Azotobacter Market Size, Share, Trends and Forecast by Crop Type and Region 2026-2034

Azotobacter Market Size, Share, Trends & Forecast (2026-2034)

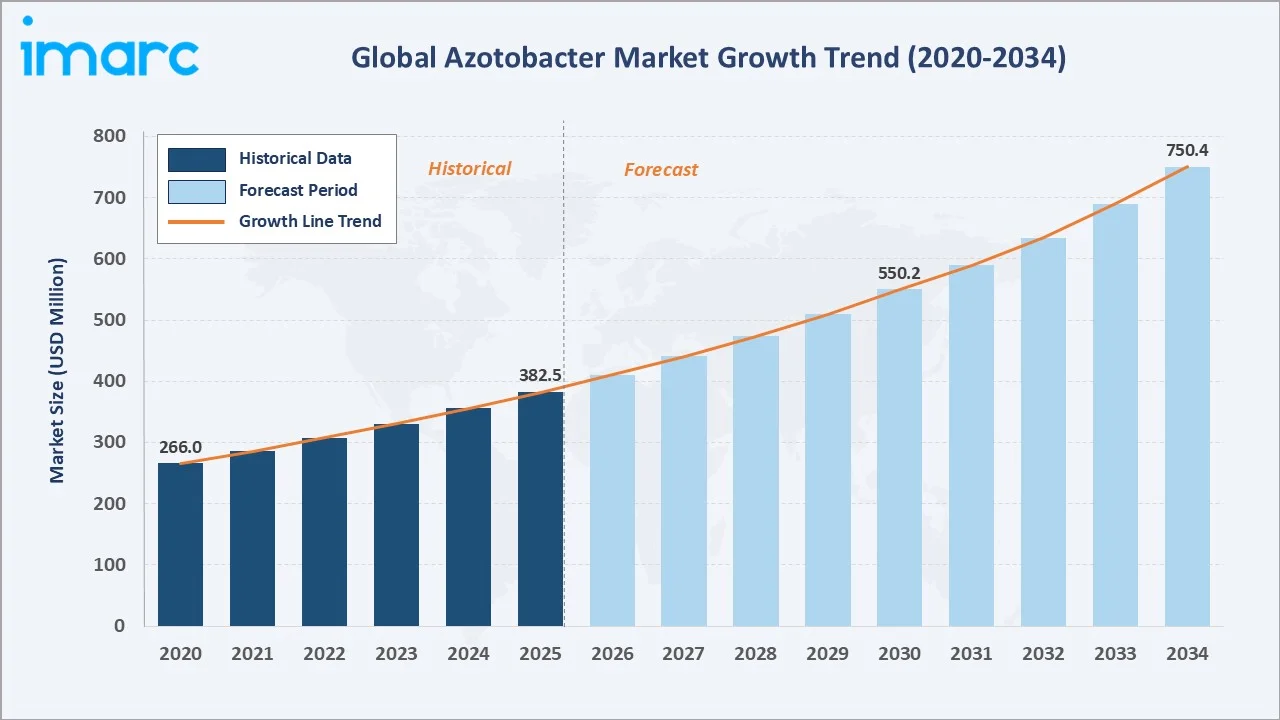

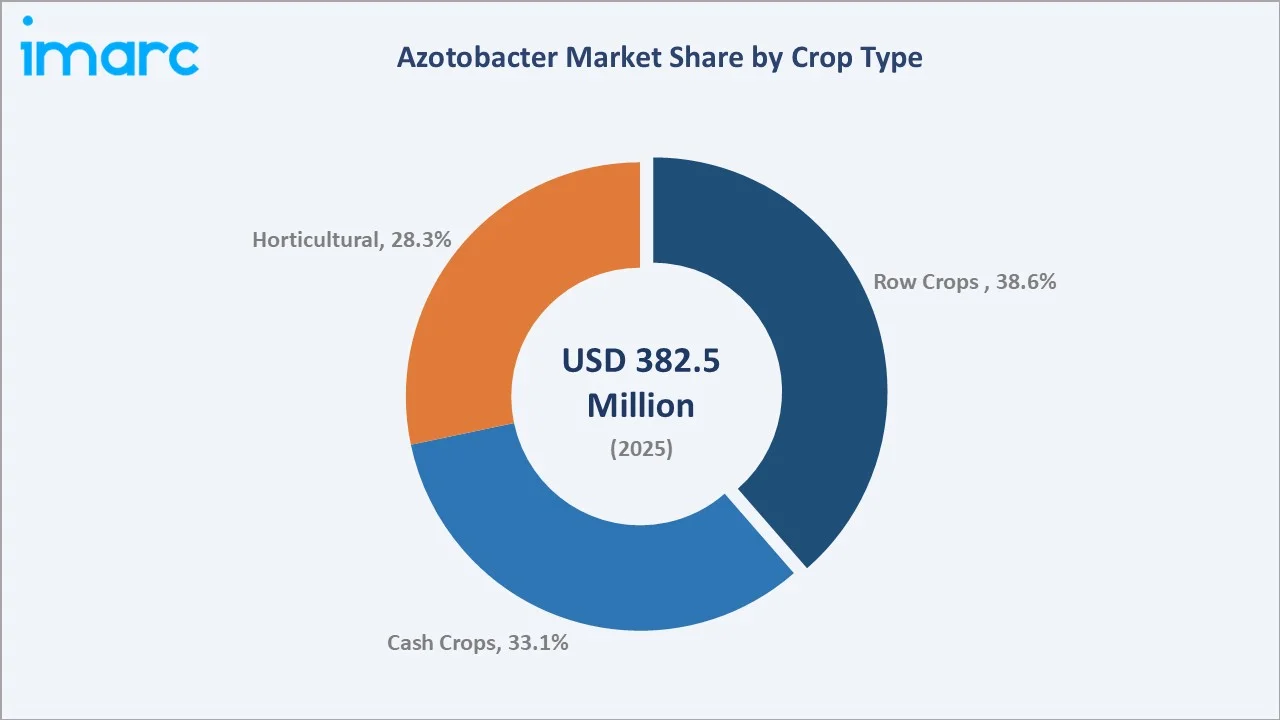

The global azotobacter market reached USD 382.5 Million in 2025 and is projected to reach USD 750.4 Million by 2034, growing at a CAGR of 7.54% during 2026-2034. The market is driven by rising demand for sustainable agriculture, environmental conservation, biotechnology advancements, and growing need for eco-friendly alternatives to synthetic fertilizers.

