Automotive Differential Market Size, Share, Trends and Forecast by Type, Drive Type, Vehicle, Component, Vehicle Propulsion Type, and Region, 2026-2034

Global Automotive Differential Market Size, Share, Trends & Forecast (2026-2034)

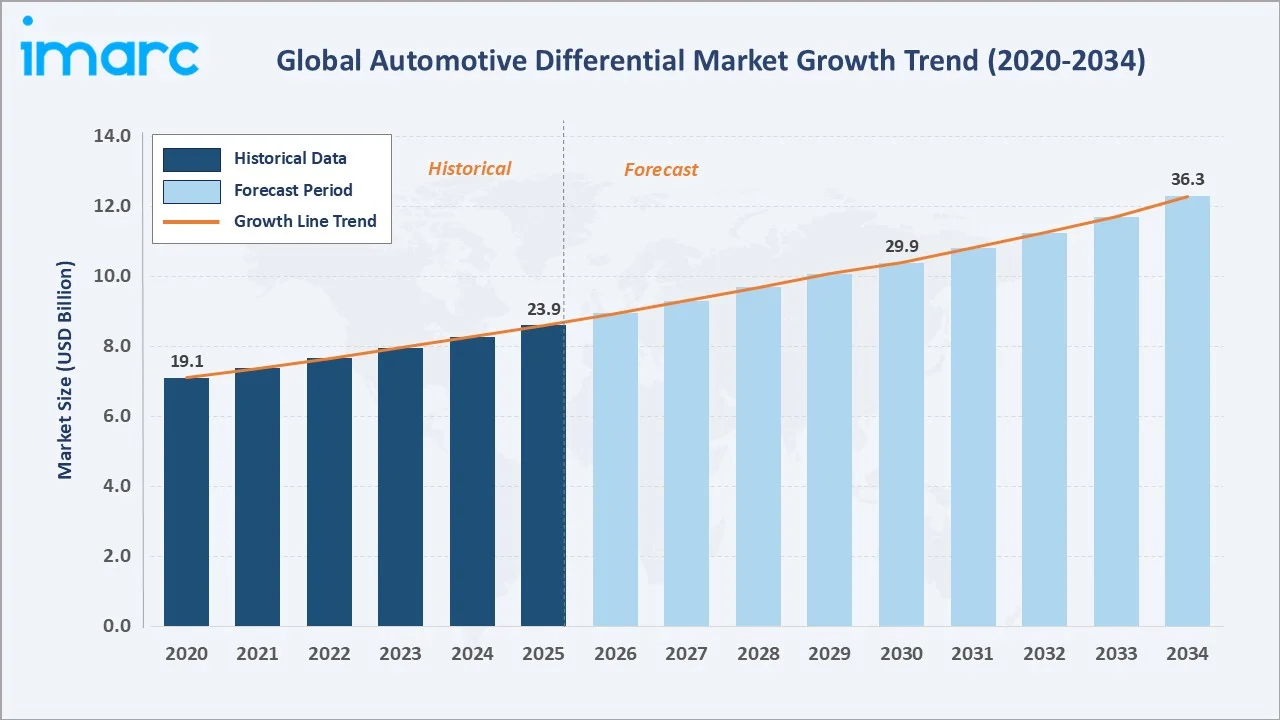

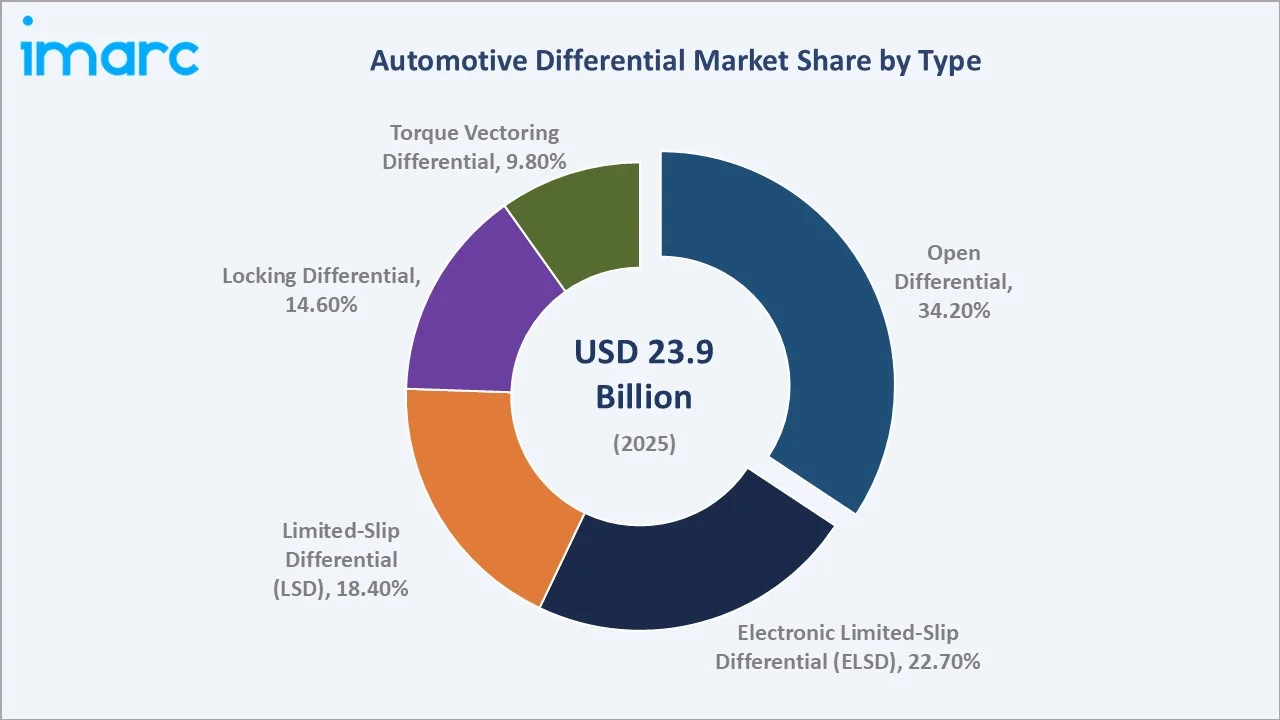

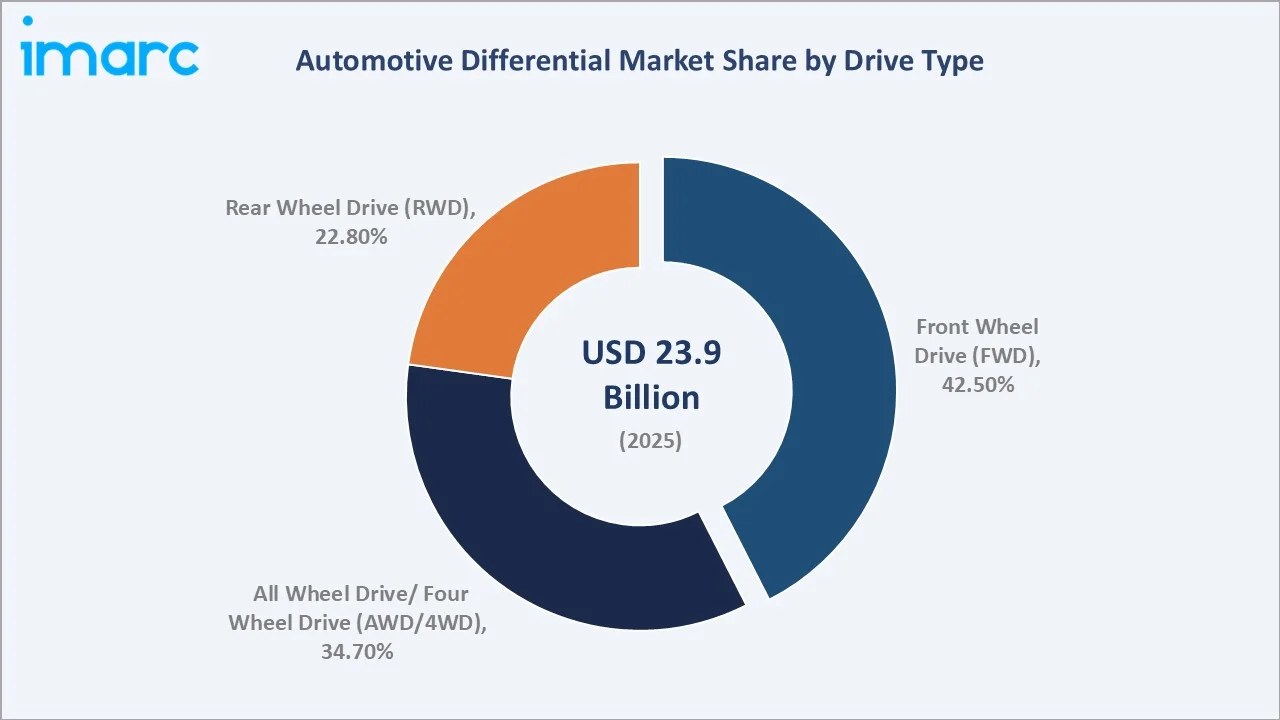

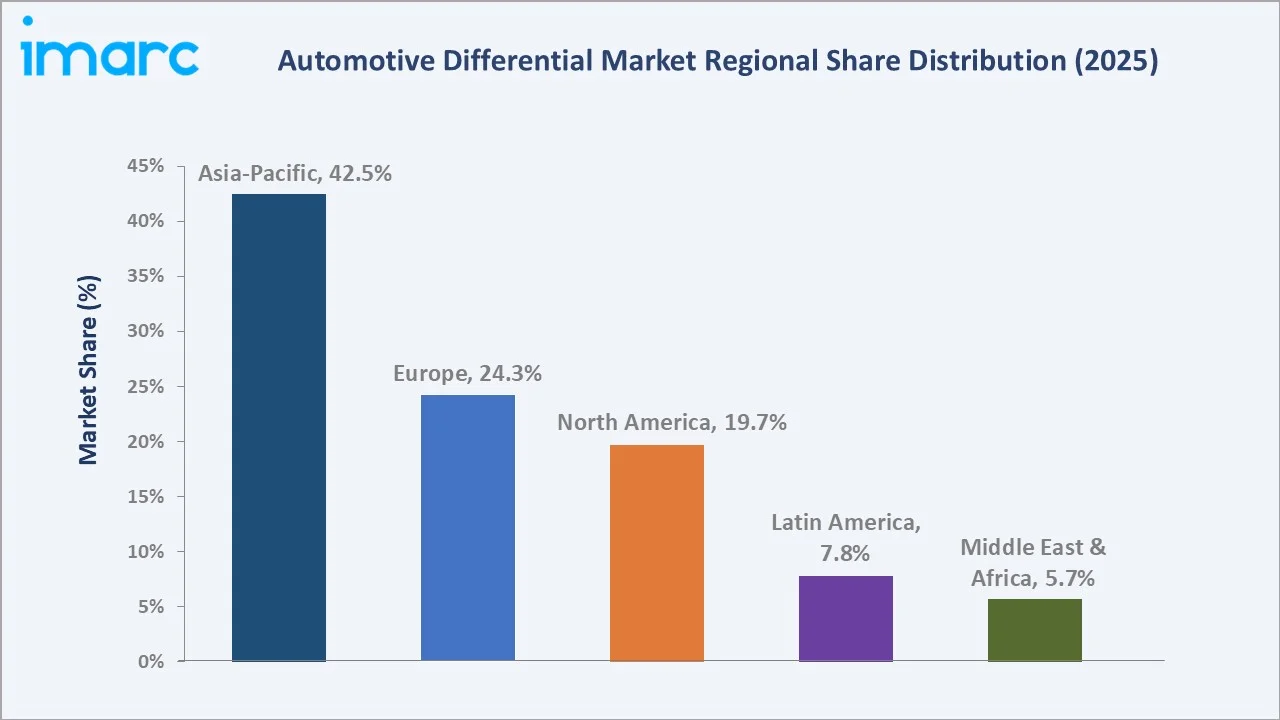

The global automotive differential market size was valued at USD 23.9 Billion in 2025 and is projected to reach USD 36.3 Billion by 2034, exhibiting a CAGR of 4.6% during the forecast period 2026-2034. Growing global vehicle production volumes, accelerating adoption of all-wheel drive (AWD) systems in the SUV and crossover segment, the electrification of powertrains via e-Axle architectures, and OEM demand for advanced torque vectoring and electronic limited-slip technologies are the primary drivers propelling automotive differential market growth. Open differential commands the largest type share at 34.5% in 2025, while front wheel drive (FWD) leads the drive type segment at 42.5%. Asia-Pacific dominates regional revenue with a 42.5% share in 2025, underpinned by China and India's expanding automotive manufacturing ecosystems.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 23.9 Billion |

|

Forecast Market Size (2034) |

USD 36.3 Billion |

|

CAGR (2026-2034) |

4.6% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (42.5% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Leading Type Segment |

Open Differential (34.5%, 2025) |

|

Leading Drive Type |

Front Wheel Drive / FWD (42.5%, 2025) |

The chart below illustrates the global automotive differential market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by electrification, AWD penetration in the SUV super-cycle, and advanced torque management adoption across vehicle categories.

