Automotive Hydrostatic Fan Drive System Market Size, Share, Trends and Forecast by Component, Pump Type, Vehicle Type, and Region 2026-2034

Automotive Hydrostatic Fan Drive System Market Size, Share, Trends & Forecast (2026-2034)

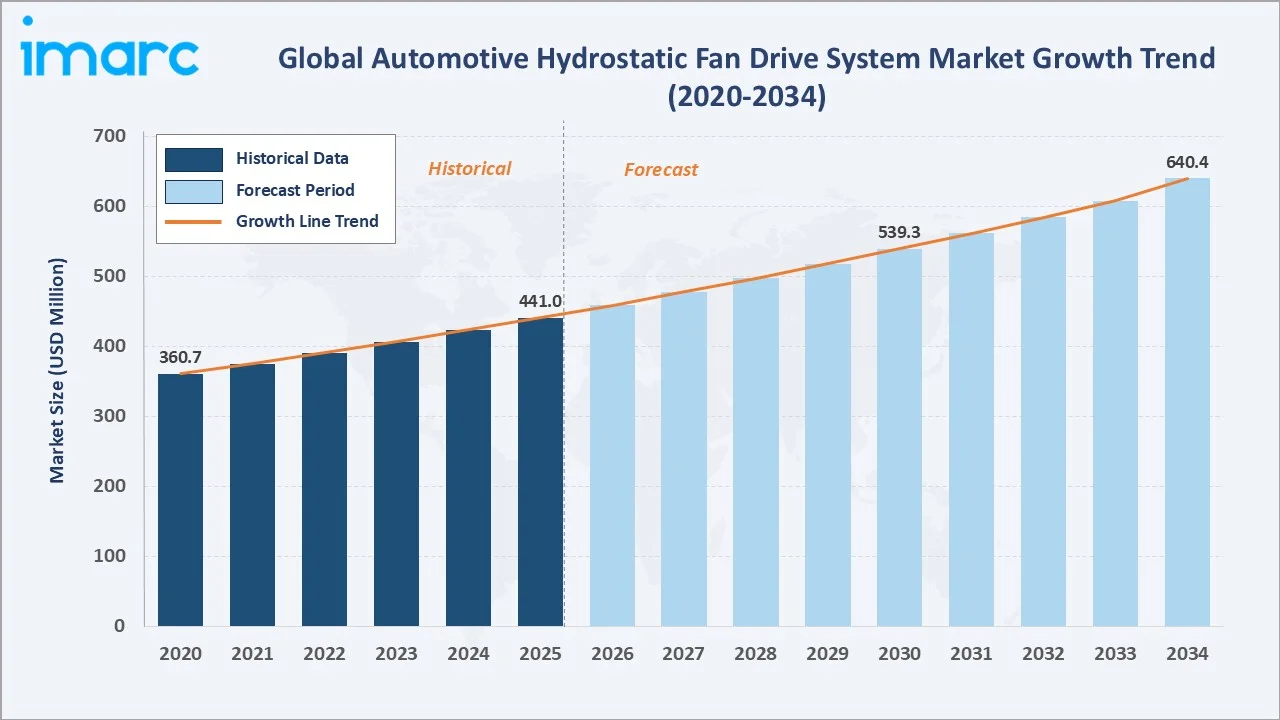

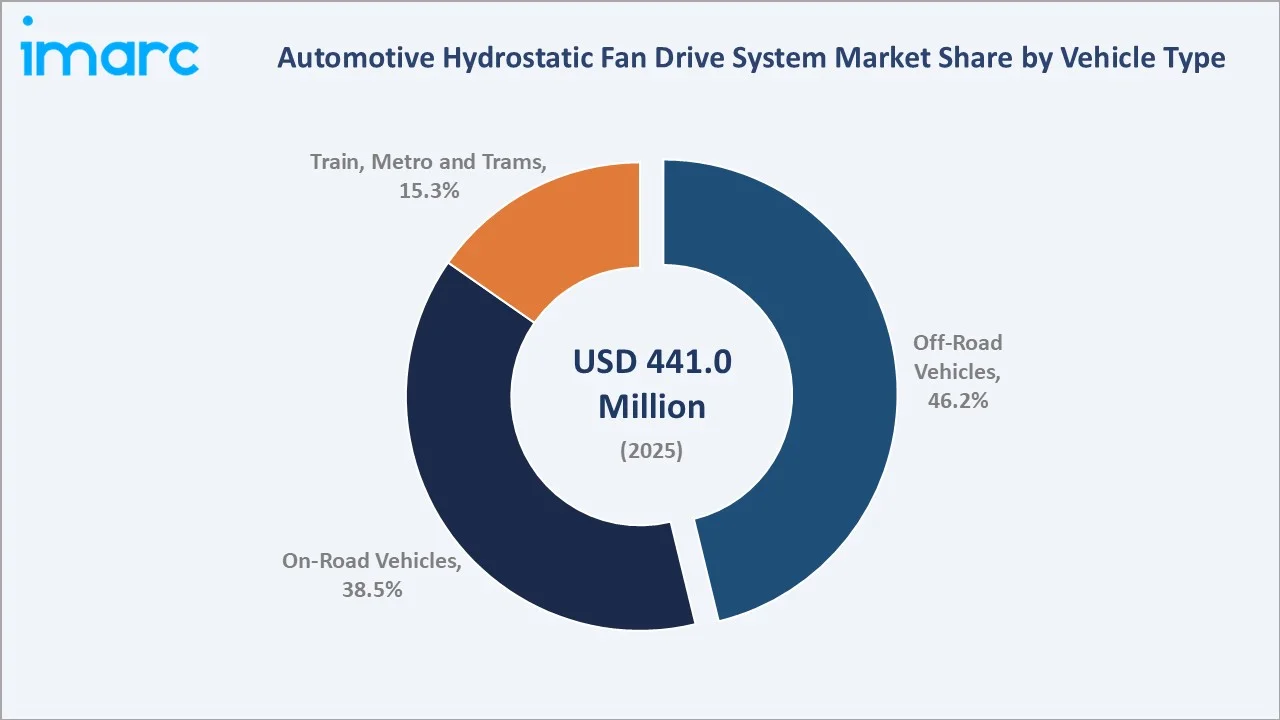

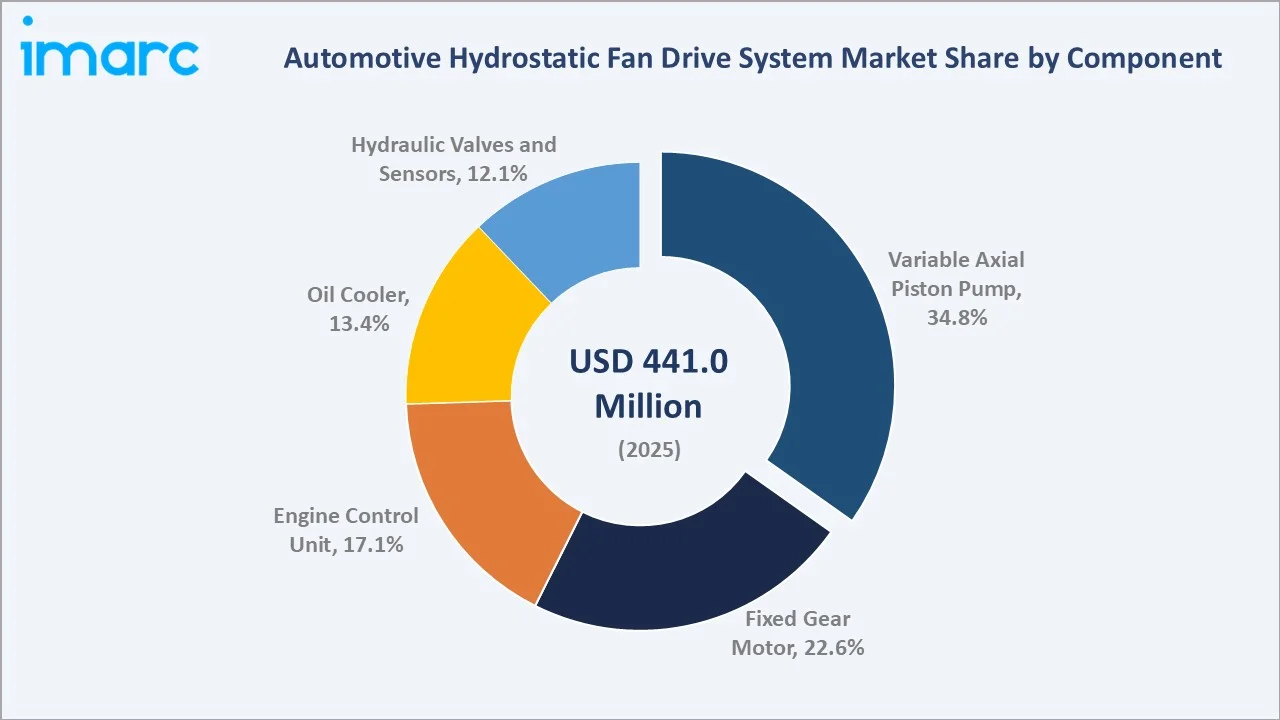

The global automotive hydrostatic fan drive system market reached USD 441.0 Million in 2025 and is projected to reach USD 640.4 Million by 2034, growing at a CAGR of 4.10% during 2026-2034. Market growth is driven by stringent emission and fuel economy regulations, expanding off-road and commercial vehicle fleets, and rising adoption of variable-speed hydrostatic cooling systems that reduce parasitic engine losses.

