Autosamplers Market Size, Share, Trends and Forecast by Product, End Use, and Region, 2026-2034

Autosamplers Market Size, Share, Trends & Forecast (2026-2034)

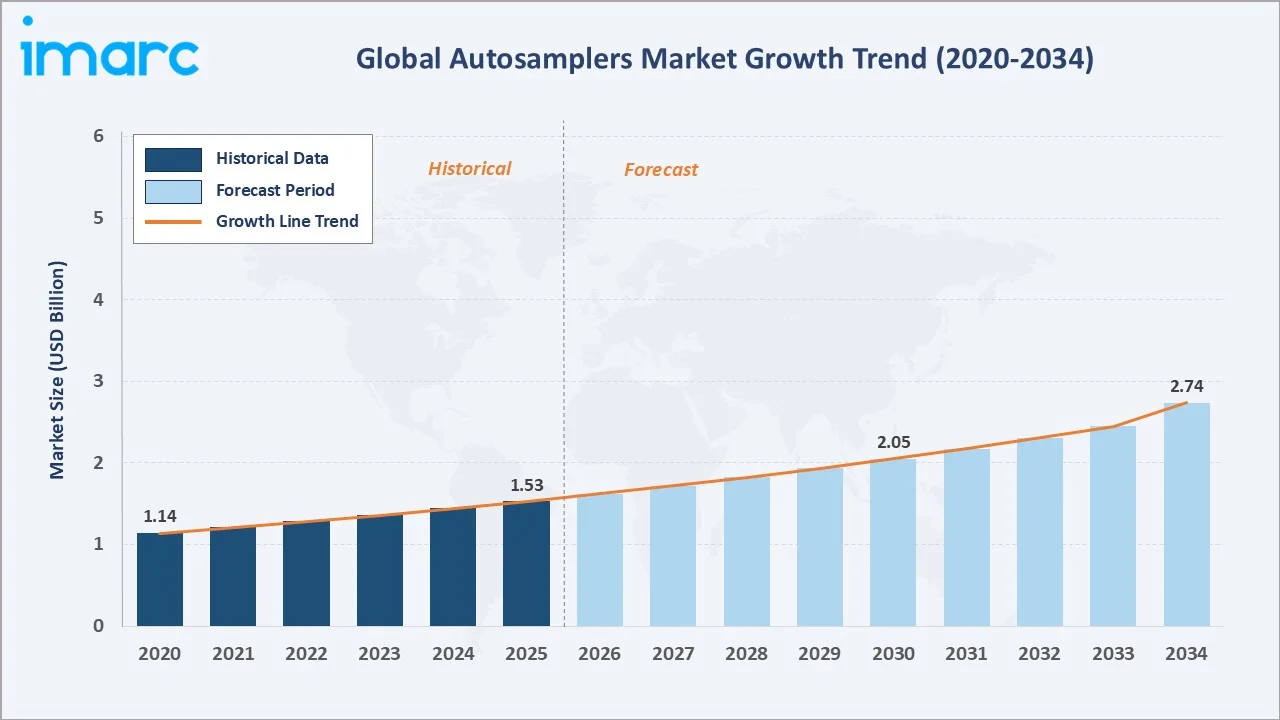

The autosamplers market was valued at USD 1.53 Billion in 2025 and is projected to reach USD 2.74 Billion by 2034, exhibiting a CAGR of 6.05% during 2026-2034. Rising pharmaceutical research and development (R&D) activity, stringent regulatory testing mandates, and rapid expansion of chromatography-based quality control workflows are the primary drivers shaping market growth. Under the Scheme for Promotion of Research and Innovation in Pharma MedTech (PRIP), as of November 2025, a total of 111 research projects were sanctioned, 46 research articles were released, and 6 patents were submitted through the Centres of Excellence in India.

