Automotive Antifreeze Market Size, Share, Trends and Forecast by Fluid Type, Technology, Vehicle Type, Distribution Channel, and Region, 2026-2034

Automotive Antifreeze Market Size, Share, Trends & Forecast (2026-2034)

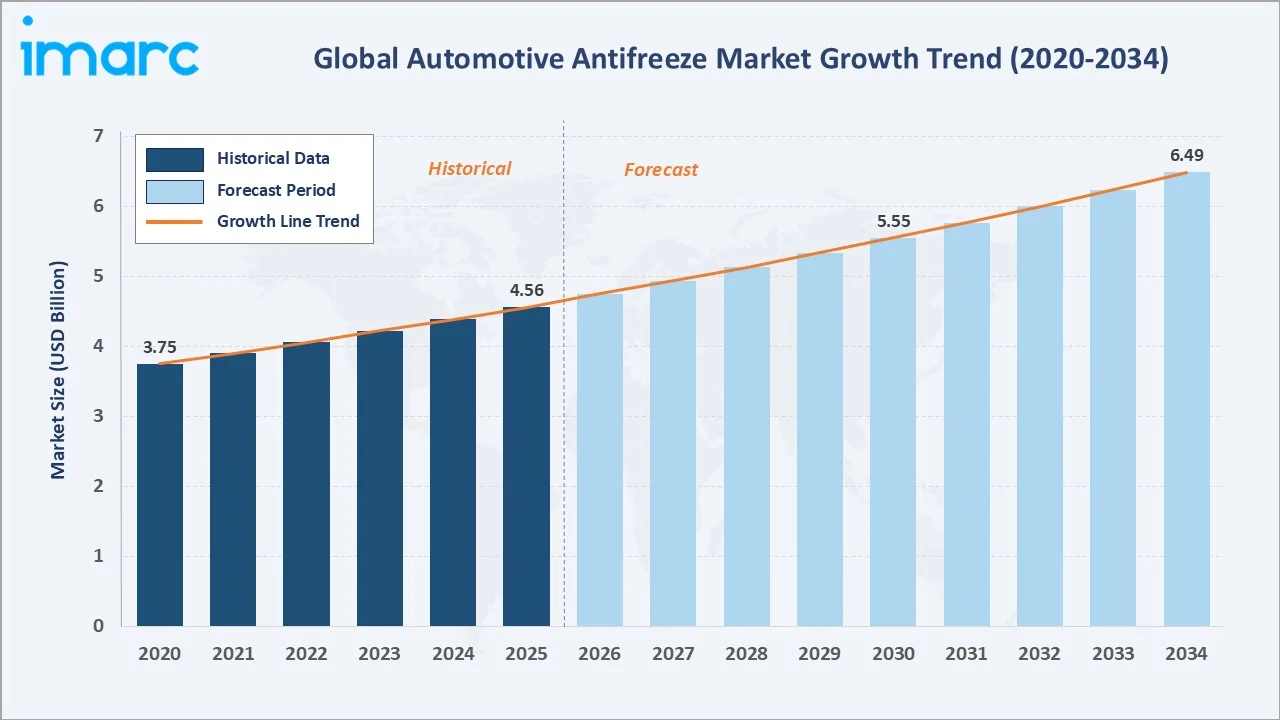

The global automotive antifreeze market size reached USD 4.56 Billion in 2025 and is projected to reach USD 6.49 Billion by 2034, exhibiting a CAGR of 4.00% during 2026-2034. Rising vehicle production, growing EV adoption, and advancements in engine technology are the primary forces shaping this market.

