Automotive Fascia Market Size, Share, Trends and Forecast by Material, Position Type, Vehicle Type, Sales Channel, and Region, 2026-2034

Automotive Fascia Market Size, Share, Trends & Forecast (2026-2034)

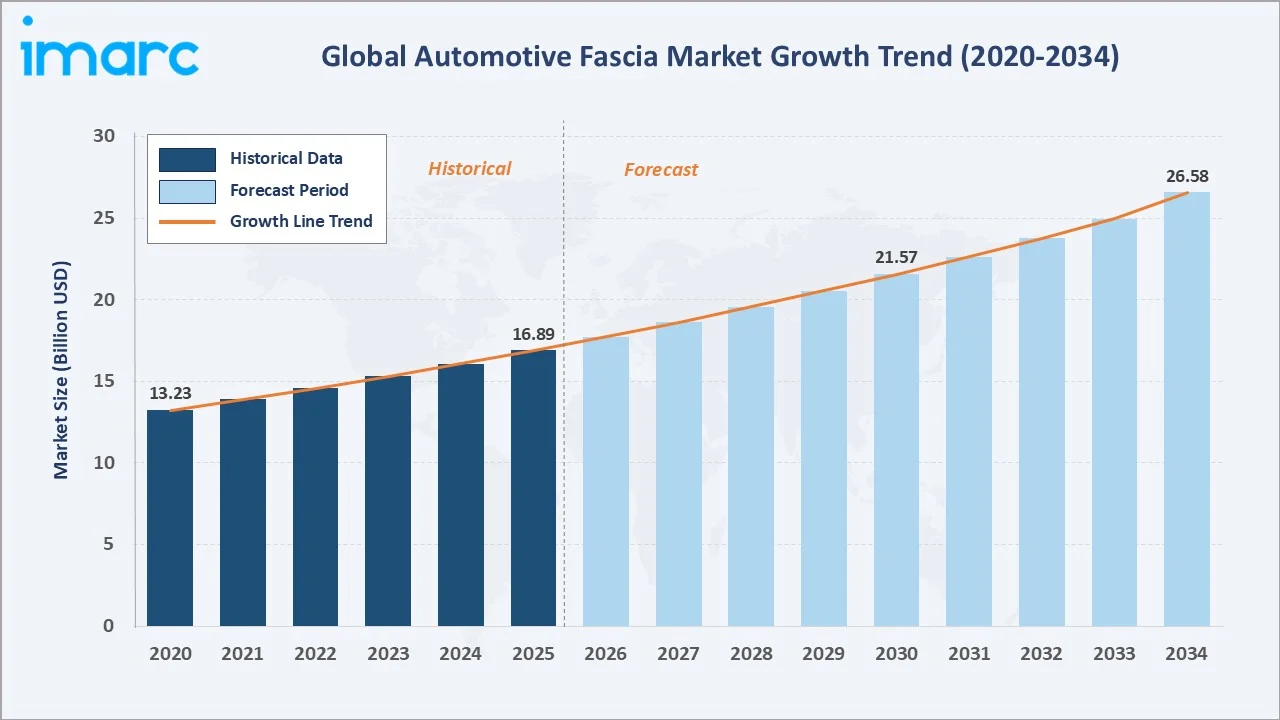

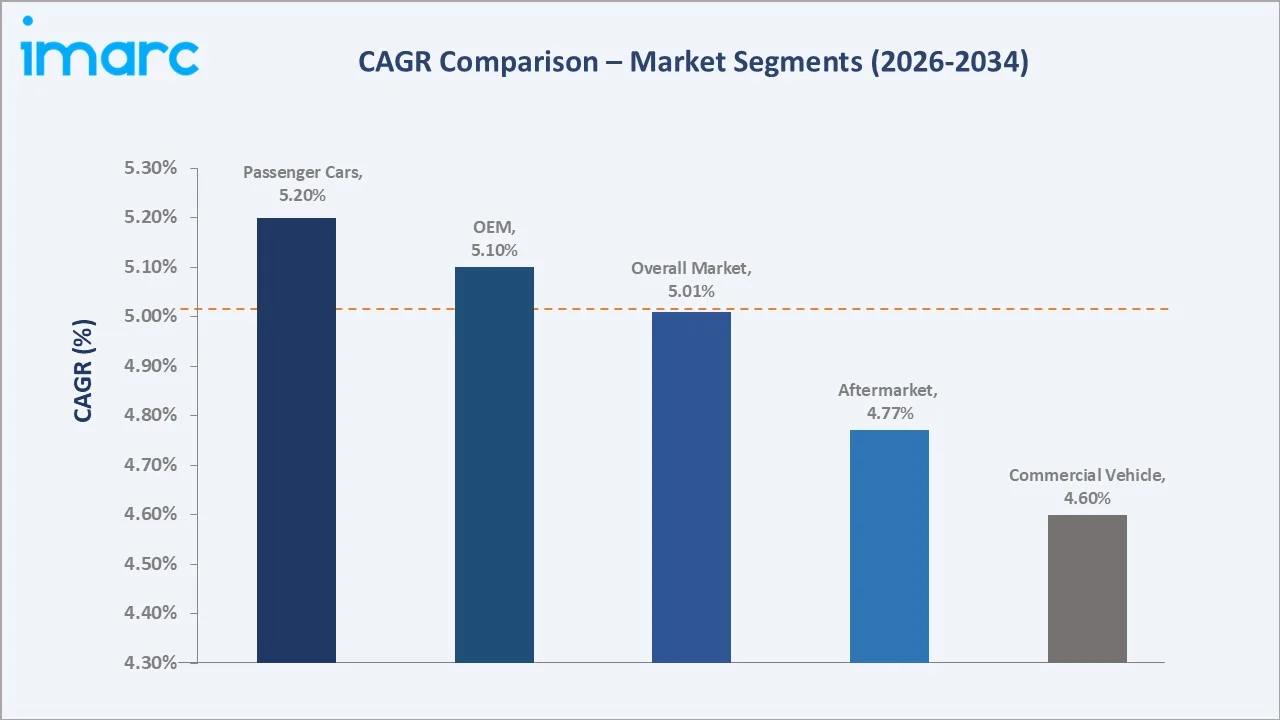

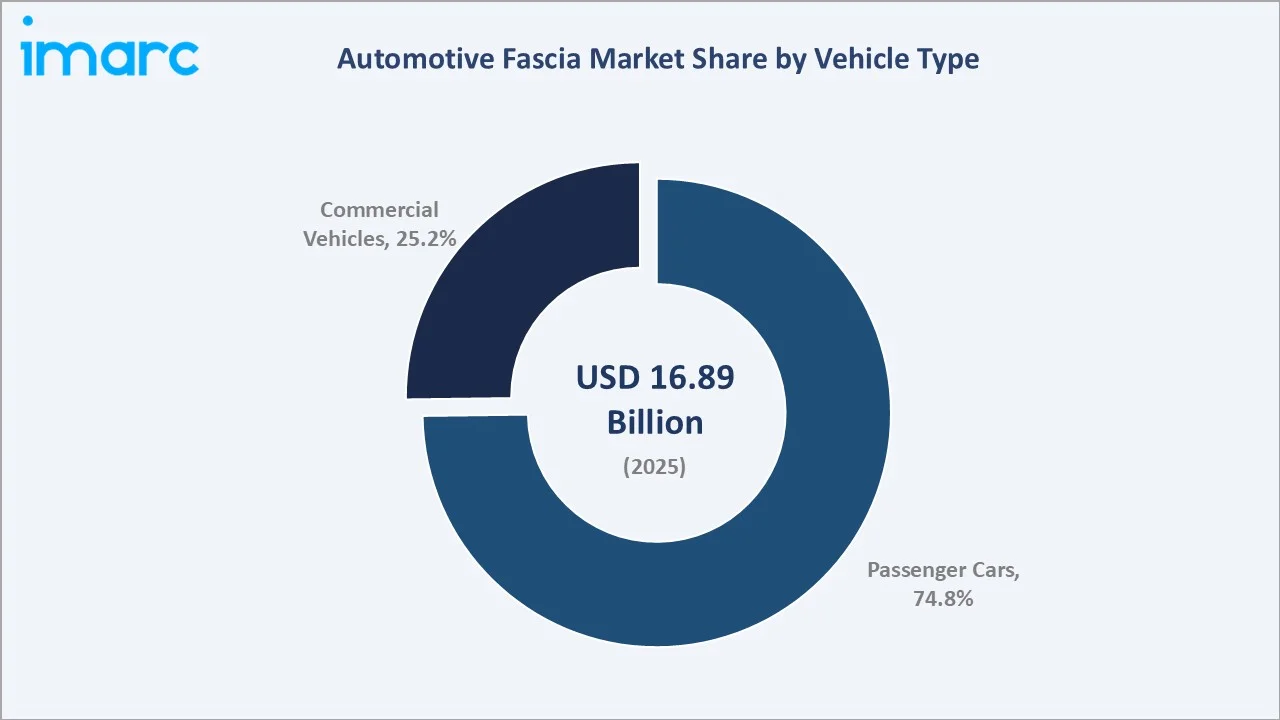

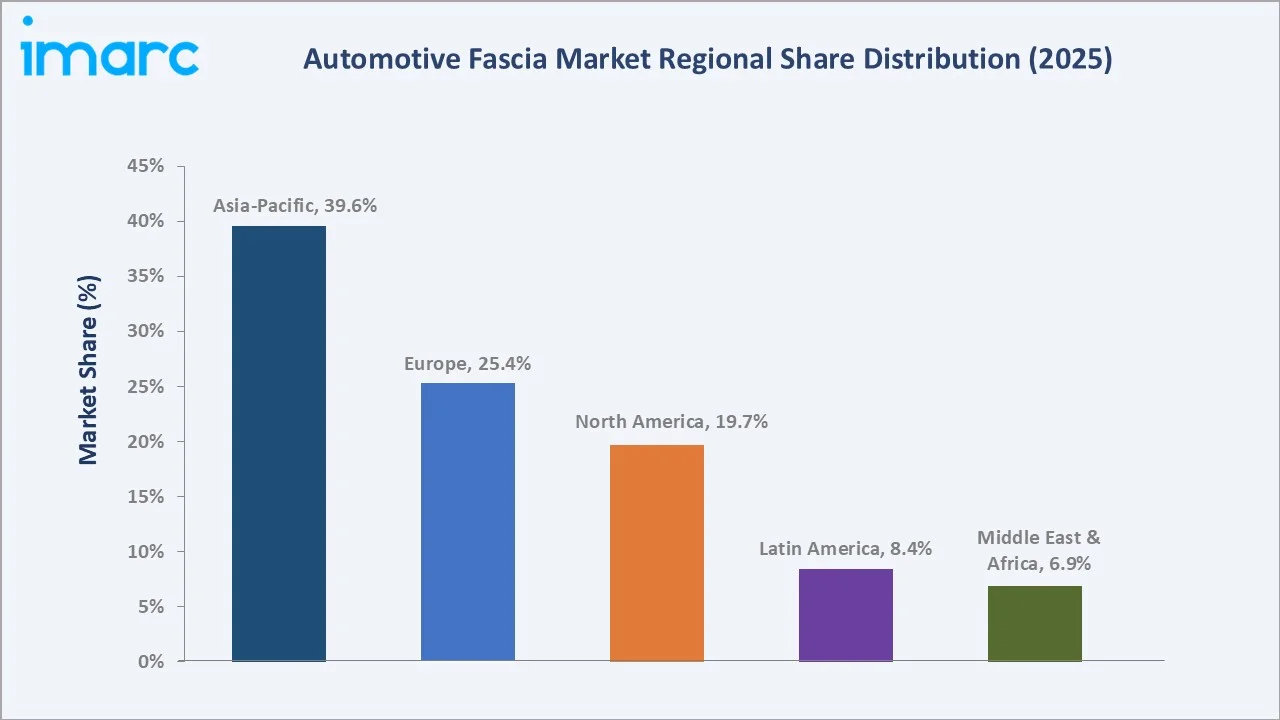

The global automotive fascia market reached USD 16.89 Billion in 2025 and is projected to reach USD 26.58 Billion by 2034, growing at a CAGR of 5.01% during 2026-2034. The market is driven by increasing vehicle production, rising demand for lightweight and aerodynamic vehicle components, and growing emphasis on vehicle aesthetics and front-end design. Expanding adoption of electric vehicles and advanced safety integration is further supporting fascia demand. Global car registrations increased 3.5% in 2025, reaching 77.6 million units, with China recording 5.5% growth supported by scrappage incentives and new energy vehicle policies. This growth is driving the automotive fascia market, as higher vehicle production and sales increase demand for front-end and rear-end fascia components used for styling, aerodynamics, safety integration, and vehicle differentiation. Passenger cars dominate the vehicle type at 74.8%. OEM channel leads at 71.5%. Asia-Pacific commands 39.6% of the global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 16.89 Billion |

