Automotive Connectors Market Size, Share, Trends and Forecast by Connection Type, Connector Type, System Type, Vehicle Type, Application, and Region, 2026-2034

Global Automotive Connectors Market Size, Share, Trends & Forecast (2026-2034)

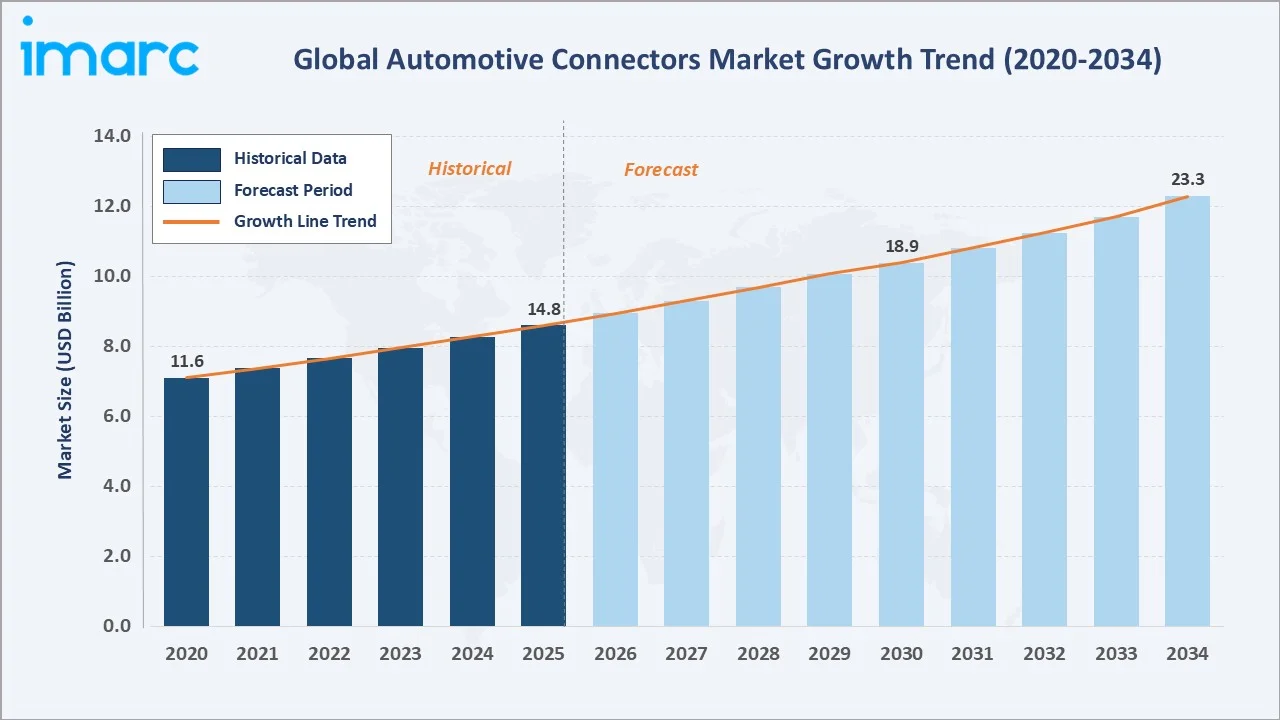

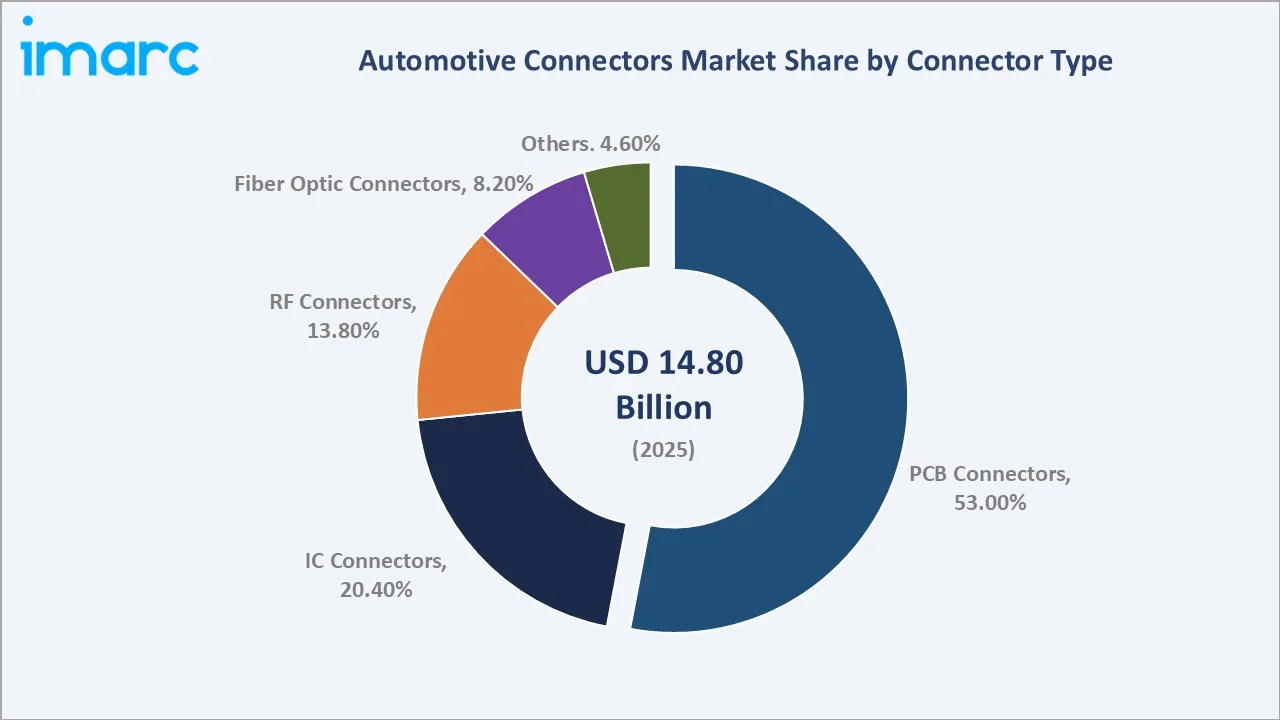

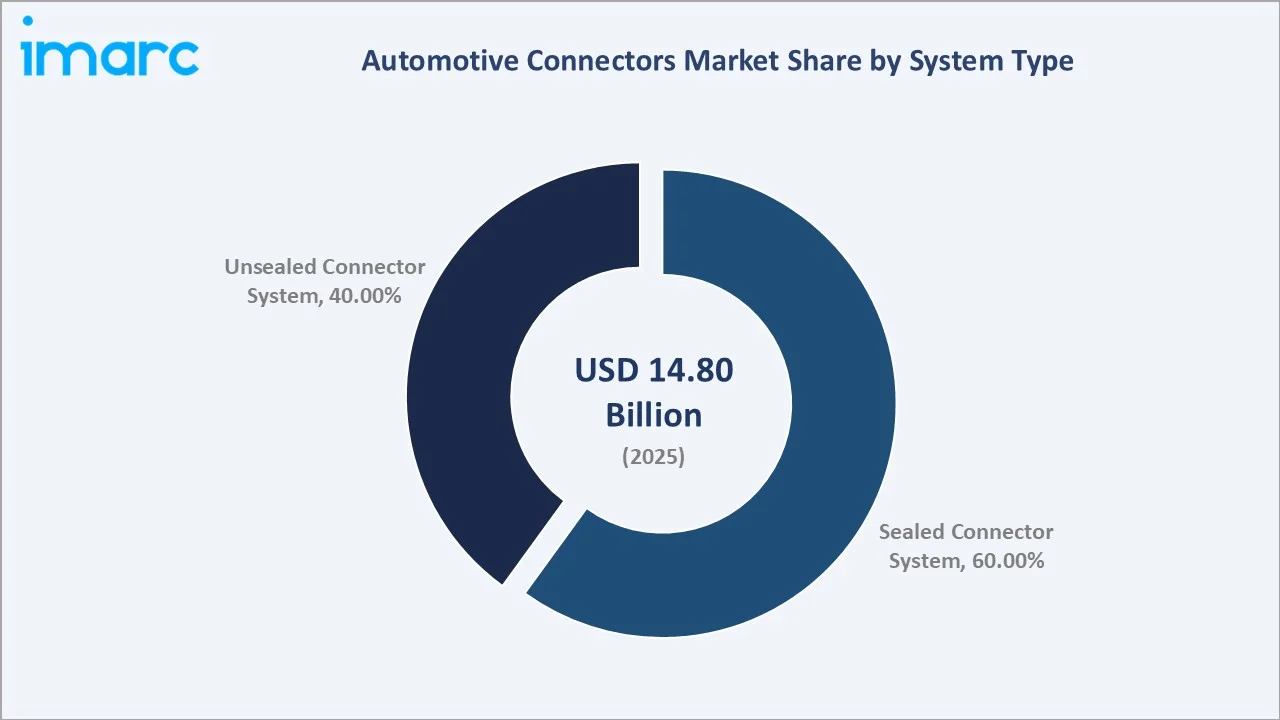

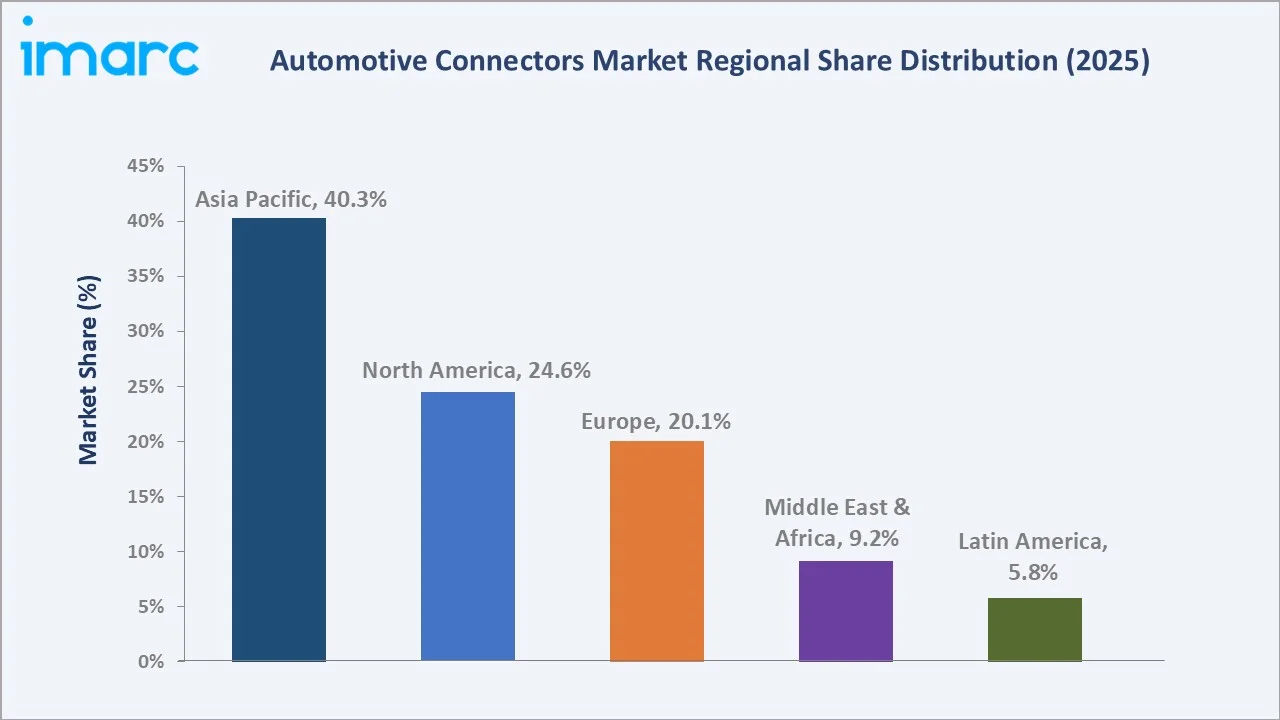

The global automotive connectors market size was valued at USD 14.80 Billion in 2025 and is projected to reach USD 23.30 Billion by 2034, exhibiting a CAGR of 5.05% during the forecast period 2026-2034. Accelerating electrification of global vehicle fleets, rapid expansion of advanced driver-assistance systems (ADAS), and rising electronic content per vehicle are the primary growth catalysts. Global electric vehicle sales surpassed 17 million units in 2024, per IEA data, each requiring 2-3x more connectors than a conventional ICE vehicle. PCB connectors dominate the connector type segment at 53.0% share in 2025, while sealed connector systems command 60.0% of system type revenue. Asia-Pacific leads all regions with 40.3% of global revenue in 2025, driven by China's vehicle production of approximately 31.3 million units annually.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 14.80 Billion |

|

Forecast Market Size (2034) |

USD 23.30 Billion |

|

CAGR (2026-2034) |

5.05% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (40.3% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Largest Connector Type |

PCB Connectors (53.0%, 2025) |

|

Leading System Type |

Sealed Connector System (60.0%, 2025) |

The chart below illustrates the global automotive connectors market growth trajectory from 2020 through 2034, contrasting historical expansion with a sustained forecast curve powered by EV proliferation, ADAS integration, and rising electronic content per vehicle.

