Automotive Robotics Market Size, Share, Trends and Forecast by Product Type, Component Type, Application, End User, and Region, 2026-2034

Global Automotive Robotics Market Size, Share, Trends & Forecast (2026-2034)

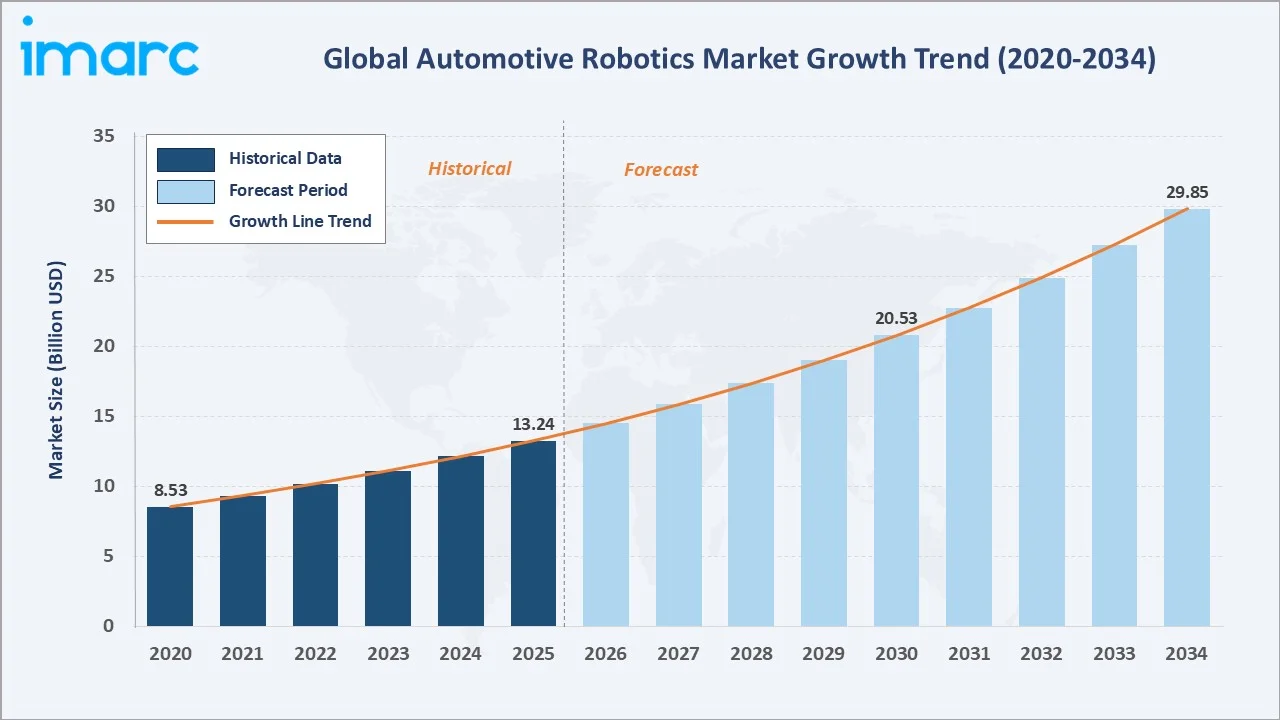

The global automotive robotics market size was valued at USD 13.24 Billion in 2025 and is projected to reach USD 29.85 Billion by 2034, exhibiting a CAGR of 9.17% during the forecast period 2026-2034. Rising demand for automation in vehicle manufacturing, rapid EV adoption requiring specialized assembly processes, and Industry 4.0 integration are key growth levers for the automotive robotics market growth.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 13.24 Billion |

|

Forecast Market Size (2034) |

USD 29.85 Billion |

|

CAGR (2026-2034) |

9.17% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

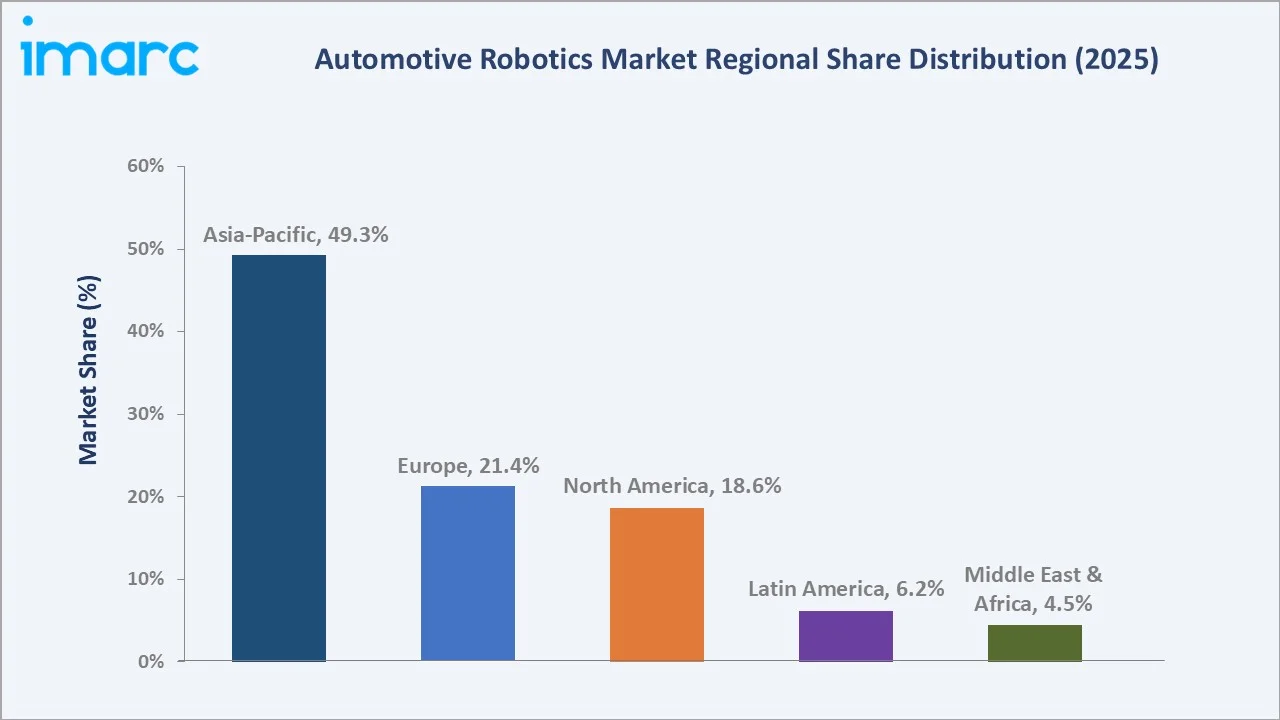

Largest Region |

Asia-Pacific (49.3% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (~10.4% CAGR) |

