Basalt Fiber Market Size, Share, Trends and Forecast by Product, Type, Form, Method, End Use Industry, and Region 2026-2034

Global Basalt Fiber Market Size, Share, Trends & Forecast (2026-2034)

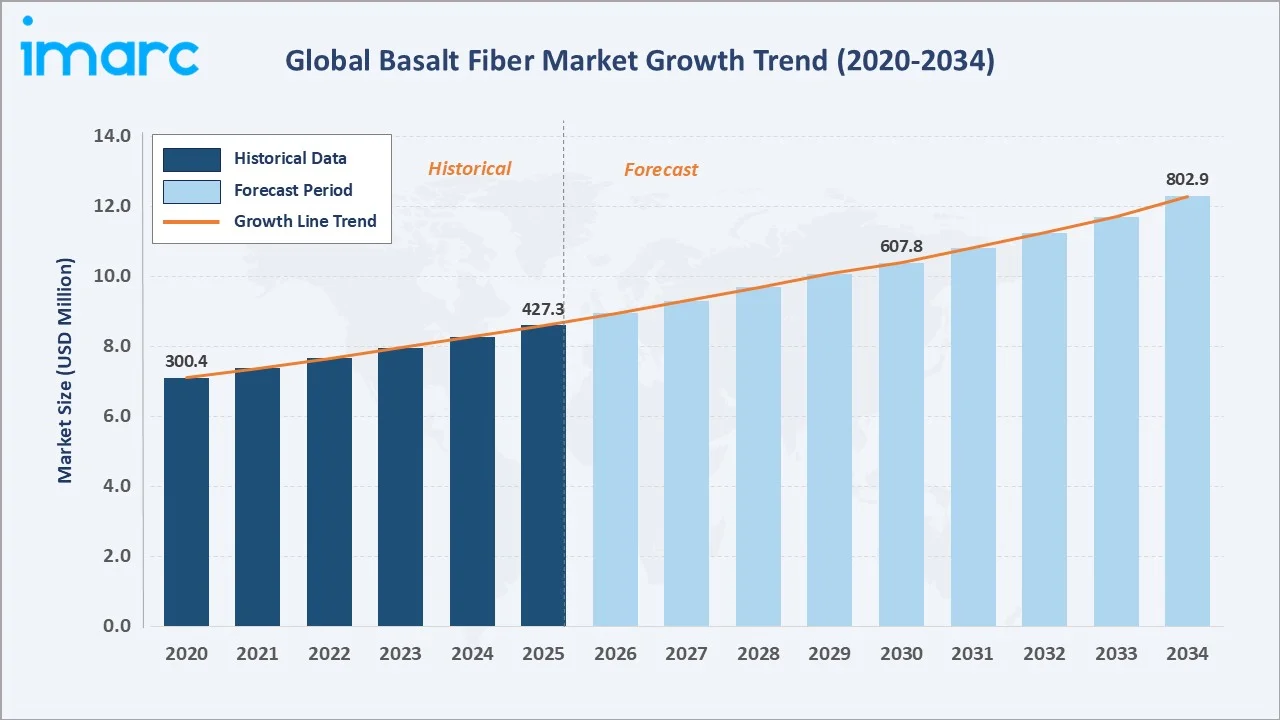

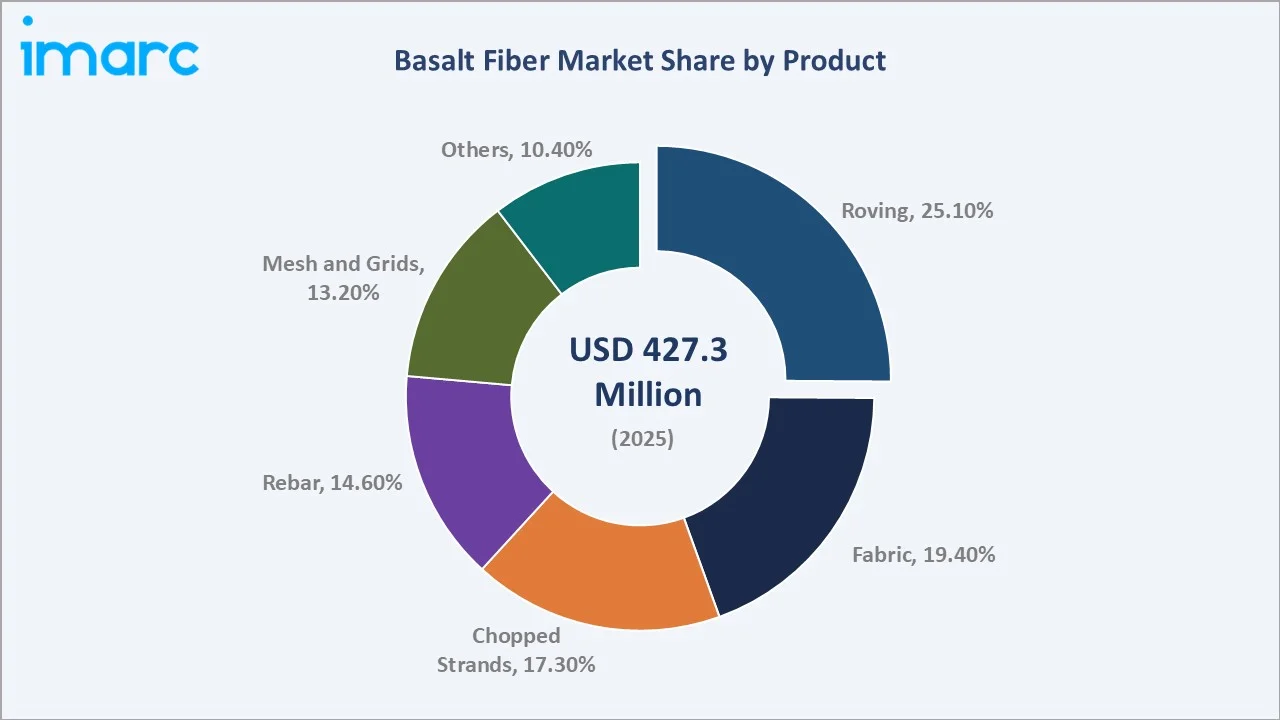

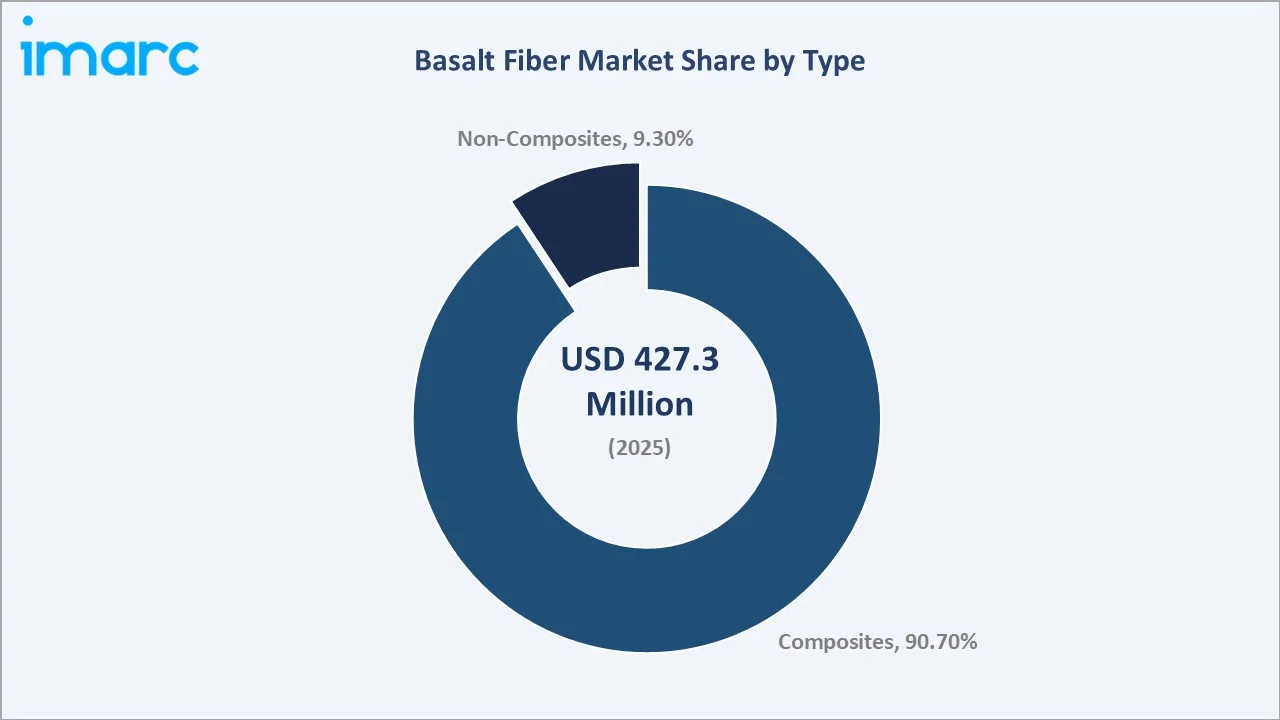

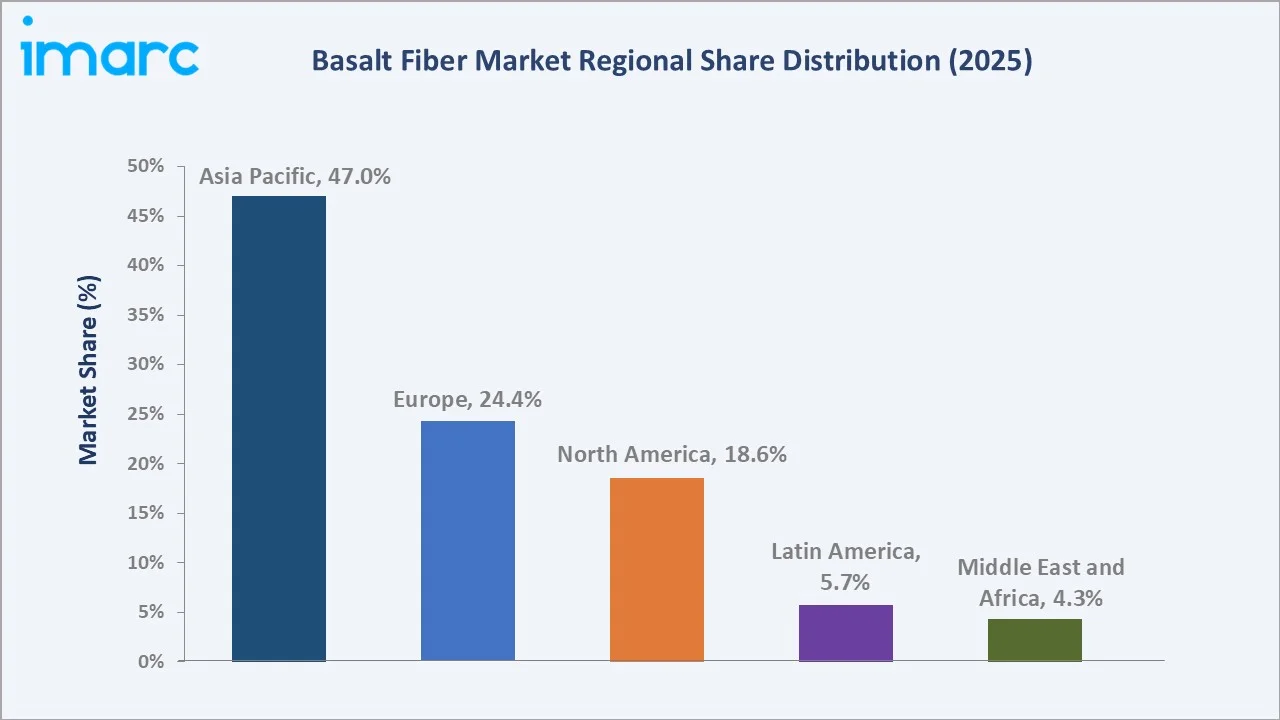

The global basalt fiber market size was valued at USD 427.3 Million in 2025 and is projected to reach USD 802.9 Million by 2034, exhibiting a CAGR of 7.3% during the forecast period 2026-2034. Escalating demand for lightweight, corrosion-resistant, and eco-friendly reinforcement materials across construction, automotive, aerospace, and renewable energy sectors is driving the basalt fiber market growth. Roving leads the product segment at 25.1% in 2025, while composites dominate the type segment at 90.7%. Asia Pacific accounts for 47.0% of global revenue in 2025, the world's largest regional market.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 427.3 Million |

|

Forecast Market Size (2034) |

USD 802.9 Million |

|

CAGR (2026-2034) |

7.3% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Asia Pacific (47.0% share, 2025) |

|

Fastest Growing Segment |

Non-Composites (~10.3% CAGR) |

|

Leading Product Segment |

Roving (25.1%, 2025) |

|

Leading Type Segment |

Composites (90.7%, 2025) |

The global basalt fiber market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by rising infrastructure investment, automotive lightweighting mandates, wind energy deployments, and growing preference for sustainable composite reinforcement materials.