To get more information on this market, Request Sample

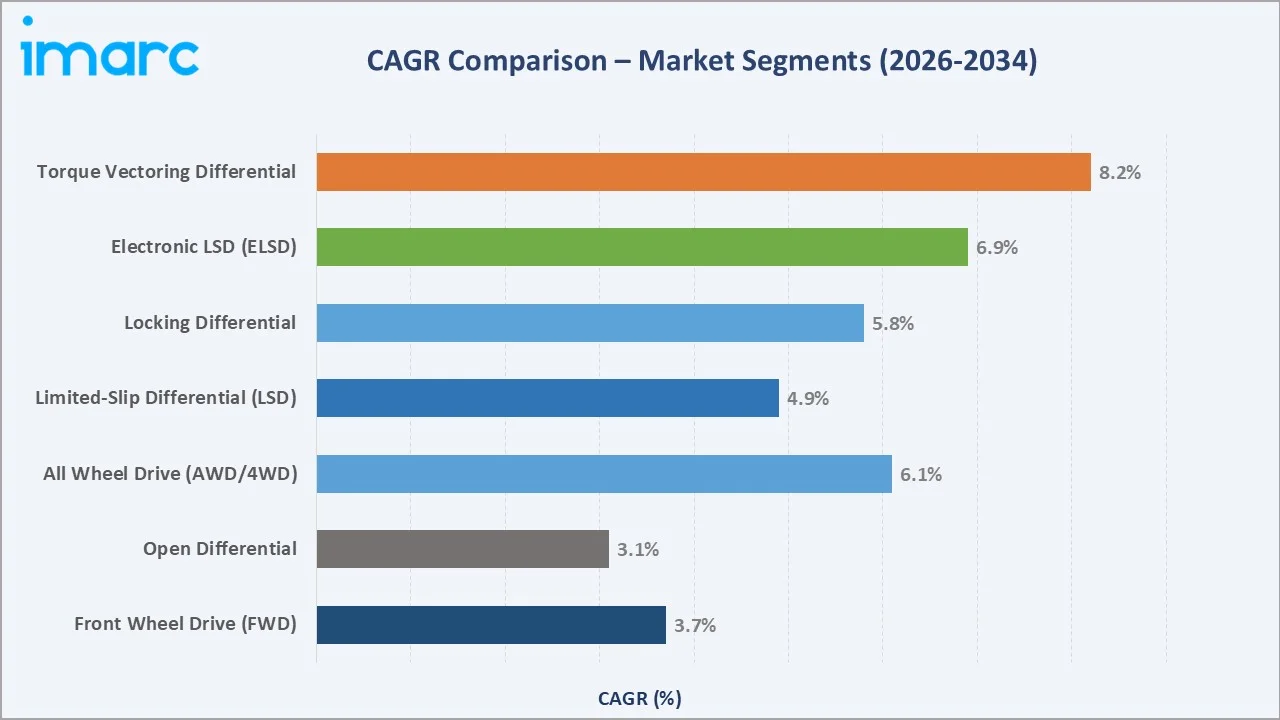

Segment-level CAGR comparisons highlight Torque Vectoring Differential (8.2% CAGR) and Electronic Limited-Slip Differential (6.9% CAGR) as the two fastest-growing type sub-categories within the global automotive differential industry analysis through 2034.

Executive Summary

The global automotive differential market is undergoing a fundamental evolution driven by three concurrent forces: the electrification of powertrains, the rapid proliferation of all-wheel drive systems in passenger and commercial vehicles, and OEM investment in electronically controlled torque management technologies. Valued at USD 23.9 Billion in 2025, the market is forecast to reach USD 36.3 Billion by 2034 at a CAGR of 4.6%.

Open Differential commands the highest type share at 34.5% in 2025, reflecting its cost-effectiveness across high-volume passenger car segments. Electronic variants combined – ELSD at 22.7% and Torque Vectoring at 9.8% – represent 32.5% of the type mix in 2025 and are growing at an above-average CAGR as OEMs integrate driveline electronics into broader vehicle dynamics systems.

Asia-Pacific accounts for 42.5% of global automotive differential revenue in 2025, underpinned by China's position as the world's largest vehicle manufacturing market with over 30 million annual production units and India's rapidly expanding passenger car ecosystem. Europe at 24.3% remains a premium driveline technology hub, while North America contributes 19.7%, supported by dominant pickup truck and SUV segments.

Key Market Insights

|

Insight |

Data |

|

Largest Type Segment |

Open Differential – 34.5% share (2025) |

|

Fastest Growing Type |

Torque Vectoring Differential – ~8.2% CAGR (2026–2034) |

|

Leading Drive Type |

Front Wheel Drive (FWD) – 42.5% share (2025) |

|

Fastest Growing Drive Type |

AWD/4WD – driven by SUV super-cycle (47%+ of global sales, 2024) |

|

Leading Region |

Asia-Pacific – 42.5% revenue share (2025) |

|

Second Largest Region |

Europe – 24.3% revenue share (2025) |

|

Market Size (2025) |

USD 23.9 Billion |

|

Market Size (2034) |

USD 36.3 Billion (projected) |

|

Top Key Companies |

ZF Friedrichshafen, BorgWarner, GKN Automotive, Dana, Eaton, JTEKT, American Axle |

|

Key Market Opportunity |

EV e-Axle integrated differential & torque vectoring platform growth |

Key Analytical Observations Supporting The Above Data:

- Open Differential's 34.5% dominance in 2025 reflects persistent cost sensitivity in high-volume compact and mid-size passenger car platforms, where mechanical simplicity and low manufacturing cost remain primary OEM procurement criteria in FWD vehicle architectures.

- Electronic Limited-Slip Differential (ELSD) at 22.7% share in 2025 signals strong OEM adoption of electronically controlled traction management in C-segment and above passenger cars, premium crossovers, and performance vehicles, increasingly integrated with ESC and ADAS domain controllers.

- Asia-Pacific's 42.5% global dominance in 2025 reflects China's dual role as the world's largest vehicle production market and the most aggressive adopter of AWD/4WD systems in crossover and SUV segments, complemented by India's passenger car production surge above 4.5 million units in 2024–25.

- AWD/4WD at 34.7% drive type share in 2025 is growing as SUVs exceeded 47% of global new car sales in 2024. Each AWD vehicle requires two differential assemblies – front and rear – doubling per-vehicle differential content versus FWD equivalents.

Global Automotive Differential Market Overview

An automotive differential is a mechanical or electromechanical device that transmits engine torque to driven wheels while allowing each wheel to rotate at different speeds – essential for cornering without wheel slip, tire wear, or drivetrain stress. Modern differentials range from simple open gear mechanisms to electronically controlled torque vectoring systems that actively distribute torque between individual wheels in real time, functioning as integrated vehicle dynamics actuators.

Applications span the full automotive ecosystem: passenger cars, light commercial vehicles, heavy trucks, buses, off-highway construction and agricultural equipment, and increasingly battery electric vehicle e-Axle assemblies where motor-integrated differential designs replace conventional driveshaft-based architectures.