|

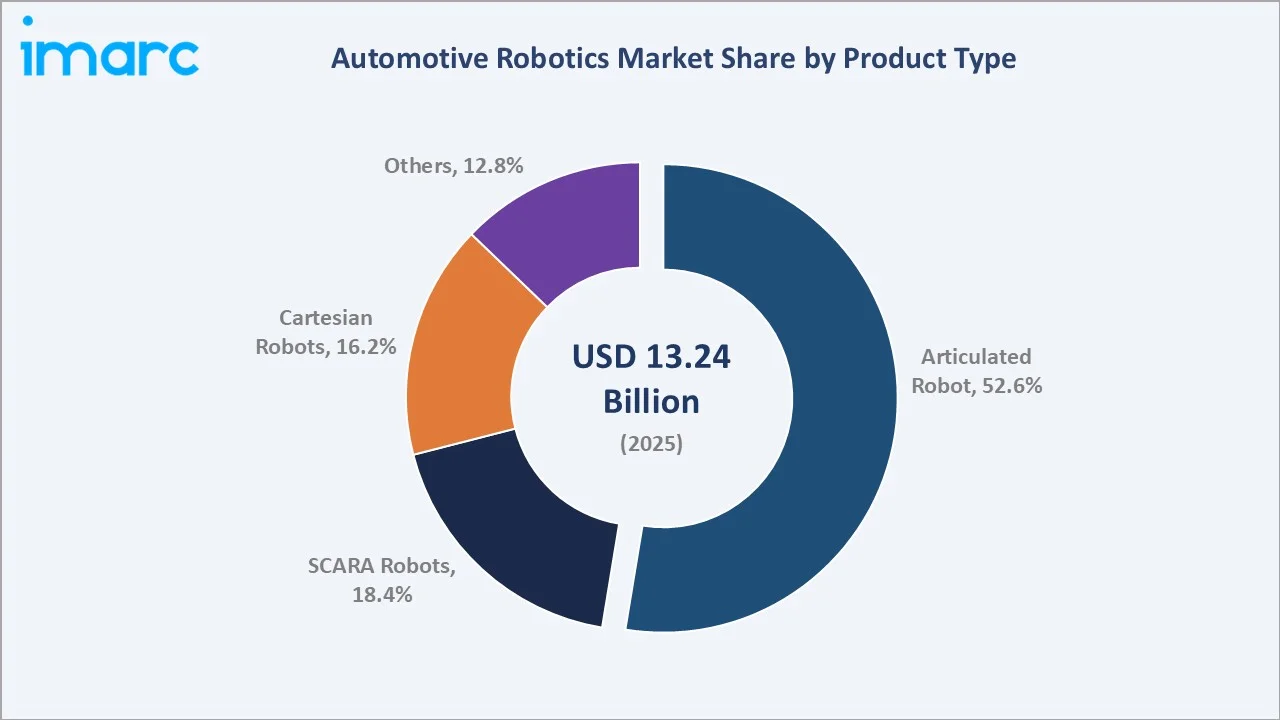

Leading Product Type |

Articulated Robot (52.6%, 2025) |

|

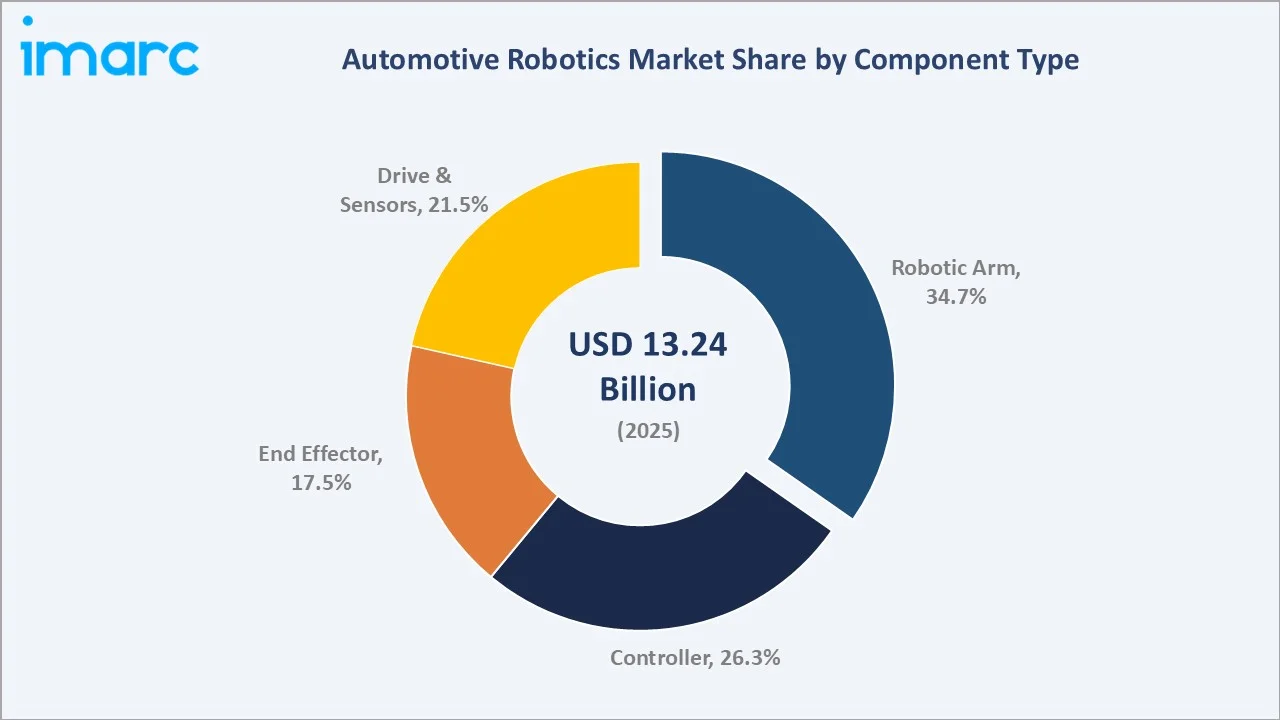

Leading Component Type |

Robotic Arm (34.7%, 2025) |

The global automotive robotics market growth trajectory from 2020 through 2034 reflects the compounding momentum of electrification, automation mandates, and Industry 4.0 adoption—contrasting a solid historical expansion phase against an accelerated forecast curve.

