Australia Wine Market Size, Share, Trends and Forecast by Product Type, Color, Distribution Channel, and Region, 2026-2034

Australia Wine Market Summary:

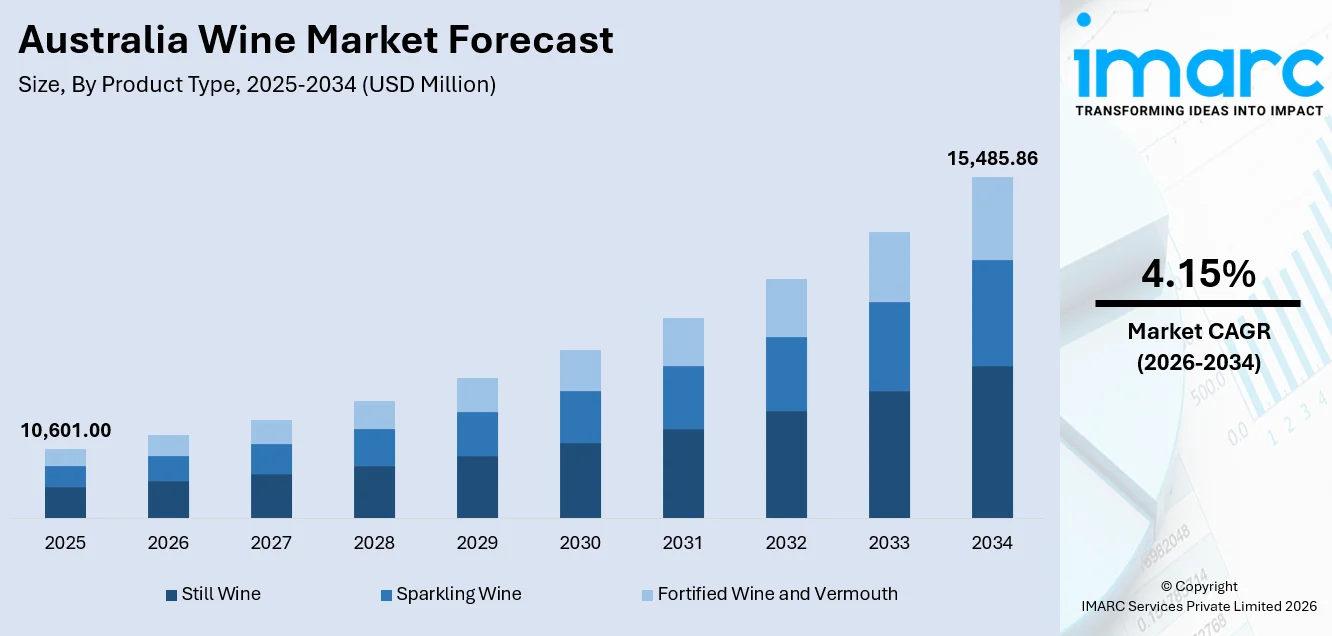

The Australia wine market size was valued at USD 10,601.00 Million in 2025 and is projected to reach USD 15,485.86 Million by 2034, growing at a compound annual growth rate of 4.15% from 2026-2034.

The Australia wine market is experiencing steady expansion driven by premiumization trends, growing consumer preference for sustainably produced wines, and strengthening export channels across key international markets. Increasing wine tourism activity, rising demand for diverse varietals, and innovative packaging formats are reshaping consumption patterns. Advancements in precision viticulture and evolving regional specialization further contribute to long-term value creation within the domestic wine industry.

Key Takeaways and Insights:

- By Product Type: Still wine dominates the market with a share of 74.5% in 2025, owing to its deep-rooted cultural significance in Australian dining, widespread availability across retail and hospitality channels, and strong export demand for premium still wine varietals from established wine regions.

- By Color: Red wine leads the market with a share of 44.5% in 2025, driven by enduring consumer preference for iconic Australian red varietals such as Shiraz and Cabernet Sauvignon, reinforced by strong brand recognition in international markets and favorable growing conditions.

