Baby Drinking Water Market Size, Share, Trends and Forecast by Type, Application, Distribution Channel, and Region 2026-2034

Global Baby Drinking Water Market Size, Share, Trends & Forecast (2026-2034)

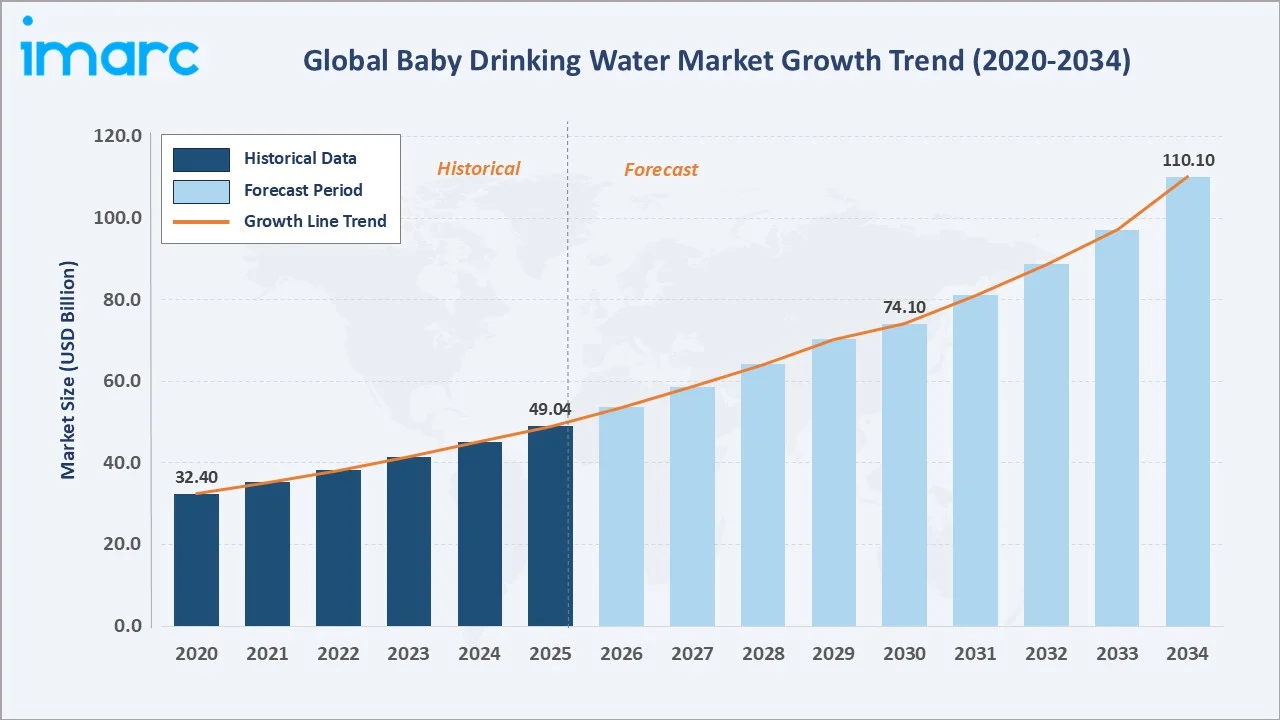

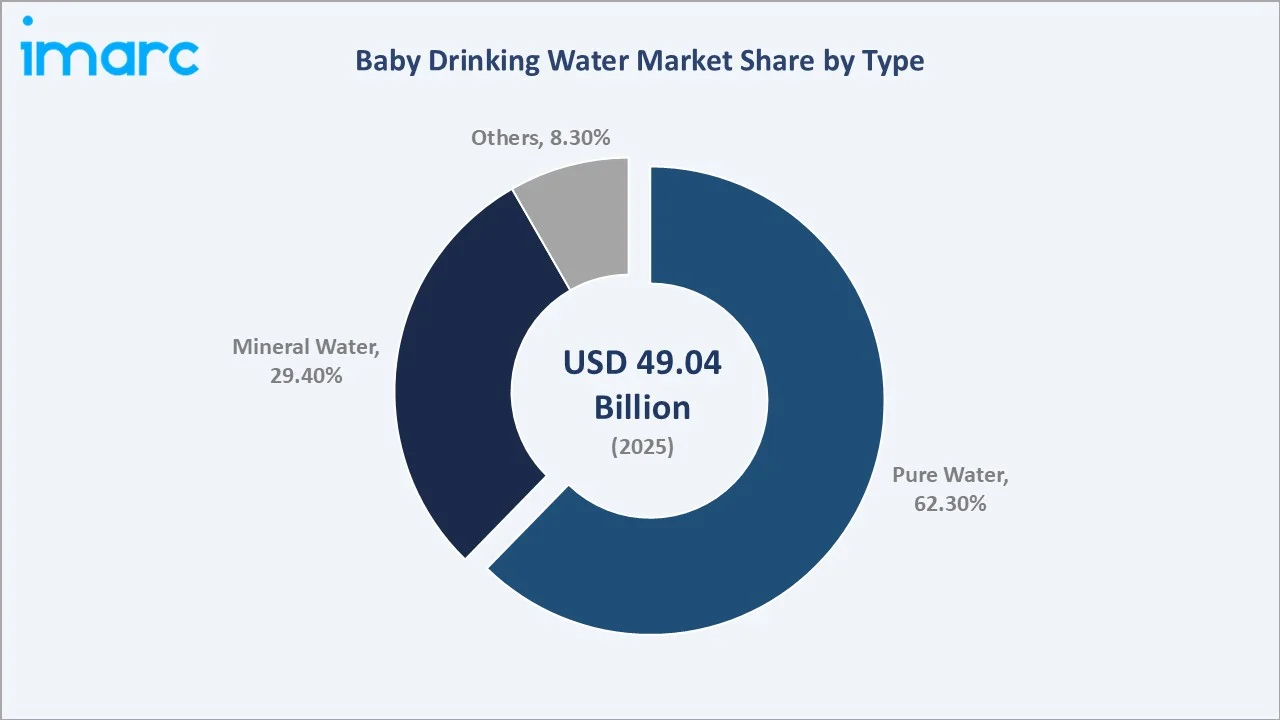

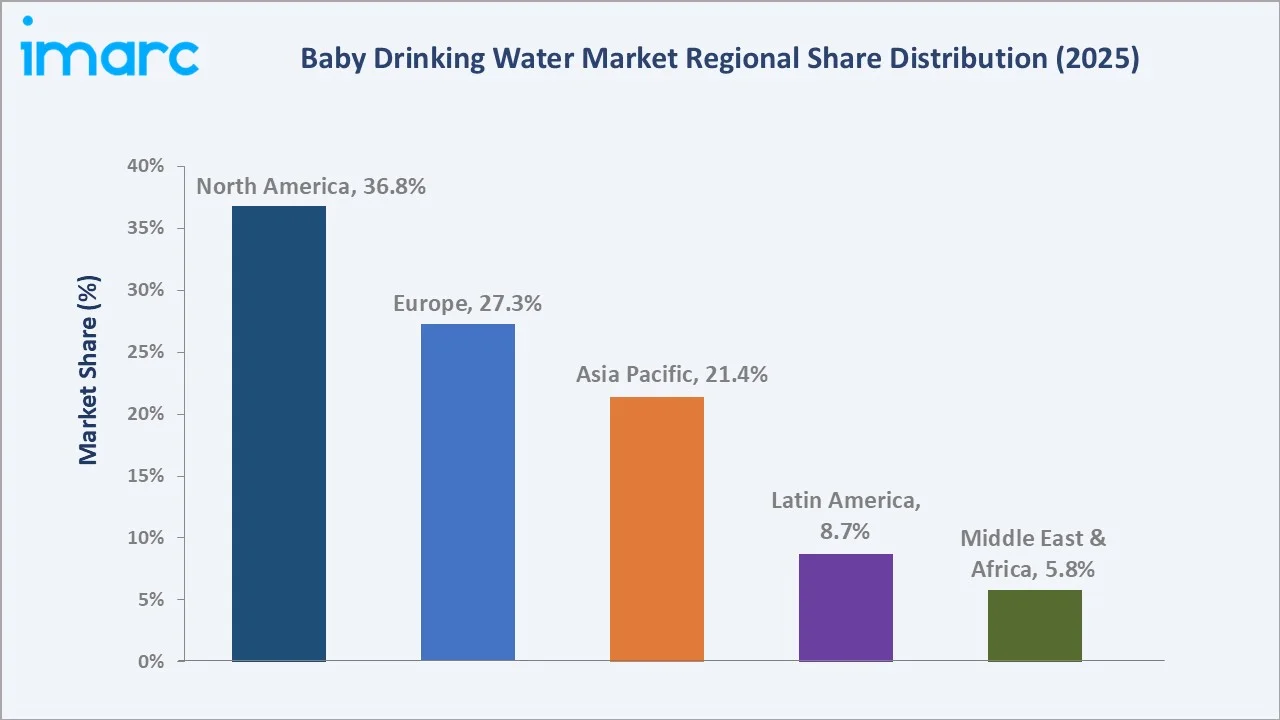

The global baby drinking water market size was valued at USD 49.04 Billion in 2025 and is projected to reach USD 110.10 Billion by 2034, exhibiting a CAGR of 8.62% during 2026-2034. Rising parental awareness of infant health and safety, growing water contamination concerns, and the expansion of supportive government nutrition programs are the primary growth catalysts. Pure water dominates with a 62.3% type share in 2025, while the 12-14 months age bracket leads application segments at 42.7%. North America retains the largest regional share at 36.8%, driven by high consumer health spending and robust infant care infrastructure.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 49.04 Billion |

|

Forecast Market Size (2034) |

USD 110.10 Billion |

|

CAGR (2026-2034) |

8.62% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (36.8%) |

|

Fastest Growing Region |

Asia Pacific |

|

Largest Segment (Type) |

Pure Water (62.3%) |

|

Largest Segment (Application) |

12-14 Months (42.7%) |

To get more information on this market, Request Sample

The global baby drinking water market growth trajectory reflects consistent historical expansion from 2020 through 2025, followed by accelerating forecast growth through 2034. Increasing urbanization, rising disposable incomes in emerging economies, and growing e-commerce penetration are reinforcing demand across all geographic segments.

