Automotive Wiring Harness Market Size, Share, Trends and Forecast by Application, Material Type, Transmission Type, Vehicle Type, Category, Component, and Region, 2026-2034

Global Automotive Wiring Harness Market Size, Share, Trends & Forecast (2026-2034)

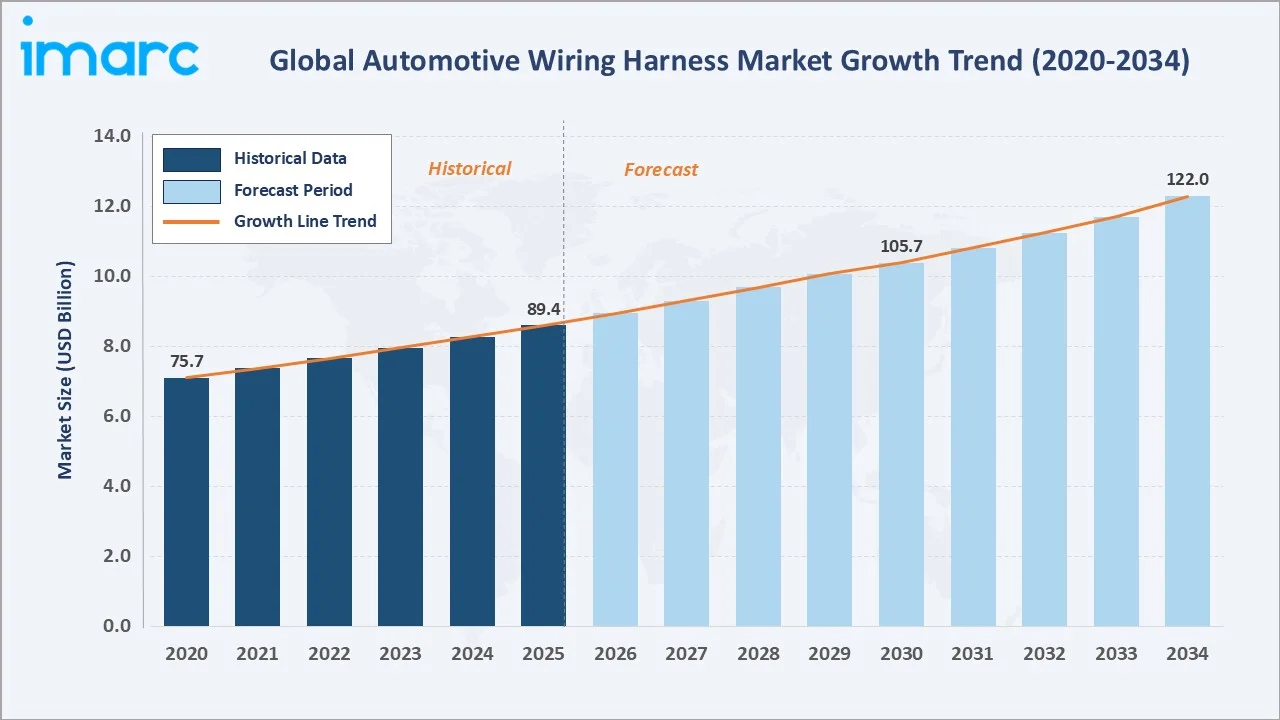

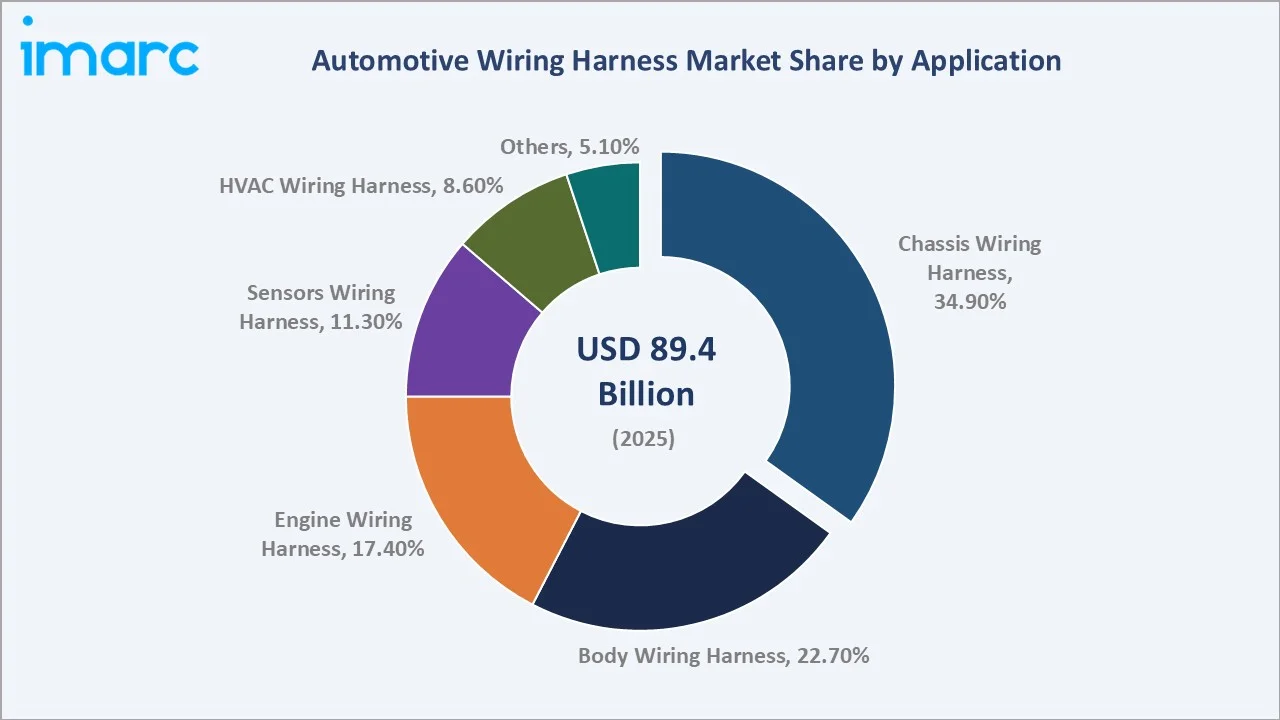

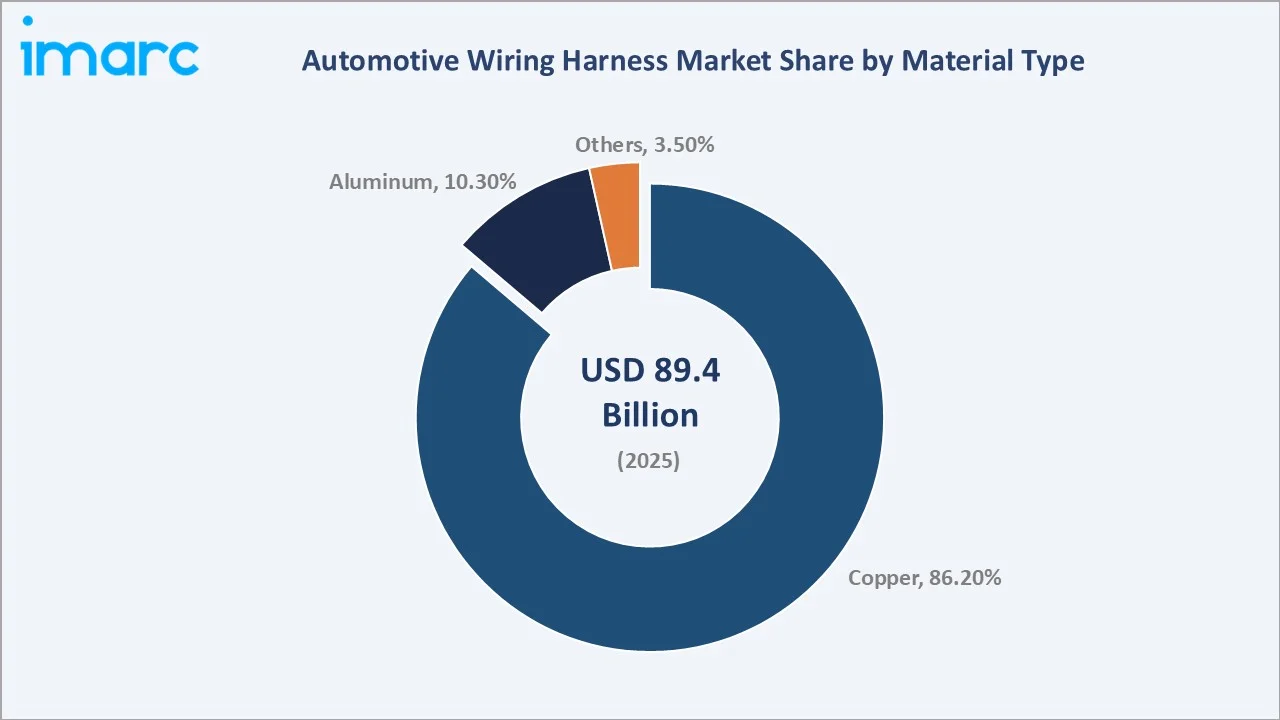

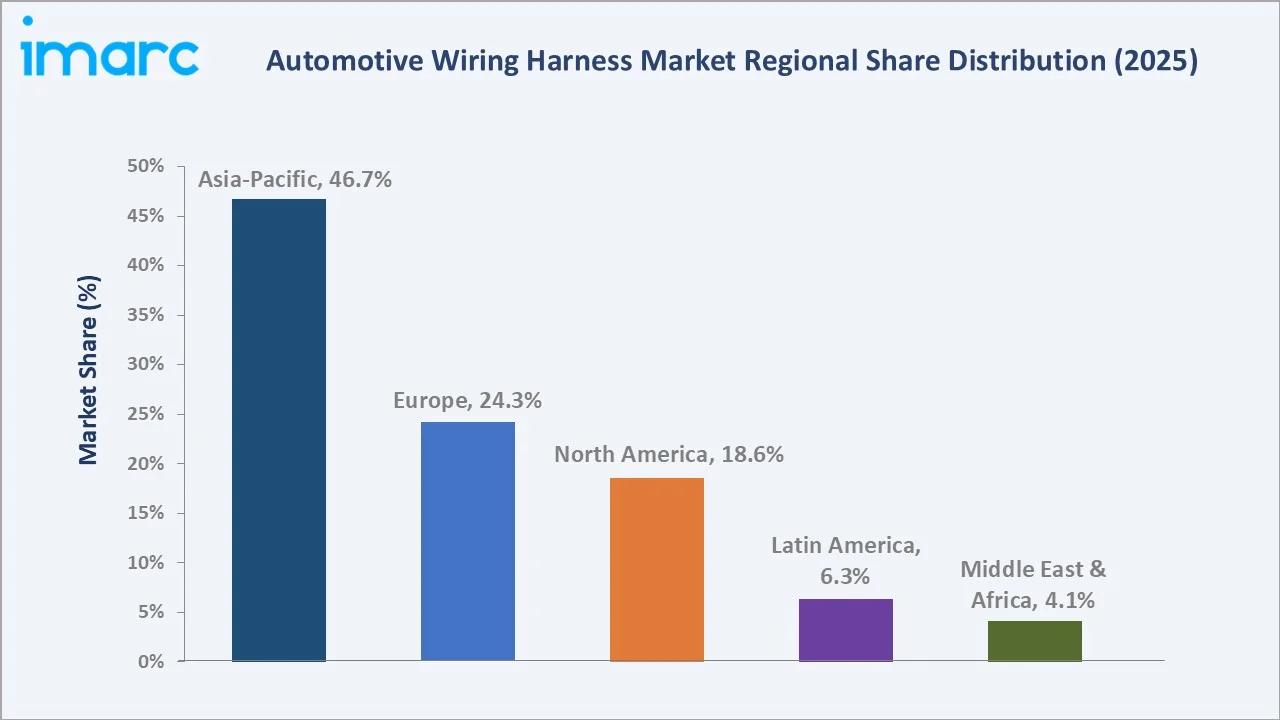

The global automotive wiring harness market size was valued at USD 89.4 Billion in 2025 and is projected to reach USD 122.0 Billion by 2034, exhibiting a CAGR of 3.4% during the forecast period 2026-2034. Surging electric vehicle (EV) production, increasing vehicle electrification, rising demand for advanced driver-assistance systems (ADAS), and proliferating automotive connectivity are key growth catalysts. Chassis Wiring Harness leads application segments at 34.9% in 2025, while Copper commands the material segment at 86.2%. Asia-Pacific accounts for 46.7% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 89.4 Billion |

|

Forecast Market Size (2034) |

USD 122.0 Billion |

|

CAGR (2026-2034) |

3.4% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia-Pacific (46.7% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific (CAGR ~4.8%) |

|

Leading Application |

Chassis Wiring Harness (34.9%, 2025) |

|

Leading Material |

Copper (86.2%, 2025) |

The global automotive wiring harness market growth trajectory from 2020 through 2034, contrasting historical expansion driven by hybrid vehicle proliferation against a sustained forecast curve powered by full EV adoption, 48V mild-hybrid architectures, and rising ADAS sensor integration.