To get more information on this market, Request Sample

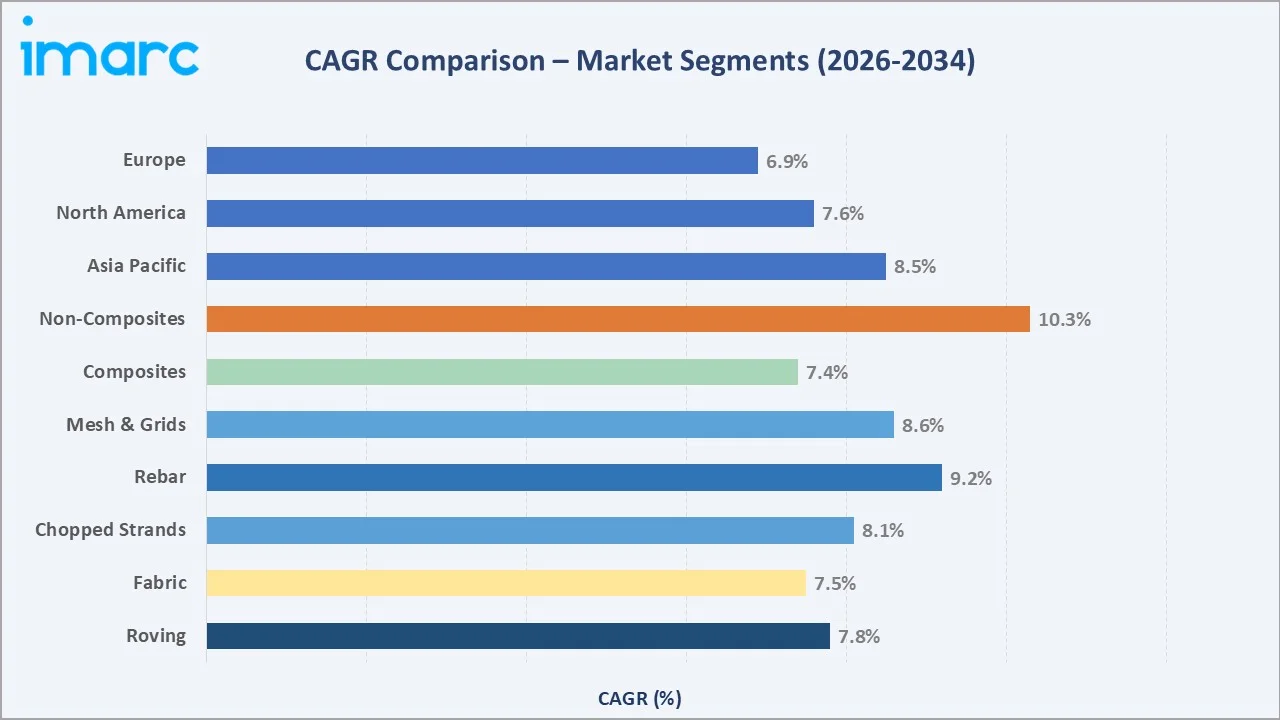

Segment-level CAGR comparisons highlighting non-composites and rebar as the two fastest-growing sub-categories within the global basalt fiber market analysis through 2034.

Executive Summary

The global basalt fiber market is undergoing a broad-based demand expansion driven by the convergence of infrastructure investment cycles, sustainability mandates, and industrial lightweighting requirements. Valued at USD 427.3 Million in 2025, the market is forecast to reach USD 802.9 Million by 2034 at a CAGR of 7.3%. Wind energy OEMs integrated basalt fiber into 23% of wind turbine blade production in Germany in 2024, up from 16% in 2023, underscoring accelerating adoption in renewable energy infrastructure. Each wind turbine deployment demands high-performance, corrosion-immune reinforcement materials capable of withstanding decades of marine and climatic extremes.

Roving commands the dominant product share at 25.1% in 2025, driven by its extensive utility in high-performance composite fabrication across wind energy, automotive, marine, and aerospace applications. Composites overwhelmingly dominate the type segment at 90.7% in 2025, reflecting basalt fiber's primary role as structural reinforcement in epoxy and vinyl-ester matrix systems. Basalt rebar demonstrates tensile strengths of 800–1,200 MPa with triple the corrosion resistance of conventional steel, enabling century-long service life in chloride-rich infrastructure environments.

Asia Pacific dominates with a 47.0% global revenue share in 2025, led by China's large-scale infrastructure programs, domestic manufacturing base, and wind energy expansion, alongside India's rapidly growing construction sector. Europe holds 24.4% in 2025, anchored by EU Net-Zero Industry Act mandates and EN 13706 code recognition of basalt composites. North America accounts for 18.6%, driven by a confirmed 15% year-over-year increase in US basalt fiber imports in 2025 attributable to automotive lightweighting and federal infrastructure programs.

Key Market Insights

|

Insight |

Data |

|

Largest Product Segment |

Roving – 25.1% share (2025) |

|

Leading Type Segment |

Composites – 90.7% share (2025) |

|

Leading Region |

Asia Pacific – 47.0% revenue share (2025) |

|

Second Region |

Europe – 24.4% revenue share (2025) |

|

Top Companies |

Kamenny Vek, MAFIC SA, Technobasalt-Invest, Deutsche Basalt Faser |

Key Analytical Observations Supporting The Above Data:

- Roving's 25.1% dominance in 2025 reflects its wide-ranging utility across composite fabrication in wind energy, automotive, marine, and aerospace applications, enabled by superior tensile strength, flexibility, and broad process compatibility.

- Composites constitute 90.7% of basalt fiber demand in 2025, driven by epoxy and vinyl-ester laminates dominating wind, automotive, and marine construction, with interfacial shear strength of ~40 MPa enabling 10–15% weight savings over equivalent glass fiber structures.

- Asia Pacific's 47.0% global dominance in 2025 reflects China's dual role as the world's largest basalt fiber production hub and the most aggressive adopter of basalt composite reinforcement in infrastructure, wind energy, and automotive sectors.

Global Basalt Fiber Market Overview

Basalt fiber is a high-performance continuous or discrete fiber manufactured through controlled melting and drawing of naturally occurring basalt rock at temperatures between 1,400°C and 1,600°C. Unlike glass fiber, basalt fiber requires no additives or blending during production, making it an inherently eco-friendly and cost-effective alternative to conventional reinforcement materials. Its combination of high tensile strength, excellent thermal stability, superior chemical and moisture resistance, and non-corrosive behaviour has established basalt fiber as a preferred reinforcement medium across demanding industrial, construction, and energy applications globally.

Applications span a diverse industrial landscape: structural reinforcement in construction and civil infrastructure, lightweight body panels and battery enclosures in automotive and electric vehicle platforms, turbine blade reinforcement in wind energy, fire containment and thermal insulation in industrial equipment, and hull and deck reinforcement in marine vessels. The material's natural volcanic origin and recyclability align with global sustainability mandates and green building certification requirements.

Macroeconomic enablers include large-scale global infrastructure investment programs, rapid EV proliferation creating structural demand for lightweight structural composites, escalating offshore and onshore wind energy deployment requiring long-life corrosion-resistant blade materials, and tightening emissions regulations incentivizing material substitution across automotive and aerospace supply chains.