Executive Summary

The global baby drinking water market is undergoing robust expansion driven by heightened parental concern for infant safety, deteriorating municipal water quality in numerous regions, and rapid premiumization across product offerings. Baby drinking water undergoes multi-stage purification - including reverse osmosis, distillation, and ozonation - to eliminate contaminants such as lead, excess fluoride, nitrates, and pathogenic microorganisms. It is used for formula preparation, medication administration, and supplemental infant hydration from 3 months onward.

Pure water commands a dominant 62.3% type share in 2025, reflecting pediatric guidelines recommending low-sodium and fluoride-controlled hydration in the critical first year. The 12-14 months application segment leads at 42.7%, driven by WHO dietary guidance endorsing water as a supplemental beverage at this developmental milestone.

North America retains its 36.8% regional dominance, supported by institutional nutrition programs and high consumer health spending. Asia Pacific, at 21.4% in 2025, is the fastest-growing region, fueled by rising birth rates, rapid urbanization, and expanding middle-class incomes in China, India, and Southeast Asia.

Key Market Insights

|

Insight |

Data |

|

Largest Segment (Type) |

Pure Water - 62.3% share (2025) |

|

Largest Segment (Application) |

12-14 Months - 42.7% share (2025) |

|

Leading Region |

North America - 36.8% share (2025) |

|

Fastest Growing Region |

Asia Pacific - rising birth rates and urbanization |

|

Top Companies |

Danone, Nongfu Spring, Nursery Water |

|

Market Opportunity |

Emerging markets in India, Indonesia, and Brazil are driving the next growth wave |

Key Analytical Observations Supporting the Above Data:

- Pure water's 62.3% dominance in 2025 reflects pediatric guidelines across North America and Europe consistently recommending low-sodium, fluoride-controlled infant hydration. Reverse osmosis and multi-stage filtration ensure contaminant removal to parts-per-billion levels.

- The 12-14 months segment at 42.7% aligns with WHO dietary guidance on introducing supplemental water around the first birthday, as maturing renal function makes babies better equipped to safely consume water at this stage.

- North America's 36.8% global share reflects high per-capita healthcare spending, strong pharmacy distribution infrastructure, and the structural support of the U.S. WIC program which served approximately 6.7 million participants in fiscal year 2024.

- Asia Pacific is the fastest-growing region, driven by large infant population growth in India and Indonesia, rising urban middle-class incomes, and rapidly expanding e-commerce platforms that improve product accessibility beyond traditional retail.

Global Baby Drinking Water Market Overview

Baby drinking water is a specialized segment of the bottled water industry, purpose-engineered for the unique physiological needs of infants and toddlers aged 0-36 months. Unlike standard bottled water, it undergoes additional multi-stage treatment to achieve a precise mineral balance, eliminating pathogens, heavy metals, excess fluoride, and nitrates that could compromise developing immune and renal systems.

Applications span formula preparation, medication dilution, cereal mixing, and supplemental drinking. The ecosystem encompasses spring water source operators, advanced purification technology providers, sustainable packaging manufacturers, cold-chain logistics operators, pharmacy chains, supermarkets, and e-commerce platforms. Macroeconomic enablers include global birth rates, rising female workforce participation, and growing household disposable incomes in emerging economies.

Regulatory frameworks are a critical structural element. Bodies, including the U.S. FDA, EU EFSA, India FSSAI, and China CFDA impose stringent mineral content, fluoride level, and labelling standards, raising entry barriers and reinforcing quality differentiation for established brands.