To get more information on this market, Request Sample

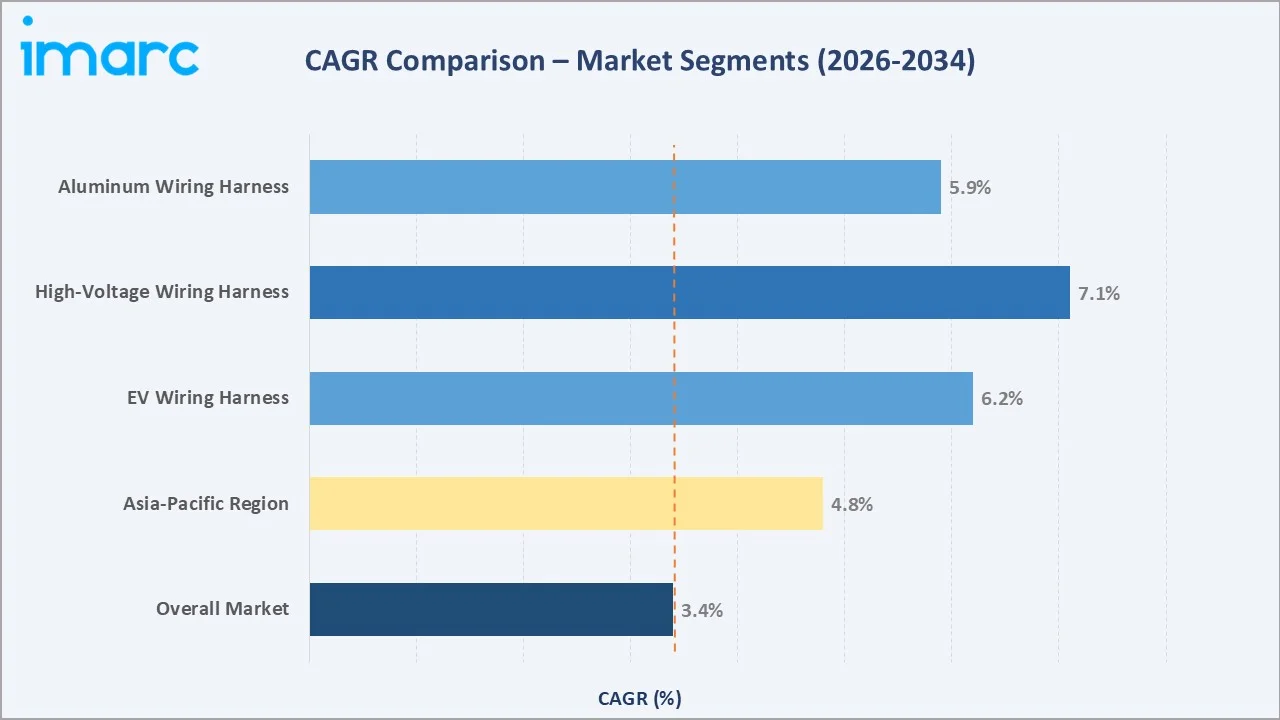

Segment-level CAGR comparisons highlighting EV high-voltage wiring harness and Asia-Pacific as the two fastest-growing sub-categories within the global automotive wiring harness industry analysis through 2034.

Executive Summary

The global automotive wiring harness market is undergoing a structural transformation driven by the convergence of vehicle electrification, digital cockpit expansion, and rising safety system mandates. Valued at USD 89.4 Billion in 2025, the market is forecast to reach USD 122.0 Billion by 2034 at a CAGR of 3.4%. The International Energy Agency reported global electric car sales exceeded 17 million units in 2024, a rise of over 25% year-on-year. Each battery-electric vehicle demands significantly more complex, high-voltage wiring architecture than its internal combustion engine (ICE) counterpart. Higher-voltage platforms at 400V and 800V require heavier gauge wiring, enhanced thermal management connectors, and multi-layered shielding.

Chassis Wiring Harness commands the dominant application share at 34.9% in 2025, driven by growing integration of chassis stability systems, electronic braking units, and advanced steering modules. The Body Wiring Harness segment holds 22.7% in 2025, supported by increasing power window, lighting, and comfort electronics. Engine Wiring Harness at 17.4% benefits from increasingly complex powertrain electronics in hybrid and full-electric platforms.

Asia-Pacific dominates with a 46.7% global revenue share in 2025, led by China's massive vehicle production exceeding 27 million units in 2024, alongside Japan's Tier-1 harness manufacturing ecosystem anchored by Yazaki and Sumitomo Electric. Europe holds 24.3% in 2025 and North America 18.6%, both characterized by premium vehicle content, stringent safety mandates, and growing EV platform transitions.

Key Market Insights

|

Insight |

Data |

|

Largest Application Segment |

Chassis Wiring Harness – 34.9% share (2025) |

|

Leading Material |

Copper – 86.2% share (2025) |

|

Leading Region |

Asia-Pacific – 46.7% revenue share (2025) |

|

Second Region |

Europe – 24.3% revenue share (2025) |

|

Top Companies |

Yazaki, Sumitomo Electric, Delphi Technologies, Leoni AG, Lear Corp., Aptiv |

|

Market Opportunity |

High-voltage EV harness segment growing at ~6.2% CAGR (2026–2034) |

Key Analytical Observations Supporting The Above Data:

- Chassis Wiring Harness's 34.9% dominance in 2025 reflects the industry-wide expansion of electronic stability control, ABS, and ADAS sensors mandated by regulatory bodies across major markets.

- Copper's 86.2% material dominance persists despite cost headwinds, as its superior electrical conductivity remains unmatched for high-current EV applications; LME copper prices averaging ~USD 9,000/tonne in 2024 elevate input cost pressure across the supply chain.

- Asia-Pacific's 46.7% global share in 2025 reflects China's dual role as the world's largest vehicle market and the most aggressive adopter of EV architectures demanding complex multi-circuit harness assemblies.

- Aluminum harness adoption is accelerating in the 10.3% material segment as OEMs pursue weight reduction targets; aluminum wiring is ~50% lighter than copper at equivalent current capacity, supporting EV range extension goals.

- High-voltage wiring harness for 800V EV platforms is the fastest-growing sub-category at ~7.1% CAGR through 2034, with Hyundai, Porsche, and Kia leading 800V platform deployments commercially.

Global Automotive Wiring Harness Market Overview

Automotive wiring harnesses are integrated electrical assemblies composed of cables, wires, connectors, terminals, and protective conduits that transmit electrical power and signals across vehicle subsystems. As the nervous system of modern vehicles, wiring harnesses interconnect the engine, chassis, body electronics, safety systems, infotainment, and powertrain management units into a unified electrical architecture.

Applications span passenger cars, light commercial vehicles, heavy trucks, buses, off-highway equipment, and increasingly battery-electric and hybrid-electric vehicle platforms where high-voltage power distribution harnesses represent a distinct and growing sub-market. Macroeconomic enablers include global vehicle production exceeding 92.5 million units in 2024, growing vehicle content per unit driven by electronics proliferation, and regulatory mandates for ADAS, emission controls, and occupant safety systems expanding wiring complexity across all vehicle categories.

