Autonomous Tractors Market Size, Share, Trends and Forecast by Component, Power Output, Crop Type, Application, and Region, 2026-2034

Autonomous Tractors Market Size, Share, Trends & Forecast (2026-2034)

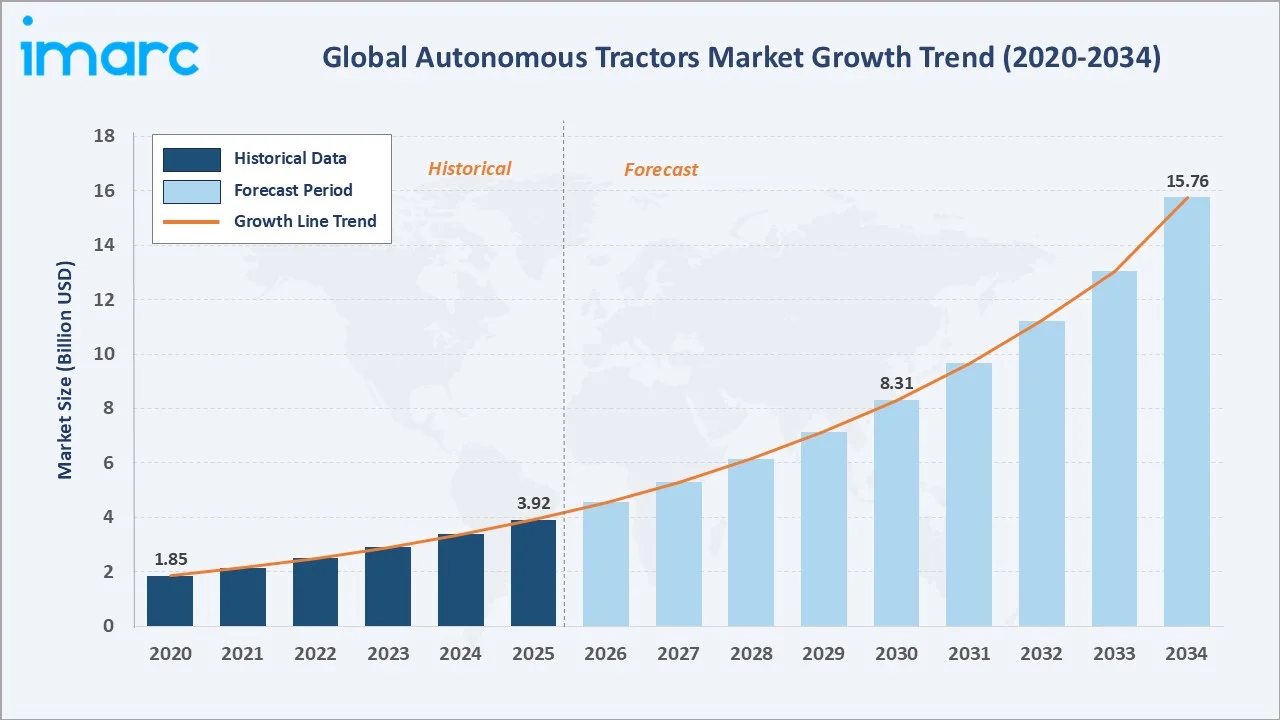

The autonomous tractors market was valued at USD 3.92 Billion in 2025 and is projected to reach USD 15.76 Billion by 2034, exhibiting a CAGR of 16.22% during 2026-2034. Accelerating farm labor shortages are a primary catalyst. Increasing adoption of precision agriculture technologies and rising demand for operational efficiency are further supporting market expansion globally.