Market Dynamics

To evaluate market opportunities, Request Sample

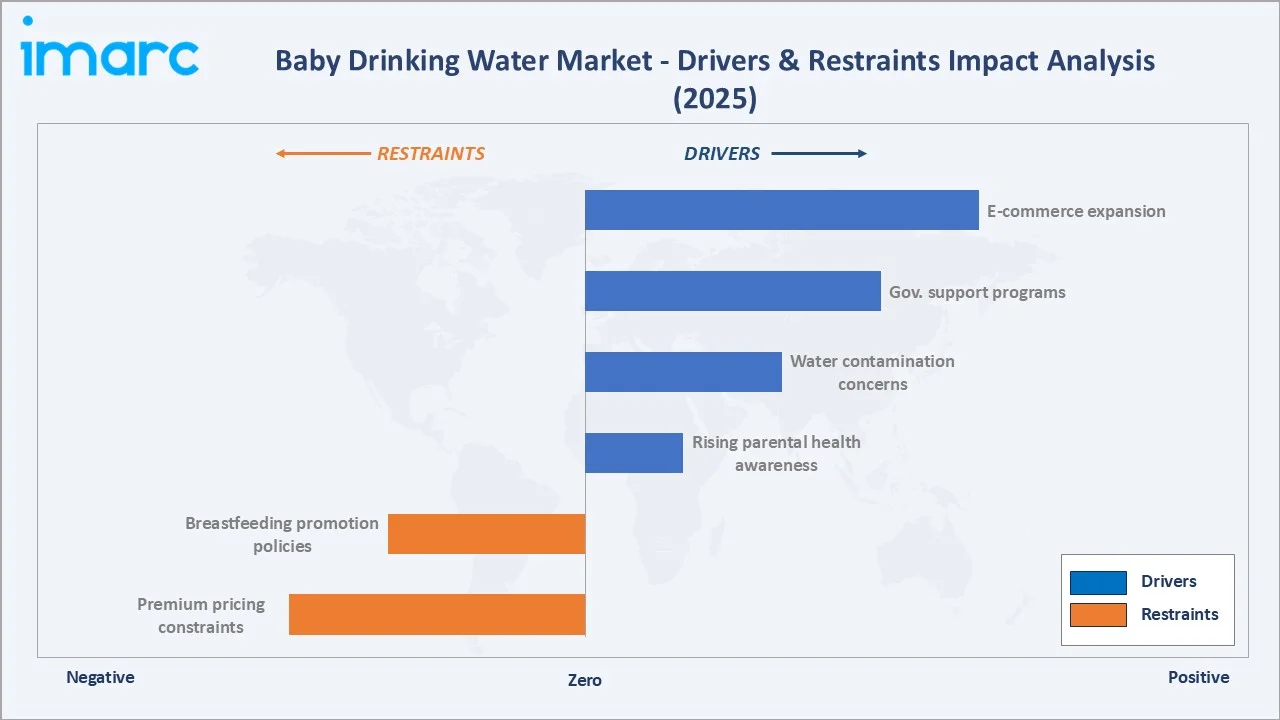

Market Drivers

- Rising Parental Health Awareness: Growing knowledge of waterborne risks and pediatric nutrition guidelines is the primary market catalyst. Parents increasingly prefer certified pure or mineral baby water over tap water for formula mixing. The National Toxicology Program's August 2024 review linking fluoride exposure above 1.5 mg/L to lower IQ in children has further intensified demand for fluoride-controlled infant water options globally.

- Water Contamination Concerns: WHO estimates diarrheal disease caused by contaminated water accounts for approximately 395,000 annual deaths in children under five globally, compelling parents to invest in specialized purified infant water products that guarantee pathogen-free, contaminant-controlled hydration.

- Government Nutrition Programs: The U.S. Special Supplemental Nutrition Program for Women, Infants, and Children (WIC), EU child nutrition initiatives, and analogous programs in India and Brazil promote infant nutritional health, creating both awareness and demand subsidies that underpin market growth.

- E-Commerce and Digital Retail Expansion: Subscription models on platforms such as Amazon Subscribe & Save and JD.com's auto-replenishment enable parents to access baby water conveniently. Online baby care categories recorded double-digit growth rates in 2024 across North America and the Asia Pacific.

Market Restraints

- Premium Pricing Constraints: Baby drinking water commands significant price premiums over standard tap water, limiting market penetration in low- and middle-income households across Sub-Saharan Africa, South Asia, and rural Latin America, where affordability is a primary purchase barrier.

- Breastfeeding Promotion Policies: WHO and UNICEF guidelines recommending exclusive breastfeeding for the first six months restrict market opportunity in the 0-6 months age bracket, particularly in countries with strong institutional compliance and organized public health infrastructure.

Market Opportunities

- Emerging Market Penetration: Rising urban middle-class populations in India, Indonesia, Nigeria, and Brazil represent underserved yet high-potential markets. Growing income levels and increasing health awareness are creating favourable conditions for premium infant water adoption through both organized retail and e-commerce channels.

- Sustainable Packaging Innovation: Growing environmental consciousness among millennial and Gen Z parents is creating strong demand for BPA-free, biodegradable, and recyclable packaging. Brands investing in sustainable packaging are differentiating effectively and commanding premium price points in competitive retail environments.

Market Challenges

- Regulatory Complexity: Varying national standards for mineral content, fluoride levels, and bottled water labelling across more than 195 countries create compliance complexity and significantly increase time-to-market for new product launches by international brands.

- Intense Competitive Pricing Pressure: The presence of numerous local and regional brands, particularly in the Asia Pacific, creates significant pricing pressure that challenges international players seeking to maintain premium brand positioning while expanding into emerging market geographies.

Emerging Market Trends

1. Premiumization and Clean-Label Baby Water Demand

Parents are gravitating toward premium baby water products characterized by clean labels, certified mineral composition, and transparent sourcing. Third-party purity certifications and natural spring sourcing are gaining market share, particularly in North America and Western Europe, where consumers exhibit a high willingness to pay for quality-assured infant nutrition products. Clean-label claims are becoming a primary differentiator in pharmacy and premium supermarket channels.

2. Sustainable and Eco-Friendly Packaging Adoption

EU plastic packaging regulations and growing global environmental consciousness are accelerating the shift toward recyclable and biodegradable baby water packaging. Brands adopting plant-based plastics, glass alternatives, and refillable packaging formats are capturing premium market segments. This trend is simultaneously reducing carbon footprints and serving as a key brand differentiator in competitive retail environments, particularly among environmentally-conscious millennial parents.

