Automotive Lightweight Materials Market Size, Share, Trends and Forecast by Material Type, Propulsion Type, Component, Application, Vehicle Type, and Region, 2026-2034

Automotive Lightweight Materials Market Size and Share:

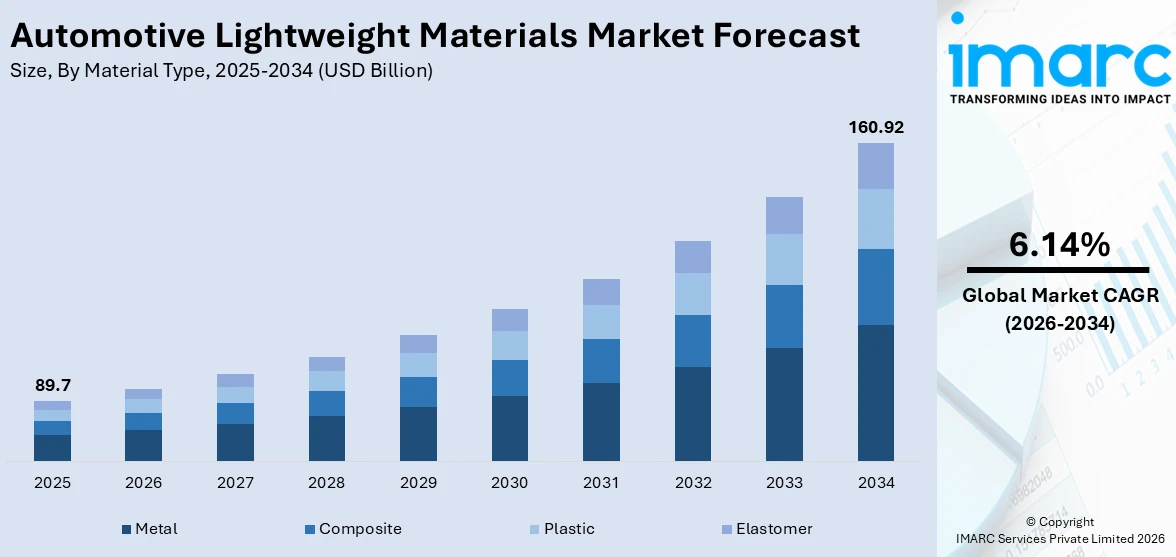

The global automotive lightweight materials market size was valued at USD 89.7 Billion in 2025. Looking forward, IMARC Group estimates the market to reach USD 160.92 Billion by 2034, exhibiting a CAGR of 6.14% from 2026-2034. Europe currently dominates the market, holding a market share of 31.5% in 2025. The region benefits from stringent environmental regulations and well-established automotive manufacturing capabilities, with leading automakers prioritizing lightweight materials to meet rigorous emission targets and enhance vehicle performance, alongside a strong emphasis on sustainable production practices and advanced material innovation, all contributing to the automotive lightweight materials market share.

Escalating fuel-efficient vehicle requirements globally is one of the key drivers for the growth of the market. Governments worldwide have introduced strict regulations regarding vehicle emissions, prompting automakers to use materials such as high-strength steel, aluminum alloys, and carbon fiber composites for reducing vehicle weight and ensuring fuel efficiency. In addition, the growth of the electric vehicle market has also contributed significantly towards the growth of the market, driven by the requirements for lightweight materials that can be used for offsetting the weight of the batteries and enhancing the driving range of the vehicle. Furthermore, the growing focus on sustainable living and the adoption of the circular economy have also contributed towards the growth of the market, driven by the use of aluminum recycling techniques for the manufacture of lightweight materials for the automotive sector. In addition, the growing requirements for high-performance vehicles, driven by the need for better handling, acceleration, and braking capabilities, have also contributed towards the growth of the market, driven by the use of lightweight materials for vehicle structures, powertrains, and exteriors, thereby widening the scope of the market for different types of vehicles globally.