Market Snapshot

| Metric | Value |

|---|---|

| Market Size (2025) | USD 441.0 Million |

| Forecast Market Size (2034) | USD 640.4 Million |

| CAGR (2026-2034) | 4.10% |

| Base Year | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

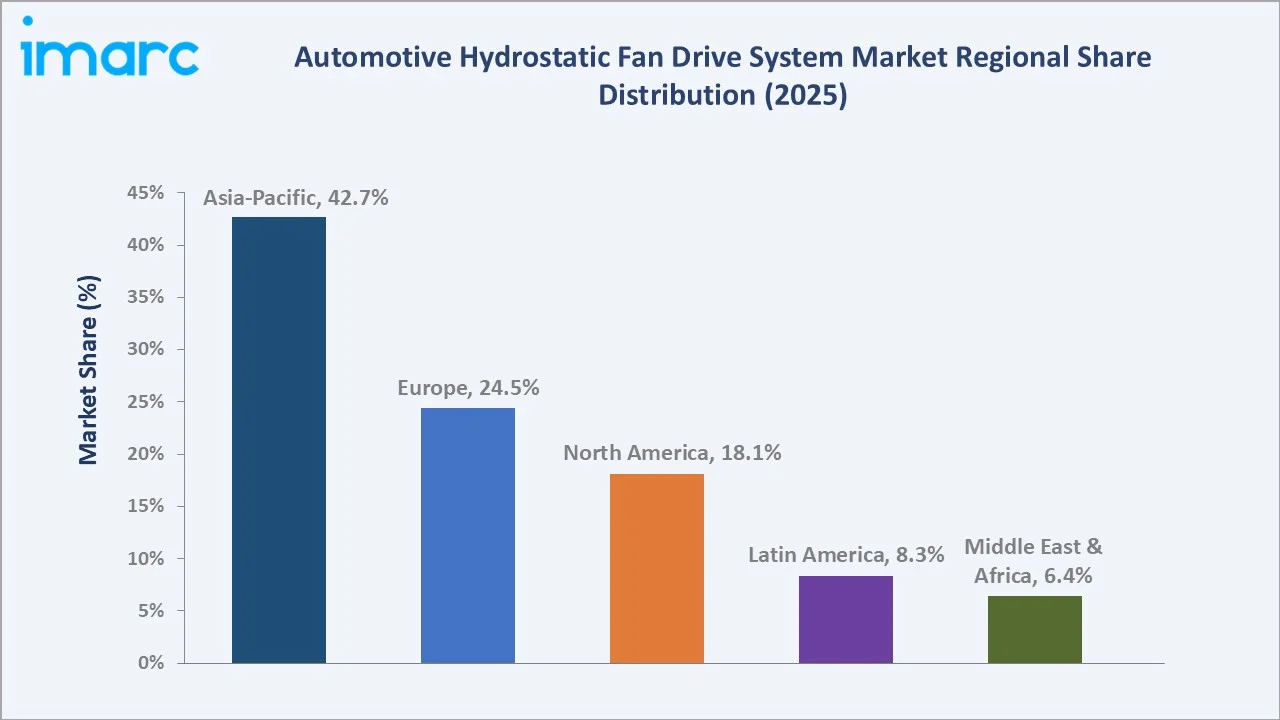

Asia-Pacific leads with a 42.7% regional share in 2025, while off-road vehicles represent the largest vehicle type segment at 46.2%, and variable axial piston pumps command the highest component share at 34.8%. Asia-Pacific's dominance is anchored by China's large off-highway equipment manufacturing base, India's growing commercial vehicle fleet under BS-VI compliance mandates, and Japan's advanced hydraulics industry.