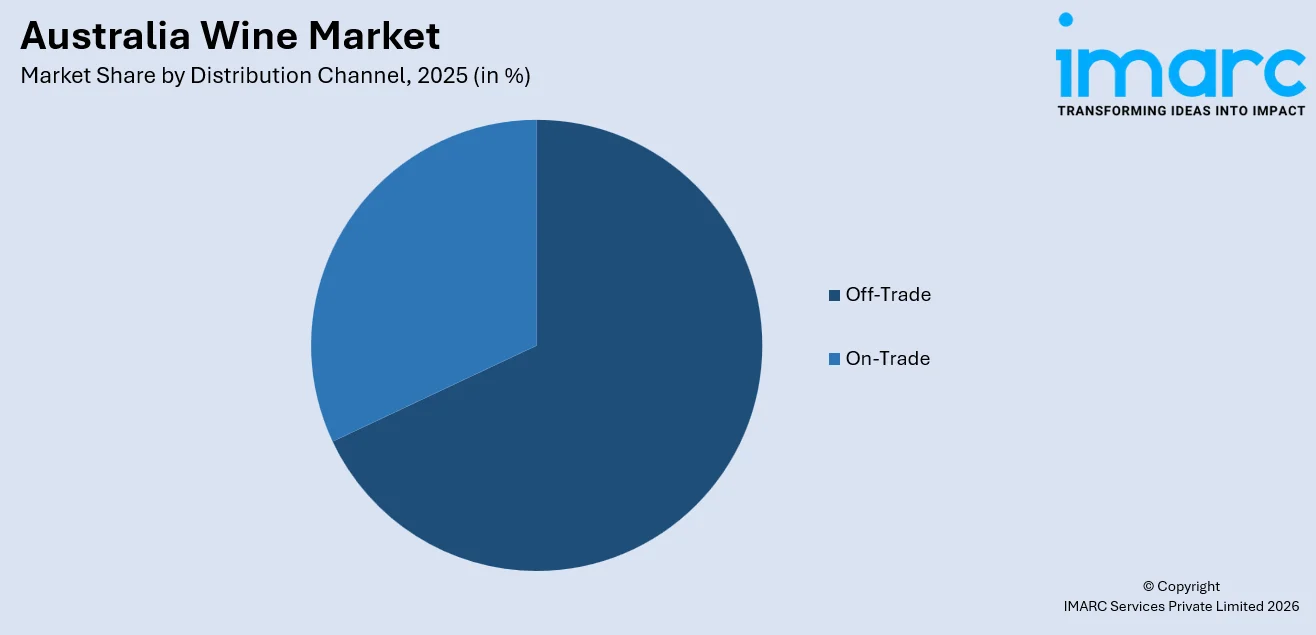

- By Distribution Channel: Off-trade holds the largest segment with a share of 68.5% in 2025, reflecting the dominance of supermarket chains and specialty liquor retailers in Australian wine purchasing, supported by growing online wine sales and convenient home delivery services.

- By Region: Australia Capital Territory & New South Wales represents the largest region with a share of 28.5% in 2025, driven by the concentration of Australia’s largest consumer base in Sydney, a thriving wine tourism ecosystem anchored by the Hunter Valley, and strong retail and hospitality infrastructure.

- Key Players: Key players drive the Australia wine market by investing in premium brand portfolios, expanding sustainable viticulture practices, strengthening export distribution networks, and leveraging wine tourism to deepen consumer engagement and strengthen brand loyalty across domestic and international markets. Some of the key players operating in the industry are Australian Vintage Limited, Casella, Kingston Estate Wines, Meditrina Beverages, The Australian Wine Company, The Little Wine Company, Treasury Wine Estates Ltd. and Vinarchy.

The Australia wine industry is moving forward as wineries and grape growers begin to focus on premiumization, sustainability, and export diversification in response to changing global consumption trends. The industry is capitalizing on its long-standing reputation for producing high-quality, regionally distinctive wines to drive value creation in both the local and global markets. Wineries are increasingly turning to organic and biodynamic viticulture, with the best wineries seeking formal sustainability certification as a reflection of the industry’s overall commitment to environmentally responsible wine production. With cellar door experiences, vineyard tours, and culinary partnerships fostering direct-to-consumer interaction and economic growth in strategic wine regions, wine tourism has emerged as a significant economic driver. The recent reopening of key export markets is giving the industry a boost, while premiumization initiatives continue to allow wineries to command higher price points and build strong brand equity. Innovation in packaging, e-commerce, and experiential marketing is also expanding consumer accessibility and attracting younger consumers to the category, setting the stage for long-term value creation in the growing Australia wine market share.

Australia Wine Market Trends:

Premiumization and shift toward quality-driven consumption

Australian wine consumers are increasingly gravitating toward premium and super-premium products, favoring quality over quantity as overall per capita wine consumption moderates. Producers are responding by investing in terroir-driven expressions, single-vineyard offerings, and limited-release collections that command higher price points. In August 2025, Treasury Wine Estates reported a 16% rise in annual underlying profit to AUD 470.6 Million, driven primarily by strong demand for its flagship Penfolds luxury portfolio, underscoring the growth potential within the premium segment of the Australia wine market growth.