|

Forecast Market Size (2034) |

USD 26.58 Billion |

|

CAGR (2026-2034) |

5.01% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Vehicle Type |

Passenger Cars (74.8%, 2025) |

|

Dominant Sales Channel |

OEM (71.5%, 2025) |

|

Leading Region |

Asia-Pacific (39.6%, 2025) |

The market expanded from USD 13.23 Billion in 2020 to USD 16.89 Billion in 2025, anchored at USD 21.57 Billion in 2030, and forecast to reach USD 26.58 Billion by 2034. COVID-19 supply chain disruptions (2020-2021) and the global semiconductor shortage created vehicle production reductions, temporarily suppressed fascia demand, but the recovery from 2022 onward was sustained by the simultaneous onset of BEV model launches requiring new fascia design and tooling investment, ADAS content growth adding sensor housing value to front fascia assemblies, and global vehicle production recovery to pre-pandemic levels.

To get more information on this market, Request Sample

Passenger cars grow at ~5.2% CAGR as BEV platform launch cadence each requiring new front fascia tooling investment, and ADAS front fascia sensor content progressively growing from single forward radar in 2020 to multi-sensor fusion front fascia modules by 2028-2030. OEM channel grows at ~5.1% CAGR driven by new vehicle model launches, platform refreshes, and the content value uplift from ADAS-integrated front fascia modules.

Executive Summary

The global automotive fascia market reached USD 16.89 Billion in 2025, representing one of the automotive exterior component industry's most dynamically evolving product categories. An automotive fascia is the vehicle's most visually defining exterior element and increasingly its functional interface for ADAS sensors, aerodynamic active management, and pedestrian safety systems. The market encompasses injection-moulded polypropylene (PP) and thermoplastic polyolefin (TPO) fascia covers, painted fascia systems with Class A surface quality, active aerodynamic fascia, sensor-integrated front fascia modules, and premium chrome and decorative trim fascia components. The market is projected to reach USD 26.58 Billion by 2034.

Passenger cars at 74.8% dominate through their vastly larger production volume and the highest per-unit fascia value uplift from ADAS sensor integration and premium design language investment concentrated in passenger car platforms. The OEM channel at 71.5% leads as new vehicle production represents the primary fascia procurement event, with the aftermarket providing the collision repair and replacement market. Asia-Pacific at 39.6% leads through China's world-leading vehicle production and BEV model launch cadence, Japan's fascia quality standard-setting, and South Korea's distinctive EV design language.

Key Market Insights

|

Insight |

Data |

|

Dominant Vehicle Type |

Passenger Cars - 74.8% revenue share (2025) |

|

Dominant Sales Channel |

OEM - 71.5% market share (2025) |

|

Leading Region |

Asia-Pacific - 39.6% market share (2025) |

Key Analytical Observations Supporting the Above Data:

- Passenger Cars at 74.8%: The passenger cars segment dominates due to high global passenger vehicle production and strong demand for attractive exterior styling. Rising adoption of EVs and SUVs is also increasing fascia use for aerodynamics, sensor integration, and brand differentiation.

- OEM channel at 71.5%: The OEM channel dominates as fascias are primarily installed during vehicle manufacturing and are customized to each model’s design, safety, and aerodynamic requirements. Strong vehicle production volumes and automaker-led styling updates further support OEM demand.

- Asia-Pacific at 39.6%: The Asia-Pacific region dominates due to high vehicle production volumes, especially in China, India, Japan, and South Korea. Strong passenger car demand, expanding EV manufacturing, and cost-efficient automotive component production further support regional dominance.

Automotive Fascia Market Overview

The global automotive fascia market encompasses the design, manufacture, and supply of all bumper cover and front fascia system components fitted to passenger cars, commercial vehicles, buses, and specialty vehicles at original equipment manufacturer (OEM) production and through aftermarket collision replacement channels.

The ecosystem integrates fascia module manufacturers, polymer resin suppliers, paint and surface finish suppliers, tooling and mould manufacturers, ADAS sensor companies integrating into front fascia, OEM vehicle manufacturers specifying and integrating front fascia systems, and aftermarket distribution organizations. Macroeconomic factors include rising vehicle production, urbanization, growing disposable incomes, and increasing consumer preference for stylish and fuel-efficient vehicles.

