Beta Glucan Market Size, Share, Trends and Forecast by Type, Source, Industry Vertical, and Region, 2026-2034

Beta Glucan Market Size, Share, Trends & Forecast (2026-2034)

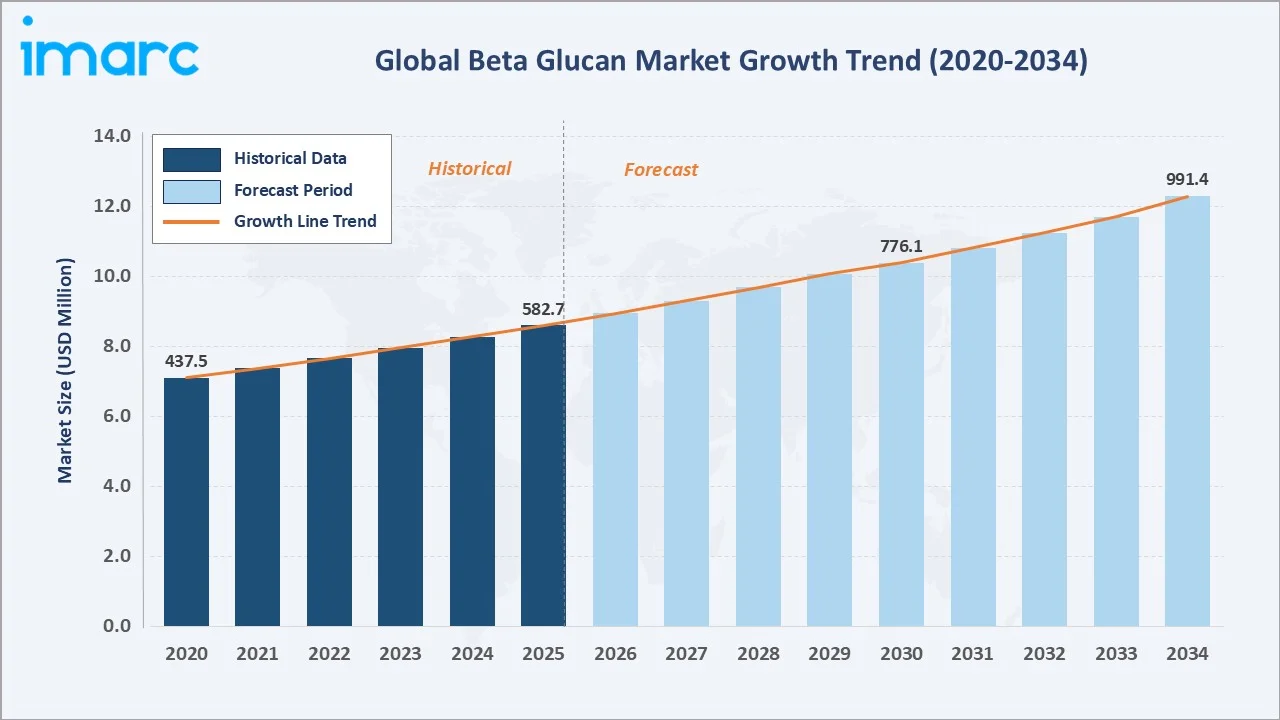

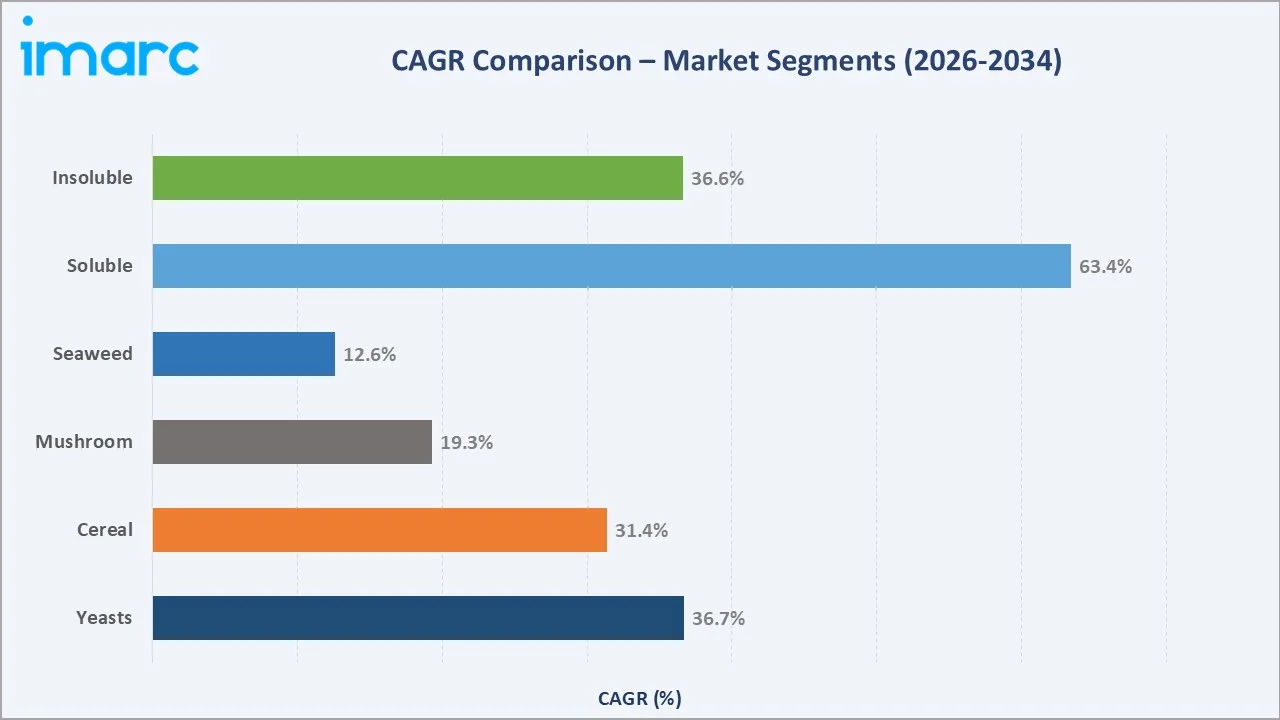

The global beta glucan market was valued at USD 582.7 Million in 2025 and is projected to reach USD 991.4 Million by 2034, exhibiting a CAGR of 5.90% during 2026-2034. Market expansion is driven by escalating demand for natural immunity boosters, rising incorporation of beta-glucan in functional foods, expanding pharmaceutical applications, and regulatory endorsements from the FDA and EFSA. Yeasts lead the source segment with 36.7% share, while Soluble beta-glucan dominates the type segment at 63.4%. Europe commands the largest regional share at 36.7%, underpinned by strong consumer awareness and EFSA-approved health claims.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 582.7 Million |

