Australia Waste Management Market Size, Share, Trends and Forecast by Waste Type, Service, Source, and Region, 2026-2034

Australia Waste Management Market Size, Share, Trends & Forecast (2026-2034)

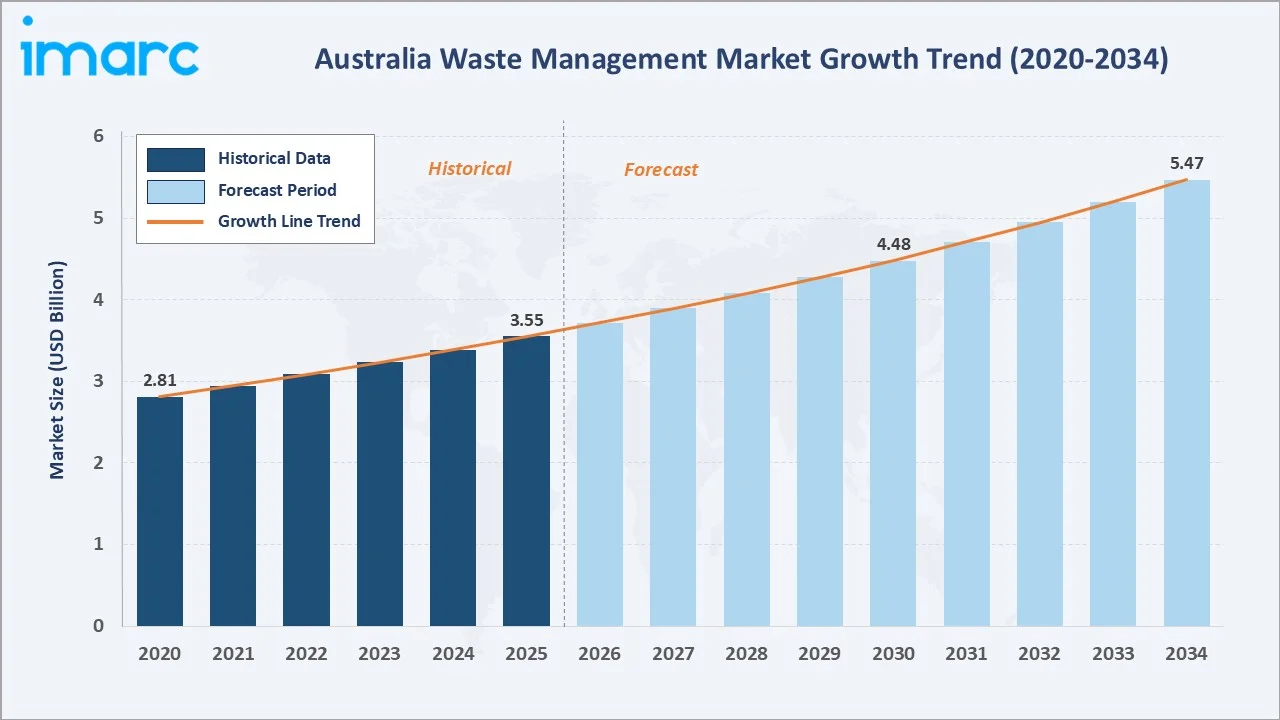

The Australia waste management market reached USD 3.55 Billion in 2025 and is projected to reach USD 5.47 Billion by 2034, exhibiting a CAGR of 4.77% during 2026-2034. Growth is anchored by Australia's National Waste Policy targets, state-level landfill diversion mandates, expanding container deposit schemes, scaling waste-to-energy infrastructure, and structural demand from industrial, residential, and commercial waste streams across metropolitan and regional Australia.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.55 Billion |

|

Market Forecast (2034) |

USD 5.47 Billion |

|

CAGR (2026-2034) |

4.77% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

Rising urbanization, industrial activity, construction waste generation, and growing environmental concerns are increasing the need for efficient collection, sorting, treatment, recycling, and disposal services.

To get more information on this market, Request Sample

In addition, businesses and households are becoming more conscious of sustainable waste handling, supporting demand for services such as e-waste recycling, food waste recovery, hazardous waste treatment, and waste-to-energy solutions across Australia.

Executive Summary

Australia's waste management market is a structurally mature, regulation-led category supported by federal and state-level commitments to landfill diversion, circular economy outcomes, and resource recovery. The market accounted for USD 3.55 Billion in 2025 and is expected to reach USD 5.47 Billion at a CAGR of 4.77% from 2026 to 2034.

The 2018 National Waste Policy and the Recycling and Waste Reduction Act 2020 frame the regulatory environment, complemented by state-level targets: Victoria's 72% landfill diversion (2025), Queensland's 50–75% recycling rate targets, Western Australia's 70% recovery objective, and South Australia's 70–90% diversion targets. Industry consolidation continues with major M&A across Cleanaway, Veolia, REMONDIS, and Bingo.