Market Dynamics

To evaluate market opportunities, Request Sample

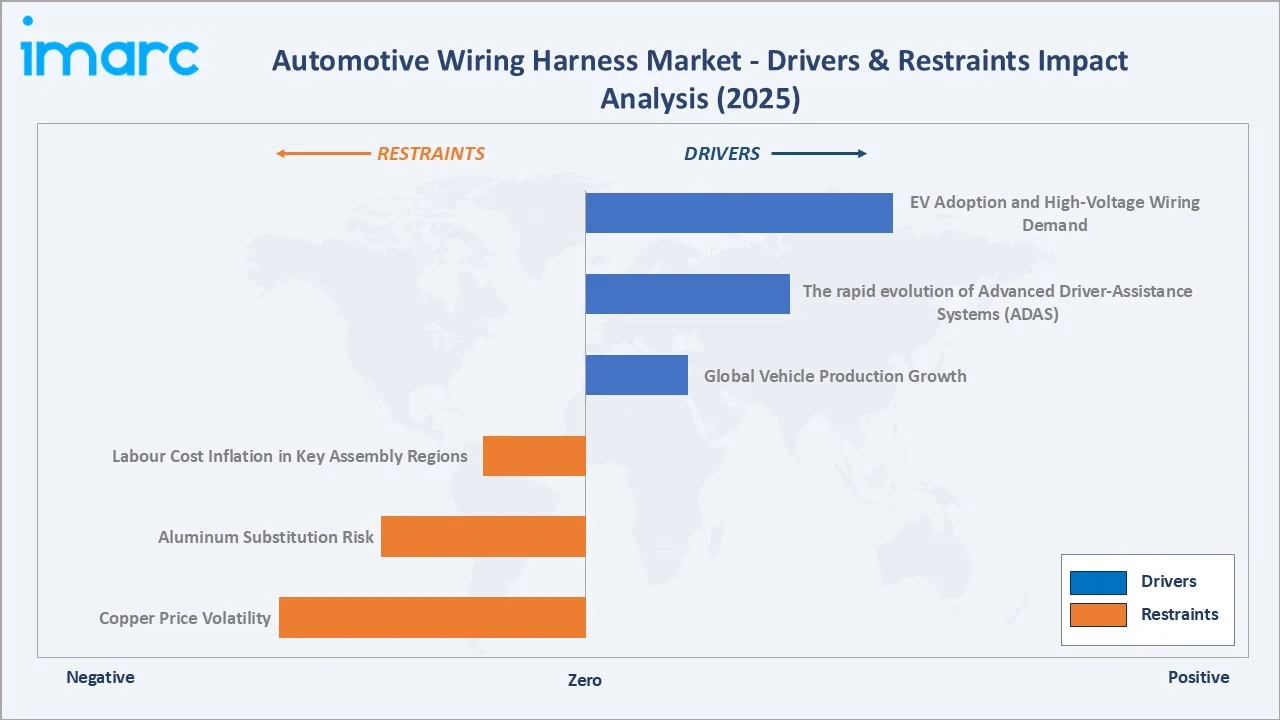

Market Drivers

- EV Adoption and High-Voltage Wiring Demand: Global electric car sales exceeded 17 million units in 2024 (IEA), driving structural uplift for high-voltage wiring harnesses. EV platforms operating at 400V–800V require specialised cables, thermal-resistant connectors, and electromagnetic shielding solutions significantly more complex and higher-value than conventional 12V ICE wiring.

- The rapid evolution of Advanced Driver-Assistance Systems (ADAS) including lane keeping, adaptive cruise control, automated emergency braking, and parking automation—is significantly increasing the complexity of in-vehicle electronics architecture. These systems rely on a network of cameras, radar, LiDAR, and ultrasonic sensors, all of which must be interconnected through high-speed, reliable wiring harnesses to enable real-time data processing and decision-making.

- Global Vehicle Production Growth: Emerging markets including India, ASEAN nations, and Brazil are accelerating vehicle production growth, with India's annual output projected to cross 6 million vehicles by 2030, all demanding locally assembled wiring harnesses.

Market Restraints

- Copper Price Volatility: Copper constitutes ~60–70% of wiring harness material cost. Copper prices averaging USD 9,000/tonne in 2024 and subject to sharp cyclical swings directly impact harness manufacturing margins. OEMs resist price pass-through, squeezing Tier-1 supplier profitability during commodity spikes.

- Aluminum Substitution Risk: Lightweight aluminum wiring harnesses are ~50% lighter than copper equivalents, a critical advantage for EV range extension. Growing aluminum adoption, particularly in body harness applications, could displace copper demand and compress copper harness market share below the current 86.2% by 2034.

- Labour Cost Inflation in Key Assembly Regions: Wiring harness assembly is highly labour-intensive. Rising wages in traditional low-cost assembly hubs such as Morocco, Mexico, and Eastern Europe are compressing the cost advantages that originally drove harness production to these regions.

Market Opportunities

- High-Voltage EV Harness Premium Segment: The transition to 800V EV platforms represents a ~2.5–3x value-per-vehicle uplift for harness suppliers compared to conventional 12V ICE wiring. Suppliers with certified 800V harness capabilities, including Aptiv and Lear, are positioned to capture premium content growth as OEMs scale high-voltage EV production.

- Lightweight and Optical Fibre Integration: Automotive Ethernet and MOST (Media Oriented Systems Transport) fibre-optic harness integration for infotainment and safety domain communication is expanding. Optical harnesses offer significant weight reduction and EMI immunity advantages, particularly relevant for autonomous vehicle architectures.

- Emerging Market Localisation Advantage: India, South-East Asia, and Africa represent structurally underpenetrated automotive manufacturing regions where local wiring harness assembly capabilities are being established in parallel with vehicle production growth.

Market Challenges

- Zone Architecture Disruption: Software-defined vehicle (SDV) zone architecture designs – where traditional ECU-per-function is replaced by fewer, more powerful zone controllers – could fundamentally reduce the number of discrete harness circuits per vehicle, potentially compressing harness value-per-vehicle in next-generation platforms.

- Counterfeit and Quality Risk in Cost-Sensitive Markets: Low-cost harness producers in emerging markets occasionally supply substandard wiring assemblies, creating vehicle safety risks and warranty liability. Tier-1 OEMs are implementing stricter supplier qualification and audit frameworks in response, adding compliance cost.