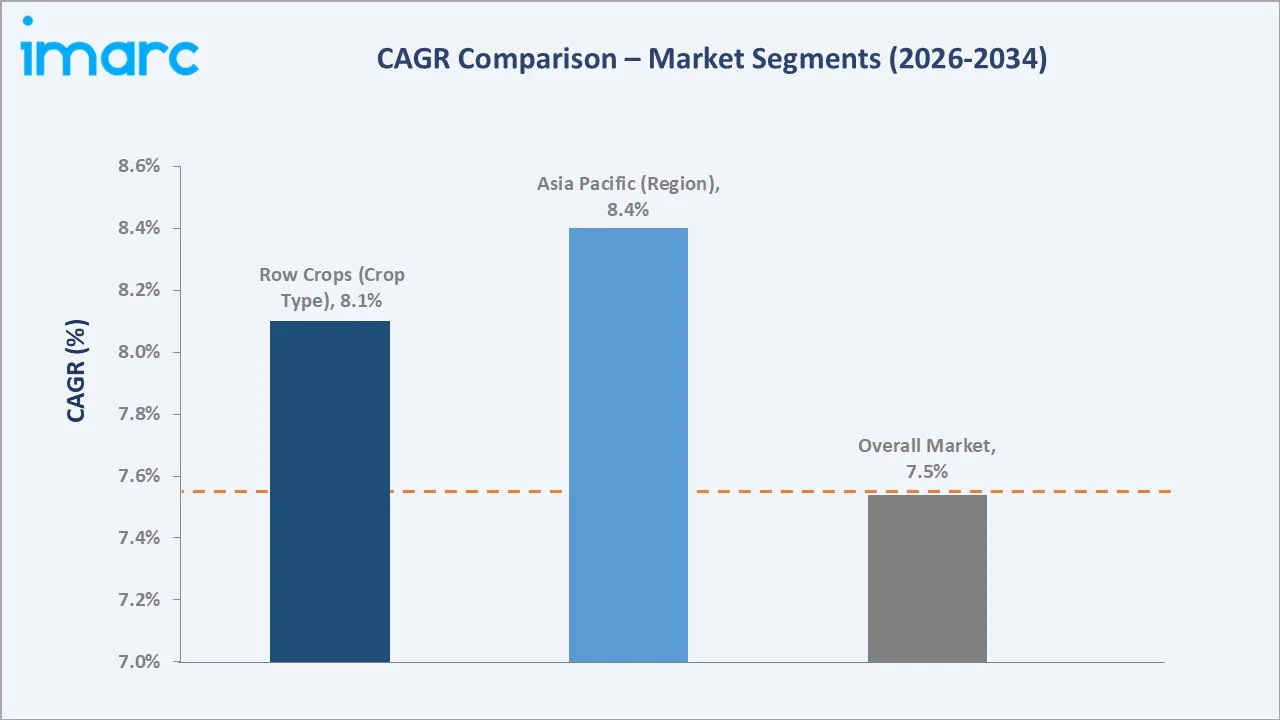

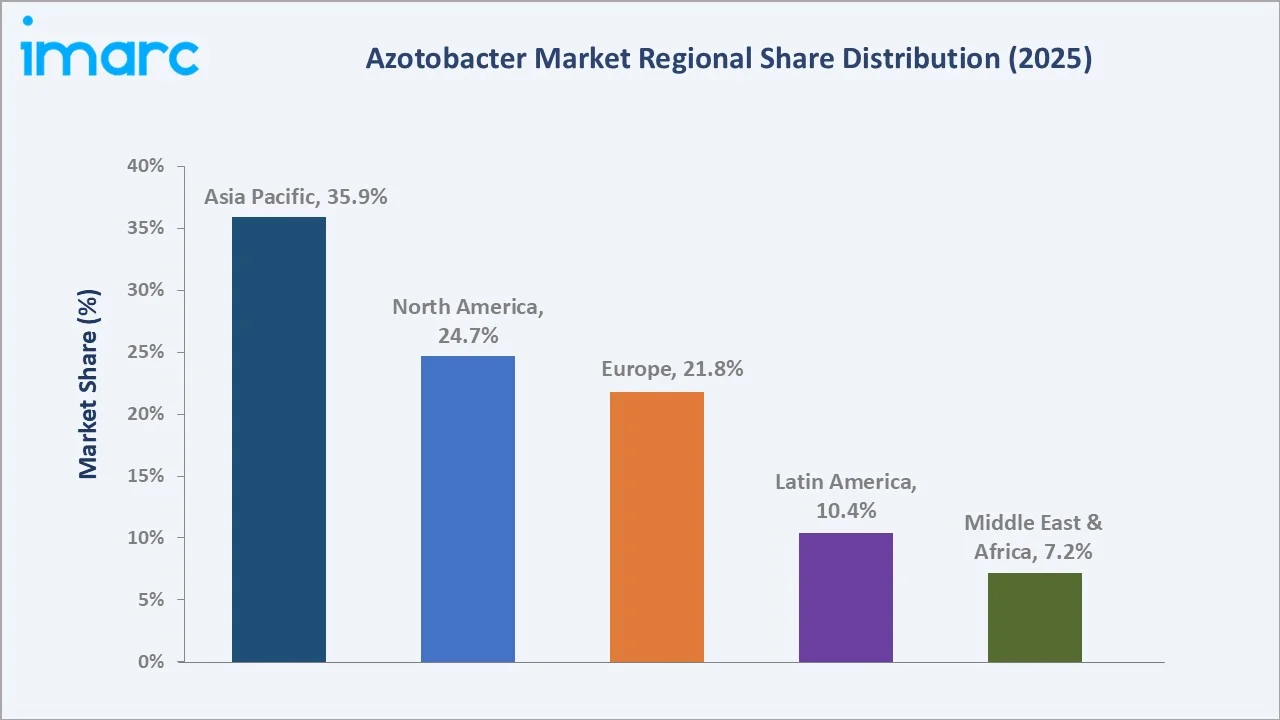

Row Crops lead at 38.6%. Asia Pacific commands 35.9% of global market share.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 382.5 Million |

|

Forecast Market Size (2034) |

USD 750.4 Million |

|

CAGR (2026-2034) |

7.54% |

|

Base Year |

2025 |

|

Historical Period |

2025 |

|

Forecast Period |

2026-2034 |

|

Dominant Crop Type |

Row Crops (38.6%, 2025) |

|

Leading Region |

Asia Pacific (35.9%, 2025) |

The market expanded from USD 266.0 Million in 2020 to USD 382.5 Million in 2025, anchored at USD 550.2 Million in 2030 and forecast to reach USD 750.4 Million by 2034. Growth is underpinned by expanding biofertilizer adoption and government policy support across major agricultural economies.

To get more information on this market, Request Sample

Row Crops grow fastest at ~8.1% CAGR as global food security demands drive sustainable nitrogen-fixation adoption. Asia Pacific leads regional growth at ~8.4% CAGR, driven by India and China's large-scale agricultural expansion and biofertilizer programs.

Executive Summary

The global azotobacter market reached USD 382.5 Million in 2025, representing one of agriculture's highest-growth biofertilizer segments driven by the global transition toward sustainable farming. The market is projected to reach USD 750.4 Million by 2034.

Row Crops at 38.6% dominate through large-scale cereal and grain production requiring nitrogen supplementation. Asia Pacific at 35.9% leads globally through India and China's combined biofertilizer demand and strong government support.

Key Market Insights

|

Insight |

Data |

|

Dominant Crop Type |

Row Crops – 38.6% share (2025) |

|

Second Crop Type |

Cash Crops – 33.1% market share (2025) |

|

Leading Region |

Asia Pacific – 35.9% market share (2025) |

|

Market Opportunity |

Consortium biofertilizers; precision fermentation; organic farming expansion |

Key Analytical Observations Supporting The Above Data:

- Row Crops at 38.6%: Row crops dominate as they account for the largest cultivated area globally, with azotobacter enhancing nitrogen availability for wheat, rice, corn, and soybean, improving yields while reducing synthetic fertilizer dependence.

- Cash Crops at 33.1%: Cash crops are the second-largest segment as cotton, sugarcane, and tobacco farmers adopt azotobacter to meet sustainability standards and reduce input costs required by global commodity buyers.

- Asia Pacific at 35.9%: Asia Pacific leads due to its vast agricultural base, government biofertilizer promotion schemes, and high crop area under nitrogen-demanding cereals across India, China, and Southeast Asia.