|

Forecast Market Size (2034) |

USD 991.4 Million |

|

CAGR (2026-2034) |

5.90% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

Europe (36.7% share, 2025) |

|

Fastest Growing Region |

Asia Pacific (CAGR ~9.5%) |

|

Leading Source |

Yeasts (36.7%, 2025) |

|

Leading Type |

Soluble (63.4%, 2025) |

The chart below maps the global beta glucan market growth trajectory from 2020 through 2034, contrasting a consistent historical expansion base against a sustained forecast curve powered by functional food adoption, expanding pharmaceutical applications, and growing consumer health consciousness.

To get more information on this market, Request Sample

Segment-level share comparisons highlighting Yeasts and Soluble beta-glucan as the two dominant sub-categories within the global beta glucan industry analysis through 2034.

Executive Summary

The global beta glucan market is undergoing a significant transformation driven by the convergence of health-conscious consumer behavior, functional food innovation, and expanding pharmaceutical applications. Valued at USD 582.7 Million in 2025, the market is forecast to reach USD 991.4 Million by 2034 at a CAGR of 5.90%. The FDA and EFSA-approved heart health and cholesterol-reduction claims have substantially elevated consumer confidence and driven incorporation across mainstream food, nutraceutical, and cosmetics categories.

Yeasts dominate the source segment with a 36.7% share in 2025, driven by the economical and scalable availability of Saccharomyces cerevisiae as a fermentation byproduct. Soluble beta-glucan leads the type segment at 63.4%, reflecting its superior functional versatility across beverage, dairy, and supplement formulations.

Europe commands a 36.7% share in 2025, anchored by stringent regulatory frameworks and high consumer awareness. Asia Pacific is the fastest-growing region, projected at ~9.5% CAGR through 2034, fueled by rising disposable incomes and expanding nutraceutical adoption across China, India, and Japan.

Key Market Insights

|

Insight |

Data |

|

Largest Source Segment |

Yeasts – 36.7% share (2025) |

|

Largest Type Segment |

Soluble – 63.4% share (2025) |

|

Leading Region |

Europe – 36.7% revenue share (2025) |

|

Fastest Growing Region |

Asia Pacific – ~9.5% CAGR (2026-2034) |

|

Second Region |

North America – 28.4% revenue share (2025) |

|

Top Companies |

Kerry Group, Lesaffre, Lallemand, Givaudan, Kemin Industries |

Key Analytical Observations Supporting The Above Data:

- Yeasts' 36.7% dominance in 2025 reflects the widespread commercial availability of Saccharomyces cerevisiae and its high-purity (70–85%) standardized extracts preferred in nutraceutical and pharmaceutical applications.

- Soluble beta-glucan leads at 63.4% in 2025, driven by its seamless incorporation into liquid formulations, FDA/EFSA-approved cholesterol-reduction claims, and superior bioavailability in functional food applications.

- Europe's 36.7% global dominance in 2025 reflects the region's mature functional food culture, EFSA-backed health claims, and strong consumer willingness to invest in premium-quality natural ingredients.

- Asia Pacific's ~9.5% CAGR through 2025 is driven by China's expanding yeast-fermentation capacity, India's growing nutraceutical sector, and Japan's mature health and wellness market.

- Post-pandemic health consciousness has driven a measurable shift toward immune-supporting functional ingredients, with beta-glucan positioned as one of the most scientifically validated natural immunity boosters globally.

Global Beta Glucan Market Overview

Beta-glucan is a naturally occurring polysaccharide found in the cell walls of cereals (oats, barley), yeast (Saccharomyces cerevisiae), mushrooms (shiitake, reishi, maitake), and seaweed. It is widely recognized for its immune-modulating, cholesterol-lowering, blood sugar-regulating, and skin-health properties.

Applications span functional foods, dietary supplements, pharmaceuticals, cosmetics, and animal feed. The ingredient is incorporated as a fiber source, fat replacer, thickening agent, and bioactive functional component across formulations globally. Macroeconomic enablers include rising health expenditure, global prevalence of chronic diseases, and consumer preference for clean-label, plant-derived ingredients.