Emerging Market Trends

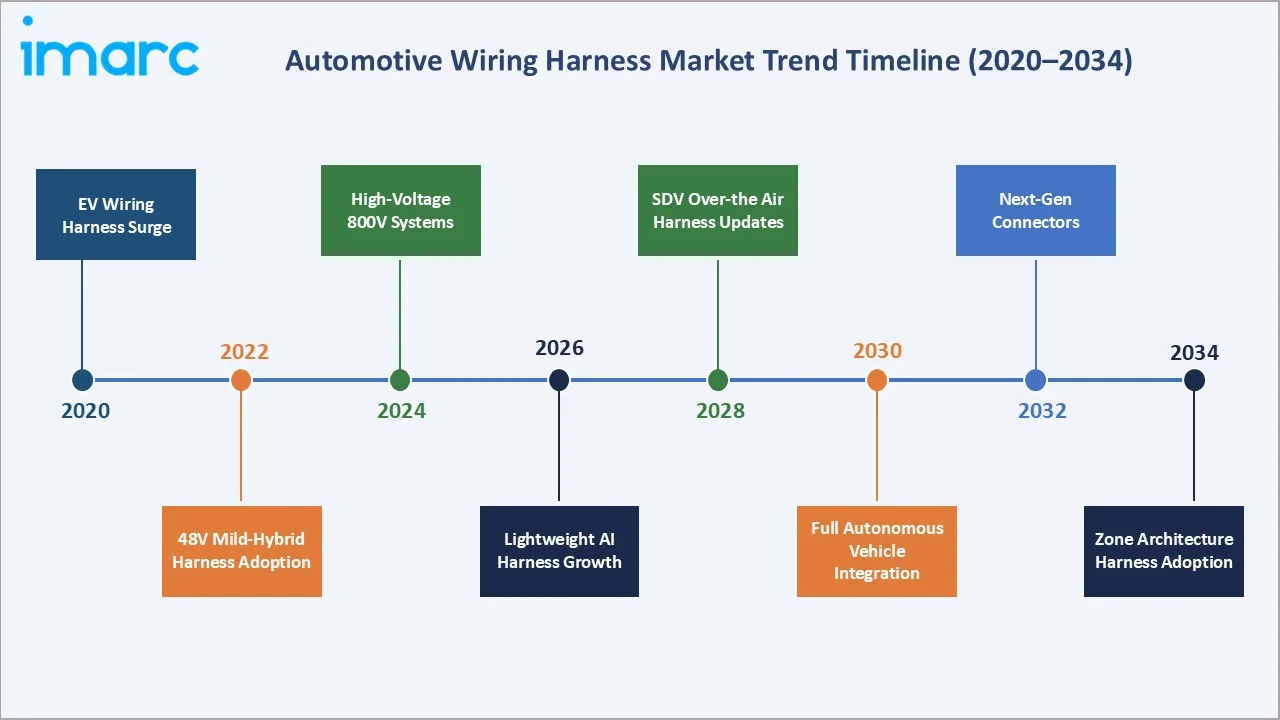

1. High-Voltage Wiring Harness for BEV and 800V Platforms

The proliferation of battery-electric vehicles operating at 400V and increasingly 800V architectures is creating a new premium sub-category within automotive wiring harness. 800V-capable harnesses require orange-coded high-voltage cabling, specialised connectors rated at 1,000V DC, and enhanced thermal management. Hyundai's IONIQ 5 and 6, Kia EV6, and Porsche Taycan deployed commercial 800V platforms by 2023–2024. More than 15 OEMs have announced 800V platforms scheduled by 2027.

2. Lightweight Aluminum Wiring Harness Expansion

Aluminum wiring harnesses, already adopted in body and chassis applications by BMW, Volkswagen, and Audi, are expanding into powertrain applications. Aluminum wiring is approximately 50% lighter than copper equivalents at the same current-carrying capacity. For a premium EV with ~4–5 kg of copper harness in body applications, aluminum substitution can reduce weight by ~2 kg, directly contributing to range extension. The aluminum harness segment is growing at ~5.9% CAGR through 2034.

3. Centralized / Zone Architecture Reducing Harness Complexity

Traditional vehicle architectures with 60–100+ ECUs are transitioning toward zone architectures with 3–5 high-performance zone controllers managing vehicle subsystems. Tesla's Model S/X/3/Y centralised compute architecture reduced wiring harness length by approximately 100 metres versus conventional architectures. Major OEMs including Volkswagen, BMW, and GM are transitioning to zone architectures by 2025–2028, which will structurally reduce circuit count but increase connector complexity per harness unit.

4. Automotive Ethernet and Optical Harness Integration

High-bandwidth in-vehicle communication for ADAS sensor fusion, OTA update pipelines, and digital cockpit data requires Automotive Ethernet (100BASE-T1, 1000BASE-T1) and MOST optical fibre integration. Harness suppliers are investing in new tooling and assembly processes for Ethernet and optical wiring, with Aptiv's SVA (Smart Vehicle Architecture) platform being the industry benchmark for next-generation data harness integration.

5. Sustainability and Recycled-Content Harness Manufacturing

OEM sustainability mandates are driving demand for recycled copper, bio-based wire insulation materials, and halogen-free flame-retardant jacket compounds. The EU End-of-Life Vehicles (ELV) Regulation revision and OEM net-zero 2040–2050 commitments are creating supply chain transformation requirements across the wiring harness ecosystem. Leoni AG announced fully halogen-free harness product lines targeting compliance with evolving EU regulations.

Industry Value Chain Analysis

The automotive wiring harness value chain spans six integrated stages from raw material extraction through end-consumer vehicle delivery. Each stage presents distinct competitive dynamics, margin profiles, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Raw Materials |

Freeport-McMoRan (copper), Rio Tinto, Norsk Hydro (aluminum), BASF (insulation polymers) |

|

Wire & Connector Manufacturing |

TE Connectivity, Molex, Amphenol, Leoni, Nexans (wire) |

|

Harness Assembly |

Yazaki Corporation, Sumitomo Electric, Aptiv, Lear Corporation, Furukawa Electric |

|

Quality Testing & Validation |

In-house OEM validation labs, Tier-1 supplier test centres, TÜV SÜD, Bureau Veritas |

|

OEM Vehicle Integration |

Toyota, Volkswagen Group, Ford, GM, Stellantis, Hyundai-Kia, BYD, NIO, SAIC |

|

End Users |

Passenger car owners, commercial fleet operators, EV fleet operators, autonomous vehicle platforms |

Harness assemblers occupy the critical value-adding position, transforming commodity wire and connectors into vehicle-specific, quality-certified assemblies. However, this position faces margin pressure from both raw material cost volatility upstream and OEM insourcing threats downstream, as some OEMs evaluate bringing harness design in-house for next-generation zone architecture platforms.

Technology Landscape in the Automotive Wiring Harness Industry

High-Voltage Cable and Connector Technology

800V EV platforms require high-voltage cables rated at 1,000V DC with silicone or cross-linked polyethylene (XLPE) insulation, offering superior thermal resistance above 150°C. Multi-layer electromagnetic shielding is essential to prevent EMI interference with adjacent ADAS sensors. Connector standards including IEC 62196 and SAE J1772 define the interface requirements for vehicle-side high-voltage harness termination.

Lightweight Materials Innovation

Aluminum conductor technology with advanced aluminium alloys (AA1350, AA8030 series) is enabling reliable crimp terminations that were previously a reliability weakness of aluminum wiring. Weight savings of 40–50% versus copper in body harness circuits are directly achievable. Bio-based and recycled polymer insulation materials are entering production validation, reducing lifecycle carbon footprint of harness assemblies.