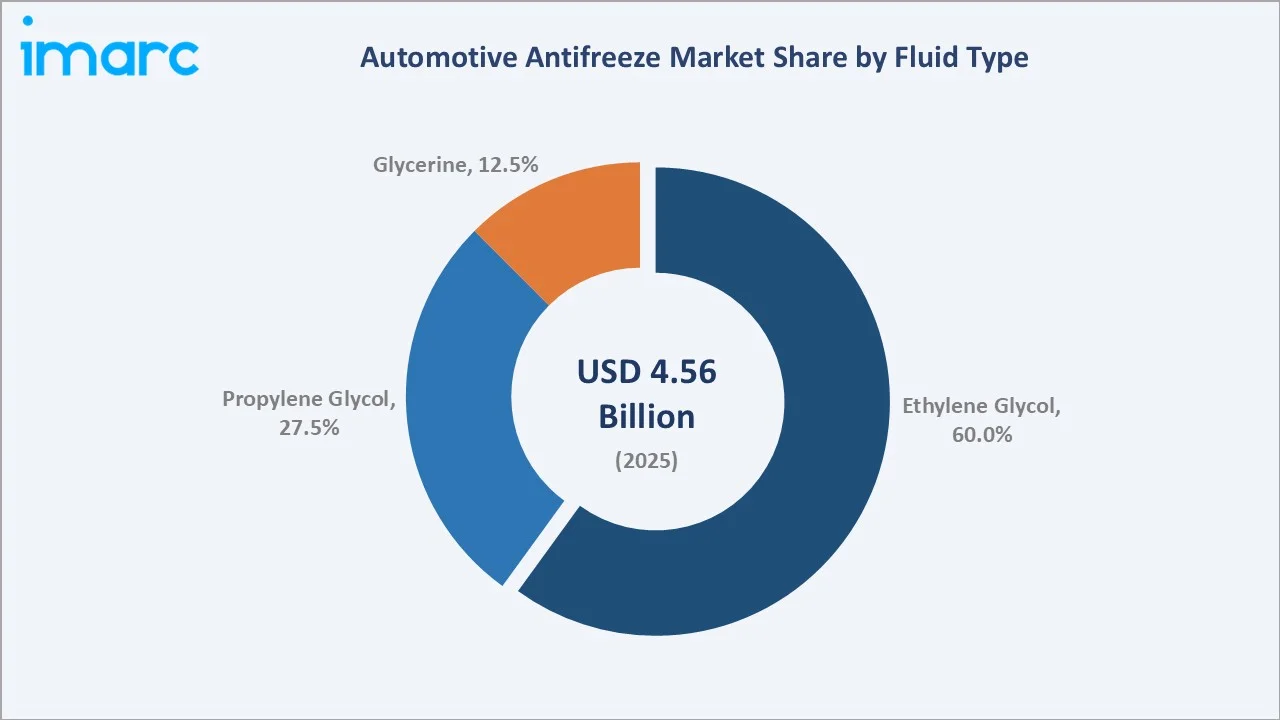

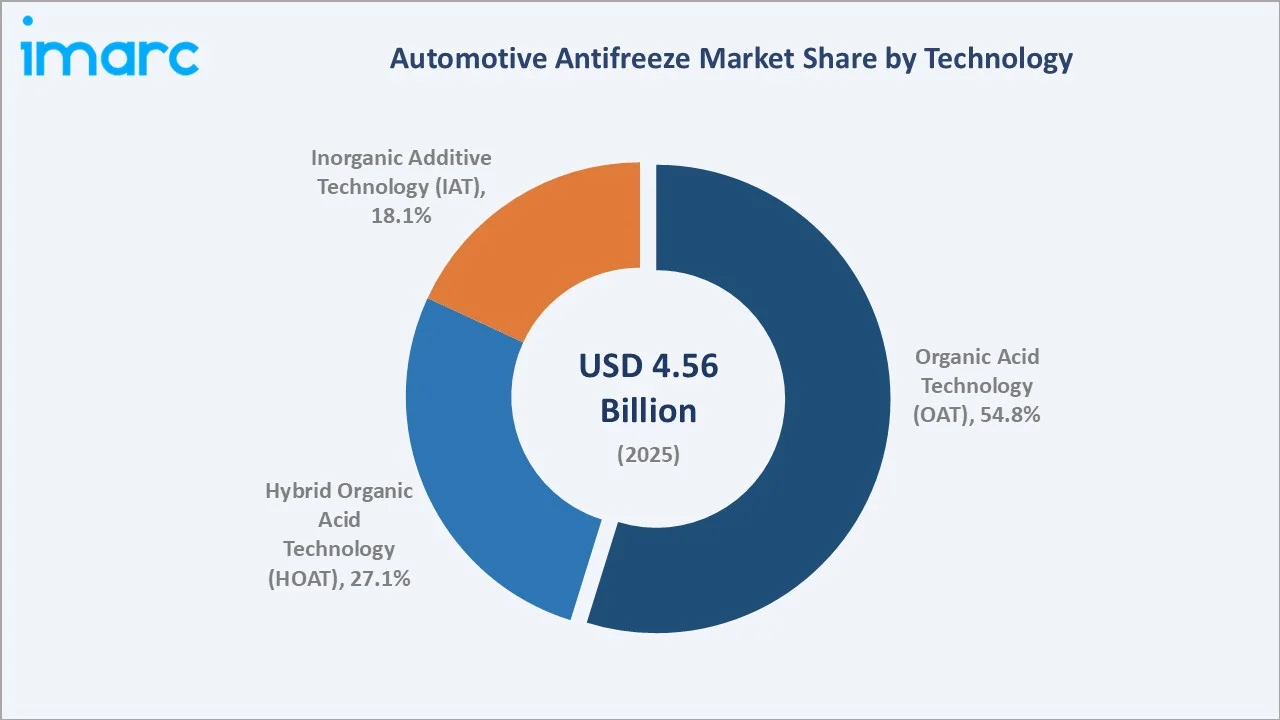

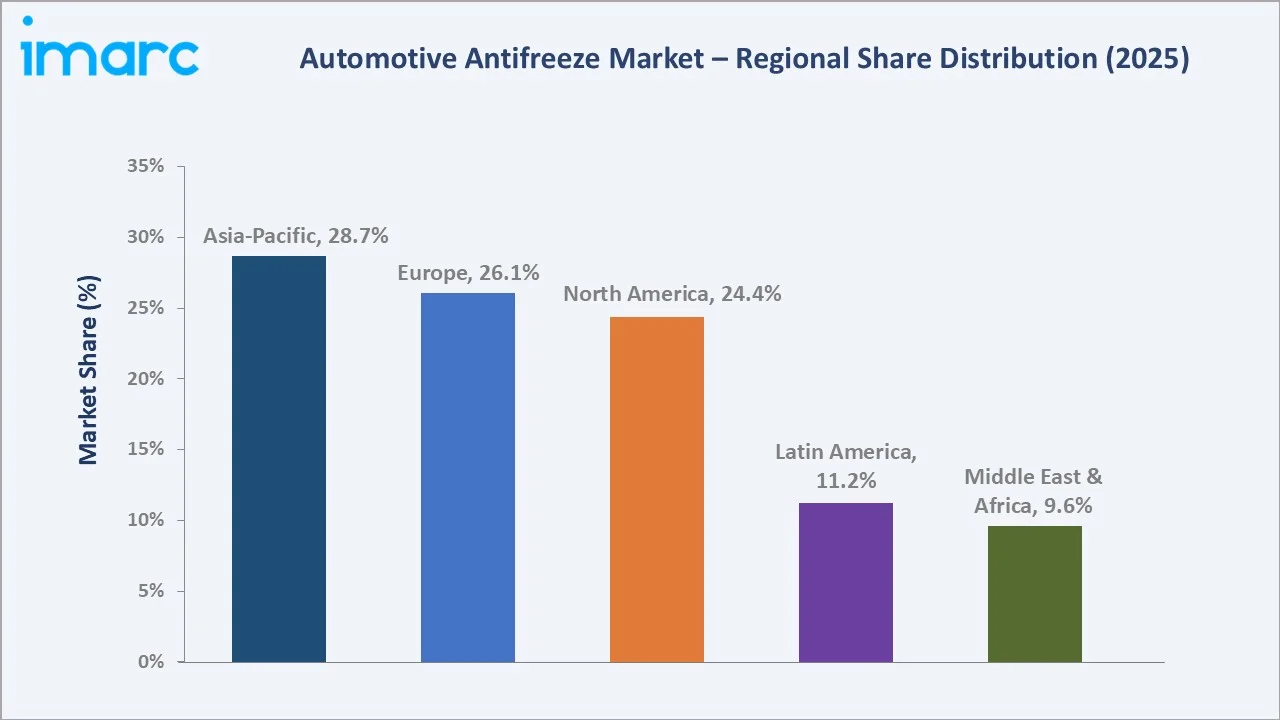

Ethylene Glycol leads fluid type segmentation at 60.0% in 2025, driven by widespread OEM adoption. Organic Acid Technology (OAT) commands 54.8% technology share. Asia-Pacific dominates the regional landscape with a 28.7% share, underpinned by strong vehicle production and expanding automotive aftermarkets.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 4.56 Billion |