Azotobacter Market Overview

The global azotobacter market encompasses the production, formulation, and distribution of azotobacter-based biofertilizers used across row crops, cash crops, and horticultural crops. The ecosystem integrates raw material suppliers, fermentation manufacturers, formulators, distributors, regulatory bodies, and end-users.

Macroeconomic drivers include rising population-driven food demand, government policies promoting organic farming, soil health deterioration from synthetic fertilizers, and increasing farmer awareness of biofertilizer benefits globally.

Market Dynamics

To evaluate market opportunities, Request Sample

Market Drivers

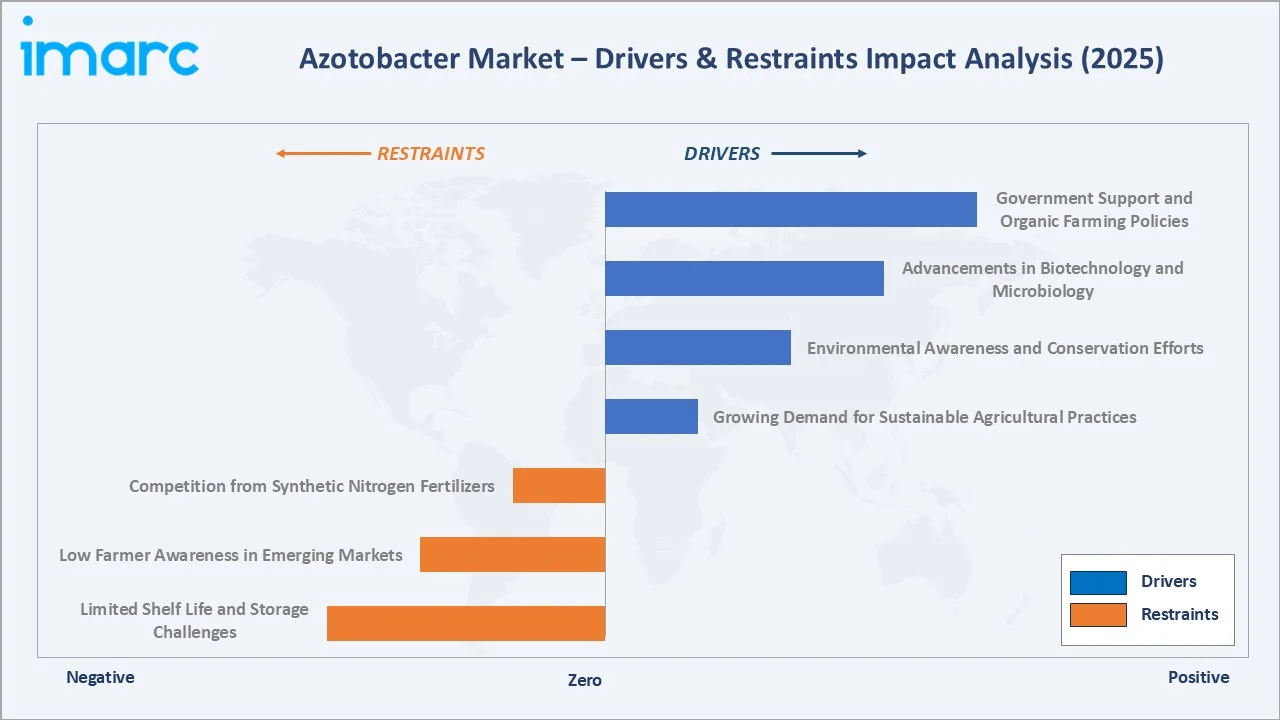

- Growing Demand for Sustainable Agricultural Practices: Rising global population increases pressure on food production, accelerating demand for eco-friendly nitrogen solutions. Azotobacter converts atmospheric nitrogen into plant-available ammonia, reducing synthetic fertilizer reliance while improving soil health and crop yields sustainably.

- Environmental Awareness and Conservation Efforts: Increasing concerns about soil degradation, greenhouse gas emissions, and water eutrophication from synthetic fertilizers drive azotobacter adoption. Its ability to reduce chemical nitrogen application supports climate goals and sustainable farming mandates adopted by governments globally.

- Advancements in Biotechnology and Microbiology: Ongoing R&D has enabled discovery of high-efficiency azotobacter strains with improved nitrogen-fixing capabilities. Genetic engineering and genome-editing advances further optimise bacterial performance, leading to commercially superior biofertilizer products with broader crop applicability.

- Government Support and Organic Farming Policies: Governments across Asia Pacific, Europe, and Latin America implement subsidies, incentive schemes, and regulations promoting biofertilizer adoption. India's PM-PRANAM scheme and the EU Farm-to-Fork strategy are directly accelerating azotobacter market penetration across major agricultural economies.

Market Restraints

- Limited Shelf Life and Storage Challenges: Azotobacter-based biofertilizers contain live microorganisms requiring controlled storage. Short shelf life, sensitivity to heat and UV radiation, and improper handling reduce product efficacy, limiting adoption in regions with inadequate cold-chain infrastructure.