Market Dynamics

To evaluate market opportunities, Request Sample

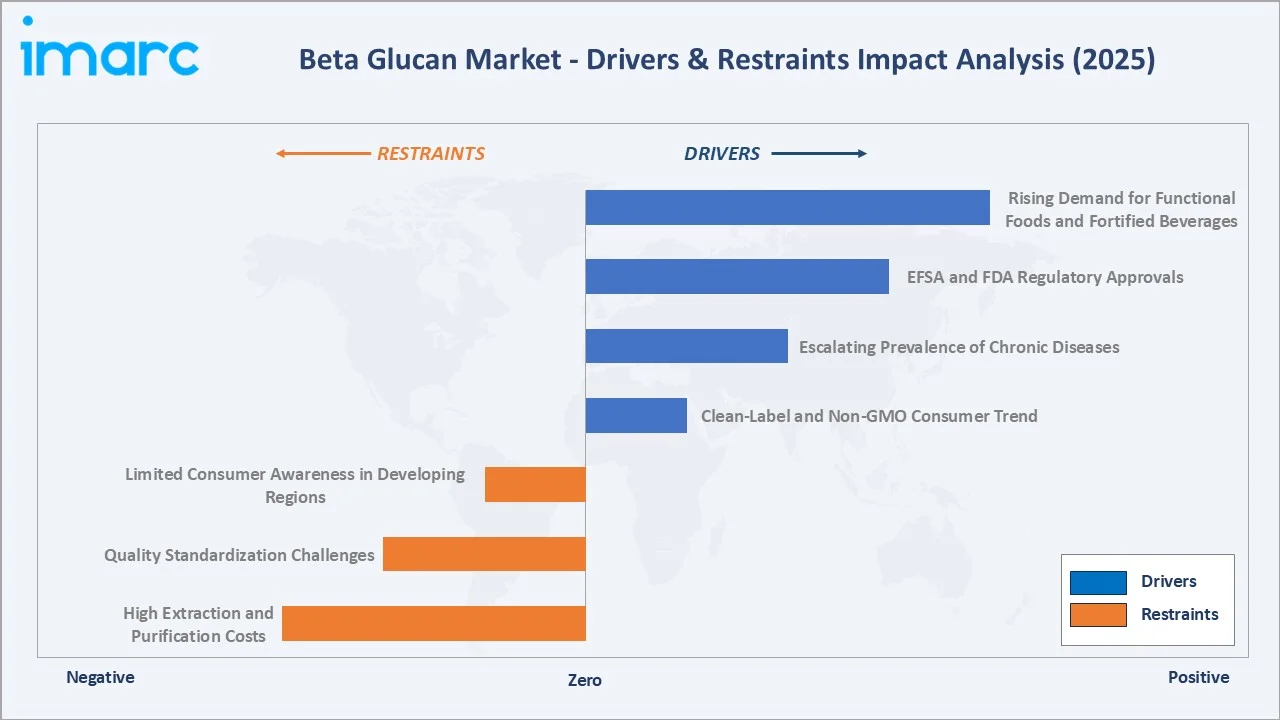

The beta glucan market is shaped by a balanced interplay of strong structural growth drivers, emerging restraints, and high-potential opportunities that collectively define its competitive landscape through 2034.

Market Drivers

- Rising Demand for Functional Foods and Fortified Beverages: Beta-glucan's clinically proven role in cholesterol reduction and immune support has driven broad incorporation into cereals, bread, dairy alternatives, and supplement beverages. The functional food ingredient market was valued at over USD 90 Billion globally in 2024.

- EFSA and FDA Regulatory Approvals: Both the US FDA and European EFSA have approved health claims for oat beta-glucan in cholesterol reduction and cardiovascular risk management, providing manufacturers with substantiated marketing tools that directly translate into consumer demand.

- Escalating Prevalence of Chronic Diseases: The growing global burden of cardiovascular disease, diabetes, and obesity—with the CDC reporting adult obesity rates reaching 42.4% in 2020–2021—is driving preventive healthcare adoption, positioning beta-glucan as a key functional ingredient.

- Clean-Label and Non-GMO Consumer Trend: Over 47% of global consumers in 2024 prioritized natural attributes in at least one food category, aligning directly with beta-glucan's natural origin profile and expanding non-GMO project verification by key manufacturers.

Market Restraints

- High Extraction and Purification Costs: Advanced extraction methodologies, including enzyme-assisted and fractionation processes, require significant capital investment, limiting market accessibility for smaller manufacturers in price-sensitive emerging markets.

- Quality Standardization Challenges: Beta-glucan quality varies considerably based on source, cultivation conditions, and processing methods, making consistent standardization across global supply chains a persistent technical and commercial challenge.

- Limited Consumer Awareness in Developing Regions: In Latin America, Southeast Asia, and Africa, consumer familiarity with beta-glucan's health benefits remains limited, constraining market penetration rates without targeted education and marketing initiatives.

Market Opportunities

- Precision Fermentation and Biotechnology Advancements: Emerging precision fermentation platforms enable scalable, high-purity yeast beta-glucan production at reduced costs. In February 2025, Layn Natural Ingredients opened a dedicated biotechnology facility targeting this production paradigm.

- Cosmetics and Dermatological Expansion: Beta-glucan's skin-soothing and collagen-stimulating properties are driving adoption in premium skincare, competing directly with hyaluronic acid. The global cosmetics ingredient market is expanding at approximately 5.8% CAGR through 2030.

- Animal Feed Applications: Rising demand for antibiotic-free livestock production is creating opportunities for beta-glucan as a natural immune enhancer in animal feed formulations, particularly in aquaculture and poultry sectors across Asia Pacific.

Market Challenges

- Regulatory Variability Across Geographies: Divergent labelling, usage limits, and health claim regulations across the US, EU, and Asian markets require manufacturers to develop region-specific compliance strategies, adding complexity and cost to global operations.

- Competition from Substitute Ingredients: Alternatives such as guar gum, inulin, and other natural polysaccharides compete for functional food formulation slots, potentially constraining beta-glucan's market share in price-sensitive commodity applications.

Emerging Market Trends

The beta glucan market forecast is shaped by several structural trends that are redefining ingredient development, consumer expectations, and industrial applications through 2034.

1. Rising Incorporation in Functional and Fortified Foods

Consumer preference for 'better-for-you' foods is driving beta-glucan fortification across cereals, snack bars, dairy alternatives, and beverages. In July 2023, Beneo introduced Orafti β-Fit, a clean-label barley beta-glucan ingredient targeting consumer demand for sustainable, plant-based nutrition—illustrating the rapid pace of product innovation in this segment.

2. Expansion into Premium Cosmetics and Skincare

Beta-glucan is an emerging skincare ingredient with demonstrated moisturizing, barrier-repair, and anti-inflammatory properties, and is increasingly used alongside hyaluronic acid to enhance overall skin hydration and resilience. Leading dermatology brands are launching targeted beta-glucan serums and creams for eczema management, post-procedure recovery, and anti-aging applications.

3. Precision Fermentation and Enzyme-Based Extraction

Advanced biotechnology platforms are enabling higher-purity, lower-cost yeast beta-glucan production. Precision fermentation eliminates variability in source quality, improves bioavailability of finished formulations, and reduces the environmental footprint of production—directly addressing two of the market's most critical commercial constraints.