|

Forecast Market Size (2034) |

USD 6.49 Billion |

|

CAGR (2026-2034) |

4.00% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Leading Fluid Type |

Ethylene Glycol (60.0% share, 2025) |

|

Leading Technology |

Organic Acid Technology – OAT (54.8% share, 2025) |

|

Leading Region |

Asia-Pacific (28.7% share, 2025) |

The automotive antifreeze market growth from 2020 through 2034 reflects sustained demand driven by expanding global vehicle fleets, rising EV thermal management requirements, and growing OEM specification upgrades. The forecast to USD 6.49 Billion by 2034 captures accelerating long-life OAT coolant adoption and eco-friendly formulations across major automotive markets globally.

To get more information on this market, Request Sample

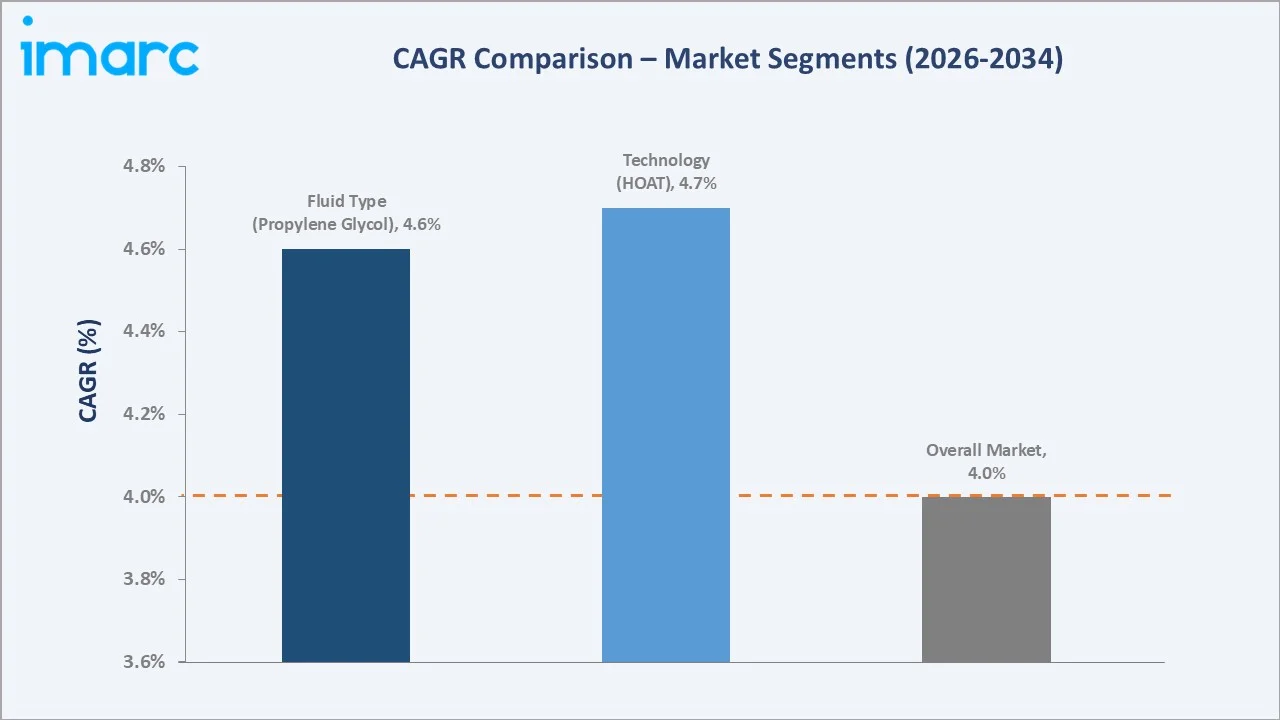

The CAGR trajectories across key fluid type and technology sub-segments highlight Propylene Glycol at approximately 4.6% CAGR and Hybrid Organic Acid Technology (HOAT) at approximately 4.7% CAGR as the fastest-growing categories within the automotive antifreeze market through 2034.

Executive Summary

The automotive antifreeze market is on a sustained growth trajectory from USD 4.56 Billion in 2025 to USD 6.49 Billion by 2034. The market encompasses ethylene glycol, propylene glycol, and glycerine-based formulations deployed across passenger vehicles, commercial vehicles, and electric vehicle platforms worldwide.

Ethylene Glycol leads at 60.0% in 2025, owing to its superior heat transfer efficiency, cost-effectiveness, and universal compatibility with OEM-specified cooling systems across passenger and heavy-duty commercial vehicle segments globally.

Organic Acid Technology (OAT) commands 54.8% technology share in 2025, driven by its extended service life of up to 5 years, reduced maintenance frequency, and compatibility with modern aluminium engine components across major automotive OEM platforms globally.

Asia-Pacific dominates at 28.7% in 2025, supported by the world’s largest vehicle production base in China, India, Japan, and South Korea. Europe follows at 26.1%, with North America at 24.4%, driven by stringent coolant specification requirements and growing EV adoption rates.

