse startup stages.

To get more information on this market Request Sample

Australia's venture capital market has established itself as one of the most capital-efficient innovation ecosystems globally, with a growing number of high-value startups attracting both domestic and international investment. The market has witnessed sustained momentum across software, biotechnology, fintech, and clean technology sectors, with Sydney and Melbourne serving as the twin anchors of deal activity. Supporting this performance is a network of government programs, including the Innovation Investment Fund and the Biomedical Translation Fund, which have catalysed private co-investment across early and growth stages. University spin-outs and corporate venture arms have diversified the deal pipeline, while international funds from the United States, Singapore, and Hong Kong have increasingly sought entry into Australian rounds, reinforcing the country's reputation as a credible and scalable destination for high-growth capital. This multi-source funding environment continues to underpin the Australia venture capital market share.

Australia Venture Capital Market Trends:

Rise of Artificial Intelligence as a Core Investment Theme:

Artificial intelligence has emerged as the defining investment theme in Australia's venture capital landscape, with AI-native and AI-integrated startups capturing a disproportionate share of deal flow. Investors are prioritising businesses where AI compresses development cycles, reduces capital intensity, and unlocks new revenue streams. This trend cuts across verticals, from legal technology and healthcare diagnostics to agriculture and financial services, reflecting a broad maturation of AI capabilities within the Australian startup pipeline.

Surge in Climate Technology and Clean Energy Investment:

Australia's venture capital ecosystem has seen accelerating capital allocation toward climate and clean technology, driven by national net-zero commitments, ESG mandates from institutional limited partners, and the commercial viability of renewable energy solutions. Investors are backing startups focused on battery storage, carbon capture, green hydrogen, and circular economy models. In June 2024, Pollination launched a AUD 150 Million Climate and Nature Impact Venture Fund targeting early-stage Australian startups across energy, agriculture, and sustainable infrastructure sectors.

Growing Institutional and Superannuation Fund Participation:

A structural shift is underway as Australian superannuation funds, family offices, and large institutional investors increase their allocations to venture capital as a distinct asset class. This trend is reshaping fund formation dynamics, enabling domestic VC managers to raise larger vehicles and extend their investment horizons. The entry of superannuation capital has added stability to the limited partner base, reduced dependency on overseas fundraising, and improved the ability of Australian fund managers to lead significant late-stage and growth-stage rounds domestically.

Market Outlook 2026-2034:

The Australia venture capital market is positioned for sustained and broad-based growth across the forecast period, supported by an increasingly mature startup ecosystem, deepening institutional capital participation, and continued expansion of government co-investment programs. Demand for venture-backed innovation in software, health technology, artificial intelligence, and clean energy is expected to remain robust, with both domestic and international investors expanding their Australian exposure. Increasing deal sizes across pre-seed through Series B stages, a growing pipeline of globally ambitious founders, and the emergence of new regional innovation clusters beyond Sydney and Melbourne are expected to drive diversified deal flow. The ongoing maturation of exit pathways, including international acquisitions and a recovering IPO environment, will further strengthen investor confidence and support continued capital formation within Australia's venture capital market. The market generated a revenue of USD 4.47 Billion in 2025 and is projected to reach a revenue of USD 10.33 Billion by 2034, growing at a compound annual growth rate of 8.74% from 2026-2034.

Australia Venture Capital Market Report Segmentation:

| Segment Category | Leading Segment | Market Share |

|---|---|---|

|

Sector |

Software |

38.5% |

|

Fund Size |

$100 M to $250 M |

32.7% |

|

Funding Type |

Follow-on Venture Funding |

61.8% |

|

Region |

New South Wales & ACT |

36.9% |

Sector Insights:

- Software

- Pharma and Biotech

- Media and Entertainment

- Medical Devices and Equipment

- Medical Services and Systems

- IT Hardware

- IT Services and Telecommunication

- Consumer Goods and Recreation

- Energy

- Others

Software dominates with a market share of 38.5% of the total Australia Venture Capital market in 2025.