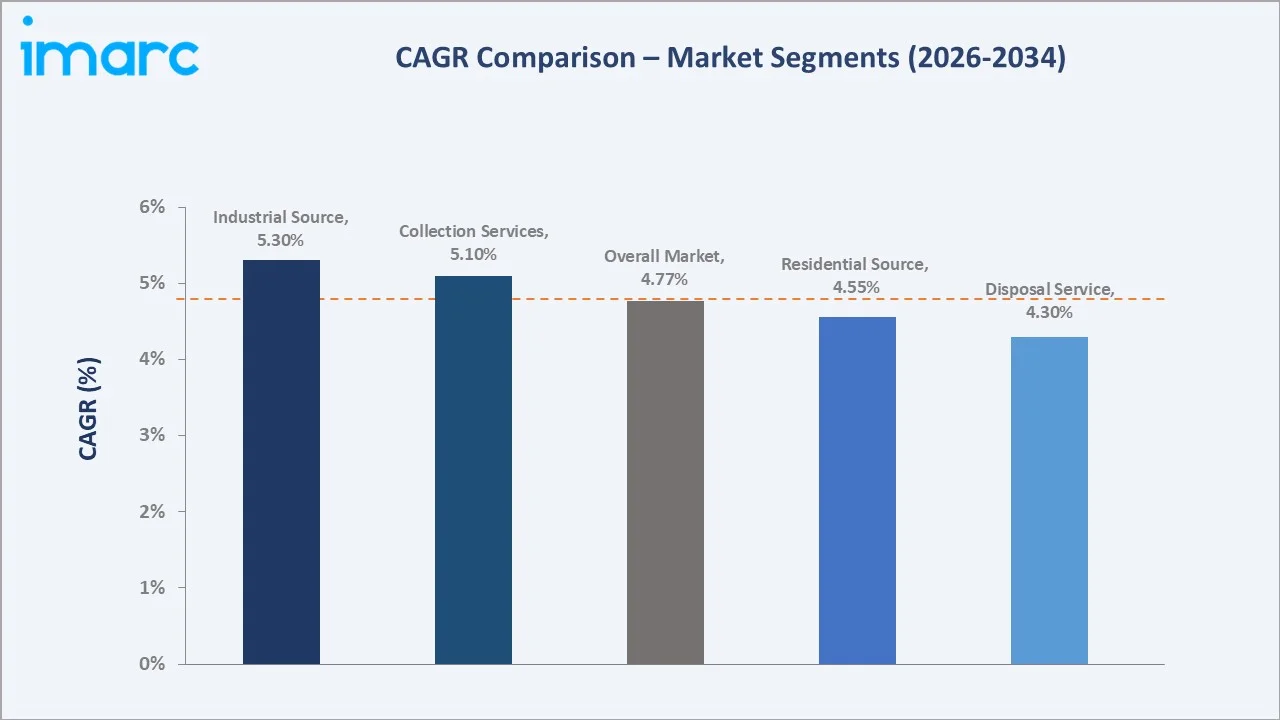

Key market milestones include Cleanaway's six-year Defense contract in QLD and WA (December 2024) and Veolia ANZ and ResourceCo partnership to supply over 1 million tons of sustainable refuse-derived fuel (RDF) from its Adelaide facility to Adbri Cement’s Birkenhead plant, helping replace natural gas in cement production. Collection dominates services at 57.6%, industrial leads sources at 38.5%, and Australian Capital Territory & New South Wales anchor regional share at 33.6%.

Key Market Insights

|

Indicator |

Value (2025) |

|

Leading Service |

Collection (57.6%) |

|

Fastest-Growing Service |

Collection (~5.1% CAGR) |

|

Leading Source |

Industrial (38.5%) |

|

Fastest-Growing Source |

Industrial (~5.3% CAGR) |

|

Largest Region |

Australian Capital Territory & New South Wales (33.6%) |

|

Key Players |

Cleanaway Waste Management Limited, Veolia Environnement SA, REMONDIS SE & Co. KG, Waster Pty Ltd |

Key Analytical Observations Supporting the Above Data:

- Collection services account for 57.6% of the Australian waste management market in 2025, reflecting demand for kerbside pickup, skip bin services, industrial waste collection, and commercial waste removal across all states and territories.

- Disposal services at 42.4% (2025) encompass engineered landfills, transfer stations, hazardous waste treatment, organics composting, and emerging waste-to-energy facilities, with Veolia's Kwinana Energy Recovery Facility representing flagship infrastructure.

- Industrial waste at 38.5% (2025) leads the source segmentation, supported by mining, manufacturing, construction, and demolition activity. The segment is projected to grow at approximately 5.3% CAGR through 2034, anchored by ResourceCo's refuse-derived fuel agreements and industrial-decarbonization contracts.

- Residential waste at 34.2% (2025) benefits from urbanization, household formation, expanding container deposit schemes, and rising kerbside recycling adoption. Commercial waste at 27.3% reflects retail, hospitality, and office building activity across major metropolitan markets.