3. E-Commerce and Subscription Model Growth

Digital retail is fundamentally reshaping baby drinking water distribution. Subscription-based auto-delivery models are popular among working parents, offering convenience and reliability. Subscription-based purchasing models—such as Amazon’s Subscribe & Save in North America and similar offerings on JD.com and Shopee—are seeing strong consumer adoption in the baby care segment. These models help reduce purchase friction while improving customer convenience and strengthening brand retention.

4. Mineral-Enhanced Functional Baby Water

Manufacturers are introducing mineral-enriched baby water formulations providing specific benefits - low sodium for kidney development, balanced calcium for bone health, and controlled fluoride levels for dental safety. These functional variants command higher price points and address specific paediatric nutrition gaps, reflecting the broader personalized nutrition trend. The segment is particularly strong in European markets with an established mineral water culture.

5. Influencer Marketing and Digital Parenting Communities

Social media platforms and parenting blogs are becoming critical marketing channels for baby drinking water brands. Paediatric influencers, mommy bloggers, and healthcare professionals' endorsements on Instagram, YouTube, and TikTok are directly influencing purchase decisions among first-time parents. Brands investing in digital content strategies are achieving significantly higher brand recall and product trial rates than traditional advertising approaches, particularly in reaching millennial and Gen Z parent demographics.

Industry Value Chain Analysis

The baby drinking water value chain spans six integrated stages from raw water sourcing through end-consumer use. Each stage adds critical value through purification, safety validation, packaging, and distribution. Manufacturers occupying the purification and bottling stage hold the highest strategic value, as proprietary multi-stage treatment technologies constitute the primary competitive differentiator and regulatory compliance anchor.

|

Stage |

Key Players / Examples |

|

Water Sourcing |

Natural spring operators, groundwater extraction firms, municipal utilities |

|

Purification & Treatment |

Reverse osmosis tech providers, multi-stage filtration equipment manufacturers |

|

Bottling & Packaging |

PET bottle manufacturers, eco-packaging suppliers, labelling and sealing units |

|

Quality & Compliance |

Third-party testing labs, FDA, EFSA, FSSAI, codex-certified bodies |

|

Distribution & Logistics |

3PL operators, cold-chain logistics, e-commerce fulfilment centres |

|

Retail & End Users |

Pharmacies, supermarkets, baby specialty stores, online marketplaces |

The certification and compliance stage is increasingly significant, as regulatory bodies in North America (FDA), the European Union (EFSA), and the Asia Pacific (FSSAI in India, CFDA in China) impose stringent standards. Companies with pre-established regulatory expertise hold meaningful time-to-market and market access advantages over new entrants. Distribution channel partnerships with pharmacy chains represent the most trusted retail positioning for infant-specific water products.

Technology Landscape in the Baby Drinking Water Industry

Purification Technology: Reverse Osmosis, Distillation, and Ozonation

Reverse osmosis (RO) is the dominant purification method, removing 95-99% of contaminants including heavy metals, nitrates, and pathogenic microorganisms. Multi-stage RO combined with activated carbon filtration and UV sterilization represents the industry standard. Ozonation - the injection of ozone gas - provides chemical-free disinfection and extended shelf life without chlorine residues. Nursery Water, for example, applies reverse osmosis and/or distillation combined with ozonation for its flagship purified baby water range.

Sustainable Packaging Innovation

Packaging technology is evolving rapidly in response to regulatory pressure and consumer demand. BPA-free polypropylene bottles, rPET (recycled PET) materials, and plant-based bio-plastics are entering commercial-scale production. European brands are trialing glass packaging in premium supermarket channels. Single-serve 10-ounce portion formats are gaining traction for on-the-go convenience, as demonstrated by Nursery Water. EU Packaging and Packaging Waste Regulation (PPWR) is driving mandatory recycled content requirements across the industry.

Digital Commerce and Smart Labelling

QR-code-enabled traceability labels allow parents to verify purification batch data, mineral content, and source information via smartphone in real time. IoT-enabled inventory management in subscription models enables automated re-ordering, reducing stockout risk for time-pressed caregivers. These digital tools are enhancing consumer trust, building brand loyalty, and driving retention in competitive online retail environments where product transparency is a key purchase factor.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Pure Water |

62.3% |

2025 |

|

Application |

12-14 Months |

42.7% |

2025 |

|

Distribution channel |

Offline |

🔒 |

2025 |

|

Region |

North America |

36.8% |

2025 |

By Type

Pure water commands a dominant 62.3% majority share in 2025, reflecting widespread alignment with paediatric guidelines for low-sodium and fluoride-controlled infant hydration. Multi-stage reverse osmosis and distillation processes ensure contaminant removal to parts-per-billion levels, providing parents with maximum safety assurance for formula preparation and supplemental drinking.

To access detailed market analysis, Request Sample

Mineral water holds a 29.4% share in 2025 and is growing at an above-average rate. Naturally sourced mineral water containing balanced calcium, magnesium, and potassium appeals to parents seeking naturally occurring nutrients to supplement infant formula.