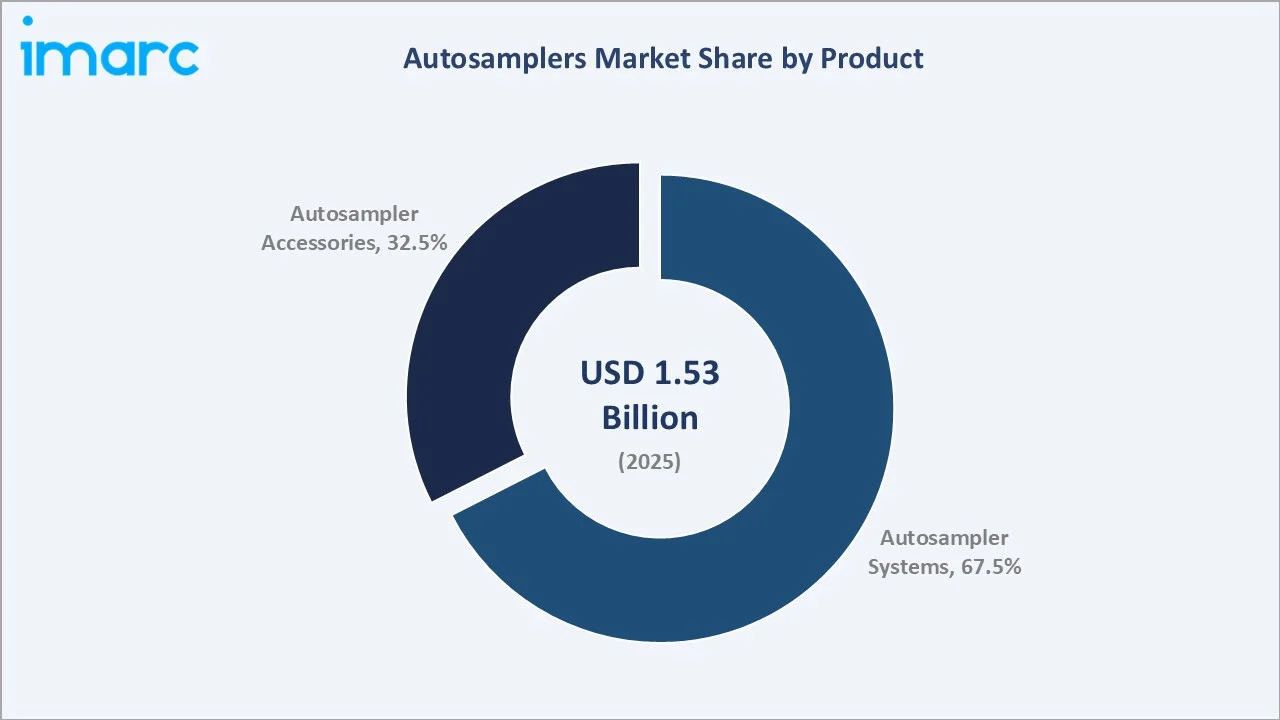

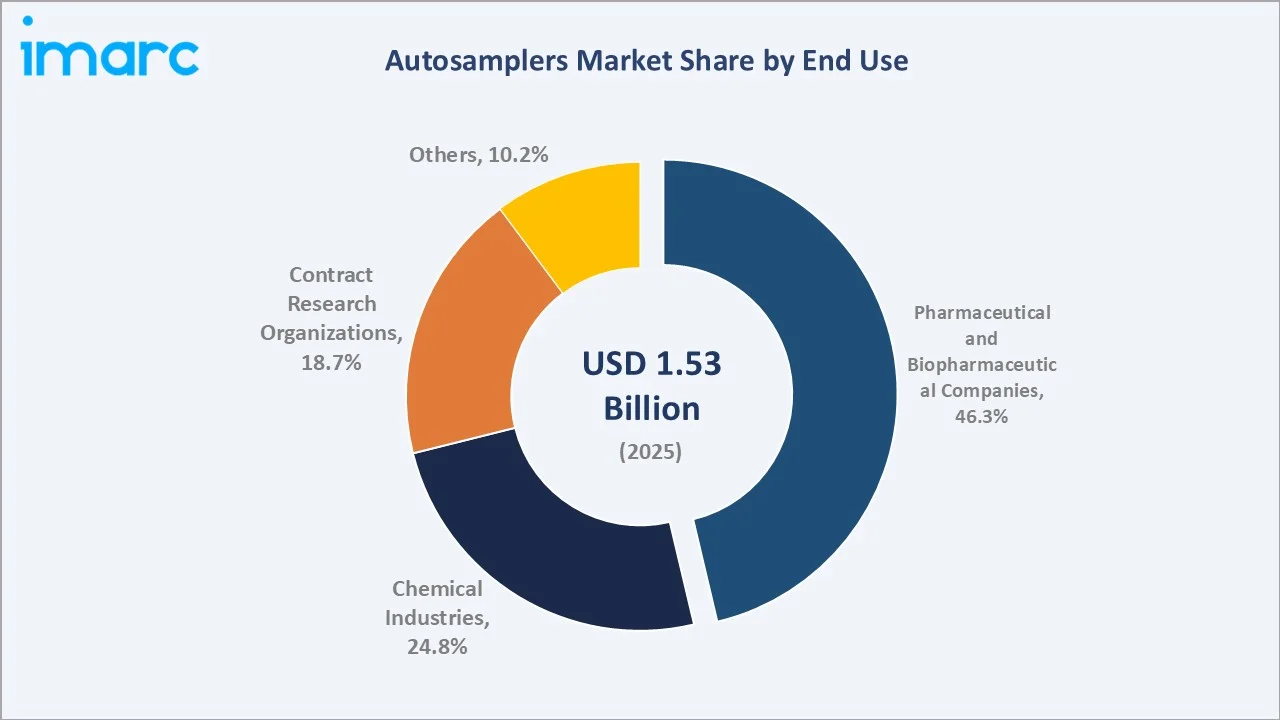

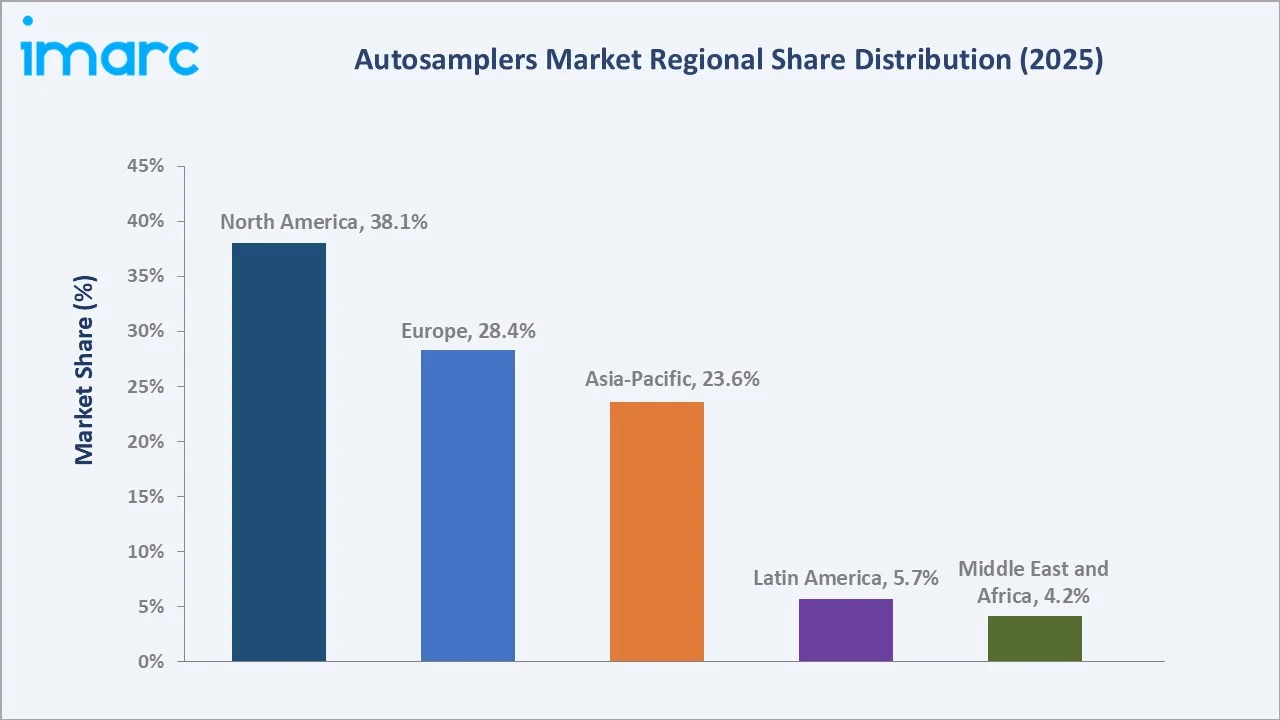

Autosampler systems dominate the product segment at 67.5%, pharmaceutical and biopharmaceutical companies lead end use segment at 46.3%, and North America commands the largest regional share at 38.1%.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 1.53 Billion |