4. Personalized Nutrition and Targeted Health Formulations

Beta-glucan is being incorporated into personalized supplement regimens tailored to specific health outcomes—immune support, cardiovascular wellness, metabolic management, and gut health. Combination formulations pairing beta-glucan with probiotics, vitamins, and adaptogens represent the next evolution of the nutraceutical product category.

5. Seaweed-Derived Beta-Glucan and Sustainable Sourcing

Marine-derived beta-glucan from seaweed sources is gaining traction as a sustainable, ocean-based alternative to land-crop-derived variants. With seaweed cultivation requiring no freshwater or fertilizers, it aligns with growing demand for environmentally responsible functional ingredients, particularly across European and North American markets.

Industry Value Chain Analysis

The beta glucan value chain spans six integrated stages from raw material cultivation through end-consumer delivery. Each stage presents distinct competitive dynamics, margin structures, and technology investment requirements.

|

Stage |

Key Players / Examples |

|

Raw Material Sourcing |

Oat and barley farms (Europe, North America), Saccharomyces cerevisiae breweries, Mushroom cultivators (Asia Pacific), Seaweed aquaculture farms |

|

Extraction & Processing |

Enzyme-assisted extraction, wet/dry fractionation, precision fermentation, chemical extraction (acid-base) |

|

Ingredient Manufacturing |

Kerry Group, Lesaffre, Lallemand Inc., Biorigin, Kemin Industries, Givaudan, Lantmännen Biorefineries |

|

Formulation & Product Development |

Nutraceutical companies, food & beverage manufacturers, pharmaceutical firms, cosmetics brands |

|

Distribution Channels |

Direct sales, specialty ingredient distributors, e-commerce platforms, retail health-food channels |

|

End Consumers |

Health-conscious individuals, pharmaceutical manufacturers, cosmetic brands, livestock/aquaculture producers |

Technology Landscape

Extraction Technologies

Advances in enzyme-assisted extraction and fractionation have substantially improved beta-glucan purity levels from conventional 40–50% to pharmaceutical-grade 70–85%, enabling broader adoption in high-value supplement and pharmaceutical formulations.

Precision Fermentation Platforms

Synthetic biology and precision fermentation are enabling controlled, high-yield production of yeast beta-glucan independent of agricultural supply chain variability. This technology reduces batch-to-batch quality inconsistencies—a key commercial barrier in the pharmaceutical segment.

Formulation Innovations

Encapsulation technologies, nano-emulsification, and water-dispersible formats (such as Kemin's BetaVia WD series) are improving solubility, bioavailability, and shelf stability of beta-glucan across diverse food, beverage, and supplement applications.

Digital Quality Monitoring

AI-driven quality control and spectroscopic analysis tools are being adopted by leading manufacturers to ensure consistent beta-glucan molecular weight and purity—critical parameters that directly influence clinical efficacy and regulatory compliance.

Market Segmentation Analysis

The report covers the following segments:

|

Segment Category |

Leading Segment |

Market Share |

Year |

|

Type |

Soluble |

63.4% |

2025 |

|

Source |

Yeasts |

36.7% |

2025 |

|

Industry Vertical |

🔒 |

🔒 |

2025 |

|

Region |

Europe |

36.7% |

2025 |

Breakup by Source

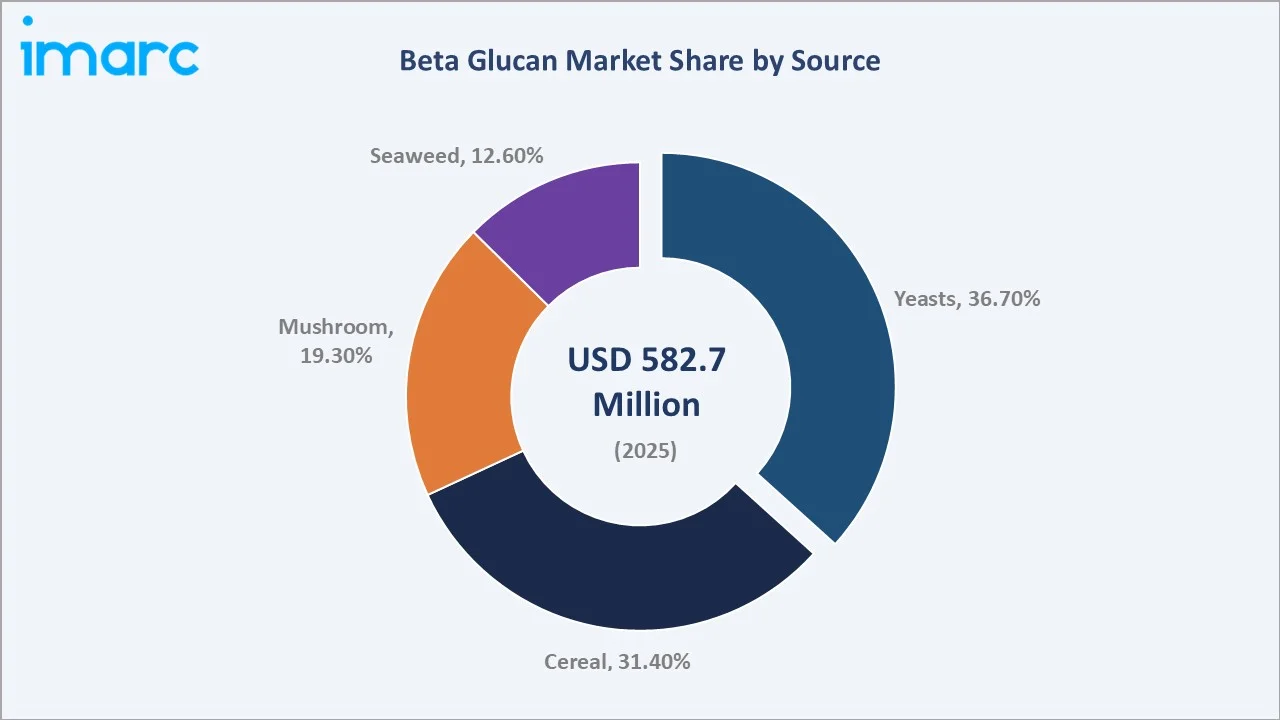

The beta glucan market is segmented by source into Yeasts, Cereal, Mushroom, and Seaweed. Yeasts dominate with 36.7% share in 2025, followed by Cereal at 31.4%, Mushroom at 19.3%, and Seaweed at 12.6%.