Market Dynamics

To evaluate market opportunities, Request Sample

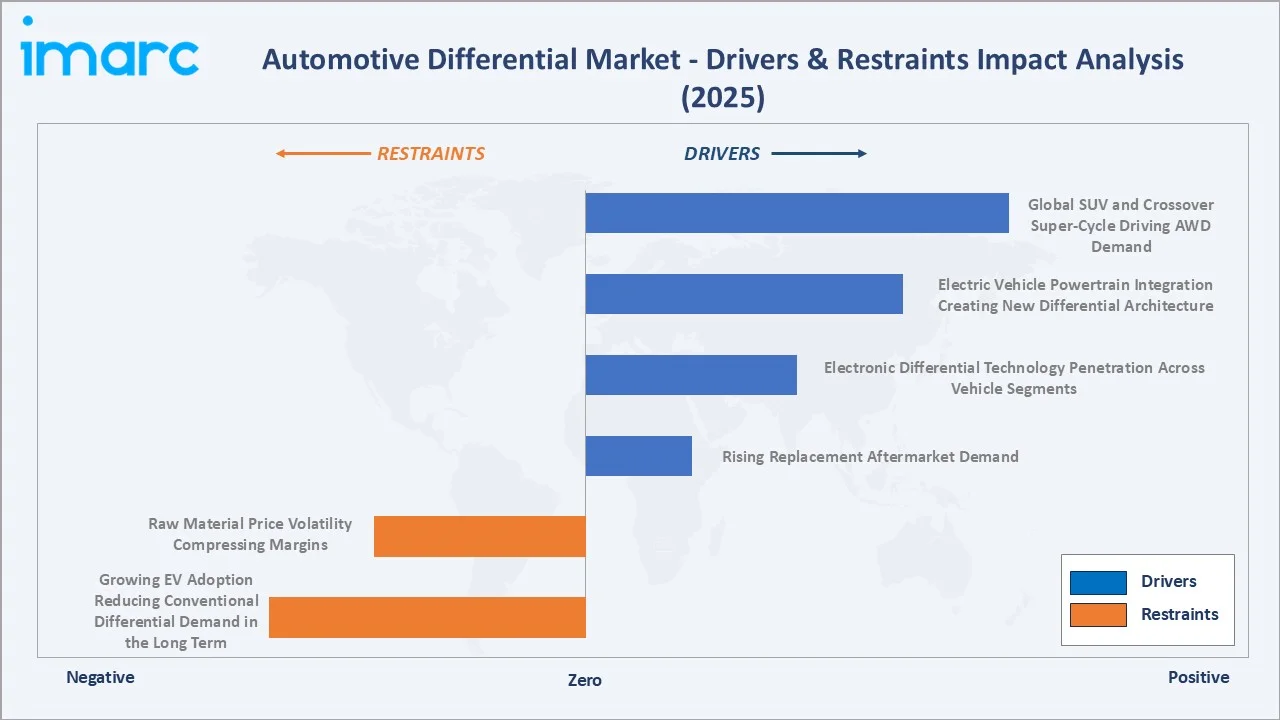

The global automotive differential market dynamics are shaped by a combination of structural demand drivers from vehicle electrification and SUV proliferation, counterbalanced by transitional restraints from EV cannibalization of conventional differential formats and raw material cost pressures.

Market Drivers

- Global SUV and Crossover Super-Cycle Driving AWD Demand: SUVs and crossovers represented over 47% of global new vehicle sales in 2024, surpassing traditional passenger sedans as the dominant body style worldwide. Each AWD/4WD-equipped SUV requires two differential assemblies – front and rear – compared to one for a FWD vehicle.

- Electric Vehicle Powertrain Integration Creating New Differential Architecture: Battery electric vehicles require differential mechanisms designed around e-Axle architectures where the electric motor, power electronics, and differential are co-integrated.

- Electronic Differential Technology Penetration Across Vehicle Segments: Electronic Limited-Slip Differentials (ELSD) and torque vectoring systems are transitioning from luxury/performance-only features to mainstream premium vehicle standard equipment. ELSDs improve vehicle stability, cornering performance, and off-road traction by electronically controlling wheel speed differentiation within 10–50 milliseconds.

- Rising Replacement Aftermarket Demand: With the global vehicle parc exceeding 1.4 Billion vehicles in 2024, wear-related differential component replacement – particularly bearings, ring-and-pinion gear sets, and seals in heavy commercial vehicles and off-highway equipment – provides a stable baseline revenue stream.

Market Restraints

- Growing EV Adoption Reducing Conventional Differential Demand in the Long Term: Single-motor battery electric vehicles use a fixed-ratio reducer with an open differential but eliminate multi-speed gearboxes and conventional driveshafts. As EV penetration grows toward 30–35% of new car sales by 2030, conventional open differential volumes in passenger cars may plateau from 2027–2028 onward.

- Raw Material Price Volatility Compressing Margins: Automotive differentials rely on high-grade steel alloys, case-hardened bearing steels, and precision-machined components. Global hot-rolled coil steel prices fluctuated over 40% between 2022 and 2024. Chinese steel overcapacity and geopolitical trade dynamics create sustained pricing uncertainty for Tier-1 differential suppliers managing thin margin profiles.

Market Opportunities

- Torque Vectoring Integration with EV Platforms: Motor-per-wheel EV architectures enable unprecedented individual wheel torque control, opening a design space for software-defined torque vectoring differentials. This represents a category-creating opportunity estimated at a multi-billion-dollar incremental market by 2030 for differential suppliers with software and controls competence.

- Off-Highway and Agricultural Equipment Expansion: Global construction equipment production is projected to grow at 5–6% annually through 2030, driven by infrastructure investment in India, Southeast Asia, and Africa. Off-highway vehicles require heavy-duty locking and limited-slip differentials with extreme load-bearing capacity – a niche with strong aftermarket attachment and premium pricing power.

- Emerging Markets Passenger Car Expansion: India is projected to become the world's third-largest automotive market by 2026, with passenger car sales forecast to exceed 5 million units annually. Indonesia, Vietnam, and Brazil are expanding domestic production bases, directly expanding addressable differential unit demand for cost-effective open and limited-slip variants.

Market Challenges

- Consolidation Pressure Among Tier-1 Driveline Suppliers: As OEMs rationalize from 15–20 drivetrain variants to 3–5 modular architectures per brand, supplier selection determines platform-level volume commitment over 6–8 year production runs – creating winner-take-all competitive dynamics among Tier-1 differential manufacturers.

- Supply Chain Localization and Regionalization Pressures: US Inflation Reduction Act local content requirements, EU strategic autonomy initiatives, and India's PLI automotive component scheme are reshaping global differential supply chains. Suppliers without regional manufacturing presence in North America, Europe, and Asia-Pacific risk losing OEM sourcing consideration regardless of technology capability.

