Australia Warehouse Market Size, Share, Trends and Forecast by Sector, Ownership, Type of Commodities Stored, and Region, 2026-2034

Australia Warehouse Market Size, Share, Trends & Forecast (2026-2034)

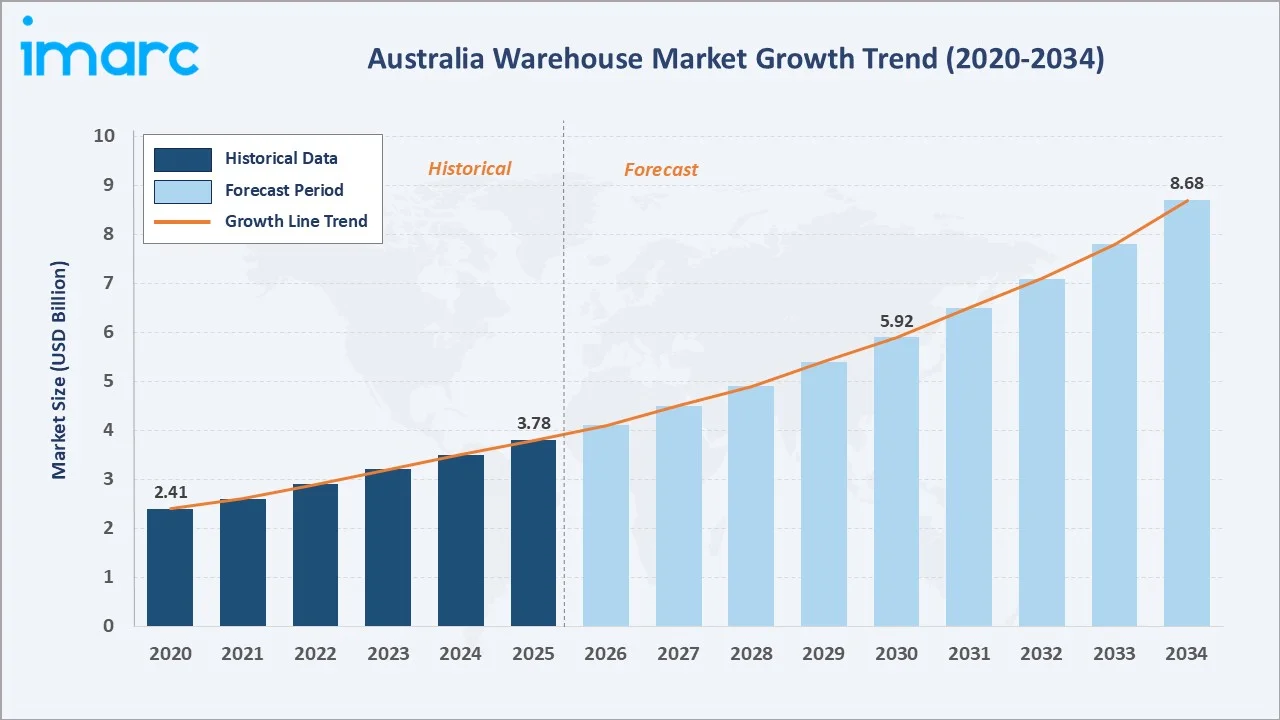

The Australia warehouse market reached USD 3.78 Billion in 2025 and is projected to reach USD 8.68 Billion by 2034, growing at a CAGR of 9.40% during 2026-2034. The market is driven by rapid growth in retail, with total online retailing sales reached $4,703.8 Million in June 2025, in seasonally adjusted terms, third-party logistics, and demand for faster last-mile delivery. Industrial warehouses dominate at 64.7%. Private warehouses lead ownership at 46.9%. Australia Capital Territory & New South Wales command 33.5% of the regional market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.78 Billion |

|

Forecast Market Size (2034) |

USD 8.68 Billion |

|

CAGR (2026-2034) |

9.40% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Sector |

Industrial Warehouses (64.7%, 2025) |

|

Dominant Ownership |

Private Warehouses (46.9%, 2025) |

|

Leading Region |

Australia Capital Territory & New South Wales (33.5%, 2025) |

The market expanded from USD 2.41 Billion in 2020 to USD 3.78 Billion in 2025, anchored at USD 5.92 Billion in 2030, and forecast to reach USD 8.68 Billion by 2034. COVID-19 permanently transformed Australian warehouse market dynamics, and pandemic supply chain disruptions created strategic safety stock requirements across every Australian industry sector, driving unprecedented warehouse space demand.