Market Dynamics

To evaluate market opportunities, Request Sample

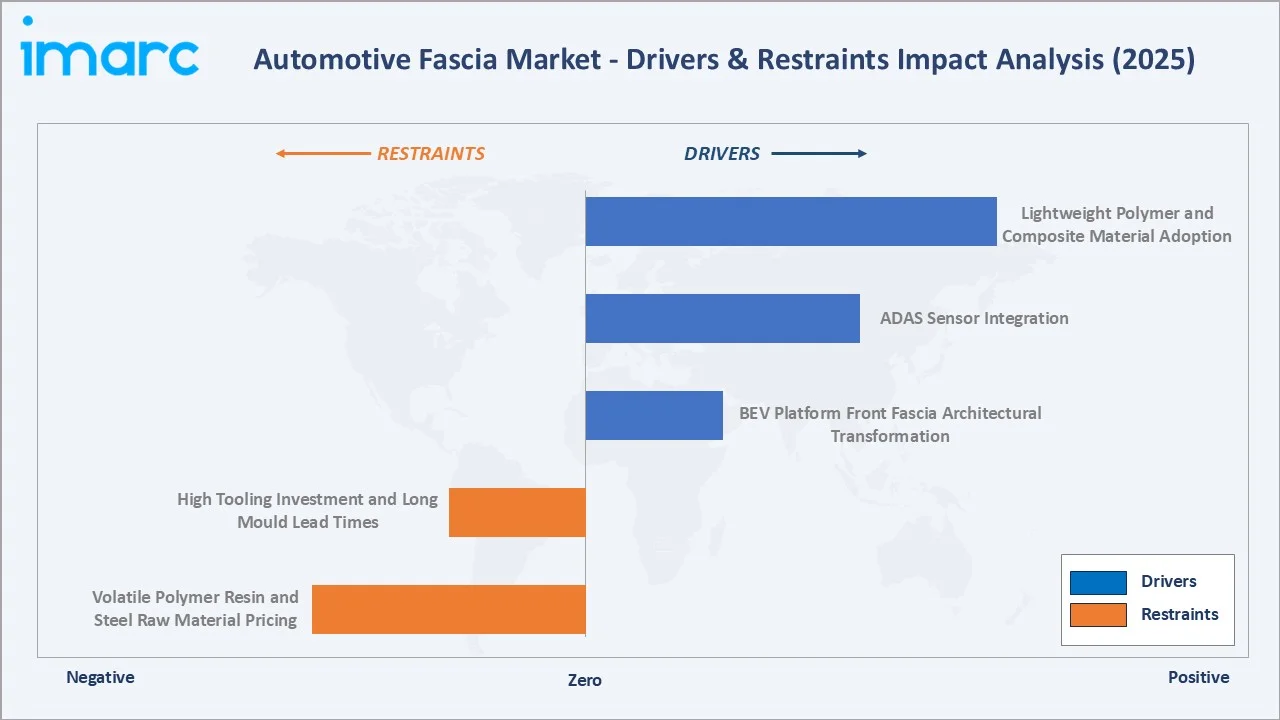

Market Drivers

- BEV Platform Front Fascia Architectural Transformation: The BEV platform front fascia architectural transformation is reshaping front-end vehicle design due to the absence of traditional internal combustion engine components. BEVs increasingly use closed grilles, aerodynamic fascia designs, and integrated sensor housings to improve efficiency and support ADAS technologies. This shift is increasing demand for lightweight, multifunctional, and aesthetically advanced fascia systems in electric vehicles.

- ADAS Sensor Integration: ADAS sensor integration is driving as modern vehicles increasingly incorporate radar, cameras, LiDAR, and other sensors within front and rear fascia systems. Fascias are being redesigned to support sensor placement while maintaining aerodynamic performance and vehicle aesthetics. This is increasing demand for advanced fascia materials and multifunctional designs, particularly in EVs and autonomous-ready vehicles. In October 2025, Aptiv introduced its most advanced radar technology, Gen 8 radars, designed to meet the growing requirements of future ADAS applications. Built with Aptiv’s proprietary antenna and silicon design, the radars deliver high-resolution sensing and strong performance to support AI- and machine learning-enabled driver assistance systems. This growing ADAS adoption is pushing fascia designs to accommodate sensors while maintaining vehicle styling, aerodynamics, and safety performance.

- Lightweight Polymer and Composite Material Adoption: Lightweight polymer and composite material adoption helps automakers reduce vehicle weight and improve fuel efficiency or EV driving range. These materials also offer better design flexibility, impact resistance, corrosion resistance, and aerodynamic shaping. As OEMs focus on sustainability, performance, and advanced exterior styling, demand for polymer- and composite-based fascia systems continues to grow.

Market Restraints

- Volatile Polymer Resin and Steel Raw Material Pricing: Volatile polymer resin and steel raw material pricing are increasing production cost uncertainty for fascia manufacturers. Fluctuating prices of plastics, composites, reinforcement materials, and steel components can pressure supplier margins and raise OEM procurement costs. This may delay sourcing decisions, affect pricing contracts, and reduce profitability across the fascia supply chain.

- High Tooling Investment and Long Mould Lead Times: High tooling investment and long mould lead times increase upfront development costs for new vehicle models and design updates. Fascia production requires model-specific moulds, precision tooling, validation, and testing, which can extend launch timelines. This creates challenges for suppliers and OEMs, especially when frequent styling changes or EV platform redesigns require new fascia tooling.

Market Opportunities

- Heated Radome Integration Solving Cold Climate ADAS Performance Challenge: Heated radome integration improves ADAS sensor performance in snow, ice, fog, and cold-weather conditions. Heated radomes help keep radar and sensor areas clear, ensuring reliable detection and safety functionality. As automakers expand ADAS-equipped vehicles across colder regions, demand is rising for advanced fascia systems with integrated heating, sensor protection, and styling compatibility.

- Fascia as Structural Battery Enclosure Integration for Future EV Architectures: Fascia as structural battery enclosure integration, making future EV fascia designs more functional beyond styling and aerodynamics. As EV architectures evolve, fascia systems may support battery protection, crash energy absorption, thermal management, and underbody packaging efficiency. This can increase demand for advanced lightweight materials, reinforced polymers, and multifunctional fascia modules designed specifically for next-generation EV platforms.

Market Challenges

- Increasingly Complex ADAS Sensor Mounting Accuracy Requirements Demanding Precision Manufacturing Capability: Increasingly complex ADAS sensor mounting accuracy requirements demanding tighter manufacturing tolerances and precise sensor positioning. Even minor alignment errors in radar, camera, or LiDAR mounting areas can affect ADAS performance and safety reliability. This increases the need for advanced tooling, quality control, material stability, and precision manufacturing, raising production complexity and costs.

- ADAS Recalibration Revenue Shift from Fascia Manufacturers to Dealer and OEM Service Networks Disrupting Traditional Aftermarket Economics: ADAS recalibration revenue shift is challenging as sensor-equipped fascia repairs increasingly require calibration by OEMs, dealers, or certified service networks. This reduces aftermarket revenue opportunities for traditional fascia suppliers and independent repair channels. As ADAS complexity grows, fascia replacement becomes more service-intensive, increasing repair costs and changing the traditional aftermarket value chain.