To get more information on this market, Request Sample

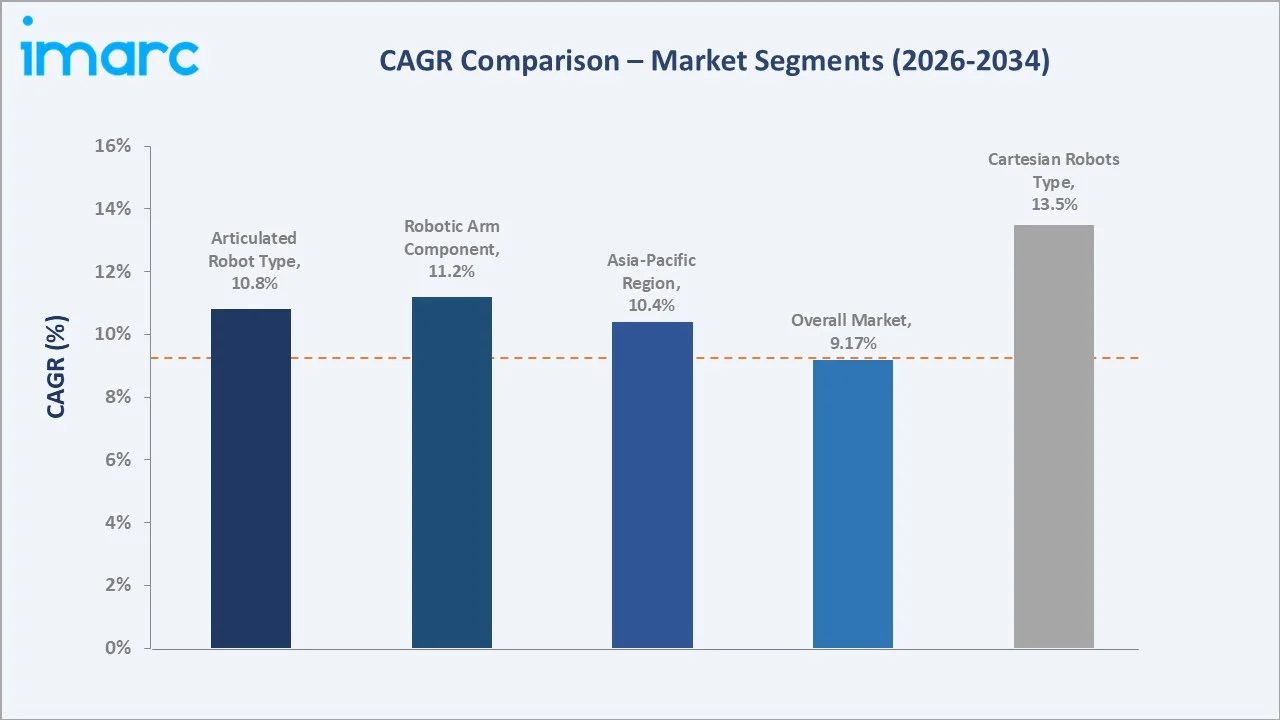

Segment-level CAGR comparisons highlight articulated robots, EV manufacturing applications, and robotic arm components as the fastest-growing sub-categories within the global automotive robotics market forecast through 2034.

Executive Summary

The global automotive robotics market is undergoing a profound structural transformation. Valued at USD 13.24 Billion in 2025, the market is projected to expand at a CAGR of 9.17%, reaching USD 29.85 Billion by 2034. This growth is driven by the accelerating shift to electric vehicles (EVs), increased manufacturing complexity, and the need for consistent, high-precision production. Industry 4.0 integration—encompassing AI, machine vision, and IoT connectivity—has become a central pillar of modern automotive manufacturing strategy.

Articulated robots dominate with a 52.6% product type share in 2025, prized for their multi-axis flexibility across welding, painting, and assembly tasks. SCARA and Cartesian robots serve complementary roles in precision component handling and linear operations. The robotic arm component leads at 34.7% share, underscoring the mechanical core of every automation cell. From controllers to end effectors, component innovation is accelerating in tandem with AI-driven programming platforms.

Asia-Pacific commands 49.3% of global revenue in 2025, anchored by China's position as the world's largest automotive manufacturing base and Japan's historic leadership in industrial robotics. Europe holds 21.4%, supported by Volkswagen, BMW, and Mercedes-Benz investments. The automotive robotics market outlook remains highly positive as EV production scales globally, collaborative robots enter mainstream deployment, and software-defined automation reshapes factory architectures across all major regions through 2034.

Key Market Insights

|

Insight |

Data |

|

Largest Product Type |

Articulated Robot – 52.6% share (2025) |

|

2nd Largest Product Type |

SCARA Robots – 18.4% share (2025) |

|

Largest Component Type |

Robotic Arm – 34.7% share (2025) |

|

Fastest Growing Component Type |

Drive and Sensors – highest AI integration rate |

|

Leading Region |

Asia-Pacific – 49.3% revenue share (2025) |

|

Top Companies |

ABB, FANUC Corporation, YASKAWA ELECTRIC CORPORATION., DENSO CORPORATION, Kawasaki Heavy Industries, Ltd., Omron Corporation, NACHI-FUJIKOSHI CORP., Seiko Epson Corporation, Yamaha Motor Co., Ltd |

|

Market Opportunity |

EV gigafactory expansion: 80+ planned globally, requiring high-throughput robotic cells |

Key Analytical Observations Supporting the Above Data:

- Articulated robots' 52.6% dominance in 2025 reflects their unmatched flexibility in performing welding, painting, material handling, and assembly across diverse vehicle platforms—critical as OEMs navigate high-mix, low-volume production for EVs and ICE models simultaneously.

- SCARA robots' 18.4% share is driven by their precision in pick-and-place operations, electronic component assembly for EV battery management systems, and small-part handling—use cases expanding rapidly as vehicle electronics content grows.

- Robotic arm's 34.7% component lead underscores its role as the mechanical backbone of every robot cell. The total number of industrial robots in operational use worldwide was 4,664,000 units in 2024 – an increase of 9% compared to the previous year.

- Asia-Pacific's 49.3% global dominance is anchored by China is targeting 35 million vehicle sales by 2025 and Japan's world-class robotics manufacturing base home to FANUC Corporation, Yaskawa ELECTRIC CORPORATION, and DENSO CORPORATION.

- EV battery assembly represents a high-growth application niche, with ABB estimating that 80 planned gigafactories globally will still leave supply short of demand, necessitating high-throughput robotic production to meet EV targets.

Global Automotive Robotics Market Overview

Automotive robotics encompasses programmable mechanical systems—including articulated arms, SCARA units, Cartesian platforms, and collaborative robots—deployed across vehicle design, manufacturing, quality inspection, and logistics. The ecosystem spans raw material suppliers, component manufacturers, OEM integrators, software developers, and end users ranging from vehicle OEMs to Tier-1 suppliers. Macroeconomic forces including EV mandates, labor cost inflation, and productivity imperatives are reshaping capital allocation across global automotive plants. The automotive robotics market trends now reflect a convergence of mechanical precision, AI cognition, and real-time connectivity that is redefining competitive manufacturing benchmarks through 2034.