To get more information on this market, Request Sample

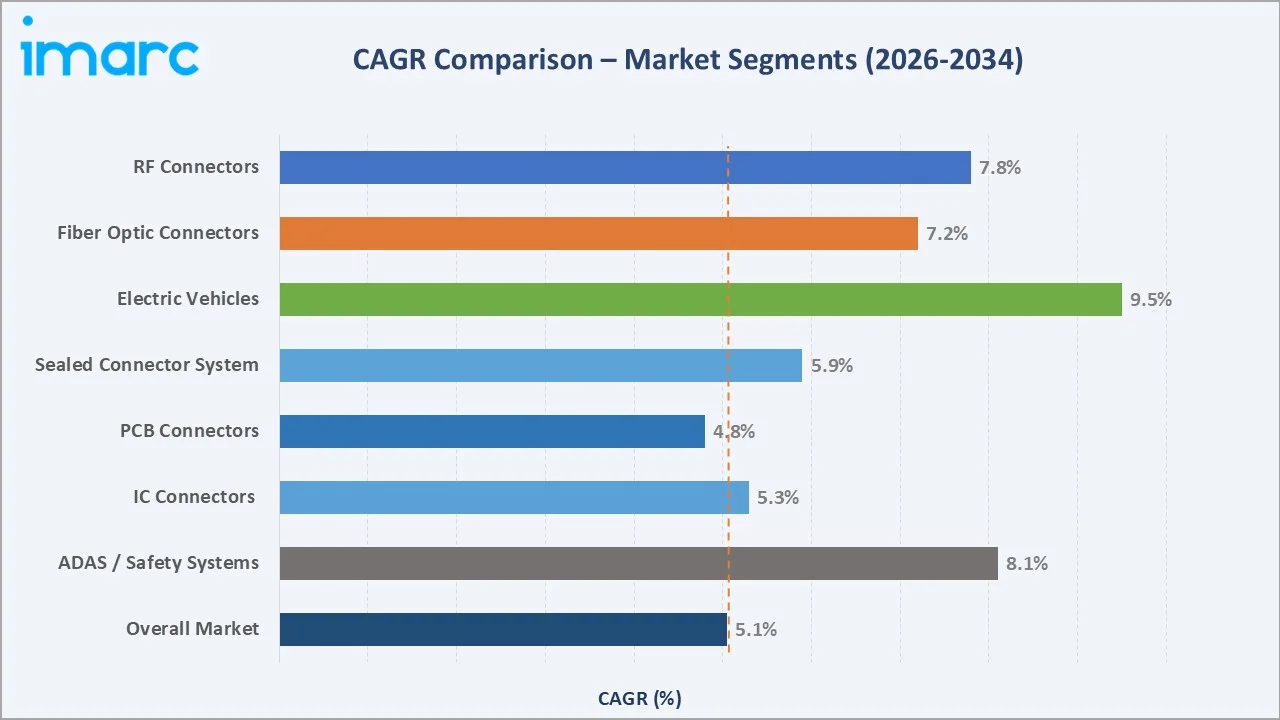

Segment-level CAGR comparisons below highlight the Electric Vehicles sub-segment and RF Connectors as the two fastest-growing categories within the global automotive connectors industry analysis through 2034.

Executive Summary

The global automotive connectors market is undergoing a structural transformation driven by the convergence of vehicle electrification, connected mobility, and ADAS proliferation. Valued at USD 14.80 Billion in 2025, the market is forecast to expand to USD 23.30 Billion by 2034 at a CAGR of 5.05%. The global transition to electric vehicles is the most powerful structural driver, with EV sales exceeding 17 million units in 2024, each vehicle demanding significantly more high-density, sealed connector solutions than conventional ICE vehicles. Automotive connector manufacturers are investing in miniaturised, high-voltage-rated products capable of handling 400V-800V EV powertrain architectures.

PCB Connectors command the dominant connector type share at 53.0% in 2025, driven by the proliferation of ECUs across body control, powertrain, safety, and infotainment modules. IC Connectors hold the second-largest share at 20.4%, underpinned by automotive semiconductor content growth projected to exceed USD 1,000 per vehicle by 2030. Sealed connector systems represent 60.0% of system type revenue in 2025, reflecting OEM preferences for IP67/IP69K-rated connections in engine bays, chassis, and EV battery packs exposed to moisture and vibration.

Asia-Pacific dominates with a 40.3% global revenue share in 2025, led by China's vehicle production exceeding 30 million units annually ((CAAM), Japan's world-class connector Tier-1 supplier base, and South Korea's expanding EV platform development. North America holds 24.6% share, bolstered by robust EV adoption and regulatory mandates on vehicle safety systems. In the United States, electric car sales increased to 1.6 million in 2024, with the sales share growing to more than 10%, Europe accounts for 20.1%, driven by stringent Euro 7 emission standards and premium automotive OEM density.

Key Market Insights

|

Insight |

Data |

|

Largest Connector Type |

PCB Connectors – 53.0% share (2025) |

|

Second Connector Type |

IC Connectors – 20.4% share (2025) |

|

Leading System Type |

Sealed Connector System – 60.0% share (2025) |

|

Leading Region |

Asia-Pacific – 40.3% revenue share (2025) |

|

Second Region |

North America – 24.6% revenue share (2025) |

|

Top Companies |

TE Connectivity, Aptiv, Amphenol, Yazaki, Molex, Sumitomo |

|

Market Opportunity |

EV high-voltage connectors, ADAS sensor wiring, 5G-V2X modules |

Key Analytical Observations Supporting the Above Data:

- PCB Connectors' 53.0% dominance in 2025 reflects the exponential increase in ECUs per vehicle. Modern premium vehicles now incorporate 70-100 ECUs, each requiring multiple PCB interconnect solutions.

- IC Connectors hold 20.4% share in 2025, driven by rapid automotive semiconductor content growth. Vehicle semiconductor value per unit is projected to exceed USD 1,000 by 2030, up from approximately USD 400 in 2020.

- Sealed Connector Systems' 60.0% leadership reflects the industry's response to automotive-grade IP67/IP69K environmental protection requirements for under-hood, chassis, and EV battery applications.

- Asia-Pacific's 40.3% regional dominance is anchored by China's vehicle production leadership of approximately 31.3 million units in 2024 and Japan's world-class Tier-1 connector supplier ecosystem.

- North America's 24.6% share in 2025 is increasingly driven by EV investments. The United States recorded over 1.4 million EV sales in 2024, generating disproportionate demand for high-voltage connector solutions.

- The Electric Vehicle segment presents the highest growth opportunity. Each BEV requires approximately 400-800 individual connector points versus 200-300 in a typical ICE vehicle, driving strong volume and ASP uplift.

Global Automotive Connectors Market Overview

Automotive connectors are precision electromechanical components that establish reliable electrical pathways between vehicle sub-systems, electronic control units, sensors, actuators, and power distribution networks within modern automobile architectures. They form the critical physical and electrical infrastructure of every vehicle's nervous system, enabling data communication, power delivery, and signal transmission across powertrains, chassis, safety systems, infotainment modules, and body electronics.

The industry ecosystem encompasses raw material suppliers, precision contact manufacturers, housing producers, connector assemblers, Tier-1 automotive suppliers, OEMs, and aftermarket distributors. Macro-economic enablers include the global acceleration of EV adoption, government-mandated ADAS integration, the growth of software-defined vehicles, and vehicle content electronics intensity growth – with average electronic content per vehicle rising from approximately USD 400 in 2020 to an estimated USD 800-plus by 2028.