Market Dynamics

To evaluate market opportunities, Request Sample

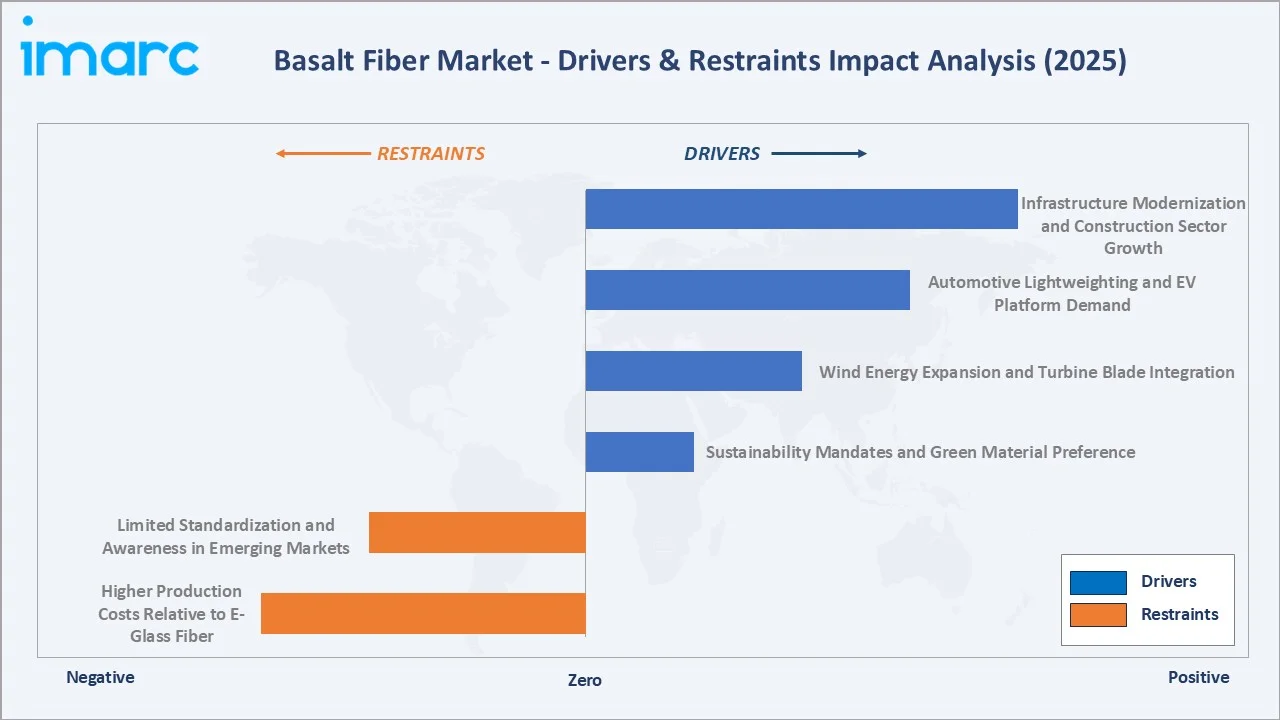

Market Drivers

- Infrastructure Modernization and Construction Sector Growth: Governments and private developers are increasingly specifying basalt fiber-reinforced composites for bridges, tunnels, pavements, and coastal structures. EN 13706 now explicitly references basalt, removing earlier specification barriers. Basalt rebar provides tensile strengths of 800–1,200 MPa and triple the corrosion resistance of steel, enabling a century-long service life in chloride-rich environments.

- Automotive Lightweighting and EV Platform Demand: Automakers are adopting basalt fiber composites for body panels, battery casings, and structural components, achieving 30–50% weight reduction versus steel. EV platforms demand lighter structures to offset battery weight and maximize driving range, creating structural demand for basalt composites. The increasing US basalt fiber imports in 2025 reflect this accelerating demand.

- Wind Energy Expansion and Turbine Blade Integration: Basalt fiber is increasingly being considered for wind turbine blade production due to its high modulus-to-weight ratio, corrosion resistance, and fatigue performance, making it a promising material for spar cap reinforcement in large turbines.

- Sustainability Mandates and Green Material Preference: The EU Net-Zero Industry Act compels project owners to adopt low-GWP reinforcements, placing basalt rebar on specification lists for bridge decks and seawalls. Basalt fiber's recyclability, natural volcanic origin, and minimal additive production process align strongly with global ESG reporting requirements and green building certifications.

Market Restraints

- Higher Production Costs Relative to E-Glass Fiber: Basalt fiber production requires higher melting temperatures and more specialized equipment compared to conventional E-glass, resulting in a price premium that limits adoption in cost-sensitive applications where performance differentiation is not fully specified by engineers.

- Limited Standardization and Awareness in Emerging Markets: While EN 13706 and Florida DOT validations have opened Western markets, many emerging economies lack equivalent code recognition for basalt fiber composites, slowing uptake in public infrastructure procurement and requiring time-consuming independent engineering approval processes.

Market Opportunities

- EV Battery Casing and Thermal Management Applications: Electric vehicle manufacturers are evaluating basalt fiber composites for battery enclosure structures and thermal management panels, where electromagnetic neutrality, fire resistance, and lightweight properties provide distinct advantages. In January 2025, Michelman partnered with FibreCoat to launch AluCoat, an aluminum-coated basalt fiber targeting lightweight conductive material applications.

- Hybrid Fiber Composite Technologies: Combining basalt with carbon or glass fibers creates hybrid reinforcement systems offering tailored strength, modulus, and cost profiles. Growing commercial availability of hybrid prepreg and woven fabric formats is expanding basalt fiber's addressable market beyond standalone applications in sports equipment, marine hull construction, and industrial infrastructure.

- Offshore Wind Energy Scale-Up: Offshore wind projects using 15 MW turbines are increasingly incorporating basalt fiber to withstand extreme temperatures and corrosive environments. Demand for basalt fiber in energy applications is expected to grow rapidly through 2034, making it the fastest-expanding end-use segment, supported by multi-year procurement commitments from global OEMs.

Market Challenges

- Competition from Established E-Glass and Carbon Fiber: Well-entrenched glass fiber supply chains and the cost performance of E-glass in standard composite applications create significant switching barriers. Carbon fiber's superior modulus limits basalt fiber penetration in aerospace structural applications requiring the highest stiffness-to-weight ratios.

- Scaling Manufacturing Capacity: Global basalt fiber production remains concentrated among a limited number of manufacturers in Russia, China, and Europe. Meeting rapidly expanding demand from wind energy and infrastructure sectors requires substantial capital investment in additional melting furnace capacity and fiber drawing technology.

Emerging Market Trends

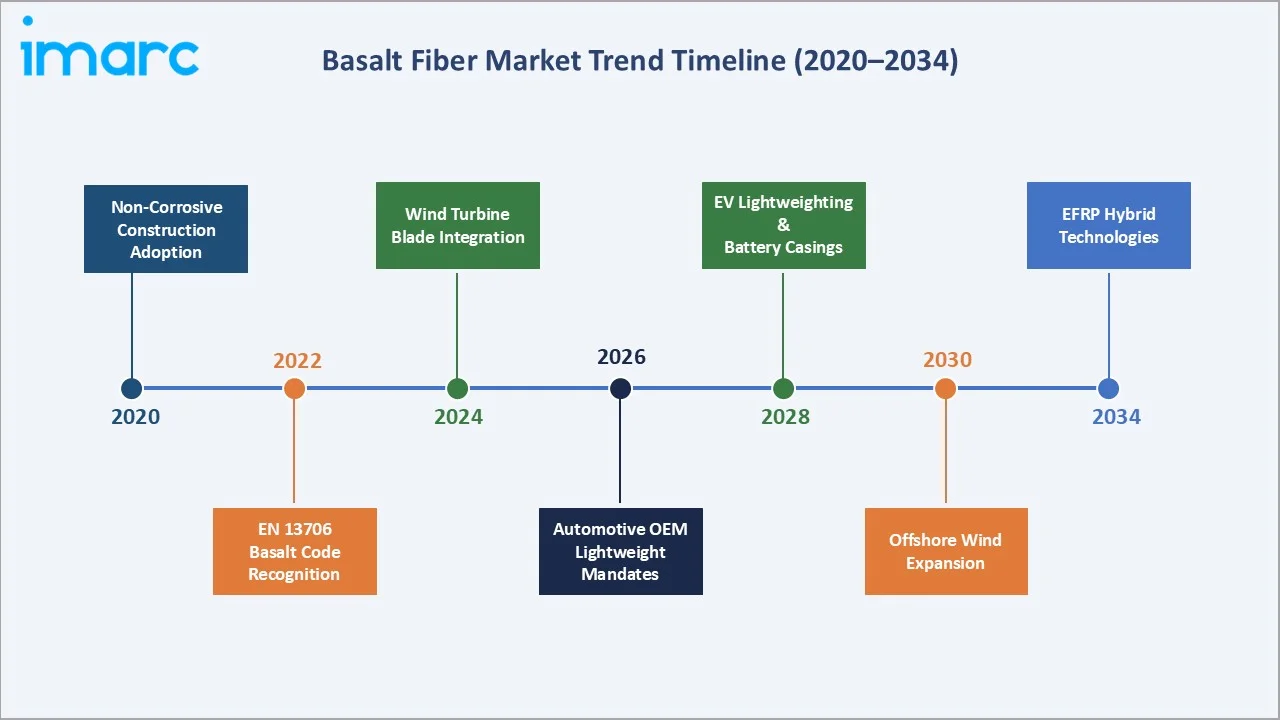

1. Infrastructure Decarbonization Driving Basalt Rebar Specification

The revised EU Net-Zero Industry Act and equivalent national decarbonization programs are compelling infrastructure project owners to specify low-global-warming-potential reinforcement materials, placing basalt rebar on approved lists for bridge decks, seawalls, and parking structures. Basalt rebar demonstrates tensile strengths of 800–1,200 MPa with triple the corrosion resistance of steel, enabling century-long service life in chloride-rich environments. Florida DOT highway bridge validations have opened US public procurement, while the University of Maine's ARPA-I bridge program targets a 30% construction time reduction using basalt composite components.