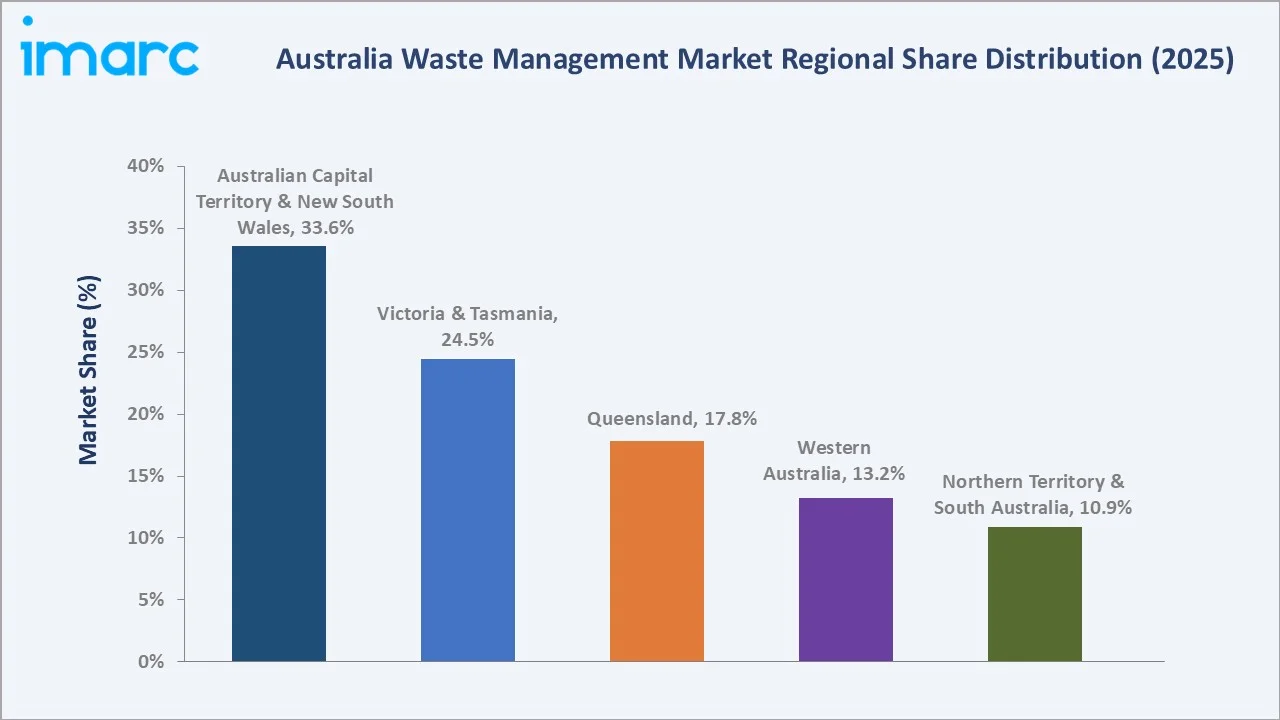

- Australian Capital Territory & New South Wales' 33.6% (2025) regional share reflects Sydney's position as Australia's largest metropolitan market, the highest concentration of waste collection contracts, and strong policy alignment with NSW Waste and Sustainable Materials Strategy targets.

Australia Waste Management Market Overview

Waste management refers to the collection, transport, processing, recycling, treatment, and disposal of waste materials generated by industrial, residential, commercial, and institutional sources. The Australian market spans municipal solid waste (MSW), commercial and industrial (C&I) waste, construction and demolition (C&D) waste, hazardous and clinical waste, e-waste, and organics.

Australia's waste management framework is anchored by the National Waste Policy, the Recycling and Waste Reduction Act 2020, the Product Stewardship Act 2011, and state-level waste levies. The National Plastics Plan and Container Deposit Schemes underpin material-stream recovery, while waste-to-energy projects including Kwinana represent strategic infrastructure additions.