To get more information on this market, Request Sample

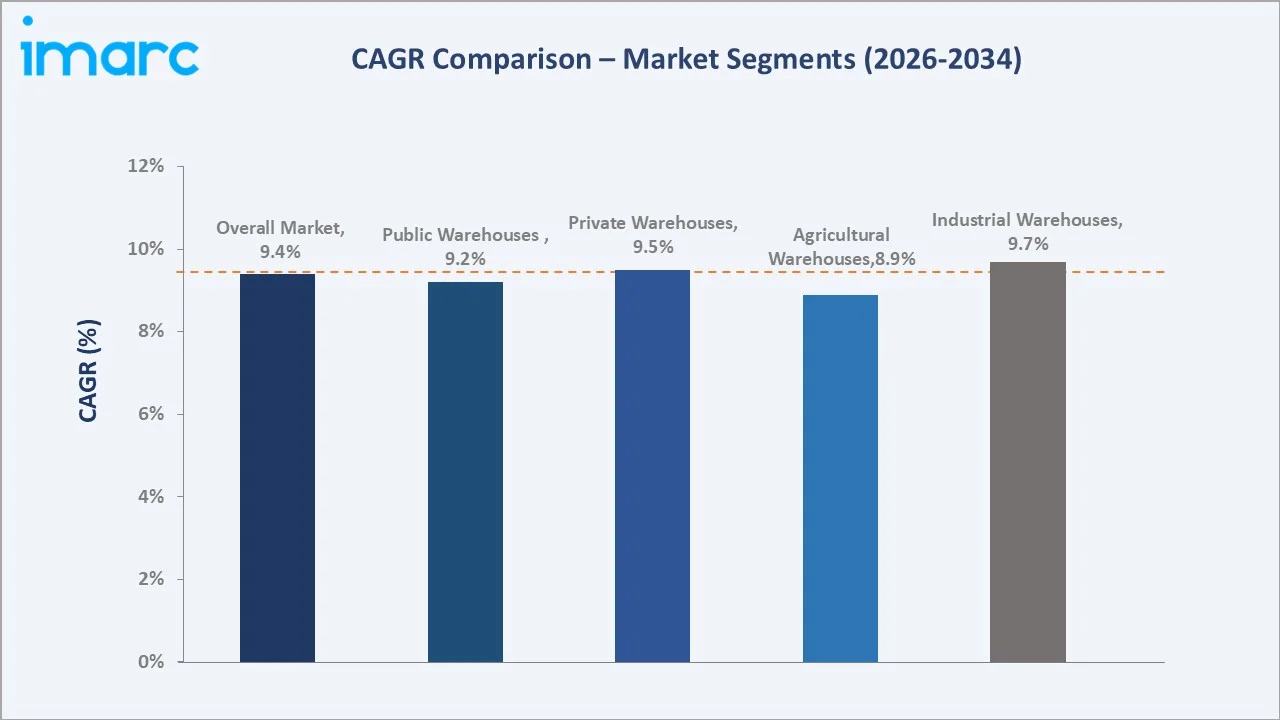

Industrial warehouses grow fastest at ~9.7% CAGR through e-commerce mega-DC development, pharmaceutical cold chain expansion, and manufacturing goods storage investment. Public warehouses grow at ~9.2% CAGR as third-party logistics adoption expands across Australian SME and mid-market businesses that previously managed warehousing in-house but outsource to providers to reduce capital investment and gain operational scalability without fixed warehouse lease commitments.

Executive Summary

The Australia warehouse market reached USD 3.78 Billion in 2025, representing the intersection of Australia's property investment markets, logistics and supply chain industry, and technology sector as automation and digital warehousing transform what was historically a passive real estate category into an active, technology-intensive, and strategically critical industrial asset class. Australian industrial and logistics property has become the highest-performing real estate sub-sector in the country. The market is projected to reach USD 8.68 Billion by 2034.