Market Dynamics

To evaluate market opportunities, Request Sample

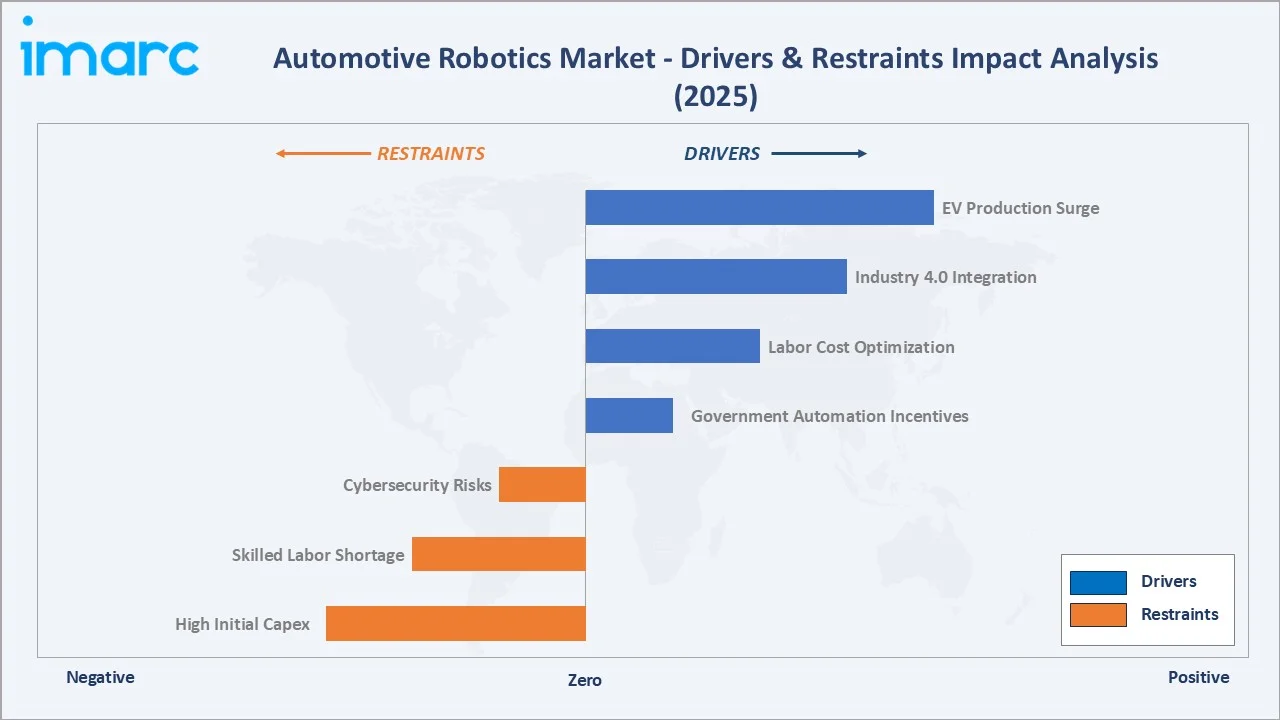

Market Drivers

- Rising EV Production and Specialized Assembly Needs: Global electric vehicle sales exceeded 20.7 million units in 2025, requiring precision robotics for battery pack integration, e-powertrain assembly, and lightweight material handling. Governments across the U.S., EU, and China have mandated EV fleet conversions, structurally driving demand for advanced robotic solutions tailored to EV architectures.

- Industry 4.0 and IIoT Integration: The convergence of robotics with IoT sensors, AI-based vision systems, and cloud analytics is enabling predictive maintenance, zero-downtime production, and real-time quality control. NVIDIA's release of the Cosmos platform in January 2025 exemplifies this advancement, enhancing capabilities for autonomous robotics and data-driven factory optimization.

- Labor Cost Optimization and Skilled Worker Shortage: Automotive manufacturers face rising labor costs and widening skill gaps. Robots perform welding, painting, and assembly at continuous operational cadence, reducing cycle times and human error margins. International Federation of Robotics logged a rise in operational industrial robots, confirming accelerating adoption.

- Government Automation Incentive Programs: National programs across South Korea, Germany, Japan, and the United States offer tax incentives, subsidies, and low-cost financing for industrial automation investments, lowering the capital barrier to robotics adoption for mid-tier suppliers.

Market Restraints

- High Initial Capital Investment: Robotic systems require substantial upfront expenditure covering hardware (robotic arms, sensors, controllers), software licensing, integration services, and workforce training—creating barriers for small and medium-sized Tier-2/Tier-3 suppliers in emerging markets.

- Cybersecurity and Data Integrity Risks: As automotive factories become more connected through Industry 4.0 platforms, the attack surface for cyber threats expands. Securing robot control systems, OT networks, and cloud analytics pipelines requires significant ongoing investment.

- Workforce Displacement and Reskilling Complexity: Automation transitions create skills mismatches, requiring manufacturers to invest in retraining programs. Balancing productivity gains with workforce management obligations adds operational complexity, particularly in high-employment automotive regions.

Market Opportunities

- EV Gigafactory Expansion: ABB estimates that over 80 planned gigafactories globally will still leave battery supply short of demand through 2030. Each gigafactory requires thousands of robotic cells for electrode manufacturing, cell assembly, and pack integration—representing a structured, multi-billion-dollar opportunity for robotic system suppliers.

- Collaborative Robot Deployment in Mixed-Model Plants: Cobots enable flexible mixed-model assembly without protective fencing, reducing integration costs and deployment timelines. The cobot segment is projected to grow through 2030, presenting a high-growth avenue for automation solution providers targeting mid-size OEMs and suppliers.

- Emerging Market Modernization: India's automotive manufacturing modernization drive, Southeast Asian plant upgrades, and Latin American EV investment programs represent significant greenfield opportunities for robotics vendors seeking international expansion beyond the mature Japan-Germany-U.S. markets.

Market Challenges

- Integration Complexity in Legacy Facilities: Retrofitting existing assembly lines with modern robotic systems requires significant engineering effort, production downtime, and process redesign—particularly challenging in brownfield automotive plants with decades-old infrastructure.

- Supply Chain Vulnerabilities for Critical Components: Robotic systems depend on rare earth elements, precision semiconductors, and specialized actuators—supply chains vulnerable to geopolitical disruptions, trade restrictions, and sourcing concentration risks in specific geographies.