Sustainability and organic wine production gaining traction

The Australian wine industry is witnessing a transformative shift toward environmentally responsible production methods, with wineries increasingly pursuing organic, biodynamic, and sustainable certifications to align with evolving consumer values. The Sustainable Winegrowing Australia program, administered by the Australian Wine Research Institute, had enrolled 1,844 members representing 99,500 hectares of vineyards by late 2024. Health-conscious consumers are driving demand for organic wines with lower sulfite levels and transparent production processes, prompting wineries across the Hunter Valley, Barossa Valley, and McLaren Vale to expand their sustainable portfolios.

Evolution of regional varietals and diversified wine styles

Australian winemakers are broadening their varietal portfolios beyond traditional Shiraz and Cabernet Sauvignon, embracing alternative grape varieties and lighter wine styles that resonate with modern palates. Wine Australia’s National Vintage Report for 2024 revealed that Chardonnay surpassed Shiraz as the most-crushed variety nationally for the first time in a decade, with 332,643 tonnes of Chardonnay grapes processed. This shift reflects growing consumer interest in white wines, rosé, and sparkling varieties, as well as the emergence of Mediterranean-climate varietals that perform well in Australian terroirs.

Market Outlook 2026-2034:

The Australian wine industry is poised for growth as wineries leverage the opportunities presented by premiumization, wine tourism, and the revival of export markets. The re-establishment of major international trade routes is giving the country’s exports a much-needed boost, allowing wineries to re-establish business ties and increase their presence in premium markets. At the same time, the local market is also undergoing development as younger generations of wine drinkers discover new varieties of wine, lighter styles, and eco-friendly labels. New packaging trends, such as canned wines and mini bottles, are making wine more accessible to new markets. Wine tourism also remains an important driver of growth as wine tourism experiences, wine and food pairings, and events continue to develop regional economies and help wineries establish direct consumer ties. Premiumization initiatives are also allowing wineries to charge higher prices and build brand equity in both local and international markets. The market generated a revenue of USD 10,601.00 Million in 2025 and is projected to reach a revenue of USD 15,485.86 Million by 2034, growing at a compound annual growth rate of 4.15% from 2026-2034.

Australia Wine Market Report Segmentation:

|

Segment Category |

Leading Segment |

Market Share |

|

Product Type |

Still Wine |

74.5% |

|

Color |

Red Wine |

44.5% |

|

Distribution Channel |

Off-Trade |

68.5% |

|

Region |

Australia Capital Territory & New South Wales |

28.5% |

Product Type Insights:

- Still Wine

- Sparkling Wine

- Fortified Wine and Vermouth

Still wine dominates with a market share of 74.5% of the total Australia wine market in 2025.

The still wine market continues to hold a leading market position in the Australian market, thanks to the rich wine culture and the international recognition of the key varieties of wines produced in the premium regions of the country. The Australians have a strong preference for home-produced still wines, with imported still wines contributing about one-fifth of the total still wine consumption in the country. The off-trade channel is the major distribution channel for the sale of still wines.

The export performance of Australian still wine has shown significant momentum, with still red wine export volumes increasing by 16% to 356 Million Liters according to Wine Australia, driven substantially by the reopening of trade with mainland China. Producers are also responding to changing consumer palates by expanding their still wine portfolios to include lighter-bodied whites, aromatic varietals, and region-specific expressions that emphasize terroir-driven quality and appeal to both traditional enthusiasts and new generation wine consumers.

Color Insights:

- Red Wine

- Rose Wine

- White Wine

Red wine leads with a share of 44.5% of the total Australia wine market in 2025.

Red wine retains the largest share by color in the Australia wine market, underpinned by the enduring popularity of signature Australian red varietals including Shiraz, Cabernet Sauvignon, and Merlot. The Barossa Valley, McLaren Vale, and Coonawarra remain premier sources for internationally acclaimed red wines, benefiting from optimal growing conditions and decades of winemaking expertise. Red wine also dominates Australia's export mix, reflecting strong international demand for premium Australian reds.

Despite evolving consumer preferences toward lighter wine styles, red wine continues to benefit from strong brand loyalty and cultural associations with Australian culinary traditions. Shiraz remains the most-planted red variety nationally, reinforcing its position as the country's flagship grape. However, producers are adapting red wine styles toward more elegant, lighter-bodied expressions with greater emphasis on regional character, reflecting the broader industry shift toward terroir-focused winemaking and sustainable production methods.