Emerging Market Trends

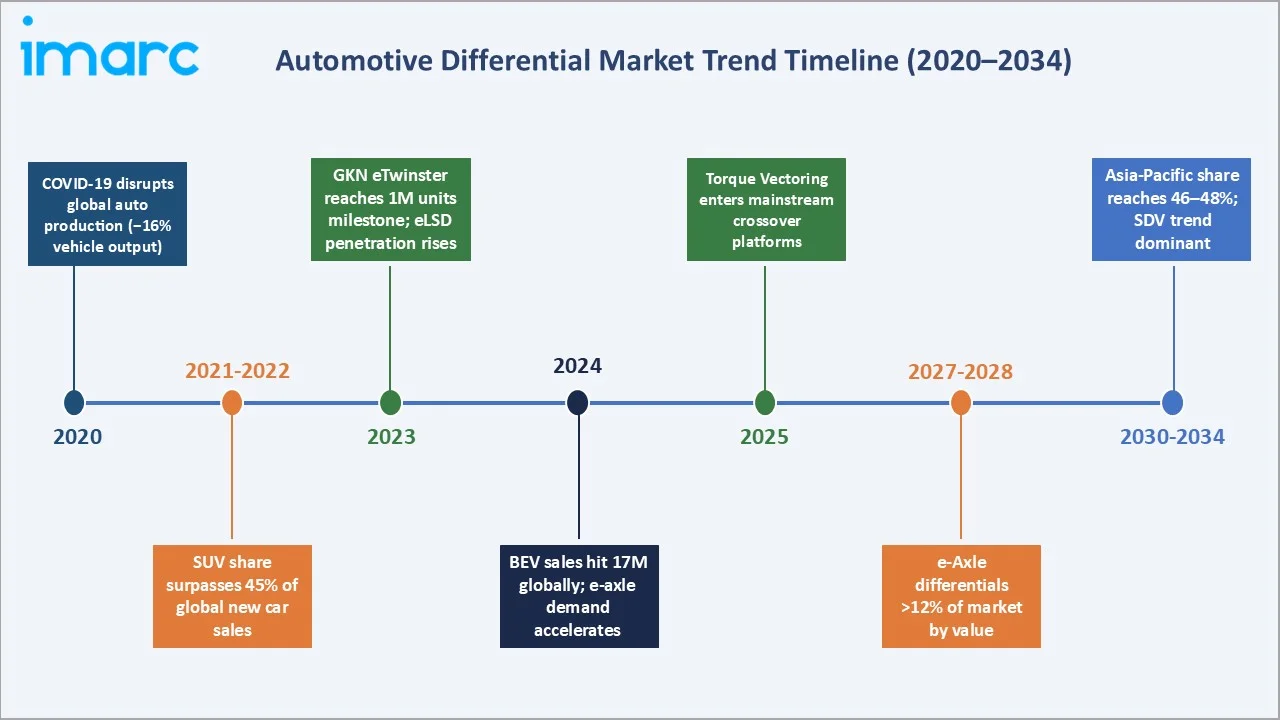

The global automotive differential market is being reshaped by five transformative trends spanning electrification, software integration, advanced materials, connected monitoring, and ADAS convergence. The trend timeline below captures key technology milestones from 2020 through 2034.

1. Electrification of Differentials and e-Axle Architecture Integration

The integration of electric motors directly into axle assemblies is redefining differential design requirements. e-Axle platforms from ZF (eBeam), GKN (eTwinster), and Dana (Spicer Electrified) incorporate differential mechanisms within compact electrified assemblies targeting BEV and PHEV OEM platforms.

2. Electronically Controlled Torque Vectoring as Mainstream Safety Feature

Torque vectoring differential technology – historically confined to Porsche 911, BMW M, and Ferrari performance vehicles – is transitioning toward mainstream premium vehicles. The integration of torque vectoring with Electronic Stability Control (mandatory in all EU and US vehicles since 2014) creates a clear regulatory and safety mandate pathway.

3. Lightweight Materials and Additive Manufacturing Adoption

Aluminium differential housings, titanium fasteners, and carbon-fibre-reinforced components are replacing cast iron in performance and electrified vehicle differential assemblies. Weight reduction of 15–25% per differential assembly contributes directly to EV range extension targets.

4. Predictive Maintenance and Connected Differential Monitoring

IoT-enabled differential monitoring systems – using vibration sensors, thermal sensors, and oil condition monitoring – are entering fleet management applications for commercial vehicle and off-highway equipment operators. Connected differential health monitoring can reduce unplanned downtime by 35–50% in heavy commercial vehicle applications.

5. Software-Defined Differential Control Integration with ADAS and Vehicle Dynamics

Advanced Driver Assistance Systems – lane-keeping assist, active yaw control, and autonomous emergency steering – require millisecond-precision differential torque modulation inputs. The integration of ELSD and torque vectoring differentials with ADAS domain controllers is creating demand for differential systems with CAN/LIN/Automotive Ethernet communication interfaces, elevating differentials from purely mechanical components to software-integrated vehicle dynamics actuators.

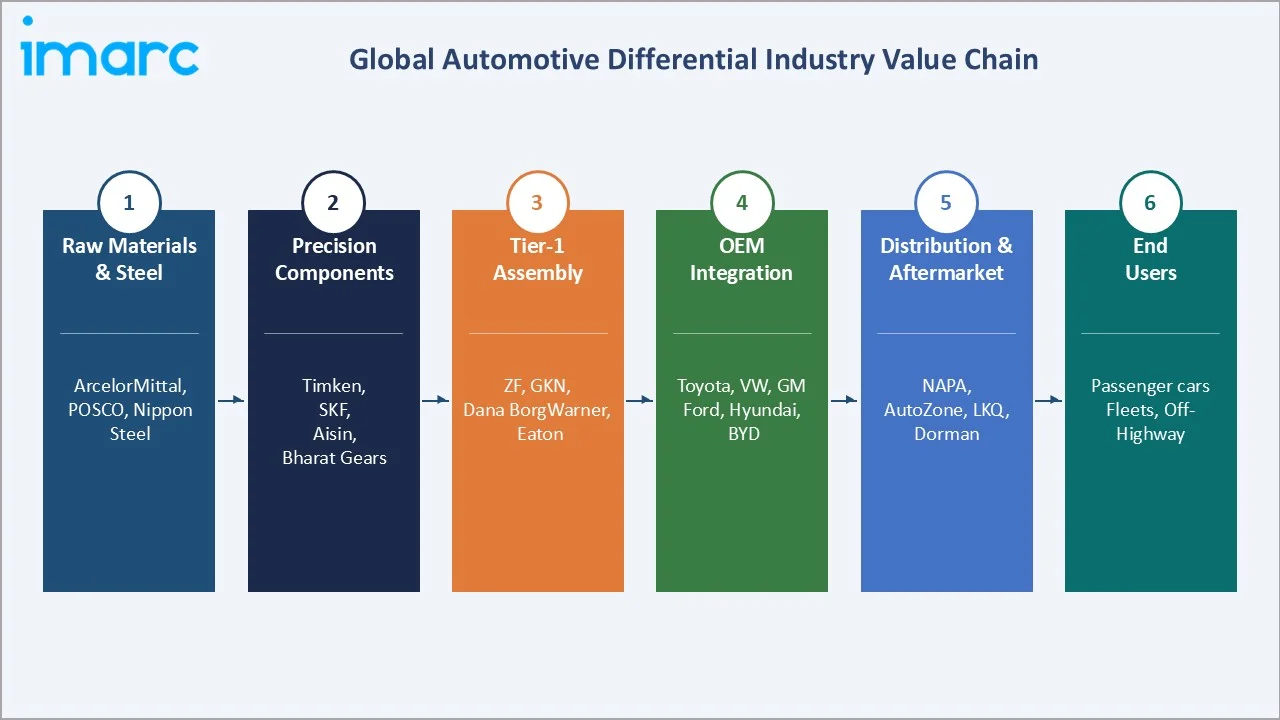

Industry Value Chain Analysis

The automotive differential value chain spans six integrated stages from raw material and component supply through end-consumer vehicle delivery and aftermarket service. Each stage presents distinct competitive dynamics, margin profiles, and technology requirements.