To get more information on this market, Request Sample

The market's consistent 4.10% CAGR is underpinned by the structural shift from belt-driven mechanical fans to electronically controlled hydrostatic systems, which reduce fuel consumption by 3–8% and lower cooling-system noise by up to 10 dB across heavy commercial and off-road vehicle applications.

Executive Summary

The global automotive hydrostatic fan drive system market is experiencing steady, broad-based growth driven by emission compliance imperatives, expanding off-road equipment fleets, and the industry-wide transition from fixed-speed mechanical fans to variable-speed hydrostatic cooling platforms. From USD 441.0 Million in 2025, the market is forecast to reach USD 640.4 Million by 2034, creating incremental value of USD 199.4 Million at a 4.10% CAGR.

Off-road vehicles lead with a 46.2% vehicle type share, driven by the deployment of hydrostatic fan drives in excavators, wheel loaders, agricultural tractors, and mining haul trucks, all applications where variable engine-load profiles demand intelligent, demand-responsive cooling. Variable axial piston pumps command a 34.8% share of the component segment, reflecting their role as the highest-value, performance-critical element in any hydrostatic fan drive system.

Key players, including Robert Bosch GmbH, Parker-Hannifin Corporation, and Bucher Industries AG, compete through proprietary variable-displacement pump and motor technologies, integrated ECU-control algorithms, and long-term OEM supply agreements in the off-highway and commercial vehicle segments.

Key Market Insights

| Insight | Data |

|---|---|

| Largest Vehicle Type | Off-Road Vehicles – 46.2% share (2025) |

| Largest Component | Variable Axial Piston Pump – 34.8% share (2025) |

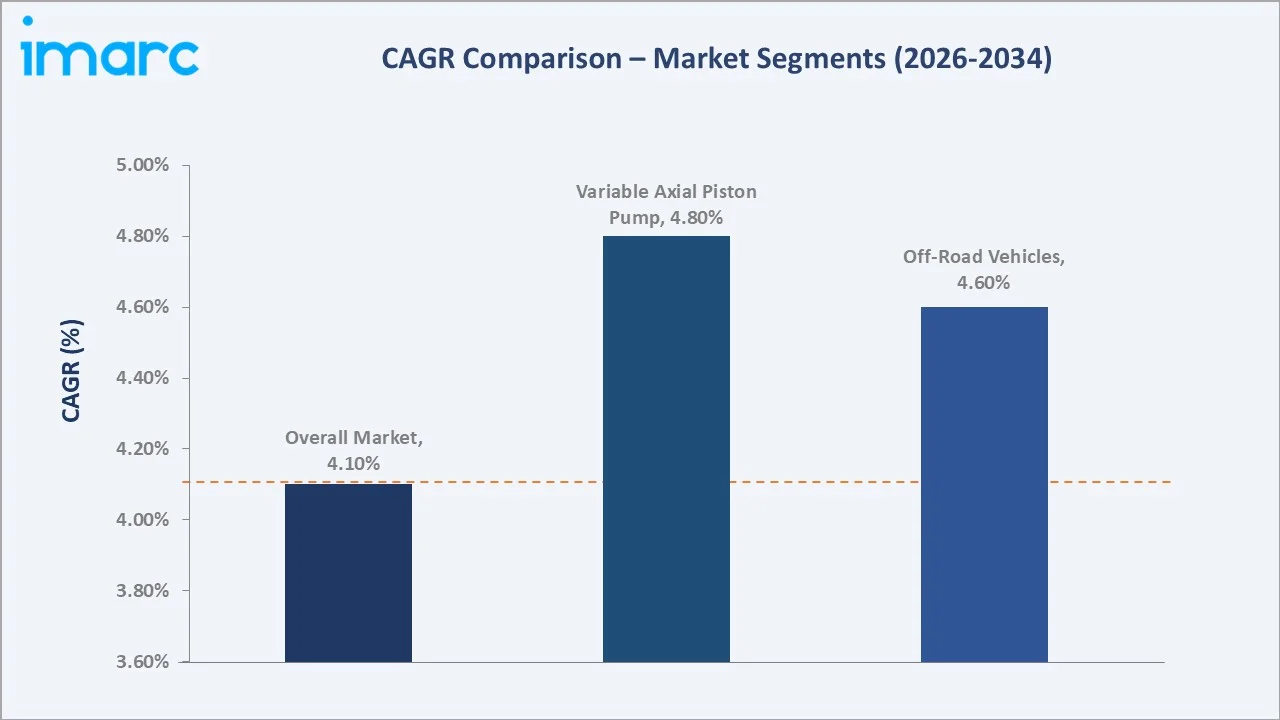

| Fastest Growing Vehicle Type | Off-Road Vehicles – ~4.60% CAGR (2026-2034) |

| Fastest Growing Component | Variable Axial Piston Pump – ~4.80% CAGR (2026-2034) |

| Leading Region | Asia-Pacific – 42.7% share (2025) |

| Top Companies | Robert Bosch GmbH, Parker-Hannifin Corporation, Bucher Industries AG |

Key Analytical Observations:

- Off-road vehicles account for 46.2% of the global hydrostatic fan drive market in 2025. This dominance reflects the inherent thermal management challenges of construction, agricultural, and mining equipment that operate under high and variable engine loads.

- Variable axial piston pumps at 34.8% (2025) are the highest-value component in hydrostatic fan drive systems. These variable-displacement hydraulic pumps regulate fan speed continuously based on ECU signals and coolant temperature feedback, enabling 3–8% fuel savings.

- On-road vehicles represent 38.5% of the market in 2025. Heavy commercial trucks, long-haul buses, and urban transit vehicles in this segment require hydrostatic fan drives for their ability to decouple fan speed from engine RPM, delivering consistent cooling performance during low-speed urban operation.