Emerging Market Trends

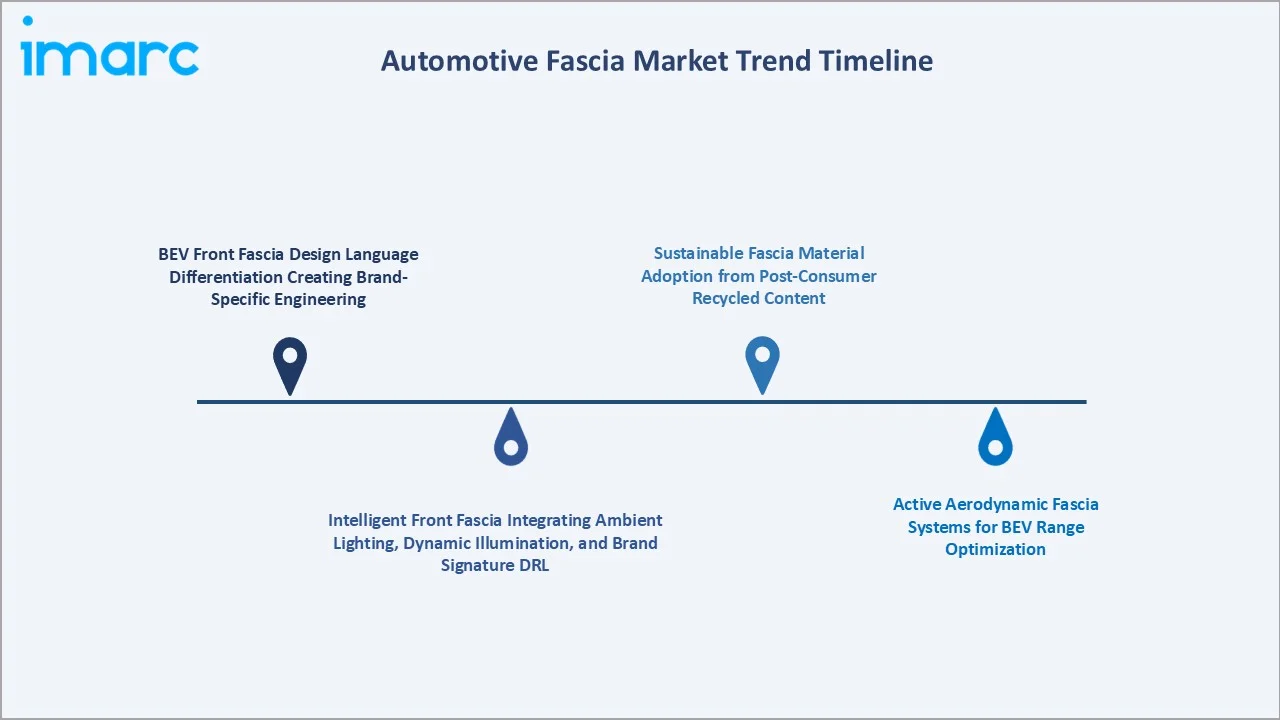

1. BEV Front Fascia Design Language Differentiation Creating Brand-Specific Engineering

BEV front fascia design language differentiation is emerging as electric vehicles move away from traditional grille-based designs. Automakers are using closed grilles, illuminated panels, aerodynamic surfaces, and brand-specific styling to create unique EV identities. This is increasing demand for customized fascia engineering, advanced materials, and model-specific tooling across EV platforms.

2. Intelligent Front Fascia Integrating Ambient Lighting, Dynamic Illumination, and Brand Signature DRL

Intelligent front fascia integration is emerging as automakers use ambient lighting, dynamic illumination, and signature DRLs to create distinctive vehicle identities. These features transform fascias from simple exterior panels into smart styling and communication surfaces. Rising EV and premium vehicle adoption is increasing demand for advanced fascia designs that combine lighting, sensors, aerodynamics, and brand differentiation. In April 2026, Leapmotor launched its new flagship SUV, the D19, offering seven variants priced from 219,800 yuan to 269,800 yuan. The SUV features a “cosmic horizon” front fascia design shared across BEV and extended-range versions, while the BEV variant adds a 176-liter frunk and active air intake. Such designs are increasing demand for advanced fascia systems that integrate lighting, aerodynamics, and signature front-end elements.

3. Sustainable Fascia Material Adoption from Post-Consumer Recycled Content

Sustainable fascia material adoption from post-consumer recycled content is emerging as automakers focus on reducing vehicle carbon footprints and improving circularity. Recycled polymers and composites help lower dependence on virgin plastics while supporting lightweight fascia designs. As OEMs set stronger sustainability targets, demand is rising for fascia components made with recycled, durable, and design-flexible materials.

4. Active Aerodynamic Fascia Systems for BEV Range Optimization

Active aerodynamic fascia systems for BEV range optimization are emerging as EV manufacturers focus on improving energy efficiency and driving range. These systems use active air intakes, movable shutters, and airflow control elements integrated into the fascia to reduce drag and optimize cooling. By improving aerodynamics, automakers can enhance BEV efficiency while maintaining advanced front-end styling and functionality.

