Australia Workwear Market Size, Share, Trends and Forecast by Product, Application, Distribution Channel, End User, and Region, 2026-2034

Australia Workwear Market Overview:

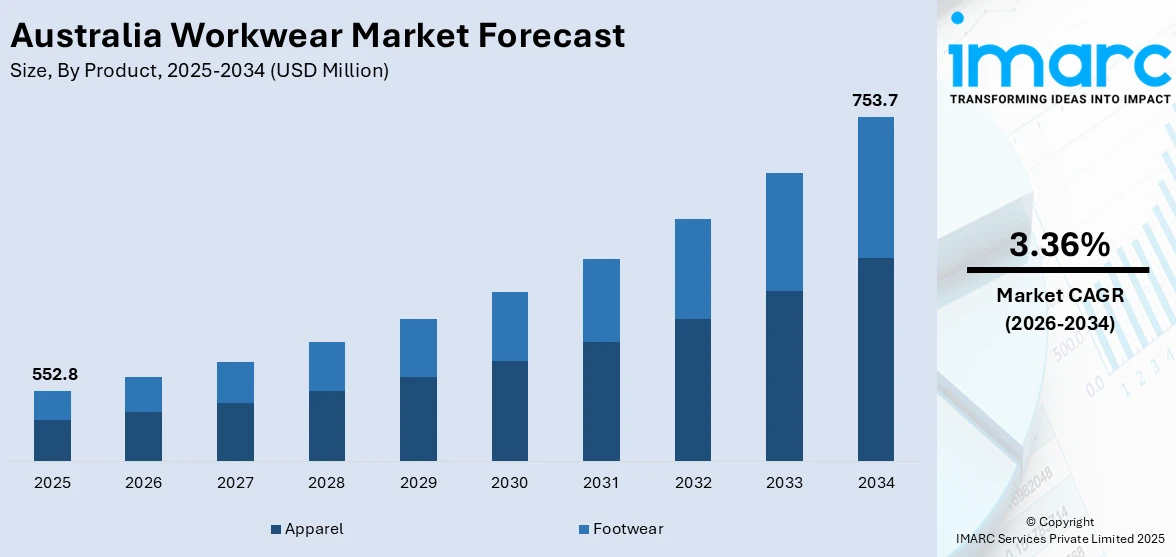

The Australia workwear market size reached USD 552.8 Million in 2025. The market is projected to reach USD 753.7 Million by 2034, exhibiting a growth rate (CAGR) of 3.36% during 2026-2034. The market is witnessing consistent growth, catalyzed by increasing demand in different industries such as construction, healthcare, and manufacturing. Growing emphasis on employee safety, adherence to occupational standards, and the increasing culture of professional dress are fueling market growth. The trend towards green and functional clothing is also driving consumer behavior. Both physical and digital channels of distribution serve as key drivers for product availability. Increased innovation and personalization are bound to impact the Australia workwear market share.

|

Report Attribute

|

Key Statistics

|

|---|---|

|

Base Year

|

2025

|

|

Forecast Years

|

2026-2034

|

|

Historical Years

|

2020-2025

|

| Market Size in 2025 | USD 552.8 Million |

| Market Forecast in 2034 | USD 753.7 Million |

| Market Growth Rate 2026-2034 | 3.36% |

Australia Workwear Market Trends:

E‑Commerce Expansion and Digital Distribution

Digital channels are becoming a major force in the way workwear is purchased and distributed across Australia. As more industries prioritise convenience and nationwide access, online platforms are helping workwear suppliers reach a broader customer base, especially in regional and hard-to-service areas. E-commerce provides greater product visibility, easier bulk ordering, and efficient returns features that are particularly valued by businesses managing diverse and mobile teams. In July 2025, official data highlighted a clear increase in workwear related transactions across major online marketplaces, indicating a shift in how procurement is handled across sectors. This move to digital is not just about convenience; it supports more agile inventory strategies, encourages customisable uniform options, and shortens lead times for fulfilment. It’s also helping level the playing field for newer entrants in the market who can compete online without needing a national retail footprint. Altogether, these changes underscore the importance of digital access and adaptability within Australia workwear market trends, as purchasing behaviours continue evolving with broader retail transformations.