Market Dynamics

To evaluate market opportunities, Request Sample

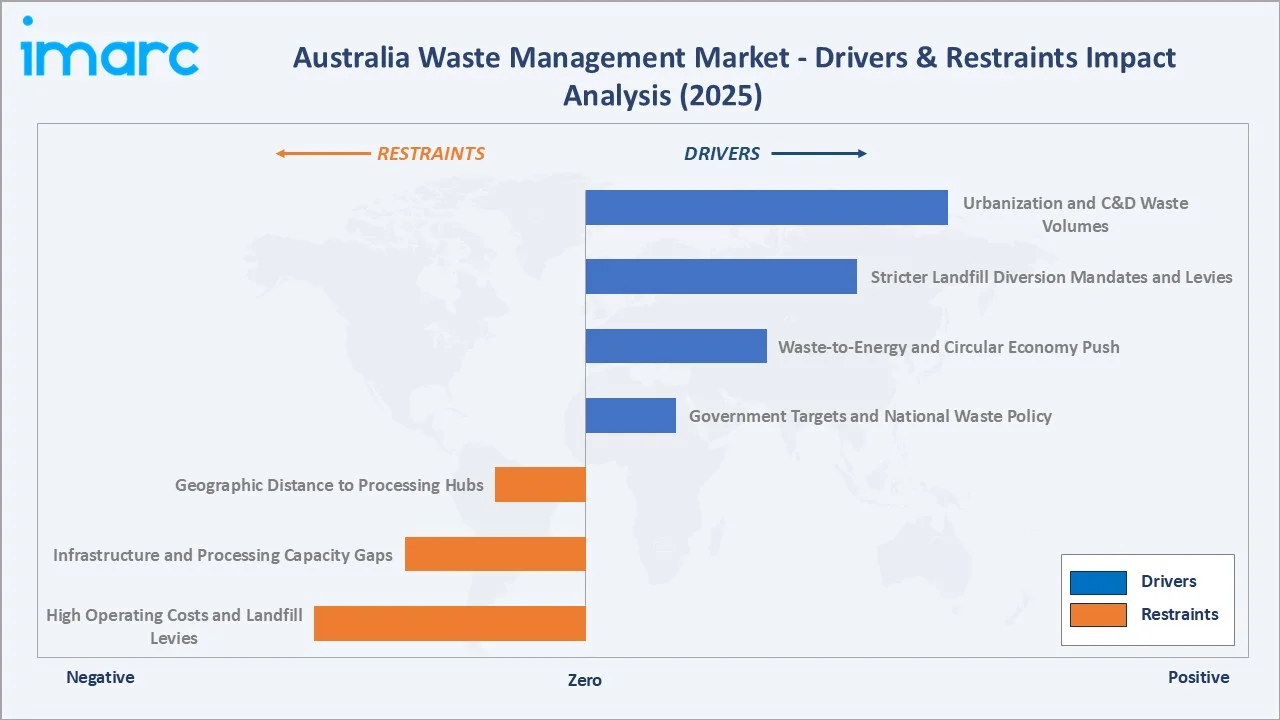

Market Drivers

- Government Targets and National Waste Policy: Australia's National Waste Policy, the Recycling and Waste Reduction Act 2020, and the National Plastics Plan have established binding landfill diversion, recycling, and product stewardship targets. State commitments include Victoria's 72% landfill diversion by 2025 and Queensland's 55–65% recycling rate targets, collectively driving sustained infrastructure investment.

- Waste-to-Energy and Circular Economy Push: Australia's first commercial-scale waste-to-energy plant, the Kwinana Energy Recovery Facility, began commercial operations in December 2025 and was officially opened in November 2025. The facility processes up to 460,000 tons of municipal and commercial non-recyclable waste each year, equivalent to about 25% of Perth’s residual waste.

- Stricter Landfill Diversion Mandates and Levies: State-level landfill levies and tightening enforcement are accelerating substitution toward recycling, organics treatment, and resource recovery. Container Deposit Schemes are now operational in every Australian state, with TOMRA Cleanaway contributing to record material-stream recovery volumes.

- Urbanization and C&D Waste Volumes: Australia's urban population reached 23 million in 2025, with urban areas generating the majority of national waste. Residential construction activity recorded a 19.4% increase to AUD 7.14 billion in new construction value (January 2024), driving structural C&D waste volume growth.

Market Restraints

- High Operating Costs and Landfill Levies: Rising operational costs across fuel, labor, vehicle maintenance, and processing facilities, combined with escalating state-level landfill levies, compress operator margins and increase end-customer pricing. Higher levies are policy-effective in driving diversion but require sustained capital investment in alternative treatment infrastructure.

- Infrastructure and Processing Capacity Gaps: Australia faces persistent gaps in advanced recycling, organics treatment, and waste-to-energy processing capacity, particularly outside metropolitan areas. Post-2018 China National Sword policy impacts continue to drive domestic processing investment requirements, with long lead times for new facility commissioning.

- Geographic Distance to Processing Hubs: Australia's geographic scale and dispersed population create high transport costs for regional and remote waste streams. Processing hubs concentrated in major metropolitan centers limit cost-effective diversion in regional areas, particularly the Northern Territory and parts of Western Australia.

Market Opportunities

- Waste-to-Energy Infrastructure Expansion: Following Kwinana's commercial operation, further waste-to-energy projects are in development across New South Wales and Victoria. Operators with operations-and-maintenance and feedstock supply capability are positioned for multi-decade contract value, exemplified by Cleanaway's non-recyclables supply contract with Acciona for Kwinana.

- Advanced Recycling and Soft Plastics: In April 2025, Cleanaway and Viva Energy signed a Memorandum of Understanding to advance to a full feasibility study for Australia's first large-scale advanced soft plastics recycling facility, following successful completion of their pre-feasibility assessment.

Market Challenges

- Regulatory Complexity Across States: Varying landfill levies, waste levy bands, container deposit scheme implementations, and state-specific waste strategies create operational complexity for national operators. Compliance and reporting overhead remains significant, particularly across multi-state collection and processing operations.

- Workforce and Heavy-Vehicle Capacity: Skilled driver, plant operator, and engineer shortages affect collection fleet reliability and processing facility operations. Heavy-vehicle cost inflation and electrification transition pressures add operational complexity for national fleet operators.

Emerging Market Trends

1. Waste-to-Energy Becomes Operational Reality

In December 2025, Veolia reopened its refurbished EarthPower facility, restoring Australia’s first food waste-to-energy plant and strengthening the country’s organic waste recovery infrastructure. The facility can process 62,500 tons of solid and liquid food waste annually and generate enough green electricity to power approximately 4,000 homes at full capacity.

2. Strategic Consolidation and Capability Acquisition

In March 2025, Cleanaway announced its intention to acquire Contract Resources Group to enhance technical services and decontamination capabilities. Bingo Industries Limited was acquired by Macquarie Infrastructure and Real Assets, and REMONDIS has expanded through targeted acquisitions following ACCC divestiture requirements related to Veolia's acquisition of SUEZ assets.

3. Industrial Decarbonization Through Refuse-Derived Fuel

In May 2024, Veolia ANZ and ResourceCo partnered to supply more than 1 million tons of sustainable refuse-derived fuel (RDF) from its Adelaide facility to Adbri Cement’s Birkenhead plant, helping replace natural gas use. The model represents a scalable circular-economy pathway combining waste diversion targets with industrial fossil-fuel substitution outcomes.