Distribution Channel Insights:

Access the comprehensive market breakdown Request Sample

- Off-Trade

- Supermarkets and Hypermarkets

- Specialty Stores

- Online Stores

- Others

- On-Trade

Off-trade represents the largest segment with a 68.5% share of the total Australia wine market in 2025.

The off-trade market continues to lead the market in Australia, thanks to the large retail presence of key players such as Dan Murphy’s and BWS, which fall under the Endeavour Group. Supermarkets and hypermarkets act as the main purchasing points for consumers who purchase wine for daily consumption. This is supplemented by wine specialty stores, which target consumers who are looking for premium wine and are willing to pay for the expertise of the wine connoisseurs who stock boutique wines. The trend of online wine shopping is also on the rise.

The off-trade segment benefits from Australia's well-established retail infrastructure and consumer purchasing habits that favor at-home wine consumption. The channel is supported by a mature ecosystem of supermarkets, specialty retailers, and emerging online platforms that collectively ensure broad product accessibility across diverse price points. Retailers are investing in digital loyalty programs, personalized recommendations, and subscription-based delivery models to strengthen customer retention and drive repeat purchases. These evolving strategies are enhancing consumer convenience and expanding the off-trade landscape nationwide.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

Australia Capital Territory & New South Wales holds the largest share with 28.5% of the total Australia wine market in 2025.

Australia Capital Territory and New South Wales commands the largest regional share of the wine market, driven by Sydney's position as the nation's most populous city and a major consumer hub for both premium and everyday wine categories. The Hunter Valley, located in New South Wales, is one of Australia's oldest and most celebrated wine regions, renowned for its distinctive Semillon and Shiraz varieties. The region's proximity to Sydney supports a thriving wine tourism ecosystem that generates significant direct-to-consumer revenue.

New South Wales is one of Australia's largest wine-producing states, encompassing diverse viticultural areas including the Riverina, Mudgee, Orange, and Cowra regions, each contributing distinct varietals and wine styles to the national portfolio. The concentration of hospitality venues, fine dining establishments, and cultural events across Sydney further strengthens on-trade wine demand and enhances consumer exposure to premium offerings. The state's well-developed retail and logistics infrastructure ensures efficient distribution across both metropolitan and regional markets, supporting sustained consumption growth.

Market Dynamics:

Growth Drivers:

Why is the Australia Wine Market Growing?

Expanding export opportunities and restored trade with China

The Australian wine market is currently undergoing a substantial growth momentum driven by the revival of international export routes, especially after the reinstatement of trade access to major Asian markets following the abolition of high tariffs on Australian bottled wine. The reinstatement of trade has opened the door to what was previously the most valuable single-country export market for Australia, allowing wine producers to re-establish trade ties and take advantage of the long-standing consumer preference for Australian premium red wines. The re-establishment of vital export routes has revitalized export volumes and values, re-establishing vital trade ties that had been severed for the past few years. Wine producers are taking advantage of established brand recognition and trade agreement advantages to facilitate re-entry into the market and make up for lost time. In addition to established markets, Australian wine exporters are embarking on diversification initiatives in Southeast Asia, South Korea, India, and other emerging markets, ensuring that the industry is not vulnerable to trade disruptions in the future while increasing the overall addressable market for Australian wine products.

Rising premiumization and consumer preference for quality wines

A fundamental structural shift toward premium and luxury wine consumption is driving sustained value growth across the Australia wine market. Consumers are increasingly prioritizing quality, provenance, and brand prestige over volume, supporting higher average price points and margin expansion for producers positioned in the premium segment. This trend is particularly evident in the performance of luxury-focused companies, where flagship brands are commanding significant revenue contributions and reinforcing the commercial viability of premium-oriented strategies. Premiumization is also accelerating innovation in single-vineyard bottlings, reserve-tier releases, and regionally distinctive expressions that command premium pricing. Cool-climate regions such as the Yarra Valley, Tasmania, and Adelaide Hills are gaining recognition for producing elegant, terroir-driven wines that appeal to discerning domestic and international consumers seeking authentic quality experiences beyond mass-market offerings.

Growth in wine tourism and direct-to-consumer engagement

Wine tourism has become a paradigm-shifting growth driver for the Australian wine sector, adding immense economic value to the traditional production and export chain. Wineries in the country are luring millions of tourists every year, and the resultant visitor spending is adding to the economic viability of the regions. The government's commitment to ensuring the continued growth of this economic driver through specific funding initiatives for wine tourism and cellar door projects further underlines the economic significance of the sector. Wine tourism helps in direct consumer interaction, and this allows wineries to create brand loyalty and tap into the premium segment through cellar door sales. The Barossa Valley, Hunter Valley, Margaret River, and Yarra Valley wine regions are working towards creating engaging experiences for tourists that include wine tastings, vineyard tours, culinary experiences, and accommodation, thus turning traditional wineries into hospitality destinations.