2. Automotive Lightweighting and Electric Vehicle Composite Integration

Tightening vehicle emissions standards and rapid EV proliferation are creating durable, multi-cycle demand for basalt fiber composites in automotive structural, body, and battery management applications. EV platforms require structural components that minimize battery-offset weight, and basalt fiber's electromagnetic neutrality, fire resistance, and 20–30% weight reduction versus steel make it highly attractive for battery casings and under-floor shield applications.

3. Wind Energy Turbine Blade Reinforcement Scale-Up

Wind turbine blade manufacturers are progressively integrating basalt fiber roving and fabric for spar cap reinforcement as turbine platforms scale to 15 MW and above, where blade lengths exceeding 100 meters place extreme mechanical and environmental demands on reinforcement systems. Basalt fiber's superior fatigue resistance, corrosion immunity, and compatibility with standard epoxy matrix systems make it a technically validated alternative to glass fiber in offshore environments. This representing the fastest-growing end-use vertical in the global basalt fiber market.

4. Hybrid Basalt-Carbon and Basalt-Glass Composite Development

Manufacturers and research institutions are developing hybrid reinforcement architectures combining basalt fiber with carbon or glass fibers to achieve tailored strength, modulus, cost, and environmental profiles for specific application requirements. Hybrid systems enable access to basalt fiber's corrosion resistance and sustainability credentials while supplementing mechanical performance with carbon fiber's high stiffness in aerospace and premium automotive applications. The growing commercial availability of hybrid prepreg and woven fabric formats is expanding basalt fiber's addressable market beyond standalone applications.

5. Strategic Partnerships and Capacity Expansion Reshaping the Competitive Landscape

The global basalt fiber industry is undergoing a consolidation and capacity expansion phase. In October 2024, Basanite Industries secured a U.S. patent for an innovative basalt rebar production method designed to enhance strength and corrosion resistance in construction applications.

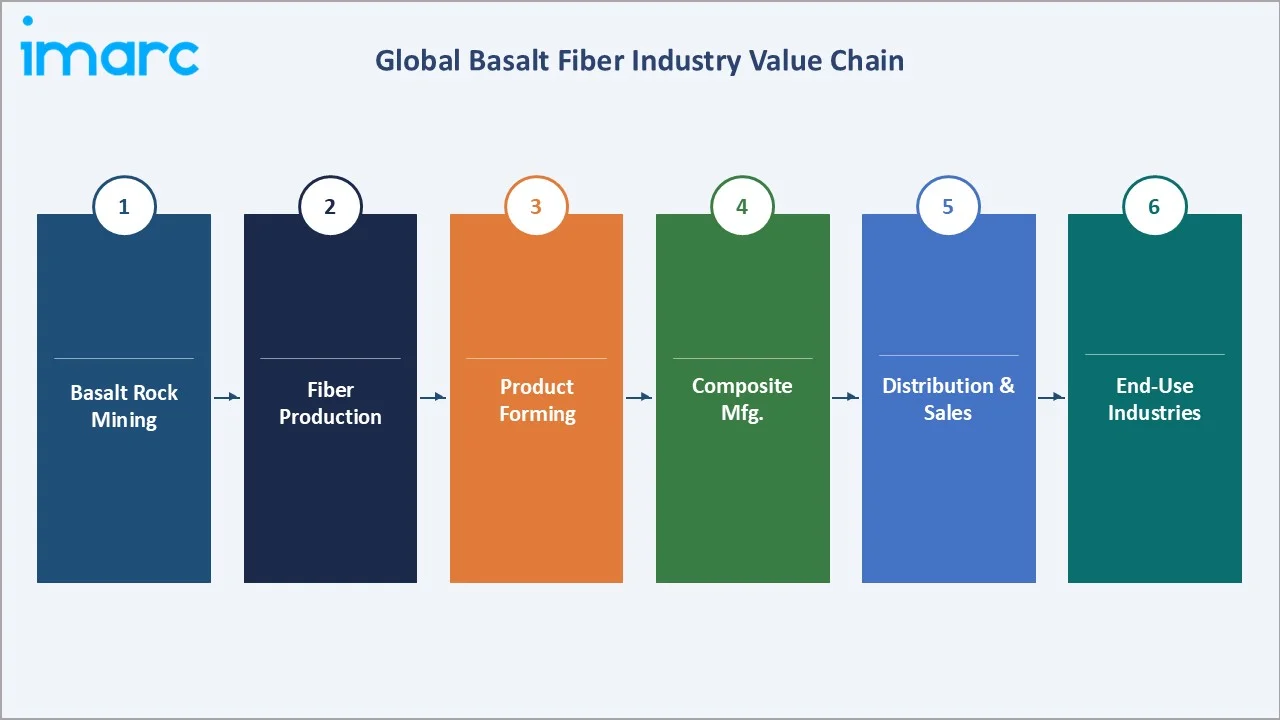

Industry Value Chain Analysis

The basalt fiber value chain spans five integrated stages from raw material extraction through end-consumer application delivery. Each stage presents distinct competitive dynamics, technology requirements, and margin profiles. The concentrated nature of basalt rock reserves and specialized melting equipment creates entry barriers at the production stage, while downstream composite manufacturing offers higher value-add opportunities for participants integrating product design and application engineering capabilities.

|

Stage |

Key Players / Activities |

|

Basalt Rock Mining & Sourcing |

Volcanic basalt rock quarrying primarily in Russia, Ukraine, China, and Eastern Europe; quality assessment for melt homogeneity and fiber yield |

|

Fiber Production |

High-temperature melting (1,400–1,600°C) and fiber drawing; key producers: Kamenny Vek (Russia), MAFIC SA (Ireland/USA), Technobasalt-Invest (Ukraine) |

|

Product Forming |

Converting continuous fiber into roving, fabric, chopped strands, rebar, and mesh; includes surface treatment and sizing chemistry for matrix compatibility |

|

Composite Manufacturing |

BFRP fabrication via pultrusion, resin transfer moulding, vacuum infusion, filament winding; integration with epoxy and vinyl-ester matrix systems |

|

Distribution & Sales |

Specialty materials distributors, direct OEM supply; geographic concentration in Asia Pacific, Europe, and North America |

|

End-Use Industries |

Construction & infrastructure, automotive & transportation, wind energy, aerospace & defense, marine, electrical & electronics |

Fiber producers occupy the most strategically concentrated position in the basalt fiber value chain. Specialized melt furnace technology, fiber drawing expertise, and quality control capability represent significant entry barriers, limiting the global production base to a small number of established manufacturers. This structural position is evolving as downstream composite manufacturers integrate backward into fiber production to secure supply and capture margin, particularly in China, where vertically integrated basalt composite producers are gaining scale.