|

Forecast Market Size (2034) |

USD 2.74 Billion |

|

CAGR (2026-2034) |

6.05% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.1%, 2025) |

|

Fastest Growing Region |

Asia-Pacific (23.6%, 2025) |

|

Leading Product |

Autosampler Systems (67.5%, 2025) |

|

Leading End Use |

Pharmaceutical and Biopharmaceutical Companies (46.3%, 2025) |

The autosamplers market expanded from USD 1.14 Billion in 2020 to USD 1.53 Billion in 2025, driven by increasing laboratory automation adoption, tightening analytical testing regulations, and growing pharmaceutical pipeline activity. The market is anchored at USD 2.05 Billion in 2030, with the forecast to USD 2.74 Billion by 2034 supported by expanding biopharmaceutical manufacturing and growing contract research activity.

To get more information on this market, Request Sample

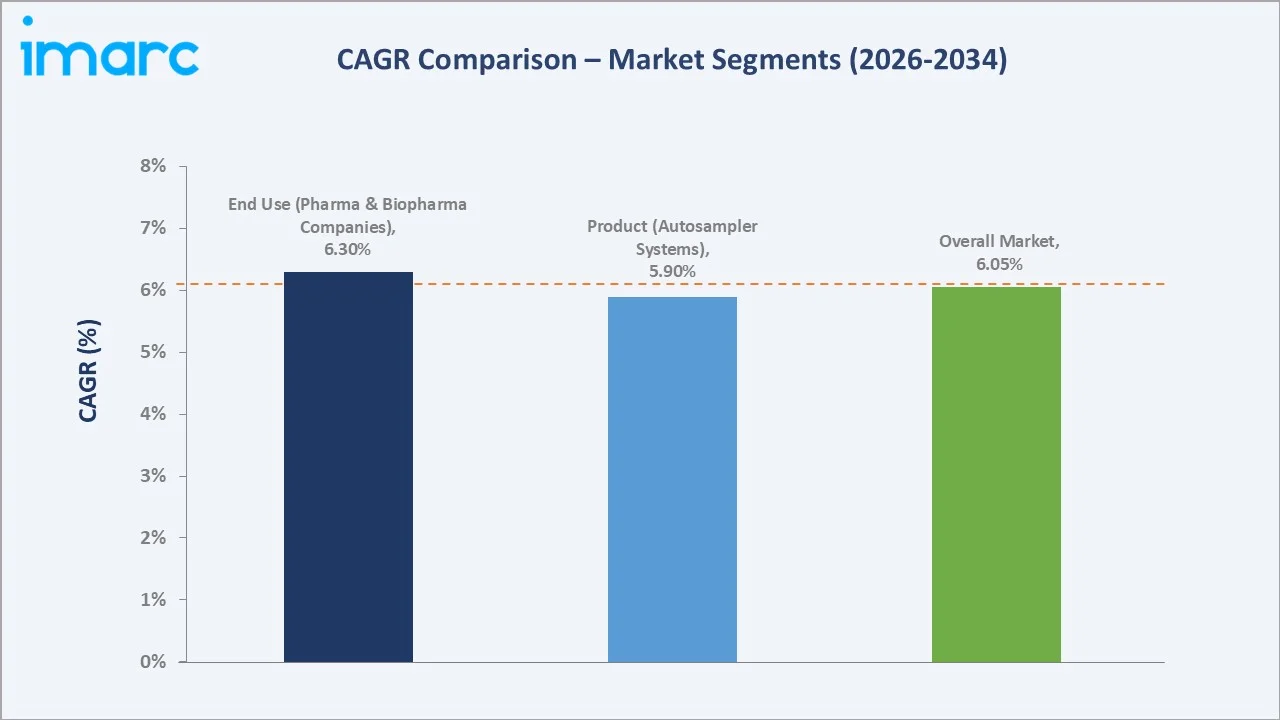

CAGR trajectories across product and end use sub-segments show contract research organizations and autosampler accessories expanding faster than the overall 6.05% market CAGR, driven by pharmaceutical outsourcing trends and consumable replacement cycles in high-throughput analytical environments.

Executive Summary

The autosamplers market is on a steady growth trajectory, expanding from USD 1.14 Billion in 2020 to a projected USD 2.74 Billion by 2034. Autosamplers have evolved from basic injection devices to intelligent systems with integrated temperature control, fraction collection, and real-time diagnostics. Rising adoption of liquid chromatography and gas chromatography across pharmaceutical, chemical, and research applications continues to sustain demand.

Autosampler systems dominate the product segment at 67.5%, supported by continued investment in high-performance liquid chromatography (HPLC) and gas chromatography (GC) infrastructure. Pharmaceutical and biopharmaceutical companies lead end use demand at 46.3% in 2025, fueled by rising drug development activities and growing reliance on analytical testing for quality control and regulatory compliance. North America commands 38.1% in 2025, anchored by a dense pharmaceutical manufacturing base and rigorous FDA compliance mandates. As per IMARC Group, the United States pharmaceutical market size was valued at USD 511.01 Billion in 2025.

Key Market Insights

|

Insight |

Data |

|

Leading Product |

Autosampler Systems – 67.5% share (2025) |

|

Second Product |

Autosampler Accessories – 32.5% share (2025) |

|

Leading End Use |

Pharmaceutical and Biopharmaceutical Companies – 46.3% share (2025) |

|

Second End Use |

Chemi0cal Industries – 24.8% share (2025) |

|

Leading Region |

North America – 38.1% share (2025) |

|

Fastest Growing Region |

Asia-Pacific – 23.6% share (2025) |

|

Top Companies |

Shimadzu Corporation, Agilent Technologies, Inc., Waters Corporation, PerkinElmer |

Key Analytical Observations Expanding on the Data Above:

- Autosampler systems dominance at 67.5% is driven by widespread adoption of HPLC, GC, and IC platforms in regulated industries, where complete autosampler systems with injection modules, sample coolers, and integrated diagnostics are standard procurement choices.