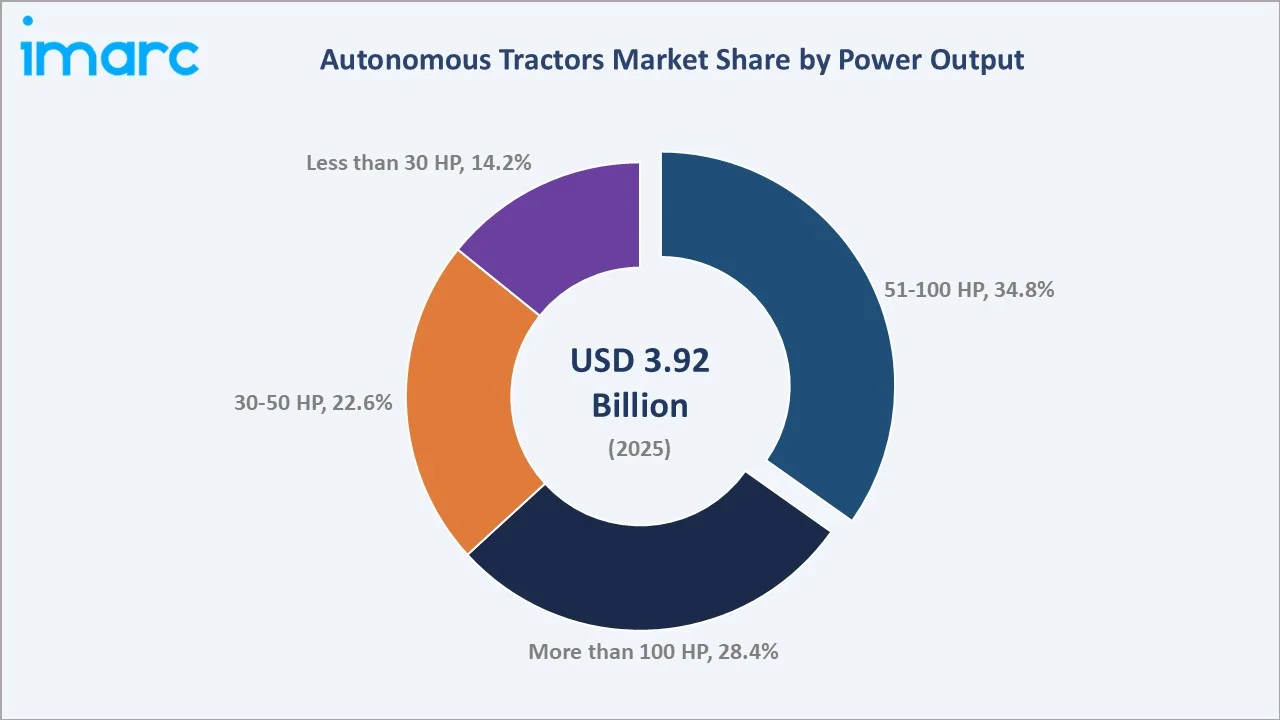

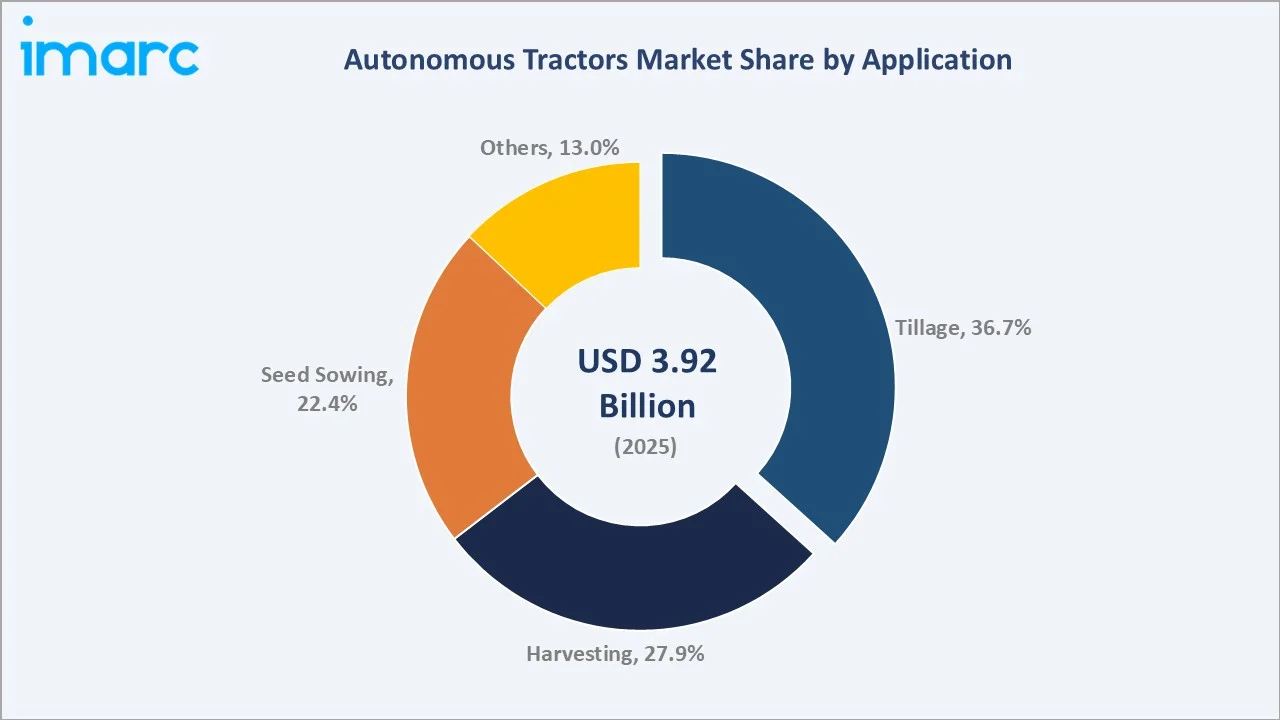

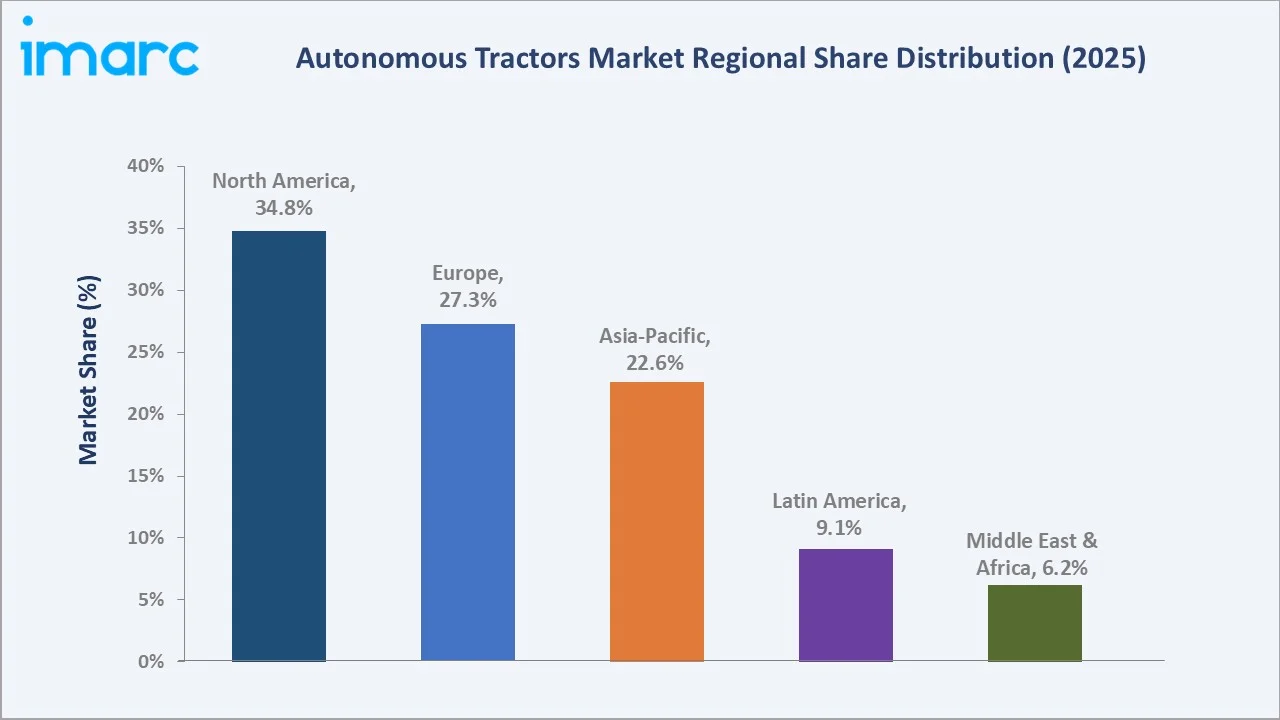

51-100 HP commands the power output segment at 34.8%, tillage leads the application landscape at 36.7%, and North America holds the top regional position at 34.8% in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 3.92 Billion |

|

Forecast Market Size (2034) |

USD 15.76 Billion |

|

CAGR (2026-2034) |

16.22% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (34.8%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (18.4% CAGR, 2026-2034) |

|

Leading Power Output |

51-100 HP (34.8%, 2025) |

|

Leading Application |

Tillage (36.7%, 2025) |

The autonomous tractors market expanded from USD 1.85 Billion in 2020 to USD 3.92 Billion in 2025, driven by rising farm labor shortages, declining sensor and computing costs, and accelerating precision agriculture adoption across major crop-producing economies. Anchored at USD 8.31 Billion in 2030, the market is forecast to reach USD 15.76 Billion by 2034, representing a CAGR of 16.22% during 2026-2034.