Technology Landscape in the Basalt Fiber Industry

Fiber Production Technology: Melt Furnace and Drawing Advances

The primary manufacturing technology for basalt fiber involves single-component melting of basalt rock in electric or gas-fired furnaces, followed by fiber drawing through platinum-rhodium bushings. Advances in bushing design, thermal management, and automated tension control have progressively improved fiber diameter uniformity and tensile strength consistency. Energy-efficient furnace designs, including resistance-heated direct-melt systems, are reducing production costs and carbon intensity per kilogram of fiber, making basalt fiber increasingly cost-competitive versus conventional E-glass in regulated market applications.

Surface Treatment and Sizing Chemistry

Surface treatment and sizing chemistry are critical performance determinants in basalt fiber composites. Proprietary silane-based sizing systems applied during fiber production govern fiber-to-matrix interfacial adhesion, directly determining laminate mechanical performance, fatigue life, and moisture resistance. Advances in coupling agent chemistry and surface modification techniques have significantly improved the compatibility between basalt fibers and epoxy or vinyl‑ester matrix systems, enhancing interfacial bonding and mechanical performance in optimized composites. Researchers have demonstrated that such enhancements in fiber–matrix adhesion support better stress transfer and enable the design of more efficient laminate structures with potential weight savings. Compatibility of basalt fiber sizing’s with standard composite manufacturing processes, including wet lay-up, pultrusion, and vacuum infusion, is broadening adoption across industrial sectors.

Hybrid Composite and Advanced Application Technologies

Emerging hybrid fiber architectures combine basalt with carbon or glass fibers in biaxial and multiaxial weave configurations, enabling performance tailoring for specific application requirements. Automated fiber placement and filament winding technologies are being adapted for basalt fiber processing, improving manufacturing speed and geometric precision in complex structural components. The development of basalt fiber-reinforced thermoplastic composites is opening new automotive and consumer electronics application segments where recyclability and high-volume manufacturing are priorities. Additive manufacturing research is evaluating chopped basalt fiber-reinforced polymers for structural prototyping and low-volume industrial components.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Product |

Roving |

25.1% |

2025 |

|

Type |

Composites |

90.7% |

2025 |

|

Form |

Continuous |

76.9% |

2025 |

|

Method |

Pultrusion |

26.4% |

2025 |

| End Use Industry | Construction and Infrastructure | 56.8% | 2025 |

|

Region |

Asia-Pacific |

47% |

2025 |

By Product

Roving commands a 25.1% majority share in the global basalt fiber market in 2025, reflecting its extensive utility as the primary input format for composite fabrication across wind energy, automotive, marine, and aerospace structural applications. Roving's mechanical properties – high tensile strength, flexibility, and compatibility with filament winding, pultrusion, and wet lay-up processes – make it the preferred format for manufacturers producing load-bearing structural components requiring consistent fiber alignment and superior strength-to-weight performance.

To access detailed market analysis, Request Sample

Fabric accounts for 19.4% in 2025, driven by demand in marine hull construction, automotive body panel fabrication, and building cladding. Chopped strands at 17.3% serve the concrete reinforcement, short-fiber composite injection moulding, and friction material markets. Rebar at 14.6% is among the fastest-growing product types driven by infrastructure regulatory recognition. Mesh and grids at 13.2% are gaining traction in civil engineering and geotechnical reinforcement applications.

By Type

Composites constitute the dominant type segment at 90.7% of global basalt fiber market revenue in 2025, underpinned by the material's primary application as structural reinforcement in epoxy, vinyl-ester, and polyester matrix systems across construction, energy, automotive, and marine end-use sectors. Basalt fiber composites deliver superior interfacial shear strength of approximately 40 MPa, enabling thinner laminates with 10–15% weight savings compared to equivalent glass fiber structures, while providing corrosion immunity and extended service life in demanding environmental exposures.

Non-composites account for 9.3% of market value in 2025 but are growing at the fastest rate (~10.3% CAGR through 2034), driven by basalt rebar and mesh adoption in highway bridge decks, seawalls, and parking structures following regulatory code recognition. Florida DOT highway bridge validations and the University of Maine's ARPA-I bridge program are creating important proof-of-concept deployments, signaling a structural shift in North American public infrastructure specification norms toward basalt composite reinforcement.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

Asia Pacific |

47.0% |

China infrastructure boom, domestic fiber manufacturing, rapid wind energy growth, India construction expansion, Japan/Korea advanced composite demand |

|

Europe |

24.4% |

EU Net-Zero Industry Act, EN 13706 code recognition, Germany wind turbine blade integration, offshore wind scale-up, sustainable construction mandates |

|

North America |

18.6% |

15% YoY import growth (2025), federal infrastructure investment, Florida DOT bridge validations, EV lightweighting demand, aerospace adoption |

|

Latin America |

5.7% |

Brazil road/bridge infrastructure investment, Mexico automotive assembly growth, expanding composite manufacturing capacity |

|

Middle East and Africa |

4.3% |

GCC infrastructure expansion, high-humidity corrosion-resistant applications, Saudi Vision 2030 smart mobility investments |

Asia Pacific commands a 47.0% global revenue share in 2025, the most dominant regional position in the basalt fiber market. China is the single most important national market, combining extensive domestic basalt rock reserves, a concentrated fiber manufacturing ecosystem, and the world's most aggressive infrastructure investment programs in highway, bridge, and coastal infrastructure. India is emerging as a high-growth market, with basalt fiber adoption accelerating across bridge construction and industrial infrastructure. Japan and South Korea contribute advanced composite manufacturing demand from their automotive and electronics industries.

North America, with 18.6% in 2025, is anchored by the US market where a confirmed 15% year-over-year increase in basalt fiber imports confirms accelerating automotive lightweighting and federal infrastructure program demand. The US EV market's rapid expansion is creating structural demand for basalt composite battery casings and structural components. Canada's growing wind energy deployment and Mexico's expanding automotive assembly base add further North American breadth. Europe's 24.4% share is driven by Germany's leadership in wind turbine blade integration, France's offshore wind expansion, and UK construction sustainability mandates aligning with basalt fiber's green credentials.