- Autosampler accessories at 32.5% reflect strong recurring demand for vials, septa, sample trays, and replacement components across high-throughput analytical laboratories with established chromatographic workflows.

- Pharmaceutical and biopharmaceutical companies lead at 46.3% as the largest end use segment. NIH received a total program level of USD 47.493 Billion in FY 2026, sustaining extensive biomedical research activity that drives high-volume chromatographic testing demand across pharmaceutical and biopharmaceutical quality control, stability testing, and drug discovery workflows.

- Chemical industries at 24.8% are sustained by quality control testing mandates, environmental monitoring requirements, and routine analytical workflows across petrochemical, specialty chemical, and agrochemical manufacturing facilities.

- North America at 38.1% leads globally owing to a highly developed pharmaceutical and biotechnology sector, rigorous FDA compliance frameworks, and broad adoption of modern laboratory automation technologies across research and manufacturing facilities.

Autosamplers Market Overview

Autosamplers are automated laboratory instruments that inject precise, reproducible volumes of liquid or gas-phase samples into chromatographic systems, replacing manual injection and reducing analytical variability. They are integral to HPLC, GC, IC, and CE workflows across pharmaceutical quality control, environmental testing, food safety, and chemical analysis applications.

The market ecosystem incorporates precision engineering manufacturers, chromatography OEMs, analytical reagent suppliers, laboratory software developers, regulatory compliance service providers, and end user institutions. Macroeconomic influences include growth in global pharmaceutical output, tightening environmental testing mandates, and increased contract research activity worldwide.

Market Dynamics

To evaluate market opportunities, Request Sample

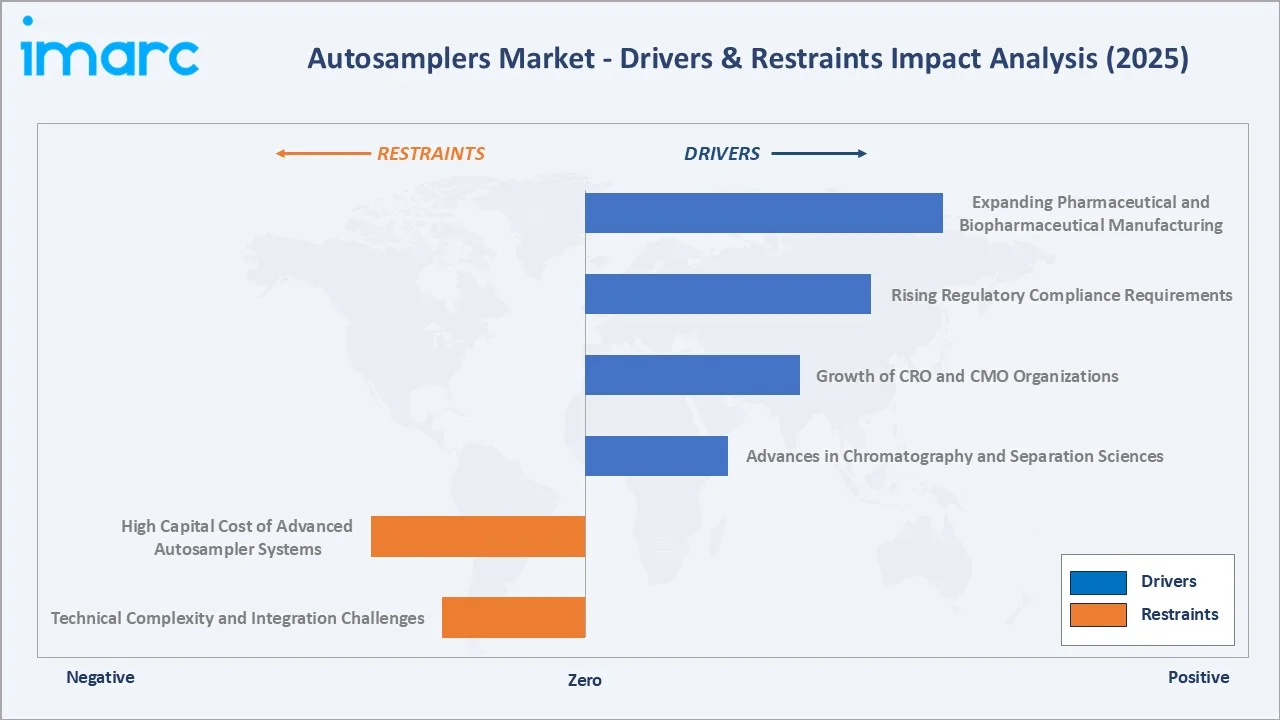

Market Drivers

- Expanding Pharmaceutical and Biopharmaceutical Manufacturing: Growing global drug production volumes and an expanding pipeline of novel therapeutics are driving sustained demand for validated chromatographic testing infrastructure, with autosamplers serving as critical components across analytical quality control and method development workflows.

- Rising Regulatory Compliance Requirements: Pharmacopeial standards from the United States Pharmacopeia (USP), European Pharmacopoeia (Ph.Eur.), and Japan Pharmacopoeia (JP) mandate reproducible sample injection protocols. These requirements are accelerating the adoption of automated autosampler systems that support audit trails, minimize human error, and ensure consistent analytical performance across regulated laboratory environments.

- Growth of CRO and CMO Organizations: The global expansion of CRO and CMO sectors, driven by pharmaceutical outsourcing trends, is increasing demand for high-throughput autosamplers that support parallel sample processing, method transfer, and multi-compound analytical workflows.

- Advances in Chromatography and Separation Sciences: Continued innovation in UPLC, ion chromatography, and multi-dimensional separation techniques is driving upgrades to compatible autosampler systems with higher pressure ratings, broader solvent compatibility, and improved injection precision.

Market Restraints

- High Capital Cost of Advanced Autosampler Systems: Fully configured laboratory-grade HPLC autosampler systems involve substantial capital investment due to their advanced throughput capabilities, precision injection mechanisms, and integrated analytical functionalities, limiting adoption among small analytical laboratories and contract testing organizations in cost-sensitive emerging markets.

- Technical Complexity and Integration Challenges: Advanced autosampler configurations require specialized technical expertise for installation, method validation, and system qualification, creating barriers for smaller laboratories with limited technical resources and increasing total cost of ownership beyond initial acquisition costs.