Key Market Insights

|

Insight |

Data |

|

Largest Fluid Type Segment |

Ethylene Glycol – 60.0% share (2025) |

|

Leading Technology |

Organic Acid Technology (OAT) – 54.8% share (2025) |

|

Leading Region |

Asia-Pacific – 28.7% share (2025) |

|

Second Largest Region |

Europe – 26.1% share (2025) |

|

Top Companies |

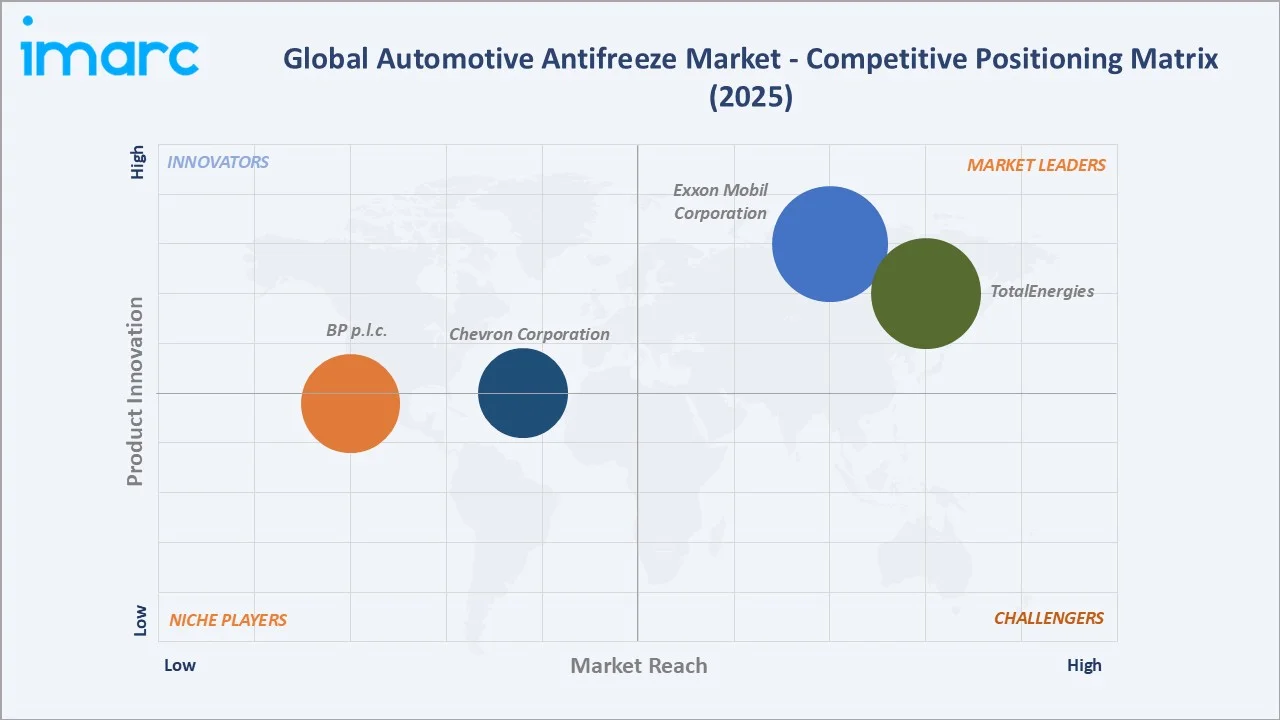

BP p.l.c., Chevron Corporation, Exxon Mobil Corporation, and TotalEnergies |

- Ethylene Glycol at 60.0% dominates because it delivers superior freeze and boil-over protection at a lower cost per litre than alternatives. OEM adoption across mass-market passenger vehicles and heavy-duty commercial applications ensures sustained volume demand throughout the forecast period globally.

- OAT at 54.8% leads technology segmentation because modern engine designs favour long-life inhibitor chemistry that protects aluminium heat exchangers and plastic cooling components. Extended service intervals reduce vehicle lifecycle costs, driving systematic OEM transitions from IAT to OAT globally.

- Asia-Pacific’s 28.7% regional dominance reflects its unrivalled vehicle production capacity, rapidly expanding automotive aftermarket, and growing EV fleet requiring specialised thermal management fluids. China and India are expanding domestic coolant manufacturing capacity to serve both OEM and aftermarket channels.

Automotive Antifreeze Market Overview

The automotive antifreeze market encompasses ethylene glycol-based, propylene glycol-based, and glycerine-based formulations across OAT, HOAT, and IAT technology platforms serving passenger vehicles, commercial vehicles, electric vehicles, and off-highway equipment globally.

The ecosystem integrates petrochemical feedstock producers, antifreeze formulators, additive suppliers, OEM specification bodies, independent aftermarket distributors, service networks, and regulatory agencies across major automotive markets globally.