- Low Farmer Awareness in Emerging Markets: Despite proven agronomic benefits, awareness of azotobacter biofertilizers remains limited among smallholder farmers in parts of Africa, Southeast Asia, and Latin America. Lack of extension services and demonstration programs slow adoption rates.

- Competition from Synthetic Nitrogen Fertilizers: Synthetic nitrogen fertilizers offer predictable, rapid-action results at competitive costs, creating persistent competition for azotobacter products. Established distribution infrastructure of chemical fertilizer companies poses significant barriers to accelerated biofertilizer market penetration.

Market Opportunities

- Consortium Biofertilizer Development: Combining azotobacter with phosphate-solubilizing bacteria, mycorrhizae, or rhizobium creates high-performance multi-microbial consortia offering superior agronomic results. Growing farmer demand for integrated soil nutrition solutions creates a premium product market for advanced consortium biofertilizers globally.

- Precision Fermentation and Strain Optimization: Investment in precision fermentation enables large-scale, cost-efficient production of superior azotobacter strains. Optimised manufacturing reduces unit costs, improves shelf life, and enables formulation diversity, opening new growth pathways for manufacturers and biotechnology startups entering the market.

Market Challenges

- Regulatory Variability Across Markets: Inconsistent registration requirements and approval timelines for biofertilizer products across countries create market entry barriers. Manufacturers face increased compliance costs, delayed product launches, and market access limitations in regions without streamlined biofertilizer regulatory frameworks.

- Quality Standardisation and Efficacy Consistency: Variability in azotobacter strain potency, carrier material quality, and manufacturing standards results in inconsistent field performance. Building farmer trust requires rigorous quality control and certification, increasing production costs and operational complexity for market participants.

Emerging Market Trends

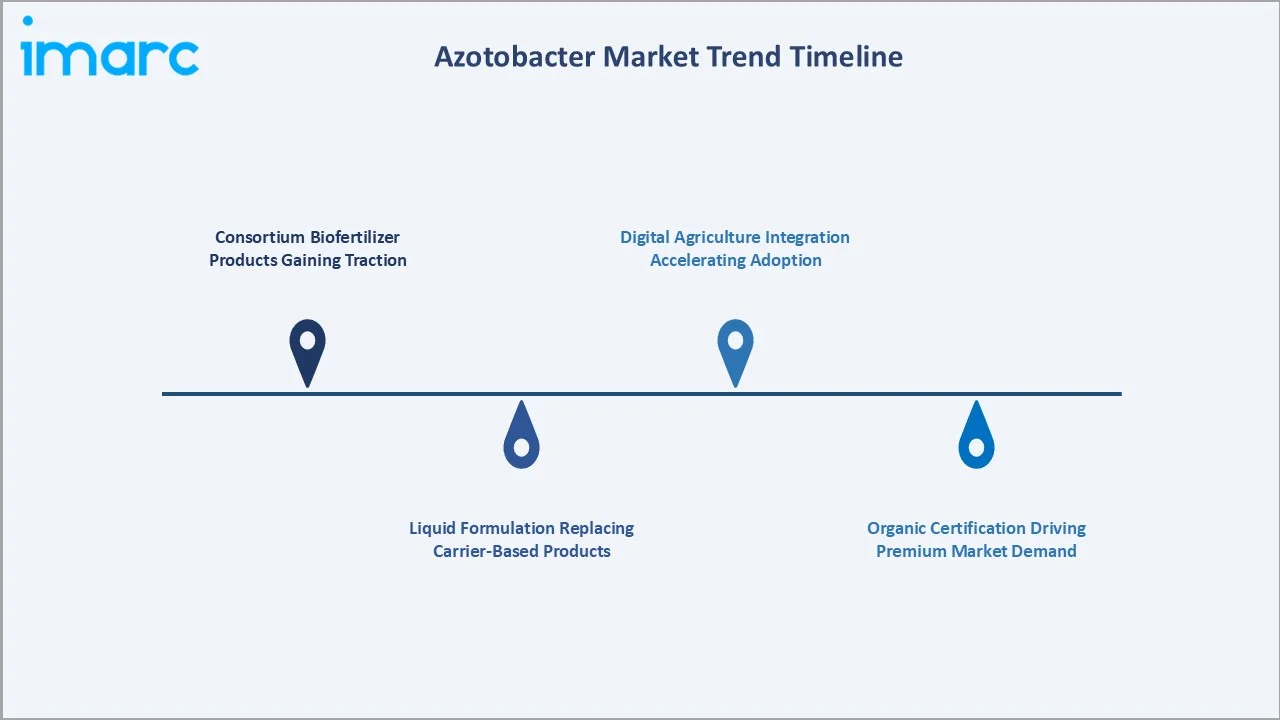

1. Consortium Biofertilizer Products Gaining Traction

Azotobacter combined with phosphate-solubilizing bacteria or mycorrhizal fungi is gaining commercial acceptance. Multi-microbial consortia offer farmers comprehensive soil nutrition management, improving overall crop productivity and creating premium product opportunities for manufacturers with advanced fermentation capabilities.