|

Stage |

Key Players / Examples |

|

Raw Materials & Steel |

ArcelorMittal, POSCO, Nippon Steel, ThyssenKrupp Steel, Baosteel – high-alloy differential case and gear steels |

|

Precision Components |

Timken, SKF, NSK, NTN – differential bearings; Aisin Seiki, Bharat Gears – ring-and-pinion gear sets; precision machining subcontractors |

|

Differential Assembly (Tier-1) |

ZF Friedrichshafen, BorgWarner, GKN Automotive, Dana Incorporated, Eaton, JTEKT, American Axle & Manufacturing, Hyundai WIA |

|

Electronics & Controls |

Continental, Bosch, Aptiv – ELSD control modules; Sensata Technologies – differential sensors; Delphi Technologies – power electronics |

|

OEM Vehicle Integration |

Toyota, Volkswagen Group, Stellantis, GM, Ford, Hyundai-Kia, BMW Group, Mercedes-Benz, BYD, SAIC – final assembly |

|

Aftermarket & Distribution |

Cardone Industries, Dorman Products, NAPA Auto Parts, AutoZone, LKQ Corporation, O'Reilly Auto Parts – global distribution |

|

End Users |

Passenger car owners, light and heavy commercial fleet operators, construction equipment operators, off-highway vehicle users |

Tier-1 differential assembly manufacturers occupy the highest strategic value position in the automotive differential value chain. The trend toward modular e-Axle assemblies, where the differential is co-integrated with the electric motor and gearbox, is creating opportunities for Tier-1 driveline specialists to capture additional value beyond standalone differential supply.

Technology Landscape in the Automotive Differential Industry

Mechanical Differential Technologies: Open, LSD, and Locking Systems

Open Differential remains the dominant technology due to low manufacturing cost, mechanical simplicity, and suitability for standard passenger car FWD applications. Limited-Slip Differentials (LSD) at 18.4% use clutch packs, viscous couplings, or Torsen helical gear mechanisms to limit speed differentiation under traction loss.

Electronic Control and Actuation Technologies

Electronic Limited-Slip Differentials (ELSD) at 22.7% market share in 2025 use electronically controlled multi-plate wet clutch systems – actuated by hydraulic or electromechanical solenoids – to modulate torque distribution within 10–50 milliseconds.

Torque Vectoring and e-Axle Technologies

Torque Vectoring Differentials use superposition planetary gearsets combined with electric motors to actively transfer torque between individual wheels, enabling yaw moment generation and precision vehicle dynamics control.

Lubrication, Smart Monitoring, and Advanced Materials

Advanced differential lubricant formulations using synthetic polyalphaolefin (PAO) base oils and gear friction modifiers are extending differential service intervals from 60,000 km to 120,000+ km in passenger car applications. IoT-enabled oil condition monitoring systems – measuring viscosity, contamination, and temperature in real time are entering premium vehicle and commercial fleet applications.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Open Differential |

34.5% |

2025 |

|

Drive Type |

Front Wheel Drive (FWD) |

42.5% |

2025 |

|

Vehicle |

Passenger Car |

58.5% |

2025 |

|

Component |

Differential Gear |

42.5% |

2025 |

| Vehicle Propulsion Type | I.C. Engine Vehicle | 75.5% | 2025 |

|

Region |

Asia Pacific |

42.5% |

2025 |

Market Breakup by Type

To access detailed market analysis, Request Sample

Open Differential's 34.5% dominance reflects persistent cost-sensitivity in high-volume compact vehicle segments. Electronic variants combined (ELSD + Torque Vectoring) represent 32.5% of the type mix in 2025 and are growing at above-average CAGR as OEMs integrate driveline electronics into broader vehicle dynamics domain controllers.

Market Breakup by Drive Type

Front Wheel Drive (FWD) leads the drive type segmentation at 42.5% in 2025, reflecting FWD's dominant position in global passenger car production, particularly in Europe and Asia-Pacific where compact and mid-size vehicles constitute the majority of new car sales. AWD/4WD systems hold 34.7%, driven by the SUV and crossover market expansion globally. Rear Wheel Drive (RWD) contributes 22.8%, anchored by pickup trucks, performance vehicles, and heavy commercial vehicles.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Markets / Companies |

|

Asia-Pacific |

42.5% |

China/India vehicle production boom; SUV/crossover expansion; EV e-Axle demand; Japan Tier-1 tech |

China, Japan, India, South Korea, Indonesia |

|

Europe |

24.3% |

Premium AWD vehicles; EU EV mandate 2035; ZF/GKN/Dana Tier-1 base; Porsche/BMW TVD programmes |

Germany, France, UK, Italy, Spain, Russia |

|

North America |

19.7% |

Pickup truck AWD dominance (F-Series, Silverado); ADAS mandates; EV transition by Ford/GM/Tesla |

USA, Canada, Mexico |

|

Latin America |

7.8% |

Brazil/Mexico auto production growth; LCV expansion; rising SUV adoption; MERCOSUR tariff dynamics |

Brazil, Mexico |

|

Middle East & Africa |

5.7% |

4WD utility vehicle demand; GCC premium adoption; Saudi Vision 2030; South Africa auto sector |

Saudi Arabia, UAE, South Africa |

Asia-Pacific commands a 42.5% global revenue share in 2025, the most dominant regional position in the global automotive differential market. Europe at 24.3% in 2025 is anchored by Germany's premium automotive manufacturing dominance – BMW Group, Volkswagen Group (including Audi, Porsche), and Mercedes-Benz – all leading adopters of ELSD, torque vectoring, and AWD differential technologies in premium and performance vehicle platforms.