Market Dynamics

To evaluate market opportunities, Request Sample

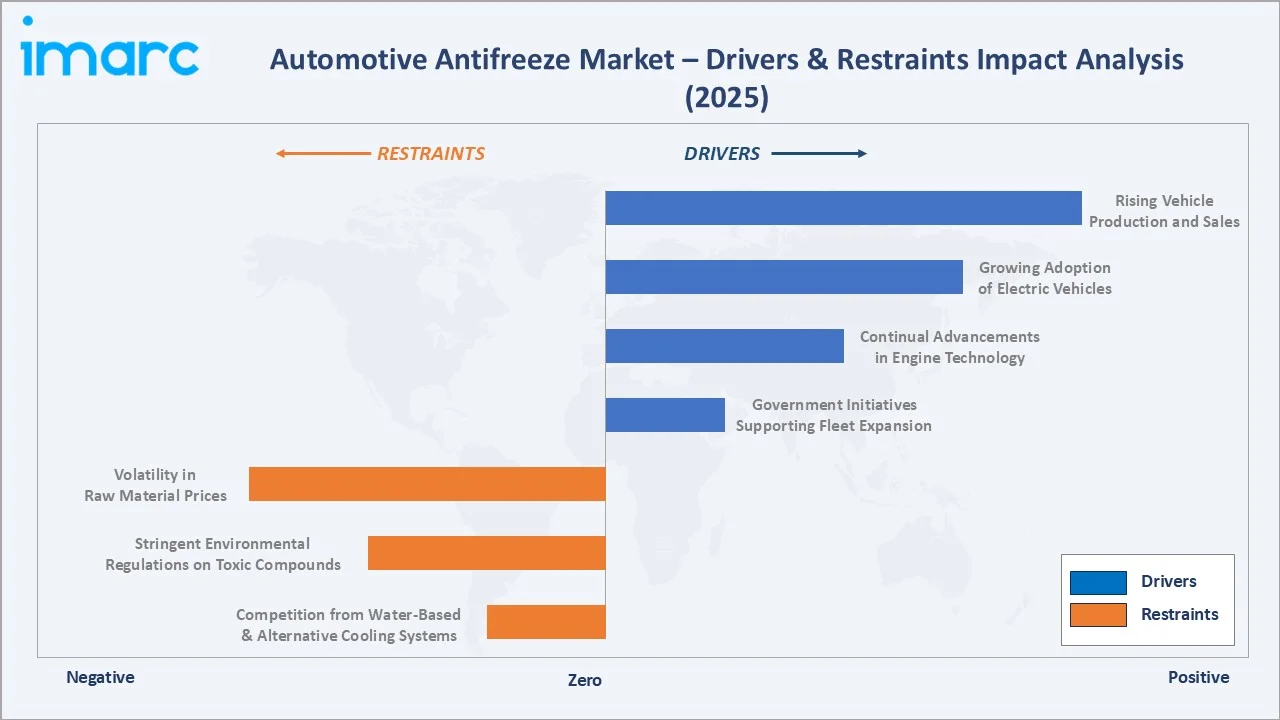

Market Drivers

- Rising Vehicle Production and Sales: Global vehicle production continues to expand steadily, with passenger car in use totalled 62.32 million unit in 2024. Growing middle-class populations across Asia and Latin America drive vehicle ownership rates, directly increasing demand for antifreeze and coolant products in both OEM and aftermarket channels globally.

- Continual Advancements in Engine Technology: Modern engines operate at higher thermal loads, requiring advanced coolant formulations with superior heat transfer efficiency. Turbocharged and downsized engines increase thermal stress on cooling systems, while direct injection platforms demand coolants compatible with aluminium and magnesium alloy components throughout the vehicle lifecycle.

- Growing Adoption of Electric Vehicles (EVs): EV battery thermal management systems require specialised glycol-based coolants to regulate battery pack temperatures within optimal operating ranges. With global electric car market reached new highs in 2025, growing by 20% from 2024 to exceed 20 million sales, demand for low-conductivity, corrosion-inhibited antifreeze formulations is growing rapidly across all major markets.

- Government Initiatives Supporting Automotive Fleet Expansion: Government programmes expanding public transport fleets, subsidising commercial vehicle purchases, and developing automotive manufacturing hubs in emerging economies drive OEM coolant procurement volumes. Fleet electrification mandates further stimulate demand for specialised EV-compatible thermal management fluids globally.

Market Restraints

- Volatility in Raw Material Prices: Ethylene glycol and propylene glycol prices are subject to volatility linked to ethylene feedstock costs and global petrochemical market dynamics. Input cost fluctuations compress manufacturer margins and create pricing uncertainty across supply chains, constraining profitability particularly for smaller regional antifreeze producers.

- Stringent Environmental Regulations on Toxic Compounds: Regulatory pressure on ethylene glycol toxicity and coolant disposal requirements increases compliance costs across major markets. Europe’s REACH regulations and EPA guidelines in the United States require reformulation investments and disposal infrastructure, creating barriers to entry and raising operating costs for antifreeze manufacturers.

- Competition from Water-Based and Alternative Cooling Systems: Advances in heat pump technology and phase-change materials are offering performance alternatives to traditional glycol-based antifreeze in certain EV applications. Water-cooled systems with reduced glycol concentrations are gaining interest as automakers pursue cost reduction, creating margin pressure on premium antifreeze formulations.

Market Opportunities

- Expanding EV Thermal Management Fluid Segment: The rapid growth of battery electric vehicles creates a structurally new demand category for low-electrical-conductivity antifreeze. Specialised EV coolants command premium pricing over conventional formulations, representing a high-value growth opportunity for major antifreeze manufacturers investing in EV-compatible product development globally.

- Biodegradable and Propylene Glycol-Based Formulation Growth: Rising consumer and regulatory preference for environmentally responsible automotive fluids is accelerating adoption of propylene glycol-based antifreeze, which offers lower toxicity than ethylene glycol alternatives. Organic certification requirements in fleet and municipal procurement policies are driving conversion to bio-based antifreeze formulations.

Market Challenges

- Counterfeit and Substandard Coolant Products in Emerging Markets: Proliferation of counterfeit antifreeze products in price-sensitive markets undermines demand for quality-certified formulations, erodes brand value, and creates warranty liability risks for automotive OEMs. Strengthening distribution channel integrity and consumer education represent ongoing challenges across Asia, Africa, and Latin America.

- Extended Service Intervals Reducing Replacement Frequency: Adoption of OAT and HOAT long-life coolants extending service intervals to 5–10 years reduces replacement frequency and aftermarket volume per vehicle over time. This structural shift requires manufacturers to capture higher value per unit to sustain revenue growth despite lower per-vehicle replacement rates globally.

Emerging Market Trends

1. Transition from IAT to OAT and HOAT Formulations:

The global automotive coolant market is undergoing a systematic technology transition from conventional inorganic additive technology to organic acid and hybrid organic acid formulations. OEM service interval extensions and aluminium engine compatibility requirements are accelerating this shift across all vehicle categories globally.

2. Development of EV-Specific Low-Conductivity Coolants:

Electric vehicle battery thermal management requires coolants with electrical conductivity below 1 µS/cm to prevent battery degradation and short-circuit risks. Major manufacturers are developing purpose-engineered EV coolants combining low conductivity, superior heat transfer, and extended service life for battery, motor, and inverter cooling circuits.