2. Liquid Formulation Replacing Carrier-Based Products

Liquid azotobacter formulations are displacing carrier-based products due to longer shelf life, easier application, and compatibility with irrigation systems. The liquid format enables seed coating and fertigation, expanding addressable markets in precision agriculture and large-scale commercial farming operations.

3. Organic Certification Driving Premium Market Demand

Growing consumer demand for organically certified food creates a premium pricing environment for azotobacter-enhanced produce. Farmers targeting organic certification adopt azotobacter as a mandatory biofertilizer input, creating a structurally growing demand segment unaffected by commodity price cycles.

4. Digital Agriculture Integration Accelerating Adoption

Precision agriculture platforms are integrating biofertilizer application recommendations into digital farm management systems. AI-driven soil health monitoring enables targeted azotobacter application, improving efficacy and reducing waste across Asia Pacific and North America commercial farming operations.

Industry Value Chain Analysis

The azotobacter value chain integrates raw material and culture sourcing, fermentation and biomass production, formulation and quality control, packaging and storage, distribution, and end-use application. Vertically integrated manufacturers capture fermentation and formulation stages for cost and quality advantages.

|

Stage |

Key Activities |

|

Raw Material & Culture Sourcing |

Procurement of growth media, peat, lignite or vermiculite carriers, and azotobacter culture strains for biofertilizer production |

|

Fermentation & Biomass Production |

Large-scale fermentation of azotobacter cultures to produce high-density microbial biomass with consistent nitrogen-fixing activity |

|

Formulation & Quality Control |

Blending cultures with carriers or suspending in liquid media; conducting viability testing and certifying product potency and shelf life |

|

Packaging & Storage |

Filling into pouches, bottles, or bags under controlled conditions to maintain bacterial viability during transit and warehousing |

|

Distribution & Marketing |

Supply through distributors, agricultural cooperatives, and direct farm service channels across rural markets and online agri-platforms |

|

End-Use Application |

Farmer application via seed treatment, soil drenching, or foliar spray for nitrogen fixation benefits across row, cash, and horticultural crops |

Technology Landscape in the Azotobacter Industry

Carrier-Based Biofertilizer Technology

Carrier-based azotobacter formulations using peat, lignite, or vermiculite provide an established, cost-effective delivery medium for smallholder farmers across price-sensitive emerging markets globally.

Liquid Biofertilizer Technology

Liquid azotobacter formulations offer extended shelf life, higher microbial density, and compatibility with irrigation and seed-treatment equipment, driving progressive replacement of carrier-based products in commercial farming.

Nano-Encapsulation and Controlled-Release Technology

Emerging nano-encapsulation technologies improve azotobacter viability under field conditions, protecting bacteria from UV radiation and heat. Controlled-release formulations enable sustained nitrogen-fixing activity throughout the crop growth cycle.

Market Segmentation Analysis

The report includes the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Crop Type |

Row Crops |

38.6% |

2025 |

|

Region |

Asia Pacific |

35.9% |

2025 |

By Crop Type

Row Crops lead at 38.6% in 2025, encompassing the largest cultivated area globally including cereals such as wheat, rice, corn, and soybean. The segment captures the highest biofertilizer procurement volumes driven by large-scale commercial farming operations worldwide.

To access detailed market analysis, Request Sample

Cash Crops at 33.1% represent cotton, sugarcane, tobacco, and oilseed producers increasingly adopting azotobacter to meet sustainability standards and reduce input costs. Horticultural Crops at 28.3% cover fruits and vegetables, where premium organic markets drive biofertilizer premiums.

Regional Market Insights

|

Region |

Share |

Key Market Drivers & Characteristics |

|

Asia Pacific |

35.9% |

Large agricultural base, government biofertilizer subsidies, high crop area under nitrogen-demanding cereals, and growing organic farming movements |

|

North America |

24.7% |

Organic farming expansion, precision agriculture adoption, high-value horticultural markets, and growing consumer demand for organically certified produce |

|

Europe |

21.8% |

EU Farm-to-Fork strategy mandating reduced synthetic fertilizer use, strong organic certification markets, and sustainable agriculture policy framework |

|

Latin America |

10.4% |

Soybean and sugarcane expansion, increasing sustainable agriculture practices, and growing biofertilizer awareness among commercial farmers in Brazil and Argentina |

|

Middle East & Africa |

7.2% |

Soil fertility improvement needs, food security initiatives, government-backed sustainable agriculture programs, and expanding smallholder farmer awareness |

Asia Pacific, at 35.9%, leads through India's government biofertilizer programs and China's expanding organic farming movement. North America, at 24.7%, reflects organic crop area growth and precision biofertilizer application technology adoption.

Europe, at 21.8%, reflects mandatory synthetic nitrogen reduction targets under the EU Green Deal. Latin America, at 10.4%, and MEA, at 7.2%, represent early-stage but structurally growing markets driven by soil health improvement priorities.