To get more information on this market, Request Sample

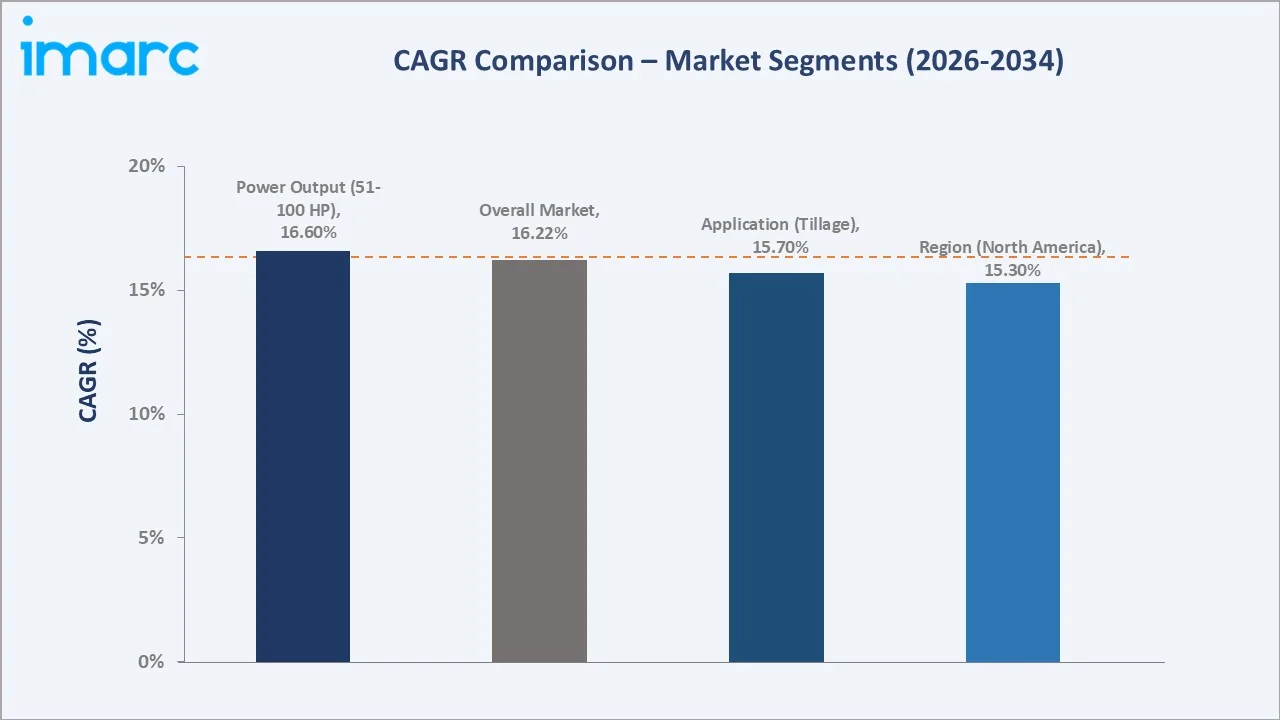

CAGR trajectories across power output and application sub-segments show the more than 100 HP and seed sowing categories expanding faster than the overall 16.22% market CAGR, driven by large-scale precision farming adoption and increasing demand for automated planting operations.

Executive Summary

The autonomous tractors market expanded from USD 1.85 Billion in 2020 to USD 3.92 Billion in 2025, demonstrating consistent double-digit growth anchored by chronic agricultural labor shortfalls, falling sensor and computing costs, and a wave of precision farming mandates across major crop-producing economies. Autonomous tractors have transitioned from experimental platforms to commercially deployed workhorses, with leading original equipment manufacturers (OEMs) offering production-ready systems equipped with real-time kinematic (RTK) GNSS guidance, lidar-based obstacle detection, and cloud-connected fleet management.

51-100 HP commands the power output segment at 34.8% in 2025, reflecting high demand from medium-scale farms across North America and Europe. Tillage leads the application segment at 36.7%, given its repetitive, high-acreage nature that is ideally suited to autonomous field operations. North America leads regional contributions at 34.8%, propelled by large consolidated farm structures, strong dealer-channel penetration, and technology-forward growers. In May 2026, U.S. Sugar, in collaboration with Autonomous Solutions, Inc. (ASI) and Everglades Equipment Group, introduced the largest commercial deployment of autonomous tractors in the American sugar industry, operating a fleet of driverless John Deere tractors across its farmland in South Florida.

Key Market Insights

|

Insight |

Data |

|

Leading Power Output |

51-100 HP – 34.8% share (2025) |

|

Second Largest Power Output |

More than 100 HP – 28.4% share (2025) |

|

Leading Application |

Tillage – 36.7% share (2025) |

|

Second Largest Application |

Harvesting – 27.9% share (2025) |

|

Leading Region |

North America – 34.8% share (2025) |

|

Fastest Growing Region |

Asia-Pacific – 18.4% CAGR (2026-2034) |

|

Top Companies |

Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, Autonomous Solutions, Inc. |

Key Analytical Observations Expanding on the Data Above:

- The 51-100 HP power output segment commands a 34.8% share in 2025, driven by its suitability for medium-scale corn, soybean, and wheat operations – the segment where return-on-investment payback periods for autonomous systems are most attractive to farm operators.

- The more than 100 HP category captures 28.4% in 2025, supported by large-acreage commercial farms across the United States and Canada where high-horsepower tractors are standard for primary tillage and row-crop operations.

- Tillage dominates application at 36.7% in 2025 due to its repetitive, straight-line nature that maximizes the efficiency gains from autonomous systems, making tillage the primary entry-point application for most first-time autonomous tractor buyers.

- Harvesting at 27.9% is gaining traction as labor shortages during peak harvest seasons and the need for continuous field operations are accelerating the adoption of autonomous tractors and combine support systems across large-scale farming operations.

- North America leads regional share at 34.8%, reflecting a mature precision agriculture ecosystem, strong OEM dealer networks, and favorable financing structures that have lowered barriers to autonomous tractor adoption among commercial growers. As per IMARC Group, the North America precision agriculture market size was valued at USD 5.18 Billion in 2025.

Global Autonomous Tractors Market Overview

Autonomous tractors are self-propelled agricultural machines equipped with GNSS-based positioning, machine vision, AI, and telematics systems that enable fully driverless or remotely supervised field operations. Typical systems integrate RTK-GNSS receivers providing sub-centimeter accuracy, lidar and camera arrays for obstacle detection, inertial measurement units for terrain compensation, and cloud-based fleet management platforms for remote monitoring and mission planning.