3. Adoption of Bio-Based and Sustainable Antifreeze Products:

Bio-derived propylene glycol and glycerine-based antifreeze products are gaining traction as automotive OEMs and fleet operators target reduced environmental footprint. Bio-based formulations offer comparable performance to petroleum-derived counterparts while meeting voluntary sustainability standards and regulatory biodegradability criteria globally.

4. Digital Supply Chain and Condition Monitoring Integration:

Connected vehicle platforms are enabling real-time coolant condition monitoring, predictive replacement scheduling, and remote fluid health diagnostics. Integration of IoT sensors with coolant management systems is creating new aftermarket service models and shifting demand from scheduled to condition-based coolant replacement globally.

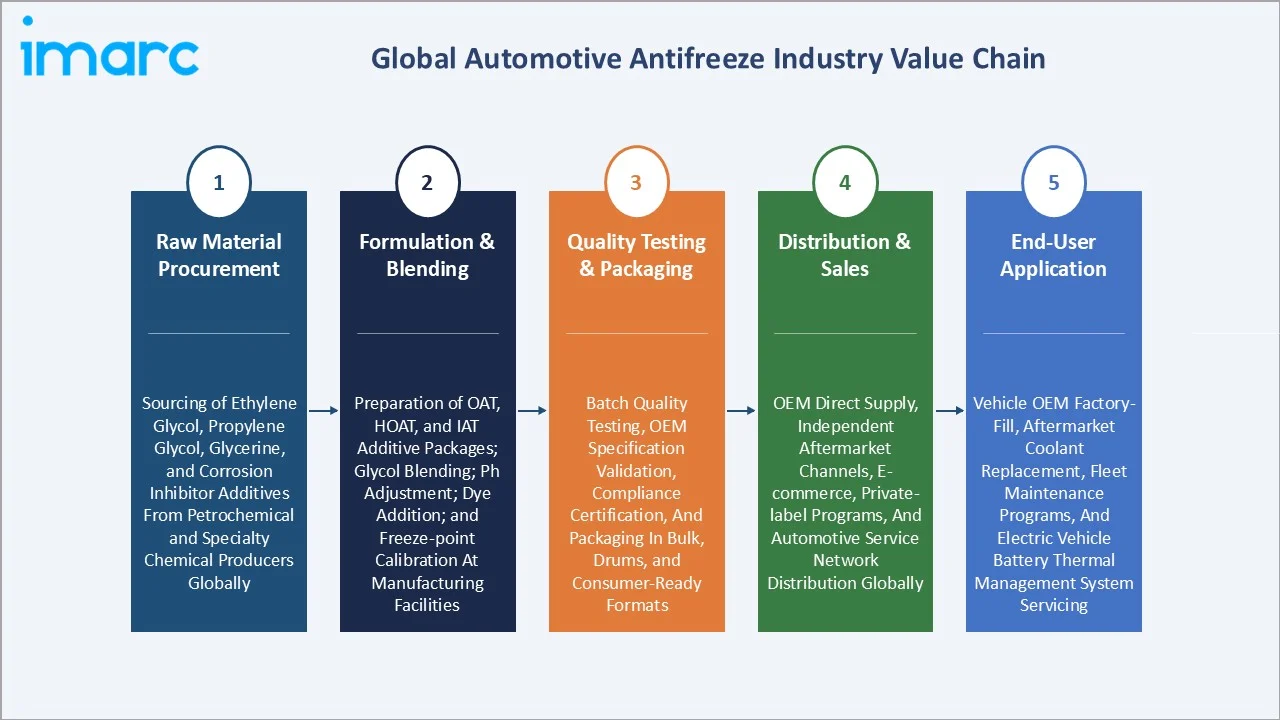

Industry Value Chain Analysis

The automotive antifreeze value chain spans five integrated stages from petrochemical feedstock procurement through end-user vehicle application. Antifreeze formulators capture primary value through additive package development, while distribution networks generate recurring revenue through aftermarket channel management across global automotive markets.

|

Stage |

Key Activities |

|

Raw Material Procurement |

Sourcing of ethylene glycol, propylene glycol, glycerine, and corrosion inhibitor additives from petrochemical and specialty chemical producers globally |

|

Formulation & Blending |

Preparation of OAT, HOAT, and IAT additive packages; glycol blending; pH adjustment; dye addition; and freeze-point calibration at manufacturing facilities |

|

Quality Testing & Packaging |

Batch quality testing, OEM specification validation, compliance certification, and packaging in bulk, drums, and consumer-ready formats |

|

Distribution & Sales |

OEM direct supply, independent aftermarket channels, e-commerce, private-label programs, and automotive service network distribution globally |

|

End-User Application |

Vehicle OEM factory-fill, aftermarket coolant replacement, fleet maintenance programs, and electric vehicle battery thermal management system servicing |

Formulation and blending stages capture the highest value in the antifreeze supply chain, requiring specialised additive chemistry expertise and OEM approval investments. Aftermarket distribution and branded retail channels represent growing recurring revenue streams as vehicle populations expand, and maintenance cycles continue.

Technology Landscape in the Automotive Antifreeze Industry

Organic Acid Technology (OAT) Advancement

OAT coolants utilise carboxylate-based inhibitors that selectively adsorb onto metal surfaces, providing targeted corrosion protection with minimal additive depletion. Next-generation OAT formulations extend service life to 10 years or 300,000 kilometres, reducing maintenance costs while meeting stringent aluminium protection requirements for modern engine architectures.

Hybrid Organic Acid Technology (HOAT) Innovation

HOAT formulations combine OAT carboxylate chemistry with selected inorganic inhibitors to provide rapid initial protection and extended service life. Latest HOAT developments focus on silicate-free, phosphate-free variants meeting Mercedes-Benz, BMW, and VW Group specifications for mixed-metal cooling system protection across global vehicle platforms.

EV Thermal Management Fluid Engineering

EV-specific coolant development integrates low-electrical-conductivity requirements with superior heat transfer performance for battery cell cooling loops. Advanced dielectric fluid formulations are being developed for immersion-cooled battery architectures, representing the most technologically demanding segment of the automotive thermal fluid market.