- Asia-Pacific's 42.7% (2025) dominance is driven by China's construction equipment boom, India's commercial vehicle growth under BS-VI emission norms, and Japan's precision hydraulics manufacturing ecosystem supplying global OEM platforms with high-quality pump, motor, and valve components.

Automotive Hydrostatic Fan Drive System Market Overview

An automotive hydrostatic fan drive system is a specialized mechanism that uses hydraulic fluid and a variable-displacement pump-motor circuit to control radiator fan speed based on real-time cooling demand. Unlike belt-driven mechanical fans that operate at a fixed ratio to engine speed, hydrostatic systems allow the fan to run at any speed from zero to maximum, regardless of engine RPM. The system architecture includes a variable axial piston pump, a fixed gear motor, an engine control unit (ECU), an oil cooler, and hydraulic control valves and sensors.

The market serves off-road vehicles (excavators, wheel loaders, agricultural tractors, mining haul trucks), on-road commercial vehicles (HCVs, buses, emergency vehicles), and rail applications (locomotives, metro trains, trams). Demand is primarily OEM-driven at the vehicle assembly stage, with a growing aftermarket replacement channel serving the aging global commercial and off-highway vehicle installed base.

Market Dynamics

To evaluate market opportunities, Request Sample

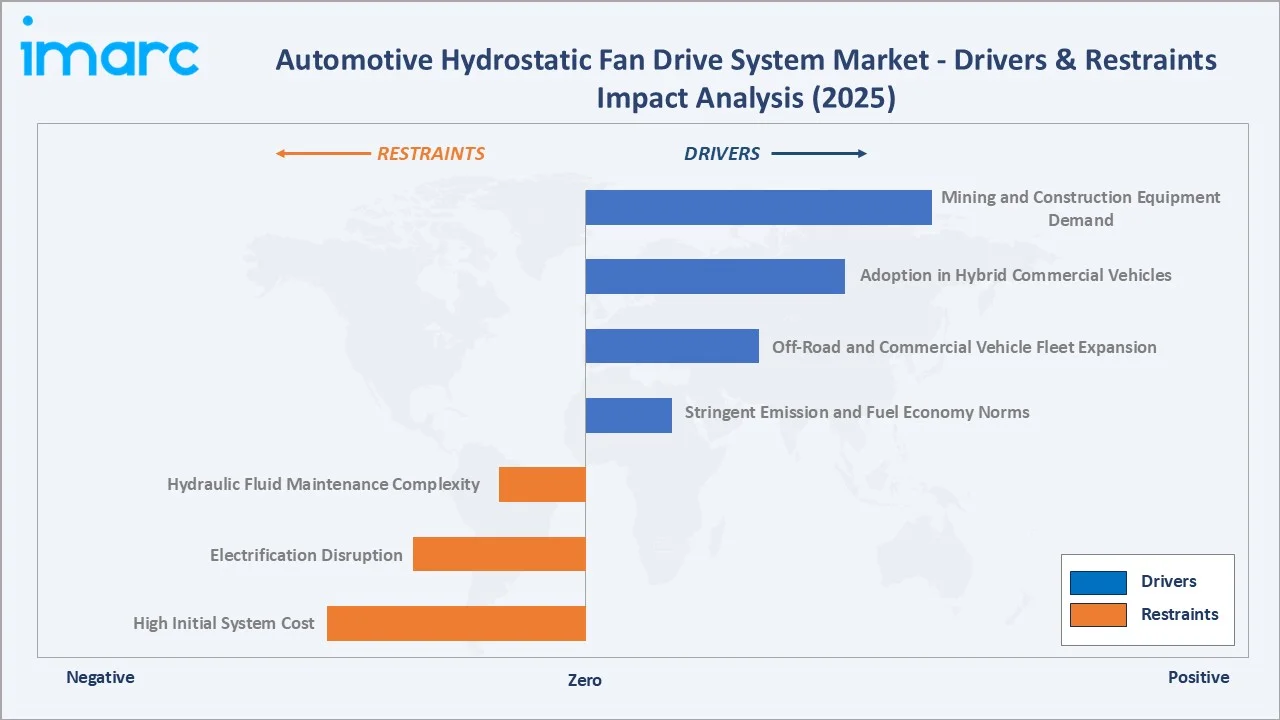

Market Drivers

- Stringent Emission and Fuel Economy Norms: Euro VI, China-VI, and EPA GHG Phase 3 standards mandate measurable reductions in fuel consumption and CO₂ emissions from heavy commercial vehicles. Hydrostatic fan drives that deliver 3–8% fuel savings over belt-driven alternatives provide a cost-effective compliance pathway, making them a standard OEM specification for new commercial vehicles in regulated markets.

- Off-Road and Commercial Vehicle Fleet Expansion: The global construction equipment market is projected to grow at approximately 3.31% CAGR through 2034, driven by infrastructure programs in Asia-Pacific, the Middle East, and Africa. Each excavator, wheel loader, or mining truck produced requires a hydrostatic fan drive system, directly underpinning market volume growth.

- Adoption in Hybrid Commercial Vehicles: Hybrid trucks and buses, where the engine operates intermittently and at variable loads, benefit disproportionately from hydrostatic fan drives. The ability to maintain cooling independently of engine RPM is architecturally required for hybrid powertrain configurations, making hydrostatic fan drives a design necessity rather than a premium option.

- Mining and Construction Equipment Demand: The global mining equipment market exceeded USD 162.9 Billion in 2025 and continues to grow as resource extraction expands in Australia, Chile, and Central Africa. Mining haul trucks operating in extreme ambient temperatures of 40–50°C demand hydrostatic fan drives for reliable, continuous thermal management under the highest duty cycles.

Market Restraints

- High Initial System Cost: A hydrostatic fan drive system costs USD 800–2,500 per vehicle at OEM pricing, representing a significant premium over conventional belt-driven fan assemblies costing USD 150–400. This cost differential constrains adoption in price-sensitive vehicle segments and developing market applications where total cost of ownership considerations are secondary.

- Electrification Disruption: Electric and fuel-cell commercial vehicles do not require engine-driven cooling circuits, replacing hydrostatic fan drive systems with electric fans controlled directly by battery management systems. As electrification penetrates HCV and bus segments, it creates a structural long-term headwind for hydrostatic fan drive demand in certain on-road applications.