By Application

The 12-14 months segment leads with a 42.7% application share in 2025. At this developmental stage, WHO guidelines endorse the introduction of water as a supplemental beverage. Maturing renal and immune systems at 12-14 months allow safer water consumption, making this the highest-adoption age bracket. Parents exhibit heightened brand consciousness and quality sensitivity at this stage as children transition from formula to a broader nutritional diet.

The 7-12 months segment holds 33.6% share in 2025, driven by partial water introduction alongside formula during the weaning and solid food phase. The 3-6 months segment at 23.7% covers primarily formula preparation use cases, where purified baby water serves as the precise, contaminant-controlled mixing medium to maintain formula nutritional accuracy and infant safety standards.

Regional Market Insights

North America commands a 36.8% global revenue share in 2025, the most dominant regional position, anchored by the United States mature baby care infrastructure and high per-capita consumer health spending. The U.S. WIC program, FDA-enforced quality standards, and strong pharmacy retail network drive consistent demand across premium and value segments.

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

36.8% |

High health awareness, WIC program support, strong pharmacy retail network, and lead contamination concerns in tap water |

|

Europe |

27.3% |

EU food safety regulations, mineral water tradition, rising female workforce participation, and sustainability mandates |

|

Asia Pacific |

21.4% |

Large infant population, rising disposable incomes, rapid urbanization, expanding e-commerce ecosystems |

|

Latin America |

8.7% |

Expanding middle class, urban water quality concerns, and improving organized retail infrastructure |

|

Middle East & Africa |

5.8% |

Limited clean tap water access, high GCC per-capita income, and growing organized retail |

Asia Pacific at 21.4% in 2025 is positioned as the fastest-growing region, driven by China's large infant population, India's expanding middle class, and rapidly growing organized retail and e-commerce ecosystems. Europe's 27.3% share reflects strong EU regulatory frameworks and a deep-rooted mineral water culture.

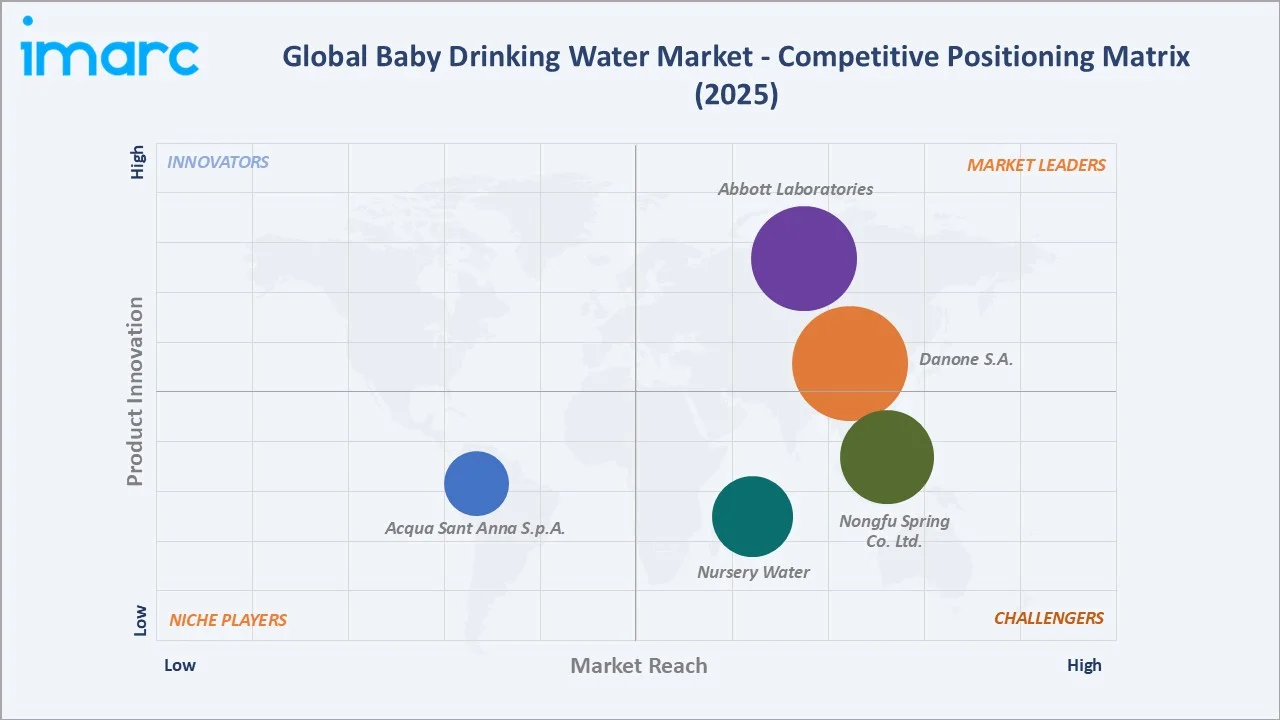

Competitive Landscape

The global baby drinking water competitive landscape is moderately consolidated, with multinational consumer goods corporations holding substantial market share alongside regional specialists. Key competitive dimensions include proprietary purification technology capabilities, paediatric brand endorsement strength, sustainable packaging credentials, distribution network depth, and e-commerce platform integration.