Market Dynamics

To evaluate market opportunities, Request Sample

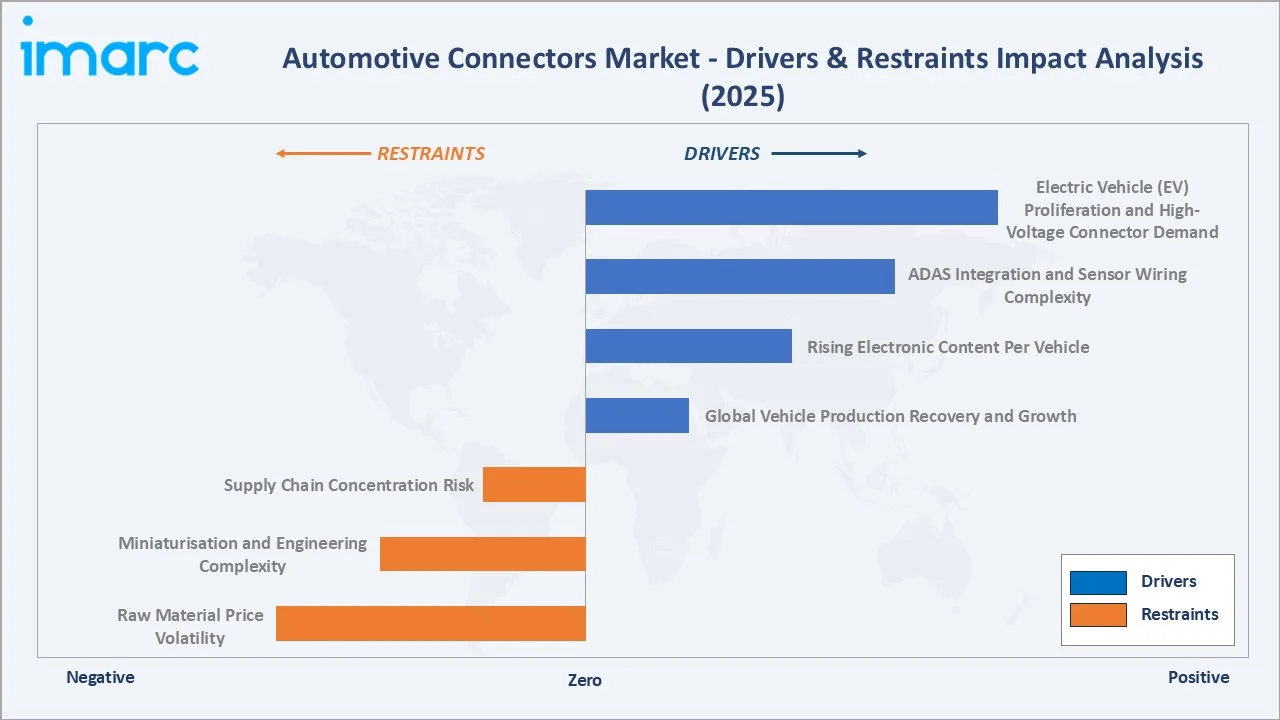

Market Drivers

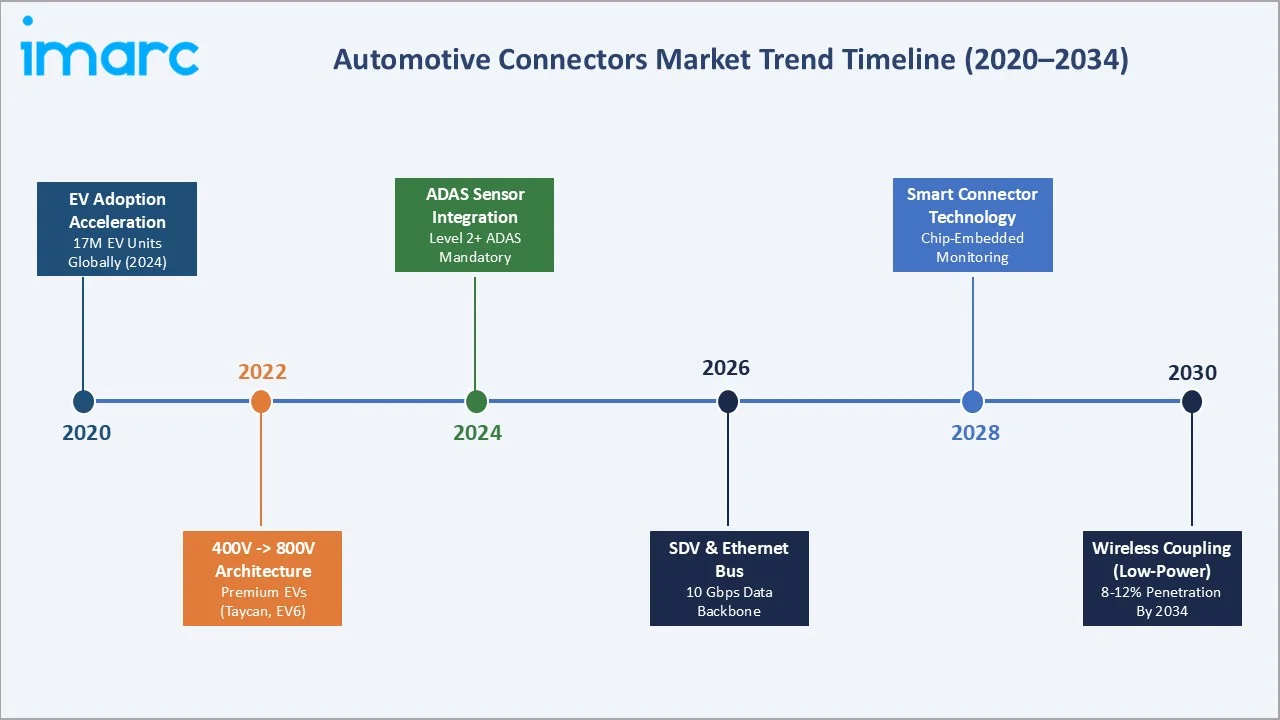

- Electric Vehicle (EV) Proliferation and High-Voltage Connector Demand: Global EV sales exceeded 17 million units in 2024, marking a 25%-plus increase versus 2023. Each battery electric vehicle requires 3-4x more connector points than a comparable ICE vehicle, with specific demand for 800V-rated, thermally-managed, sealed high-voltage connector systems for battery packs, charging inlets (CCS2, NACS), and inverter interconnects.

- ADAS Integration and Sensor Wiring Complexity: Modern level 2+ vehicles incorporate 8-12 radar sensors, 4-8 cameras, 3-5 LiDAR units, and 12-plus ultrasonic sensors, each requiring individual shielded connector harnesses. The global ADAS and autonomous driving component market is valued at USD 33.5 Billion in 2024 and it is projected to reach USD 83.6 Billion by 2032, with a direct correlation to connector demand growth.

- Rising Electronic Content Per Vehicle: Average electronics content per vehicle has grown from approximately USD 400 in 2020 to USD 650 in 2025 and is forecast to exceed USD 1,000 by 2030. This growth directly drives connector volume and specification escalation across all vehicle segments.

- Global Vehicle Production Recovery and Growth: Global automobile production reached approximately 92.5 million units in 2024. Commercial vehicle production growth in Asia-Pacific, coupled with premium vehicle penetration in North America and Europe, sustains baseline connector demand across all segments.

Market Restraints

- Raw Material Price Volatility: Automotive connectors are copper-intensive components, with copper prices exhibiting 20-35% annual price swings in recent years. Platinum-group metals used in high-reliability contact plating further compound raw material cost instability, compressing manufacturer margins.

- Miniaturisation and Engineering Complexity: The simultaneous demand for higher data transmission speeds (up to 10 Gbps for automotive Ethernet), higher current capacity (up to 250A for HV connectors), and reduced physical footprints creates significant engineering and manufacturing challenges.

- Supply Chain Concentration Risk: Over 60% of precision connector contact stamping capacity is concentrated in Japan, Taiwan, and China, creating geopolitical and logistics disruption risks that remain a structural concern for global OEM procurement.

Market Opportunities

- 800V Architecture and Ultra-Fast Charging Connector Innovation: The industry shift from 400V to 800V EV battery architectures requires entirely new high-voltage connector families. Connector manufacturers able to deliver 800V-rated, IP69K-sealed solutions face multi-billion-dollar addressable market expansion over the forecast period.

- Vehicle-to-Everything (V2X) Communication and Antenna Connector Integration: 5G-V2X connectivity mandates across the EU and rollouts in China and the United States are driving demand for precision RF and coaxial connector solutions integrated into vehicle communication antennas and DSRC modules.

- Software-Defined Vehicle (SDV) Architecture: Central compute-based vehicle architectures replacing distributed ECUs with 2-4 domain computers require ultra-high-speed backplane connector solutions capable of 25-100 Gbps throughput for real-time autonomous driving data processing.

Market Challenges

- Standardisation Gaps in EV Charging Protocols: Competing standards (CCS, NACS, CHAdeMO, GB/T) across geographic markets force connector manufacturers to maintain multiple product families, fragmenting economies of scale and increasing tooling and certification costs.

- EMC Compliance in High-Density Electronic Environments: As vehicle ECU density and switching frequencies increase, ensuring connector-level EMC shielding effectiveness at 10 GHz and above represents a growing technical and cost challenge.

- Skilled Workforce and Precision Manufacturing Capacity: Automotive connector manufacturing requires sub-micron precision in contact stamping, plating, and assembly. Global competition for skilled precision manufacturing technicians is intensifying, particularly in high-growth EV markets.