- Hydraulic Fluid Maintenance Complexity: Hydrostatic fan drive systems require periodic hydraulic fluid changes, filter replacements, and pressure calibration, maintenance activities that demand specialized technicians not universally available in developing markets, creating operational barriers that favor simpler mechanical alternatives.

Market Opportunities

- Smart IoT-Enabled Hydrostatic Controls: Integration of IoT sensors and cloud-connected diagnostics into hydrostatic fan drive ECUs enables predictive maintenance, remote calibration, and performance optimization. Parker-Hannifin Corporation's LifeSense technology and Bosch Rexroth's Open Core Engineering platform exemplify this trend, commanding 15–25% revenue premiums over standard systems.

- Rail and Mass Transit Applications: Modernization of locomotive and metro train fleets in Asia-Pacific and Europe is creating a growing market for hydrostatic fan drive systems adapted for rail traction applications. The train, metro, and trams segment at 15.3% represents a high-value, regulatory-driven growth opportunity with long-duration OEM contract economics.

Market Challenges

- Engineering Integration Complexity: Hydrostatic fan drive systems must interface precisely with the vehicle's engine management, coolant circuit, and transmission systems. Integration engineering for each vehicle platform requires significant OEM collaboration, creating long product development cycles of 18–36 months that limit agility in responding to new vehicle platform launches.

- Competition from Electronically Controlled Viscous Clutch Fans: Advanced electronically controlled viscous clutch fan systems offer a lower-cost alternative to hydrostatic drives for certain truck and bus applications, providing some demand-side cooling responsiveness at a cost point closer to conventional mechanical fans, creating direct competitive pressure in the on-road HCV segment.

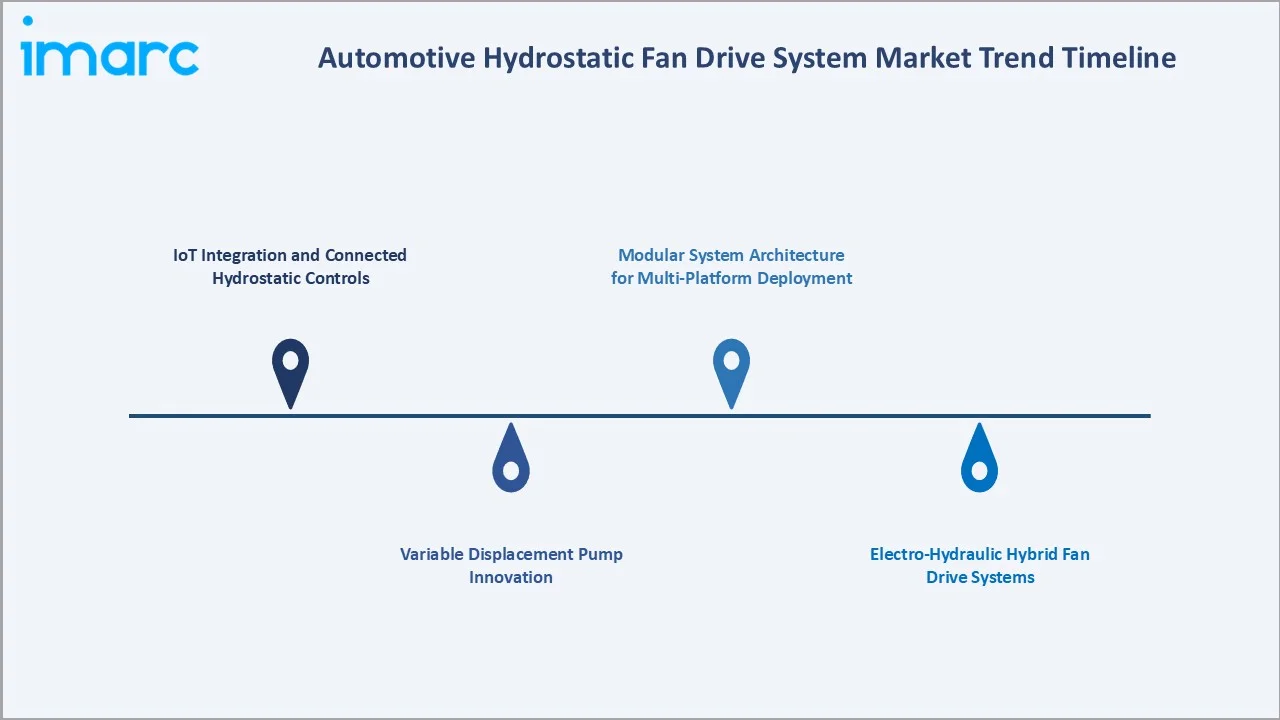

Emerging Market Trends

1. IoT Integration and Connected Hydrostatic Controls

Hydrostatic fan drive ECUs are increasingly being integrated with vehicle telematics platforms, enabling real-time monitoring of pump pressure, motor speed, fluid temperature, and fan efficiency.

2. Variable Displacement Pump Innovation

Bosch Rexroth A1VO Series 10 is a compact axial piston variable pump for open-circuit hydrostatic drives, offering infinitely adjustable flow, low noise, high power density, and adaptable control options. Designed for smaller load-sensing machines, it supports up to 250 bar nominal/280 bar maximum pressure and can deliver up to 15% fuel savings with longer service life than gear pumps.

3. Electro-Hydraulic Hybrid Fan Drive Systems

As mild-hybrid powertrains penetrate the commercial vehicle segment, suppliers are developing electro-hydraulic fan drive architectures that integrate electric motor-driven hydraulic pumps with conventional hydrostatic circuits.

4. Modular System Architecture for Multi-Platform Deployment

Modular hydrostatic fan drive platforms with standardized pump-motor-ECU interfaces can be adapted across multiple vehicle platforms without full system redesign. This approach reduces OEM integration engineering time by an estimated 30–40%, accelerating time-to-market for new vehicle programs and expanding the addressable market to mid-volume vehicle platforms where custom engineering was previously cost-prohibitive.