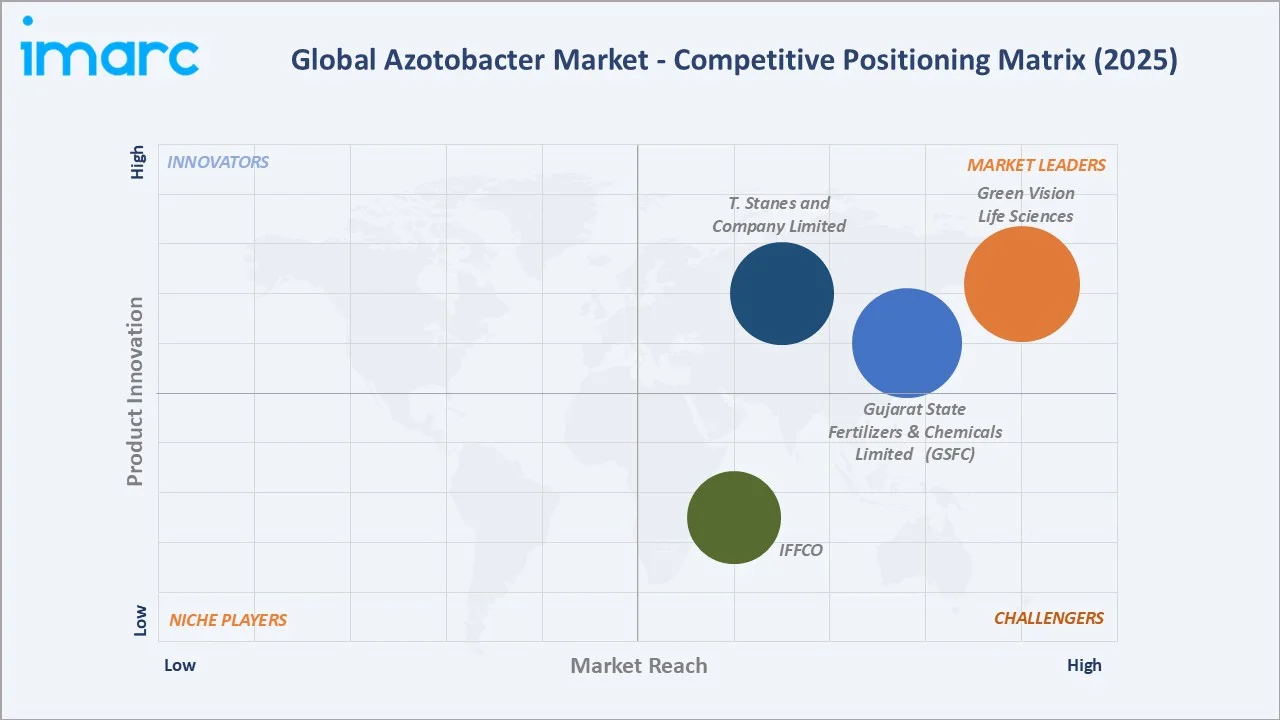

Competitive Landscape

The global azotobacter market is highly fragmented, with the top five companies collectively accounting for approximately 14% of global market revenue. Domestic Indian and multinational biotechnology companies compete across product efficacy, distribution network breadth, and pricing dimensions.

|

Company Name |

Key Products |

Market Position |

Core Strength |

|

Green Vision Life Sciences |

GreenAzospirillum, MicroMix- Biofert Powder, MicroMix- Biofert Liquid |

Market Leader |

Specialises in high-viability liquid and carrier-based azotobacter products with wide crop applicability |

|

Gujarat State Fertilizers & Chemicals Limited (GSFC) |

Azotobacter and Azospirillum |

Market Leader |

State-backed manufacturer with established distribution across India and strong agronomic extension support |

|

T. Stanes and Company Limited |

SYMBION-N |

Leader |

Diversified agri-inputs company with strong biofertilizer brand recognition across multiple crop segments |

|

IFFCO |

Azotobacter |

Strong Challenger |

India's largest fertilizer cooperative |

Key players include Green Vision Life Sciences, Gujarat State Fertilizers & Chemicals Limited (GSFC), T. Stanes and Company Limited, IFFCO, and others.

Key Company Profiles

Green Vision Life Sciences

Green Vision Life Sciences is an India-based biofertilizer manufacturer specialising in azotobacter-based products for row crops, cash crops, and horticultural applications with a strong presence across Indian agricultural markets.

- Key Products: GreenAzospirillum, MicroMix- Biofert Powder, MicroMix- Biofert Liquid

- Strategic Focus: Expanding liquid biofertilizer portfolio and strengthening distribution partnerships with agricultural cooperatives across major crop-producing states in India.

Gujarat State Fertilizers & Chemicals Limited (GSFC)

Gujarat State Fertilizers & Chemicals Limited (GSFC) is a state government-backed integrated fertilizer manufacturer offering azotobacter biofertilizers as part of its sustainable agriculture input portfolio alongside chemical fertilizer products.