To access detailed market analysis, Request Sample

Yeasts (36.7%): Yeast-derived beta-glucan from Saccharomyces cerevisiae dominates due to economical scalability, standardized purity (70–85%), and strong clinical evidence supporting immune modulation. Strategic investments in β-glucan technologies—including acquisitions of proprietary manufacturing processes and expansion of biotech production facilities—are accelerating commercialization across nutraceutical and functional health segments, particularly in immune-support applications.

Cereal (31.4%): Oat and barley beta-glucan benefits from FDA and EFSA-approved cardiovascular health claims, driving widespread use in breakfast cereals, bread, and dairy alternatives. In February 2025, Layn Natural Ingredients announced the launch of Galacan, a novel beta-glucan ingredient developed to support applications in functional foods, nutraceuticals, and immune health solutions.

Mushroom (19.3%): Mushroom-derived beta-glucan from shiitake, reishi, and maitake is gaining traction in nutraceuticals and holistic wellness segments, reflecting growing interest in medicinal mushrooms and functional immunity products, particularly in Asia Pacific.

Seaweed (12.6%): Though the smallest segment, seaweed-derived beta-glucan is attracting investment from marine biotechnology firms for its sustainable sourcing profile and unique structural properties suited to cosmetics and specialty pharmaceutical applications.

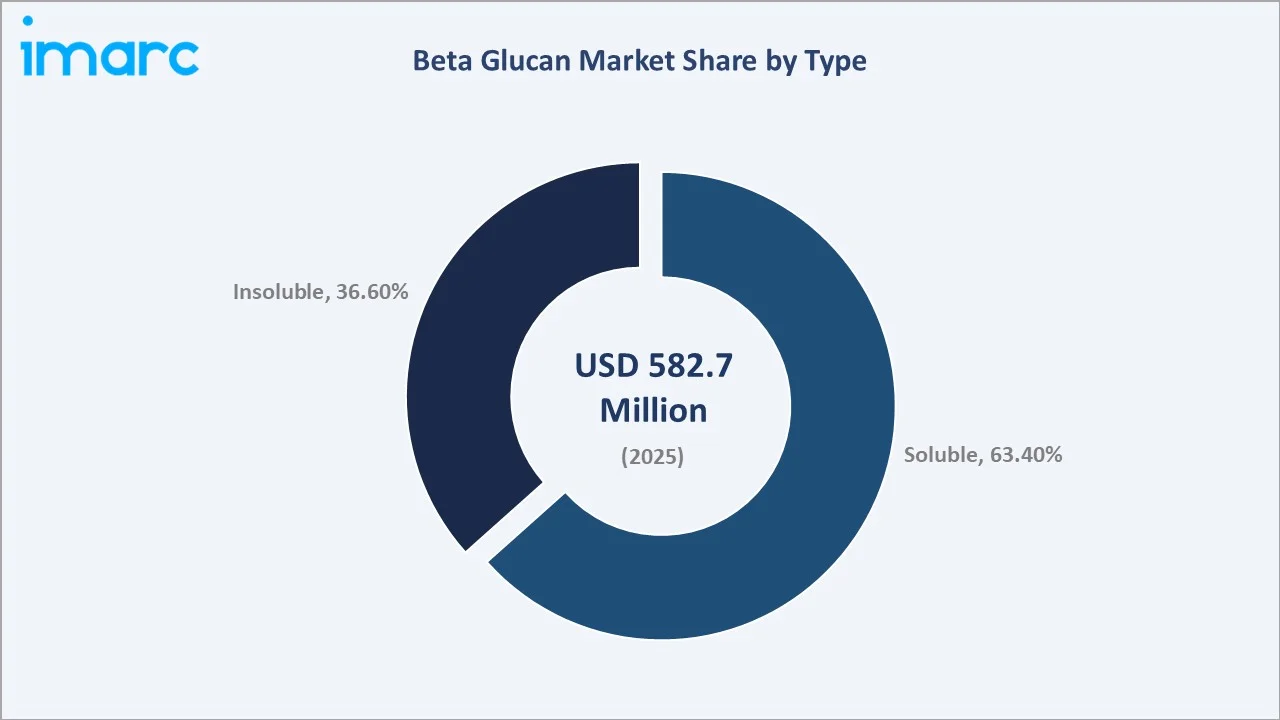

Breakup by Type

The beta glucan market is segmented by type into Soluble and Insoluble. Soluble beta-glucan leads with 63.4% share in 2025, while Insoluble accounts for the remaining 36.6%.

Soluble (63.4%): Soluble beta-glucan commands the largest type segment share owing to its seamless water-dispersibility, which enables integration into beverages, dairy, and supplement formulations. FDA and EFSA-approved cholesterol-reduction health claims further bolster commercial adoption across functional food applications globally.

Insoluble (36.6%): Insoluble beta-glucan is gaining momentum in cosmetic and personal care applications due to its inert compatibility with diverse ingredient matrices. It is widely used in antifungal creams, deodorants, and oral care products. Animal feed represents a growing secondary application channel for insoluble variants.