|

Company Name |

Key Brand / Product |

Market Position |

Core Strength |

|

Danone S.A. |

Evian / Volvic Baby Range |

Leader |

Natural mineral water expertise, global distribution, sustainability programs |

|

Nongfu Spring Co. Ltd. |

Nongfu Spring Baby Water |

Challenger |

Asia-Pacific dominance, extensive distribution network, competitive pricing |

|

Nursery Water |

Nursery Purified Water |

Challenger |

75+ years brand heritage, US pharmacy leadership, RO purification standard |

|

Acqua Sant'Anna S.p.A. |

Sant'Anna Baby Water |

Niche Player |

European mineral water quality, premium positioning, BPA-free packaging |

The competitive environment is being disrupted by private-label offerings from major pharmacy chains and supermarkets capturing price-sensitive segments. Simultaneously, premium organic and sustainably sourced baby water brands from Europe are expanding into North American and Asia Pacific markets through digital retail channels, intensifying competition at the premium tier.

Key Company Profiles

Acqua Sant'Anna S.p.A.

Acqua Sant'Anna is Italy's leading natural mineral water brand, recognized for its commitment to purity, sustainability, and product quality. The brand offers dedicated baby mineral water products specifically formulated with low sodium and balanced mineral content for infant consumption.

- Product & Platform Portfolio: Sant'Anna Baby natural mineral water, low-sodium variants specifically formulated for infants and toddlers, and eco-packaged formats.

- Recent Developments: In May 2023, Acqua Sant'Anna further expanded its mineral water capacity with Krones. This fuels its presence in the market.

- Strategic Focus: Sant'Anna's strategy targets premium mineral water consumers in Europe, emphasizing Alpine natural sourcing, third-party quality certification, and BPA-free packaging sustainability credentials.

Danone S.A.

Danone is a global leader in food and beverages with a dedicated Early Life Nutrition division encompassing infant formula, dairy, and specialized water products. Through its Evian and Volvic brands and dedicated baby hydration lines, Danone serves parents seeking premium naturally sourced infant water across Europe, Asia Pacific, and North America.

- Product & Platform Portfolio: Evian Natural Mineral Water, Volvic baby hydration range, specialized low-sodium infant mineral water formulations.

- Recent Developments: In April 2022, Danone and Compañía Cervecerías Unidas (CCU) announced a strategic alliance, as CCU Argentina has acquired a large minority stake in Aguas Danone de Argentina. This partnership will allow both companies to enrich their its water business and strengthen their operations in the country.

- Strategic Focus: Danone's strategy integrates hydration science, sustainability commitments, and pediatric nutrition expertise, targeting health-conscious parents through premium retail, digital channels, and pediatric healthcare professional partnerships.

Nongfu Spring Co. Ltd.

Nongfu Spring is China's leading beverage company and a dominant force in the Asia Pacific baby drinking water segment. Its dedicated infant water products benefit from extensive distribution across China's retail and e-commerce ecosystems, strong brand recognition, and competitive pricing targeting China's expanding middle-class parent demographic.

- Product & Platform Portfolio: Nongfu Spring Baby Natural Water, fluoride-controlled purified variants for infants and toddlers, bulk and single-serve formats.

- Recent Developments: In July 2019, Nongfu Spring launched the lithium-containing natural mineral water to develop a new concept for commercial drinking water. This adds another layer to the Nongfu Spring bottled water segment after red bottled water, high-end water, baby water, and student water.

- Strategic Focus: Nongfu Spring's strategy leverages its unmatched China distribution infrastructure, competitive pricing discipline, and rapid e-commerce adoption to consolidate its dominant Asia Pacific market position.

Nursery Water

Nursery Water is one of the most recognized baby drinking water brands in the United States, with over 75 years of market presence. Products are processed through reverse osmosis and/or distillation, followed by ozonation, producing consistently pure hydration for infants. Nursery Water is widely available in pharmacies, supermarkets, and online platforms.

- Product & Platform Portfolio: Nursery Purified Water (fluoridated and non-fluoridated variants), 10-ounce single-serve portable format, 1-gallon family formats.

- Recent Developments: Nursery Water offers a new 10-ounce single-serve format nationwide across Target, Walmart, and Amazon, specifically targeting on-the-go parents and formula preparation convenience.

- Strategic Focus: Nursery Water focuses on reinforcing its 75-year heritage brand equity through paediatric endorsements, pharmacy distribution leadership, and expanding into convenient portable packaging formats for modern active parent lifestyles.

Market Concentration Analysis

The global baby drinking water market exhibits moderate concentration, with the top four players - Danone, Nongfu Spring, Nursery Water, and Acqua Sant'Anna - collectively commanding approximately 45-55% of global revenue in 2025. The remaining market is served by regional and private-label brands, particularly in Asia Pacific and Latin America.

Investment & Growth Opportunities

Fastest-Growing Segments

Mineral water for the 7-12 months application bracket is the highest-growth sub-segment, expanding at above-average CAGR, driven by rising parental awareness of naturally occurring minerals for infant development during the critical weaning period. Premium organic and naturally sourced spring water products are experiencing particularly strong demand from health-conscious parents in North America and Western Europe seeking clean-label alternatives.