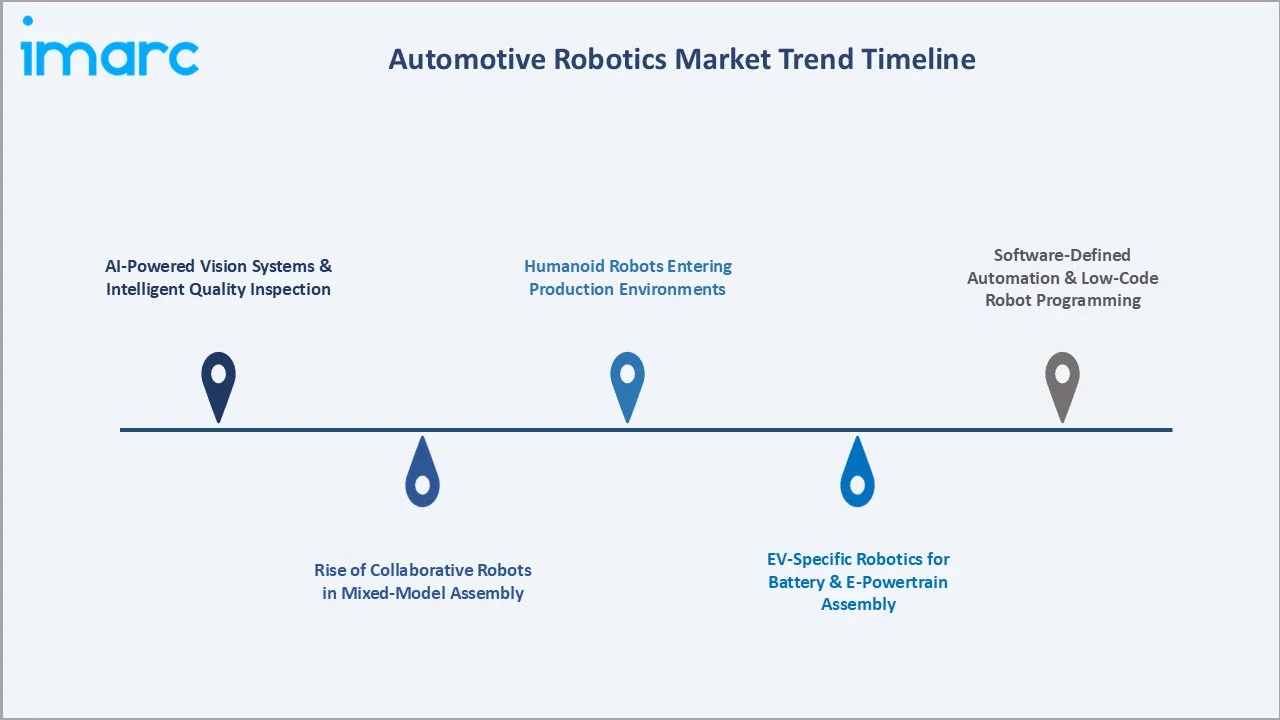

Emerging Market Trends

1. AI-Powered Vision Systems and Intelligent Quality Inspection

Advanced AI-enabled machine vision systems are redefining quality assurance in automotive manufacturing. These systems can detect ultra-fine defects in body-in-white welding and final trim operations—inspecting parts significantly faster than traditional coordinate-measuring machines. As OEMs move toward fully inline inspection without extending cycle time, AI vision is becoming standard across body shop, paint shop, and final assembly operations.

2. Rise of Collaborative Robots in Mixed-Model Assembly

The cobot market expected to reach approximately USD 5.6 Billion in 2027. At BMW's Spartanburg plant, cobots work alongside operators to apply adhesive insulation in door panels—a repetitive, ergonomically demanding task. Audi and Volkswagen have embedded cobots into intelligent factory strategies to increase flexibility across multi-model production platforms without requiring traditional guarding infrastructure.

3. EV-Specific Robotics for Battery and E-Powertrain Assembly

Electric vehicles introduce heavier battery modules, fewer but more complex sub-assemblies, and distinct sealing, welding, and wiring requirements. Robotics specifically engineered for EV battery assembly—including precision torque control, laser welding for cell interconnects, and vision-guided pack handling—represent one of the fastest-growing application segments.

4. Humanoid Robots Entering Production Environments

Humanoid robots are transitioning from laboratory demonstrations into active production pilots. In 2025, Hyundai Motor Group announced a USD 21 billion U.S. investment plan through 2028, allocating USD 6 billion to expand future industries and strengthen external partnerships and energy infrastructure, including EV charging—signaling that humanoid robots will increasingly perform flexible assembly, quality checks, and component handling tasks by 2028-2030.

5. Software-Defined Automation and Low-Code Robot Programming

Traditional robot programming requiring specialized expertise is giving way to AI-assisted, low-code platforms that enable faster deployment, rapid model changeovers, and real-time workflow optimization. This democratization of robotics programming is expanding adoption beyond large OEMs into Tier-2 and Tier-3 suppliers who previously lacked the engineering resources to manage complex robotic installations at scale.

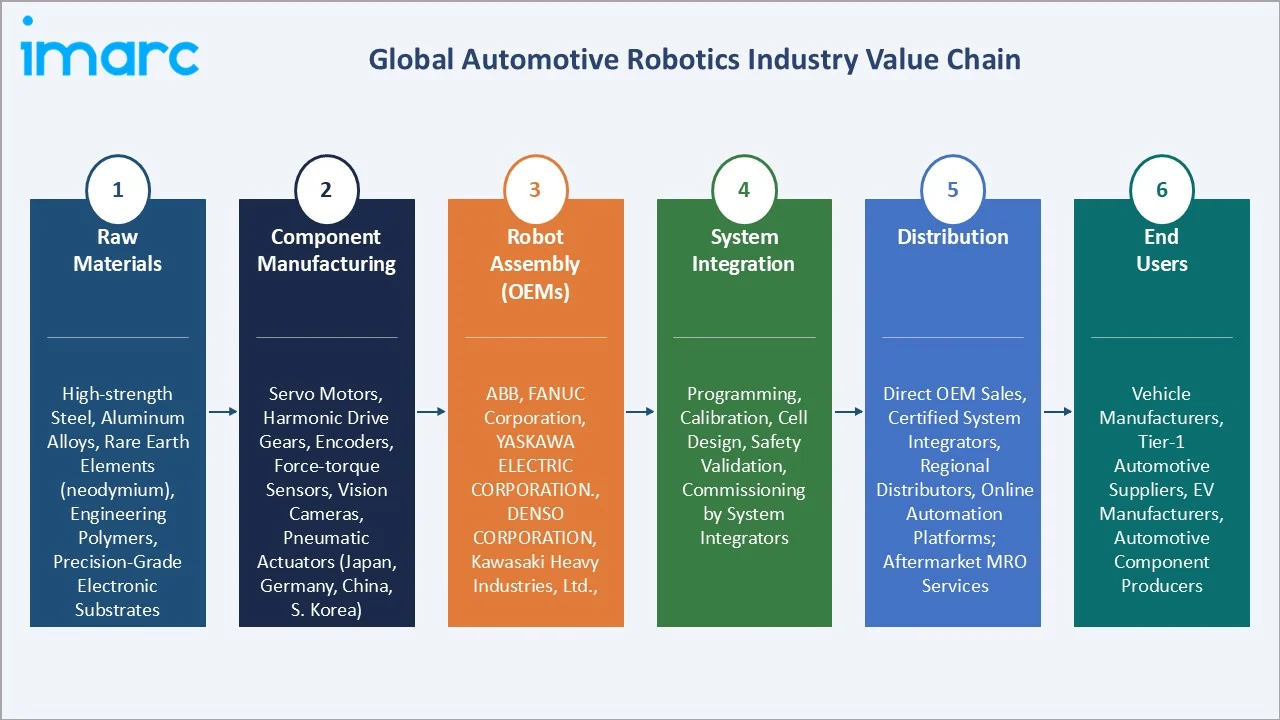

Industry Value Chain Analysis

The global automotive robotics industry value chain spans six integrated stages from raw material supply through end-user deployment. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements relevant to the overall automotive robotics market analysis.