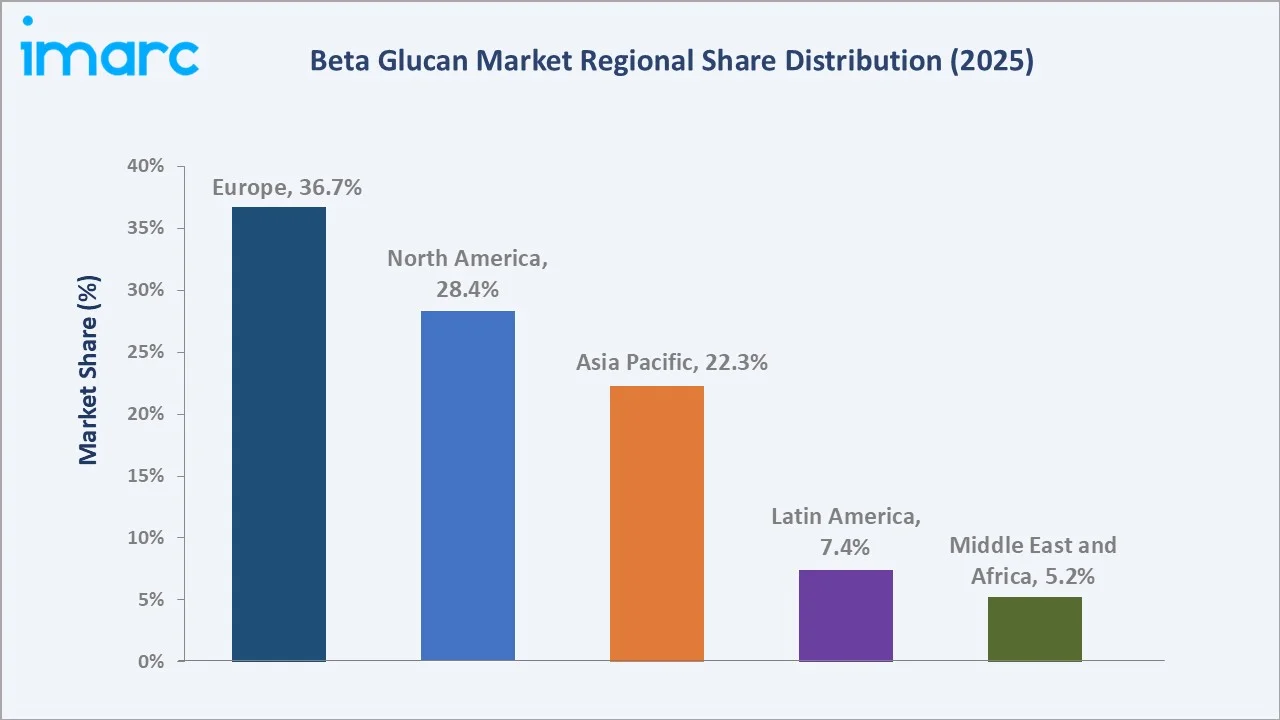

Breakup by Region

Geographically, Europe dominates with 36.7% share in 2025, followed by North America (28.4%), Asia Pacific (22.3%), Latin America (7.4%), and Middle East and Africa (5.2%).

Europe (36.7%): Europe's dominance reflects its well-established functional food culture, EFSA-approved beta-glucan health claims for cholesterol management, and high consumer awareness. Germany, France, and the UK lead regional demand. The Europe beta glucan market was valued at USD 241.31 Million in 2024 and is anticipated to reach USD 459.11 Million by 2034.

North America (28.4%): Strong demand for immune-supporting functional foods and dietary supplements anchors North America's market. North America, particularly the United States, leads the β-glucan market due to FDA-approved health claims supporting cardiovascular benefits and strong R&D capabilities in functional ingredients. In Canada, supportive regulatory frameworks and innovation funding—such as the CAD 350 million Regulatory Innovation Agenda—are further fostering the development of functional and bioactive compounds.

Asia Pacific (22.3%): Asia Pacific is the fastest-growing region at ~9.5% CAGR, driven by China's yeast-fermentation expansion, India's booming nutraceutical sector, and Japan's mature health and wellness market. In April 2025, Meiji introduced a beta-glucan-fortified ready-to-drink beverage, reflecting growing integration of functional fibers into mainstream food and beverage products in Japan.

Latin America (7.4%): Brazil and Mexico lead regional growth, supported by rising health awareness around chronic diseases, expanding middle-class populations, and growing fortified food adoption. Manufacturers are tailoring formulations around metabolic health benefits—blood sugar and cholesterol management—relevant to the region's disease profile.

Middle East and Africa (5.2%): An emerging but high-potential region. Saudi Arabia leads in consumer adoption of immune-boosting functional ingredients. Improving healthcare infrastructure, rising disposable incomes, and increasing penetration of international nutraceutical brands are creating favourable long-term growth conditions.