Bio-Based Glycol Production Technologies

Second-generation bio-derived propylene glycol and glycerine extraction from biodiesel by-products are reducing production costs for bio-based antifreeze formulations. Fermentation-derived glycols and bio-catalytic conversion processes are improving cost parity with petrochemical equivalents, supporting commercial scale-up of sustainable antifreeze manufacturing.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Fluid Type | Ethylene Glycol | 60.0% | 2025 |

| Technology | Organic Acid Technology (OAT) | 54.8% | 2025 |

| Vehicle Type | 🔒 | 🔒 | 2025 |

| Distribution Channel | 🔒 | 🔒 | 2025 |

| Region | Asia-Pacific | 28.7% | 2025 |

By Fluid Type

Ethylene Glycol commands a 60.0% majority share in 2025 owing to its superior anti-freeze and anti-boil performance, cost efficiency, and universal compatibility with OEM-specified cooling systems. Mass-market passenger vehicles and heavy-duty commercial applications drive volume consumption of ethylene glycol-based antifreeze across all major global automotive markets.

To access detailed market analysis, Request Sample

Propylene Glycol (27.5%) captures demand from fleet operators and consumers preferring lower-toxicity antifreeze formulations, particularly in markets with stringent environmental regulations. Glycerine (12.5%) serves niche bio-based and recycled coolant applications, representing the fastest-growing segment as sustainability requirements intensify across automotive aftermarkets globally.

By Technology

Organic Acid Technology (OAT) dominates at 54.8% in 2025, driven by OEM transitions from IAT to long-life coolant specifications across passenger car platforms. OAT’s extended service interval of 5 years or 150,000 miles provides vehicle owners with significant maintenance cost savings, reinforcing its dominant position in the global automotive coolant market.

Hybrid Organic Acid Technology (HOAT) at 27.1% serves European and Asian OEM platforms requiring combined silicate and carboxylate inhibitor performance for mixed-metal systems. Inorganic Additive Technology (IAT) at 18.1% remains in legacy vehicle populations requiring conventional green coolant specifications in price-sensitive aftermarket segments globally.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

28.7% |

Large vehicle production base, expanding EV fleet, and growing automotive aftermarket |

|

Europe |

26.1% |

Stringent OEM coolant specifications, high EV adoption, and established replacement demand |

|

North America |

24.4% |

Large legacy vehicle fleet, growing EV market, and environmental compliance requirements |

|

Latin America |

11.2% |

Expanding vehicle ownership, growing commercial fleet, and rising OAT coolant adoption |

|

Middle East & Africa |

9.6% |

High-temperature climate demand, expanding aftermarket, and infrastructure development |

Asia-Pacific’s 28.7% market dominance in 2025 is driven by China’s position as the world’s largest vehicle producer and EV market, India’s rapidly expanding passenger vehicle fleet, and Japan and South Korea’s sophisticated OEM coolant specification requirements. The region’s large population base and rising disposable incomes sustain robust aftermarket coolant demand.

Europe, at 26.1% in 2025, is anchored by stringent OEM-specific coolant specifications from Volkswagen Group, BMW, Daimler, and Stellantis. Growing EV adoption and regulatory pressure for extended-life, low-toxicity coolants support premium product adoption. North America at 24.4% reflects large vehicle fleet maintenance demand and expanding EV infrastructure cooling requirements.

Competitive Landscape

The automotive antifreeze market is moderately concentrated, with major global energy and chemical companies leveraging integrated glycol supply chains, established OEM approvals, and extensive automotive aftermarket distribution networks to maintain competitive leadership across global markets.

|

Company Name |

Key Products / Operations |

Market Position |

Global Strategic Focus |

|

BP p.l.c. |

Isocool, Diesel Coolant HD-50, ProCool Premixed Coolant |

Established |

Targeting EV thermal management fluid development through integrated lubricants strategy |

|

Chevron Corporation |

Havoline Xtended Life Antifreeze/Coolant, Havoline Universal Antifreeze/Coolant, Havoline Conventional Antifreeze/Coolant, Delo XLC Antifreeze/Coolant, Delo ELC Antifreeze/Coolant |

Established |

Strengthening OEM-approved coolant portfolio; advancing OAT and HOAT formulations for commercial vehicle and EV applications globally |

|

Exxon Mobil Corporation |

Mobil Antifreeze Coolant |

Leader |

Leveraging global distribution network; investing in EV-compatible thermal management fluid development and long-life OAT reformulations |

|

TotalEnergies |

Neotech range, Cartech range, Plus EVO Range |

Leader |

Investing in bio-based and EV-compatible antifreeze innovations; expanding automotive lubricant and coolant distribution across Europe, Asia, and Africa |

Key players include BP p.l.c., Chevron Corporation, Exxon Mobil Corporation, and TotalEnergies, among others.

Key Company Profiles

ExxonMobil Corporation

ExxonMobil Corporation is a global energy leader with a comprehensive automotive fluids portfolio that includes Mobil-branded antifreeze and engine coolant products distributed across OEM, commercial fleet, and independent aftermarket channels worldwide.

- Product Portfolio: Mobil Antifreeze/Coolant

- Strategic Focus: ExxonMobil is investing in developing next-generation electric vehicle thermal management fluids under the Mobil brand, building on its established global distribution network and OEM approval portfolio to capture premium coolant market opportunities across passenger EV and commercial EV platforms worldwide.

Chevron Corporation

Chevron Corporation is a leading player in the global automotive antifreeze/coolant market. Chevron develops formulations with advanced inhibitor technologies to ensure corrosion resistance and thermal stability, supporting industrial efficiency by delivering reliable cooling solutions that enhance equipment performance and reduce maintenance requirements.

- Product Portfolio: Havoline Xtended Life Antifreeze/Coolant, Havoline Universal Antifreeze/Coolant, Havoline Conventional Antifreeze/Coolant, Delo XLC Antifreeze/Coolant, Delo ELC Antifreeze/Coolant, and others.