Market Opportunities

- Automation of High-Throughput Screening in Drug Discovery: Growing adoption of automated analytical platforms in drug discovery and bioanalytical testing is creating strong demand for multi-position autosamplers with integrated sample management, fraction collection, and real-time analytical monitoring capabilities.

- Expansion in Emerging Markets: Rapidly growing pharmaceutical manufacturing bases across India, China, Brazil, and Southeast Asia are generating new demand for chromatographic laboratory infrastructure, presenting significant growth opportunities for autosampler suppliers seeking to establish or expand presence in high-growth markets.

Market Challenges

- Maintenance and Lifecycle Management: Autosamplers require regular maintenance of injection needles, seals, and wash systems to maintain analytical performance, creating ongoing operational costs and potential instrument downtime that challenge laboratory throughput in high-volume testing environments.

- Compatibility with Diverse Analytical Platforms: Ensuring broad compatibility between autosampler systems and a wide range of chromatographic instruments, column chemistries, and detection systems remains a technical and commercial challenge for manufacturers serving multi-instrument laboratory environments.

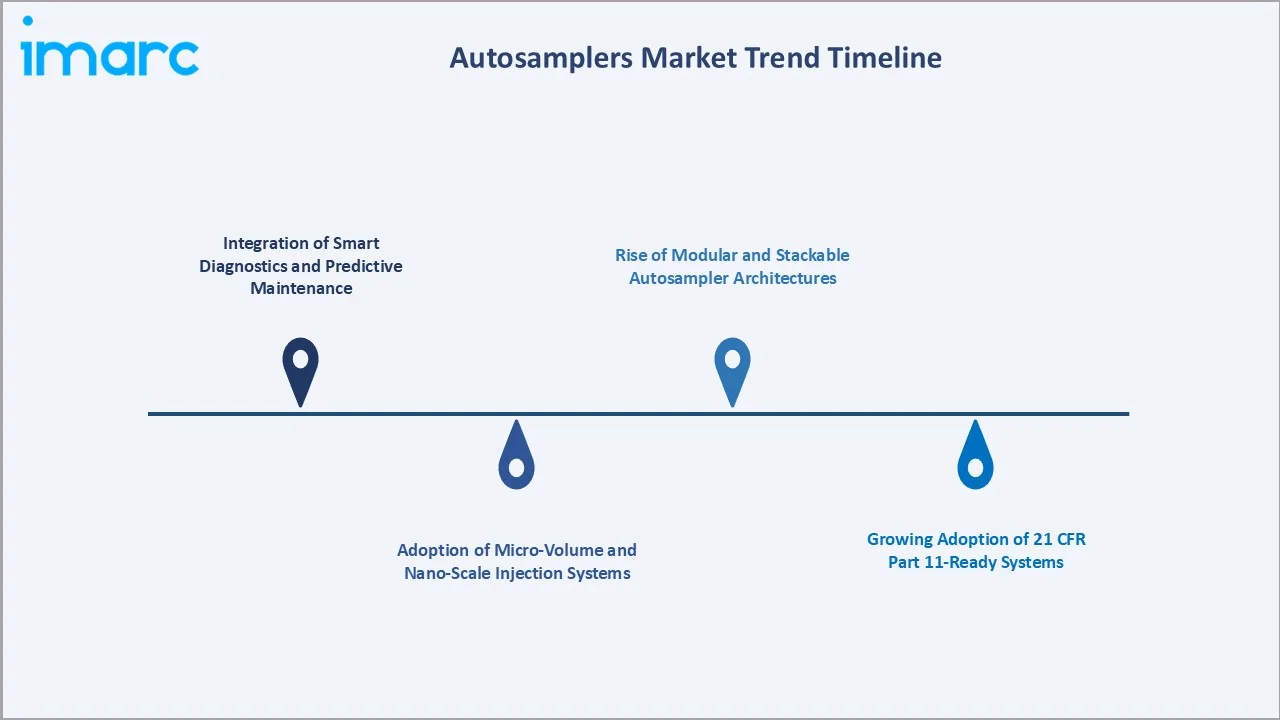

Emerging Market Trends

1. Integration of Smart Diagnostics and Predictive Maintenance

Modern autosamplers are increasingly equipped with built-in sensors, self-diagnostic modules, and connectivity to laboratory information management systems (LIMS). These capabilities enable real-time monitoring of injection performance, early detection of seal wear or needle fouling, and data-driven maintenance scheduling. The integration reduces unplanned downtime across high-throughput analytical operations and supports compliance with data integrity requirements in regulated laboratory environments.

2. Adoption of Micro-Volume and Nano-Scale Injection Systems

The growing use of precious biological samples in biopharmaceutical research and clinical bioanalysis is driving demand for autosamplers capable of precise micro-volume and nano-scale injections. Systems offering sub-microliter injection volumes with high repeatability are becoming standard requirements in peptide, protein, and antibody characterization workflows across leading biopharmaceutical research facilities.

3. Rise of Modular and Stackable Autosampler Architectures

Instrument manufacturers are transitioning toward modular autosampler platforms that can be configured for different throughput levels, sample types, and analytical applications. These flexible architectures enable laboratories to scale operations incrementally, optimize bench space utilization, and integrate autosamplers seamlessly with evolving chromatographic and spectroscopic workflows.

4. Growing Adoption of 21 CFR Part 11-Ready Systems

Regulatory requirements surrounding electronic data integrity, audit trails, and system validation are driving the adoption of GxP-compliant autosamplers equipped with 21 CFR Part 11 and Annex 11-ready capabilities. Pharmaceutical and biopharmaceutical quality control laboratories are increasingly favoring instruments that support secure data handling, automated audit documentation, and seamless integration with validated laboratory informatics and data management systems.