|

Value Chain Stage |

Key Participants / Description |

|

Raw Materials |

High-strength steel, aluminum alloys, rare earth elements (neodymium for magnets), engineering polymers, precision-grade electronic substrates |

|

Component Manufacturing |

Servo motors, harmonic drive gears, encoders, force-torque sensors, vision cameras, pneumatic actuators produced by Tier-2/Tier-3 suppliers in Japan, Germany, China, and South Korea |

|

Robot Assembly (OEMs) |

ABB, FANUC Corporation, YASKAWA ELECTRIC CORPORATION., DENSO CORPORATION, Kawasaki Heavy Industries, Ltd. – full product assembly, control system integration, AI software embedding, and international safety certification (ISO 10218) |

|

System Integration |

Programming, calibration, cell design, safety validation, and commissioning by system integrators and robot OEM service teams |

|

Distribution |

Direct OEM sales, certified system integrators, regional distributors, online automation platforms; aftermarket MRO services including spare parts and remote diagnostics |

|

End Users |

Vehicle manufacturers, Tier-1 suppliers, EV manufacturers, and automotive component producers |

Robot OEMs hold the highest strategic value by integrating precision mechanics, software intelligence, and safety systems into turnkey solutions. System integrators are critical translators between OEM hardware and customer-specific production needs, commanding significant value-add margins. Direct sales to large OEMs remain dominant, but digital procurement and remote commissioning platforms are reshaping distribution dynamics.

Technology Landscape in the Automotive Robotics Industry

AI and Machine Learning Integration

Artificial intelligence is transforming automotive robotics from deterministic, pre-programmed systems into adaptive, learning-capable machines. AI-powered vision systems detect sub-millimeter defects in real time, while machine learning algorithms enable robots to optimize motion paths, predict component wear, and adjust grip parameters autonomously. NVIDIA's Cosmos platform, released in January 2025, provides enhanced AI training capabilities for autonomous robots operating in dynamic factory environments.

Collaborative Robot Technology

Cobots equipped with force-torque sensors, proximity detection, and safety-rated control systems certified under ISO 10218 (updated 2025) and ISO/TS 15066 can operate adjacent to human workers without conventional protective guarding. This technology enables flexible, safe human-robot interaction in assembly, quality inspection, and material handling—expanding automation reach into operations previously considered unsuitable for traditional industrial robots.

Smart Connectivity and Industry 4.0

Modern automotive robots are embedded nodes within intelligent production networks. OPC-UA and MQTT protocols enable real-time machine-to-machine communication, while cloud-based analytics platforms aggregate production data to identify inefficiencies and predict maintenance needs. This connectivity reduces unplanned downtime, supports predictive maintenance cycles, and enables remote monitoring and programming across geographically distributed manufacturing sites.

Advanced Sensing and Precision Control

High-resolution force-torque sensors, 3D vision cameras, LIDAR, and multi-spectral imaging systems are expanding robot perception capabilities beyond simple proximity detection. These sensors enable robots to handle variable-geometry components, adapt to part-to-part dimensional variation, and perform 100% quality inspection inline—replacing slower and less scalable coordinate-measuring machine processes in body shop and trim assembly.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product Type | Articulated Robot | 52.6% | 2025 |

| Component Type | Robotic Arm | 34.7% | 2025 |

| Application | Welding | 🔒 | 2025 |

| End User | 🔒 | 🔒 | 2025 |

| Region | Asia-Pacific | 49.3% | 2025 |

By Product Type

To access detailed market analysis, Request Sample

Articulated robots lead the global automotive robotics market with a 52.6% share in 2025. Their six-axis configuration enables full spatial mobility—reaching around obstacles, welding interior structures, and applying coatings with consistent film thickness across complex geometries. As EV body architectures shift from steel to aluminum and carbon-fiber composites, articulated robots are being reconfigured for friction stir welding, laser bonding, and structural adhesive dispensing.

By Component Type

The robotic arm component segment leads with a 34.7% share in 2025, reflecting its status as the foundational mechanical element in every robot installation. Robotic arm innovation is advancing toward lighter payloads using carbon-fiber-reinforced polymer structures, enabling higher speed-to-payload ratios for EV applications.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

Major Markets |

|

Asia-Pacific |

49.3% |

China auto production, Japan robotics leadership, India modernization, EV expansion |

China, Japan, South Korea, India |

|

Europe |

21.4% |

EU EV mandates, Volkswagen/BMW investment, advanced automation standards |

Germany, France, UK, Italy |

|

North America |

18.6% |

IRA Act incentives, U.S. EV plant investments, labor cost automation |

USA, Canada, Mexico |

|

Latin America |

6.2% |

Brazil/Mexico auto sector modernization, EV investment |

Brazil, Mexico, Argentina |

|

Middle East & Africa |

4.5% |

GCC industrial diversification, new auto assembly capacity |

Saudi Arabia, UAE, South Africa |

Asia-Pacific commands 49.3% global revenue share in 2025. China is the world's largest vehicle manufacturing market by annual sales and production output, with domestic production expected to reach 35 million vehicles by 2025—driving massive procurement of industrial robots across OEM assembly plants.