4. Advanced Recycling for Difficult Waste Streams

In April 2025, Cleanaway and Viva Energy signed a MoU to conduct a full feasibility study for Australia's first large-scale advanced soft plastics recycling facility, addressing one of the country's most challenging recyclate streams. Visy continues to invest in upstream recycling capability, including an AUD 37 million drum pulping system to eliminate contaminants from wastepaper.

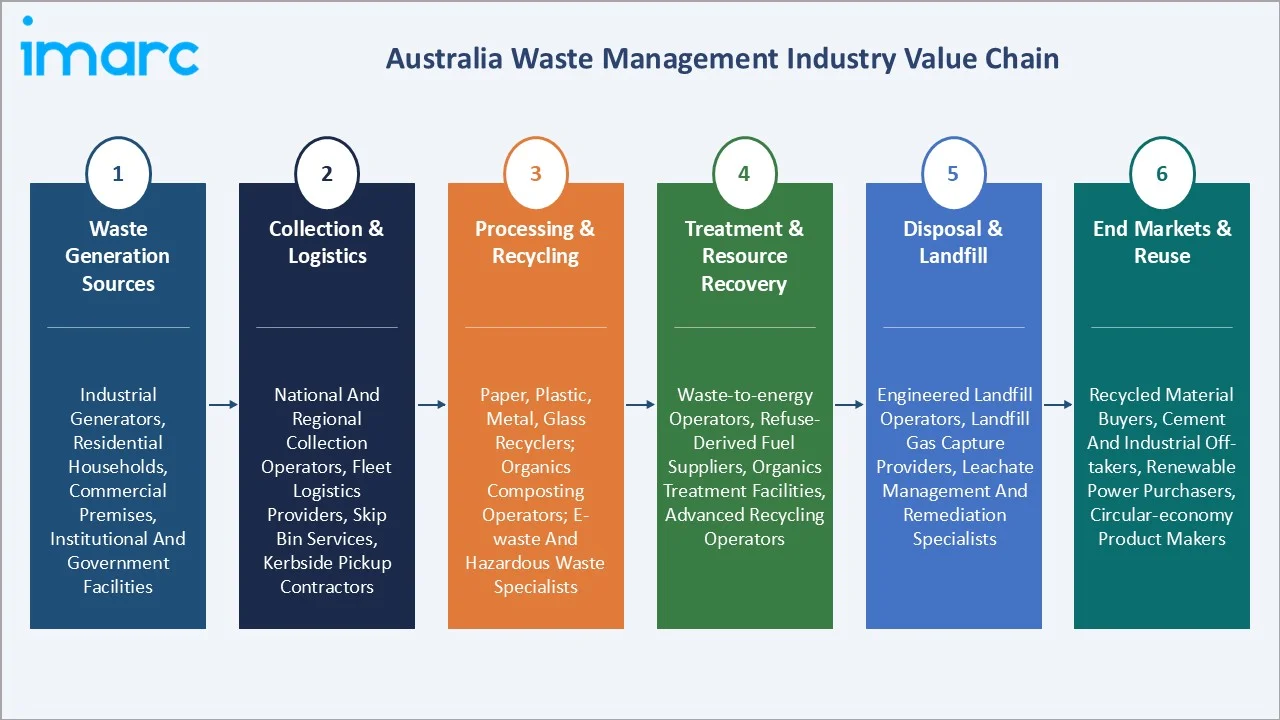

Industry Value Chain Analysis

|

Stage |

Key Players / Activities |

|

Waste Generation Sources |

Industrial generators, residential households, commercial premises, institutional and government facilities |

|

Collection & Logistics |

National and regional collection operators, fleet logistics providers, skip bin services, kerbside pickup contractors |

|

Processing & Recycling |

Paper, plastic, metal, glass recyclers; organics composting operators; e-waste and hazardous waste specialists |

|

Treatment & Resource Recovery |

Waste-to-energy operators, refuse-derived fuel suppliers, organics treatment facilities, advanced recycling operators |

|

Disposal & Landfill |

Engineered landfill operators, landfill gas capture providers, leachate management and remediation specialists |

|

End Markets & Reuse |

Recycled material buyers, cement and industrial off-takers, renewable power purchasers, circular-economy product makers |

Technology Landscape in the Australia Waste Management Industry

Material Recovery Facilities (MRFs) and Sorting Automation

Modern MRFs deploy automated sorting technologies including optical sorters, ballistic separators, eddy current separators, and AI-driven robotic picking systems to improve recyclate purity and recovery rates. Investment continues across major Sydney, Melbourne, and Brisbane MRFs to address post-2018 China National Sword export quality requirements and to support container deposit scheme recoveries.

Waste-to-Energy and Refuse-Derived Fuel

Waste-to-energy technologies span moving-grate combustion, gasification, and refuse-derived fuel (RDF) production for industrial off-takers. The Kwinana Energy Recovery Facility represents the first major commercial-scale Australian deployment, while Veolia ResourceCo's Adbri Cement RDF contract demonstrates an industrial decarbonization business model.