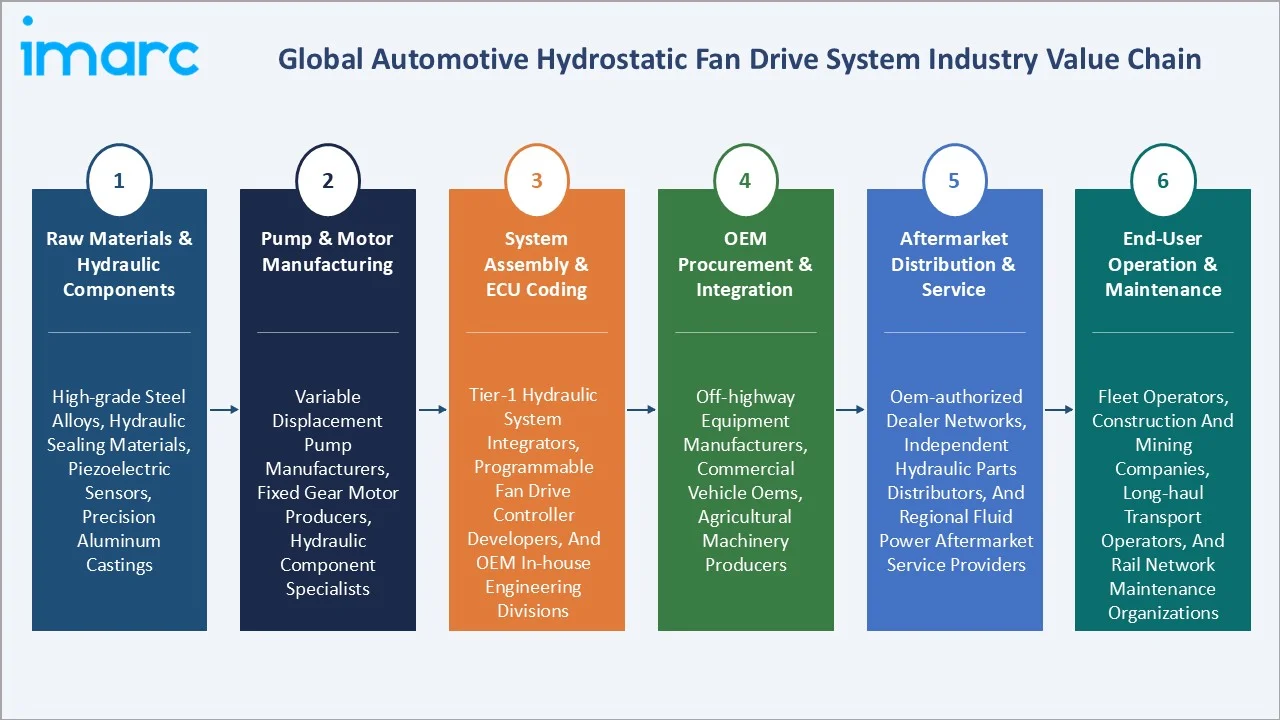

Industry Value Chain Analysis

The automotive hydrostatic fan drive system value chain extends from raw hydraulic component manufacturing through precision system assembly, OEM vehicle integration, and aftermarket service networks, with each stage demanding specialized engineering and quality management.

| Stage | Key Players / Examples |

|---|---|

| Raw Materials & Hydraulic Components | High-grade steel alloys, hydraulic sealing materials, piezoelectric sensors, precision aluminum castings |

| Pump & Motor Manufacturing | Variable displacement pump manufacturers, fixed gear motor producers, hydraulic component specialists |

| System Assembly & ECU Coding | Tier-1 hydraulic system integrators, programmable fan drive controller developers, and OEM in-house engineering divisions |

| OEM Procurement & Integration | Off-highway equipment manufacturers, commercial vehicle OEMs, agricultural machinery producers |

| Aftermarket Distribution & Service | OEM-authorized dealer networks, independent hydraulic parts distributors, and regional fluid power aftermarket service providers |

| End-User Operation & Maintenance | Fleet operators, construction and mining companies, long-haul transport operators, and rail network maintenance organizations |

Technology Landscape in the Automotive Hydrostatic Fan Drive System Industry

Variable Axial Piston Pump Technology

Variable axial piston pumps are the core hydraulic power source in hydrostatic fan drive systems. Operating at pressures of 200–400 bar with variable displacement from 0 to maximum delivery, they translate ECU control signals into precise hydraulic flow to the fan motor.

Fixed Gear Motor Technology

Fixed displacement gear motors convert the hydraulic flow from the piston pump into mechanical rotation for fan drive. Their simplicity, low cost, and reliability in contaminated environments make them the default motor type in most hydrostatic fan drive architectures.

Engine Control Unit (ECU) and Sensor Integration

The ECU is the intelligence layer of the hydrostatic fan drive system, processing inputs from coolant temperature sensors, engine load signals, and ambient temperature data to optimize fan speed in real time.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Vehicle Type | Off-Road Vehicles | 46.2% | 2025 |

| Component | Variable Axial Piston Pump | 34.8% | 2025 |

| Pump Type | 🔒 | 🔒 | 2025 |

| Region | Asia-Pacific | 42.7% | 2025 |

By Vehicle Type

Off-road vehicles lead with a 46.2% share in 2025. This segment encompasses construction equipment (excavators, wheel loaders, bulldozers), agricultural machinery (tractors, combine harvesters), and mining vehicles (haul trucks, loaders), all of which operate under highly variable thermal loads that demand the precise cooling control only hydrostatic fan drives can provide.

To access detailed market analysis, Request Sample

On-road vehicles represent 38.5%, led by heavy commercial trucks, long-haul buses, and specialized municipal vehicles. Train, metro, and trams account for 15.3%, representing a high-value niche driven by fleet modernization programs in Europe and Asia-Pacific, where rail network operators require hydrostatic fan drives for traction motor and brake resistor cooling in demanding duty cycles.

By Component

Variable axial piston pumps dominate with a 34.8% component share in 2025. As the primary hydraulic power source in any hydrostatic fan drive system, variable piston pumps are the highest-value component at USD 300–800 per unit at OEM pricing. Their ability to precisely modulate hydraulic output in response to ECU control signals is the fundamental enabler of the fuel savings and cooling precision that justify hydrostatic fan drive system adoption over conventional mechanical alternatives.

Fixed gear motors hold a 22.6% share, forming the output stage of the hydraulic circuit. Engine control units represent 17.1%, with increasing ECU value driven by IoT connectivity and multi-input control logic. Oil coolers account for 13.4%, while hydraulic valves and sensors collectively represent 12.1% of the component breakdown, both segments growing as system sophistication increases.