The United States has emerged as a key market in the automotive lightweight materials market due to a number of factors. The country has a strong automotive manufacturing sector with key original equipment manufacturers continuously investing in R&D to adopt advanced lightweight materials. Fuel efficiency and emission control regulations set by government agencies are forcing domestic automobile manufacturers to look for innovative solutions to reduce vehicle weight. According to the Aluminum Association, aluminum content in North American light vehicles is expected to reach 514 pounds per vehicle by 2026, which is 12% higher than 2020 levels. Moreover, the rising adoption of electric vehicles in the United States is driving demand for materials to enhance battery efficiency. In addition to this, environmental sustainability is also playing a key role in driving demand for automotive materials. With increasing environmental awareness among consumers, manufacturers are forced to adopt recycled and environmentally friendly materials.

To get more information on this market Request Sample

Automotive Lightweight Materials Market Trends:

Accelerating Adoption of Advanced Composites

The increasing rate of utilization of advanced composite materials such as carbon fiber reinforced polymer and glass fiber reinforced polymer is turning out to be one of the major trends in the automotive industry. These materials have better strength-to-weight ratios, allowing automobile manufacturers to achieve weight reduction in vehicles without compromising the safety features. The shift towards multi-material vehicle platforms using metals along with composite materials in selective areas is also gaining traction in the industry. This is because manufacturers are looking to achieve cost and weight reduction simultaneously. Advances in manufacturing processes such as automated fiber placement and resin transfer molding are also helping to improve the rate of production while reducing cycle times. For example, in March 2025, McLaren Automotive announced its new automated rapid tape manufacturing process, which uses aerospace industry-automated fiber placement technology to produce automotive materials. This is a combination of over 40 years of McLaren’s expertise in carbon fiber.

Growing Electric Vehicle Lightweight Integration

The growing market for electric vehicles is creating unprecedented market demands for lightweight materials that can help minimize the significant weight of battery packs while optimizing energy efficiency. The battery systems used in modern electric vehicles have a curb weight of about 300 to 500 kilograms, making it necessary for manufacturers to minimize the weight of other vehicle systems to maintain the desired performance and range requirements. Lightweight materials such as aluminum, magnesium, and engineering plastics are being used in strategic applications in battery enclosures, chassis frames, and body structures to optimize weight distribution. The automotive lightweight materials market outlook is strengthened by the growing number of electric vehicle platforms incorporating aluminum-intensive designs. For instance, Novelis filed for a USD 2.5 billion initial public offering to fund the expansion of its lightweight aluminum production capacity across North America and Asia. Site activities are currently in progress, and the company anticipates starting commissioning by mid-2025. This trend is expected to intensify as electric vehicle production volumes continue to rise globally.

Rising Emphasis on Sustainable Material Solutions

The increasing focus on environmental sustainability and circular economy principles is shaping material selection strategies across the automotive industry. Manufacturers are progressively adopting recycled aluminum, bio-based polymers, and low-carbon production methods to reduce the environmental footprint of vehicle manufacturing. The automotive aluminum recycling rate currently exceeds 95%, making it one of the most sustainable material choices for vehicle components. Additionally, partnerships between material suppliers and automakers are facilitating the development of closed-loop recycling systems that minimize waste and reduce dependence on primary raw materials. The automotive lightweight materials market forecast reflects a strong trajectory driven by these sustainability initiatives. For instance, in April 2025, Covestro launched Desmopan FLY, a sustainable thermoplastic polyurethane series optimized for lightweight applications, supporting recyclable and circular design principles. These developments are encouraging the automotive sector to embrace environmentally responsible material solutions while maintaining high performance standards.

Automotive Lightweight Materials Industry Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the global automotive lightweight materials market, along with forecast at the global, regional levels from 2026-2034. The market has been categorized based on material type, propulsion type, component, application, and vehicle type.