- Strategic Focus: Chevron is focused on reinforcing its brand leadership in the global antifreeze/coolant market through continued investment in advanced inhibitor technology and extended-life coolant formulations, while expanding its international footprint across Asia-Pacific, Europe, and Latin America through its integrated Havoline lubricants and fluids distribution network to broaden its global revenue base.

Market Concentration Analysis

The automotive antifreeze market is moderately concentrated, with major integrated energy companies including BP, ExxonMobil Corporation, and TotalEnergies holding significant shares through broad product portfolios, established OEM approvals, and global distribution capabilities alongside strong regional players and specialty chemical manufacturers.

At the product technology level, the OAT segment exhibits higher concentration reflecting the capital-intensive nature of OEM specification approval processes. Aftermarket channels show greater fragmentation, with private-label and regional brands competing on price in developing markets alongside premium global brands targeting brand-conscious consumers.

Investment & Growth Opportunities

Fastest-Growing Segments

Propylene Glycol represents the highest-growth fluid type segment through 2034 at approximately 4.6% CAGR, capturing rising demand for low-toxicity, bio-based antifreeze formulations. HOAT technology leads technology segment growth at approximately 4.7% CAGR, driven by European OEM adoption and growing HOAT specification requirements in Asian markets globally.

Emerging Markets

India, Southeast Asia, and Latin America are emerging as significant investment frontiers. India’s rapidly expanding vehicle production and growing automotive aftermarket present substantial opportunity for both OEM-specified coolant supply and branded aftermarket distribution. Southeast Asian fleet operators are increasingly adopting OAT-grade specifications for commercial vehicle maintenance.

Venture & Investment Trends

Strategic investment is flowing into EV thermal management fluid development, bio-based coolant manufacturing capacity, and digital supply chain platforms. Partnership between antifreeze manufacturers and EV OEMs for co-engineered thermal fluid development represents the most capital-intensive growth investment category through 2034.

Future Market Outlook (2026-2034)

The automotive antifreeze market is forecast to expand from USD 4.56 Billion in 2025 to USD 6.49 Billion by 2034 at a CAGR of 4.00%, driven by continued vehicle production growth, accelerating EV adoption, and systematic OAT/HOAT technology transitions across global automotive aftermarkets through the forecast horizon.

Three structural forces will shape the market through 2034: EV thermal management fluid demand will create a new premium segment displacing conventional antifreeze in battery-electric platforms; sustainability mandates will accelerate propylene glycol and bio-based product adoption; and digital condition monitoring will shift aftermarket replacement from scheduled to predictive maintenance models globally.

Research Methodology

Primary Research

Primary research encompassed structured interviews with antifreeze manufacturers, automotive OEM purchasing managers, independent aftermarket distributors, automotive service technicians, and EV platform thermal engineers. Primary data validated market sizing, segment shares, regional demand estimates, and technology adoption trends across the global automotive antifreeze industry.

Secondary Research

Key secondary sources include OEM technical service bulletins, ASTM coolant standard documentation, industry association publications, annual reports from major energy and chemical companies, trade publications covering automotive aftermarket sectors, and market intelligence databases covering automotive fluids and lubricants globally.

Forecasting Models

Market size estimations and growth projections were derived using combined top-down and bottom-up forecasting models incorporating global vehicle production forecasts, OEM specification transition timelines, EV fleet growth projections, and regional aftermarket demand modelling. Scenario modelling encompassed base, optimistic, and conservative cases through the 2034 horizon.

Automotive Antifreeze Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Fluid Types Covered | Ethylene Glycol, Propylene Glycol, Glycerine |

| Technologies Covered | Inorganic Additive Technology (IAT), Organic Acid Technology (OAT), Hybrid Organic Acid Technology (HOAT) |

| Vehicle Types Covered | Passenger Vehicle, Commercial Vehicle, Construction Vehicle |

| Distribution Channels Covered | Original Equipment Manufacturers (OEMs), Aftermarket |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | BP p.l.c., Chevron Corporation, Exxon Mobil Corporation, TotalEnergies, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive antifreeze market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global automotive antifreeze market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive antifreeze industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive Antifreeze Market Report

The global automotive antifreeze market reached USD 4.56 Billion in 2025, reflecting sustained demand driven by expanding global vehicle fleets, rising EV thermal management requirements, and ongoing OAT and HOAT coolant adoption across passenger and commercial vehicle platforms worldwide.

The market is projected to reach USD 6.49 Billion by 2034, growing at a CAGR of 4.00% during 2026–2034, driven by vehicle production growth, EV thermal management fluid adoption, sustainability-driven propylene glycol demand, and expansion of automotive aftermarket channels across emerging economies.

Ethylene Glycol leads the market with a 60.0% share in 2025, driven by superior freeze and boil-over performance, cost efficiency, and universal OEM compatibility across passenger and commercial vehicle platforms globally. This segment is expected to maintain leadership through 2034 despite growing propylene glycol adoption.

Organic Acid Technology (OAT) commands the largest technology share at 54.8% in 2025. Its extended service life, aluminium corrosion protection, and OEM adoption across major global vehicle platforms sustain its dominant position, with continued growth supported by fleet-wide transitions from legacy IAT products through the forecast period.

Asia-Pacific dominates with a 28.7% share in 2025, underpinned by the world’s largest vehicle production base, rapidly expanding EV fleet, and growing automotive aftermarket in China, India, Japan, and South Korea. The region is expected to maintain its leading position through the 2034 forecast horizon.

Key market drivers include rising global vehicle production and sales, continual advancements in engine technology requiring advanced coolant formulations, growing adoption of electric vehicles requiring specialised thermal management fluids, and government initiatives supporting automotive fleet expansion across emerging economies globally.

Major challenges include volatility in ethylene glycol and propylene glycol raw material prices, stringent environmental regulations on coolant toxicity and disposal, proliferation of counterfeit products in price-sensitive markets, and structural demand reduction from extended OAT service intervals reducing per-vehicle replacement frequency globally.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)