- Key Products: Azotobacter and Azospirillum

- Strategic Focus: Targeting smallholder and commercial farmers across western India.

Market Concentration Analysis

The azotobacter market is highly fragmented, with the top five companies collectively accounting for approximately 14% of global volume. Government-owned Indian fertilizer companies hold significant domestic market positions through subsidised distribution, while private and multinational players compete on product efficacy and innovation.

Market concentration is expected to moderately increase through the forecast period as larger biofertilizer companies scale production and pursue acquisitions of regional players. International biotechnology entrants are creating new competitive segments at the premium tier.

Investment & Growth Opportunities

Highest Growth Segments

Row Crops (~8.1% CAGR), Cash Crops (~7.3% CAGR), Asia Pacific (~8.4% CAGR), liquid biofertilizer formulations (~9% CAGR), consortium biofertilizer market (~12% CAGR), and organic certified produce supply chains (~15%+ CAGR) represent the highest-growth investment vectors through 2034.

Emerging Investment Opportunities

Precision fermentation-based azotobacter production represents the market's most capital-efficient emerging opportunity. Government-backed organic farming expansion in India, Brazil, and EU markets creates structurally growing institutional procurement demand through the forecast period.

Investment Themes

- Consortium Biofertilizer Platform Development: Building multi-microbial platforms combining azotobacter with complementary bacteria creates differentiated, premium-priced products capturing organic and precision agriculture market premiums globally.

- Asia Pacific Distribution Infrastructure Investment: Establishing direct farmer outreach, cooperative partnerships, and digital agri-platform integration in India, Vietnam, and Indonesia captures the world's fastest-growing azotobacter unit volume markets.

Future Market Outlook (2026-2034)

The global azotobacter market is projected to grow from USD 382.5 Million in 2025 to USD 750.4 Million by 2034, delivering a 7.54% CAGR. The market anchor of USD 550.2 Million in 2030 represents a biofertilizer sector at its commercial inflection toward mainstream adoption across major global crop production systems.

Three structural forces define market growth: global organic farming area expansion creating self-reinforcing biofertilizer demand; government regulatory pressure reducing synthetic nitrogen use in key agricultural economies; and biotechnology advances creating superior products with broader crop applicability through 2034.

Research Methodology

Primary Research

Primary research comprised structured interviews with 45+ industry stakeholders (2025), including biofertilizer manufacturers, agricultural extension officers, crop scientists, organic farming specialists, and distribution channel partners across key global markets.

Secondary Research

Secondary research encompassed company annual reports; FAO agricultural statistics; India's National Biofertilizer Development Centre reports; USDA organic farming data; EU Farm-to-Fork strategy documentation; and biofertilizer industry conference proceedings. Over 55 secondary sources reviewed.

Forecasting Models

Market revenue forecasts developed using a bottom-up crop area model: (i) global crop area by type; (ii) biofertilizer adoption rate by crop type and region; (iii) average azotobacter product cost per hectare; (iv) technology premium adjustment for liquid versus carrier-based formulations.

Azotobacter Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Crop Types Covered | Cash Crops, Horticultural Crops, Row Crops |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Green Vision Life Sciences, Gujarat State Fertilizers & Chemicals Limited (GSFC), T. Stanes and Company Limited, IFFCO, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the azotobacter market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global azotobacter market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the azotobacter industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Azotobacter Market Report

The global azotobacter market reached USD 382.5 Million in 2025, driven by Row Crops at 38.6%, Asia Pacific at 35.9%, and growing demand for sustainable nitrogen-fixation solutions. Expanding organic farming programs and government biofertilizer subsidies across India, China, and Europe are primary market drivers.

The azotobacter market grows at 7.54% CAGR during 2026-2034, reaching USD 750.4 Million by 2034. This reflects global organic farming expansion, government policy support, biotechnology advances creating superior strains, and progressive substitution of synthetic nitrogen fertilizers.

Row Crops lead at 38.6%, capturing the largest global cultivated area under cereals and grains. This segment benefits from large-scale commercial farming procurement and government programs supporting nitrogen-fixing biofertilizer adoption across wheat, rice, and corn cultivation.

Asia Pacific leads at 35.9% through India's large biofertilizer manufacturing base and government support programs, China's expanding organic farming movement, and high-demand cereal cultivation areas requiring affordable nitrogen supplementation across the region.

Leading companies include Green Vision Life Sciences, Gujarat State Fertilizers & Chemicals Limited (GSFC), T. Stanes and Company Limited, IFFCO, and others.

The azotobacter market is projected to reach approximately USD 550.2 Million by 2030, with liquid formulations becoming the dominant product format, consortium biofertilizers achieving commercial scale, and Asia Pacific maintaining its leadership position through structural demand growth.

Three priority investment opportunities: precision fermentation-based strain development for superior product performance; consortium biofertilizer platform building capturing premium organic market pricing; and Asia Pacific distribution infrastructure investment capturing the world's fastest-growing azotobacter unit volume markets.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)