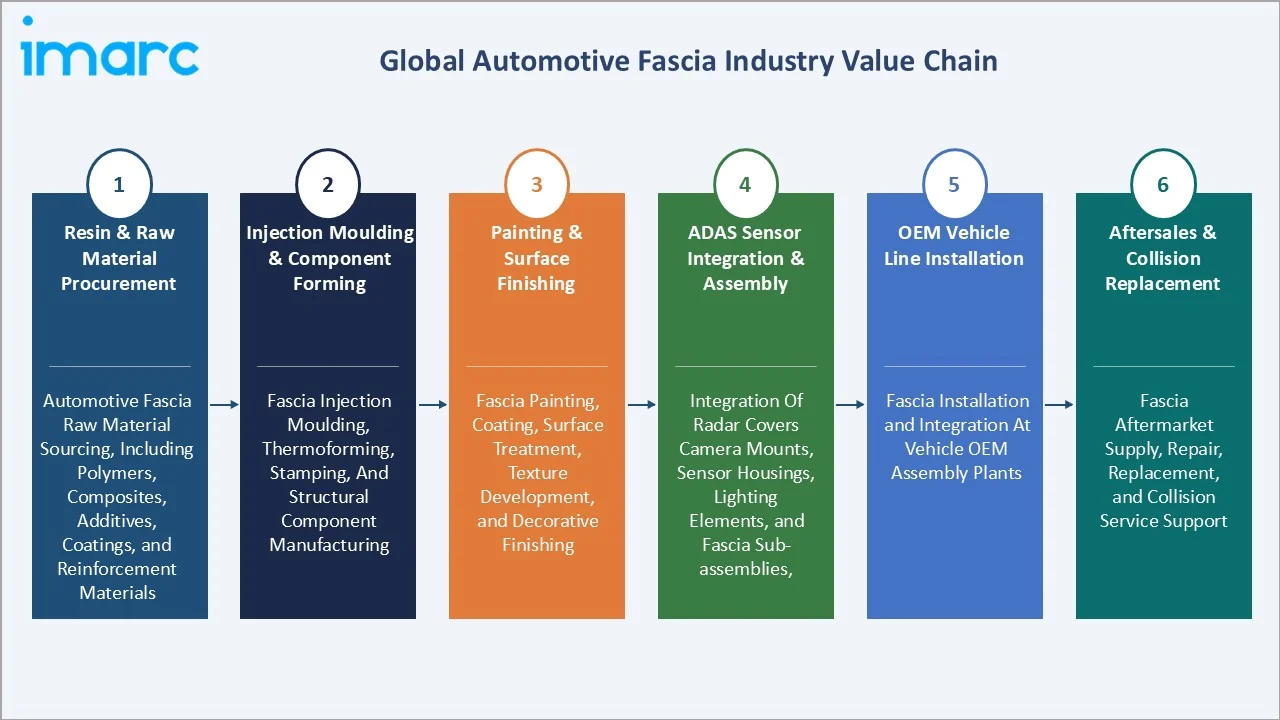

Industry Value Chain Analysis

The automotive fascia value chain integrates resin and raw material procurement, injection moulding & component forming, painting and surface finishing, ADAS sensor integration and assembly, OEM vehicle line installation, and aftersales collision replacement.

|

Stage |

Key Participants |

|

Resin & Raw Material Procurement |

Automotive fascia raw material sourcing, including polymers, composites, additives, coatings, and reinforcement materials |

|

Injection Moulding & Component Forming |

Fascia injection moulding, thermoforming, stamping, and structural component manufacturing |

|

Painting & Surface Finishing |

Fascia painting, coating, surface treatment, texture development, and decorative finishing |

|

ADAS Sensor Integration & Assembly |

Integration of radar covers camera mounts, sensor housings, lighting elements, and fascia sub-assemblies |

|

OEM Vehicle Line Installation |

Fascia installation and integration at vehicle OEM assembly plants |

|

Aftersales & Collision Replacement |

Fascia aftermarket supply, repair, replacement, and collision service support |

The ADAS sensor integration stage is the value chain's most commercially dynamic and technically challenging tier, integrating forward radar, camera brackets, ultrasonic sensors, and active grille shutter actuators with precise mounting accuracy into an injection-moulded polymer fascia assembly, which requires a manufacturing environment combining plastic component dimensional control with electronic sensor mounting precision.

Technology Landscape in the Automotive Fascia Industry

Advanced Polymer Materials for Front Fascia

Advanced polymer materials for front fascia enabling lightweight, durable, and aerodynamically optimized designs. Materials such as polypropylene blends, thermoplastic olefins (TPO), and composite polymers offer improved impact resistance, corrosion resistance, and design flexibility. Their use also supports EV range improvement, sustainability goals, and integration of ADAS sensors and lighting elements.

Injection Moulding Technology for Large-Format Fascia

Injection moulding technology for large-format fascia enables the production of complex, lightweight, and large-sized fascia components with high dimensional accuracy. The technology supports integrated designs incorporating aerodynamic features, sensor mounts, and lighting elements in a single moulded structure. It also improves production efficiency, reduces assembly steps, and supports mass manufacturing for EV and passenger vehicle platforms.

Active Grille Shutter Technology

Active grille shutter technology integrates dynamic airflow control directly into front fascia systems. These shutters automatically open or close to optimize cooling and reduce aerodynamic drag, improving fuel efficiency and EV driving range. In April 2026, Porsche confirmed that its all-electric Cayenne variant debuted globally at the Beijing Auto Show. Built on the PPE platform, the Cayenne Electric Turbo variant delivers 1,156 horsepower and features a closed front fascia with active lower-bumper grille shutters to improve aerodynamics. These shutters help reduce drag, manage cooling needs, and improve overall vehicle efficiency and driving range.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Material |

🔒 |

🔒 |

2025 |

|

Position Type |

🔒 |

🔒 |

2025 |

|

Vehicle Type |

Passenger Cars |

74.8% |

2025 |

|

Sales Channel |

OEM |

71.5% |

2025 |

|

Region |

Asia Pacific |

39.6% |

2025 |

By Vehicle Type

Passenger cars lead at 74.8% (2025). The passenger car fascia market is driven by the highest global production volumes, the BEV model launch cadence creating continuous new fascia tooling investment, and the highest per-vehicle ADAS and design content value concentration. The transition from ICE-architecture fascia to BEV-architecture fascia is creating above-production-volume fascia revenue growth in the passenger car segment as content value per vehicle increases with each technology generation.

To access detailed market analysis, Request Sample

Commercial vehicles at 25.2% represent the truck, bus, and commercial van fascia market with above-average per-unit fascia content from large-format front systems, progressive ADAS adoption, and electric commercial vehicle platform transformation.

By Sales Channel

OEM channel leads at 71.5% (2025). OEM fascia is procured through multi-year platform supply contracts with just-in-time delivery logistics, creating stable, high-volume relationships between fascia manufacturers and vehicle assembly plants. The OEM channel's ~5.1% CAGR reflects both vehicle production growth and content value inflation from ADAS integration. BEV model launches, creating new OEM fascia tool investment cycles, sustain OEM channel growth above base vehicle production volume growth through the forecast period.

The aftermarket channel at 28.5% is experiencing structural change from ADAS technology. While traditional aftermarket fascia replacement economics sustain volume in the large legacy vehicle parc, ADAS-equipped vehicle fascia replacement increasingly favours OEM-quality and certified aftermarket products that guarantee sensor mounting accuracy.

Regional Market Insights

|

Region |

Share (2025) |

Key Automotive Fascia Market Drivers & Characteristics |

|

Asia-Pacific |

39.6% |

Driven by high vehicle production volumes, expanding EV manufacturing, and strong demand for passenger vehicles and lightweight automotive components |

|

Europe |

25.4% |

Driven by premium vehicle production, EV adoption, advanced exterior styling trends, and integration of ADAS-enabled vehicle components |

|

North America |

19.7% |

Supported by strong SUV and pickup vehicle demand, increasing EV production, and the adoption of advanced front-end design technologies |

|

Latin America |

8.4% |

Driven by vehicle production expansion, rising passenger car demand, and automotive manufacturing investments |

|

Middle East and Africa |

6.9% |

Emerging with increasing vehicle imports, premium vehicle demand, and growing interest in modern automotive styling and EV adoption |

Asia-Pacific, at 39.6%, leads through China's BEV production scale, Japan's quality manufacturing standard, South Korea's BEV distinctive design, and India's growing vehicle production. Europe, at 25.4%, reflects premium fascia engineering and BEV regulatory mandate transformation.