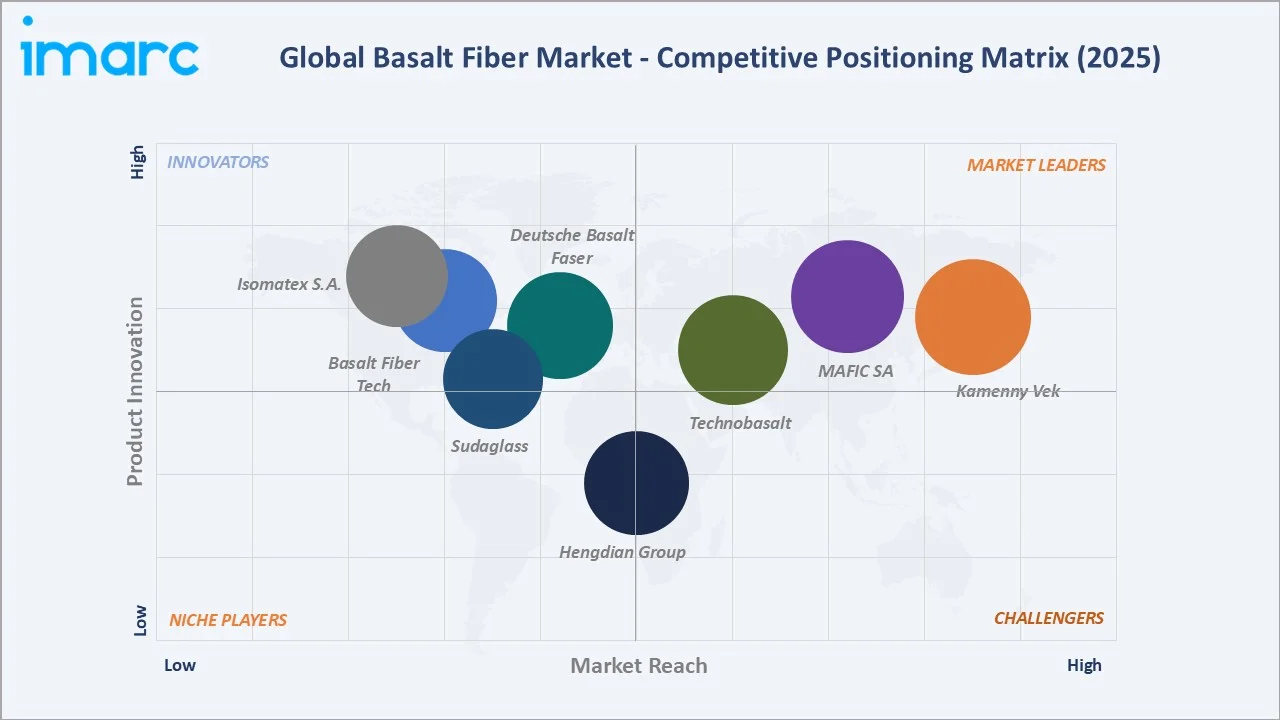

Competitive Landscape

|

Company Name |

Key Platform / Product |

Market Position |

Core Strength |

|

Kamenny Vek |

Continuous roving, fabric, BFRP |

Leader |

World's largest producer; broad product range; North American expansion via Basalt Rock Fibers acquisition (Jan 2025) |

|

MAFIC SA |

Continuous fiber, rovings, fabric |

Leader |

ISO-certified production; Ireland/USA manufacturing; strong wind energy and automotive OEM relationships |

|

Technobasalt-Invest LLC |

Continuous fiber, roving, mesh, rebar |

Leader |

Established construction and infrastructure specification track record in European markets; basalt rebar expertise |

|

Deutsche Basalt Faser GmbH |

Chopped fiber, insulation, specialty |

Challenger |

German-based; industrial insulation and construction applications; European sustainability certifications |

|

Sudaglass Fiber Technology |

Roving, woven fabric, BFRP |

Challenger |

US-based; aerospace and defense composite applications; growing wind energy roving supply capabilities |

|

Hengdian Group |

Basalt fiber products, composites |

Emerging |

China-based diversified manufacturer; growing basalt fiber capacity within larger industrial conglomerate |

|

Basalt Fiber Tech |

High-strength composite solutions |

Emerging |

Partnership with Shanghai Zhongfu (Jun 2025) for automotive and aerospace composite co-development |

|

Isomatex S.A. |

Basalt woven textiles, specialty fiber |

Emerging |

Belgian-based; specialty woven basalt products for high-temperature industrial and technical textile applications |

The basalt fiber competitive landscape is characterized by a moderately concentrated structure featuring established producers from Russia, Ukraine, and China alongside newer entrants from Ireland, the United States, and Germany. Major participants are investing in capacity expansion, surface treatment chemistry refinement, and hybrid fiber development to enhance product performance and reduce production costs relative to E-glass benchmarks. Strategic partnerships between fiber producers and composite manufacturers are accelerating as value chain participants seek downstream margin capture and improved market penetration in high-growth verticals, including wind energy and EV platforms.

Key Company Profiles

Kamenny Vek

Kamenny Vek is the world's largest basalt fiber manufacturer, headquartered in Dubna, Russia, with over two decades of production experience and a comprehensive product portfolio spanning roving, fabric, chopped strands, and BFRP systems. The company operates one of the highest-capacity basalt fiber production facilities globally and has been a primary supplier to the European construction and wind energy composite sectors.

- Product & Platform Portfolio: Continuous basalt roving (1,200 tex to 4,800 tex), woven and knitted basalt fabric, chopped strands for concrete reinforcement, basalt fiber-reinforced polymer systems for structural applications.

- Recent Developments: In November 2025, Kamenny Vek produced thick rovings by using raw materials from a new quarry at the Kimry plant.

- Strategic Focus: Kamenny Vek's strategy centers on geographic diversification through North American manufacturing, expanding OEM supply relationships in wind energy and automotive sectors, and broadening its BFRP product portfolio to capture downstream composite value chain margin beyond raw fiber supply.

MAFIC SA

MAFIC SA is an ISO-certified basalt continuous fiber manufacturer with production facilities in Ireland and the United States, positioning it as the primary Western Hemisphere basalt fiber producer. MAFIC has established strong OEM supply relationships across wind energy blade manufacturing and automotive lightweight composite sectors, with a strategic focus on supply chain reliability for North American and European composite manufacturers.

- Product & Platform Portfolio: Continuous basalt fiber (direct rovings and assembled rovings), woven fabrics, preformed mats, and specialty fiber formats tailored for vacuum infusion and filament winding composite manufacturing processes.

- Recent Developments: In December 2021, Mafic announced plans to double production capacity at its continuous basalt fiber manufacturing facility in Shelby, N.C. The facility, according to the company, is the world’s largest producer of basalt fiber and is the first of its kind in North America. Mafic USA says the additional capacity is necessary to meet increasing demand and is projected to be online before the end of 2021.

- Strategic Focus: MAFIC's competitive differentiation rests on its Western Hemisphere manufacturing locations, ISO certification, and deep application engineering support for OEM composite manufacturers requiring consistent fiber quality and supply chain reliability outside of Asia Pacific.

Technobasalt-Invest LLC

Technobasalt-Invest is a Ukraine-based basalt fiber manufacturer with established market presence in European construction, infrastructure, and industrial insulation sectors. The company offers a comprehensive range of continuous and discrete basalt fiber products and has accumulated substantial engineering data supporting code-compliant specification for basalt rebar in public infrastructure projects across Central and Eastern Europe.

- Product & Platform Portfolio: Continuous roving, chopped fiber, basalt rebar, basalt mesh and grids, woven and non-woven fabrics, needle-punched felts, and specialty insulation formats for industrial high-temperature applications.

- Recent Developments: Technobasalt has been an active participant in European infrastructure project specifications following EN 13706 recognition of basalt composites, supplying basalt rebar to bridge deck and coastal structure projects across Central and Eastern Europe.

- Strategic Focus: Technobasalt's strategy focuses on leveraging established European code recognition and application engineering expertise to expand infrastructure specification wins, grow industrial insulation market share, and develop new geographic markets in the Middle East and Africa where corrosion-resistant reinforcement demand is emerging.

Market Concentration Analysis

The global basalt fiber market exhibits moderate concentration among the top producers, with Kamenny Vek, MAFIC SA, and Technobasalt-Invest collectively accounting for approximately 40–48% of global fiber production capacity in 2025. The specialized nature of basalt fiber production technology, the requirement for substantial capital investment in high-temperature melting furnaces, and the importance of fiber quality consistency for demanding composite applications create meaningful barriers to entry sustaining this concentration.