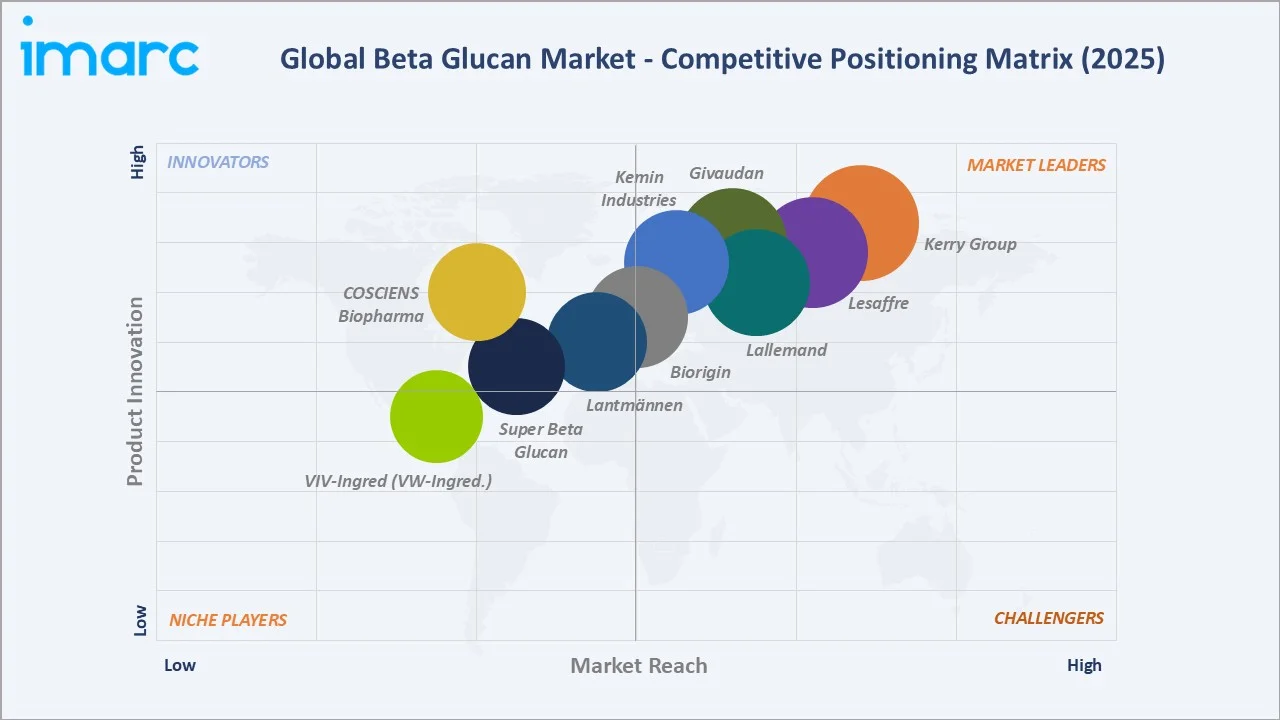

Competitive Landscape

|

Company Name |

Key Product/Platform |

Market Position |

Core Strength |

|

Kerry Group plc |

Wellmune® |

Leader |

Functional fiber, oat-based formulations |

|

Lesaffre |

Yeast Beta-Glucan |

Leader |

Fermentation expertise, pharmaceutical-grade |

|

Lallemand Inc. |

Yeast-derived BG |

Leader |

Biotechnology, fermentation, global scale |

|

Givaudan |

Active Beauty BG |

Challenger |

Cosmetics-grade, skin-health applications |

|

Kemin Industries |

BetaVia (Algae BG) |

Challenger |

Algae-derived, immune support, WD format |

|

Biorigin |

Yeast-derived BG |

Challenger |

Brazilian yeast extracts, animal nutrition |

|

Lantmännen Biorefineries |

Cereal BG |

Emerging |

Scandinavian oat/barley specialty fibers |

|

COSCIENS Biopharma |

Pharmaceutical BG |

Emerging |

Pharmaceutical-grade, clinical applications |

|

Super Beta Glucan |

SBG Pure BG |

Emerging |

Direct-to-consumer, supplement channel |

|

VW-Ingredients |

Yeast BG |

Emerging |

Specialty ingredient distribution, EU market |

The global beta glucan market exhibits moderate fragmentation, with a small number of global ingredient companies holding significant OEM and formulation relationships alongside specialized biotechnology and niche producers. Leading players compete through R&D investment, capacity expansion, clean-label certification, and strategic partnerships with functional food and pharmaceutical manufacturers.

Key Company Profiles

Kerry Group plc

Kerry Group is one of the world's largest taste and nutrition companies, with a comprehensive beta-glucan portfolio spanning both oat-derived and yeast-derived ingredients. The company’s Wellmune range is a globally recognized ingredient brand for immune health support, backed by strong clinical evidence.

- Product Portfolio: Wellmune is a unique baker’s yeast beta 1,3/1,6 glucan postbiotic and the first ingredient clinically studied as an oral trainer of the innate immune system. It helps prepare the immune system to respond more efficiently to future challenges, with recent findings published in Methods and BioTech journals demonstrating its immune-modulating effects.

- Recent Development: Kerry continues to strengthen its functional ingredient portfolio through clinically validated solutions such as its Wellmune beta-glucan, leveraging globally recognized EFSA and FDA health claim frameworks—particularly in cardiovascular and immune health—to support commercialization across North America and Europe.

- Strategic Focus: Kerry's strategy centers on sustainable oat sourcing, clean-label certification, and application-specific beta-glucan ingredient customization for food manufacturing and dietary supplement clients globally.

Lesaffre

Lesaffre is a global leader in yeast and fermentation-based ingredients, with a strong presence in beta-glucan production through its comprehensive yeast extract and active nutrition portfolio. The company's biotechnology expertise supports pharmaceutical-grade beta-glucan purification.

- Product Portfolio: Beta-glucan derived from Saccharomyces cerevisiae yeast, available in various purity grades for nutraceutical, pharmaceutical, and animal nutrition applications.

- Recent Development: Lesaffre has invested in expanding its fermentation capacity and sustainable yeast-sourcing infrastructure to meet growing demand from immune-support supplement and pharmaceutical formulation clients across Europe and Asia Pacific.

- Strategic Focus: Lesaffre's beta-glucan strategy prioritizes pharmaceutical-grade purity standardization, strategic partnerships with nutraceutical manufacturers, and geographic expansion into Asia Pacific's rapidly growing functional ingredient markets.

Kemin Industries, Inc.

Kemin Industries is a global science-based ingredient manufacturer with a differentiated position in algae-derived beta-glucan through its proprietary BetaVia platform, offering one of the few non-yeast, non-cereal beta-glucan options with clinical immune-health validation.

- Product Portfolio: BetaVia Complete and BetaVia Pure in water-dispersible (WD) formats for drink mixes, sachets, beverages, and dietary supplement formulations.

- Recent Development: Kemin introduced BetaVia Complete WD and BetaVia Pure WD in December 2022, specifically engineered for integration into beverage applications requiring rapid dispersibility and clean taste profile.

- Strategic Focus: Kemin's strategy leverages algae-derived beta-glucan's unique positioning as a non-GMO, sustainable marine-origin ingredient with published clinical trial data supporting its immune-enhancing and antioxidant-protective efficacy.

Market Concentration Analysis

The global beta glucan market displays moderate-to-low concentration among the top players, with Kerry Group, Lesaffre, and Lallemand collectively accounting for approximately 25–32% of global market revenue in 2025.

The market is experiencing a bifurcated structural dynamic. At the premium pharmaceutical and nutraceutical tier, consolidation is occurring—high-purity production and clinical validation requirements create significant technical barriers that favor established ingredient manufacturers. Simultaneously, the functional food segment is fragmenting, with regional manufacturers and specialty biotechnology firms entering through clean-label and organic product positioning.