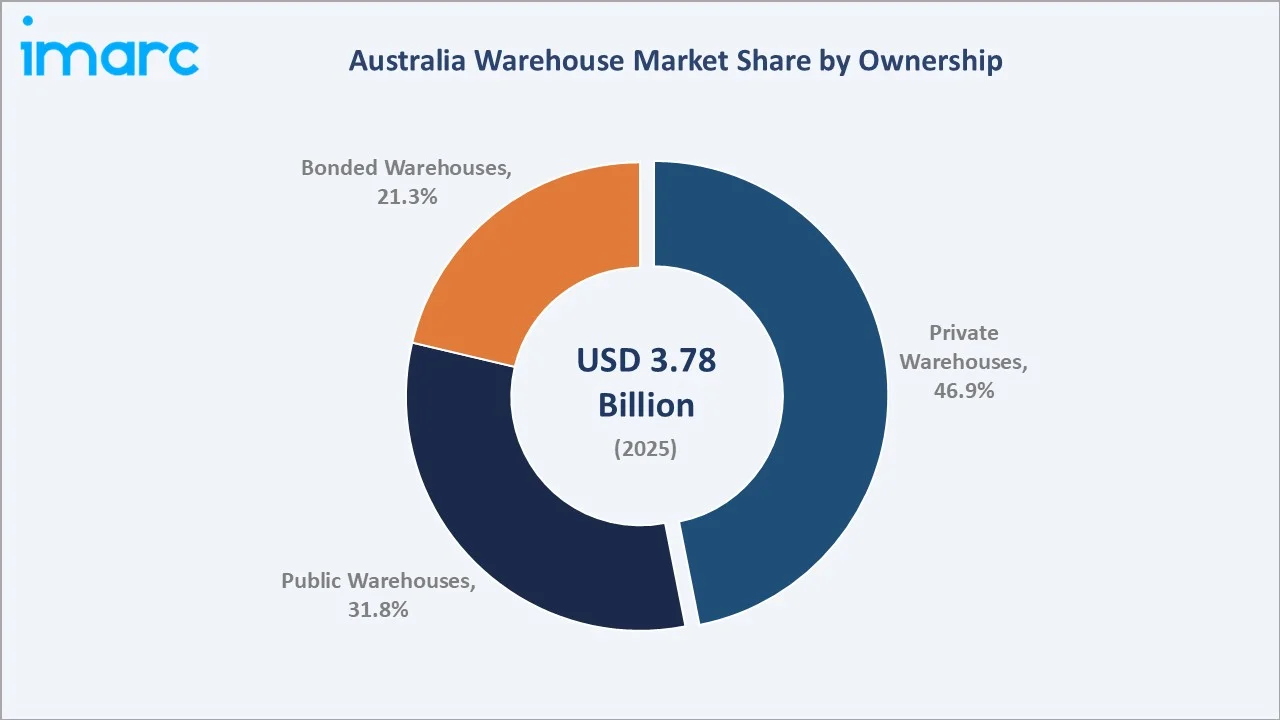

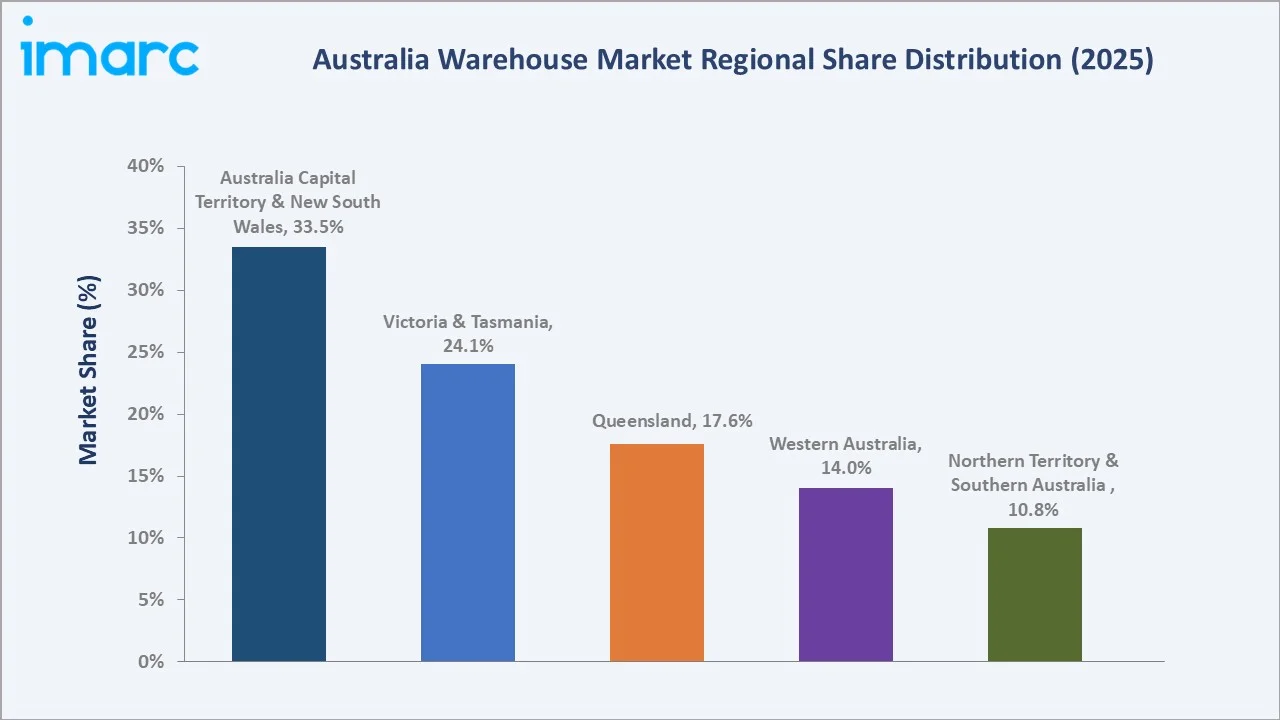

Industrial warehouses at 64.7% dominate through the concentration of Australia's manufacturing, e-commerce fulfillment, retail distribution, and pharmaceutical logistics in metropolitan fringe and semi-urban industrial areas requiring large-format, purpose-built distribution center facilities that command the highest rents and attract the largest institutional capital investment. Private warehouses at 46.9% reflect the preference of Australia's largest occupiers for dedicated, long-term-leased facilities in which they invest in bespoke automation systems that cannot be cost-effectively installed in shared or public warehousing. Australia Capital Territory & New South Wales dominated regionally at 33.5%.

Key Market Insights

|

Insight |

Data |

|

Dominant Sector |

Industrial Warehouses - 64.7% share (2025) |

|

Dominant Ownership |

Private Warehouses - 46.9% market share (2025) |

|

Leading Region |

Australia Capital Territory & New South Wales - 33.5% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Industrial warehouses at 64.7%: The industrial warehouses dominate the market due to strong demand from manufacturing, e-commerce, retail distribution, automotive, FMCG, and third-party logistics operations. The rising need for large-scale storage, inventory management, and efficient supply chain movement is further supporting higher adoption of industrial warehouse facilities.

- Private warehouses at 46.9%: Private warehouses dominate the market as large retailers, manufacturers, and logistics companies prefer dedicated storage facilities for better inventory control, operational flexibility, and faster distribution. Growing e-commerce, FMCG, cold chain, and industrial supply chain needs are further supporting investment in privately owned or leased warehouse spaces.

- Australia Capital Territory & New South Wales at 33.5%: The Australian Capital Territory & New South Wales region dominates the market due to the strong concentration of government procurement, corporate offices, ports, retail networks, and major logistics hubs around Sydney and Canberra. High demand from e-commerce, FMCG, manufacturing, and last-mile delivery operations further supports warehouse expansion across the region.

Australia Warehouse Market Overview

The Australia warehouse market encompasses the development, ownership, leasing, operation, and management of industrial property infrastructure used for storage, distribution, fulfillment, and value-added logistics services across all sectors of the Australian economy. The market includes super-prime logistics facilities, prime distribution centers, cold chain warehouses, self-storage facilities, agricultural grain and commodity storage, bonded customs warehouses, and specialist technical storage.

The ecosystem integrates industrial property developers and REITs, logistics operators and 3PL providers, warehouse technology providers, construction contractors, capital providers, occupiers, and the Australian Border Force for customs and bonded warehouse management. Macroeconomic factors include steady economic growth, rising consumer spending, expanding e-commerce, and increasing demand for faster distribution networks.