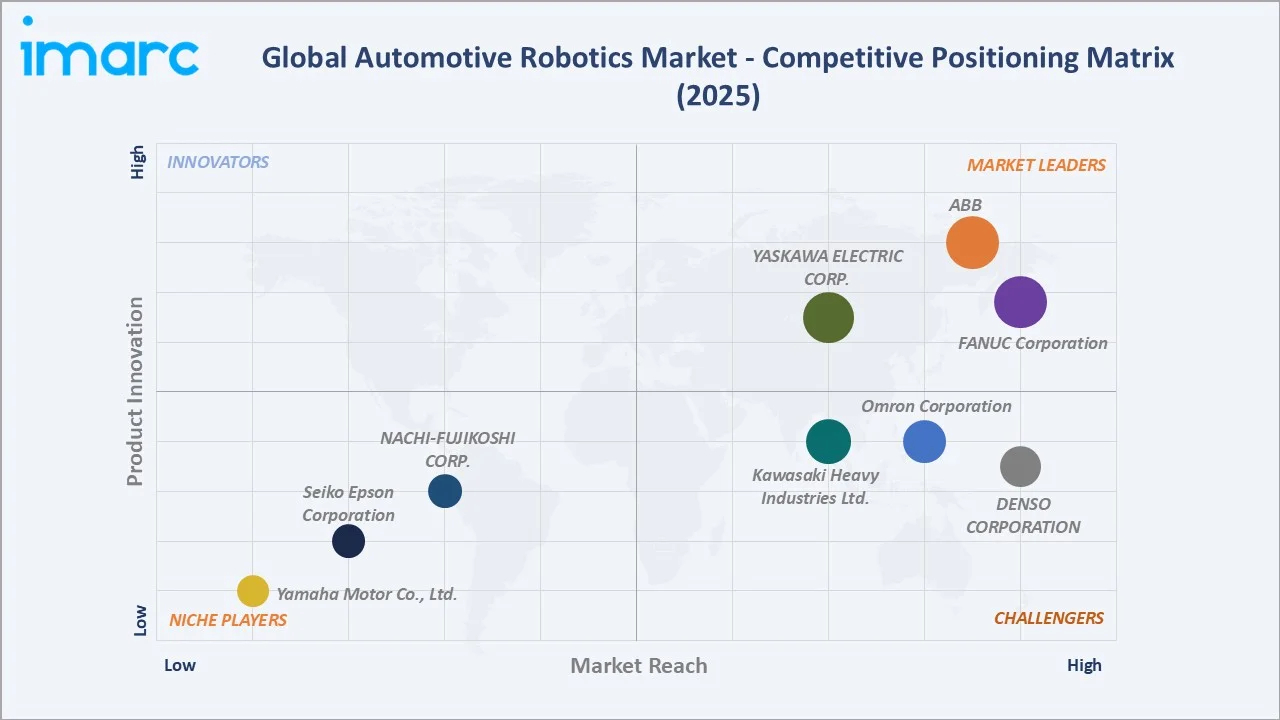

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

ABB |

ABB Robotics, YuMi |

Leader |

Global scale, AI integration, EV automation expertise |

|

FANUC Corporation |

FANUC Series, CRX Cobots |

Leader |

Largest industrial robot installed base, precision manufacturing |

|

YASKAWA ELECTRIC CORPORATION. |

MOTOMAN |

Leader |

High-speed welding, global automotive customer base |

|

DENSO CORPORATION |

VS Series, VM Series |

Challenger |

SCARA expertise, Asian automotive supplier networks |

|

Kawasaki Heavy Industries, Ltd. |

RS/RA Series, BA Series, BX Series |

Challenger |

Painting and welding robots, Japanese OEM alignment |

|

Omron Corporation |

TM Series Cobots |

Challenger |

Integrated machine vision, collaborative automation |

|

NACHI-FUJIKOSHI CORP. |

SRA Series, EZ Series |

Emerging |

Japan-focused, strong in spot welding applications |

|

Seiko Epson Corporation |

T Series, N Series, C Series |

Emerging |

SCARA/compact robot precision, clean-room capability |

|

Yamaha Motor Co., Ltd. |

YK Series |

Emerging |

Linear conveyor modules, electronics assembly focus |

The global automotive robotics market competitive landscape is moderately consolidated, with global powerhouses competing alongside regional specialists and innovative cobot manufacturers.

Key Company Profiles

ABB

ABB is a global leader in electrification, automation, and industrial robotics, headquartered in Zurich, Switzerland. Founded in 1988 through a merger of ASEA and BBC Brown Boveri, ABB operates across 100+ countries with a dedicated Robotics and Discrete Automation business unit serving automotive, electronics, and logistics sectors.

- Product & Platform Portfolio: ABB's automotive robotics portfolio includes the IRB series (welding, material handling, painting), the SWIFTI and GoFa collaborative robots, and the YuMi dual-arm cobot. The OmniCore controller platform integrates AI-assisted programming and fleet management, supporting deployments from single cells to fully automated production lines.

- Recent Developments: In 2025, ABB launched the Flexley Mover P603 AMR (autonomous mobile robot) with a 1,500‑kg payload, aimed at moving large automotive components and supporting flexible line‑reconfiguration in EV and ICE plants.

- Strategic Focus: ABB's strategy centers on EV manufacturing automation, AI-enhanced robot programming through its Wizard easy programming tool, and expansion of its collaborative robot portfolio. The company is investing in digital twin capabilities and remote monitoring platforms to reduce customer total cost of ownership.

FANUC Corporation

FANUC Corporation is a global leader in factory automation, industrial robotics, and CNC systems, headquartered in Oshino, Yamanashi, Japan. Founded in 1956, the company operates in over 100 countries and is a dominant supplier of automation solutions to automotive, electronics, and heavy manufacturing industries.

- Product & Platform Portfolio: FANUC's automotive robotics portfolio spans the M-Series (high-payload material handling, up to 2,300 kg), R-Series welding robots, P-Series painting robots, and the CRX collaborative robot series designed for safe, tool-free reprogramming by production workers. The FANUC Series 30i control platform supports Industry 4.0 connectivity.

- Recent Developments: In 2022, FANUC introduced the M-1000iA, a 1,000 kg payload industrial robotic arm designed for EV battery pack and heavy automotive component handling. FANUC has since expanded CRX cobot deployments across Tier-1 automotive suppliers seeking flexible mixed-model assembly capabilities.

- Strategic Focus: FANUC's strategy focuses on maintaining its global installed base leadership through lifecycle service contracts, expanding cobot adoption among mid-tier automotive suppliers, and integrating AI-based zero-downtime manufacturing capabilities within its FIELD (FANUC Intelligent Edge Link and Drive) IoT platform.

YASKAWA ELECTRIC CORPORATION

Yaskawa Electric Corporation is a global leader in industrial automation, robotics, and motion control solutions. Founded in 1915 and headquartered in Kitakyushu, Japan, the company is recognized as a pioneer in drive technology and robotics, supporting productivity and efficiency across diverse industrial sectors.

- Product & Platform Portfolio: Yaskawa’s automotive robotics portfolio includes the MOTOMAN series for arc welding, spot welding, painting, assembly, and material handling. Its HC-series collaborative robots enable human-robot interaction, while the YRC controller platform supports high-speed, synchronized multi-robot operations and flexible production line integration.

- Recent Developments: In 2025, Yaskawa Electric Corporation has announced a major robotics manufacturing expansion in the U.S., with plans to build a new state-of-the-art facility in Wisconsin. The site will enable local production of high-volume industrial robots, strengthen supply chains and reducing lead times for automotive and industrial customers.

- Strategic Focus: Yaskawa’s strategy centers on expanding automation in EV manufacturing, strengthening collaborative robot adoption, and integrating AI-driven motion control and predictive maintenance. The company is also investing in smart factory solutions and digital integration to improve production efficiency and lifecycle performance.

Market Concentration Analysis

The global automotive robotics market exhibits moderate consolidation. The top five players— ABB, FANUC Corporation, YASKAWA ELECTRIC CORPORATION., DENSO CORPORATION, Kawasaki Heavy Industries, Ltd —collectively account for approximately 55-65% of global market revenue in 2025.

The market exhibits a bifurcated competitive dynamic. At the premium OEM tier, consolidation is occurring around AI platform depth, safety certification portfolios, and EV-specific application expertise. ABB and FANUC Corporation maintain the widest global sales and service networks, providing significant scale advantages in large automotive OEM procurement processes. Meanwhile, Chinese robotic challengers—backed by domestic government automation subsidies and deep supply chain integration—are advancing quality benchmarks and targeting export markets, compressing margins in standard welding and material handling applications across Asia-Pacific.

Strategic acquisitions such as Hyundai Motor Group's partnership with Boston Dynamics, and BMW's engagement with Figure AI for humanoid robot pilots, are reshaping the competitive boundary between automotive OEMs and robotics suppliers through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

EV battery assembly robotics represent the single highest-growth application niche, driven by multiple planned gigafactories globally requiring specialized robotic systems for electrode manufacturing, cell-to-module integration, and pack assembly. Collaborative robots are the fastest-growing robot category, expanding through 2030, as mid-size automotive suppliers adopt flexible automation without traditional guarding infrastructure. AI-powered vision and inspection systems are achieving mainstream adoption across body shop and final assembly, creating a rapidly expanding software and sensor aftermarket.

Emerging Market Expansion

India represents the highest-potential emerging market for automotive robotics, supported by Production-Linked Incentive (PLI) schemes for automotive and auto components, rapid vehicle demand growth, and a government push toward domestic EV manufacturing. Southeast Asian automotive assembly modernization in Thailand, Vietnam, and Indonesia offers incremental volume opportunities. Latin America's EV investment pipeline—particularly Brazil's USD multi-billion EV production commitments and incentive frameworks—is creating structured demand for robotic assembly systems across the mid-2020s.

Venture and Strategic Investment Trends

Hyundai Motor Group's USD 21 billion U.S. investment plan (2025-2028), USD 6 billion to expand future industries and strengthen external partnerships and energy infrastructure, including EV charging, exemplifies the magnitude of strategic automotive-robotics convergence. NVIDIA's Cosmos platform (January 2025) is attracting venture investment in AI-native robot training environments. Investments in digital twin platforms, low-code robot programming, and remote fleet management systems are attracting both corporate venture and private equity capital as automotive manufacturers seek to compress deployment timelines and reduce system integration costs.

Future Market Outlook (2026-2034)

The global automotive robotics market forecast projects sustained value expansion from USD 13.24 Billion in 2025 to USD 29.85 Billion by 2034 at a CAGR of 9.17%. Asia-Pacific will retain its dominant regional position—advancing at approximately 10.4% CAGR—while Europe and North America sustain growth through EV mandate compliance and renovation of legacy manufacturing infrastructure.

Three structural shifts will reshape the automotive robotics market through 2034. First, humanoid robots will move from production pilots to targeted deployment in flexible assembly tasks by 2028-2030.

Second, AI-native robot programming platforms will compress deployment cycles from months to weeks, democratizing automation access for Tier-2 and Tier-3 suppliers who represent the next major growth frontier. Third, the EV architecture transition—eliminating traditional engine assembly while creating entirely new requirements for battery, e-axle, and power electronics production, creating both displacement and growth across the competitive landscape.

Research Methodology

Primary Research

Primary research encompassed structured interviews conducted in 2024-2025 with automotive robotics industry stakeholders, including automation directors at vehicle OEMs, procurement leaders at Tier-1 automotive suppliers, product managers at robot manufacturers, system integrators, and institutional investors in industrial automation. Primary insights were used to validate market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include the International Federation of Robotics (IFR) Annual World Robotics Report, U.S. International Trade Administration data, European Commission automotive industry publications, International Energy Agency EV outlook, company annual reports and investor presentations, industry trade publications including Automotive Manufacturing Solutions and Assembly Magazine, and regional automotive association databases.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating vehicle production volume data, automation penetration rates by application, regional capex trends, and historical robot shipment growth rates. Scenario analysis—base, optimistic, and conservative cases—was performed to account for EV adoption pace uncertainty and macroeconomic variability.

Automotive Robotics Market Report Scope

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Types Covered | Cartesian Robots, SCARA Robots, Articulated Robot, Others |

| Component Types Covered | Controller, Robotic Arm, End Effector, Drive and Sensors |

| Applications Covered | Assembly, Dispensing, Material Handling, Welding, Others |

| End Users Covered | Vehicle Manufacturers, Automotive Component Manufacturers |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | ABB, FANUC Corporation, YASKAWA ELECTRIC CORPORATION., DENSO CORPORATION, Kawasaki Heavy Industries, Ltd., Omron Corporation, NACHI-FUJIKOSHI CORP., Seiko Epson Corporation, Yamaha Motor Co., Ltd., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive robotics market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global automotive robotics market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive robotics industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive Robotics Market Report

The global automotive robotics market was valued at USD 13.24 Billion in 2025, driven by EV production growth, Industry 4.0 integration, and rising demand for precision manufacturing automation.

The market is projected to reach USD 29.85 Billion by 2034, growing at a CAGR of 9.17% during 2026-2034, supported by EV gigafactory expansion, cobot adoption, and AI-powered automation platforms.

Primary drivers include accelerating EV production requiring specialized robotics, Industry 4.0 and IIoT integration, rising labor costs, government automation incentives, and the growing need for precision manufacturing in high-mix automotive assembly.

Asia-Pacific dominates with a 49.3% share in 2025, underpinned by China's massive vehicle production base, Japan's world-class robotics ecosystem, South Korea's advanced manufacturing, and India's modernization drive.

Articulated robots lead with a 52.6% share in 2025, valued for their six-axis flexibility in welding, painting, material handling, and EV body shop assembly across diverse vehicle platforms.

The robotic arm segment holds the largest component share at 34.7% in 2025, as the primary mechanical execution unit underpinning all robot configurations across automotive manufacturing applications.

EV battery and e-powertrain assembly is the fastest-growing application, driven by over 80 planned gigafactories globally requiring specialized robotic systems for precision battery manufacturing and pack integration.

Major players include ABB, FANUC Corporation, YASKAWA ELECTRIC CORPORATION., DENSO CORPORATION, Kawasaki Heavy Industries, Ltd., Omron Corporation, NACHI-FUJIKOSHI CORP., Seiko Epson Corporation, and Yamaha Motor Co., Ltd.

North America held an 18.6% share of the global automotive robotics market in 2025, with the U.S. market projected to reach USD 8.28 Billion by 2033, growing at approximately 10.74% CAGR driven by IRA incentives and EV manufacturing investments.

AI enables predictive maintenance, real-time defect detection, adaptive motion planning, and low-code robot programming—compressing deployment timelines and expanding automation access to mid-tier automotive suppliers.

Key opportunities include EV gigafactory robotic system supply, cobot deployment for Tier-2 suppliers, AI vision and inspection platforms, humanoid robot production pilots, and robotics-as-a-service models for capital-constrained manufacturers.

The market is moderately consolidated, with the top five players (ABB, FANUC Corporation, YASKAWA ELECTRIC CORPORATION., DENSO CORPORATION, Kawasaki Heavy Industries, Ltd) holding approximately 55-65% of global revenue, while cobot specialists and Chinese manufacturers are intensifying competition across emerging segments.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)