Chinese domestic players are emerging as new competitive forces, driven by local fermentation infrastructure, lower production costs, and expanding domestic demand for immune-support supplements—creating competitive pressure on established international ingredient suppliers in the Asia Pacific market.

Investment & Growth Opportunities

Fastest-Growing Segments

Cosmetics and personal care applications represent the highest-growth application sub-segment, supported by growing demand for bioactive skin-health ingredients and beta-glucan's clinical evidence base for skin hydration and anti-aging. Pharmaceutical applications—particularly immune-adjunct therapies for aging populations—are emerging as a high-value clinical market.

Emerging Market Expansion

Asia Pacific, particularly China (9.5% CAGR), India, and ASEAN markets, represents the most dynamic geographic investment opportunity. Rising disposable incomes, expanding nutraceutical retail infrastructure, and growing chronic disease burden are collectively creating a favorable demand environment for beta-glucan adoption. Latin America and the Middle East offer secondary emerging market expansion potential.

Innovation Investment Trends

Key innovation investment areas include precision fermentation platform development for consistent high-purity yeast beta-glucan; algae-derived marine beta-glucan sourcing technologies; combination nutraceutical formulations integrating beta-glucan with probiotics, vitamins, and adaptogens; and encapsulation technologies improving bioavailability in targeted release supplement formulations.

Future Market Outlook (2026-2034)

The global beta glucan market forecast projects steady value expansion from USD 582.7 Million in 2025 to USD 991.4 Million by 2034 at a CAGR of 5.90%—representing a near-doubling of market value underpinned by functional food fortification, pharmaceutical adoption, and structural shifts in consumer preventive health behavior.

Three technology developments are most likely to reshape the beta-glucan market through 2034. Commercialization of precision fermentation platforms will reduce production costs and variability, enabling broader adoption of pharmaceutical-grade products. Personalized nutrition integration—where beta-glucan is incorporated into AI-guided dietary supplement regimens—will create new direct-to-consumer product categories. Additionally, the convergence of beta-glucan with probiotic and prebiotic formulations will define the next generation of gut-immune health products globally.

By 2034, the beta glucan industry is forecast to complete its transition from a specialty functional ingredient to a mainstream health and wellness commodity, with broad adoption across food, pharmaceutical, cosmetics, and animal nutrition sectors globally.

Research Methodology

Primary Research

Primary research encompassed structured interviews with ingredient manufacturers, nutraceutical brand managers, food technologists, clinical nutritionists, pharmaceutical procurement managers, and institutional investors across North America, Europe, and Asia Pacific. Primary insights validated market sizing, segmentation estimates, technology adoption timelines, and competitive positioning assessments.

Secondary Research

Secondary sources include EFSA and FDA regulatory databases, WHO nutrition reports, trade publications including Nutraceuticals World and Food Navigator, company annual reports, patent databases, and peer-reviewed journals including the Journal of Applied Polymer Science and the Journal of Functional Foods.

Forecasting Models

Market size estimations and growth projections were derived using a combination of top-down and bottom-up forecasting models, incorporating GDP growth rates, consumer health expenditure trends, regulatory approval timelines, and historical ingredient market evolution patterns across all five global regions.

Beta Glucan Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Million USD |

| Scope of the Report | Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Types Covered | Soluble, Insoluble |

| Sources Covered | Cereal, Mushroom, Yeasts, Seaweed |

| Industry Verticals Covered | Animal Feed, Personal Care and Cosmetics, Pharmaceuticals, Others |

| Regions Covered | North America, Europe, Asia Pacific, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Kerry Group plc, Lesaffre, Lallemand Inc., Givaudan, Kemin Industries, Biorigin, Lantmännen Biorefineries, COSCIENS Biopharma, Super Beta Glucan, VW-Ingredients, etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the beta glucan market from 2020-2034.

- The research study provides the latest information on the market drivers, challenges, and opportunities in the global beta glucan market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assist stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the beta glucan industry and its attractiveness.

- Competitive landscape allows stakeholders to understand their competitive environment and provides an insight into the current positions of key players in the market.

Frequently Asked Questions About the Beta Glucan Market Report

The global beta glucan market was valued at USD 582.7 Million in 2025, driven by demand for immune-boosting functional foods and nutraceutical supplements.

The market is projected to reach USD 991.4 Million by 2034, growing at a CAGR of 5.90% during 2026-2034, supported by expanding pharmaceutical and cosmetics applications.

Yeasts lead with a 36.7% share in 2025, driven by the economical availability of Saccharomyces cerevisiae and its standardized high-purity (70–85%) extracts preferred in nutraceutical applications.

Soluble beta-glucan leads with a 63.4% share in 2025, driven by its versatile water-dispersibility, FDA/EFSA-approved cholesterol-reduction health claims, and wide use in functional food formulations.

Europe leads with a 36.7% share in 2025, driven by EFSA-backed health claims, high consumer awareness of functional nutrition, and strong demand from Germany, France, and the United Kingdom.

Asia Pacific is the fastest-growing region at ~9.5% CAGR through 2034, fueled by China's fermentation expansion, India's nutraceutical boom, and Japan's mature health and wellness sector.

Key drivers include FDA/EFSA regulatory approvals, rising prevalence of cardiovascular disease and diabetes, growing demand for clean-label functional foods, and expanding applications in cosmetics and pharmaceuticals.

Key applications include functional foods and beverages, dietary supplements, pharmaceuticals (immune therapy adjuncts), cosmetics and skincare, and animal feed immune enhancement.

Leading companies include Kerry Group, Lesaffre, Lallemand Inc., Givaudan, Kemin Industries, Biorigin, Lantmännen Biorefineries, COSCIENS Biopharma, Super Beta Glucan, and VW-Ingredients.

Asia Pacific offers significant opportunity through China's yeast fermentation capacity expansion, India's growing nutraceutical sector, and rising middle-class demand for functional immunity and cholesterol-management products.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)