The global ecosystem encompasses upstream raw material and component suppliers, sensor and semiconductor manufacturers, software and AI algorithm developers, OEM assemblers, dealer and distribution networks, precision agriculture service providers, and final farm operators. Macroeconomic influences shaping the market include rising agricultural wage pressures, government programs promoting food security and digital farming, declining hardware costs for advanced sensors and edge computing, and the accelerating consolidation of farm holdings into larger, economically viable units suited for autonomous equipment deployment.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

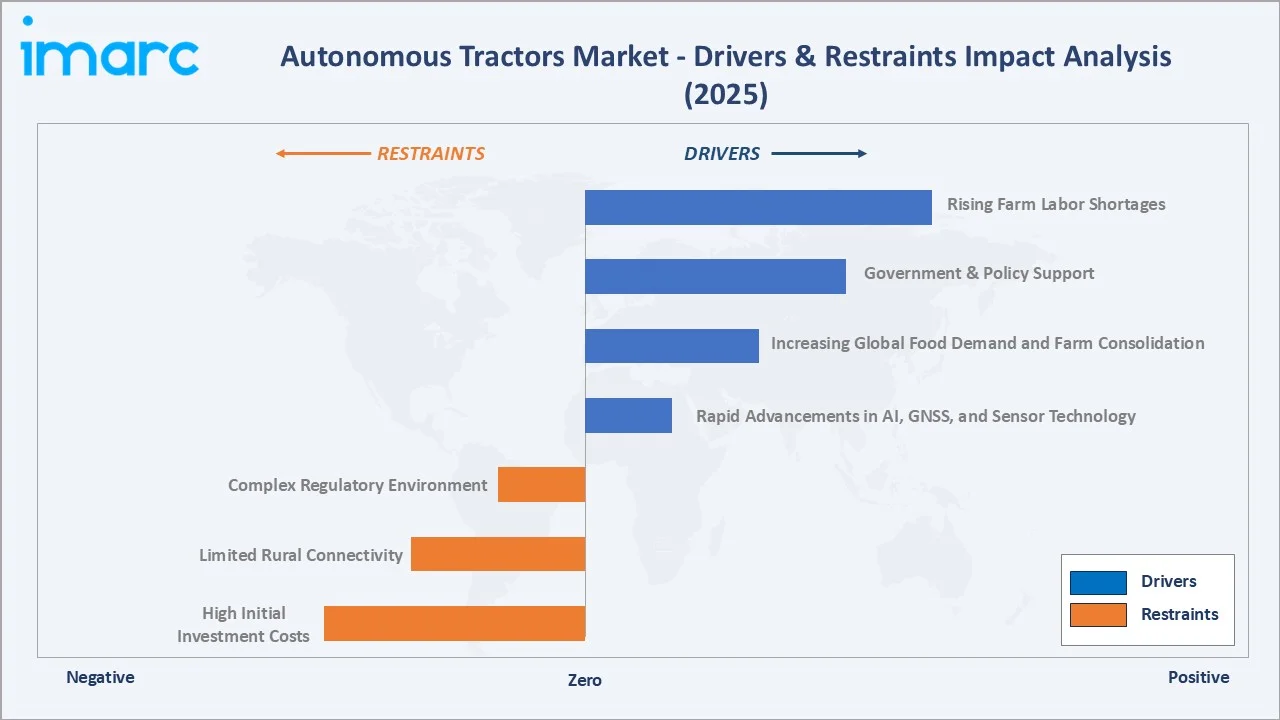

- Rising Farm Labor Shortages: Agricultural economies across North America, Europe, and Asia-Pacific are facing persistent farm labor deficits. The growing difficulty in recruiting seasonal workers for tasks, such as tillage, seeding, and harvesting, is compelling farm operators to invest in autonomous equipment that can operate around the clock with minimal human oversight, directly driving tractor automation adoption.

- Government Support and Precision Agriculture Policies: National programs promoting digital farming, food security, and rural modernization are providing financial incentives, such as subsidies, tax credits, and low-interest loans, to farmers purchasing precision agriculture equipment.

- Increasing Global Food Demand and Farm Consolidation: Growing global population is intensifying pressure on agricultural productivity. The United Nations' 2024 World Population Prospects report estimates that the worldwide population will reach 9.7 Billion by 2050 and will peak at 10.3 Billion in 2085. Farm consolidation trends have produced larger average field sizes in the United States, Brazil, and Australia, where economies of scale make autonomous systems financially compelling, creating strong pull demand for high-capacity autonomous tractors.

- Rapid Advancements in AI, GNSS, and Sensor Technology: The maturation of RTK-GNSS positioning (achieving 2 cm accuracy), real-time AI-powered path planning, and affordable lidar and camera systems have dramatically reduced technical barriers to commercially viable autonomous tractor deployment, enabling safe, reliable driverless field operations at competitive cost points.

Market Restraints

- High Initial Investment Costs: Fully configured autonomous tractor systems carry a considerably higher cost than conventional farm equipment, creating a major affordability challenge for small and medium-sized family farms with limited financing access and narrow operating margins.

- Limited Rural Connectivity Infrastructure: Reliable high-speed internet and mobile network coverage, which are essential for real-time telematics, over-the-air software updates, and remote fleet supervision, remain inadequate across large portions of agricultural land in developing economies and remote rural areas of developed nations, restricting the operational effectiveness of connected autonomous tractor platforms.

- Complex and Evolving Regulatory Environment: Autonomous agricultural equipment operates in an inconsistently regulated space, with varying national and regional requirements for machine safety standards, liability frameworks, and operational licensing. The lack of harmonized international regulations increases compliance costs for OEMs and creates market entry uncertainty, slowing adoption in several key emerging markets.

Market Opportunities

- Expansion into Emerging Agricultural Economies: Countries in Southeast Asia, Sub-Saharan Africa, and Latin America represent large untapped markets where rising rural wages, growing farm scale, and government modernization programs are creating first-mover opportunities for affordable, entry-level autonomous tractor platforms tailored to smaller plot sizes and diverse crop types.

- Autonomous-as-a-Service and Leasing Models: Emerging equipment-as-a-service platforms allow farmers to access autonomous tractor capabilities through pay-per-use or monthly subscription models, eliminating upfront capital barriers and accelerating adoption among cost-sensitive mid-tier growers.

- Integration with Precision Agriculture Ecosystems: Autonomous tractors that natively connect with variable-rate application controllers, soil sensor networks, drone-captured field maps, and farm management information systems offer substantial value-added differentiation, creating strong cross-sell opportunities across the precision farming technology stack.

Market Challenges

- Cybersecurity and Data Privacy Risks: Cloud-connected autonomous tractors generate and transmit vast volumes of farm operational data, including field geometry, crop performance metrics, and yield estimates. Inadequate cybersecurity measures expose farmers to data theft and machine interference risks, raising concerns that slow adoption among privacy-conscious farm operators in key markets.

- Skills Gap and Farmer Training Requirements: Effective operation of autonomous tractor platforms requires training in digital interfaces, fleet management software, and basic troubleshooting of guidance and sensing systems. The existing agricultural workforce in many regions lacks the digital literacy needed to maximize the benefits of autonomous equipment, creating an adoption gap that requires significant dealer-supported training investment.