Market Dynamics

To evaluate market opportunities, Request Sample

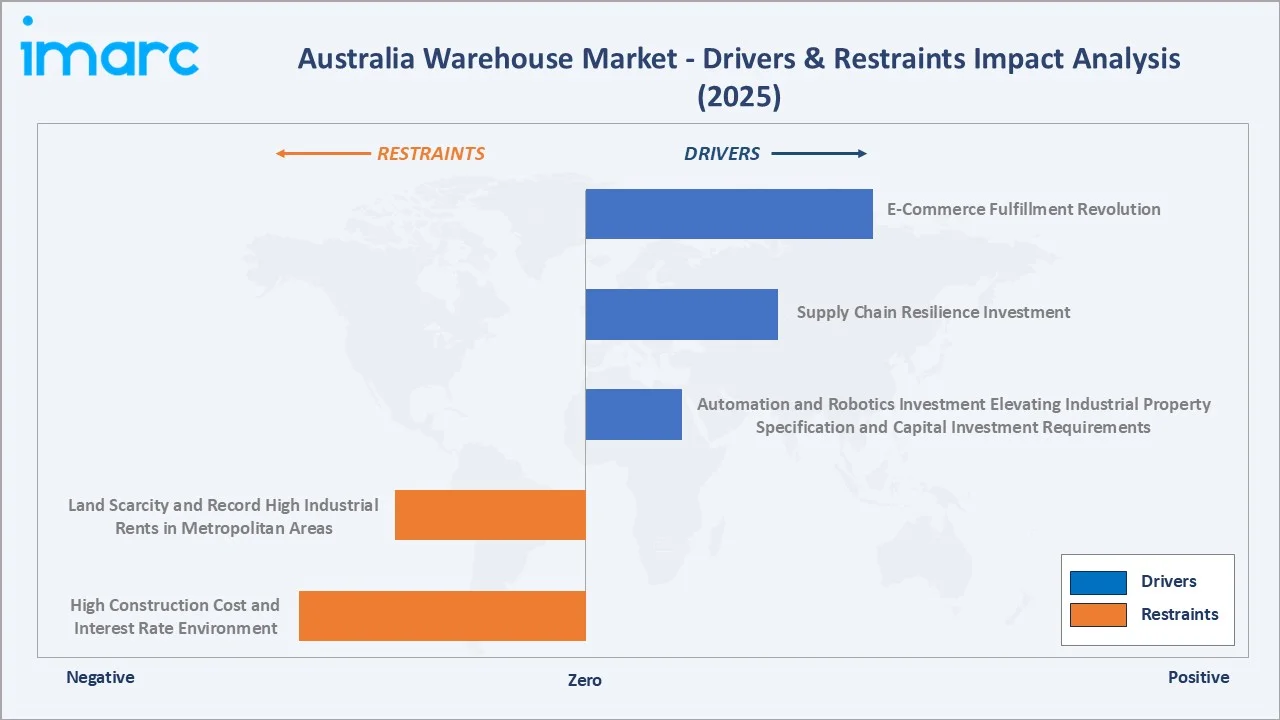

Market Drivers

- E-Commerce Fulfillment Revolution: The e-commerce fulfillment revolution is driving the market as online retailers require faster order processing, real-time inventory control, and efficient last-mile delivery networks. Rising demand for same-day and next-day delivery is encouraging investment in modern warehouses, automated fulfillment centers, and urban distribution hubs. This is increasing warehouse demand near major consumer markets, ports, and transport corridors across Australia.

- Supply Chain Resilience Investment: In Australia, the Supply Chain Resilience Initiative offers funding of up to $2 million to help establish or expand manufacturing capabilities, or related activities, that reduce supply chain vulnerabilities for critical products or inputs listed under the Sovereign Manufacturing Capability Plan. This supply chain resilience investment is driving as companies strengthen domestic storage, inventory buffering, and distribution capacity to reduce dependence on disrupted global supply chains. Government support for critical manufacturing and supply chain security is also encouraging demand for modern warehouses near industrial hubs, ports, and logistics corridors.

- Automation and Robotics Investment Elevating Industrial Property Specification and Capital Investment Requirements: The adoption of warehouse automation technology in Australia is creating a bifurcation of the industrial property market between conventional warehouses and automated facilities that command rental premiums over conventional properties and require 3-5x the capital investment per square metre.

Market Restraints

- Land Scarcity and Record High Industrial Rents in Metropolitan Areas: Land scarcity and record-high industrial rents in major metropolitan areas are increasing occupancy costs for logistics providers, retailers, and manufacturers. Limited availability of well-connected warehouse land near ports, highways, and urban consumers makes expansion difficult. This can push companies toward outer locations, raising transport costs and slowing last-mile delivery efficiency.

- High Construction Cost and Interest Rate Environment: High construction costs and elevated interest rates are increasing project development expenses, financing costs, and rental expectations. This makes new warehouse construction less attractive for developers and raises occupancy costs for tenants, especially SMEs and logistics operators. As a result, some companies may delay expansion, renegotiate leasing plans, or shift to lower-cost outer locations.

Market Opportunities

- Multi-Storey Urban Infill Warehouse Development Addressing Inner-Metropolitan Logistics Demand Near Population Centers: Multi-storey urban infill warehouse development addressing rising last-mile delivery demand near dense population centers. As land availability tightens in major cities, vertical warehouse formats allow logistics firms, retailers, and e-commerce players to maximize storage and fulfillment capacity on limited urban land. This supports faster delivery, lower transport distance, and stronger demand for high-value inner-metropolitan industrial assets.

- Western Sydney Airport (WSA) Aerotropolis Creating a Once-in-a-Generation Industrial Precinct Investment Opportunity: Western Sydney Airport Aerotropolis is developing a large-scale industrial, logistics, and advanced manufacturing precinct around the new airport. Its strong connectivity to air freight, road networks, and future supply chain corridors will attract e-commerce, 3PL, cold chain, and distribution operators. This is expected to drive demand for modern warehouses, fulfillment centers, and high-spec industrial facilities in Western Sydney.

Market Challenges

- Infrastructure Bottlenecks at Australian Ports Creating Supply Chain Inefficiency That Constrains Warehouse Throughput Economics: Infrastructure bottlenecks at Australian ports are slowing cargo movement, increasing dwell times, and disrupting inventory flow into distribution networks. Port congestion, limited transport connectivity, and delays in container handling can reduce warehouse throughput efficiency and raise logistics costs. This creates pressure on warehouse operators to invest in better inventory planning, buffer storage, and alternative distribution routes.

- FIRB (Foreign Investment Review Board) Scrutiny of Agricultural Land and Strategic Logistics Assets: FIRB scrutiny of agricultural land and strategic logistics assets is adding approval complexity for foreign investors targeting warehouse, cold chain, and logistics-linked land assets. Longer review timelines and national interest considerations can delay acquisitions, joint ventures, and large industrial property developments. This may slow capital inflows into strategic warehouse locations, especially near ports, transport corridors, food supply chains, and critical infrastructure zones.

Emerging Market Trends

1. Automated Mega-Distribution Centers Defining Australia's Next-Generation Warehouse Format

Automated mega-distribution centers are emerging as retailers, e-commerce companies, and 3PL providers invest in large, technology-enabled facilities. These centers use robotics, automated storage, conveyor systems, and real-time inventory platforms to improve speed, accuracy, and throughput. Rising demand for faster fulfillment and cost-efficient logistics is making automation-ready mega warehouses a preferred format across major Australian supply chain hubs. In November 2024, Coles Group Limited announced an investment of $880 million to develop a new Automated Distribution Center (ADC) in Truganina, Victoria, in partnership with WITRON Australia Pty Ltd.

2. ESG and Net-Zero Warehouse Development Becoming Standard Specification for Major Occupiers

ESG and net-zero warehouse development is emerging as major occupiers increasingly prefer facilities with solar panels, energy-efficient lighting, green building materials, water-saving systems, and lower-carbon operations. Developers are incorporating sustainability features to meet tenant ESG targets, reduce operating costs, and improve asset value. This is making green-certified, energy-efficient warehouses a standard requirement for large retailers, logistics firms, and industrial occupiers.

3. Cold Chain Warehouse Expansion Driven by Australia's Food Export Ambitions and Pharmaceutical Sector Growth

Cold chain warehouse expansion is emerging as food exporters require temperature-controlled storage to preserve quality, shelf life, and compliance during domestic and international distribution. Growth in pharmaceuticals, vaccines, biologics, and healthcare logistics is further increasing demand for specialized refrigerated and frozen storage facilities. This is encouraging investment in modern cold chain warehouses with automation, real-time temperature monitoring, and strong last-mile delivery connectivity.

4. Last-Mile Logistics Infrastructure Creating Urban Consolidation Center Demand

Last-mile logistics infrastructure is emerging as retailers, e-commerce firms, and logistics providers seek faster delivery closer to urban consumers. This is increasing demand for urban consolidation centers that can aggregate, sort, and dispatch goods efficiently within metropolitan areas. These facilities help reduce delivery times, manage congestion, lower transport costs, and improve fulfillment efficiency across major Australian cities. In July 2025, Emirates introduced its Emirates Courier Express service in Australia. The expansion reflects the airline’s focus on reshaping cross-border delivery with faster, more reliable, and flexible logistics support. Backed by an integrated first- and last-mile transport partner, the service is positioned to cover Australia.

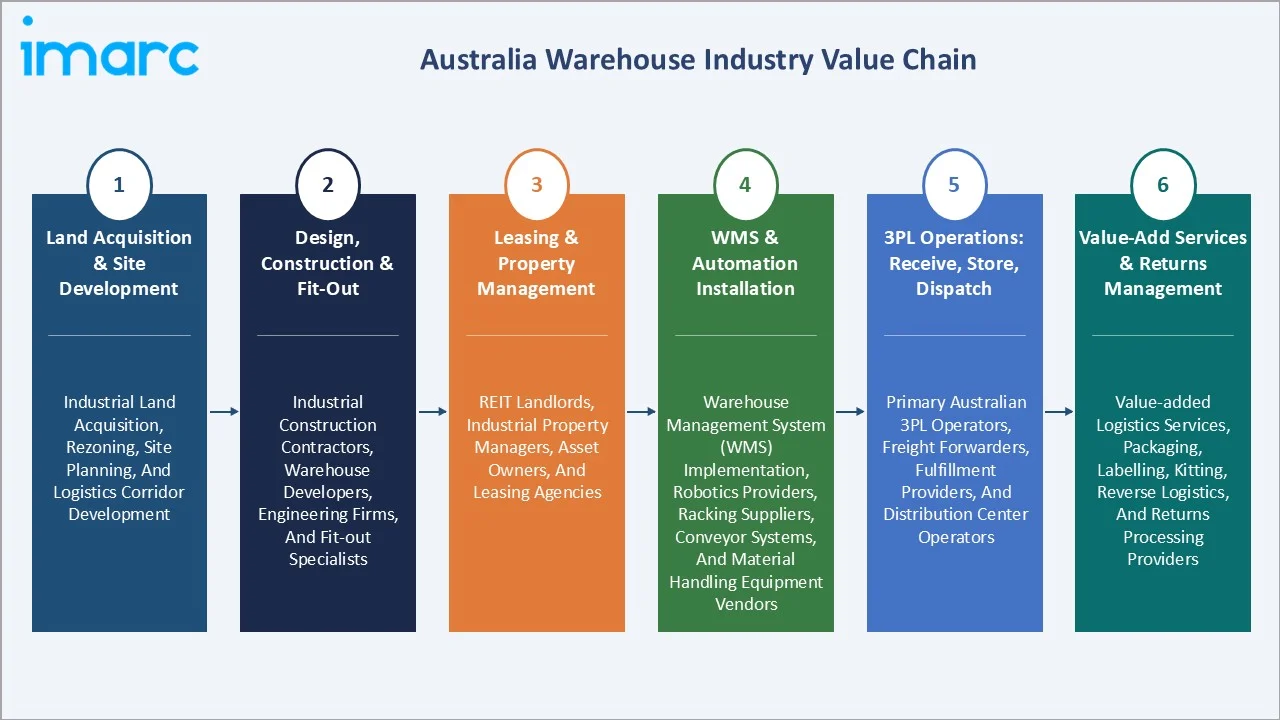

Industry Value Chain Analysis

The Australia warehouse market value chain integrates land acquisition and site development, design, construction and fit-out, leasing and property management, automation installation, 3PL operations, and value-added services and returns management. The value chain's commercial structure creates distinct revenue streams across property, services, and technology that are each addressable as distinct market segments.

|

Stage |

Key Participants |

|

Land Acquisition & Site Development |

Industrial land acquisition, rezoning, site planning, and logistics corridor development |

|

Design, Construction & Fit-Out |

Industrial construction contractors, warehouse developers, engineering firms, and fit-out specialists |

|

Leasing & Property Management |

REIT landlords, industrial property managers, asset owners, and leasing agencies |

|

WMS & Automation Installation |

Warehouse Management System (WMS) implementation, robotics providers, racking suppliers, conveyor systems, and material handling equipment vendors |

|

3PL Operations: Receive, Store, Dispatch |

Primary Australian 3PL operators, freight forwarders, fulfillment providers, and distribution center operators |

|

Value-Add Services & Returns Management |

Value-added logistics services, packaging, labelling, kitting, reverse logistics, and returns processing providers |

The value-added services and returns management tier are the warehouse value chain's highest-margin operating segment. Australian 3PL operators have progressively expanded value-added services capability as the most commercially differentiated capability that prevents commoditization of standard warehousing and transport services. E-commerce returns management is the fastest-growing value-added service.

Technology Landscape in the Australia Warehouse Industry

Warehouse Management Systems

Warehouse management systems are enabling real-time inventory tracking, order management, labour planning, and warehouse process automation. As e-commerce, 3PL, retail, and cold chain operations expand, WMS platforms help improve fulfillment speed, accuracy, and space utilization. Integration with robotics, barcode/RFID systems, transport management, and analytics is making WMS a core technology layer for modern Australian warehouses.

Collaborative Mobile Robots

Collaborative mobile robots are automating goods movement, picking support, sorting, and replenishment within fulfillment centers. As labour costs rise and e-commerce volumes grow, warehouses are adopting robots that work alongside human workers to improve speed, accuracy, and productivity. In March 2026, Amazon Australia announced plans to invest over AU$750 million in a new robotics fulfillment center designed to handle more than 125 million packages annually. This is driving collaborative mobile robots technology in the Australia warehouse industry by accelerating the adoption of robotics-enabled picking, sorting, movement, and fulfillment operations.

Yard and Dock Management Technology

Yard and dock management technology is improving vehicle scheduling, dock allocation, trailer tracking, and loading/unloading coordination. As warehouse volumes rise across e-commerce, 3PL, retail, and cold chain logistics, these systems help reduce congestion, waiting time, and manual coordination at warehouse gates. Integration with WMS, TMS, RFID, GPS, and real-time analytics is making yard and dock visibility essential for faster warehouse throughput and supply chain efficiency.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Sector |

Industrial Warehouses |

64.7% |

2025 |

|

Ownership |

Private Warehouses |

46.9% |

2025 |

|

Type of Commodities Stored |

🔒 |

🔒 |

2025 |

|

Region |

Australia Capital Territory & New South Wales |

33.5% |

2025 |

By Sector

Industrial warehouses lead at 64.7% market share (2025). Industrial warehouses encompass the full range of logistics and distribution infrastructure, e-commerce fulfillment centers, retail distribution centers, pharmaceutical distribution, manufacturing parts storage, automotive distribution, electronics assembly and distribution, and third-party logistics facilities.

To access detailed market analysis, Request Sample

Agricultural warehouses at 35.3% encompass grain silos and bulk storage, sugar mills and storage, cotton gin warehouses, refrigerated cool stores for fruit and vegetables, and livestock facilities for live export staging.

By Ownership

Private warehouses lead at 46.9% market share (2025). Private warehouse revenue reflects long-term occupied facilities where the occupier controls the building either through ownership or a 15-20+ year lease, investing in bespoke fit-out and automation.

Public warehouses at 31.8% serve the 3PL-managed shared user segment, where multiple clients share building, labour, and infrastructure. Bonded warehouses at 21.3% serve Australia's import and export trade, requiring customs duty deferral.

Regional Market Insights

|

Region |

Share (2025) |

Key Warehouse Market Drivers & Characteristics |

|

Australia Capital Territory & New South Wales |

33.5% |

Driven by strong logistics activity, e-commerce demand, port connectivity, and Sydney’s role as a major consumption and distribution hub. |

|

Victoria & Tasmania |

24.1% |

Benefit from strong manufacturing, retail distribution, food processing, and freight movement activity, with Melbourne serving as a major warehousing and logistics hub. |

|

Queensland |

17.6% |

Supported by population growth, expanding urban logistics, infrastructure development, and rising demand from retail, FMCG, cold chain, and regional distribution networks. |

|

Northern Territory & Southern Australia |

10.8% |

Driven by resource-linked logistics, defense supply chains, agricultural storage, and regional freight distribution requirements. |

|

Western Australia |

14.0% |

Shaped by mining, energy, industrial supply chains, export activity, and the need for storage facilities supporting remote and resource-based operations. |

ACT and NSW at 33.5% leads through Western Sydney's mega-warehouse development pipeline and Port Botany's container port-adjacent logistics demand. Victoria and Tasmania, at 24.1%, reflect Melbourne's port-driven logistics infrastructure and Victoria's role as Australia's food manufacturing distribution hub.

Queensland, at 17.6%, is growing through Brisbane's Olympic infrastructure investment and the state's agricultural export supply chain. Western Australia, at 14.0%, reflects a resources sector goods distribution hub and an agricultural storage network. NT and SA, at 10.8%, are anchored by defence logistics and their role as Northern Australia's trade gateway.

Competitive Landscape

The Australian warehouse market's competitive landscape is structured across three distinct competitive domains: industrial property development and ownership; logistics operations and 3PL services; and agricultural storage infrastructure. These three competitive domains intersect in the growing segment of integrated logistics real estate, where property developer-operator models compete with pure property and pure operations across the warehouse value chain.

|

Company Name |

Key Portfolio |

Market Position |

Core Strength |

|

Linfox Pty Ltd. |

Modern warehousing, Automated distribution centers, Distribution, Multiuser operations, Industrial warehousing, Remote logistics, Dangerous goods storage |

Market Leader |

Linfox is leading the way in designing and managing efficient, safe and sustainable warehouse operations. |

|

Charter Hall Group |

Next-Generation Warehouses and Logistics Facilities |

Challenger |

Charter Hall Group is recognized for delivering premium, next-generation warehouses and logistics facilities. |

|

The GPT Group |

Leasing Warehouse Spaces and Logistics |

Established Player |

The GPT Group’s logistics portfolio and development pipeline enable the delivery of warehouse solutions designed for growth and adaptability. |

The competitive landscape is being reshaped by the emergence of global logistics REIT capital competing with domestic ASX-listed REITs for the limited premium industrial land and completed stock in Australia's major logistics precincts. The global capital advantage competes with domestic capital's relationship advantage in determining who wins industrial development opportunities in the Australian market.

Key Company Profiles

Linfox Pty Ltd.

Linfox Pty Ltd. is advancing efficient, safe, and sustainable warehouse operations designed for the specific needs of the industries it serves and built to scale for future growth. Its advanced warehouse management systems support a wide network of multi-user facilities, enabling the company to handle large goods volumes, manage demand fluctuations, and provide flexible short-term, long-term, and overflow storage solutions for customers.

- Key Portfolio: Modern warehousing, Automated distribution centers, Distribution, Multiuser operations, Industrial warehousing, Remote logistics, Dangerous goods storage.

- Recent Developments: In January 2026, Linfox introduced advanced AI-powered autonomous technology to improve warehouse efficiency across its operations. The system is being used to conduct daily warehouse scans at Linfox’s BevChain Laverton facility in Victoria, supporting better visibility, accuracy, and operational control.

- Strategic Focus: To enhance efficient, safe, and scalable warehousing through advanced WMS, AI-enabled operations, multi-user facilities, and sustainable logistics solutions.

Charter Hall Group

Charter Hall Group is a major Australia-headquartered property investment and development company with a strong presence in industrial and logistics real estate. The company develops, owns, and manages next-generation warehouse and logistics facilities designed for major Australian and global occupiers, supported by national scale and local market expertise.

- Key Portfolio: Next-Generation Warehouses and Logistics Facilities.

- Recent Developments: In March 2025, Charter Hall Group announced that its Charter Hall Core Logistics Partnership completed its first multi-level warehouse, Ascent on Bourke, located in Alexandria, Sydney.

- Strategic Focus: To expand premium, technology-ready, and sustainable industrial and logistics assets across Australia, serving retail, e-commerce, manufacturing, and 3PL occupiers.

Market Concentration Analysis

The Australian industrial property development market exhibits high concentration at the top - Linfox Pty Ltd., Charter Hall Group, and The GPT Group collectively account for an estimated 50-60% of new Australian industrial development completions annually by floor area, reflecting the substantial capital, development expertise, and occupier relationship advantages that these three scaled industrial property groups hold over smaller developers. The 3PL logistics operations market is more fragmented at the tier-2 level. The agricultural storage market is the most concentrated sub-sector. Market concentration is expected to increase through 2034 as automation capital requirements escalate the minimum scale for competitive mega-DC operations, further favouring large REITs and global logistics operators over smaller competitors.

Investment & Growth Opportunities

Highest Growth Segments

Industrial warehouses (~9.7% CAGR), private warehouses (~9.5% CAGR), cold chain and pharmaceutical warehousing (~12-15% CAGR within industrial warehouse), automated mega-DC fulfillment (~15-20% CAGR from growing base), Western Sydney Aerotropolis industrial development (~20%+ CAGR for new builds in the precinct 2026-2030), and e-commerce last-mile urban consolidation center (~18-25% CAGR from small base) represent the highest-growth investment vectors in the Australian warehouse market through 2034.

Emerging Investment Opportunities

Australian data center-adjacent industrial land represents the most commercially transformative emerging opportunity in industrial property. The global data center investment pipeline, driven by AI infrastructure demand, creates a once-per-generation value creation opportunity for industrial landholders in precincts adjacent to high-voltage power infrastructure and major fibre routes.

Investment Themes

- Cold chain pharmaceutical and healthcare warehouse development as high-yield industrial sub-sector: TGA-compliant pharmaceutical cold chain warehouses command industrial property yields of 7.5-9.5% versus 5.0-6.5% for prime ambient industrial, reflecting the regulatory compliance premium, specialist fit-out cost, and tenant quality.

- Agricultural warehouse modernisation and digital cold chain investment for premium export market access: Premium Australian agricultural export markets require cold chain provenance documentation that current Australian agricultural warehouse infrastructure cannot provide at scale.

Future Market Outlook (2026-2034)

The Australia warehouse market is projected to grow from USD 3.78 Billion in 2025 to USD 8.68 Billion by 2034, delivering a 9.40% CAGR over the forecast period. The market's anchor value of USD 5.92 Billion in 2030 represents the Australian warehouse industry at its most transformative phase. Three structural forces define Australian warehouse market growth through 2034 with high confidence. The e-commerce penetration trajectory creates a permanent structural increment to warehouse space demand per dollar of retail turnover that compounds with population growth and household formation. Population growth adds 1.0-1.3 million Australians to the metropolitan consumption base per decade, creating demand for 800,000-1.0 million sqm of additional retail distribution warehouse space per decade from population growth alone. Automation investment, creating a replacement investment cycle that sustains warehouse fit-out and technology spending above the simple rental revenue growth trajectory.

Research Methodology

Primary Research

Primary research comprised structured interviews with 50+ industry stakeholders (2025); Head of Industrial Leasing; National Operations Directors; Development Directors; Cold Chain Operations Managers; Agricultural Warehouse Operations Directors; and major occupier Supply Chain Directors.

Secondary Research

Secondary research encompassed Australia Industrial and Logistics Market Outlook 2025 (quarterly market statistics for all major Australian industrial markets); JLL Australia Industrial Snapshot; Colliers Australia Industrial Market Report; Building Approvals data (industrial building approvals by state); National Industrial Supply Census (Industrial property industry data); company publications and media disclosures; individual company annual reports. Over 60 secondary sources reviewed.

Forecasting Models

Market revenue forecasts were developed using a combination of (i) industrial property market rent and floor area modelling, (ii) 3PL logistics revenue modelling (warehousing revenue component from IBISWorld Australia Logistics and Warehousing Industry data, 3PL market size estimates, and individual company revenue disclosures), (iii) agricultural storage revenue modelling, warehouse automation investment accelerating effective rent equivalence, cold chain segment above-market growth calibrated against pharmaceutical and agricultural export data.

Australia Warehouse Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Sectors Covered | Industrial Warehouses, Agricultural Warehouses |

| Ownerships Covered | Private Warehouses, Public Warehouses, Bonded Warehouses |

| Types of Commodities Stored Covered | General Warehouses, Speciality Warehouses, Refrigerated Warehouses |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Linfox Pty Ltd., Charter Hall Group, The GPT Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia warehouse market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia warehouse market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia warehouse industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Warehouse Market Report

The Australia warehouse market reached USD 3.78 Billion in 2025, driven by Western Sydney mega-distribution center development, record-low industrial vacancy rates sustaining 10-20% annual rental growth in Sydney and Melbourne prime logistics precincts, cold chain pharmaceutical and fresh food warehouse expansion, agricultural grain and commodity storage investment, and 3PL logistics operators expanding managed warehouse capacity to serve growing e-commerce fulfillment demand.

The market grows at 9.40% CAGR during 2026-2034, reaching USD 8.68 Billion by 2034. Growth is driven by e-commerce penetration growing toward 30%+ of Australian retail, pharmaceutical cold chain investment sustaining above-market growth, agricultural warehouse modernisation investment, and automation technology refresh cycles creating recurring warehouse fit-out investment.

Industrial warehouses lead at 64.7% through e-commerce fulfillment mega-DCs, pharmaceutical distribution, retail supply chain, and manufacturing goods storage. Industrial warehouses also grow fastest at ~9.7% CAGR.

Private warehouses lead at 46.9% through pharmaceutical distributors occupying dedicated long-lease facilities, enabling AUD 50-200 Million automation investment.

ACT and New South Wales lead at 33.5% through Western Sydney's mega-DC development pipeline and Port Botany's container logistics hub.

Leading companies include Linfox Pty Ltd., Charter Hall Group, and The GPT Group, among others.

The market is projected to reach approximately USD 5.92 Billion by 2030, with Western Sydney International Airport opening catalysing Aerotropolis industrial development momentum, automated mega-DCs becoming standard for major retailers, cold chain pharmaceutical warehouse investment, and multi-storey urban warehouses normalising in inner metropolitan markets.

Warehouse automation is creating a bifurcation between automated mega-DCs and conventional warehouses. Automated facilities command 20-40% rental premiums over conventional properties and require 15-20 year leases to amortise automation capital, creating long-duration institutional income that attracts superannuation fund investment to industrial property at an unprecedented scale.

Three priority opportunities: Western Sydney Aerotropolis land development, pharmaceutical cold chain warehousing, and agricultural cold chain technology investment for premium export.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)