Organics Treatment and Composting

In-vessel composting, anaerobic digestion, and open-windrow composting technologies underpin organics diversion targets across all states. FOGO (Food Organics and Garden Organics) collection has expanded across major metropolitan local government areas, supported by operator investment in regional composting facilities.

Advanced and Soft Plastics Recycling

Advanced recycling technologies, including chemical recycling and pyrolysis, are emerging as solutions for soft plastics and contaminated streams. In April 2025, Cleanaway and Viva Energy signed a Memorandum of Understanding to proceed with a full feasibility study for Australia’s first large-scale advanced soft plastics recycling facility, after completing the pre-feasibility assessment.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Service |

Collection |

57.6% |

2025 |

|

Source |

Industrial |

38.5% |

2025 |

|

Waste Type |

🔒 |

🔒 |

2025 |

|

Region |

Australian Capital Territory & New South Wales |

33.6% |

2025 |

By Service

Collection services dominate with a 57.6% share in 2025, reflecting demand for kerbside pickup, skip bin services, industrial waste collection, and commercial waste removal. National operators including Cleanaway Waste Management Limited, Veolia Environnement SA, and REMONDIS SE & Co. KG anchor the segment with broad fleet capability and multi-stream contracts across metropolitan and regional Australia.

To access detailed market analysis, Request Sample

Disposal services account for 42.4% in 2025, encompassing engineered landfills, transfer stations, hazardous waste treatment, organics composting, material recovery facilities, and waste-to-energy infrastructure. The disposal segment includes specialized operators in C&D recycling, e-waste processing, hazardous waste treatment, and energy recovery, with significant capital intensity and long contract durations.

By Source

Industrial waste leads with a 38.5% share in 2025, supported by mining, manufacturing, construction, and demolition activity across Australia. The segment is projected to grow at approximately 5.3% CAGR through 2034, anchored by ResourceCo's refuse-derived fuel agreements with cement producers and broader industrial-decarbonization contracts.

Residential waste at 34.2% reflects urbanization, household formation, and rising kerbside recycling adoption. Commercial waste at 27.3% covers retail, hospitality, office, and institutional waste streams, benefiting from sustainability-led procurement decisions by major brands and corporate sustainability reporting requirements.

Regional Market Insights

Australian Capital Territory and New South Wales together lead at 33.6% in 2025, anchored by Sydney's position as Australia's largest metropolitan market, the highest concentration of waste collection contracts, and strong alignment with NSW Waste and Sustainable Materials Strategy targets. Canberra's policy leadership in zero-waste objectives further reinforces the region's scale.

Victoria and Tasmania at 24.5% hold the second-largest share, anchored by Melbourne's metropolitan scale, Victoria's 72% landfill diversion target by 2025, and the 50% reduction in organic waste sent to landfill goal.

|

Region |

Share (2025) |

Key Growth Drivers |

|

ACT & New South Wales |

33.6% |

Sydney metropolitan scale; NSW Waste and Sustainable Materials Strategy; highest concentration of waste collection contracts; ACT zero-waste policy leadership |

|

Victoria & Tasmania |

24.5% |

Melbourne metropolitan market; Victoria 72% landfill diversion target by 2025; 50% organic waste reduction; Tasmania container deposit scheme; resource recovery investment |

|

Queensland |

17.8% |

Brisbane and SEQ growth corridor; 55–65% MSW and C&I recycling targets; waste levy reform; large industrial and mining waste base |

|

Western Australia |

13.2% |

70% waste recovery target by 2025; Kwinana Energy Recovery Facility operational; Perth metropolitan growth; mining sector industrial waste |

|

Northern Territory & South Australia |

10.9% |

70–80% landfill diversion targets in SA; container deposit scheme heritage; Northern Territory regional infrastructure development |

Queensland at 17.8% reflects Brisbane's growth corridor and 55–65% recycling rate targets, while Western Australia at 13.2% benefits from the Kwinana Energy Recovery Facility operational milestone and 70% waste recovery objective. The Northern Territory and South Australia together at 10.9% draw on SA's container deposit scheme heritage and 70–80% landfill diversion targets.

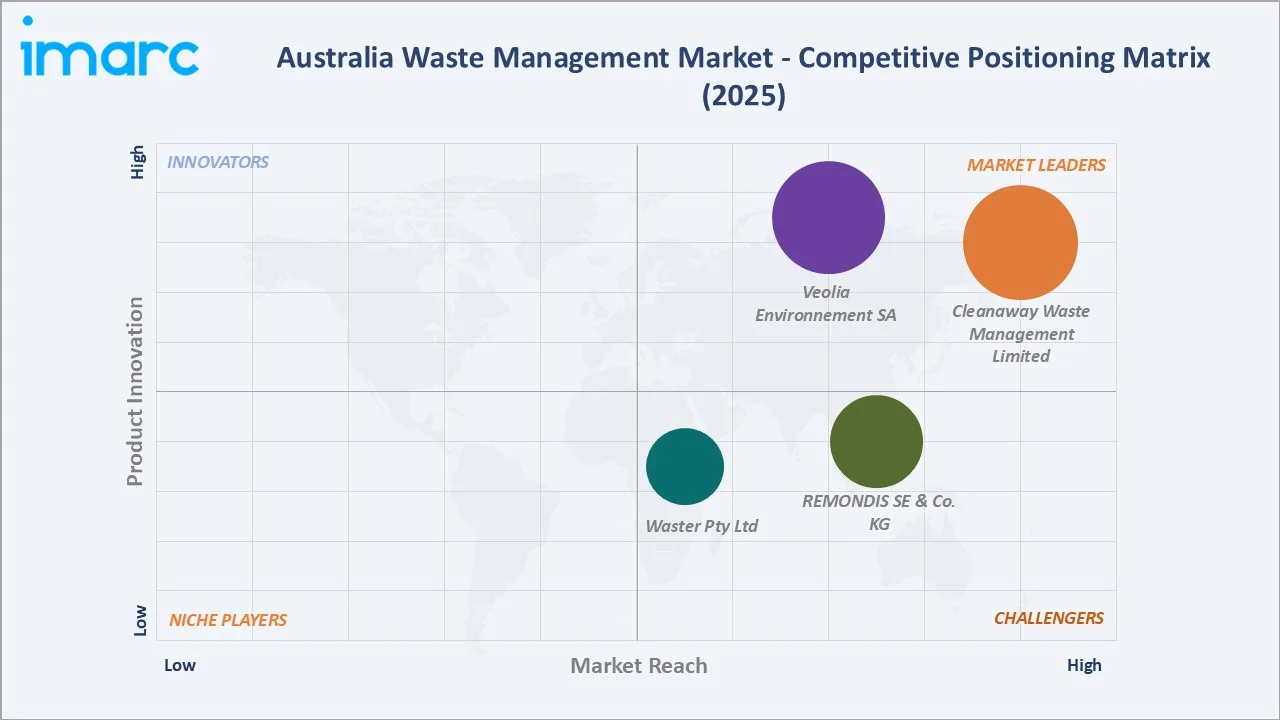

Competitive Landscape

Australia's waste management market is moderately consolidated. Leading players include Cleanaway Waste Management Limited, Veolia Environnement SA, REMONDIS SE & Co. KG, and Waster Pty Ltd.

|

Company Name |

Services |

Market Position |

Core Strength |

|

Cleanaway Waste Management Limited |

Health services, industrial services, liquid waste, oils, organics, grease trap, product destruction, waste audit, general waste, recycling, and skips and construction |

Market Leader |

Largest national waste management operator; integrated collection, processing, and landfill capability; large defense and infrastructure contracts |

|

Veolia Environnement SA |

Waste Collection & Sorting, Waste-to-energy, recovering materials from waste, industrial waste management, treatment and recovery of hazardous and special waste |

Market Leader |

Global environmental services scale; Kwinana waste-to-energy O&M; technology-led services |

|

REMONDIS SE & Co. KG |

Collections, recycling, processing and treatment, industrial services, and managed services |

Strong Challenger |

Family-owned global waste services scale; strategic acquisitions across collection, recycling, and landfill assets |

|

Waster Pty Ltd |

General waste bins, cardboard & paper recycling, medical waste disposal, organic food waste, sanitary & nappy bins, skip bins. |

Challenger |

Established business operations, offer transparency & flexibility |

The competitive structure reflects a balance between listed national operators, multinationals, family-owned regional specialists, and emerging waste-to-energy joint ventures.

Key Company Profiles

Cleanaway Waste Management Limited

Cleanaway Waste Management Limited is Australia's largest national waste management operator with an integrated collection, processing, landfill, liquids, and resource recovery footprint across all states and territories. Cleanaway holds the leading national market position by revenue and operates a comprehensive solid-waste, liquids and industrials, and health-services portfolio.

- Product Portfolio: Solid waste services including kerbside collection, commercial collection, transfer stations, landfills, organics, and MRFs; liquids and industrials including hazardous waste treatment, decontamination, and tank cleaning; health services and medical waste.

- Recent Developments: In October 2025, Cleanaway Waste Management Limited entered a long-term agreement with ACCIONA to supply waste feedstock to the Kwinana Energy Recovery Facility in Western Australia.

- Strategic Focus: National scale across all waste streams; expansion into technical services and complex waste decontamination; circular-economy investment in advanced soft plastics recycling; defense and infrastructure contract growth.

Veolia Environnement SA

Veolia Environnement SA is a global environmental services leader with substantial Australian operations spanning waste collection, processing, hazardous waste treatment, waste-to-energy, and refuse-derived fuel production.

- Product Portfolio: Waste collection and processing, hazardous waste treatment, waste-to-energy operations and maintenance, refuse-derived fuel production, liquid and industrial waste services.

- Recent Developments: In September 2025, Veolia Environnement SA installed Australia’s first AI-powered robot arm at its Bibra Lake Resource Recovery Park in Western Australia to improve plastic sorting.

- Strategic Focus: Waste-to-energy infrastructure leadership; industrial decarbonization through refuse-derived fuel; integrated environmental services across all states; technology-led process services and circular-economy capability.

Market Concentration Analysis

Australia's waste management market is moderately consolidated. The top players, Cleanaway Waste Management Limited, Veolia Environnement SA, REMONDIS SE & Co. KG, and Waster Pty Ltd, collectively hold a substantial revenue share, with Veolia widely cited as the leader in waste treatment and disposal services.