Emerging Market Trends

1. High-Voltage Connector Architecture for 800V EV Platforms

The industry's shift from 400V to 800V battery architectures, enabling 350 kW ultra-fast charging and reducing charge times below 20 minutes, is driving demand for a new generation of HV connectors. Manufacturers including TE Connectivity and Aptiv are commercialising 800V-rated connector families with integrated thermal management, vibration resistance, and IP69K protection. This trend is expected to become mainstream across mid-premium vehicle segments by 2028.

2. Miniaturised High-Speed Connectors for Automotive Ethernet and LiDAR

Automotive Ethernet adoption supporting 100 Mbps, 1 Gbps, and 10 Gbps data rates for ADAS sensor data buses is driving demand for miniaturised HSD and FAKRA connector solutions. LiDAR sensor proliferation in level 3-plus autonomous vehicles adds incremental demand for precision RF coaxial interconnects capable of signal integrity at multi-gigahertz frequencies across minus 40 to plus 125 degrees Celsius temperature ranges.

3. Wireless Connector Alternatives and Inductive Coupling

Emerging wireless inductive coupling technologies are beginning to replace physical connectors in select vehicle applications, primarily infotainment smartphone charging pads and some interior lighting control modules. While penetration remains below 5% of total connector points in 2025, the technology is expected to expand to approximately 8-12% by 2034 in non-critical low-power signal applications.

4. Integrated Sealed Connector Systems for EV Waterproofing Requirements

IP67 and IP69K waterproofing standards, formerly limited to exterior lighting and under-hood applications, are now being specified for virtually all connector applications in electric and hybrid vehicles. This mandatory sealing upgrade is driving connector ASP escalation estimated at 15-25% per unit across the EV connector portfolio versus equivalent ICE connector specifications.

5. Circular Economy and Recyclable Connector Materials

EU End-of-Life Vehicle regulations and OEM sustainability commitments are driving the development of automotive connectors using bio-sourced polyamide housings and recycled-content copper alloy contacts. Molex and Amphenol have both disclosed 2030 sustainability roadmaps targeting 30-40% recycled material integration in automotive connector housings, responding to OEM supply chain sustainability audit requirements.

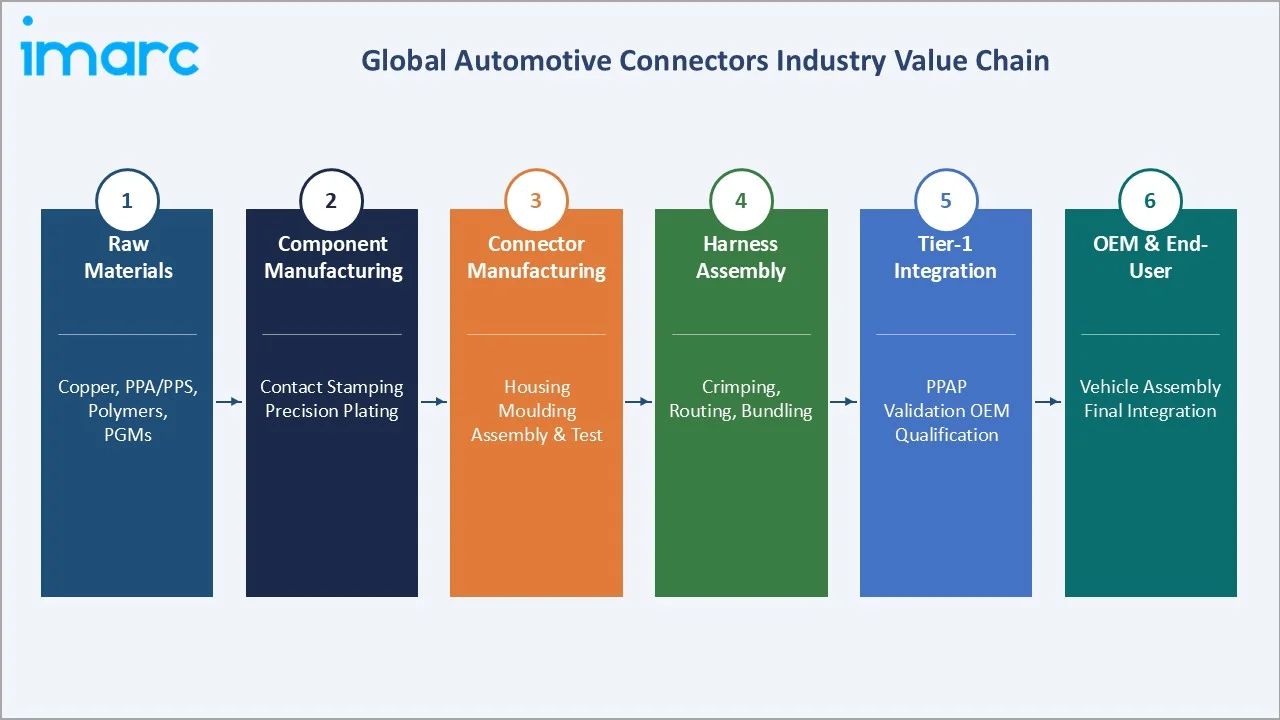

Industry Value Chain Analysis

The automotive connectors value chain spans six integrated stages from raw material supply through end-vehicle delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements that shape industry competitiveness and supply chain resilience.

|

Stage |

Key Players / Examples |

Key Activities |

|

Raw Materials |

Wieland-Werke, Aurubis, Sumitomo Metal Mining, Umicore |

Copper alloy strip, PGM plating materials, high-temp polymer compounds |

|

Component & Contacts |

Precision Parts Corp, Samtec, JAE, Hirose |

Contact stamping, precision plating, spring-force calibration, testing |

|

Connector Manufacturing |

TE Connectivity, Amphenol, Molex, Aptiv, Yazaki, Sumitomo |

Housing moulding, contact insertion, sealing assembly, overmoulding |

|

Harness Assembly |

Yazaki, Sumitomo Wiring, Delphi Technologies, Lear Corp |

Harness integration, connector crimping, bundling, routing design |

|

Tier-1 System Integration |

Aptiv, Bosch, Continental, Denso, Valeo |

System-level validation, OEM specification compliance, PPAP approval |

|

OEM / End-User |

Toyota, Volkswagen, GM, BMW, Tesla, Hyundai, Stellantis |

Vehicle assembly, subsystem integration, final quality validation |

The value chain illustration below maps the flow of components and finished connectors from raw material extraction through vehicle integration, highlighting the key players and value-add activities at each stage.

Technology Landscape in the Automotive Connectors Industry

The technology landscape is defined by four interrelated innovation vectors: high-voltage power management, precision signal integrity, environmental sealing, and digital/smart connectivity.

High-Voltage Power Technology

The transition to 400V and 800V EV battery architectures has necessitated entirely new connector contact and housing material platforms. High-voltage automotive connectors now incorporate copper-beryllium alloy contacts with 15-25 N contact normal force, integrated thermal management chambers, and plastic housings from polyphthalamide (PPA) or polyphenylene sulphide (PPS) rated for continuous 150 degrees Celsius operation. TE Connectivity's MPC series supports up to 250A continuous current with IP67 sealing.

Signal Integrity and EMC Shielding

Automotive Ethernet (100BASE-T1, 1000BASE-T1, 10GBASE-T1) connectivity for ADAS and central compute architectures requires connector solutions maintaining below minus 40 dB insertion loss and above 30 dB crosstalk isolation across 0 to 10 GHz frequency ranges. Shielded FAKRA-Z and HSD4+ connector formats are the leading standards, with Rosenberger Group and Amphenol leading the precision RF automotive connector category.

Environmental Sealing and Durability Innovation

IP69K sealing, resistance to high-pressure steam cleaning at 80 bar and 80 degrees Celsius, has become a baseline requirement for EV underbody and battery connector applications. Silicone-based cavity seals, overmoulded wire seal technologies, and integrated flap-seal designs from manufacturers such as Aptiv and Rosenberger now enable IP69K-compliant connector families at mounting densities previously achievable only with unsealed alternatives.

Smart and Connected Connector Technologies

Emerging smart connector technologies integrate microelectronics directly into connector housings for real-time impedance monitoring, thermal condition sensing, and CAN bus error logging. Qualcomm and NXP semiconductor solutions are enabling chip-in-connector architectures targeting predictive maintenance applications in commercial vehicle fleets. Industry forecasts suggest smart connector penetration reaching 8-12% of premium vehicle connector BOM value by 2032.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Connection Type |

🔒 |

🔒 |

2025 |

|

Connector Type |

PCB Connectors |

53.0% |

2025 |

|

System Type |

Sealed Connector System |

60.0% |

2025 |

|

Vehicle Type |

🔒 |

🔒 |

2025 |

| Application | Safety and Security System | 25.6% | 2025 |

|

Region |

Asia Pacific |

40.3% |

2025 |

By Connector Type

To access detailed market analysis, Request Sample

|

Connector Type |

Share (2025) |

Key Growth Driver |

|

PCB Connectors |

53.0% |

ECU proliferation; 70-100 control units per modern premium vehicle |

|

IC Connectors |

20.4% |

Automotive semiconductor content growth; projected USD 1,000+ per vehicle by 2030 |

|

RF Connectors |

13.8% |

ADAS radar/camera sensor wiring; 5G-V2X antenna integration |

|

Fiber Optic Connectors |

8.2% |

MOST bus infotainment networks; high-bandwidth data backbones in EVs |

|

Others |

4.6% |

Circular connectors, power connectors, specialty sealed harness connectors |

PCB Connectors lead all connector type categories with 53.0% share in 2025, reflecting the explosion of ECUs in modern vehicles. IC Connectors hold 20.4%, driven by rapid semiconductor content escalation. RF Connectors at 13.8% represent the fastest-growing type on a percentage basis, fuelled by ADAS radar and camera integration and emerging 5G-V2X connectivity mandates. Fiber Optic Connectors at 8.2% serve premium infotainment MOST networks and high-bandwidth EV data architectures.

By System Type

|

System Type |

Share (2025) |

Key Application |

|

Sealed Connector System |

60.0% |

Engine bay, chassis, EV battery packs, exterior lighting, underbody components |

|

Unsealed Connector System |

40.0% |

Interior cabin electronics, infotainment, instrument cluster, HVAC controls |

Sealed Connector Systems command a dominant 60.0% of the system type segment in 2025. Mandatory IP67/IP69K sealing requirements for EV powertrain, battery, and exterior connector applications are the primary growth accelerator. The growing proportion of EVs in global production is progressively shifting the sealed-to-unsealed ratio toward greater sealed connector penetration through the forecast period.

Regional Market Insights

|

Region |

Share (2025) |

Market Size (2025) |

Key Driver |

|

Asia-Pacific |

40.3% |

~USD 5.97B |

China vehicle production ~30M units; Japan Tier-1 supplier density |

|

North America |

24.6% |

~USD 3.64B |

EV adoption; ADAS mandates; US IRA EV incentive programs |

|

Europe |

20.1% |

~USD 2.97B |

Euro 7 regulations; premium OEM EV electrification programs |

|

Middle East and Africa |

9.2% |

~USD 1.36B |

Vehicle production localisation; infrastructure investments |

|

Latin America |

5.8% |

~USD 0.86B |

Brazil and Mexico vehicle assembly expansion; Mercosur trade |

Asia-Pacific (40.3% Share, 2025)

Asia-Pacific is the dominant global region accounting for 40.3% of market revenue in 2025. China alone produces approximately 31 million vehicles annually, and Japan's connector supply ecosystem anchored by Yazaki, Sumitomo Wiring Systems, JAE, and Hirose generates exceptional vertical integration efficiency. South Korea's rapid EV platform expansion through Hyundai and Kia's 800V architecture platforms drives premium connector demand growth in the region.

North America (24.6% Share, 2025)

North America holds 24.6% of global revenue in 2025, with the United States market increasingly shaped by the Inflation Reduction Act's USD 7,500 EV tax credit. US EV sales exceeded 1.6 million units in 2024. Ford, GM, and Tesla's combined EV investment exceeds USD 50 billion through 2030, directly driving high-voltage connector procurement growth. Regulatory mandates for automatic emergency braking in all US light vehicles by 2027 provide additional structural connector demand.

Europe (20.1% Share, 2025)

Europe accounts for 20.1% of market revenue, driven by the EU's Euro 7 emission standards and the mandate for all new cars sold to be zero-emission from 2035. Germany remains the largest individual market, with its automotive sector investing over EUR 50 billion annually in electrification and digitisation. The EU's world-class premium OEM density including Volkswagen, BMW, Mercedes-Benz, Stellantis, and Renault sustains technical connector specification escalation.

Middle East and Africa (9.2% Share, 2025)

The Middle East and Africa region holds 9.2% of market revenue, with growth supported by vehicle production localisation initiatives in Morocco, South Africa, and Egypt. Saudi Arabia's Vision 2030 program includes automotive manufacturing incentives. Saudi Arabia and UAE vehicle fleet electrification programmes, including a target for 30% EV share in the national fleet, represent emerging connector demand opportunities.

Latin America (5.8% Share, 2025)

Latin America represents 5.8% of revenue, with Brazil and Mexico constituting the two primary markets. Mexico benefits from proximity to US OEM assembly plants and USMCA preferential tariff arrangements, supporting a domestic automotive parts manufacturing base. Brazil's flex-fuel vehicle production programme and Mercosur trade framework sustain stable mid-volume connector demand across passenger car and commercial vehicle segments.

Competitive Landscape

The global automotive connectors market exhibits a moderately consolidated competitive structure. The top 5 players – TE Connectivity, Aptiv, Amphenol, Yazaki, and Sumitomo Wiring Systems – are estimated to account for approximately 55-65% of global revenue in 2025. TE Connectivity and Aptiv lead through comprehensive product portfolios, deep OEM qualification relationships, and global manufacturing footprints. Japanese players Yazaki and Sumitomo dominate wiring harness-integrated connector supply in Asia-Pacific. Amphenol and Molex compete on high-performance RF and PCB connector specialisations respectively.

|

Company Name |

Brand / Known For |

Competitive Position |

|

TE Connectivity |

AMP / AMPSEAL, PicoMQS system |

Market Leader – broadest automotive connector portfolio globally |

|

Aptiv PLC |

APEX, METRI-PACK, Weather-Pack, SICMA, and HES |

Leader – wiring architecture and HV EV connector systems |

|

Amphenol Corporation |

Amphenol RF |

Leader – RF, fiber optic, and high-reliability connector specialist |

|

Yazaki Corporation |

Yazaki |

Leader – wiring harness and connector integration, dominant in Asia |

|

Molex LLC (Koch) |

KK (wire-to-board), Mizu (sealed), EXTreme Power (high-current), and Quad-Row (high-density) |

Challenger – PCB, IC, and miniaturised connector specialisations |

|

Sumitomo Wiring Systems |

TS Series Sealed 0.64mm Type Connector, Sealed 153way connector |

Leader – harness-integrated connector supply, strong Asia base |

|

Hirose Electric Co. |

Hirose HR Series |

Challenger – miniaturised high-reliability connectors, Japan OEM |

|

Rosenberger Group |

Rosenberger RF |

Emerging – premium RF/HSD connectors for ADAS sensor wiring |

|

JAE |

Board-to-board connectors, Board-FPC/FFC connectors |

Emerging – board-to-board and fine-pitch automotive connectors |

|

Kyocera AVX |

KYOCERA AVX |

Emerging – ceramic and capacitive connector components for EV/ADAS |

|

Lumberg Holding GmbH |

Lumberg |

Niche – modular connector systems for body and chassis applications |

The competitive positioning matrix below maps leading players on portfolio breadth versus technology strength, with bubble size reflecting estimated global market share percentage in 2025.

Key Company Profiles

TE Connectivity

- Company Overview: TE Connectivity is a global industrial technology leader generating approximately USD 15 Billion in annual revenues (FY2024), with the Automotive segment representing over 40% of group revenues. The company employs approximately 90,000 associates across 140 countries and maintains the industry's broadest certified automotive connector portfolio spanning PCB, power, RF, fiber optic, and high-voltage EV connector families.

- Product Portfolio: TE's automotive connector portfolio encompasses PCB connectors, power connectors (up to 250A), sealed and unsealed harness connectors, FAKRA and HSD RF connectors, fiber optic connectors, and EV high-voltage charging connectors supporting CCS2, NACS, and CHAdeMO standards.

- Recent Developments: TE announced expanded 800V EV high-voltage connector production capacity in 2024-2025, with new manufacturing facilities in Germany and China. The company launched its next-generation MPC family targeting 250A-rated EV battery pack applications.

- Strategic Focus: TE's strategic focus centres on EV electrification connectivity, ADAS sensor wiring systems, and central compute architecture interconnects for software-defined vehicles.

Aptiv PLC

- Company Overview: Aptiv, formerly Delphi Technologies, generated USD 19.7 Billion in revenues in 2024. The company's Signal & Power Solutions segment is the world's largest producer of automotive wiring harness systems and integrated connector solutions, with manufacturing operations across 45 countries and supply relationships with virtually every global OEM.

- Product Portfolio: Aptiv's connector portfolio focuses on high-voltage EV connectors, shielded ADAS sensor connectors, HVIL systems, wire-to-board and board-to-board connectors, and sealed connector housings certified to IP67 and IP69K environmental standards.

- Recent Developments: Aptiv secured multi-year EV platform connector supply agreements with GM and Stellantis in 2023-2025. The company expanded its Central Science innovation centre to accelerate software-defined vehicle wiring architecture development and zone-based connector solutions.

- Strategic Focus: Aptiv's strategic focus is on intelligent vehicle architectures, enabling the transition from distributed ECU wiring to zone-based and central-compute connector architectures for next-generation electric and autonomous vehicles.

Amphenol Corporation

- Company Overview: Amphenol Corporation generated USD 14.8 Billion in total revenues in 2024, with its Automotive and Industrial Electronics division representing a significant and growing revenue share. The company is internationally recognised for high-reliability, precision RF, coaxial, and fiber optic connector solutions across defence, automotive, and industrial markets.

- Product Portfolio: Amphenol's automotive connector portfolio spans RF coaxial connectors (FAKRA, Mini-FAKRA), fiber optic connectors, sealed PCB connectors, EV charging connectors, and industrial-grade sealed connectors for ADAS and telematics applications requiring extreme reliability.

- Recent Developments: Amphenol completed the acquisition of majority ownership in Carlisle Interconnect Technologies in 2024, strengthening its position in high-reliability defence and automotive electronics connectors. The company also expanded manufacturing operations in Mexico and India.

- Strategic Focus: Amphenol's strategic emphasis is on next-generation ADAS and autonomous vehicle sensor connectivity, high-frequency signal integrity solutions, and fiber optic harness integration for premium and EV vehicle segments globally.

Yazaki Corporation

- Company Overview: Yazaki Corporation is a Japanese private conglomerate and the world's second-largest automotive wiring harness manufacturer, with estimated revenues exceeding USD 14 Billion and operations across 45 countries. The company has supply relationships with virtually every major global OEM and a particularly dominant position in Asia-Pacific and European market segments.

- Product Portfolio: Yazaki's connector product range is deeply integrated with its wiring harness systems business, encompassing sealed and unsealed wire-to-wire, wire-to-board connectors, EV high-voltage connectors, and OBD diagnostic interface connectors across all vehicle categories.

- Recent Developments: Yazaki announced significant investments in EV harness and connector production facilities in Vietnam and Mexico in 2023-2024, positioning for EV production ramp-ups by Asian OEMs and North American EV assembly operations under IRA-qualifying supply chains.

- Strategic Focus: Yazaki's strategy centres on maintaining its dominant wiring harness-integrated connector supply position while aggressively expanding EV-specific high-voltage connector production to serve global OEM electrification programmes.

Molex LLC (Koch Industries)

- Company Overview: Molex, a wholly-owned subsidiary of Koch Industries since 2013, is a leading global connector manufacturer with estimated automotive division revenues exceeding USD 4 Billion. The company is particularly strong in miniaturised PCB, IC, and high-density connector applications for automotive ECU and body electronics segments.

- Product Portfolio: Molex's automotive connector portfolio includes Micro-Fit, Mini-Fit, and Nano-Fit PCB connectors, MX150 sealed connectors, CLIK-Mate board-to-board connectors, automotive-grade USB and power delivery connectors, and EV-charging interface solutions.

- Recent Developments: Molex launched its next-generation EV powertrain connector platform in 2024, specifically engineered for 800V battery architectures, and expanded its automotive technology centre in Maumee, Ohio to accelerate EV connector design validation and OEM qualification.

- Strategic Focus: Molex's strategic priority is capturing the high-growth EV connector segment while maintaining leadership in miniaturised, high-density PCB connector solutions for increasingly compact automotive ECU form factors in software-defined vehicle platforms.

Market Concentration Analysis

The global automotive connectors market exhibits moderate-to-high concentration at the global level. The top 5 players – TE Connectivity, Aptiv, Amphenol, Yazaki, and Sumitomo Wiring Systems – collectively account for approximately 55-65% of total global revenue in 2025. This concentration reflects the significant capital investment required for automotive-grade connector tooling, the multi-year OEM qualification and PPAP approval processes, and the supply chain integration requirements of wiring harness manufacturers that create high switching costs.

The remaining 35-45% of market share is distributed among approximately 200-plus regional and specialist connector manufacturers, with a higher fragmentation level in Asia-Pacific where Japanese, Chinese, South Korean, and Taiwanese regional players serve domestic OEM programmes. The RF and fiber optic connector sub-segments exhibit the highest fragmentation, with specialist players including Rosenberger, JAE, and Hirose competing effectively against the portfolio majors.

Consolidation trends are actively shaping the competitive landscape. TE Connectivity, Amphenol, and Molex have collectively completed approximately 15 acquisitions between 2020-2025. The EV transition is expected to accelerate consolidation as smaller connector manufacturers lacking capital to develop 800V-rated product families are acquired or exit. The Herfindahl-Hirschman Index (HHI) for the global automotive connectors market is estimated at 1,200-1,500, indicating moderate market concentration with a trajectory toward moderate-high over the 2026-2034 forecast period.

Investment & Growth Opportunities

Fastest Growing Segments

- Electric Vehicle High-Voltage Connectors: The highest CAGR sub-segment within the market. EV penetration in global vehicle production is projected to grow from approximately 20% in 2025 to 40-50% by 2034, with each EV requiring 300-800 connector points in high-voltage applications alone.