Regional Market Insights

Asia-Pacific leads global automotive hydrostatic fan drive demand with a 42.7% market share in 2025. The region's position reflects China's status as the world's largest construction equipment market, India's rapidly expanding commercial vehicle fleet under BS-VI emission norms, and Japan's established hydraulics supply industry that serves global OEM platforms.

Europe's 24.5% share is driven by the region's stringent Stage V off-highway and Euro VI on-road emission standards, which make hydrostatic fan drives a compliance-mandated component for major OEMs. North America at 18.1% is anchored by the heavy-duty trucking and mining equipment sectors.

| Region | Share (2025) | Key Growth Drivers |

|---|---|---|

| Asia-Pacific | 42.7% | Rapid expansion of construction and off-highway equipment fleets, growing adoption of emission-compliant commercial vehicle powertrains, a well-established hydraulics component manufacturing base |

| Europe | 24.5% | Stringent off-highway and on-road emission compliance requirements driving variable-speed cooling system adoption, large installed base of commercial and heavy-duty vehicles |

| North America | 18.1% | Sustained demand from heavy-duty trucking and mining equipment segments, tightening vehicular emission and fuel efficiency regulations |

| Latin America | 8.3% | Growing agricultural machinery and mining equipment fleets, increasing regulatory focus on vehicle emissions and fuel consumption, rising demand for thermal management solutions |

| Middle East & Africa | 6.4% | Expanding construction and mining activity driven by infrastructure investment programs, extreme ambient operating temperatures increasing demand for precision cooling systems |

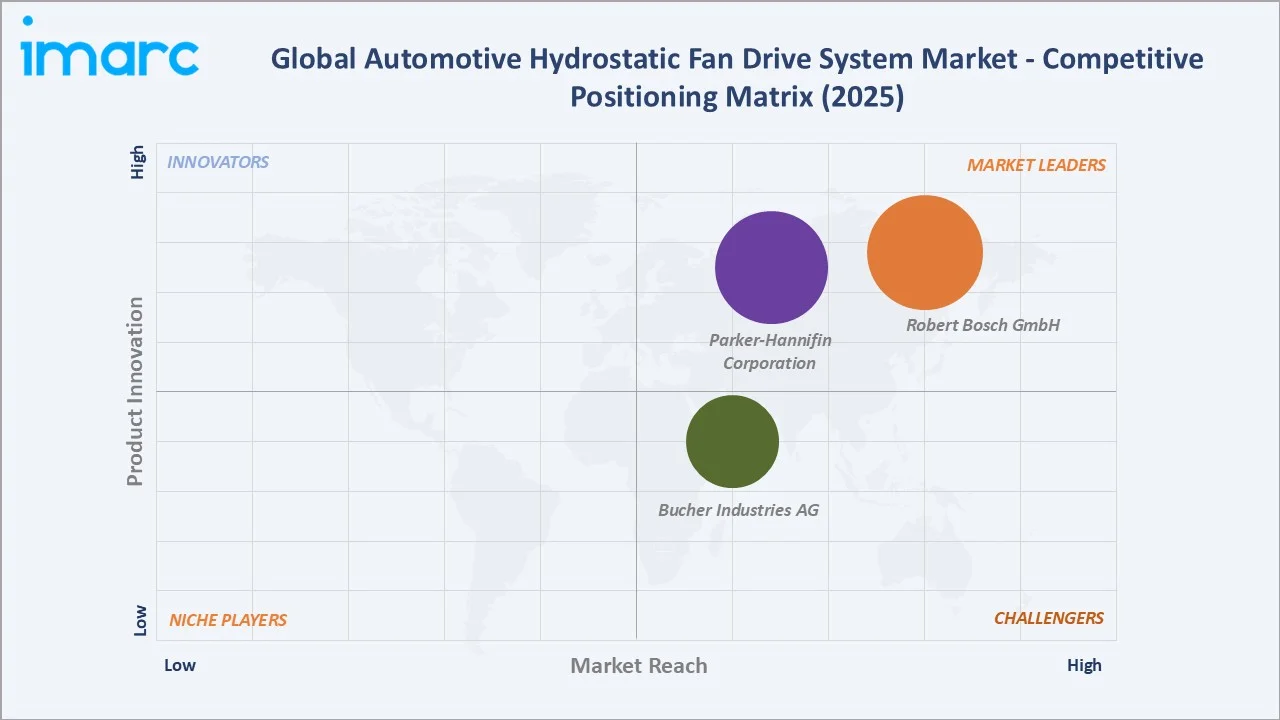

Competitive Landscape

The global automotive hydrostatic fan drive system market is moderately consolidated. Robert Bosch GmbH, Parker-Hannifin Corporation, and Bucher Industries AG, collectively hold an estimated 55–60% of global revenues in 2025.

| Company Name | Brand Name | Market Position | Core Strength |

|---|---|---|---|

| Robert Bosch GmbH | Bosch Rexroth | Market Leader | Broad variable displacement pump platform portfolio, advanced electro-hydraulic system integration capabilities |

| Parker-Hannifin Corporation | Parker | Market Leader | Comprehensive pump and motor product range, widest off-highway application engineering portfolio among global hydraulic system suppliers |

| Bucher Industries AG | Bucher | Challenger | Compact and modular hydrostatic fan drive system architecture, specialized manifold and valve block engineering expertise |

Competition centers on variable-pump efficiency, ECU control algorithm sophistication, system integration capabilities, and the breadth of application engineering support provided to OEM customers.

Key Company Profiles

Robert Bosch GmbH

Robert Bosch GmbH operates Bosch Rexroth AG, which is one of the global leaders in drive and control technologies, including hydraulic fan drive systems.

- Product Portfolio: A1VO and A10VO variable axial piston pumps; fixed displacement gear motors; HydraForce cartridge valve manifolds; Open Core Engineering ECU platforms; complete fan drive system assemblies for off-highway and commercial vehicle applications.

- Recent Developments: Bosch Rexroth AG recorded sales of EUR 6.45 billion in FY 2025, broadly stable year-on-year, while order intake rose 8.9% to EUR 6.6 billion. The company invested around EUR 560 million in R&D and facilities, strengthened AI-enabled automation and digital hydraulic services.

- Strategic Focus: Electro-hydraulic hybrid fan drive development, IoT-connected system diagnostics, Stage V and Euro 7 pre-compliance architecture, and OEM co-engineering programs with Caterpillar, Komatsu, and CNH Industrial.