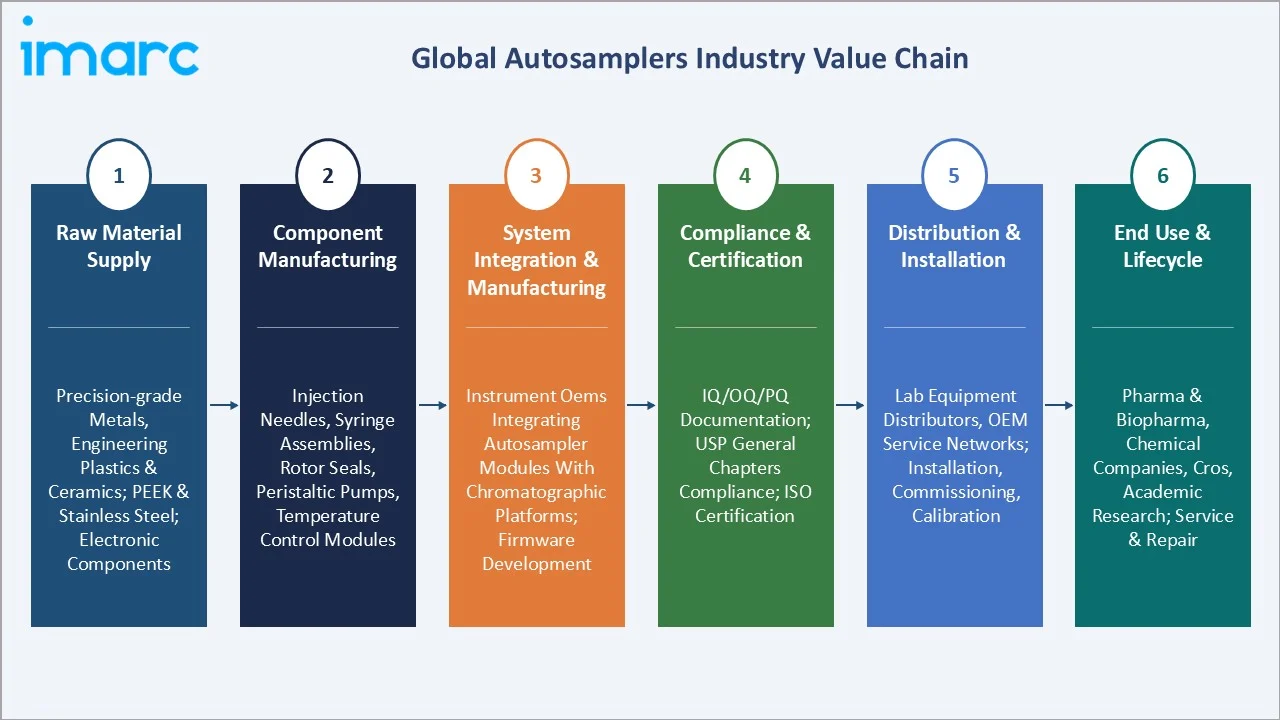

Industry Value Chain Analysis

The autosamplers market value chain spans six key stages from precision raw material sourcing through end user deployment and after-sales lifecycle management. System integration and component manufacturing represent the highest value-add stages, while technical service and consumable supply generate consistent downstream revenue streams for established instrument manufacturers.

|

Stage |

Key Players / Examples |

|

Raw Material Supply |

Suppliers of precision-grade metals, engineering plastics, and ceramics; PEEK and stainless steel component manufacturers; electronic component providers supporting autosampler assembly |

|

Component Manufacturing |

Manufacturers of injection needles, syringe assemblies, rotor seals, peristaltic pumps, temperature control modules, and electronic control boards |

|

System Integration & Manufacturing |

Instrument OEMs integrating autosampler modules with chromatographic platforms, developing firmware, and conducting factory acceptance testing |

|

Compliance & Certification |

Regulatory testing bodies and qualification service providers supporting IQ/OQ/PQ documentation, USP General Chapters compliance, and ISO certification processes |

|

Distribution & Installation |

Laboratory equipment distributors, OEM service networks, and specialist chromatography suppliers providing installation, commissioning, and calibration services |

|

End Use & Lifecycle |

Pharmaceutical and biopharmaceutical manufacturers, chemical companies, CROs, academic research institutions; service and repair organizations |

Technology Landscape in the Autosamplers Industry

Precision Injection Engineering

Advances in needle geometry, syringe drive accuracy, and valve switching technology are enabling autosamplers to achieve high injection volume reproducibility. These engineering improvements directly support method validation requirements across regulated pharmaceutical and clinical applications where analytical precision is critical to regulatory compliance.

Temperature Control and Sample Stability

Thermostatically controlled sample compartments with precise temperature management are becoming standard across modern autosampler platforms. Stable temperature conditions are essential for preserving sample integrity in biopharmaceutical applications involving labile proteins, peptides, and nucleic acids, particularly across extended analytical sequences in stability testing and bioanalytical studies.

Smart Connectivity and Software Integration

Current autosampler systems increasingly incorporate Ethernet and wireless connectivity, enabling remote diagnostics, electronic audit trail generation, and seamless integration with laboratory data management platforms. These capabilities align with industry-wide digitalization trends and support compliance with 21 CFR Part 11 and Annex 11 data integrity requirements in regulated analytical environments.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product | Autosampler Systems | 67.5% | 2025 |

| End Use | Pharmaceutical and Biopharmaceutical Companies | 46.3% | 2025 |

| Region | North America | 38.1% | 2025 |

By Product

Autosampler systems command a 67.5% majority share in 2025, underpinned by broad adoption across HPLC, GC, and IC analytical platforms in pharmaceutical QC, environmental testing, and food safety laboratories. These complete systems, incorporating sample coolers, injection modules, and multi-tray configurations, are preferred for their validated performance and ease of system qualification.

To access detailed market analysis, Request Sample

Autosampler accessories hold a 32.5% share, benefitting from high recurring purchase volumes driven by consumable replacement cycles in established laboratory environments. Continuous demand for vials, syringes, septa, trays, and replacement components across routine analytical workflows supports steady aftermarket revenue generation for manufacturers and distributors.

By End Use

Pharmaceutical and biopharmaceutical companies lead end use segment at 46.3% in 2025, driven by extensive regulatory testing requirements, broad adoption of HPLC and GC-based quality control methods, and growing biopharmaceutical pipeline activity.