North America, at 19.7%, sustains through pickup truck large-format fascia premium and US BEV model launches. Latin America, at 8.4%, and MEA, at 6.9%, represent emerging growth markets with progressive ADAS content adoption from global platform localization.

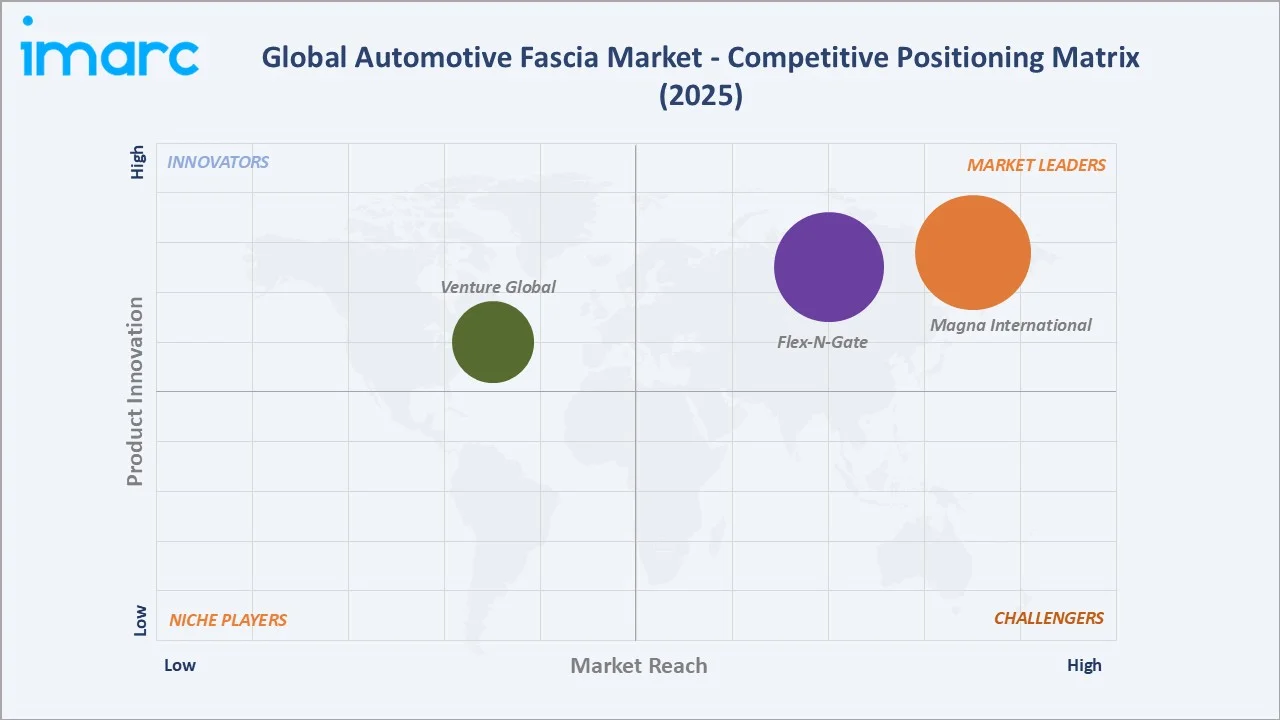

Competitive Landscape

The automotive fascia market's competitive landscape is moderately concentrated at the Tier-1 system supplier level. The concentration reflects the capital intensity of large-format injection moulding equipment and fascia tooling, proximity manufacturing requirements, and the technical barriers of Class A painting quality, ADAS sensor integration capability, and logistics that limit meaningful market participation to large, well-capitalized Tier-1 suppliers with global manufacturing networks.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Magna International Inc. |

Front and rear fascias |

Market Leader |

Magna International Inc. plays a significant role in the design, engineering, and manufacturing of automotive fascias (front and rear bumper covers). |

|

Venture Global |

Fascia systems |

Niche Player |

Venture Global focuses on the design, engineering, and manufacturing of interior and exterior plastic components, including fascia systems. |

|

Flex-N-Gate |

Front and Rear Fascia |

Market Leader |

Flex-N-Gate specializes in the design, engineering, and manufacturing of automotive fascia systems, front/rear bumper systems, and exterior trim. |

The competitive boundary between fascia manufacturers and ADAS sensor companies is progressively blurring as fascia content increasingly includes sensor housing, mounting calibration, and functional integration, creating collaboration and competition between traditional fascia Tier-1s and ADAS Tier-1s.

Key Company Profiles

Magna International Inc.

Magna International Inc. is a global automotive supplier with a strong presence in the automotive fascia market through its front and rear fascias, exterior systems, front-end modules, and active aerodynamic components. The company designs and manufactures fascia systems for passenger vehicles, SUVs, and electric vehicles, supporting both conventional and next-generation vehicle platforms.

- Key Products: Front and rear fascias.

- Recent Developments: In May 2026, Magna honored by General Motors with five 2025 Supplier of the Year awards, highlighting its strong performance and trusted supplier role across global programs. The company received recognition in the Creativity Team categories of frames, transfer cases, rubber sealing, exterior moldings, and fascias.

- Strategic Focus: Developing lightweight, aerodynamic, and ADAS-compatible fascia systems for conventional and electric vehicles.

Flex-N-Gate

Flex-N-Gate is a privately held automotive component manufacturer with a strong presence in the automotive fascia market through its front and rear fascia systems, painted exterior components, front-end modules, and grille assemblies.

- Key Products: Front and Rear Fascia.

- Strategic Focus: Expanding large-scale bumper fascia and painted exterior component manufacturing for global OEMs.

Market Concentration Analysis

The automotive fascia market is moderately concentrated at the global Tier-1 system supplier level. Concentration is highest in North America and lower in the Asia Pacific, where Japanese OEM-captive fascia relationships and Chinese domestic suppliers distribute market share across a broader supplier base. The competitive dynamics in China are creating market concentration disruption. Chinese domestic fascia quality has improved sufficiently for Chinese domestic OEM standard applications, while Japanese and European fascia manufacturers maintain quality differentiation for export-destined China production and highest-specification OEM programmes requiring premium surface quality and ADAS precision.

