Australia Waste Plastic Recycling Market Size, Share, Trends and Forecast by Treatment, Material, Application, Recycling Process, and Region, 2026-2034

Australia Waste Plastic Recycling Market Size and Share:

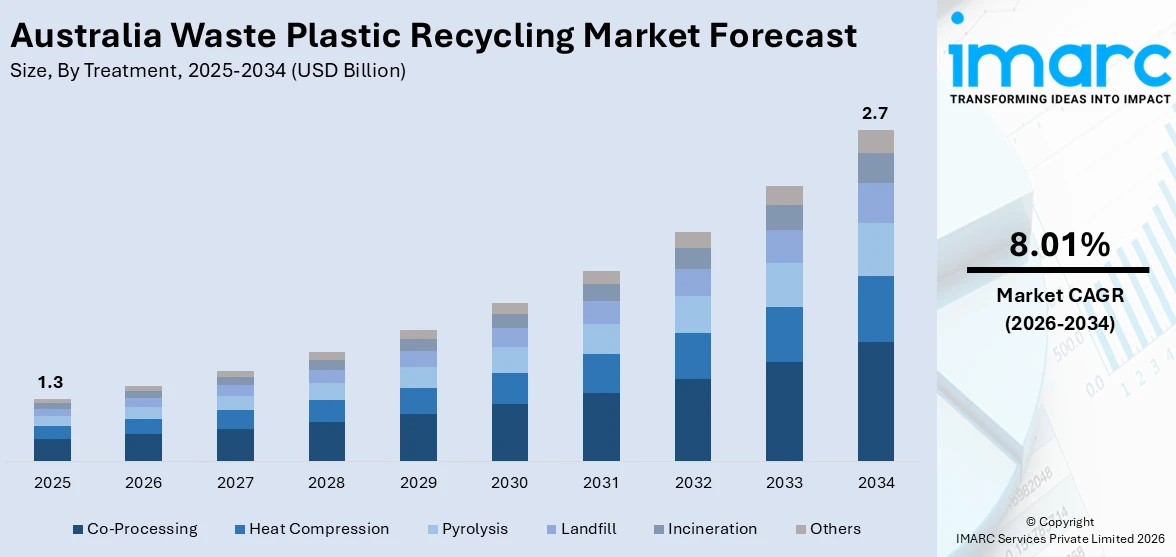

The Australia waste plastic recycling market size reached USD 1.3 Billion in 2025. Looking forward, the market is expected to reach USD 2.7 Billion by 2034, exhibiting a growth rate (CAGR) of 8.01% during 2026-2034. The market is driven by heightening environmental awareness, policy actions, and country-level sustainability targets, leading to better recycling infrastructure and better management of plastic wastes in the nation.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 1.3 Billion |

| Market Forecast in 2034 | USD 2.7 Billion |

| Market Growth Rate 2026-2034 | 8.01% |

Key Trends of Australia Waste Plastic Recycling Market:

Growing Use of Highly Advanced Mechanical Recycling Methods

Australia is witnessing a notable shift toward the adoption of advanced mechanical recycling technologies as part of its efforts to address plastic waste in a more environmentally sustainable manner. While mechanical recycling remains the predominant method, recent technological advancements have significantly enhanced its efficiency and effectiveness in material recovery. The arrival of advanced sorting technologies, including near-infrared (NIR) sensors and automation powered by artificial intelligence (AI), has enabled plants to sort higher volumes of plastic materials with better accuracy. These machines lower contamination rates and yield quality recycles that can be used again in the domestic manufacturing value chain. The transformation is further elevated by elevated investment in infrastructure development and government-sponsored recycling programs aimed at bridging national sustainability goals. Australia plastic waste recycling market outlook predicts consistent growth, fueled by a mix of regulatory compulsion, technological advancements, and business need for high-quality recycled feedstock. This is consistent with overall action to move toward a circular economy and mitigate ecosystem damage.

To get more information on this market Request Sample

Post-Consumer Recycled Plastics Usage in Packaging Applications Increases

There has been an increasing trend in Australia's recycling market toward the use of post-consumer recycled (PCR) plastics, especially within the packaging segment. Spurred by environmental issues and government mandates, producers are adding higher amounts of recycled material to packaging materials, particularly for food, beverage, and household products. This is creating increased demand for high-quality recycled polymers, which is stimulating the creation of localized supply chains that can deliver consistent, contamination-free material. Recycling plants are, in turn, upgrading their equipment to create packaging-grade PCR plastics that are safe and healthy. For instance, in December 2023, Victoria opened its biggest PET plastic bottle recycling factory in Melbourne. The $50 million plant can recycle as many as one billion PET bottles every year, playing a major role in the state's Container Deposit Scheme and furthering recycling efforts. Moreover, consumer behavior is moving towards eco-friendly brands, putting increased pressure on sectors to change. Australia waste plastic recycling market share is growing as the packaging sector is a primary driver of demand, facilitating market stability and material circulation. The trend indicates the nation's support for sustainable production processes and demonstrates a changing attitude among producers and consumers towards circular packaging options.

Government-Inspired Circular Economy Strategies and Recycling Requirements

Australia's recycling industry is increasingly being defined by national and state policies aimed at steering the economy toward a circular approach. Government programs, such as recycling requirements, landfill prohibition, and extended producer responsibility (EPR) systems, are playing a tremendous role in guiding waste plastic management processes. For instance, in October 2023, the Plasrefine plastic recycling facility in Moss Vale, NSW, went ahead amid community protest, with intentions to recycle as much as 120,000 tonnes of plastic a year, fulfilling Australia's plastic recycling requirements. Furthermore, these policies are promoting investments in recycling facilities and enhancing public-private partnership cooperation. Specifically, the rollout of national goals for recycled content in products and packaging is convincing industries to embrace recycled material on a large scale. Government incentives programs are further facilitating innovation in sorting, processing, and re-manufacturing, hence augmenting the overall capacity of the sector. Implementation of standard recycling labeling and unified collection systems is enhancing material stream quality, thus further promoting recycling efficiency. Australia plastic recycling market growth of waste is being driven substantially by these policy initiatives, which are making recycling businesses more predictable and supportive and allowing a long-term transition to sustainable waste management solutions.

Growth Drivers of Australia Waste Plastic Recycling Market:

Rising Consumer and Corporate Sustainability Awareness

Environmental awareness is becoming increasingly widespread among Australian consumers, leading to heightened expectations for sustainable products and packaging. Consumers are more ready to patronize those brands that show green credentials, and a business is compelled to engage in recycled plastics in their products. To this effect, the operations of many corporations are related to the environmental, social, and governance (ESG) targets to stay competitive and socially responsible. This change not only promotes proper waste treatment but also contributes to a stable demand for recycles. The increased focus on sustainability is critical in supporting efforts to recycle plastics in the country, with both individuals and entities supporting the creation of a circular economy, and the minimization of the adverse effects plastic waste has on the environment.

Technological Integration in Waste Collection and Sorting

Australia is witnessing a steady integration of smart technologies into its waste management systems. Innovations such as AI-powered sorting equipment, IoT-enabled collection bins, and RFID tracking solutions are revolutionizing how waste is monitored and processed. These advancements enhance traceability and purity of plastic waste streams, making recycling more efficient and cost-effective, which is boosting the Australia waste plastic recycling market demand. Improved automation also helps reduce contamination rates and labor dependence, allowing recyclers to produce high-quality secondary plastic materials suitable for diverse applications. As these technologies become more accessible and scalable, they are expected to significantly boost recycling outcomes across the country. This tech-driven evolution is essential for achieving long-term sustainability goals and supporting the market growth of recycled plastics.

Localized Recycling Infrastructure Expansion

Australia has made significant progress in decentralizing its recycling system by investing in regional and state-level facilities. By developing localized recycling hubs, the country is reducing its reliance on overseas processing and managing waste more efficiently within its borders. These facilities lower logistics costs and carbon emissions associated with long-distance transportation, while also creating job opportunities and economic activity in local areas. Additionally, enhanced infrastructure ensures better handling of plastic waste volumes and enables quicker, more flexible responses to regional waste management demands. This localized approach not only boosts processing capacity but also improves the overall efficiency and sustainability of Australia’s waste plastic recycling network.

Opportunities of Australia Waste Plastic Recycling Market:

Emergence of Chemical Recycling Innovations

Chemical recycling technologies are gaining momentum in Australia as a complementary solution to traditional mechanical recycling methods. Techniques such as pyrolysis and depolymerization allow for the breakdown of complex or contaminated plastic waste into their original monomers or fuels, creating outputs that can match the quality of virgin plastics. These methods significantly expand the types of plastics that can be effectively recycled, including multilayer packaging and hard-to-sort waste. The scalability of chemical recycling is drawing interest from major chemical manufacturers, energy firms, and sustainability-focused investors looking to capitalize on circular production models. With growing technological maturity, chemical recycling is expected to play a critical role in closing the loop on plastic waste management in Australia.

Industrial Partnerships and Vertical Integration

Australia's waste plastic recycling sector is seeing an increasing number of strategic partnerships among stakeholders across the value chain, including raw material suppliers, product manufacturers, retailers, and recyclers. According to the Australia waste plastic recycling market analysis, these collaborations enable better coordination and alignment in the collection, processing, and reuse of recycled plastics. By vertically integrating operations, companies can secure stable supplies of recycled feedstock while reducing costs and operational risks. Such partnerships encourage investment in recycling facilities, innovation, and supply chain resilience. This cooperative model enhances transparency and traceability in material flows, making it easier to meet environmental compliance standards. In the long term, vertical integration supports the development of closed-loop systems that are essential for achieving sustainable and circular plastic economies.

Export Market Potential for Recycled Resin

As Australia boosts its recycling efficiency and output, the potential to export high-quality recycled plastic resins is becoming a significant market opportunity. Countries across the Asia-Pacific region, many of which face recycling infrastructure limitations, are actively seeking reliable sources of sustainable materials. Australian recycled resin—produced under strict environmental and quality standards—has the potential to meet this growing demand. By developing international trade relationships in the recycling sector, Australia can enhance its role in the global circular economy while supporting regional sustainability efforts. This export-oriented growth also provides domestic recyclers with a broader customer base, reducing dependency on local demand cycles and encouraging continuous improvements in processing capabilities and material quality.

Challenges of Australia Waste Plastic Recycling Market:

Contamination and Material Sorting Complexities

One of the persistent challenges in Australia’s waste plastic recycling market is contamination caused by poor waste segregation at the source. Despite public awareness campaigns, many households and businesses continue to dispose of recyclables incorrectly, leading to mixed or soiled waste streams. This contamination reduces the efficiency of recycling operations, increases processing costs, and often results in lower-quality recycled output. Moreover, heavily contaminated plastics may become non-recyclable and end up in landfills, defeating the purpose of collection programs. Sorting complexities are especially problematic in residential and commercial sectors where diverse materials are disposed of together. Addressing this issue requires improved education, stricter sorting regulations, and investments in smarter, automated sorting systems.

Economic Viability and Market Volatility

Recycling plastic in Australia continues to face financial hurdles due to unstable market dynamics and high operating costs. Recycled plastics often struggle to compete with virgin plastic, especially when oil prices are low, making new plastic cheaper to produce. Without consistent demand from end-users and strong financial incentives, many recycling businesses find it difficult to achieve profitability. Additionally, rising energy and labor costs contribute to the financial strain. In the absence of robust procurement policies or long-term purchasing commitments from manufacturers, recyclers face uncertainty in revenue streams. To overcome these barriers, more comprehensive support is needed, including subsidies, tax breaks, and guaranteed market access for recycled content across key industries.

Limited Standardization and End-Market Certainty

A major bottleneck in Australia’s recycling sector is the lack of standardized guidelines for recycled plastic quality, composition, and permitted applications. Without uniform national standards, manufacturers are hesitant to incorporate recycled content into their products due to concerns over performance, safety, and regulatory compliance. This lack of clarity discourages investment in new recycling technologies and infrastructure. Furthermore, the absence of long-term purchase agreements or guaranteed offtake markets for recycled plastics adds to industry uncertainty. Recyclers often struggle to secure reliable buyers, which affects capacity planning and scalability. Establishing clear standards and fostering predictable demand through public procurement or industry mandates would help build confidence in recycled materials and stabilize market growth.

Australia Waste Plastic Recycling Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the region level for 2026-2034. Our report has categorized the market based on treatment, material, application, and recycling process.

Treatment Insights:

- Co-Processing

- Heat Compression

- Pyrolysis

- Landfill

- Incineration

- Others

The report has provided a detailed breakup and analysis of the market based on the treatment. This includes co-processing, heat compression, pyrolysis, landfill, incineration, and others.

Material Insights:

- Poly Vinyl Chloride (PVC)

- Low-Density Polyethylene (LDPE)

- High-Density Polyethylene (HDPE)

- Polyethylene Terephthalate (PET)

- Polypropylene (PP)

- Acrylonitrile Butadiene Styrene (ABS)

- Others

A detailed breakup and analysis of the market based on the material have also been provided in the report. This includes poly vinyl chloride (PVC), low-density polyethylene (LDPE), high-density polyethylene (HDPE), polyethylene terephthalate (PET), polypropylene (PP), acrylonitrile butadiene styrene (ABS), and others.

Application Insights:

Access the comprehensive market breakdown Request Sample

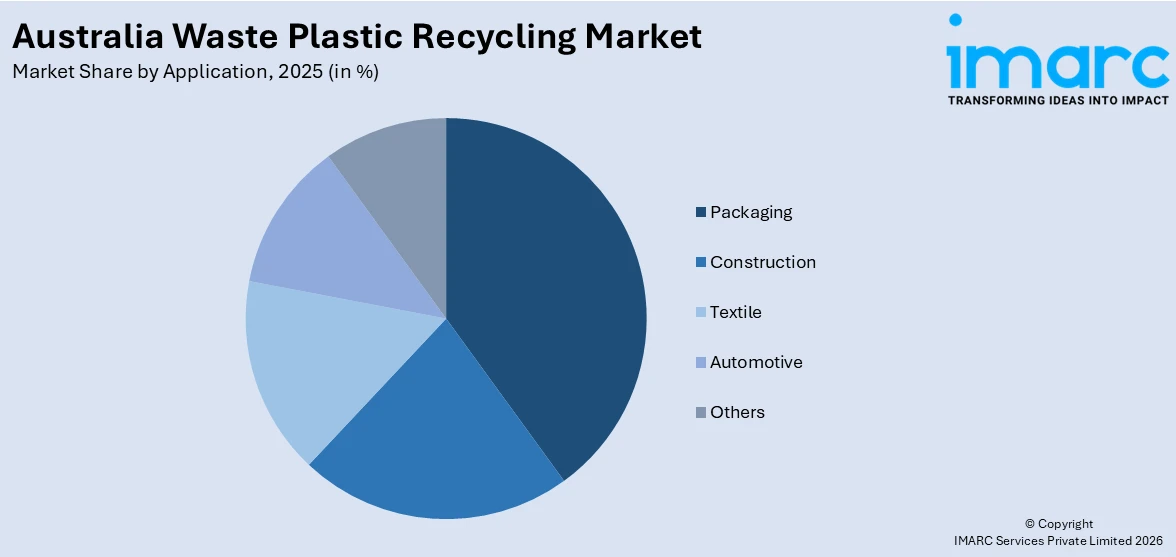

- Packaging

- Construction

- Textile

- Automotive

- Others

The report has provided a detailed breakup and analysis of the market based on the application. This includes packaging, construction, textile, automotive, and others.

Recycling Process Insights:

- Mechanical

- Others

A detailed breakup and analysis of the market based on the recycling process have also been provided in the report. This includes mechanical and others.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Waste Plastic Recycling Market News:

- In July 2024, Recycling Plastics Australia received $20 million in federal funding to build a soft plastics recycling centre at its Kilburn site. The project, under the Recycling Modernisation Fund, will keep 14,000 tonnes of soft plastics out of landfill each year, increasing the company's recycling capacity and infrastructure.

- In June 2024, Brightmark, a top waste solutions company, made the announcement of opening Australia's first next-generation plastic renewal facility in Parkes, New South Wales. The A$260 million plant will use pyrolysis technology to recycle 200,000 tons of plastic waste each year and play an important role in expanding Australia's waste plastic recycling market.

Australia Waste Plastic Recycling Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Treatments Covered | Co-Processing, Heat Compression, Pyrolysis, Landfill, Incineration, Others |

| Materials Covered | Poly Vinyl Chloride (PVC), Low-Density Polyethylene (LDPE), High-Density Polyethylene (HDPE), Polyethylene Terephthalate (PET), Polypropylene (PP), Acrylonitrile Butadiene Styrene (ABS), Others |

| Applications Covered | Packaging, Construction, Textile, Automotive, Others |

| Recycling Processes Covered | Mechanical, Others |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia waste plastic recycling market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia waste plastic recycling market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia waste plastic recycling industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Australia Waste Plastic Recycling Market Report

The waste plastic recycling market in Australia was valued at USD 1.3 Billion in 2025.

The Australia waste plastic recycling market is projected to exhibit a CAGR of 8.01% during 2026-2034.

The Australia waste plastic recycling market is projected to reach a value of USD 2.7 Billion by 2034.

The market is driven by stringent regulations on single-use plastics, rising environmental awareness, and increasing investment in recycling infrastructure. Demand from breakfast product manufacturers for eco-friendly packaging, coupled with innovations in plastic sorting and reprocessing, is encouraging large-scale adoption of recycled materials across the food and beverage supply chain.

Australia is witnessing a shift toward advanced recycling technologies, such as AI-enabled sorting and chemical recycling. Growing emphasis on circular packaging solutions in the breakfast segment, government-led sustainability mandates and retailer commitments to reduce virgin plastic use are also shaping market dynamics and long-term processing capabilities.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)