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

ZF Friedrichshafen AG |

ZF eBeam Axle |

Leader |

Full driveline system integration; e-Axle; torque vectoring; global OEM partnerships across Europe, Asia, North America |

|

GKN Automotive Limited |

eTwinster |

Leader |

Electrified AWD; torque vectoring (1M+ units milestone); Tier-1 supplier to BMW, Ford, VW, Jaguar Land Rover |

|

Dana Incorporated |

Spicer / Spicer Electrified |

Leader |

Heavy-duty differentials; e-Axle; commercial EV drivetrains; off-highway driveline expertise globally |

|

BorgWarner Inc. |

BorgWarner eAWD / eTVD |

Leader |

AWD torque management; EV-focused eTorque Vectoring Drive; eAxle systems for passenger and commercial vehicles |

|

Eaton Corporation Inc. |

Eaton Truetrac / ELocker |

Leader |

LSD and locking differentials for heavy trucks and SUVs; North America distribution dominance; ELocker CAN integration |

|

American Axle & Manufacturing |

AAM EcoTrac / e-Drive |

Challenger |

Disconnecting AWD systems; axle and driveline modules; OEM-direct engineering relationships; electrified axle R&D |

|

JTEKT Corporation |

JTEKT Torque Control AWD |

Challenger |

Compact AWD coupler differentials; steering and driveline integration; Toyota ecosystem supply partnerships |

|

Hyundai WIA Corporation |

Hyundai WIA Axle Systems |

Challenger |

Commercial vehicle differentials; in-house OEM supply for Hyundai-Kia group; Asia-Pacific manufacturing scale |

|

Quaife Engineering Ltd. |

Quaife ATB Differential |

Emerging |

Torsen helical gear LSD; performance and motorsport aftermarket; UK-based specialty manufacturer |

|

PowerTrax |

PowerTrax Locker Systems |

Emerging |

Aftermarket locking differentials; 4WD utility vehicles; USA off-road aftermarket specialty |

|

Yager Gear Enterprise |

Yager Differential Gears |

Emerging |

Differential gear manufacturing; Asia-Pacific supply chain; OEM and Tier-2 component supply |

The global automotive differential competitive landscape is characterized by a small number of large, vertically integrated Tier-1 driveline suppliers commanding dominant OEM relationships, alongside specialty manufacturers occupying niche performance, off-highway, and aftermarket positions. ZF Friedrichshafen, GKN Automotive, Dana, BorgWarner, and Eaton collectively account for an estimated 45–55% of global automotive differential revenue in 2025, with combined footprint spanning all major vehicle categories and regions.

Key Company Profiles

ZF Friedrichshafen AG

ZF Friedrichshafen is a leading global Tier-1 automotive supplier headquartered in Germany, with ~EUR 43 Billion revenue (2023). It specializes in driveline, chassis, differential systems, and electrified components across all vehicle segments.

- Product Portfolio: eBeam electric drive system, Torque vectoring & active limited-slip differentials, IRS axle differentials, e-Axle modules for BEV/PHEV.

- Recent Developments: Partnership with NVIDIA for AI-based vehicle dynamics (L3+ readiness by 2026), eBeam launched with a European premium OEM (2024).

- Strategic Focus: Transition to integrated e-Axle systems (motor + electronics + differential, ~EUR 2B annual EV R&D investment, target: 50% driveline revenue from electrification by 2030.

BorgWarner Inc.

BorgWarner is a US-based Tier-1 supplier with ~USD 14.2 Billion revenue (2023), focused on drivetrain, thermal, and EV propulsion systems with strong AWD/4WD OEM partnerships.

- Product Portfolio: eAWD coupling systems & ITM AWD solutions, dual-clutch AWD & RDM with integrated differentials, eTorque Vectoring Drive (eTVD) for BEVs.

- Recent Developments: In January 2025, BorgWarner announced its eTorque Vectoring Drive system was selected by a major European OEM for deployment in a premium BEV platform, with production start targeted for 2027.

- Strategic Focus: BorgWarner's Charging Forward strategy targets 45% of net revenue from EV products by 2030, shift to compact e-Axle platforms for global EV markets.

GKN Automotive Limited

GKN Automotive is a global driveline specialist operating in 24 countries, supplying over 90% of global OEMs and pioneering electrified AWD systems.

- Product Portfolio: eTwinster AWD torque vectoring system, eBeam electric rear axle, conventional and electronic AWD couplers, prop shafts, sideshafts, and constant velocity joint (CVJ) systems integrated with differential modules

- Recent Developments: In 2024, GKN Automotive announced the production milestone of over 1 million eTwinster units delivered to Ford for the Escape/Kuga PHEV platform since its 2019 launch.

- Strategic Focus: GKN Automotive's strategy prioritises electrified AWD and torque vectoring as the primary growth vector, alongside continued investment in advanced manufacturing for eDrive systems including e-Axle and ePropulsion modules.

Dana Incorporated

Dana is a US-based Tier-1 supplier (~USD 10.3 Billion revenue, 2023) specializing in drivetrain solutions. Its Spicer brand is a global leader in commercial and off-highway differentials.

- Product Portfolio: Spicer steer axles and drive axles with integrated differentials, Spicer Electrified e-Axle modules, heavy-duty locking differentials, Spicer AdvanTEK off-highway differential axles, and torque vectoring systems.

- Recent Developments: In 2024, Dana announced a multi-year supply agreement with a North American Class 6–7 electric truck OEM for its Spicer Electrified single-speed e-Axle platform, incorporating integrated differential and electric motor in a compact housing designed for 2025 production start.

- Strategic Focus: Dana's electrification strategy targets the commercial vehicle EV segment as its primary growth opportunity, complementing its dominant position in heavy-duty mechanical differential supply.

Eaton Corporation Inc.

Eaton’s Vehicle Group is a key supplier of drivetrain systems for trucks, SUVs, and off-highway vehicles, with strong OEM and aftermarket presence.

- Product Portfolio: Truetrac limited-slip differential, ELocker electronic locking differential with CAN bus integration, Detroit Locker automatic locking differential, Posi differential for performance vehicles, drivetrain components

- Recent Developments: In 2023, Eaton launched the next-generation ELocker with integrated CAN bus communication capability enabling direct integration with vehicle ESC and ADAS systems.

- Strategic Focus: Eaton's differential strategy focuses on its dominant position in the North American truck and SUV aftermarket and OEM supply, complemented by selective electrification of its locking differential portfolio to serve PHEV and mild hybrid light truck platforms maintaining 4WD capability.

Market Concentration Analysis

The global automotive differential market exhibits moderate-to-high concentration at the Tier-1 assembly level. ZF Friedrichshafen, GKN Automotive, Dana Incorporated, BorgWarner, and Eaton Corporation collectively account for an estimated 45–55% of global differential revenue in 2025. The remainder of the market is distributed among a broader set of regional Tier-1 suppliers (American Axle, JTEKT, Hyundai WIA, Aisin) and a long tail of specialty and aftermarket manufacturers.

The market demonstrates a bifurcated concentration structure. At the OEM-supply Tier-1 level, consolidation is intensifying as complex e-Axle and ELSD platform development requires R&D investments of USD 100–500 Million per programme. This effectively excludes mid-tier suppliers from leading OEM consideration for advanced differential platforms.

Investment & Growth Opportunities

Fastest-Growing Segments

Torque Vectoring Differentials are the highest-growth type sub-segment at approximately 8.2% CAGR through 2034. Adoption is accelerating across electrified passenger vehicles, premium crossovers, and commercial EVs. The motor-per-axle BEV architecture trend – deployed at scale by BYD, Tesla, Rivian, and Hyundai Ioniq – is converting torque vectoring from a mechanical luxury feature to a fundamental software-defined vehicle dynamics capability with addressable demand across an expanding vehicle category range.