Analysis by Material Type:

- Metal

- High Strength Steel (HSS)

- Aluminum

- Magnesium & Titanium

- Composite

- Carbon Fiber Reinforced Polymer (CFRP)

- Glass Fiber Reinforced Polymer (GFRP)

- Natural Fiber Reinforced Polymer (NFRP)

- Other Composites

- Plastic

- Elastomer

Metal holds 47.3% of the market share. Metals, including advanced high-strength steels, aluminum alloys, and magnesium compounds, remain the predominant material category in automotive lightweight applications owing to their proven durability, cost-effectiveness, and established manufacturing infrastructure. Advanced high-strength steels provide exceptional crash protection while enabling thinner, lighter structural components that reduce overall vehicle weight. Aluminum is extensively employed in body panels, engine blocks, wheels, and chassis applications due to its favorable strength-to-weight ratio and excellent corrosion resistance. Magnesium alloys are gaining adoption for their ultra-lightweight properties in steering columns, seat frames, and instrument panels. Apart from this, the recyclability of metals further supports their dominant position, aligning with the growing emphasis on sustainable and circular manufacturing practices across the automotive industry.

Analysis by Propulsion Type:

- IC Engine Powered

- Electric Powered

- Others

IC engine powered leads the market with a share of 55.9%. Internal combustion engine vehicles continue to represent the largest application base for lightweight materials as manufacturers seek to meet increasingly stringent fuel economy and emission standards through vehicle weight optimization. Automakers are investing in technologies such as turbocharging, direct fuel injection, and variable valve timing, which require lightweight engine components to maximize efficiency gains. The integration of aluminum and high-strength steel in engine blocks, cylinder heads, and transmission housings is reducing powertrain weight while maintaining structural performance. For instance, in January 2025, Gestamp introduced its GES-GIGASTAMPING product family, which combines multiple body parts into single lightweight units, reducing production time and material usage while enhancing safety. The rising demand for hybrid vehicles, which combine internal combustion engines with electric powertrains, is further driving the adoption of lightweight materials to balance performance, efficiency, and regulatory compliance.

Analysis by Component:

- Frame

- Wheel

- Bumper

- Door and Seat

- Instrument Panel

- Others

Frame holds 34.2% share of the automotive lightweight materials market as manufacturers prioritize robust yet lighter structural designs that improve both safety and fuel economy. The frame represents the largest segment in the automotive lightweight materials market because it forms the primary structural backbone of a vehicle. It supports the engine, transmission, suspension, and body components while ensuring overall stability and safety. As automakers focus on reducing vehicle weight to improve fuel efficiency and lower emissions, the use of lightweight materials in vehicle frames has become increasingly important. Traditionally, vehicle frames were made from conventional steel due to its strength and durability. However, manufacturers are now adopting advanced lightweight materials such as high-strength steel (HSS), aluminum alloys, magnesium, and carbon fiber composites. These materials provide the necessary structural integrity while significantly reducing weight compared to traditional steel structures.

Analysis by Application:

Access the comprehensive market breakdown Request Sample

- Structural

- Interior

- Exterior

- Powertrain

- Others

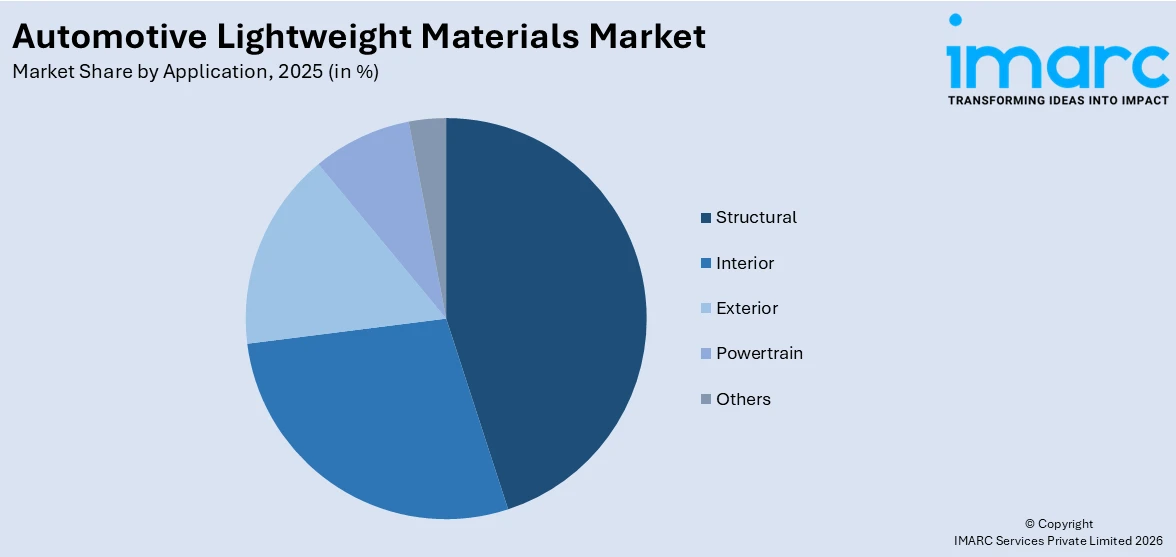

Structural holds 41.2% share in the market driven by the emphasis on vehicle safety and fuel efficiency improvements. The structural segment represents the largest application area in the automotive lightweight materials market. Structural components form the core framework of a vehicle and are responsible for maintaining its strength, rigidity, and crashworthiness. These parts include the chassis, body structure, pillars, cross members, and other load-bearing elements that support the entire vehicle. Because these components contribute significantly to the overall vehicle weight, they offer the greatest potential for weight reduction through the use of lightweight materials. Automakers are increasingly adopting advanced materials such as high-strength steel, aluminum alloys, magnesium, and carbon fiber composites for structural applications. High-strength steel remains widely used due to its excellent durability and relatively lower cost compared to other lightweight materials. Aluminum is also gaining popularity in structural parts because it can significantly reduce weight while maintaining structural performance. In premium and performance vehicles, carbon fiber composites are used to achieve even greater weight savings and improved stiffness.

Analysis by Vehicle Type:

- Passenger Vehicle

- Light Commercial Vehicle (LCV)

- Heavy Commercial Vehicle (HCV)

Passenger vehicle dominates the market, with a share of 59.8%. Passenger vehicles represent the largest consumer segment for automotive lightweight materials, driven by escalating demand for fuel-efficient, environmentally responsible, and technologically advanced personal transportation. Rising fuel costs and stringent emission regulations are compelling automakers to deploy advanced lightweight materials across body structures, closures, and interior systems to achieve measurable weight reductions. The growing popularity of electric passenger vehicles further necessitates lightweight construction to maximize battery range and overall energy efficiency. For instance, in February 2025, Chinese new energy vehicle maker Li Auto and automotive supplier Ianlon Technology signed a strategic cooperation agreement to establish a joint innovation lab focused on ultra-high-strength steel, lightweight alloys, and advanced composite materials for automotive applications. Consumer preferences for vehicles offering superior handling, enhanced safety features, and premium interior quality continue to encourage the integration of advanced lightweight materials across all passenger vehicle categories.

Regional Analysis:

To get more information on the regional analysis of this market Request Sample

- North America

- Asia Pacific

- Europe

- Middle East and Africa

- Latin America

Europe, accounting for 31.5% of the share, enjoys the leading position in the market. The Europe automotive lightweight materials market is expanding due to stricter emission standards and rising demand for fuel efficiency. Manufacturers are shifting to aluminum, magnesium, high-strength steel, and polymer composites to reduce vehicle weight without sacrificing safety. Aluminum usage is growing in body panels, engine components, and chassis parts, driven by its strength-to-weight ratio and recyclability. Composites, especially carbon fiber reinforced plastics, are gaining traction in premium and electric vehicles where range and performance matter most. High-strength steel remains widely used because it balances cost and performance, particularly in safety-critical structures. Electrification is boosting demand for lightweight materials as reducing mass directly improves battery range. Suppliers are investing in advanced material processing and joining techniques to integrate dissimilar materials efficiently. Regulations targeting lower CO₂ emissions continue to influence material choices. Collaboration between OEMs and material producers is increasing to optimize designs for manufacturability and cost control. Cost pressures and supply chain reliability are key challenges for broader adoption.