Emerging Market Expansion

India, Indonesia, Brazil, and Nigeria represent the most attractive emerging market opportunities, where rapidly expanding urban middle-class populations, rising birth rates, and growing awareness of water quality risks are creating favourable conditions for market entry. E-commerce-first market entry strategies are particularly suited to these geographies where digital penetration is outpacing physical retail expansion, enabling brands to reach health-conscious urban parents directly.

Venture & Private Investment Trends

Sustainability-focused baby water brands with certified organic sourcing, biodegradable packaging, and carbon-neutral production processes are attracting venture capital attention across the sector. Strategic M&A activity is expected to accelerate as major FMCG groups seek to acquire premium specialty baby water brands to strengthen infant nutrition portfolios. Packaging technology companies enabling smart labelling and QR-code traceability are also attracting increased investment as digital transparency becomes a key consumer demand.

Future Market Outlook (2026-2034)

The global baby drinking water market forecast projects steady value expansion from USD 49.04 Billion in 2025 to USD 110.1 Billion by 2034 at a CAGR of 8.62%, driven by structural demand tailwinds including population growth in key emerging markets, persistent water quality concerns globally, and rising health consciousness among younger parent demographics.

Three macro trends are most likely to reshape the market through 2034. First, sustainability mandates will drive packaging transformation, with the EU's Packaging and Packaging Waste Regulation (PPWR) setting mandatory recycled content requirements that will push industry-wide innovation. Second, digital retail expansion will redefine distribution economics, enabling smaller premium brands to compete nationally without heavy physical retail investment.

Third, functional and personalized baby water - featuring age-specific mineral profiles, microbiome-supporting additions, and clean-label certifications - will capture premium pricing and drive category premiumization. By 2034, the baby drinking water industry is forecast to have completed its transformation from a commodity-adjacent category to a premium, highly differentiated infant nutrition segment.

Research Methodology

Primary Research

Primary research encompassed structured interviews with paediatric nutrition specialists, baby care retail buyers, distribution channel managers, and product development executives from leading baby drinking water manufacturers. Insights from regional market participants across North America, Europe, Asia Pacific, and Latin America were incorporated to validate growth drivers, competitive positioning, and consumer preference data through direct industry engagement.

Secondary Research

Secondary sources include World Health Organization child nutrition guidelines, U.S. FDA bottled water regulations, European Food Safety Authority (EFSA) mineral water standards, World Bank fertility rate data, USDA WIC program participation statistics from fiscal year 2024, and industry publications from the International Bottled Water Association (IBWA). E-commerce sales data from Amazon and regional platforms supplemented distribution channel analysis.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, calibrated against historical CAGR trends, macroeconomic growth indicators, infant population projections, and regulatory environment assessments. Sensitivity analysis was applied to key assumptions including birth rate variability and e-commerce penetration scenarios across regions.

Baby Drinking Water Market Report Coverage:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Pure Water, Mineral Water, Others |

| Applications Covered | 3-6 Months, 7-12 Months, 12-14 Months |

| Distribution Channels Covered | Online, Offline |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Danone S.A., Nongfu Spring Co. Ltd., Nursery Water, Acqua Sant'Anna S.p.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the baby drinking water market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global baby drinking water market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the baby drinking water industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Baby Drinking Water Market Report

The global baby drinking water market was valued at USD 49.04 Billion in 2025, driven by rising parental health consciousness, water contamination concerns, and government infant nutrition support programs.

The market is projected to reach USD 110.1 Billion by 2034, growing at a CAGR of 8.62% during 2026-2034, driven by e-commerce expansion, emerging market penetration, and sustainable packaging innovation.

Pure water leads with a 62.3% share in 2025, driven by pediatric recommendations for low-sodium and fluoride-controlled infant hydration, particularly for formula preparation and supplemental drinking.

The 12-14 months segment dominates at 42.7% in 2025, aligned with WHO guidance endorsing water introduction at the 12-month milestone as infants' renal and immune systems mature sufficiently.

North America leads with 36.8% share in 2025, driven by high consumer health spending, strong pharmacy retail infrastructure, and institutional support from the U.S. WIC nutrition program.

Key drivers include rising parental awareness of water safety, WHO-reported waterborne disease risks to children, advanced purification technology adoption, government nutrition programs, and rapid e-commerce penetration globally.

Asia Pacific is the fastest-growing region, driven by large infant populations in China and India, rising middle-class incomes, rapid urbanization, and expanding e-commerce distribution infrastructure.

Leading companies include Danone S.A., Nongfu Spring Co. Ltd., Nursery Water, and Acqua Sant'Anna S.p.A., competing on purification technology, brand trust, and distribution reach.

E-commerce enables broad product accessibility, subscription-based auto-delivery, and transparent product information. Online baby care categories are growing at double-digit annual rates in North America and Asia Pacific.

Pure water is multi-stage purified to remove virtually all minerals and contaminants for maximum safety. Mineral water retains naturally occurring calcium and magnesium in balanced amounts beneficial for infant development.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)