Emerging Markets Expansion

India represents the most significant emerging market opportunity. India's passenger car production exceeded 4.5 million units in 2024–25 and is projected to reach 6 million+ by 2028, driven by rising middle-class vehicle ownership and government PLI scheme incentives for automotive component manufacturing. India's SUV market represents over 50% of Indian passenger car sales in 2025, directly driving AWD differential demand. Local production investments by ZF, GKN, and Dana are already underway targeting Indian market volume growth. The Indian differential market is forecast to grow at 7–8% CAGR through 2034, outpacing the global average.

Venture & Strategic Investment Trends

Strategic investment in automotive differential is concentrated in three areas: e-Axle differential integration for BEV platforms, software-defined torque vectoring control systems, and advanced manufacturing processes for lightweight differential components. ZF's annual driveline electrification R&D spend exceeds EUR 600 Million. GKN Automotive's parent Melrose Industries has committed to GBP 1.5 Billion in driveline electrification investment through 2030. Dana's Spicer Electrified programme is backed by USD 500+ Million in targeted EV product development investment.

Future Market Outlook (2026-2034)

The global automotive differential market forecast projects steady value expansion from USD 23.9 Billion in 2025 to USD 36.3 Billion by 2034 at a CAGR of 4.6%, representing a cumulative value addition of over USD 12.4 Billion over the forecast period. This growth is underpinned by three concurrent drivers: premium system specification migration from open to electronic differentials, EV e-Axle differential content growth per vehicle, and structural unit volume expansion from emerging market vehicle ownership growth in India, Southeast Asia, and Latin America.

Three technology discontinuities are most likely to reshape the automotive differential market through 2034. First, e-Axle integration convergence will progressively displace standalone rear differential assemblies in BEV platforms, shifting market value from mechanical hardware to electromechanical system assemblies.

Research Methodology

Primary Research

Primary research for this study encompassed structured interviews conducted in 2024–2025 with automotive driveline industry stakeholders, including engineering and product directors at Tier-1 differential suppliers, OEM powertrain and driveline procurement managers, driveline component aftermarket distributors, EV powertrain systems integrators, and institutional investors in automotive supplier companies. Primary research insights validated market sizing estimates, technology adoption timelines, competitive positioning assessments, and strategic investment trends across all five geographic regions.

Secondary Research

Secondary sources include OICA global vehicle production statistics (2020–2024), IEA Global EV Outlook (2024), S&P Global Mobility vehicle production and component fitment data, Volkswagen Group, ZF Friedrichshafen, Dana, BorgWarner, and GKN Automotive annual reports (2022–2024), JATO Dynamics global vehicle sales data, SAE International driveline technology papers, NHTSA and UNECE vehicle safety regulation publications, McKinsey Center for Future Mobility automotive reports, and trade publications including Automotive News, Just-Auto, and Wards Intelligence.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating global vehicle production forecasts by category, AWD/4WD penetration rate projections by region, EV adoption curves by geography, differential content-per-vehicle trends by drive type, and average selling price evolution models reflecting technology mix shift.

Automotive Differential Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Electronic Limited-Slip Differential (ELSD), Locking Differential, Limited-Slip Differential (LSD), Open Differential, Torque Vectoring Differential |

| Drive Types Covered | Front Wheel Drive (FWD), Rear Wheel Drive (RWD), All Wheel Drive/ Four Wheel Drive (AWD/4WD) |

| Vehicles Covered | Passenger Car, Light Commercial Vehicle, Heavy Commercial Vehicle, Off-highway Vehicle |

| Components Covered | Differential Bearing, Differential Gear, Differential Case |

| Vehicle Propulsion Types Covered |

|

| Regions Covered | North America, Asia-Pacific, Europe, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, China, Japan, India, South Korea, Australia, Indonesia, Germany, France, United Kingdom, Italy, Spain, Russia, Brazil, Mexico |

| Companies Covered | ZF Friedrichshafen AG, GKN Automotive Limited, Dana Incorporated, BorgWarner Inc., Eaton Corporation Inc., American Axle & Manufacturing, JTEKT Corporation, Hyundai WIA Corporation, Quaife Engineering Ltd., PowerTrax, Yager Gear Enterprise |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive differential market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global automotive differential market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter’s Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive differential industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive Differential Market Report

The global automotive differential market was valued at USD 23.9 Billion in 2025, driven by global vehicle production of 93+ million units annually, AWD/SUV expansion, and rising electronic differential adoption.

The market is projected to reach USD 36.3 Billion by 2034, growing at a CAGR of 4.6% during 2026-2034, driven by EV e-Axle integration, AWD penetration, and emerging market vehicle demand growth.

Open Differential leads with a 34.5% share in 2025, driven by its cost-effectiveness and dominance in high-volume passenger car FWD platforms across emerging and developed markets globally.

Torque Vectoring Differential is the fastest-growing type at ~8.2% CAGR, driven by EV e-Axle integration, PHEV AWD platforms, and OEM adoption across premium crossovers and performance vehicles through 2034.

Asia-Pacific leads with a 42.5% share in 2025, driven by China's dominant vehicle production, India's growing passenger car market, Japan's Tier-1 technology ecosystem, and South Korea's OEM expansion.

Key drivers include global SUV/AWD super-cycle (47%+ of new cars in 2024), BEV e-Axle demand (17M EV sales in 2024), ELSD adoption in ADAS-integrated vehicles, and emerging market vehicle ownership growth.

EVs are shifting differential technology toward e-Axle-integrated assemblies combining motor, reducer, and differential. Dual-motor EVs require two e-Axle differential assemblies, increasing per-vehicle differential content value by 30–50%.

Leading companies include ZF Friedrichshafen, GKN Automotive, Dana Incorporated, BorgWarner, Eaton Corporation, American Axle & Manufacturing, JTEKT Corporation, Hyundai WIA Corporation, Quaife Engineering Ltd., PowerTrax, and Yager Gear Enterprise globally.

ELSD uses electronically controlled clutch packs to modulate torque between wheels in real time, holding 22.7% market share in 2025. Growth is driven by integration with mandatory ESC and ADAS systems in mainstream premium vehicles.

AWD/4WD systems hold 34.7% of drive type share in 2025 and are growing as SUVs and crossovers exceeded 47% of global car sales in 2024. Each AWD vehicle requires two differential assemblies, doubling per-vehicle content value.

Torque vectoring differentials actively distribute torque between individual wheels for superior handling and stability. Used in performance vehicles (Porsche, BMW M) and expanding into electrified AWD crossover platforms from 2026–2028.

The automotive differential aftermarket – covering bearing, gear, and seal replacement on the 1.4 Billion+ global vehicle parc – represents a USD 3–4 Billion annual revenue segment, providing stable baseline demand for Tier-1 suppliers and specialty remanufacturers.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)