Key Regional Takeaways:

North America Automotive Lightweight Materials Market Analysis

North America represents a significant market for automotive lightweight materials, supported by a well-established automotive manufacturing ecosystem and growing emphasis on vehicle efficiency standards. The region benefits from the presence of major original equipment manufacturers and tier-one suppliers who continuously invest in research and development to advance lightweight material technologies. The expanding adoption of electric vehicles across the United States and Canada is creating substantial demand for lightweight aluminum, composites, and engineering plastics that enhance battery efficiency and driving range. The growing consumer preference for pickup trucks and sport utility vehicles, which represent a significant share of North American vehicle sales, is encouraging manufacturers to employ lightweight materials to balance performance expectations with fuel economy targets. For instance, in March 2025, Hyundai Steel Company announced a USD 5.8 billion investment in a manufacturing facility in Donaldsonville, Louisiana, to produce ultra-low carbon steel and automotive steel plates for North American automakers. The region's strong focus on sustainability and the development of closed-loop aluminum recycling infrastructure further supports the expanding adoption of lightweight materials across automotive applications, contributing to automotive lightweight materials market trends.

United States Automotive Lightweight Materials Market Analysis

The United States is a key contributor to the North American automotive lightweight materials market, driven by robust domestic vehicle production and evolving fuel economy regulations. American automakers are actively integrating aluminum, advanced high-strength steels, and composite materials across vehicle platforms to achieve weight reduction targets while maintaining safety and performance standards. The expanding electric vehicle market in the United States is generating significant demand for lightweight components that optimize battery efficiency and extend range capabilities. According to the National Highway Traffic Safety Administration, the Corporate Average Fuel Economy standards mandate an industry-wide fleet average of approximately 49 miles per gallon for passenger cars and light trucks in model year 2026, reinforcing the need for lightweight vehicle designs. The growing investment in domestic manufacturing facilities for lightweight materials is strengthening the supply chain and reducing dependence on imports. The consumer demand for advanced safety features and premium vehicle quality further encourages the adoption of sophisticated lightweight material solutions across structural, interior, and exterior applications.

Europe Automotive Lightweight Materials Market Analysis

Europe maintains a commanding position in the global automotive lightweight materials market, supported by the region's stringent environmental regulations and advanced automotive engineering capabilities. The European Union's comprehensive emission reduction framework, including the mandate for a 100% reduction in CO2 emissions from new cars by 2035, drives continuous innovation in lightweight material technologies. Germany, as the largest vehicle manufacturer in Europe, leads the adoption of aluminum, carbon fiber composites, and advanced high-strength steels across premium and mass-market vehicle segments. The region's strong emphasis on electric vehicle adoption, with battery-electric vehicle registrations reaching 1.8 million units in 2025 representing a 30% increase over the previous year, creates expanding demand for lightweight solutions that improve range and performance. Additionally, the European automotive supply chain benefits from significant investment in gigafactory projects and sustainable material production facilities, reinforcing the region's leadership in lightweight automotive manufacturing.

Asia-Pacific Automotive Lightweight Materials Market Analysis

Asia-Pacific is emerging as a rapidly growing market for automotive lightweight materials, driven by expanding vehicle production capacities and increasing regulatory pressure for emission reductions across the region. Countries including China, Japan, South Korea, and India are at the forefront of integrating lightweight materials into diverse vehicle platforms to meet domestic fuel efficiency standards and environmental targets. The region's leadership in electric vehicle manufacturing, with China accounting for a substantial share of global production, generates significant demand for lightweight aluminum and composite components. In 2025, new car sales in the European Union rose by 1.8% to 10.63 million units, driven by ongoing demand for battery electric vehicles (BEVs) and hybrid electric vehicles (HEVs), accelerating the adoption of lightweight materials. Japan's advanced material science capabilities and established carbon fiber production infrastructure further strengthen the regional supply chain.

Latin America Automotive Lightweight Materials Market Analysis

Latin America represents a developing market for automotive lightweight materials, with growth driven by expanding domestic vehicle production and increasing awareness of environmental sustainability. Countries such as Brazil, Mexico, and Argentina are witnessing gradual adoption of lightweight materials as local and international automakers establish manufacturing operations that incorporate modern material technologies. The region's evolving regulatory framework for vehicle emission standards is encouraging manufacturers to explore lightweight solutions for improved fuel efficiency. Government incentives aimed at promoting electric and hybrid vehicle adoption in select markets are creating emerging demand for advanced lightweight components across the automotive supply chain.