Chemical industries hold 24.8%, sustained by routine analytical testing mandates across the petrochemical, specialty chemical, and agrochemical sectors. Autosamplers play a critical role in supporting high-throughput quality control, process monitoring, and contamination analysis within complex chemical manufacturing environments.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.1% |

Strong pharmaceutical manufacturing base, stringent regulatory requirements, widespread laboratory automation adoption, and growing biopharmaceutical research activity |

|

Europe |

28.4% |

Robust EMA regulatory framework, established chromatography infrastructure, growing analytical outsourcing, and expanding contract research activity |

|

Asia-Pacific |

23.6% |

Expanding pharmaceutical manufacturing capacity, growing R&D investment, increasing laboratory modernization, and rising adoption of chromatographic testing standards |

|

Latin America |

5.7% |

Growing pharmaceutical industry, increasing regulatory harmonization, expanding chemical sector, and rising healthcare infrastructure investment |

|

Middle East and Africa |

4.2% |

Developing laboratory infrastructure, growing pharmaceutical manufacturing, and increasing regulatory capacity building |

North America at 38.1% in 2025 leads the autosamplers market, anchored by a highly developed pharmaceutical and biotechnology sector, extensive analytical laboratory infrastructure, and regulatory compliance mandates from FDA.

Europe at 28.4% is supported by rigorous EMA regulatory standards, strong research institution networks, and a well-established chromatographic instrument installed base across Germany, the United Kingdom, France, and Switzerland.

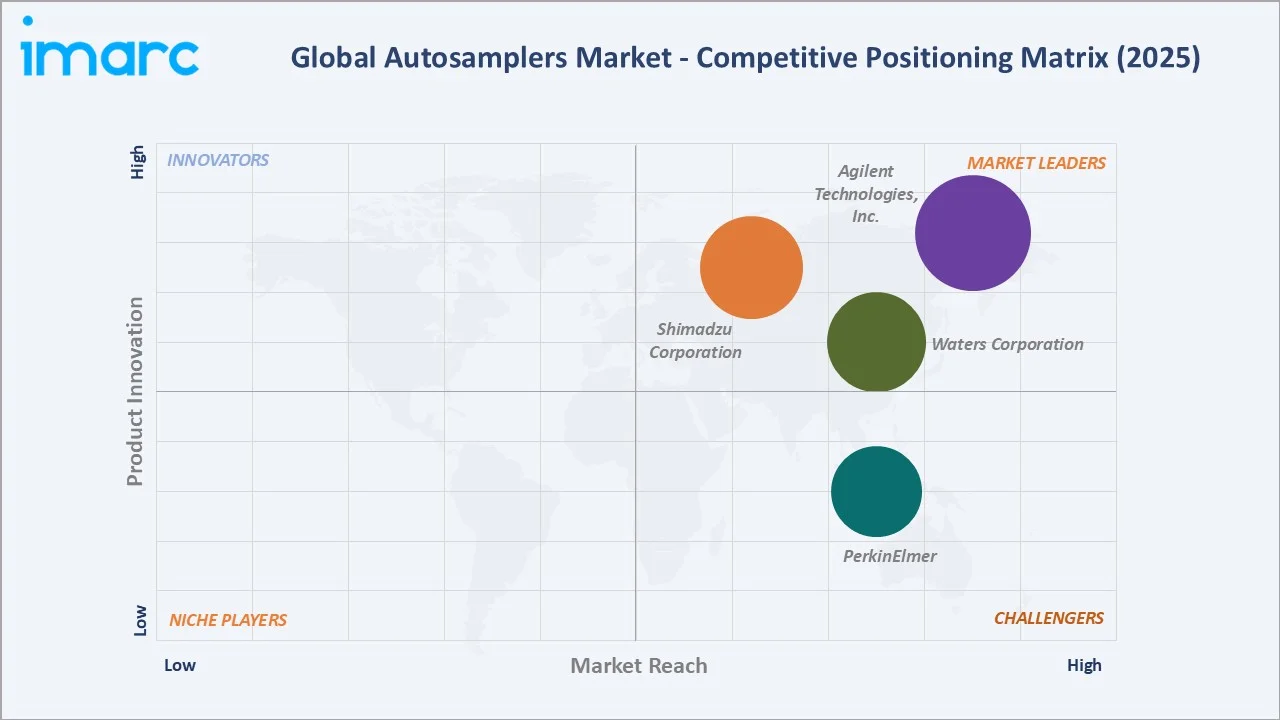

Competitive Landscape

The autosamplers market is moderately consolidated, with leading analytical instrument manufacturers leveraging integrated product portfolios, global service networks, and deep chromatography expertise to maintain competitive advantage. Innovation in injection precision, system connectivity, and compliance-ready software platforms forms the primary basis of competitive differentiation across the market.

|

Company Name |

Brand / Key Product |

Position |

Strategic Focus |

|

Shimadzu Corporation |

Nexera X4 Ultra High-Performance Liquid Chromatograph |

Leader |

High-performance chromatography and analytical workflow integration |

|

Agilent Technologies, Inc. |

1260 Infinity III LC System |

Leader |

Comprehensive analytical instrumentation and high-throughput laboratory solutions |

|

Waters Corporation |

ACQUITY series |

Leader |

Ultra-performance chromatography and advanced separation science solutions |

|

PerkinElmer |

S20 Series, HS 2400 Headspace Autosampler |

Challenger |

Analytical testing solutions across pharmaceutical, environmental, and food safety markets |

Key players include Shimadzu Corporation, Agilent Technologies, Inc., Waters Corporation, and PerkinElmer, among others.

Key Company Profiles

Shimadzu Corporation

Shimadzu Corporation is a precision instrument manufacturer with extensive experience across analytical, medical, and industrial equipment. The company is a well-established global supplier of liquid chromatography and gas chromatography systems, with its autosampler product range serving pharmaceutical, environmental, food safety, and chemical analysis laboratories worldwide.

- Product Portfolio: Nexera X4 Ultra High-Performance Liquid Chromatograph and the broader Nexera series, offering automated sample handling, integrated diagnostics, and compatibility with a broad range of analytical applications.

- Recent Developments: In April 2026, Shimadzu Corporation launched the Nexera X4 UHPLC, its next-generation platform featuring advanced fluid control technology, low-dispersion design, and AI-assisted diagnostics to support high-throughput pharmaceutical quality control and analytical research workflows.

- Strategic Focus: High-performance chromatography and analytical workflow integration.

Agilent Technologies, Inc.