The market is experiencing a bifurcated structural dynamic. At the high-performance application tier, consolidation is occurring as wind energy and automotive OEM procurement relationships require manufacturers to demonstrate consistent quality, supply security, and application engineering support that only established producers with substantial capacity can sustain. Simultaneously, the Chinese domestic market is generating new capacity from domestic producers, with Hengdian Group expanding production to serve China's rapidly growing construction and wind energy sectors, creating incremental competitive pressure on international producers in the world's largest regional market.

Investment & Growth Opportunities

Fastest-Growing Segments

Non-composites is the highest-growth type segment at ~10.3% CAGR through 2034, driven by basalt rebar adoption in regulated infrastructure applications following EN 13706 and Florida DOT code recognition. Rebar within the product segment is growing at ~9.2% CAGR, while mesh and grids at ~8.6% CAGR reflect growing civil engineering and geotechnical reinforcement applications. Wind energy and EV platform applications represent the fastest-growing end-use verticals, with energy applications forecast at a 14.26% CAGR through 2031, representing multi-year procurement commitments from OEMs building next-generation turbine platforms.

Emerging Market Expansion

Middle East and Africa represent a structurally underpenetrated opportunity where high-humidity, high-temperature coastal infrastructure environments create ideal conditions for basalt fiber's corrosion-resistance advantages over conventional steel. Latin America's expanding highway and bridge infrastructure programs in Brazil and Mexico are creating greenfield opportunities for basalt rebar specification. India within Asia Pacific represents the fastest-growing emerging market, with the Indian government's National Infrastructure Pipeline creating substantial bridge and highway construction demand aligned with basalt fiber's durability and low-maintenance value proposition.

Venture & Private Investment Trends

In November 2025, Kamenny Vek produced thick rovings by using raw materials from a new quarry at the Kimry plant. Michelman and FibreCoat's January 2025 launch of AluCoat, an aluminum-coated basalt fiber, further demonstrates active venture activity in hybrid fiber innovation for automotive and electronics applications.

Future Market Outlook (2026-2034)

The global basalt fiber market forecast projects steady value expansion from USD 427.3 Million in 2025 to USD 802.9 Million by 2034 at a CAGR of 7.3%, a near-doubling of market value underpinned by expanding infrastructure specification, wind energy scale-up, automotive lightweighting mandates, and growing sustainability-driven material substitution across industrial supply chains.

Three structural trends are most likely to shape the basalt fiber market through 2034. First, infrastructure code normalization – the progressive adoption of basalt fiber rebar and mesh in national construction codes across North America, Europe, and Asia Pacific will transition basalt composites from a specialty material to a mainstream infrastructure specification option, materially expanding the addressable market. Second, wind energy scale-up driven by 15 MW turbine platforms will create substantial sustained demand for basalt fiber roving in blade spar cap reinforcement, representing multi-year volume commitments from OEMs expanding renewable energy capacity. Third, EV platform integration will drive basalt fiber into high-volume automotive supply chains as battery casing and structural applications mature from prototype to production specification.

By 2034, the basalt fiber industry is forecast to have advanced from a materials innovation segment to an established industrial composite reinforcement category. The competitive landscape will be shaped by continued capacity expansion by Russian and Chinese producers, strategic Western Hemisphere manufacturing investment, and the emergence of hybrid fiber composite specialists targeting application-specific performance requirements in automotive, aerospace, and energy sectors.

Research Methodology

Primary Research

Primary research encompassed structured interviews with basalt fiber industry stakeholders including production directors at leading fiber manufacturers, composite OEM procurement managers, civil infrastructure engineers specifying fiber-reinforced polymer materials, wind energy turbine blade manufacturing engineers, and automotive lightweight materials programme managers. Primary insights validated market sizing estimates, product segment demand drivers, regional adoption dynamics, and competitive positioning assessments across key end-use verticals.

Secondary Research

Secondary sources include European Committee for Standardization EN 13706 publications, US Federal Highway Administration fiber-reinforced polymer program documentation, IRENA global wind energy capacity data, IEA electric vehicle deployment statistics, industry trade publications including JEC Composites, Composites World, and Reinforced Plastics, company annual reports and press releases, Grand View Research and Mordor Intelligence basalt fiber market reports, and government infrastructure investment program documentation from key regional markets including the EU, US, India, and China.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, construction investment indices, vehicle production volume data, wind energy installation capacity forecasts, and historical basalt fiber market evolution patterns. Scenario analysis across base, optimistic, and conservative cases was performed to account for macroeconomic uncertainty, raw material supply constraints, and regulatory adoption pace variation across regional markets.

Basalt Fiber Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Products Covered | Rebar, Fabric, Roving, Chopped Strands, Mesh and Grids, Others |

| Types Covered | Composites, Non-Composites |

| Forms Covered | Continuous, Discrete |

| Methods Covered | Pultrusion, Prepregs, Compression Moulding, Hand Layup, Resin Moulding, Vacuum Infusion, Spray Gun, Filament Winding, Others |

| End Use Industries Covered | Automotive and Transportation, Construction and Infrastructure, Electrical and Electronics, Wind Energy, Marines, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Kamenny Vek, MAFIC SA, Technobasalt-Invest LLC, Deutsche Basalt Faser GmbH, Sudaglass Fiber Technology, Hengdian Group, Basalt Fiber Tech, Isomatex S.A., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the basalt fiber market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global basalt fiber market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the basalt fiber industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Basalt Fiber Market Report

The global basalt fiber market was valued at USD 427.3 Million in 2025, driven by accelerating demand from construction, automotive, and wind energy sectors.

The market is projected to reach USD 802.9 Million by 2034, growing at a CAGR of 7.3% during 2026-2034, driven by infrastructure decarbonization, EV lightweighting demand, and offshore wind energy expansion.

Roving leads with a 25.1% share in 2025, driven by its extensive utility in composite fabrication across wind energy blade reinforcement, automotive structural components, and marine hull construction requiring consistent fiber alignment and superior tensile performance.

Composites lead with a 90.7% share in 2025, driven by basalt fiber's primary application as structural reinforcement in epoxy and vinyl-ester matrix systems across construction, energy, automotive, and marine end-use sectors.

Asia Pacific leads with a 47.0% share in 2025, driven by China's large-scale infrastructure investment, domestic fiber manufacturing base, rapid wind energy deployment, and India's growing construction sector demand.

Key drivers include infrastructure modernization favoring non-corrosive reinforcement, automotive lightweighting mandates driven by emissions standards, wind turbine blade integration with 23% of German wind blades incorporating basalt fiber in 2024, EU Net-Zero Industry Act sustainability mandates, and EV platform demand for lightweight battery casings and structural components.

Non-composites is the fastest-growing type segment at ~10.3% CAGR through 2034, driven by basalt rebar adoption in highway bridge decks, seawalls, and parking structures following EN 13706 and Florida DOT code recognition.

Leading companies include Kamenny Vek (Russia), MAFIC SA (Ireland/USA), Technobasalt-Invest LLC (Ukraine), Deutsche Basalt Faser GmbH (Germany), Sudaglass Fiber Technology (USA), Hengdian Group (China), Isomatex S.A. (Belgium), and Basalt Fiber Tech.

EV platforms adopt basalt fiber composites for battery casings, under-floor shields, and structural body components, achieving ~30% weight reduction versus steel while meeting crash performance standards. Basalt fiber's electromagnetic neutrality and fire resistance provide additional functional advantages for battery thermal management and EV structural applications.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)