Emerging Market Trends

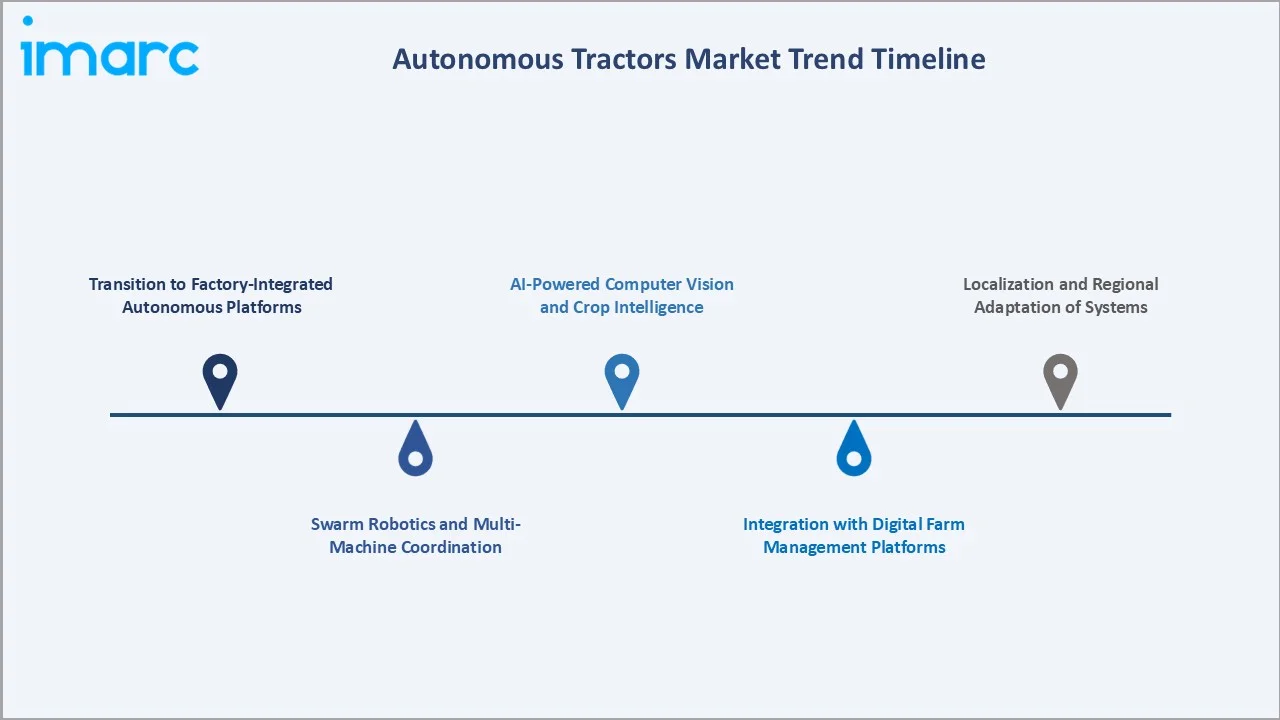

1. Transition From Retrofit Solutions to Factory-Integrated Autonomous Platforms

Early autonomous tractor deployments relied heavily on aftermarket retrofit kits – GNSS receivers, auto-steer systems, and vision modules bolted onto existing equipment. The market is now shifting toward factory-built autonomous platforms where guidance hardware, sensors, and AI software are deeply integrated with drivetrain and implement control systems by OEMs, improving reliability and enabling tighter implement coordination for precision field operations.

2. Emergence of Swarm Robotics and Multi-Machine Coordination

Advances in autonomous coordination algorithms are enabling fleets of smaller autonomous tractors to operate simultaneously across a single field, dividing tasks, such as seeding, spraying, and harvesting in parallel. Swarm approaches reduce soil compaction by distributing field passes among lighter machines and allow continuous operations across shifts without operator fatigue constraints, providing a compelling productivity case for large-scale grain producers.

3. AI-Powered Computer Vision and Crop Intelligence

Next-generation autonomous tractors are increasingly equipped with deep learning-based computer vision systems that enable real-time crop health assessment, weed identification for spot-treatment applications, and soil condition estimation from camera and spectral imagery. These intelligence layers transform the tractor from a power unit into a mobile agronomic data-collection platform.

4. Integration of Autonomous Tractors with Digital Farm Management Platforms

Autonomous tractor telematics are being deeply integrated with cloud-based farm management information systems, variable-rate controllers, and remote sensing data pipelines. This integration enables dynamic, real-time mission adjustments based on satellite soil moisture maps, drone-captured field imagery, and weather forecasting models, creating a connected precision agriculture ecosystem where field operations are continuously optimized across the entire crop production cycle.

5. Localization and Regional Adaptation of Autonomous Systems

Leading OEMs and technology providers are investing in region-specific adaptations of autonomous tractor platforms to address differences in crop types, field geometries, soil conditions, and regulatory frameworks across key markets. Localization efforts include developing guidance systems optimized for fragmented paddy fields in Asia-Pacific, enabling interoperability with local implements in Latin America, and building compliance documentation for evolving European Union machinery safety regulations.