Middle East and Africa Automotive Lightweight Materials Market Analysis

The Middle East and Africa automotive lightweight materials market is in its early growth phase, driven by increasing vehicle ownership rates and expanding automotive manufacturing activities across the region. Infrastructure development projects and rising urbanization are stimulating demand for commercial and passenger vehicles that incorporate lightweight materials for improved operational efficiency. The growing emphasis on diversifying economies beyond petroleum dependence is encouraging governments to support automotive industry development, including the adoption of advanced manufacturing technologies and lightweight material solutions. The expanding presence of international automakers in the region is facilitating technology transfer and material innovation.

Competitive Landscape:

The competitive landscape of the automotive lightweight materials market is characterized by continuous innovation, strategic partnerships, and substantial investments in research and development. Major material suppliers and manufacturers are actively expanding their production capacities and product portfolios to address the escalating demand for lightweight solutions across the automotive sector. Companies are focusing on developing next-generation materials with enhanced strength-to-weight ratios, improved recyclability, and lower carbon footprints to align with evolving regulatory requirements and sustainability objectives. Strategic collaborations between material suppliers and automotive original equipment manufacturers are accelerating the integration of advanced lightweight materials into vehicle platforms. Additionally, investments in additive manufacturing and advanced forming technologies are enabling more efficient production processes that reduce material waste and lower overall manufacturing costs.

The report provides a comprehensive analysis of the competitive landscape in the automotive lightweight materials market with detailed profiles of all major companies, including:

- BASF SE

- Magna International

- Toray Industries

- Covestro AG

- ArcelorMittal

- thyssenkrupp AG

- Alcoa Corporation

- Bayer AG

- Saudi Arabia Basic Industries Corporation (SABIC)

- PPG Industries

- LyondellBasell

- Novelis

- Owens Corning Corporation

- Grupo Antolin

Automotive Lightweight Materials Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Material Types Covered |

|

| Propulsion Types Covered | IC Engine Powered, Electric Powered, Others |

| Components Covered | Frame, Wheel, Bumper, Door and Seat, Instrument Panel, Others |

| Applications Covered | Structural, Interior, Exterior, Powertrain, Others |

| Vehicle Types Covered | Passenger Vehicle, Light Commercial Vehicle (LCV), Heavy Commercial Vehicle (HCV) |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Companies Covered | BASF SE, Magna International, Toray Industries, Covestro AG, ArcelorMittal, thyssenkrupp AG, Alcoa Corporation, Bayer AG, Saudi Arabia Basic Industries Corporation (SABIC), PPG Industries, LyondellBasell, Novelis, Owens Corning Corporation, Grupo Antolin, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive lightweight materials market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global automotive lightweight materials market.

- The study maps the leading, as well as the fastest-growing, regional markets.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive lightweight materials industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive Lightweight Materials Market Report

The automotive lightweight materials market was valued at USD 89.7 Billion in 2025.

The automotive lightweight materials market is projected to exhibit a CAGR of 6.14% during 2026-2034, reaching a value of USD 160.92 Billion by 2034.

The automotive lightweight materials market is primarily driven by stringent government emission regulations, increasing demand for fuel-efficient vehicles, rapid expansion of the electric vehicle segment, advancements in material science and manufacturing technologies, growing consumer preference for high-performance vehicles, and rising emphasis on sustainability and circular economy practices across the global automotive industry.

Europe currently dominates the automotive lightweight materials market, accounting for a share of 31.5%. The region's leadership is supported by rigorous CO2 emission standards, a strong automotive manufacturing base, advanced material innovation capabilities, and expanding electric vehicle adoption rates.

Some of the major players in the automotive lightweight materials market include BASF SE, Magna International, Toray Industries, Covestro AG, ArcelorMittal, thyssenkrupp AG, Alcoa Corporation, Bayer AG, Saudi Arabia Basic Industries Corporation (SABIC), PPG Industries, LyondellBasell, Novelis, Owens Corning Corporation, Grupo Antolin, etc.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)