Smart Connectivity and In-Vehicle Networking

Automotive Ethernet (IEEE 802.3bw, IEEE 802.3bp) and MOST (150/MOST150) optical fibre harnesses are expanding for high-bandwidth ADAS sensor data, camera image streaming, and OTA update pipelines. CAN FD (Flexible Data-rate) and LIN bus wiring remain the backbone of lower-speed body and powertrain control networks, with over 90% of production vehicles using CAN FD architectures by 2025.

Automation in Harness Assembly

Harness assembly remains one of the most labour-intensive processes in automotive manufacturing, as it relies heavily on manual operations such as routing, bundling, and connecting wires across complex vehicle architectures. Due to the high level of customization and limited scope for automation, hand-wiring stations continue to dominate the overall assembly process, making wiring harness production significantly dependent on human labor compared to other vehicle systems. Automation penetration is increasing via robotic wire cutting/stripping (Komax, Schleuniger), automated crimping, and increasingly AI-guided optical quality inspection systems.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Application |

Chassis Wiring Harness |

34.9% |

2025 |

|

Material Type |

Copper |

86.2% |

2025 |

|

Transmission Type |

Electrical Wiring |

81.5% |

2025 |

|

Vehicle Type |

Passenger Cars |

52.2% |

2025 |

| Category | General Wires | 40.0% | 2025 |

| Component | Wires | 42.2% | 2025 |

|

Region |

Asia Pacific |

46.7% |

2025 |

By Application

Chassis Wiring Harness commands a 34.9% majority share in 2025, reflecting the industry-wide integration of electronic stability control, ABS, and ADAS chassis sensors as standard equipment across mainstream and premium vehicle categories. The chassis segment benefits from regulatory mandates for autonomous emergency braking (AEB), which became mandatory in the EU for all new vehicle types from July 2022.

To access detailed market analysis, Request Sample

Body Wiring Harness at 22.7% serves the growing electronics content in comfort, convenience, and lighting systems. Engine Wiring Harness at 17.4% reflects the increasing complexity of hybrid and EV powertrain electronics. Sensors Wiring Harness at 11.3% represents the fastest-growing application sub-segment driven by ADAS sensor proliferation. HVAC Wiring Harness at 8.6% benefits from electrification of thermal management in EVs, where compressor and battery heating/cooling require dedicated high-current circuits. Others at 5.1% encompass suspension, steering, and miscellaneous body electronics.

By Material Type

Copper dominates at 86.2% in 2025, maintaining structural leadership due to its superior electrical conductivity (5.96×10⁷ S/m), ease of crimp termination, and well-established supply chain. Copper remains the preferred material for high-current EV powertrain circuits, battery management systems, and safety-critical chassis applications where maximum reliability is required.

Aluminum at 10.3% in 2025 is the fastest-growing material segment, gaining penetration in body harness, door harness, and floor harness applications where weight reduction benefits justify the engineering investment in improved termination techniques. The Others segment at 3.5% includes optical fibre, silver-plated conductors for high-frequency applications, and experimental composite materials in prototype evaluation.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia-Pacific |

46.7% |

China EV & NEV production, Japan/Korea Tier-1 harness ecosystem, India auto expansion, ASEAN growth |

|

Europe |

24.3% |

VW/BMW/Mercedes EV platforms, EU safety mandates, 2035 ICE ban driving EV harness demand |

|

North America |

18.6% |

Tesla SDV model, GM/Ford EV transition, ADAS mandates, nearshoring to Mexico |

|

Latin America |

6.3% |

Brazil/Mexico auto production growth, cost-competitive harness assembly exports |

|

Middle East & Africa |

4.1% |

GCC premium vehicle adoption, South Africa vehicle assembly, regional EV infrastructure investment |

Asia-Pacific commands a 46.7% global revenue share in 2025, the most dominant regional position reflecting China's dual role as the world's largest vehicle market and the most aggressive EV adopter. China produced 27.4 million passenger vehicles in 2024, a 5.2% year-on-year increase, with over 9 million NEVs produced domestically. Japan's Yazaki Corporation and Sumitomo Electric collectively supply approximately 40% of global automotive wiring harness volume, cementing Japan's technology leadership in harness manufacturing.

Europe, with 24.3% in 2025, is anchored by Germany's premium OEM ecosystem – Volkswagen Group, BMW Group, and Mercedes-Benz – all accelerating EV platform transitions. The EU's 2035 combustion engine ban is the defining regulatory driver for European harness market evolution, mandating full EV architecture adoption. North America at 18.6% is shaped by Tesla's centralized vehicle compute leadership and the aggressive EV transitions of GM (Ultium platform) and Ford (BlueOval), each requiring substantial high-voltage harness supplier development. Mexico serves as a critical low-cost harness assembly hub, with facilities from Yazaki, Sumitomo, Leoni, and Aptiv serving North American OEM supply chains.

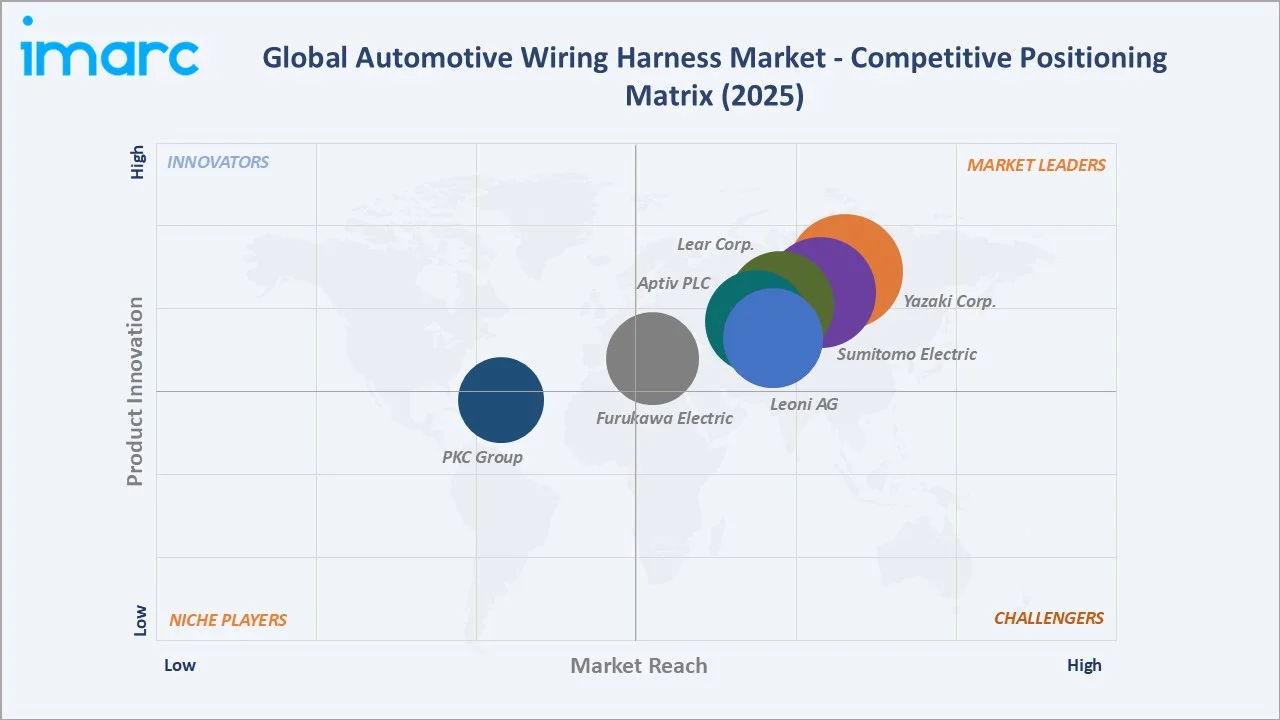

Competitive Landscape

|

Company Name |

Key Platform / Brand |

Market Position |

Core Strength |

|

Yazaki Corporation |

Yazaki Wiring Systems |

Leader |

Global harness volume, EV high-voltage expertise, OEM breadth |

|

Sumitomo Electric Industries |

Sumitomo Wiring Systems |

Leader |

Japan Tier-1, optical fibre, copper alloys, Toyota ecosystem |

|

Aptiv PLC |

Aptiv SVA Platform |

Leader |

Smart Vehicle Architecture, SDV-ready harness, data cables |

|

Lear Corporation |

Lear E-Systems |

Leader |

EV high-voltage, battery connectors, software integration |

|

Leoni AG |

LEONI Wiring Systems |

Challenger |

European OEM specialisation, halogen-free, EV cables |

|

Furukawa Electric |

Furukawa Automotive |

Challenger |

Japan / ASEAN harness, optical fibre, aluminium wiring |

|

PKC Group |

PKC Wiring Harnesses |

Emerging |

Commercial vehicle specialty, Northern Europe/Americas |

The automotive wiring harness competitive landscape is characterised by a small number of Japanese-headquartered Tier-1 global leaders commanding the highest OEM relationship volume, alongside European specialists targeting premium and commercial vehicle segments. Yazaki and Sumitomo collectively held dominant share in global harness production volume, giving them scale advantages in raw material procurement and assembly automation investment.

Key Company Profiles

Yazaki Corporation

Yazaki Corporation is the world's largest automotive wiring harness manufacturer, headquartered in Tokyo, Japan, with over 290,000 employees across 45 countries and manufacturing facilities across Asia, the Americas, Europe, and Africa.

- Product & Platform Portfolio: Conventional 12V wiring harnesses, high-voltage EV/HEV wiring harnesses (rated to 1,000V DC), charging cables (AC and DC fast charging), junction boxes, wire protection products, and automotive connectors.

- Recent Developments: In 2024, Yazaki announced expansion of its high-voltage harness manufacturing capacity in Mexico to serve North American EV platform ramp-up by GM and Ford. Yazaki also entered a strategic partnership with a leading Chinese NEV OEM for BEV platform harness supply, reinforcing its position in the world's largest EV market.

- Strategic Focus: Yazaki's strategy centres on scaling high-voltage EV harness production capacity globally, investing in aluminium wiring harness capabilities, and expanding in China's domestic NEV supply chain through local manufacturing partnerships.

Sumitomo Electric Industries

Sumitomo Electric Industries is Japan's second-largest wiring harness manufacturer and a global Tier-1 automotive supplier with approximately 280,000 employees worldwide. The company operates through its Sumitomo Wiring Systems (SWS) subsidiary.

- Product & Platform Portfolio: Automotive wiring harnesses (all vehicle types), optical fibre cables for MOST networking, wire and cable products, rubber and resin components, and automotive connectors and terminals.

- Recent Developments: Sumitomo Electric commenced volume production of 800V-compatible high-voltage harness systems for leading South Korean and European EV OEMs in 2024. The company invested over JPY 30 billion in EV-related product development during 2023–2024.

- Strategic Focus: Sumitomo prioritises high-value optical and high-voltage harness segments, leveraging its proprietary copper alloy wire technology for reliable aluminium crimping, and expanding its wiring system footprint in ASEAN emerging auto markets.

Aptiv PLC

Aptiv PLC, headquartered in Dublin, Ireland, is a global technology company focused on the development and manufacturing of smart vehicle architecture platforms that combine electrical distribution, data networking, and high-voltage power systems.

- Product & Platform Portfolio: Smart Vehicle Architecture (SVA), electrical distribution systems, high-voltage power management, data connectivity solutions, and software-defined vehicle enablement platforms.

- Recent Developments: In January 2024, Aptiv announced its acquisition of Wind River, a software company specialising in intelligent systems software, for USD 4.3 Billion, marking a significant strategic move toward software-defined vehicle platforms. Aptiv also secured multi-year EV harness contracts with three major European OEMs through 2028.

- Strategic Focus: Aptiv positions itself as the only Tier-1 harness supplier with deep software integration capabilities, targeting the convergence of physical harness architecture with digital vehicle platforms in SDV-era vehicles, a differentiation that justifies premium pricing above pure hardware competitors.

Market Concentration Analysis

The global automotive wiring harness market exhibits high concentration among the top global Tier-1 harness assemblers. Yazaki and Sumitomo Electric collectively account for approximately 40–45% of global harness production volume in 2025, with the top five players – Yazaki, Sumitomo, Aptiv, Lear, and Leoni – representing approximately 65–70% of total market revenue.

The market is experiencing a bifurcated structural dynamic. At the premium EV and ADAS harness tier, consolidation is accelerating: 800V EV harness programmes require multi-hundred-million-dollar capital investments in new tooling, certified testing facilities, and high-voltage assembly processes that only the largest Tier-1s can sustain. This concentration of investment is effectively raising barriers to entry for mid-size harness manufacturers in the highest-growth sub-segments.

Simultaneously, the Chinese domestic EV market is generating fragmentation. Chinese OEMs' strong preference for domestic suppliers, and the technical competitiveness of harness manufacturers including Kintetsu Electric Wire and Suzhou Hengfeng, is creating competitive pressure on international Tier-1s in the world's largest automotive market. By 2028, domestic Chinese harness suppliers are projected to capture 35–40% of Chinese domestic demand versus approximately 55–60% held by Japanese Tier-1 local operations today.

Investment & Growth Opportunities

Fastest-Growing Segments

High-voltage EV wiring harness is the highest-growth sub-segment at approximately 7.1% CAGR through 2034, driven by the transition to 800V EV platforms and the proliferation of DC fast charging (DCFC) infrastructure requiring vehicle-side ultra-high-current connectors. Sensor wiring harnesses for ADAS and autonomous vehicles are growing at approximately 6.5% CAGR, driven by camera, radar, LiDAR, and ultrasonic sensor integration mandates across global regulatory frameworks.

Emerging Market Expansion

India represents the highest-potential emerging market for harness manufacturing investment, with government production-linked incentive (PLI) schemes attracting OEM investment and creating demand for local Tier-1 harness supply chain development. India's domestic passenger vehicle market is projected to reach 6 million units annually by 2030. ASEAN automotive markets, particularly Thailand and Indonesia, are establishing themselves as EV production hubs for Japanese and Chinese OEMs, creating greenfield harness assembly investment opportunities.

Venture & Private Investment Trends

Aptiv's USD 4.3 Billion acquisition of Wind River underscores the strategic value investors place on the convergence of harness hardware with vehicle software platforms. Private equity interest in mid-tier harness assemblers is growing as consolidation pressure creates acquisition targets. Venture capital investment in harness assembly automation start-ups, particularly robotic routing and AI-guided quality inspection technologies, has grown materially since 2022 as harness manufacturers seek to reduce labour cost exposure in rising-wage assembly regions.

Future Market Outlook (2026-2034)

The global automotive wiring harness market forecast projects steady value expansion from USD 89.4 Billion in 2025 to USD 122.0 Billion by 2034 at a CAGR of 3.4%, a USD 32.6 Billion absolute value addition underpinned by EV platform content upgrades, sensor network expansion, and structural shifts in vehicle architecture complexity across all vehicle categories.

Three technology trajectories are most likely to reshape the market through 2034. First, 800V EV platform normalisation – the transition from current 400V mainstream EV architecture to 800V as the standard architecture for mid-range EVs by 2028–2030 – will systematically upgrade the harness specification and value content of the majority of global EV production. Second, zone architecture adoption by major OEMs reducing harness circuit count but increasing connector and data harness complexity, reshaping harness BOM economics. Third, optical fibre and Automotive Ethernet data harness integration expanding from premium to mainstream vehicle segments by 2030.

By 2034, the automotive wiring harness industry is projected to complete its transition from conventional 12V copper-centric assemblies to a mixed-architecture market encompassing high-voltage EV power harnesses, data networking harnesses (Ethernet, MOST), lightweight aluminium body harnesses, and software-defined zone controller interconnects – each representing distinct competitive sub-markets with differentiated technology and supplier requirements.

Research Methodology

Primary Research

Primary research encompassed structured interviews with automotive electronics industry stakeholders including procurement directors at Tier-1 wiring harness suppliers, OEM vehicle engineering leads, connector and terminal manufacturers, raw materials suppliers, and institutional investors in the automotive supply chain. Primary insights validated market sizing, segmentation share estimates, technology adoption timelines, and competitive positioning assessments across all five major regions covered in this report.

Secondary Research

Secondary sources include IEA Global EV Outlook, IHS Markit (S&P Global Mobility) vehicle production data, LME copper and aluminium commodity price databases, European Automobile Manufacturers' Association (ACEA) production statistics, JAMA (Japan Automobile Manufacturers Association) output data, SAE International standards publications, company annual reports, and trade publications including Automotive News, Ward's AutoWorld, and Automotive World.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating global vehicle production trajectories by powertrain type, harness content-per-vehicle escalation rates by vehicle category, regional manufacturing cost dynamics, and raw material price scenario modelling. Scenario analysis (base, optimistic, and conservative cases) was performed to account for macroeconomic uncertainty and EV adoption pace variability.

Automotive Wiring Harness Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Applications Covered | Body Wiring Harness, Engine Wiring Harness, Chassis Wiring Harness, HVAC Wiring Harness, Sensors Wiring Harness, Others |

| Material Types Covered | Copper, Aluminum, Others |

| Transmission Types Covered | Data Transmission, Electrical Wiring |

| Vehicle Types Covered | Two Wheelers, Passenger Cars, Commercial Vehicles |

| Categories Covered | General Wires, Heat Resistant Wires, Shielded Wires, Tubed Wires |

| Components Covered | Connectors, Wires, Terminals, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Yazaki Corporation, Sumitomo Electric Industries, Aptiv PLC, Lear Corporation, Leoni AG, Furukawa Electric, PKC Group, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the automotive wiring harness market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global automotive wiring harness market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's Five Forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the automotive wiring harness industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Automotive Wiring Harness Market Report

The global automotive wiring harness market was valued at USD 89.4 Billion in 2025, driven by rising vehicle electrification, ADAS proliferation, and growing electronics content per vehicle across all major markets.

The market is projected to reach USD 122.0 Billion by 2034, growing at a CAGR of 3.4% during 2026-2034 driven by EV platform high-voltage harness demand, ADAS sensor networks, and global vehicle production growth.

Chassis wiring harness leads with a 34.9% share in 2025, driven by electronic stability control, ABS, and ADAS sensor mandatory fitment across mainstream and premium vehicle categories globally.

Copper leads with 86.2% share in 2025due to superior electrical conductivity, reliable crimp termination, and established supply chain. Aluminium at 10.3% is the fastest-growing material, gaining share in body and chassis harness weight-reduction applications.

Asia-Pacific leads with 46.7% share in 2025, driven by China's 27.4-million-unit vehicle production in 2024, Japan's Tier-1 harness manufacturing leadership, South Korea's EV platform growth, and ASEAN auto sector expansion.

Key drivers include EV/HEV high-voltage harness demand (17M EV sales globally in 2024), ADAS sensor wiring expansion, rising ECUs per vehicle exceeding 100 in premium models, and global vehicle production growth in emerging markets.

Sensors Wiring Harness is the fastest-growing application, expanding with ADAS proliferation at approximately 6.5% CAGR through 2034, driven by mandatory fitment of AEB, lane departure warning, and parking assistance across global regulatory frameworks.

Leading companies include Yazaki Corporation, Sumitomo Electric Industries, Aptiv PLC, Lear Corporation, Leoni AG, Furukawa Electric, and PKC Group.

BEV platforms require 400V–800V high-voltage harnesses valued at 2.5–3x per-vehicle premium versus conventional 12V ICE wiring. EV high-voltage harness is the highest-value-growth sub-segment, growing at approximately 7.1% CAGR through 2034.

Zone architecture replaces 60–100 distributed ECUs with 3–5 zone controllers, reducing harness circuit count but increasing zone controller interconnect complexity. Tesla's implementation reduced harness length by ~100 metres, setting a benchmark for next-generation SDV platforms launching from 2025–2028.

Aluminum harness holds 10.3% material share in 2025and is growing at ~5.9% CAGR through 2034. BMW, Volkswagen, and Audi are leading adopters in body and chassis applications. Improved aluminium alloy crimp reliability is accelerating broader OEM qualification through 2026–2028.

Asia-Pacific commands 46.7% of global automotive wiring harness revenue in 2025, supported by China's massive EV production scale, Japan's Yazaki and Sumitomo leadership, and ASEAN emerging market vehicle production growth across Thailand, Indonesia, and Vietnam.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)