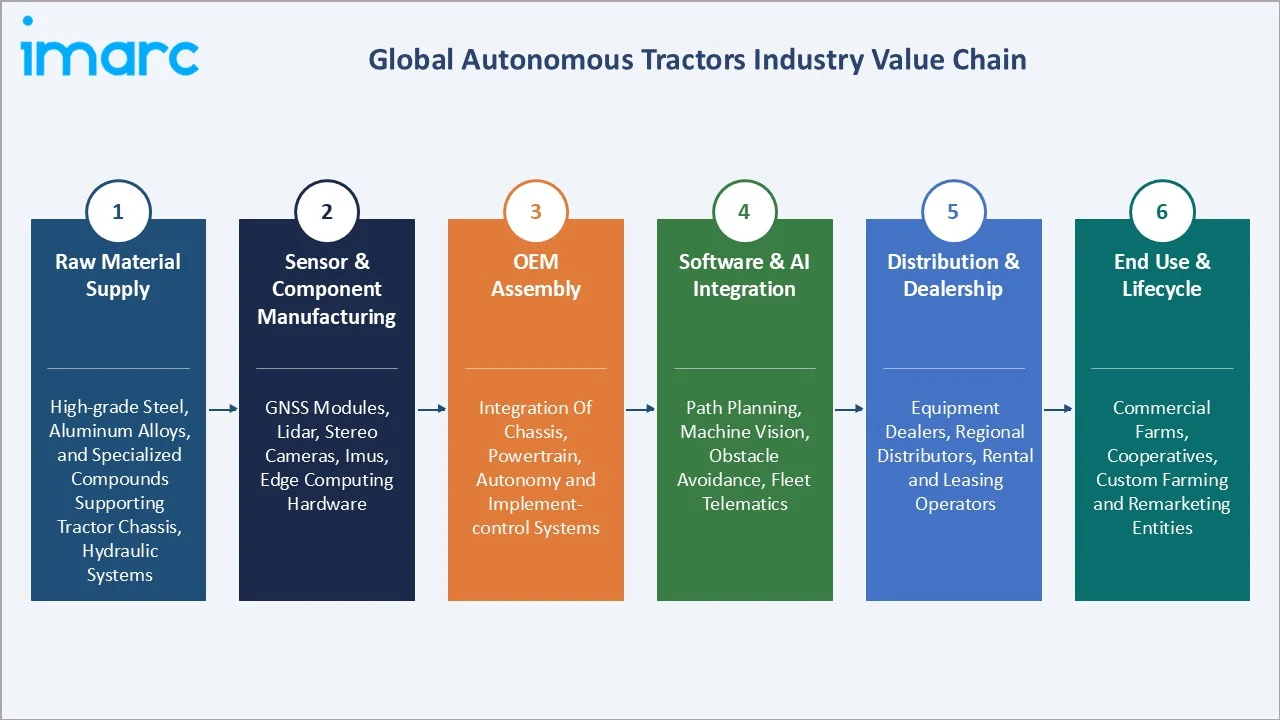

Industry Value Chain Analysis

The autonomous tractors value chain spans six interconnected stages from raw material sourcing through end-of-life and lifecycle services. OEM assembly and software or AI integration stages capture the highest value-add, while dealer-channel relationships and after-sales service generate significant downstream competitive differentiation. Vertically integrated players that control both hardware manufacturing and software platforms secure superior margin profiles and stronger farmer lock-in compared with hardware-only manufacturers.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of high-grade steel, aluminum alloys, and specialized compounds supporting tractor chassis, hydraulic systems, and drivetrain component manufacturing |

|

Sensor & Component Manufacturing |

Companies specializing in GNSS modules, lidar sensors, stereo cameras, inertial measurement units, and edge computing hardware for embedded agricultural applications |

|

OEM Assembly |

Large-scale agricultural equipment manufacturers integrating chassis, powertrain, autonomy systems, and implement-control modules into complete autonomous tractor platforms |

|

Software & AI Integration |

Technology developers providing autonomous path planning, machine vision, obstacle avoidance, fleet telematics, and cloud-based remote management applications |

|

Distribution & Dealership |

Agricultural equipment dealers, regional distributors, precision farming specialty retailers, and rental or leasing service operators |

|

End Use & Lifecycle |

Commercial farms, agricultural cooperatives, custom farming service providers, government-supported farm programs, and equipment remarketing and recycling entities |

Technology Landscape in the Autonomous Tractors Industry

GNSS and Precision Positioning

RTK-GNSS technology provides the spatial foundation for autonomous tractor operations, delivering sub-centimeter positioning accuracy that enables precise row-by-row field coverage with minimal overlap or missed passes. Multi-constellation receivers leveraging GPS, GLONASS, and BeiDou signals ensure consistent signal availability under varying field conditions. Emerging PPP-RTK technology is extending centimeter-level accuracy to regions without dense correction networks.

AI and Machine Learning (ML)

AI and ML algorithms power path planning, dynamic obstacle recognition, implement depth and pressure control, and predictive maintenance systems. Convolutional neural networks trained on large agricultural datasets enable real-time identification of field boundaries, obstacles, and crop rows across diverse conditions, while reinforcement learning approaches are being explored to enable autonomous tractors to optimize field-operation parameters based on in-season performance feedback.

Sensor Fusion and Perception Systems

Modern autonomous tractors deploy multi-sensor perception stacks that fuse data from lidar, stereo cameras, ultrasonic sensors, and radar units to build a 360-degree real-time map of the operating environment. Sensor fusion architectures using Kalman filtering and deep learning-based object classification enable reliable operation in challenging conditions including dust, fog, and low-light environments that historically limited autonomous field operations.

Telematics, Connectivity, and Over-the-Air Updates

Cloud-connected telematics platforms enable remote mission planning, real-time fleet monitoring, predictive maintenance alerts, and over-the-air software updates. The expanding rollout of 5G networks in rural areas is improving the reliability and bandwidth of field connectivity. Edge computing modules reduce dependency on continuous cloud connectivity by enabling core autonomy functions to operate locally, maintaining safe field performance even in low-signal environments.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Component |

GPS |

43.7% |

2025 |

|

Power Output |

51-100 HP |

34.8% |

2025 |

|

Crop Type |

🔒 |

🔒 |

2025 |

|

Application |

Tillage |

36.7% |

2025 |

|

Region |

North America |

34.8% |

2025 |

By Power Output

51-100 HP commands a 34.8% majority share in 2025, driven by strong demand from medium-scale grain and row-crop farms across North America and Europe. Tractors in this range balance field productivity with manageable acquisition costs, making them the most commercially attractive entry point for autonomous system integration among owner-operated farms.

To access detailed market analysis, Request Sample

The more than 100 HP segment holds 28.4% in 2025, supported by large commercial grain farms and custom farming operators in the United States, Canada, Brazil, and Australia that deploy heavy-duty equipment for primary soil tillage and large-scale harvesting support.

By Application

Tillage dominates the application landscape at 36.7% in 2025, reflecting its suitability for full autonomy. Repetitive, straight-line primary and secondary tillage passes across large fields deliver immediate, measurable fuel and labor cost savings, making tillage the primary entry-point application for autonomous tractor adoption across most markets.

Harvesting captures 27.9% of application share in 2025 and is growing rapidly as AI-based crop detection and yield mapping enable increasingly precise autonomous harvesting support. Rising pressure to reduce harvest-time labor dependency and improve operational efficiency is further accelerating adoption across large-scale farming operations.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

34.8% |

Large-scale farm consolidation, strong dealer networks, favorable precision agriculture financing programs, and high technology adoption rates among commercial grain producers |

|

Europe |

27.3% |

Robust government support for digital farming, strict labor regulations driving automation, mature precision agriculture infrastructure, and favorable EU Common Agricultural Policy incentives |

|

Asia-Pacific |

22.6% |

Rapid rural modernization programs, government subsidies for smart farming, rising rural labor costs, and growing adoption of precision agriculture across Japan, South Korea, and Australia |

|

Latin America |

9.1% |

Expanding large-scale agribusiness operations, growing soybean and corn farm consolidation in Brazil and Argentina, and rising investment in agricultural technology infrastructure |

|

Middle East and Africa |

6.2% |

Food security initiatives, government-backed agricultural modernization programs, and increasing foreign investment in commercial farming operations across the Gulf and East Africa |

North America leads the autonomous tractors market at 34.8% in 2025, sustained by a dense precision farming adoption base, well-established OEM dealer infrastructure, and a commercial farming community highly receptive to labor-saving technologies. Large average field sizes across the United States corn belt and Canadian prairies create ideal operating conditions for fully autonomous tractor systems.

Europe holds 27.3%, with Germany, France, and the United Kingdom serving as primary adoption hubs supported by subsidized precision agriculture programs and stringent labor cost dynamics. Strong regulatory emphasis on sustainable farming practices and digital agriculture integration is further encouraging autonomous tractor deployment across the region.

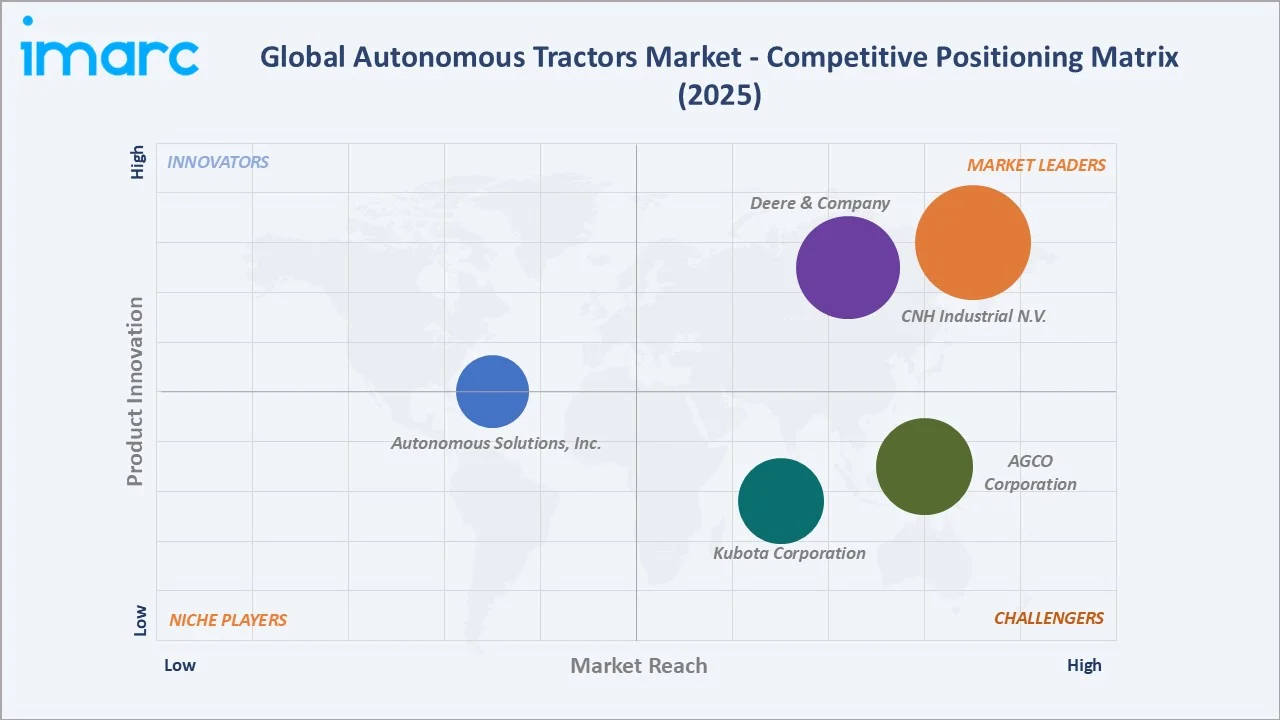

Competitive Landscape

The autonomous tractors market is moderately fragmented, with a small number of global full-line OEMs commanding significant market presence through established dealer relationships, proprietary software ecosystems, and strong brand loyalty. Regional specialists and technology-first companies serve niche application segments and provide autonomy platforms through OEM partnerships. Competitive differentiation is increasingly driven by software capabilities, data platform integration, and the breadth of autonomous implements supported.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Deere & Company |

John Deere |

Leader |

Broad autonomous product portfolio, proprietary operations center platform, and global dealer network |

|

CNH Industrial N.V. |

Case IH |

Leader |

Strong OEM integration across tractor and harvesting lines with precision farming connectivity |

|

AGCO Corporation |

Fendt |

Challenger |

Premium technology-first approach with advanced driver assistance and autonomy-ready platforms |

|

Kubota Corporation |

Kubota |

Challenger |

Strong compact and mid-range autonomous tractor offerings focused on Asia-Pacific and specialty crops |

|

Autonomous Solutions, Inc. |

Mobius |

Emerging |

Specialized autonomous retrofit systems and robotic field vehicle platforms for commercial agriculture |

Key players include Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and Autonomous Solutions, Inc., among others.

Key Company Profiles

Deere & Company

Deere & Company is a globally recognized leader in the design and manufacture of agricultural equipment, with a well-established commercial position in autonomous farming technology. The company has consistently invested in precision guidance systems, AI-powered field operations, and autonomous machinery platforms, maintaining a leadership role in commercially deployed autonomous tractor solutions across large-scale grain and row-crop farming operations worldwide.

- Product Portfolio: Autonomous and semi-autonomous tractor platforms for large-scale field operations; precision guidance and GPS-based auto-steer systems; AI-powered implement control and variable-rate application technology; cloud-based fleet management and remote operations monitoring platforms.

- Recent Developments: At CES 2025, Deere & Company unveiled the next-generation autonomous 9RX tractor equipped with a second-generation autonomy kit featuring 16 cameras in a 360-degree array, enabling fully driverless tillage operations.

- Strategic Focus: Continued expansion of autonomous capabilities across its tractor and implement lineup; deepening integration between field equipment and cloud-based farm management platforms; and growing the addressable base of farms capable of adopting autonomous operations.

CNH Industrial N.V.

CNH Industrial N.V. is a global equipment manufacturer operating multiple agricultural machinery brands. The company is actively developing precision agriculture and autonomous tractor capabilities across its agricultural brand portfolio, supported by dedicated precision technology and positioning technology subsidiaries.

- Product Portfolio: Autonomous and semi-autonomous capable agricultural tractors across multiple horsepower ranges; precision guidance and auto-steer systems for field-level accuracy; dedicated precision agriculture and autonomous systems brands; farm connectivity and fleet monitoring platforms for remote management.

- Recent Developments: The company has continued to advance its autonomous and precision technology portfolio across its agricultural brands, introducing enhanced connectivity platforms and automation-capable tractor models designed for large-scale farming operations in key global markets.

- Strategic Focus: Building commercially viable autonomous capabilities across multiple agricultural brands; leveraging dedicated precision and autonomy technology subsidiaries to accelerate deployment; and expanding connected farm platforms across its global dealer network.

AGCO Corporation

AGCO Corporation is a global agricultural equipment manufacturer serving farmers across several countries through a portfolio of established equipment brands. The company offers autonomous and precision farming solutions with a focus on integrating advanced technology across its tractor and implement portfolio and advancing a full-farm autonomy roadmap.

- Product Portfolio: High-performance tractor platforms with autonomous guidance capability; autonomous retrofit technology for tillage and field operations; precision farming and fleet management platforms; AI-powered variable-rate application and field intelligence systems.