Investment & Growth Opportunities

Highest Growth Segments

Passenger car BEV fascia (~6-7% CAGR from new platform launches), ADAS-integrated front-end modules (~8-10% CAGR from small base), active aerodynamic fascia AGS (~9% CAGR), heated radome fascia technology (~12% CAGR from near-zero base), sustainable PCR polymer fascia (~8% CAGR from regulatory mandate), commercial vehicle EV fascia (~5-6% CAGR), and India and Southeast Asia OEM fascia localization (~8-10% CAGR) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

ADAS-calibrated aftermarket fascia supply chain development represents an emerging premium aftermarket opportunity. ADAS recalibration requirements are progressively segmenting the aftermarket fascia market into a premium ADAS-calibrated tier at 2-3x standard aftermarket pricing. Companies investing in dimensional validation infrastructure, ADAS sensor mounting accuracy verification, and calibration centre partnership development can capture the premium aftermarket tier before insurance company requirements crystallise into specific product certification mandates.

Investment Themes

- BEV front fascia tooling and manufacturing investment to capture the once-per-platform new BEV model programme wave: The 2026-2034 period represents the peak BEV model launch cadence globally. Fascia manufacturers investing in BEV-specific design capability, ADAS sensor integration assembly, and active aerodynamic fascia manufacturing are positioned to win BEV programme fascia awards that carry 6-8 year production lifetime supply contracts at above-commodity content value.

- Smart front-end module integration capability combining fascia, lighting, radar, and camera in a single system delivery: Developing complete front-end module (FEM) capability, combining injection moulded fascia, active grille shutter, forward radar mounting and harness, camera bracket, ambient DRL lighting, and bumper carrier into a single verified module delivered JIT to OEM vehicle assembly, creates above-commodity fascia value capture at USD 600-1,500 per FEM versus USD 150-350 for standalone fascia.

Future Market Outlook (2026-2034)

The global automotive fascia market is projected to grow from USD 16.89 Billion in 2025 to USD 26.58 Billion by 2034, delivering a 5.01% CAGR over the forecast period. The market's anchor value of USD 21.57 Billion in 2030 represents an automotive fascia industry at its most transformative commercial inflection. BEV platforms will have displaced ICE as the majority of new vehicle sales in China and Europe, each BEV requiring a distinctive closed-grille front fascia architecture with sensor integration and active aerodynamic management that represents 30-60% higher content value than the ICE fascia it replaces. The structural shift from passive exterior panel to intelligent sensing and aerodynamic management platform is the defining commercial narrative that sustains above-vehicle-production-growth fascia market revenue through the forecast period. Three structural forces define automotive fascia market growth through 2034 with confidence. The BEV model launch cadence is irreversible. The ADAS content ladder is compounding. The global vehicle parc growth sustains aftermarket fascia demand.

Research Methodology

Primary Research

Primary research comprised structured interviews with 55+ industry stakeholders (2025), including VP Engineering Directors; Business Development Directors; Engineering Directors; OEM fascia programme leads; ADAS integration leads; paint and surface quality specialists; and aftermarket fascia distribution executives.

Secondary Research

Secondary research encompassed company annual reports; safety rating technical documentation; bumper safety standard technical analysis; Vehicle Directive revision proposal document; International Organization of Motor Vehicle Manufacturers global vehicle production statistics; Automotive global vehicle production and OEM programme data; Plastics Technology magazine automotive injection moulding technology publications; automotive coatings industry data; automotive supplier market analysis 2025. Over 60 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a vehicle-type bottom-up model: (i) global vehicle production forecast by passenger car and commercial vehicle type; (ii) average fascia content value per vehicle by segment, ADAS level, and technology tier; (iii) OEM versus aftermarket split based on historical replacement rate and growing ADAS complexity, and aftermarket value inflation.

Automotive Fascia Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Materials Covered |

|

| Position Types Covered | Front Fascia, Rear Fascia |

| Vehicle Types Covered | Passenger Cars, Commercial Vehicle |

| Sales Channels Covered | OEM, Aftermarket |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Magna International Inc., Venture Global, Flex-N-Gate, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive fascia market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global automotive fascia market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive fascia industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive Fascia Market Report

The global automotive fascia market reached USD 16.89 Billion in 2025, driven by passenger cars at 74.8% market share, global vehicle production, the OEM channel dominating at 71.5% through just-in-time vehicle assembly supply, Asia-Pacific leading at 39.6% through China's BEV model launch cadence and Japan's manufacturing standard-setting, and progressive ADAS integration creating content value growth above underlying vehicle production volume growth.

The market grows at 5.01% CAGR during 2026-2034, reaching USD 26.58 Billion by 2034. This growth reflects global vehicle production expansion of 2-3% annually, a new BEV platform fascia tooling investment wave creating above-production-growth fascia revenue, ADAS content value inflation, active aerodynamic fascia adoption, and sustainable polymer content requirements creating a compliance-driven value layer above commodity fascia pricing.

Passenger cars lead at 74.8% and grow at ~5.2% CAGR through global production volume dominance, BEV model launch cycle creating new fascia tooling investment per model, ADAS sensor integration content value growth, and premium design language investment concentrated in passenger car front fascia.

OEM channel leads at 71.5% through new vehicle production, just-in-time fascia delivery relationships, multi-year platform supply contracts creating stable high-volume procurement, and BEV model launches creating new OEM programme award cycles.

Asia-Pacific leads at 39.6% through China's world-leading BEV production and India's growing passenger vehicle production.

Leading companies include Magna International Inc., Venture Global, and Flex-N-Gate, among others.

The market is projected to reach approximately USD 21.57 Billion by 2030, with BEV front fascia accounting for 30-35% of new vehicle production, each requiring above-ICE content value, and heated radome technology transitioning from premium to mainstream segment adoption.

Automotive fascia refers to the complete front and rear bumper cover and associated assembly systems that form the vehicle's protective and aesthetic front and rear faces. Components include: injection-moulded bumper fascia cover; bumper carrier or reinforcement beam; energy absorber; grille assembly; active grille shutter; sensor mounting hardware; and decorative trim elements.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade