Automotive V2X Market Size, Share, Trends and Forecast by Communication, Connectivity, Vehicle Type, and Region, 2026-2034

Automotive V2X Market Size, Share, Trends & Forecast (2026-2034)

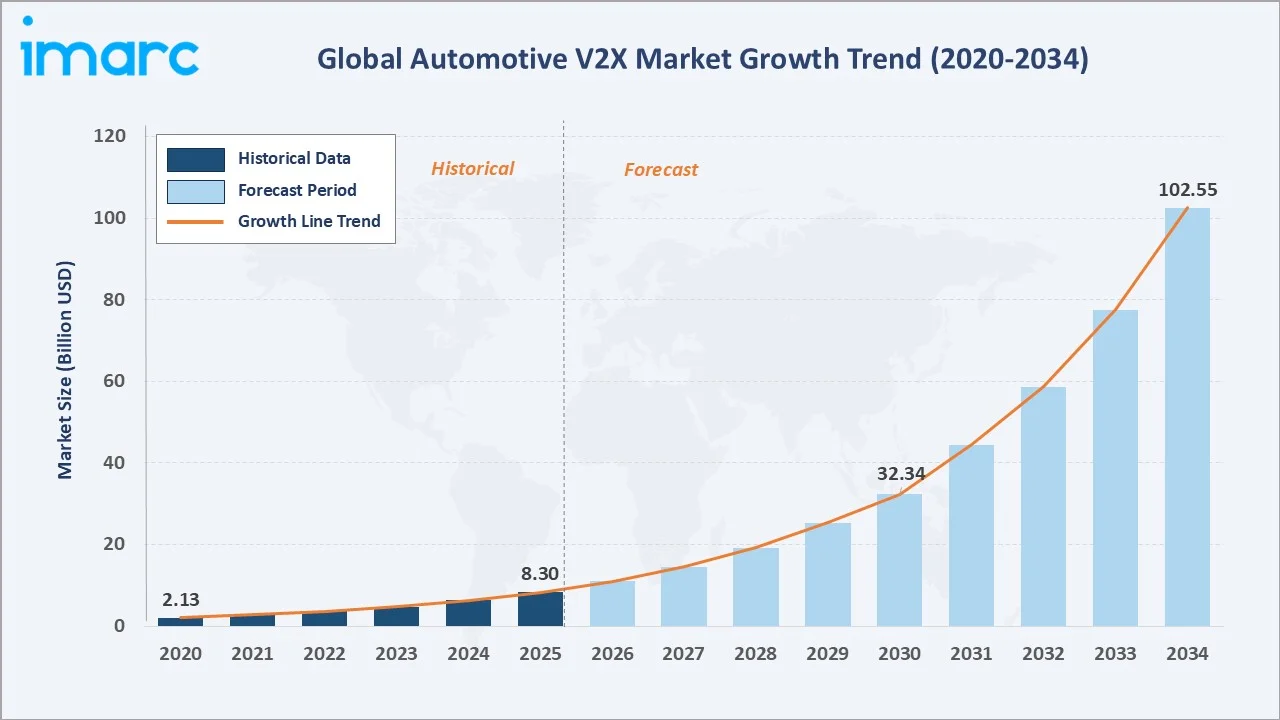

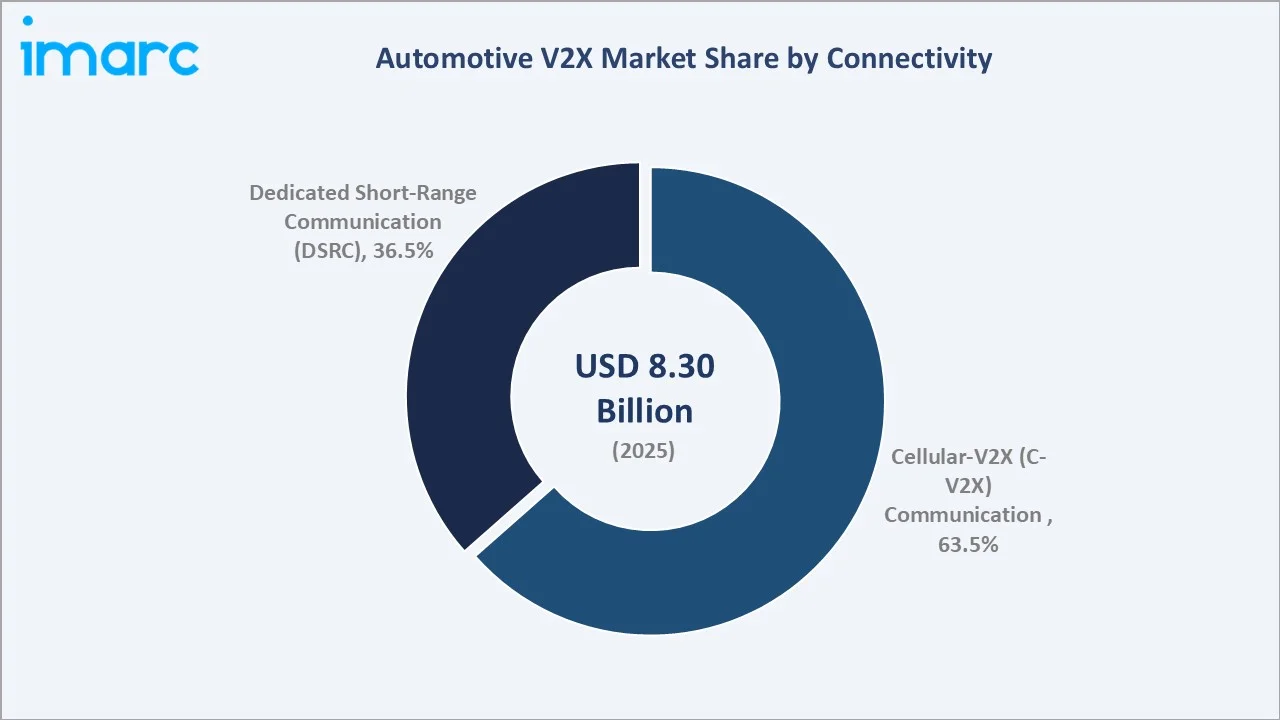

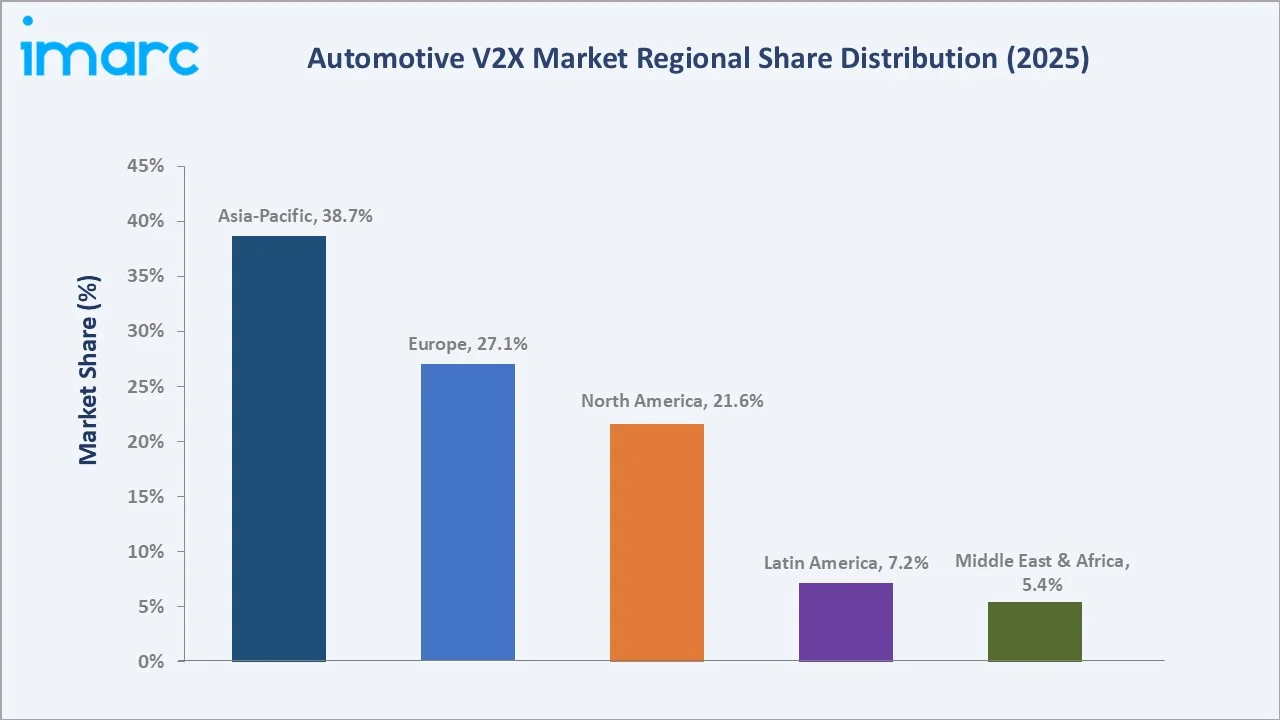

The global automotive V2X market reached USD 8.30 Billion in 2025 and is projected to reach USD 102.55 Billion by 2034, growing at a CAGR of 31.25% during 2026-2034. The market is driven by rising demand for connected vehicles, road safety, and real-time traffic management. By 2030, connected vehicles are expected to represent nearly 95% of global new vehicle sales, while level three and level four autonomous vehicles are projected to rise from 1% in 2025 to around 12% by 2030. This shift is driving the automotive V2X market as connected and semi-autonomous vehicles require real-time communication with other vehicles, infrastructure, pedestrians, and networks. Cellular-V2X (C-V2X) communication leads connectivity at 63.5%. Passenger cars lead the vehicle type at 72.4%. Asia-Pacific leads regionally at 38.7%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 8.30 Billion |

|

Forecast Market Size (2034) |

USD 102.55 Billion |

|

CAGR (2026-2034) |

31.25% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Connectivity |

Cellular-V2X (C-V2X) Communication (63.5%, 2025) |

|

Dominant Vehicle Type |

Passenger Cars (72.4%, 2025) |

|

Leading Region |

Asia-Pacific (38.7%, 2025) |

The automotive V2X market has grown rapidly, rising from USD 2.13 Billion in 2020 to USD 8.30 Billion in 2025. It is projected to reach USD 32.34 Billion by 2030, supported by connected vehicle adoption, ADAS integration, and smart mobility infrastructure. By 2034, the market is expected to reach USD 102.55 Billion, reflecting strong demand for safer, data-driven, and autonomous-ready transportation systems.

To get more information on this market, Request Sample

Cellular-V2X (C-V2X) communication grows fastest at ~33.2% CAGR through 5G NR-V2X mass OEM integration and China’s large-scale vehicle-road-cloud integration pilots and C-V2X deployment programs. Passenger cars grow at ~31.8% CAGR through OEM Level 3/4 autonomous V2X integration and EV-V2X platform bundling.

.webp)

Executive Summary

The automotive V2X (Vehicle-to-Everything) market is expanding rapidly, driven by connected vehicles, ADAS adoption, and smart mobility infrastructure. The market grew from USD 2.13 Billion in 2020 to USD 8.30 Billion in 2025 and is forecast to reach USD 102.55 Billion by 2034. Rising demand for real-time vehicle communication, road safety, and traffic efficiency is accelerating V2X deployment. Growing 5G, autonomous driving, and smart city investments are further strengthening market growth. Cellular-V2X (C-V2X) communication at 63.5% leads through OEM adoption. Passenger cars at 72.4% lead through ADAS L2+ V2X premium integration. Asia-Pacific leads regionally at 38.7% through China's national C-V2X deployment.

Key Market Insights

|

Insight |

Data |

|

Dominant Connectivity |

Cellular-V2X (C-V2X) Communication - 63.5% share (2025) |

|

Dominant Vehicle Type |

Passenger Cars - 72.4% market share (2025) |

|

Leading Region |

Asia-Pacific - 38.7% share (2025) |

|

Market Opportunity |

5G NR-V2X autonomous driving safety application; C-V2X smart intersection; EV-V2G-V2X integration; commercial fleet C-V2X logistics; China V2X highway and smart city large-scale deployment |

Key Analytical Observations Supporting the Above Data:

- Cellular-V2X (C-V2X) Communication at 63.5%: Cellular-V2X (C-V2X) communication dominates due to its ability to support low-latency, high-reliability communication between vehicles, infrastructure, pedestrians, and networks.

- Passenger Cars at 72.4%: Passenger cars dominate as they represent the largest vehicle production and sales base globally. Rising adoption of ADAS, connected infotainment, safety alerts, and semi-autonomous driving features in passenger cars is accelerating V2X integration.

- Asia-Pacific at 38.7%: Asia-Pacific dominates regionally due to strong vehicle production, rapid connected car adoption, and large-scale smart mobility investments in China, Japan, South Korea, and India.

Automotive V2X Market Overview

The automotive V2X market operates within the broader connected vehicle and intelligent transportation system (ITS) market as the fastest-growing safety-critical connected vehicle communication segment. V2X technology encompasses V2V direct sidelink communication, V2I infrastructure communication, V2P pedestrian detection, V2N network communication, and V2G energy grid. Macroeconomic factors include rising vehicle production, growing urbanization, and increasing investments in smart transport infrastructure.

Market Dynamics

.webp)

To evaluate market opportunities, Request Sample

Market Drivers

- 5G Network Rollout: 5G network rollout enables ultra-low-latency, high-bandwidth, and highly reliable communication between vehicles, infrastructure, pedestrians, and cloud networks. Compared to previous wireless technologies, 5G supports real-time data exchange required for advanced driver assistance systems (ADAS) and autonomous driving. The global 5G rollout is gaining strong momentum, with nearly 390 networks launched worldwide and 5G population coverage reaching around 60% by the end of 2025. During the year, 5G access expanded to an additional 400 million people, while coverage outside mainland China is expected to rise from 50% in 2025 to nearly 85% by 2031. This expansion directly supports the automotive V2X market by enabling low-latency, high-speed communication between vehicles, infrastructure, pedestrians, and cloud networks. Wider 5G availability strengthens C-V2X deployment, improves real-time safety alerts, and supports advanced connected and autonomous driving applications.

- Smart City and Intelligent Transportation Investment: Smart city and intelligent transportation investment are creating connected road infrastructure that can communicate with vehicles in real time. Investments in smart traffic signals, roadside units, traffic monitoring systems, and digital road networks support vehicle-to-infrastructure communication. These systems improve traffic flow, reduce congestion, and enhance road safety through collision alerts and hazard warnings. As cities modernize mobility infrastructure, demand for V2X-enabled vehicles and communication platforms continues to rise.

- EV and Connected Vehicle Platform: The electric car market reached a record level in 2025, with sales increasing by 20% from 2024 to exceed 20 million units globally. As EV adoption expands, demand for V2X-enabled functions such as smart charging, route optimization, battery monitoring, and safety alerts is also increasing. Modern EVs and connected vehicles are equipped with advanced sensors, telematics systems, and software-defined architectures that support real-time data exchange. V2X technologies enhance battery management, route optimization, charging station connectivity, and safety functions. As automakers expand connected and electric vehicle portfolios, demand for V2X-enabled communication systems continues to accelerate.

Market Restraints

- High Deployment Cost and Infrastructure ROI Barrier: High deployment cost and infrastructure ROI barrier hampers the market because large investments are required for roadside units, sensors, 5G/C-V2X infrastructure, cloud platforms, and system integration. Governments and city authorities often face uncertainty over returns, especially when V2X-enabled vehicle penetration is still developing. High upfront costs can slow large-scale deployment of smart intersections, connected highways, and vehicle-to-infrastructure networks. This delays ecosystem readiness and limits faster adoption by automakers and mobility operators.

- Cybersecurity and Data Privacy in V2X Networks: Cybersecurity and data privacy in V2X networks hamper the market as connected vehicles exchange sensitive real-time data with infrastructure, cloud systems, and other road users. Any cyberattack, data breach, or signal manipulation can create serious safety risks, including false alerts or vehicle control disruptions. Strong encryption, authentication, and regulatory compliance increase development and deployment costs. These concerns can slow consumer trust, automaker adoption, and large-scale V2X rollout.

Market Opportunities

- Vehicle-to-Infrastructure (V2I) Deployment for Traffic Optimization: Vehicle-to-Infrastructure (V2I) deployment for traffic optimization enables vehicles to communicate with traffic signals, road sensors, toll systems, and smart highways in real time. American Association of State Highway and Transportation Officials (AASHTO), with support from U.S. DOT and Transport Canada, is assessing connected vehicle field infrastructure needs for future V2I deployment. The study supports agency planning and expects a mature connected vehicle ecosystem by 2040, with up to 80% of traffic signals and 25,000 roadside locations becoming V2I-enabled. As cities invest in intelligent transport systems, demand for V2X hardware, software, and communication platforms is expected to grow.

- Vehicle-to-Grid (V2G) and Smart Charging Communication Platforms: Vehicle-to-Grid (V2G) and smart charging communication platforms enable EVs to communicate with charging stations, power grids, and energy management systems. These platforms support bidirectional energy flow, smart load balancing, and optimized charging based on grid demand and electricity prices. As EV adoption grows, automakers and infrastructure providers will need reliable V2X communication systems for charging coordination and grid integration. This expands demand for V2X software, connectivity modules, and smart mobility-energy platforms.

Market Challenges

- Interoperability Issues Across Vehicles and Infrastructure Platforms: Interoperability issues across vehicles and infrastructure platforms pose a significant challenge as different automakers, telecom providers, and infrastructure operators often use varying communication standards and technologies. Lack of seamless compatibility can limit real-time data exchange between vehicles, roadside units, and traffic management systems. These inconsistencies increase integration complexity, deployment costs, and implementation timelines. As a result, large-scale V2X adoption may be delayed until common standards and cross-platform communication frameworks become more widely established.

- Limited V2X Infrastructure in Developing Economies: Limited V2X infrastructure in developing economies challenges the market as many regions lack connected traffic signals, roadside units, smart highways, and reliable 5G coverage. This restricts real-time communication between vehicles and infrastructure, reducing the effectiveness of V2X applications. Budget constraints and slower smart city investments further delay deployment. As a result, automakers may face limited incentives to integrate V2X technologies in markets where supporting infrastructure is not yet mature.

Emerging Market Trends

.webp)

1. 5G NR-V2X Sidelink and Network-Assisted V2X

5G NR-V2X sidelink and network-assisted V2X enable ultra-reliable, low-latency communication for advanced safety and autonomous driving applications. NR-V2X sidelink allows direct communication between vehicles, pedestrians, and infrastructure without relying solely on cellular networks, while network-assisted V2X leverages 5G infrastructure for broader coverage and cloud connectivity. Together, these technologies support cooperative driving, platooning, collision avoidance, and real-time traffic management. As 5G deployment expands globally, adoption of next-generation V2X communication platforms is accelerating.

2. AI-Integrated V2X Technology

AI-integrated V2X technology enables vehicles to interpret real-time data from nearby vehicles, traffic signals, road sensors, and cloud systems. AI helps predict hazards, optimize routes, and support faster driving decisions in complex traffic environments. In October 2025, Dubai’s Roads and Transport Authority is upgraded its traffic systems by combining AI with V2X technology, moving beyond conventional signal timing toward real-time connected traffic management. The system is expected to reduce congestion by up to 37% and deliver live traffic updates directly to vehicle dashboards. It enables faster hazard detection, smoother routing, safer driving decisions, and more efficient urban mobility.

3. V2P and Vulnerable Road User V2X

V2P (Vehicle-to-Pedestrian) and vulnerable road user V2X are emerging as governments and automakers prioritize road safety. These solutions enable vehicles to communicate with pedestrians, cyclists, and other vulnerable road users through smartphones, wearable devices, and connected infrastructure. Real-time alerts help drivers detect potential collision risks, especially in blind spots and complex urban environments. As smart city initiatives expand and safety regulations become stricter, adoption of V2P technologies is expected to increase significantly.

4. V2G Energy Management and EV Smart Charging

V2G energy management and EV smart charging are emerging as EVs increasingly communicate with grids, chargers, and energy platforms. In May 2026, Polestar and charging operator Clever are testing V2X technology in selected Danish homes, allowing EVs to power households, return electricity to the grid, and provide backup energy during outages. The joint pilot is Denmark’s first complete V2X solution, demonstrating how the Polestar 4 can act as a mobile power bank to lower energy costs, support grid stability, and improve energy resilience. As EV adoption rises, V2G-ready communication systems are becoming important for connected mobility and smart energy ecosystems.

Industry Value Chain Analysis

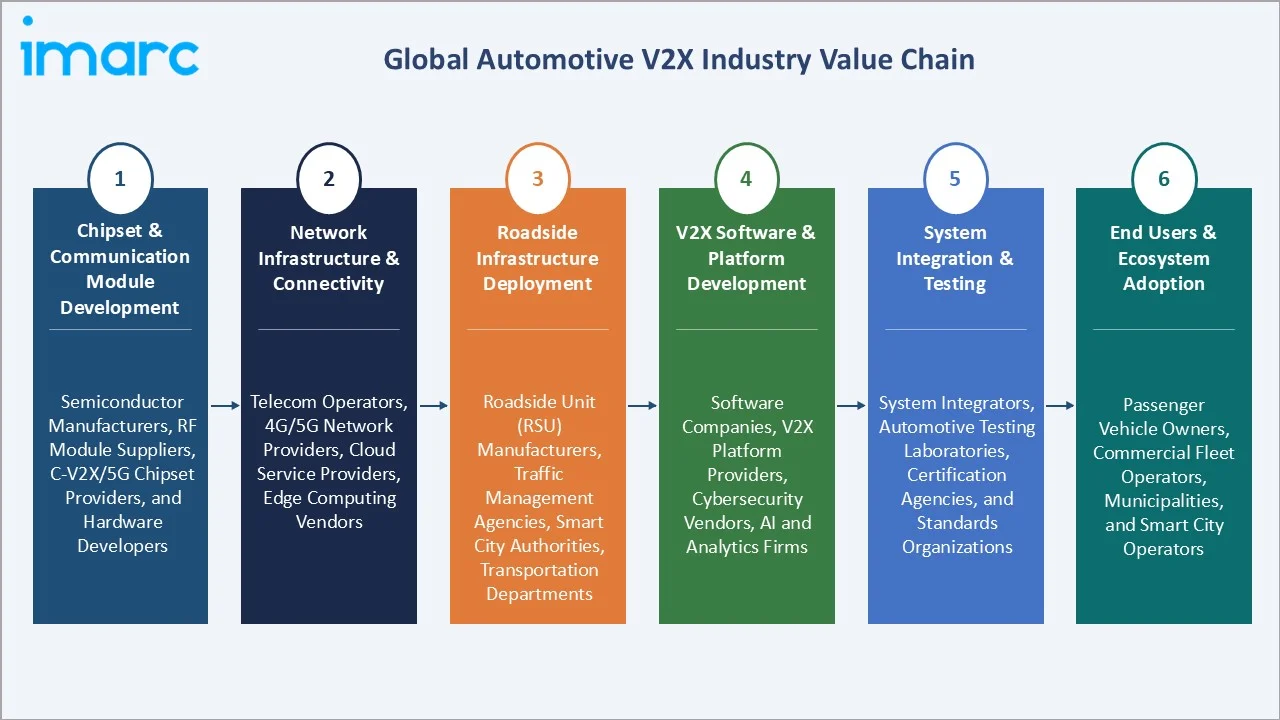

The automotive V2X value chain integrates chipset & communication module development, network infrastructure & connectivity, roadside infrastructure deployment, V2X software & platform development, system integration & testing, and end users & ecosystem adoption.

|

Stage |

Key Participants |

|

Chipset & Communication Module Development |

Semiconductor manufacturers, RF module suppliers, C-V2X/5G chipset providers, and hardware developers |

|

Network Infrastructure & Connectivity |

Telecom operators, 4G/5G network providers, cloud service providers, edge computing vendors |

|

Roadside Infrastructure Deployment |

Roadside unit (RSU) manufacturers, traffic management agencies, smart city authorities, transportation departments |

|

V2X Software & Platform Development |

Software companies, V2X platform providers, cybersecurity vendors, AI and analytics firms |

|

System Integration & Testing |

System integrators, automotive testing laboratories, certification agencies, and standards organizations |

|

End Users & Ecosystem Adoption |

Passenger vehicle owners, commercial fleet operators, municipalities, and smart city operators |

V2X software & platform development is the most value-added stage in the automotive V2X value chain as it transforms raw vehicle and infrastructure data into actionable safety, traffic management, and autonomous driving insights. AI, edge computing, cybersecurity, and real-time analytics enable cooperative perception, collision avoidance, and intelligent mobility services. As V2X ecosystems become more connected, software platforms increasingly differentiate vendors through performance, interoperability, and advanced application capabilities.

Technology Landscape in the Automotive V2X Industry

5G NR-V2X Communication Technology

5G NR-V2X communication technology enables ultra-low-latency, high-speed, and highly reliable communication between vehicles, infrastructure, pedestrians, and networks. Compared with earlier V2X technologies, 5G NR-V2X supports advanced applications such as cooperative driving, autonomous vehicle coordination, platooning, and real-time hazard alerts. Its ability to handle large volumes of data enhances situational awareness and traffic efficiency. As 5G networks expand globally, NR-V2X is becoming a foundational technology for next-generation connected and autonomous mobility ecosystems.

Autonomous Driving and Cooperative Driving Technologies

Autonomous driving and cooperative driving technologies enable vehicles to exchange real-time information with other vehicles, infrastructure, and traffic systems. V2X communication enhances autonomous driving by improving situational awareness beyond the vehicle’s onboard sensors. Cooperative driving applications support coordinated lane changes, platooning, intersection management, and collision avoidance. As automakers advance toward higher levels of vehicle autonomy, V2X-enabled cooperative intelligence is becoming a critical component of safe and efficient mobility systems.

Cloud-Enabled V2X Infrastructure Development

Cloud-enabled V2X infrastructure development providing scalable platforms for real-time data collection, processing, and distribution. Cloud systems enable vehicles, roadside infrastructure, and traffic management centers to share information seamlessly across large geographic areas. In August 2025, DENSO Products and Services Americas and AT&T Connected Solutions collaborated to provide cities and automakers with customizable services, certified hardware, and software for safer and more efficient mobility. The partnership combines AT&T’s nationwide cellular network and cloud-based Intelligent Transportation Platform with 5.9 GHz C-V2X for localized safety-critical applications. DENSO’s MobiQ V2X On-Board Unit supports hybrid communication through embedded cellular and 5.9 GHz modems, enabling interoperability for next-generation transportation systems. As connected vehicle volumes increase, cloud-enabled V2X infrastructure is becoming essential for efficient, secure, and intelligent transportation ecosystems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Communication |

Vehicle-to-Vehicle (V2V) |

🔒 |

2025 |

|

Connectivity |

Cellular-V2X (C-V2X) Communication |

63.5% |

2025 |

|

Vehicle Type |

Passenger Cars |

72.4% |

2025 |

|

Region |

Asia-Pacific |

38.7% |

2025 |

By Connectivity

Cellular-V2X (C-V2X) communication leads at 63.5% (2025), due to its ability to provide reliable, low-latency communication across vehicles, infrastructure, pedestrians, and networks. Its compatibility with existing 4G LTE and evolving 5G networks enables broader coverage and scalability than alternative technologies. C-V2X also supports advanced applications such as collision avoidance, cooperative driving, and autonomous vehicle operations, driving widespread industry adoption.

To access detailed market analysis, Request Sample

Dedicated short-range communication (DSRC) at 36.5%, by enabling direct, low-latency communication between vehicles and roadside infrastructure without relying on cellular networks. Its proven performance in safety-critical applications such as collision warnings, intersection safety, and emergency vehicle alerts continues to support deployment in intelligent transportation systems.

By Vehicle Type

Passenger cars lead at 72.4% (2025), due to their high global production volume and rapid adoption of connected vehicle technologies. Automakers are increasingly integrating V2X with ADAS, infotainment, navigation, and safety systems in passenger vehicles. Rising consumer demand for safer, smarter, and semi-autonomous driving experiences further supports V2X deployment in this segment.

.webp)

Commercial vehicles at 27.6% reflect trucking platooning V2X, emergency vehicle priority V2X, and public transit bus signal priority V2X.

Regional Market Insights

|

Region |

Share (2025) |

Key Automotive V2X Market Drivers & Characteristics |

|

Asia-Pacific |

38.7% |

Supported by strong vehicle production, rapid 5G rollout, connected car adoption, and smart mobility investments in China, Japan, South Korea, and India. |

|

Europe |

27.1% |

Driven by strong road safety regulations, autonomous driving pilots, smart city programs, and OEM-led deployment of connected vehicle technologies. |

|

North America |

21.6% |

Driven by investments in intelligent transportation systems, C-V2X trials, 5G infrastructure, and strong participation from automakers, telecom firms, and technology providers. |

|

Latin America |

7.2% |

Gradually adopting V2X technologies through urban mobility upgrades, traffic management improvements, and growing interest in connected vehicle safety applications. |

|

Middle East and Africa |

5.4% |

Supported by smart city projects, intelligent road infrastructure, and connected mobility initiatives in countries such as the UAE and Saudi Arabia. |

Asia-Pacific leads the global automotive V2X market with a 38.7% share in 2025, driven by strong vehicle production, rapid 5G deployment, and smart mobility investments. Europe follows with 27.1%, supported by road safety regulations, autonomous driving pilots, and connected vehicle programs. North America accounts for 21.6%, backed by ITS investments, C-V2X trials, and telecom-automotive partnerships.

Latin America holds 7.2%, with growth supported by urban mobility modernization and traffic management needs. The Middle East and Africa represent 5.4%, emerging through smart city projects and intelligent road infrastructure development.

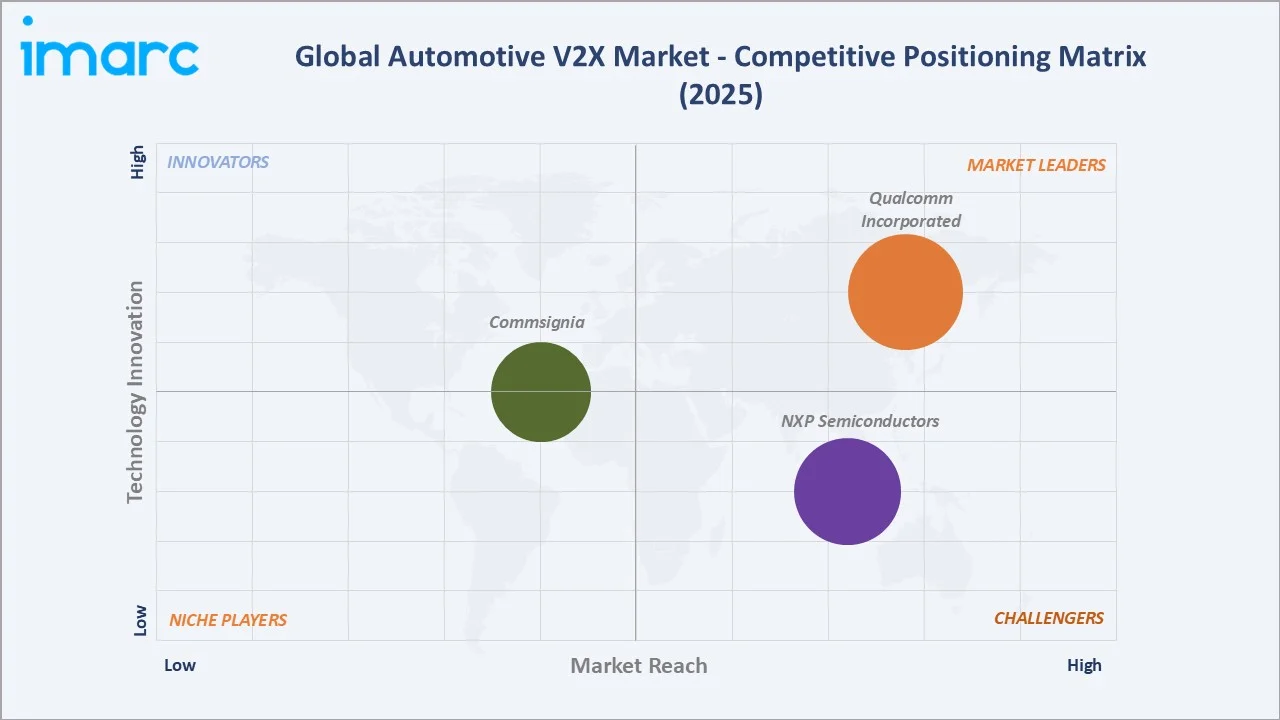

Competitive Landscape

The automotive V2X market is moderately concentrated, with competition led by automotive technology providers, semiconductor companies, telecom operators, and intelligent transportation system vendors. Major players are investing heavily in C-V2X, 5G NR-V2X, AI-powered cooperative perception, and cloud-based mobility platforms to strengthen their market positions. Strategic partnerships between automakers, network providers, and infrastructure developers are accelerating the deployment of connected vehicle ecosystems.

|

Company |

Key Products |

Market Position |

Core Strength |

|

Qualcomm Incorporated |

Qualcomm V2X 350 Chipsets, Qualcomm V2X 300 Chipsets, Qualcomm V2X 350 Demo Kits, Qualcomm V2X 250 Chipsets, Qualcomm V2X 200 Chipsets |

Market Leader |

Qualcomm Incorporated is a primary driver of automotive Cellular Vehicle-to-Everything (C-V2X) technology. They provide hardware, standards, and strategic acquisitions to enable direct communication between vehicles, infrastructure, and pedestrians without needing a cellular network. |

|

NXP Semiconductors |

i.MX 8XLite |

Strong Challenger |

NXP Semiconductors is a market leader in automotive connectivity, providing the silicon, software, and security infrastructure required for Vehicle-to-Everything (V2X) technology. |

|

Commsignia |

Roadside Unit, Onboard Unit, OBU Lite |

Established Player |

Commsignia is a market-leading developer of end-to-end Vehicle-to-Everything (V2X) hardware and software solutions. They connect vehicles to infrastructure, pedestrians, and networks to enable active collision avoidance, autonomous driving support, and smart city traffic management. |

Companies are also focusing on interoperability, cybersecurity, and edge computing capabilities to support autonomous driving and real-time traffic management applications. As governments expand smart city and intelligent transportation initiatives, competition is increasingly centered on end-to-end V2X solutions that integrate vehicles, infrastructure, and cloud networks.

Key Company Profiles

Qualcomm Incorporated

Qualcomm Incorporated is a leading global semiconductor and wireless technology company with a strong presence in the automotive V2X market through its advanced connectivity and communication solutions. The company develops Cellular-V2X (C-V2X), 4G LTE, and 5G NR-V2X chipsets that enable real-time communication between vehicles, infrastructure, pedestrians, and cloud networks. Through its Snapdragon Digital Chassis platform, Qualcomm supports connected vehicles, advanced driver assistance systems (ADAS), telematics, and autonomous driving applications.

- Key Products: Qualcomm V2X 350 Chipsets, Qualcomm V2X 300 Chipsets, Qualcomm V2X 350 Demo Kits, Qualcomm V2X 250 Chipsets, Qualcomm V2X 200 Chipsets.

- Recent Developments: In June 2025, Qualcomm Technologies, a subsidiary of Qualcomm Incorporated, completed the acquisition of Autotalks, a specialist in direct V2X communication solutions. The acquisition strengthens Qualcomm’s portfolio of production-ready, automotive-grade V2X technologies for vehicles, roadside infrastructure, and two-wheelers.

- Strategic Focus: Advancing the automotive V2X market through the development of Cellular-V2X (C-V2X) and 5G NR-V2X technologies that enable low-latency, high-reliability vehicle communications.

NXP Semiconductors

NXP Semiconductors is a leading global semiconductor company and a prominent technology provider in the automotive V2X market. The company develops secure connectivity solutions, processors, microcontrollers, and wireless communication chipsets that support vehicle-to-vehicle (V2V), vehicle-to-infrastructure (V2I), and broader V2X applications.

- Key Products: i.MX 8XLite

- Strategic Focus: Expanding its leadership in the automotive V2X market through the development of secure, low-latency communication technologies for connected and autonomous vehicles.

Market Concentration Analysis

The automotive V2X market exhibits moderate to high market concentration, with a relatively small group of technology leaders controlling key components of the ecosystem. Major semiconductor companies, communication technology providers, automotive suppliers, and telecom operators dominate through extensive intellectual property portfolios and long-term partnerships with automakers. Strategic acquisitions, joint ventures, and ecosystem collaborations are common as vendors seek to expand interoperability and accelerate deployment. While entry barriers remain high due to technology complexity, certification requirements, and infrastructure investments, the growing demand for connected and autonomous vehicles is attracting new participants across software, AI, cloud, and mobility services segments.

Investment & Growth Opportunities

Highest Growth Segments

C-V2X 5G NR-V2X (~33.2% CAGR through mass OEM integration), China V2X national highway RSU (~40-45% CAGR from deployment scale), V2G EV-to-grid V2X (~35-40% CAGR through EV-V2G integration), cooperative perception V2X for L3/L4 autonomous driving (~35-40% CAGR), V2P pedestrian V2X (~30-32% CAGR), and commercial truck platooning V2X (~28-30% CAGR) represent V2X highest-growth investment vectors through 2034.

Investment Themes

- China Vehicle-Road-Cloud Integration V2X national deployment: China’s vehicle-road-cloud integration strategy is creating significant investment opportunities by connecting vehicles, roadside infrastructure, and cloud platforms into a unified intelligent transportation ecosystem. Large-scale deployment of roadside units, edge computing, AI traffic management, and C-V2X communication networks is driving demand for V2X hardware, software, and connectivity solutions.

- V2G EV-to-Grid V2X integration for smart charging and grid stability: V2G integration is emerging as a key investment theme as electric vehicles increasingly communicate with power grids and charging networks through V2X platforms. These systems enable bidirectional energy flow, smart charging optimization, and grid balancing services, creating opportunities for automakers, utilities, charging infrastructure providers, and V2X technology developers.

Future Market Outlook (2026-2034)

The global automotive V2X market is expected to expand sharply from USD 8.30 Billion in 2025 to USD 102.55 Billion by 2034, registering a 31.25% CAGR. This growth reflects accelerating adoption of connected vehicles, 5G-enabled C-V2X, autonomous driving, and intelligent transport infrastructure. The USD 32.34 Billion anchor value in 2030 marks a commercial scale inflection point, where V2X moves from pilot deployments to wider real-world implementation. Rising smart city investments, EV integration, and vehicle-road-cloud ecosystems will further support market expansion through 2034.

Three structural forces define automotive V2X growth through 2034. First, the rapid expansion of connected and autonomous vehicles is increasing demand for real-time communication between vehicles, infrastructure, and cloud networks. Second, the global rollout of 5G and Cellular-V2X (C-V2X) infrastructure is enabling low-latency, high-reliability connectivity required for advanced safety and mobility applications. Third, rising investments in smart cities, intelligent transportation systems, and vehicle-road-cloud integration are accelerating the deployment of V2X ecosystems to improve road safety, traffic efficiency, and autonomous driving capabilities.

Research Methodology

Primary Research

Primary research comprised in-depth interviews with automotive OEMs, Tier-1 suppliers, semiconductor companies, telecom operators, V2X technology providers, intelligent transportation system developers, and industry experts. Discussions focused on V2X deployment trends, connectivity technologies, infrastructure readiness, regulatory developments, and autonomous driving adoption.

Secondary Research

Secondary research encompassed analysis of automotive industry reports, government transportation publications, telecom and 5G deployment data, company annual reports, V2X standards documentation, and intelligent transportation system studies. It also included reviews of connected vehicle initiatives, smart city programs, regulatory frameworks, and technology developments across major automotive markets.

Forecasting Models

Forecasting models employed a combination of bottom-up and top-down market estimation approaches, incorporating connected vehicle penetration, 5G deployment trends, V2X infrastructure investments, and autonomous vehicle adoption rates. Market projections were validated through CAGR modeling, scenario analysis, and triangulation with primary industry insights.

Automotive V2X Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Communications Covered | Vehicle-To-Vehicle (V2V), Vehicle-To-Infrastructure (V2I), Vehicle-To-Pedestrian (V2P), Vehicle-To-Grid (V2G), Vehicle-To-Cloud (V2C), Vehicle-To-Device (V2D) |

| Connectivities Covered | Dedicated Short-Range Communication (DSRC), Cellular V2X (C-V2X) Communication |

| Vehicle Types Covered | Passenger Cars, Commercial Vehicles |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Qualcomm Incorporated, NXP Semiconductors, Commsignia, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive V2X market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global automotive V2X market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive V2X industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive V2X Market Report

The global automotive V2X market reached USD 8.30 Billion in 2025, driven by increasing adoption of connected and autonomous vehicles, expanding 5G network infrastructure, and rising investments in intelligent transportation systems. Governments and automakers are prioritizing road safety, traffic efficiency, and real-time vehicle communication, accelerating the deployment of V2V, V2I, and C-V2X technologies. Growing smart city initiatives and EV connectivity requirements are further supporting market growth.

The global automotive V2X market grows at 31.25% CAGR during 2026-2034, reaching USD 102.55 Billion by 2034. The CAGR reflects autonomous vehicle safety mandate, China national deployment, V2G EV energy management, and smart city V2I RSU investment.

Cellular-V2X (C-V2X) communication leads at 63.5% due to its low-latency, reliable connectivity across vehicles, infrastructure, pedestrians, and networks. Its compatibility with 4G LTE and 5G makes it scalable for safety alerts, cooperative driving, and autonomous mobility applications.

Passenger cars lead at 72.4% due to their high production volume and faster adoption of connected safety technologies. Growing integration of ADAS, infotainment, navigation, and semi-autonomous features is further increasing V2X deployment in this segment.

Asia-Pacific leads at 38.7% due to strong vehicle production, rapid connected car adoption, and large-scale 5G deployment across China, Japan, South Korea, and India. Government-backed smart mobility programs, intelligent transport investments, and strong EV growth further support regional dominance.

Leading companies include Qualcomm Incorporated, NXP Semiconductors, and Commsignia, among others.

The automotive V2X market is projected to reach USD 32.34 Billion by 2030, reflecting the rapid commercialization of connected mobility solutions. This milestone indicates a shift from pilot projects to wider deployment across vehicles, roads, and smart city infrastructure. Growth will be supported by 5G-enabled C-V2X, ADAS integration, autonomous driving development, and intelligent transportation investments.

Three priority investment opportunities are emerging in the automotive V2X market. First, China's vehicle-road-cloud integration deployments offer large-scale opportunities in connected infrastructure, roadside units, and cloud mobility platforms. Second, V2G EV-to-grid integration and smart charging networks are creating demand for bidirectional communication and energy management solutions. Third, 5G NR-V2X and AI-powered cooperative perception technologies present strong growth potential as automakers advance connected, autonomous, and safety-focused mobility systems.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)