- Recent Developments: The company has continued making progress toward its full-farm autonomy roadmap, expanding its autonomous retrofit portfolio and demonstrating integrated autonomous field operation capabilities across its tractor and precision farming brands at major industry events.

- Strategic Focus: Advancing full-farm autonomy across its equipment portfolio; expanding autonomous retrofit solutions for both owned and third-party equipment; and integrating precision farming technology with autonomous operation management platforms.

Market Concentration Analysis

The autonomous tractors market is moderately concentrated, with the top five companies – Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and Autonomous Solutions, Inc. – estimated to collectively hold approximately 60-70% of global autonomous tractor and enabling-technology revenue in 2025.

Barriers to entry include the lengthy certification process for functional safety compliance, the extensive field-data requirements needed to develop reliable AI-based obstacle detection systems, and the time-intensive effort required to establish strong dealer and farm network relationships. These factors strengthen the market position of established companies with significant capital resources and long-standing expertise in precision agriculture technologies.

Consolidation is accelerating through OEM acquisitions of autonomy software startups, technology licensing partnerships between hardware OEMs and AI platform providers, and strategic alliances between tractor manufacturers and precision agriculture software companies. The competitive landscape is expected to tighten further as fully autonomous systems transition from early-adopter novelties to standard new-equipment offerings.

Investment & Growth Opportunities

Fastest-Growing Segments

Seed sowing at 22.4% is expanding faster than the overall 16.22% market CAGR through 2034, driven by the precision variable-rate planting requirements of modern hybrid and specialty crop production. The more than 100 HP power output segment at 28.4% is growing rapidly as large commercial grain farms accelerate autonomous fleet deployment for primary tillage and cover crop operations.

Emerging Markets

Asia-Pacific, growing at a CAGR of 18.4%, is the fastest-growing region, with the highest incremental volume opportunity concentrated in Australia, Japan, South Korea, China, and India. Brazil, Argentina, India, and Southeast Asian agricultural markets represent the largest untapped opportunity frontiers. Rising rural wages, growing farm consolidation, expanding mobile and satellite connectivity, and government smart farming subsidies are collectively creating favorable conditions for cost-optimized autonomous tractor platforms targeting mid-size family farm operations.

Venture & Investment Trends

Private and institutional investment is concentrated in AI and ML autonomy stack companies, multi-machine coordination and swarm robotics startups, advanced GNSS correction network providers, and agricultural data and farm management software platforms. Equipment leasing and autonomous-as-a-service business models are attracting fintech and infrastructure investment as farmers increasingly seek capex-light access to autonomous technology.

Future Market Outlook (2026-2034)

The autonomous tractors market is forecast to expand from USD 3.92 Billion in 2025 to USD 15.76 Billion by 2034, growing at a CAGR of 16.22% and adding approximately USD 11.84 Billion in incremental annual market value over the forecast period. The market will reach a pivotal scale of USD 8.31 Billion by 2030, by which point autonomous tractor capabilities are expected to be standard options on new full-size equipment from all major OEMs.

Four structural forces will shape the market through 2034: continued sensor cost deflation; the expansion of rural 5G connectivity enabling richer real-time telemetry; the maturation of AI-based predictive field analytics enabling proactive autonomous operation optimization; and the accelerating transition toward autonomous-as-a-service models that democratize access for cost-constrained mid-size and small commercial farms.

By 2034, autonomous tractors are expected to account for a meaningful share of new equipment sales across leading agricultural economies, with fully driverless primary tillage, seeding, and crop support operations becoming standard practice for large commercial grain producers. The technology will continue spreading into specialty crop, horticultural, and paddy field applications as compact swarm robotic systems progressively capture share in markets where large single-machine platforms have historically been impractical.

Research Methodology

Primary Research

Primary research included structured interviews with senior product managers and engineers at leading autonomous tractor OEMs, precision agriculture technology developers, agricultural dealer network executives, farm cooperative managers, and commercial farming operations across North America, Europe, and Asia-Pacific. These conversations provided direct validation of market sizing, segment share distributions, technology adoption timelines, and competitive positioning of key market participants.

Secondary Research

Secondary sources included annual reports, investor presentations, and press releases from listed agricultural equipment manufacturers; research publications from the Food and Agriculture Organization of the United Nations (FAO); national agriculture census data from the United States Department of Agriculture (USDA); precision agriculture association reports from the Association of Equipment Manufacturers (AEM); technical journals on agricultural robotics; and government policy documents from the European Union Common Agricultural Policy framework.

Forecasting Models

Market forecasts used a combination of top-down and bottom-up modeling approaches, incorporating tractor unit shipment data by horsepower class, autonomous system attachment rates by market, average selling price trends for guidance and autonomy hardware, and technology adoption diffusion curves calibrated against historical precision agriculture adoption patterns. Scenario analysis was conducted to assess the sensitivity of market projections to key variables including rural connectivity rollout speed, government subsidy continuity, and autonomous hardware cost deflation trajectories.

Autonomous Tractors Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Components Covered | LiDAR, Radar, GPS, Camera/Vision Systems, Ultrasonic Sensors, Hand-Held Devices |

| Power Outputs Covered | Less than 30 HP, 30-50 HP, 51-100 HP, More than 100HP |

| Crop Types Covered | Fruits and Vegetables, Cereals and Grains, Oilseeds and Pulses |

| Applications Covered | Tillage, Seed Sowing, Harvesting, Others |

| Segment Coverage | Component, Power Output, Crop Type, Application, Region |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, Autonomous Solutions, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the autonomous tractors market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global autonomous tractors market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the autonomous tractors industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Autonomous Tractors Market Report

The autonomous tractors market was valued at USD 3.92 Billion in 2025, driven by rising farm labor shortages, falling sensor costs, and expanding precision agriculture adoption globally.

The market is projected to grow at a CAGR of 16.22% from 2026 to 2034, reaching USD 15.76 Billion, supported by AI advancements, government incentives, and farm consolidation trends.

51-100 HP leads at 34.8% in 2025, favored by medium-scale grain farms in North America and Europe for its balanced productivity and cost-effective autonomous integration.

Tillage dominates at 36.7% in 2025, as repetitive straight-line field passes maximize the efficiency and ROI benefits of autonomous guidance systems for farm operators.

North America commands 34.8% in 2025, driven by large consolidated farms, established dealer networks, and high precision agriculture adoption rates among commercial grain producers.

Leading players include Deere & Company, CNH Industrial N.V., AGCO Corporation, Kubota Corporation, and Autonomous Solutions, Inc., among others.

Key drivers include chronic agricultural labor shortages, sub-centimeter RTK-GNSS accuracy, AI-powered obstacle detection, falling sensor costs, and supportive precision farming policy frameworks.

High initial investment costs, limited rural connectivity in developing regions, complex safety certification requirements, and farmer digital literacy gaps remain primary adoption constraints.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)