Bingo Industries Limited’s AUD 2.6 Billion acquisition by Macquarie Infrastructure and Real Assets' (MIRA), REMONDIS' acquisition of selected Veolia and SUEZ divestiture assets following ACCC requirements, and Cleanaway Waste Management Limited’s planned acquisition of Contract Resources Group illustrate continued consolidation. The market retains a long tail of family-owned regional specialists alongside listed and multinational operators.

Investment & Growth Opportunities

Fastest Growing Segments

- Industrial waste services are projected to grow at approximately 5.3% CAGR through 2034, supported by refuse-derived fuel contracts, mining and resources sector activity, and industrial decarbonization initiatives.

- Collection services at approximately 5.1% CAGR remain the dominant growth driver, fueled by urbanization, container deposit scheme expansion, and FOGO kerbside rollout across metropolitan local government areas.

Emerging Market Expansion

- Waste-to-energy infrastructure expansion presents the largest single-project opportunity, with further facilities in development across New South Wales and Victoria following the Kwinana operational milestone.

- Advanced soft plastics recycling, organics composting, and FOGO infrastructure expansion offer multi-year capital deployment opportunities aligned with binding state-level diversion targets.

M&A and Institutional Investment Trends

- Macquarie Infrastructure and Real Assets' AUD 2.6 Billion acquisition of Bingo Industries Limited exemplifies institutional capital appetite for Australian waste infrastructure assets.

- Cleanaway's March 2025 announcement to acquire Contract Resources Group, and REMONDIS' acquisition of selected Veolia/SUEZ divested assets, demonstrate continued strategic consolidation across the value chain.

- Long-term operations and maintenance contracts for waste-to-energy facilities, refuse-derived fuel offtake agreements, and defense and government waste contracts represent stable, infrastructure-style cash flow opportunities.

Future Market Outlook (2026-2034)

Australia's waste management market is positioned for sustained, regulation-led expansion through 2034. From USD 3.55 Billion in 2025, the market is projected to reach USD 5.47 Billion by 2034, representing incremental value of approximately USD 1.92 Billion at a 4.77% CAGR, increasingly composed of waste-to-energy operations, advanced recycling, organics treatment, and integrated resource recovery services.

Collection services will retain segment leadership above 55.0% of revenue through 2034, while disposal services gain share as waste-to-energy and advanced recycling infrastructure scales. Industrial waste will remain the largest source segment, with residential and commercial growth tied to urbanization.

Research Methodology

Primary Research

Primary research included structured interviews with over 100 industry participants in 2024–2025, comprising Australian waste management operator executives, state environmental regulators, council waste managers, industrial waste customers, container deposit scheme operators, and recycling industry association representatives, validating market sizing, segmentation, regional shares, and policy-driven adoption patterns.

Secondary Research

Secondary research covered the Department of Climate Change, Energy, the Environment and Water publications, National Waste Reports, state environmental protection authority data, ACCC merger decisions, ASX-listed operator annual reports, Australian Bureau of Statistics waste statistics, and industry coverage from Waste Management and Resource Recovery Association of Australia (WMRR).

Forecasting Models

Market size estimations used combined top-down and bottom-up forecasting, incorporating state-level waste volumes by stream, landfill levy bands, container deposit scheme recovery rates, FOGO rollout penetration, waste-to-energy project pipelines, and operator revenue disclosures. The 4.77% CAGR reflects validation against announced infrastructure investments, state diversion targets, and contract pipelines through 2034.

Australia Waste Management Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Waste Types Covered | Municipal Solid Waste, E-Waste, Hazardous Waste, Medical Waste, Construction and Demolition Waste, Industrial Waste |

| Services Covered | Collection, Disposal |

| Sources Covered | Industrial, Residential, Commercial |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Cleanaway Waste Management Limited, Veolia Environnement SA, REMONDIS SE & Co. KG, Waster Pty Ltd, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia waste management market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia waste management market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia waste management industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Waste Management Market Report

The Australia waste management market reached USD 3.55 Billion in 2025 and is projected to reach USD 5.47 Billion by 2034.

The market is expected to grow at a CAGR of 4.77% during 2026-2034, driven by National Waste Policy targets, waste-to-energy infrastructure expansion, container deposit scheme growth, and urbanization-led C&D waste volumes.

Australian Capital Territory and New South Wales together lead with a 33.6% share in 2025, anchored by Sydney's metropolitan scale and the NSW Waste and Sustainable Materials Strategy.

Collection services dominate with a 57.6% share in 2025, reflecting demand for kerbside pickup, skip bin services, industrial collection, and commercial waste removal nationwide.

Industrial waste leads at 38.5%, supported by mining, manufacturing, and construction and demolition activity across Australia.

Key players include Cleanaway Waste Management Limited, Veolia Environnement SA, REMONDIS SE & Co. KG, and Waster Pty Ltd.

Industrial waste is growing at approximately 5.3% CAGR through 2034 due to refuse-derived fuel offtake agreements with cement and lime producers, mining sector activity, and broader industrial decarbonization contracts.

Key challenges include high operating costs and landfill levies, infrastructure and processing capacity gaps, geographic distances to processing hubs, regulatory complexity across states, and workforce and heavy-vehicle capacity constraints.

Waste-to-energy infrastructure expansion, advanced soft plastics recycling, organics treatment and FOGO infrastructure, defense and government waste contracts, and M&A consolidation across the value chain represent the highest-growth investment opportunities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)