Parker-Hannifin Corporation

Parker-Hannifin Corporation is one of the world's largest industrial and mobile hydraulics companies. The company supplies hydrostatic fan drive systems to off-highway, commercial vehicle, and rail OEMs globally through an extensive application engineering and distribution network.

- Product Portfolio: PVH variable piston pumps; F12 and TF series bent-axis fixed displacement motors; LifeSense IoT-enabled fan drive controllers; hydraulic system integration kits; complete fan drive turnkey packages for truck, bus, and off-highway platforms.

- Recent Developments: Parker-Hannifin Corporation reported sales for the quarter ended March 2026 of USD 5.49 billion, up 10.6%, driven by 6.5% organic growth. Growth was also supported by North American industrial demand across in-plant, off-highway, and energy markets, as well as strong Asian performance.

- Strategic Focus: IoT connectivity and predictive maintenance commercialization, North America and European HD truck OEM penetration, modular platform architecture development, and system-level integration services for hybrid commercial vehicle programs.

Market Concentration Analysis

The global automotive hydrostatic fan drive market is moderately concentrated. The top vendors, Robert Bosch GmbH, Parker-Hannifin Corporation, and Bucher Industries AG, collectively hold approximately 55–60% of global revenues in 2025. Below the top tier, a competitive mid-market includes 15–20 regional manufacturers and specialist suppliers serving niche vehicle types, geographic markets, and application-specific configurations.

Consolidation is accelerating. Bosch Rexroth's acquisition of HydraForce and Bucher Hydraulics's Hydman Oy deal signal that global tier-1 suppliers are using M&A to extend their product capability beyond piston pumps into cartridge valves, manifolds, and digital control ecosystems. This integrated systems strategy increasingly differentiates top-tier suppliers from component-only competitors.

Investment & Growth Opportunities

Fastest Growing Segments

Variable axial piston pumps (~4.80% CAGR), IoT-enabled fan drive ECUs, electro-hydraulic hybrid systems, and rail application fan drives represent the highest-growth investment vectors through 2034. Together, these sub-segments address a combined incremental addressable market of approximately USD 120 Million by 2034 within the global hydrostatic fan drive ecosystem.

Emerging Market Expansion

India, Brazil, Indonesia, and Saudi Arabia collectively represent a USD 60+ Million incremental hydrostatic fan drive opportunity by 2034, as emission standard upgrades and expanding off-highway equipment fleets create first-time demand for sophisticated variable-speed cooling systems. India's construction equipment market alone is projected to grow at 6.5% CAGR through 2034, directly expanding the addressable market for off-road hydrostatic fan drives.

Venture and Institutional Investment Trends

- Digital connectivity investment in fan drive ECUs is generating SaaS-adjacent recurring revenue opportunities through fleet analytics subscriptions and predictive maintenance service contracts valued at USD 50–200 per vehicle annually.

- M&A activity signals private equity and strategic interest in acquiring specialized hydraulic component capabilities to build integrated fan drive system portfolios.

Future Market Outlook (2026-2034)

The automotive hydrostatic fan drive system market is positioned for consistent, broad-based growth through 2034. From USD 441.0 Million in 2025, the market will reach USD 640.4 Million by 2034, representing total incremental value creation of USD 199.4 Million at a 4.10% CAGR. Off-road and commercial vehicle demand will remain the primary growth driver, supported by the sustained global construction and mining investment cycle and tightening emission mandates.

The technology composition of the market will shift toward higher-value, electro-hydraulic hybrid and IoT-connected systems by 2034 as OEMs integrate digital controls and mild-hybrid powertrains across commercial and off-highway platforms. Rail applications will grow faster than the overall market as fleet modernization programs in Asia-Pacific and Europe create a premium-specification demand cohort for hydrostatic cooling systems.

Research Methodology

Primary Research

Primary research comprised structured interviews with over 85 industry participants in 2024–2025, including hydraulic system engineers, OEM procurement managers, fleet operators, emission compliance consultants, and institutional investors across Asia-Pacific, Europe, and North America. Expert input validated market sizing, technology adoption timelines, and regional deployment trends.

Secondary Research

Secondary research encompassed supplier annual reports, SAE and ISO hydraulics technical standards, regulatory documentation, OICA global vehicle production statistics, off-highway equipment association reports, and trade publications including Hydraulics & Pneumatics and Construction Equipment.

Forecasting Models

Market size estimations used top-down and bottom-up forecasting, incorporating global off-highway and commercial vehicle production volumes, hydrostatic fan drive penetration rates by vehicle type, average system selling price trajectories, and aftermarket replacement cycle data. A base-case CAGR of 4.10% reflects consensus validated against OEM procurement commitments and emission standard implementation schedules.

Automotive Hydrostatic Fan Drive System Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | Variable Axial Piston Pump, Fixed Gear Motor, Engine Control Unit, Oil Cooler, Hydraulic Values and Sensors |

| Pump Types Covered | Fixed Displacement Pump, Variable Displacement Type |

| Vehicle Types Covered |

|

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Robert Bosch GmbH, Parker-Hannifin Corporation, Bucher Industries AG, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive hydrostatic fan drive system market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global automotive hydrostatic fan drive system market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive hydrostatic fan drive system industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive Hydrostatic Fan Drive System Market Report

The market reached USD 441.0 Million in 2025 and is projected to reach USD 640.4 Million by 2034, growing at a CAGR of 4.10%.

Asia-Pacific leads with a 42.7% share in 2025, driven by China's construction equipment output, India's BS-VI compliance, and Japan's hydraulics manufacturing.

Off-road vehicles lead with a 46.2% share in 2025, as construction, agricultural, and mining equipment require demand-responsive hydrostatic cooling.

Variable axial piston pumps hold a 34.8% component share in 2025, as the highest-value, performance-critical element in any hydrostatic fan drive system.

Robert Bosch GmbH, Parker-Hannifin Corporation, and Bucher Industries AG, are some of the leading players.

The market is expected to grow at a CAGR of 4.10%, reaching USD 640.4 Million by 2034 from USD 441.0 Million in 2025.

Emission norms, off-road fleet expansion, hybrid vehicle adoption, and mining/construction equipment demand are the primary drivers.

High initial system cost, electrification disruption, and hydraulic maintenance complexity are the primary market challenges.

Train, metro and trams represent 15.3% of the market in 2025, driven by fleet modernization in Europe and Asia-Pacific.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)