Software leads Australia's venture capital landscape by a substantial margin, reflecting the sector's inherent scalability, recurring revenue characteristics, and relatively lower capital requirements compared to hardware or life sciences verticals. Enterprise software and software-as-a-service models attract strong investor interest due to predictable growth metrics and clear monetisation pathways. The dominance of software is reinforced by Australia's strong developer talent pool, world-class university computer science programs, and a growing cohort of founders with prior scaling experience. Investors favour software companies for their ability to address large global addressable markets from an Australian base, particularly in sectors such as financial technology, legal technology, workplace productivity, and cybersecurity.

Within the software segment, the rise of AI-native and AI-augmented platforms has significantly broadened the investment opportunity set. Startups embedding large language models, predictive analytics, and automation capabilities into existing enterprise workflows are attracting both seed and growth-stage capital. Investors are particularly drawn to software businesses that demonstrate defensible data advantages, strong user retention, and clear pathways to monetisation across large addressable markets. The software segment's dominance is expected to continue as digital transformation accelerates across healthcare, mining, agriculture, and financial services industries in Australia, sustaining a deep and diverse pipeline of venture-backable opportunities.

Fund Size Insights:

Access the comprehensive market breakdown Request Sample

- Under $50 M

- $50 M to $100 M

- $100 M to $250 M

- Above $250 M

$100 M to $250 M leads with a share of 32.7% of the total Australia venture capital market in 2025.

The $100 Million to $250 Million fund size range has emerged as the preferred vehicle for Australian venture capital deployment, reflecting the market's transition from smaller, highly diversified funds toward more concentrated portfolios with greater ability to lead meaningful rounds. Funds in this range possess sufficient capital to anchor Series A and Series B investments while retaining the operational agility characteristic of focused venture partnerships. This size bracket has attracted strong institutional limited partner participation, including allocations from Australian superannuation funds and global fund-of-funds managers who seek meaningful exposure to the domestic venture ecosystem without the operational complexities of managing mega-funds.

Mid-sized funds in the $100 Million to $250 Million range are particularly well-suited to the current Australian deal environment, where founders increasingly seek investors capable of leading rounds and providing substantial follow-on reserves. The structure enables fund managers to build diversified sector exposure across software, health technology, and clean energy while retaining enough ownership to add meaningful board-level value. As the domestic venture capital ecosystem continues to mature, this fund size bracket is expected to remain the preferred deployment vehicle, balancing portfolio diversification with the operational focus required to support high-growth portfolio companies through successive funding stages.

Funding Type Insights:

- First-Time Venture Funding

- Follow-on Venture Funding

Follow-on venture funding exhibits a clear dominance with a 61.8% share of the total Australia venture capital market in 2025.

Follow-on venture funding commands the majority of Australia's venture capital deployment, reflecting the market's maturing investment environment where investors demonstrate strong conviction in supporting portfolio companies through multiple growth stages. This funding structure reduces the risk profile associated with early-stage uncertainty by concentrating capital in businesses with demonstrated product-market fit, growing customer bases, and credible financial projections. The dominance of follow-on funding signals a shift away from speculative, first-cheque investing toward a disciplined, performance-driven approach, which has become increasingly prevalent as institutional limited partners apply greater scrutiny to deployment strategies and return expectations within the Australian market.

The prevalence of follow-on venture funding is further reinforced by the expanding reserve management practices of leading Australian venture capital firms. As fund sizes have grown, managers are allocating larger proportions of their capital to pro-rata rights in successful portfolio companies, ensuring continued ownership in breakout businesses through successive funding rounds. This approach reflects a disciplined, conviction-driven investment philosophy whereby investors deepen their commitment to portfolio companies that demonstrate strong commercial traction, improving unit economics, and clear pathways to scale, rather than continuously deploying capital into unproven early-stage opportunities across an overly broad portfolio.

Regional Insights:

- Australian Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australian Capital Territory & New South Wales represent the leading segment with a 36.9% share of the total Australia venture capital market in 2025.

New South Wales, anchored by Sydney, holds the largest regional share in Australia's venture capital market by virtue of its dominant position as the country's financial and technology capital. Sydney's Tech Central district has attracted the headquarters of numerous global technology firms, creating a concentrated talent pool and a dense ecosystem of potential founders and early adopters. The region benefits from deep venture capital networks, including the presence of leading domestic firms and local offices of international investors, which facilitate rapid deal origination and syndication. Sydney's proximity to major enterprise customers across financial services, retail, and professional services provides venture-backed startups with a natural testing ground for scaling commercial traction and validating product-market fit at a national level.

The Australian Capital Territory contributes meaningfully to the region's venture capital activity through its strong cluster of defence technology, cybersecurity, and govtech startups, many of which emerge from or maintain close links with the Australian National University and other Canberra-based research institutions. Federal government procurement activity in the Australian Capital Territory creates favourable commercial conditions for early-stage technology companies targeting the public sector. Together, New South Wales and Australian Capital Territory form a complementary innovation corridor that spans enterprise and fintech in Sydney through to deep tech and national security technology in Canberra, providing the regional segment with a uniquely diversified deal pipeline and a resilient investor base that has remained active across multiple market cycles.

Market Dynamics:

Growth Drivers:

Why is the Australia Venture Capital Market Growing?

Expanding Government Support Programs and Policy Incentives:

The Australian government has implemented a comprehensive suite of programs designed to catalyse venture capital investment across early and growth stages. The Innovation Investment Fund has been a cornerstone initiative, providing co-investment capital alongside private venture funds to reduce risk in backing early-stage technology companies. The Biomedical Translation Fund supports translational research in life sciences, while the Renewable Energy Venture Capital Programme targets clean energy innovation with dedicated funding allocations. State-level programs including the Queensland Venture Capital Development Fund and the South Australian Venture Capital Fund further extend the government's reach into regional startup ecosystems Tax-advantaged structures such as Venture Capital Limited Partnerships and Early Stage Venture Capital Limited Partnerships provide meaningful incentives for both domestic and international investors, reducing effective tax costs on capital gains and attracting foreign fund managers to establish Australian operations. The streamlining of ESVCLP registration processes as part of the March 2025 announcement is expected to lower administrative barriers and encourage greater participation from smaller domestic fund managers, broadening the base of institutional capital available to Australian startups.

Thriving Startup Ecosystem and Exceptional Capital Efficiency:

Australia has developed one of the world's most capital-efficient startup ecosystems, generating approximately 1.22 unicorns for every USD 1 Billion of venture capital deployed, a ratio that surpasses the United States and China. This performance reflects a cohort of globally ambitious founders who build for international markets from day one, reducing the incremental capital required to achieve meaningful scale. The country's world-class research universities, including the University of Melbourne, the Australian National University, and the University of Sydney, generate a steady pipeline of deep-tech spin-outs with defensible intellectual property. Startup support infrastructure including incubators, accelerators, and co-working hubs has expanded rapidly across Sydney, Melbourne, Brisbane, and Adelaide, providing early-stage founders with mentorship, networks, and initial funding. Corporate venture arms from companies across financial services, telecommunications, and mining have also increased their participation in the startup ecosystem, providing strategic capital and partnership pathways that reduce commercial risk for portfolio companies. Australia's startup ecosystem was ranked third globally in liquidity after the United States and China in 2024, reflecting the quality and international market orientation of its venture-backed companies and validating the ecosystem as a credible destination for large-scale venture capital deployment.

Rising Demand for Technology Innovation in High-Growth Sectors:

Australia's venture capital market is experiencing robust structural demand for innovation-driven investments across multiple high-growth sectors. The software sector leads deal flow, driven by enterprise digital transformation and the rapid monetisation of AI-augmented platforms. Healthcare and biotechnology are attracting increasing capital as Australia's research institutions generate clinically validated assets and as the aging population drives demand for health technology solutions. Clean energy has emerged as a particularly dynamic vertical, with investors backing startups in battery storage, green hydrogen, and sustainable agriculture to capitalise on Australia's natural resource advantages and national decarbonisation commitments. The defence technology sector is also gaining investment momentum, supported by increased government procurement and strategic national security objectives. Collectively, these sector themes provide a diversified, multi-cycle growth opportunity for venture capital investors, ensuring that deal flow remains robust even when individual verticals experience cyclical funding softness. The deepening integration of artificial intelligence across all these sectors further expands the total addressable market for Australian venture-backed startups, making the technology investment landscape broader and more resilient than at any prior point in the ecosystem's development.

Market Restraints:

What Challenges the Australia Venture Capital Market is Facing?

Limited Availability of Late-Stage and Scale-Up Capital:

Australia's venture capital ecosystem faces a structural gap at the late-stage and scale-up funding tiers, where the pool of domestic capital available for Series B and beyond remains relatively shallow compared to more mature markets. Founders seeking larger growth rounds frequently need to source the majority of capital from international investors, introducing deal complexity, extended timelines, and foreign ownership considerations. This bottleneck has constrained the growth trajectories of high-potential companies, with some choosing to relocate their headquarters to markets with more accessible growth capital rather than continue scaling from an Australian base, resulting in a gradual erosion of the domestic company roster over time.

Regulatory Complexity and Outdated Fund Structure Legislation:

The legislative framework governing venture capital fund structures in Australia has not evolved at pace with the market's growth and sophistication. Venture Capital Limited Partnerships and Early Stage Venture Capital Limited Partnerships operate under rules that include prescriptive investment eligibility criteria, rigid fund life limits without extension provisions, and sector exclusions that create diligence burdens and compliance costs. These constraints increase the administrative overhead for fund managers, discourage smaller domestic managers from accessing tax-advantaged structures, and create situations where otherwise sound investments are rendered ineligible due to technical definitional issues rather than commercial or strategic concerns.

Market Volatility and Constrained Exit Pathway Activity:

Australia's venture capital market remains exposed to the impact of global macroeconomic volatility on investor sentiment, fund deployment rates, and exit valuations. Periods of elevated interest rates, currency fluctuations, and international market uncertainty have historically reduced limited partner appetite for new fund commitments and compressed the willingness of portfolio companies to pursue IPOs or strategic acquisitions at acceptable valuations. Australia's domestic IPO market has delivered inconsistent liquidity for venture-backed companies, and dependency on international acquirers for meaningful exits creates geographic concentration risk in deal outcomes. This exit constraint lengthens the effective investment cycle and reduces the velocity of capital recycling within the ecosystem.

Competitive Landscape:

Australia's venture capital competitive landscape is characterised by a core group of leading domestic managers supported by an expanding cohort of sector-focused and emerging funds. The market has witnessed a marked increase in fund sizes as established players demonstrate strong track records and attract institutional limited partners, including superannuation funds that are diversifying into alternative assets. The participation of international venture firms targeting Australian deals has intensified competition for high-quality opportunities, particularly in software, fintech, and health technology, driving up valuations at the top end of the market while simultaneously increasing the available capital for ambitious founders. Co-investment between domestic and international funds has become increasingly common, enabling larger round sizes while distributing risk across broader investor consortia.

Australia Venture Capital Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sectors Covered | Software, Pharma and Biotech, Media and Entertainment, Medical Devices and Equipment, Medical Services and Systems, IT Hardware, IT Services and Telecommunication, Consumer Goods and Recreation, Energy, Others |

| Fund Sizes Covered | Under $50 M, $50 M to $100 M, $100 M to $250 M, Above $250 M |

| Funding Types Covered | First-Time Venture Funding, Follow-on Venture Funding |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Venture Capital Market Report

The Australia venture capital market size was valued at USD 4.47 Billion in 2025.

The Australia venture capital market is expected to grow at a compound annual growth rate of 8.74% from 2026-2034 to reach USD 10.33 Billion by 2034.

Software dominated the market with a share of 38.5%, driven by strong enterprise SaaS adoption, accelerating digital transformation across industries, and high investor confidence in scalable, recurring-revenue technology business models.

Key factors driving the Australia venture capital market include expanding government co-investment programs, a capital-efficient startup ecosystem generating high unicorn yields, growing institutional participation from superannuation funds, and sustained investor demand for innovation in software, health technology, and clean energy sectors.

Major challenges include a structural shortage of late-stage and scale-up capital domestically, outdated venture capital fund structure legislation creating compliance complexity, constrained IPO and exit activity limiting capital recycling, and exposure to global macroeconomic volatility that periodically dampens investor sentiment and limited partner commitments to new fund vintages.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)