To get more information on this market Request Sample

Innovation in Sustainable and Smart Textiles

Sustainability and intelligent design are increasingly at the center of Australia's workwear revolution, as companies seek not only regulatory compliance but also garments that optimize performance as well as environmental stewardship. Environmentally friendly materials such as organic cotton, recycled fibers, and biodegradable materials are experiencing increasing demand, particularly in sectors looking to minimize their operational impact. Concurrently, emerging smart textile advances are also making wearables more functional as clothes are now capable of tracking body temperature, fatigue, and heat or chemical exposure. These advancements indicate an industry that is changing to address safety and productivity requirements without diminishing comfort or ethics. In May 2025, the Australian government published new advice promoting adoption of sustainable and innovative materials in uniform design, further justifying this transition across industries. The shift to integrated, high‑function, and low‑impact clothing is gaining speed, fueled by evolving workforce expectations and greater focus on worker wellbeing. These innovations are not only transforming the way businesses select their uniforms but also supporting overall Australia workwear market growth, as suppliers react to demand for smarter, greener solutions.

Manufacturing Sector Decline Impacts Workwear Supply

On a more systemic level, the shrinking of domestic manufacturing is starting to influence the dynamics of workwear supply. Recently, the reports indicated that over 5,100 manufacturers shut down in the year to June 2024 an indicator of sustained industrial challenges, including energy costs and global competition. This contraction reduces local production capacity, which could impact the availability and cost structure of workwear goods traditionally sourced from Australian manufacturers. With fewer domestic factories, supply chains may lean more heavily on imports, potentially shifting the balance of quality, lead‑time, and sustainability expectations. For brands and buyers committed to Australian‑made credentials, this structural trend will require strategic responses such as partnering with remaining local producers, investing in automation, or exploring hybrid sourcing models. The downturn also underscores the importance of adaptability for the sector overall. It’s a macro‑trend that may have ripple effects on design, pricing, and supply, shaping the evolving landscape of the Australia workwear market.

Australia Workwear Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the country and regional levels for 2026-2034. Our report has categorized the market based on product, application, distribution channel, and end user.

Product Insights:

- Apparel

- Footwear

The report has provided a detailed breakup and analysis of the market based on the product. This includes apparel and footwear.

Application Insights:

Access the comprehensive market breakdown Request Sample

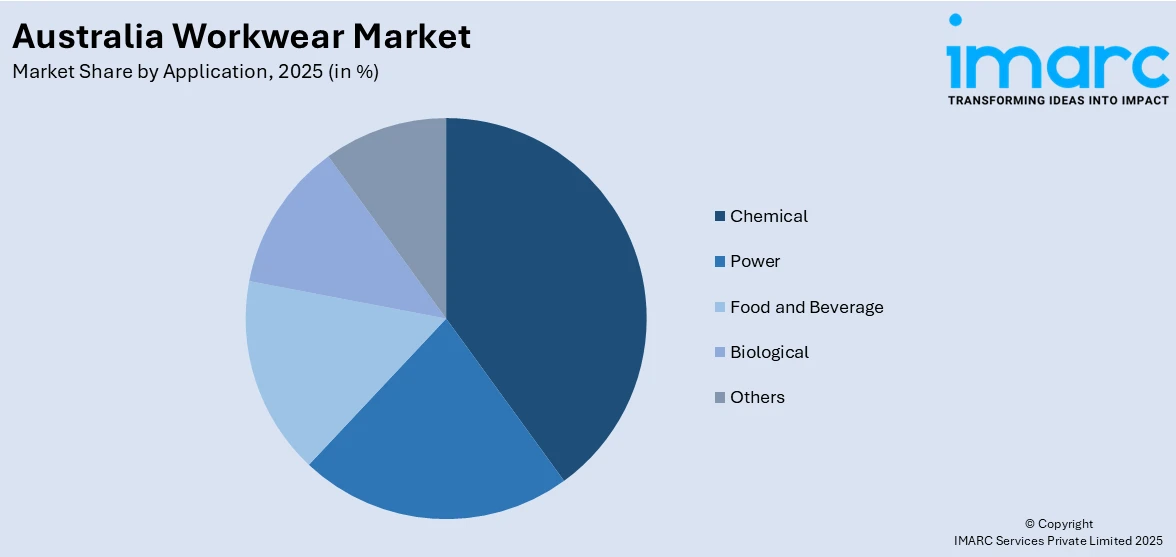

- Chemical

- Power

- Food and Beverage

- Biological

- Others

The report has provided a detailed breakup and analysis of the market based on the application. This includes chemical, power, food and beverage, biological, and others.

Distribution Channel Insights:

- Supermarkets and Hypermarkets

- Specialty Stores

- E-Commerce

- Others

A detailed breakup and analysis of the market based on the distribution channel have also been provided in the report. This includes supermarkets and hypermarkets, specialty stores, e-commerce, and others.

End User Insights:

- Men

- Women

The report has provided a detailed breakup and analysis of the market based on the end user. This includes men and women.

Regional Insights:

- Australia Capital Territory & New South Wales

- Victoria & Tasmania

- Queensland

- Northern Territory & Southern Australia

- Western Australia

The report has also provided a comprehensive analysis of all the major regional markets, which include Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, and Western Australia.

Competitive Landscape:

The market research report has also provided a comprehensive analysis of the competitive landscape. Competitive analysis such as market structure, key player positioning, top winning strategies, competitive dashboard, and company evaluation quadrant has been covered in the report. Also, detailed profiles of all major companies have been provided.

Australia Workwear Market News:

- August 2025: Arup has established a new partnership with Geared Up Culcha, an Indigenous‑owned Australian business, to supply safety gear, workwear, and branded merchandise across Australia. This collaboration reflects Arup’s Indigenous Procurement Strategy, embedding First Nations enterprises within its supply chain. Geared Up Culcha’s approach rooted in respect for Country and sustainable practices resonates deeply with Arup’s values. Together, they will enhance product design through on‑site capabilities and reinforce Australia’s commitment to inclusive and responsible sourcing.

- June 2025: City Workwear, a reputable Australian corporate apparel provider based in Perth, has launched its Premium Biz Collection of corporate uniforms for Australian workplaces. The collection includes skirts, dresses, and office shirts designed to blend elegance with comfort, catering to the modern needs of Australia's diverse and style-conscious workforce. Thoughtful fabric choices offer breathability, stretch, and easy care for busy workdays. Sizes are inclusive across genders, and businesses can customize pieces with logos, colors, and tailored fits.

Australia Workwear Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Apparel, Footwear |

| Applications Covered | Chemical, Power, Food and Beverage, Biological, Others |

| Distribution Channels Covered | Supermarkets and Hypermarkets, Specialty Stores, E-Commerce, Others |

| End Users Covered | Men, Women |

| Regions Covered | Australia Capital Territory & New South Wales, Victoria & Tasmania, Queensland, Northern Territory & Southern Australia, Western Australia |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the Australia workwear market performed so far and how will it perform in the coming years?

- What is the breakup of the Australia workwear market on the basis of product?

- What is the breakup of the Australia workwear market on the basis of application?

- What is the breakup of the Australia workwear market on the basis of distribution channel?

- What is the breakup of the Australia workwear market on the basis of end user?

- What is the breakup of the Australia workwear market on the basis of region?

- What are the various stages in the value chain of the Australia workwear market?

- What are the key driving factors and challenges in the Australia workwear market?

- What is the structure of the Australia workwear market and who are the key players?

- What is the degree of competition in the Australia workwear market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the Australia workwear market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the Australia workwear market.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the Australia workwear industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)