Agilent Technologies, Inc. is a United States-based global leader in analytical instrumentation, laboratory workflows, and related services. The company serves pharmaceutical, life sciences, chemical, food, and environmental markets with a comprehensive portfolio of liquid chromatography and gas chromatography systems, including a broad range of autosampler configurations for diverse laboratory environments.

- Product Portfolio: 1260 Infinity III LC System, featuring bio-inert configurations and high-capacity autosampler solutions for pharmaceutical and biopharmaceutical workflows.

- Recent Developments: In October 2024, Agilent launched the Infinity III LC Series, a next-generation platform designed to improve laboratory efficiency through automated HPLC diagnostics, expanded sample capacity, and enhanced sustainability features for regulated analytical environments.

- Strategic Focus: Comprehensive analytical instrumentation and high-throughput laboratory solutions.

PerkinElmer

PerkinElmer is an analytical instruments company serving pharmaceutical, environmental, food, and industrial testing markets. The company offers a portfolio of liquid chromatography and spectroscopy systems designed for diverse analytical applications, with its autosampler solutions supporting routine and demanding laboratory workflows across multiple end-use sectors.

- Product Portfolio: LC 300 HPLC and UHPLC Systems, offering customizable pump configurations, onboard sample handling capabilities, built-in solvent degassing, and compatibility with the SimplicityChrom chromatography data system for streamlined analytical workflows.

- Recent Developments: PerkinElmer has continued to develop the LC 300 platform with enhanced automation capabilities and workflow integration features, targeting pharmaceutical, environmental, and food safety laboratories seeking high-throughput analytical solutions.

- Strategic Focus: Analytical testing solutions across pharmaceutical, environmental, and food safety markets.

Market Concentration Analysis

The autosamplers market is moderately concentrated, with the top four companies (Shimadzu Corporation, Agilent Technologies, Inc., Waters Corporation, and PerkinElmer) estimated to collectively hold approximately 55–65% of global market revenue in 2025.

Barriers to entry include significant capital investment in precision engineering manufacturing, establishment of global service and calibration networks, and the lengthy process of building customer trust in regulated laboratory environments where instrument qualification is a critical procurement requirement.

Consolidation continues through strategic acquisitions, technology partnerships, and expansion of integrated software and service offerings that extend the value proposition beyond hardware alone.

Investment & Growth Opportunities

Fastest-Growing Segments

Contract research organizations at 18.7% represent the fastest-growing end use segment, expanding ahead of the overall 6.05% market CAGR as pharmaceutical outsourcing accelerates. Autosampler accessories at 32.5% benefit from high recurring consumable demand and offer stable, predictable revenue streams for suppliers serving established analytical laboratory networks.

Emerging Markets

Asia-Pacific at 23.6% is the highest-growth region through 2034, with China's expanding pharmaceutical manufacturing sector, India's growing generic drug industry, and South Korea's increasing biopharmaceutical R&D investment driving rapid market expansion. Latin America and the Middle East and Africa represent longer-term growth opportunities as laboratory infrastructure investment increases.

Venture & Investment Trends

Investment activity is focused on smart autosampler platforms with LIMS integration capabilities, IoT-enabled predictive maintenance solutions, and compliance-ready software for regulated laboratory environments. Industry consolidation through acquisitions of specialty autosampler manufacturers by larger analytical instrument companies is creating strategic value, while expansion into high-growth Asian markets is a priority for leading players.

Future Market Outlook (2026-2034)

The autosamplers market is forecast to expand from USD 1.53 Billion in 2025 to USD 2.74 Billion by 2034 at a CAGR of 6.05%, adding approximately USD 1.21 Billion in incremental annual market value over the forecast period.

Three forces will shape the market through 2034: continued pharmaceutical pipeline expansion; accelerating laboratory automation and digitalization; and growing adoption of compliance-ready, connected autosampler platforms across regulated industries globally.

By 2034, autosamplers are expected to incorporate smart diagnostic and remote monitoring capabilities as baseline specifications across pharmaceutical quality control environments.

Research Methodology

Primary Research

Primary research included structured interviews with senior analytical laboratory managers, procurement officers at pharmaceutical and CRO companies, instrument service engineers, and regulatory compliance specialists. These interactions validated market sizing, segment demand drivers, and regional adoption trends across key end use verticals in the autosamplers market.

Secondary Research

Secondary sources included pharmacopeial publications from the USP, Ph.Eur., and JP; regulatory guidelines from the FDA and EMA; industry association reports; company annual reports, investor presentations, and product launch announcements; and peer-reviewed analytical chemistry and separation science journals.

Forecasting Models

Market forecasts utilized top-down and bottom-up modeling combining pharmaceutical production volumes, chromatography instrument installation base data, replacement cycle rates, and regional regulatory compliance adoption timelines. Sensitivity analysis addressed scenarios related to pharmaceutical pipeline activity and laboratory automation investment cycles.

Autosamplers Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Product Covered |

|

| End Uses Covered | Pharmaceutical and Biopharmaceutical Companies, Chemical Industries, Contract Research Organizations, Others |

| Region Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Shimadzu Corporation, Agilent Technologies, Inc., Waters Corporation, PerkinElmer, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Autosamplers Market Report

The autosamplers market was valued at USD 1.53 Billion in 2025, supported by growing pharmaceutical testing requirements, laboratory automation adoption, and expanding chromatographic workflows globally.

The market is projected to grow at a CAGR of 6.05% from 2026 to 2034, reaching USD 2.74 Billion, driven by pharmaceutical R&D expansion and laboratory modernization investment.

Autosampler systems lead with 67.5% share in 2025, driven by widespread adoption in HPLC, GC, and IC platforms across pharmaceutical, chemical, and research laboratories.

Pharmaceutical and biopharmaceutical companies lead at 46.3% in 2025, driven by extensive regulatory testing mandates, growing biopharmaceutical pipelines, and high analytical testing volumes.

North America leads with 38.1% in 2025, anchored by a large pharmaceutical manufacturing base, FDA compliance requirements, and broad laboratory automation adoption.

Key players include Shimadzu Corporation, Agilent Technologies, Inc., Waters Corporation, and PerkinElmer.

Key trends include smart diagnostics integration, micro-volume injection systems, modular platform architectures, and growing demand for 21 CFR Part 11-compliant systems.

High capital costs of advanced systems and technical complexity of integration with diverse analytical platforms are the key challenges limiting adoption among smaller laboratories.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)