- RF Connectors for ADAS Sensor Integration: Regulatory mandates for AEB, LKA, and blind spot monitoring across EU, US, and China markets drive structural demand for precision FAKRA and Mini-FAKRA RF connector solutions at a forecast CAGR exceeding 8% through 2034.

- Fiber Optic Connectors for High-Bandwidth Data: Software-defined vehicle architectures requiring 10 Gbps-plus data throughput for central compute platforms are driving fiber optic connector demand from niche infotainment MOST applications to broader vehicle backbone data bus applications.

Emerging Markets with High Growth Potential

- India: The Indian automotive market is projecting production of 7.5 million vehicles annually by 2030, with increasing electronics content driven by mandatory ABS, airbag, and OBD requirements. Global connector players including Sumitomo and Aptiv are expanding Indian manufacturing investments.

- Southeast Asia: Thailand, Vietnam, and Indonesia are expanding as both vehicle assembly hubs and connector manufacturing locations. EV adoption in Thailand and Vietnam is accelerating connector technology upgrade cycles significantly.

- Middle East: Saudi Arabia and UAE vehicle fleet electrification programmes, including Saudi Vision 2030's 30% EV fleet share target, represent emerging demand opportunities for EV connector suppliers entering the region.

Venture Investment and Technology Funding Trends

- Smart Connector Technology: Start-ups developing chip-embedded connector solutions for predictive maintenance have attracted cumulative venture investment exceeding USD 200 Million between 2022-2025.

- Wireless Charging Infrastructure Connectors: Inductive charging technology for EVs, including SAE J2954-compliant wireless charging systems, has received over USD 300 Million in strategic investment from automotive OEMs and charging infrastructure operators since 2022.

- Sustainable Materials Innovation: EU ELV Regulation compliance is driving material science funding in bio-based polymer connector housing development, with BASF and Lanxess investing in automotive-grade bio-polyamide compound programmes targeting 2030 commercialisation.

Future Market Outlook (2026-2034)

The global automotive connectors market is projected to expand from USD 14.80 Billion in 2025 to USD 23.30 Billion by 2034, representing cumulative absolute value creation of approximately USD 8.5 Billion. The 5.05% CAGR reflects a structurally healthy growth environment underpinned by three irreversible megatrends: vehicle electrification, autonomous and connected vehicle technology integration, and the software-defined vehicle architecture transition.

EV high-voltage connector solutions are expected to grow from approximately 20% of total connector market revenue in 2025 to 35-40% by 2034, becoming the single largest application category and displacing traditional ICE engine management connectors. The 800V architecture transition will drive significant average selling price escalation across high-voltage connector product families, partially offsetting any unit volume softness in ICE vehicle production through the forecast period.

Asia-Pacific will reinforce its leadership position through 2034, with China's EV production dominance and India's rising vehicle electronics content driving incremental regional share gains. North America's share is forecast to expand modestly from 24.6% to approximately 27% by 2034, supported by onshoring of EV battery and vehicle production under the Inflation Reduction Act. Europe will maintain its 20% share range, with Euro 7 compliance and the 2035 zero-emission mandate sustaining technical connector specification escalation among premium OEMs.

Technological disruption risks include the gradual penetration of wireless inductive coupling in low-power interior applications, estimated to impact minus 2-3 percentage points of wired connector volume growth by 2034. However, the near-term trajectory through 2030 is unequivocally driven by the connector-intensive nature of EV and ADAS platforms that fundamentally require physical, high-reliability, environmentally-sealed electrical connections.

Research Methodology

Primary Research

IMARC Group's primary research for this report encompasses structured interviews and surveys conducted with 150-plus industry stakeholders across the automotive connector value chain, including connector manufacturer product managers and R&D engineers, automotive OEM procurement and engineering executives, Tier-1 supplier wiring harness technical directors, automotive electronics aftermarket distributors, and industry association representatives from CLEPA, ACEA, and JAMA member organisations.

Secondary Research

Secondary research sources include annual reports and investor presentations from leading connector manufacturers (TE Connectivity, Aptiv, Amphenol, Molex), regulatory filings and automotive production statistics from OICA, IEA EV Outlook, ACEA, SIAM, SMMT, SAE International technical standards databases, government trade databases including ITC Trade Statistics and Eurostat COMEXT, and proprietary IMARC Group industry databases updated through Q1 2026.

Market Estimation and Forecasting Models

Market sizing employs a bottom-up methodology building market revenue estimates from individual application segment connector content values per vehicle, multiplied by regional production volumes across vehicle types, cross-validated against a top-down approach using total automotive electronics market values and connector-to-electronics content ratios. Forecast models incorporate regression analysis against macroeconomic variables including GDP growth, vehicle production forecasts, EV penetration rates, and semiconductor content per vehicle trends. All data is subject to IMARC Group's three-stage quality assurance validation process.

Automotive Connectors Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Connection Types Covered | Wire to Wire Connection, Wire to Board Connection, Board to Board Connection |

| Connector Types Covered | PCB Connectors, IC Connectors, RF Connectors, Fiber Optic Connectors, Others |

| System Types Covered | Sealed Connector System, Unsealed Connector System |

| Vehicle Types Covered |

|

| Applications Covered | Body Control and Interiors, Safety and Security System, Engine Control and Cooling System, Fuel and Emission Control, Infotainment, Navigation & Instrumentation, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | TE Connectivity, Aptiv PLC, Amphenol Corporation, Yazaki Corporation Molex LLC (Koch), Sumitomo Wiring Systems, Hirose Electric Co., Rosenberger Group, JAE, Kyocera AVX, Lumberg Holding GmbH, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive connectors market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global automotive connectors market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive connectors industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive Connectors Market Report

The global automotive connectors market was valued at USD 14.80 Billion in 2025, covering all connector types across passenger cars, commercial vehicles, and electric vehicles worldwide.

The market is projected to reach USD 23.30 Billion by 2034, growing at a CAGR of 5.05% between 2026 and 2034, driven by EV proliferation, ADAS integration, and rising electronic content per vehicle.

PCB Connectors lead the market with a 53.0% share in 2025, driven by the exponential growth of electronic control units per vehicle – modern premium vehicles incorporate 70-100 individual ECUs.

Sealed Connector Systems (60.0% share, 2025) provide IP67-IP69K environmental protection for under-hood and EV applications; unsealed systems serve interior cabin electronics with lower protection requirements.

Asia-Pacific dominates with a 40.3% revenue share in 2025, led by China's vehicle production volume of approximately 30 million units annually and Japan's world-class Tier-1 connector supplier ecosystem.

Key drivers include EV platform proliferation (17 million EV sales in 2024), ADAS sensor integration mandates, rising electronic content per vehicle (projected USD 1,000-plus by 2030), and 5G-V2X connectivity rollouts.

Electric Vehicles exhibit the fastest growth trajectory, requiring 2-3x more connector units than comparable ICE vehicles, especially for high-voltage powertrain and battery pack applications.

Leading companies include TE Connectivity, Aptiv, Amphenol, Yazaki, Molex, Sumitomo Wiring Systems, Hirose Electric, JAE, Rosenberger Group, Kyocera AVX, and Lumberg Holding GmbH.

The shift to 800V architectures requires new sealed, thermally-managed high-voltage connector families rated for 250A-plus, driving 15-25% ASP premiums versus ICE connector equivalents across the EV portfolio.

The market is moderately concentrated; top 5 players hold approximately 55-65% of global revenue, with the Herfindahl-Hirschman Index estimated at 1,200-1,500 in 2025 with a consolidation trajectory.

The report covers six segmentation dimensions: Connection Type, Connector Type, System Type, Vehicle Type, Application, and Region, with 2020-2025 historical and 2026-2034 forecast data included.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)