Market Restraints:

What Challenges the Australia Wine Market is Facing?

Persistent oversupply and declining per capita consumption

The Australian wine industry faces a structural oversupply challenge, with national wine production consistently exceeding sales volumes and pushing stock levels upward. Declining per capita alcohol consumption, driven by health and wellness concerns and cost-of-living pressures, is reducing domestic demand for wine. Global wine consumption continues to fall, limiting the ability of Australian producers to absorb excess inventory through export markets. This imbalance exerts downward pressure on grape prices and profitability, particularly for growers in warm inland irrigated regions producing commercial-grade wine.

Intensifying global competition and market fragmentation

Australian wine producers face heightened competition from established wine-producing nations including France, Italy, Chile, and Spain, as well as emerging producers who are expanding their presence in key export markets. During Australia’s absence from the Chinese market, competitors such as Chile and France strengthened their market positions, making recapturing lost share more challenging. Domestic market fragmentation across numerous small-scale producers adds complexity to distribution and marketing efforts, while rising production costs and currency fluctuations create additional competitive headwinds.

Climate change and environmental vulnerability

The Australian wine industry is increasingly exposed to climate change impacts, including rising temperatures, prolonged droughts, bushfire risks, and unpredictable weather events that threaten grape quality and vineyard productivity. Warmer conditions are altering ripening patterns and shifting the suitability of traditional grape varieties across established wine regions. Water scarcity remains a critical concern for irrigated growing areas, while extreme heat events can cause sunburn damage and accelerated sugar accumulation, reducing the quality of the resulting wines and undermining regional reputations.

Competitive Landscape:

The wine industry in Australia has a competitive environment that is marked by the coexistence of large-scale multinational companies and small boutique wineries. The large companies are engaged in consolidation and premiumization strategies in order to improve their market position. Innovation in sustainable production, packaging, and digital direct-to-consumer platforms is increasing competitiveness for consumer attention and loyalty. Strategic partnerships, acquisitions, and export diversification are changing the dynamics of the competition as companies aim to retain their market share in Australia while growing their exports in international markets.

Some of the key players operating in the industry include:

- Australian Vintage Limited

- Casella

- Kingston Estate Wines

- Meditrina Beverages

- The Australian Wine Company

- The Little Wine Company

- Treasury Wine Estates Ltd.

- Vinarchy

Recent Developments:

- In June 2025, the Victoria Racing Club announced a three-year partnership with De Bortoli Wines, appointing the family-owned winery as the official wine partner of the Melbourne Cup Carnival. The agreement positions De Bortoli’s premium portfolio, including King Valley Prosecco and Yarra Valley cool-climate Pinot Noir, across dining and hospitality settings at Flemington Racecourse.

- In April 2025, Vinarchy officially launched as a new global wine company following the merger of Accolade Wines with the Australian, New Zealand, and Spanish wine businesses formerly owned by Pernod Ricard. The newly formed entity, with annual net sales exceeding AUD 1.5 Billion and 11 wineries worldwide, positions itself as one of the largest dedicated wine companies globally.

Australia Wine Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Still Wine, Sparkling Wine, Fortified Wine and Vermouth |

| Colors Covered | Red Wine, Rose Wine, White Wine |

| Distribution Channels Covered |

|

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Companies Covered | Australian Vintage Limited, Casella, Kingston Estate Wines, Meditrina Beverages, The Australian Wine Company, The Little Wine Company, Treasury Wine Estates Ltd, Vinarchy, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Australia Wine Market Report

The Australia wine market size was valued at USD 10,601.00 Million in 2025.

The Australia wine market is expected to grow at a compound annual growth rate of 4.15% from 2026-2034 to reach USD 15,485.86 Million by 2034.

Still wine dominated the market with a share of 74.5%, driven by deep cultural significance in Australian dining traditions, widespread retail availability, strong export demand, and the global recognition of premium Australian still wine varietals.

Key factors driving the Australia wine market include expanding export opportunities following restored trade relations with China, rising premiumization trends, growing wine tourism activity, increasing consumer preference for sustainable wines, and innovation in packaging and distribution.

Major challenges include persistent oversupply and elevated inventory levels, declining per capita wine consumption, intensifying competition from global producers, climate change impacts on grape quality, rising production costs, and the need for ongoing market diversification.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)