Biological Safety Testing Market Size, Share, Trends, and Forecast by Product and Services, Test Type, Application, and Region, 2026-2034

Global Biological Safety Testing Market Size, Share, Trends & Forecast (2026-2034)

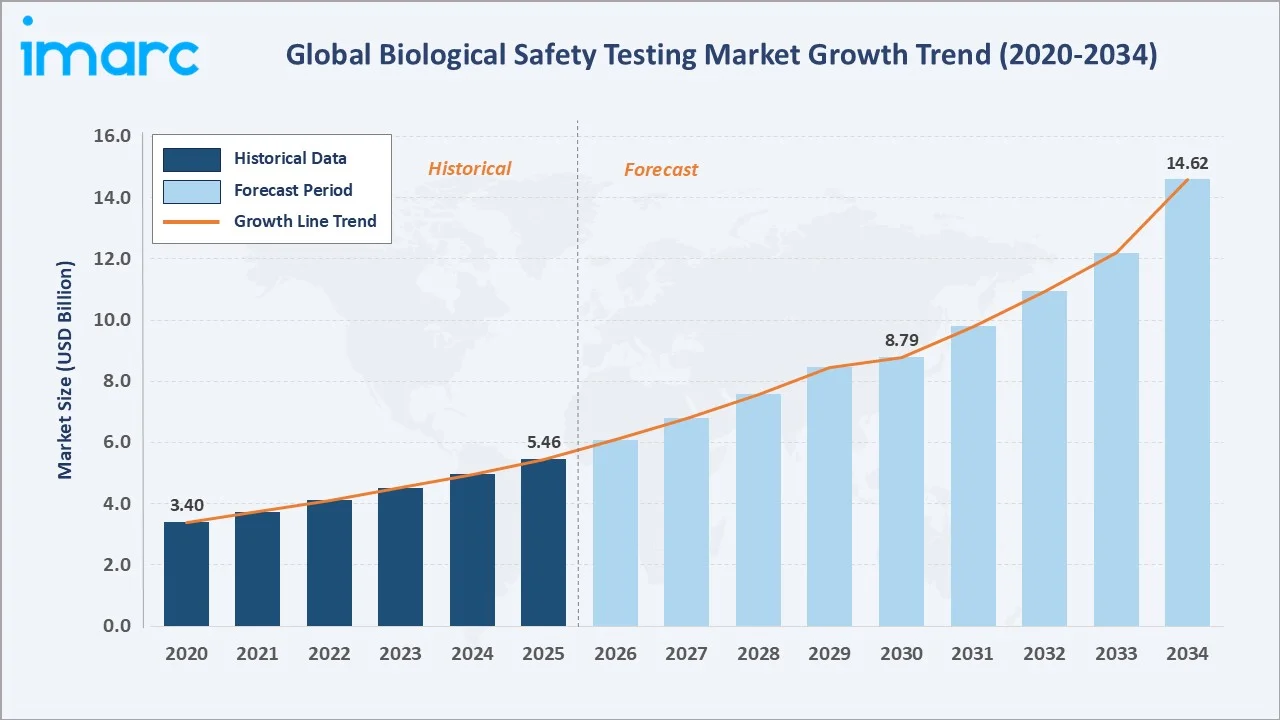

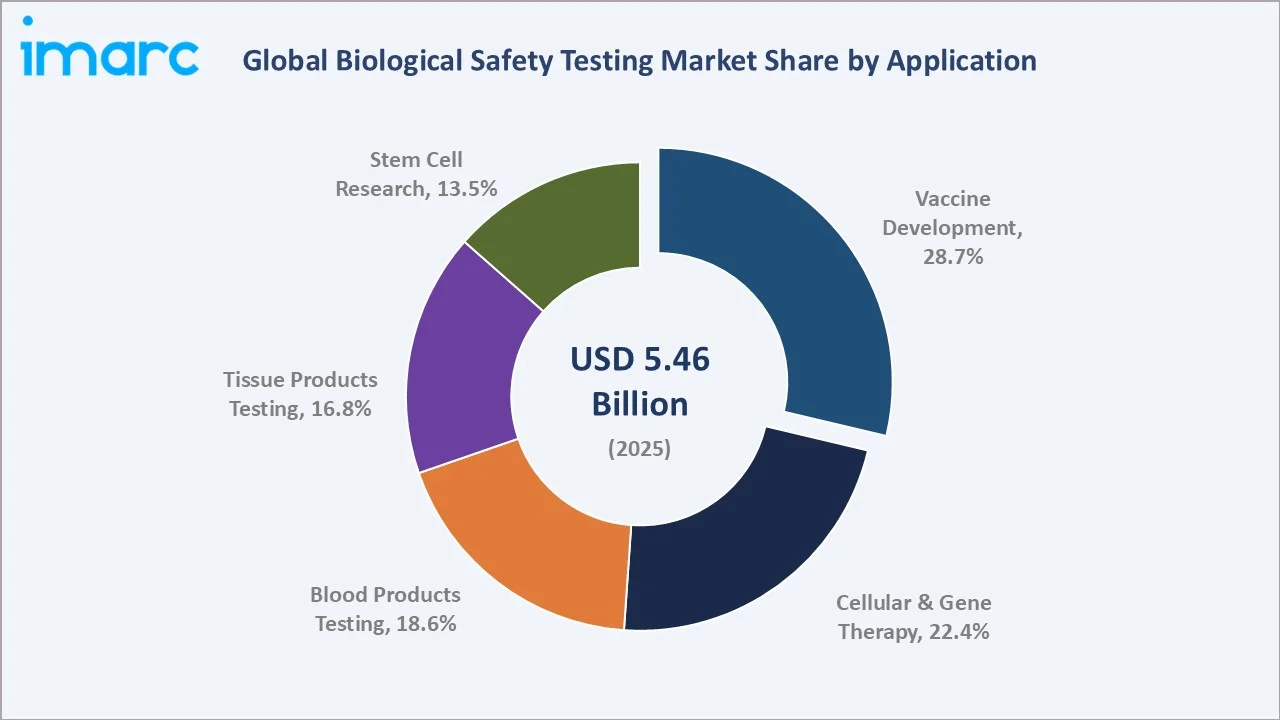

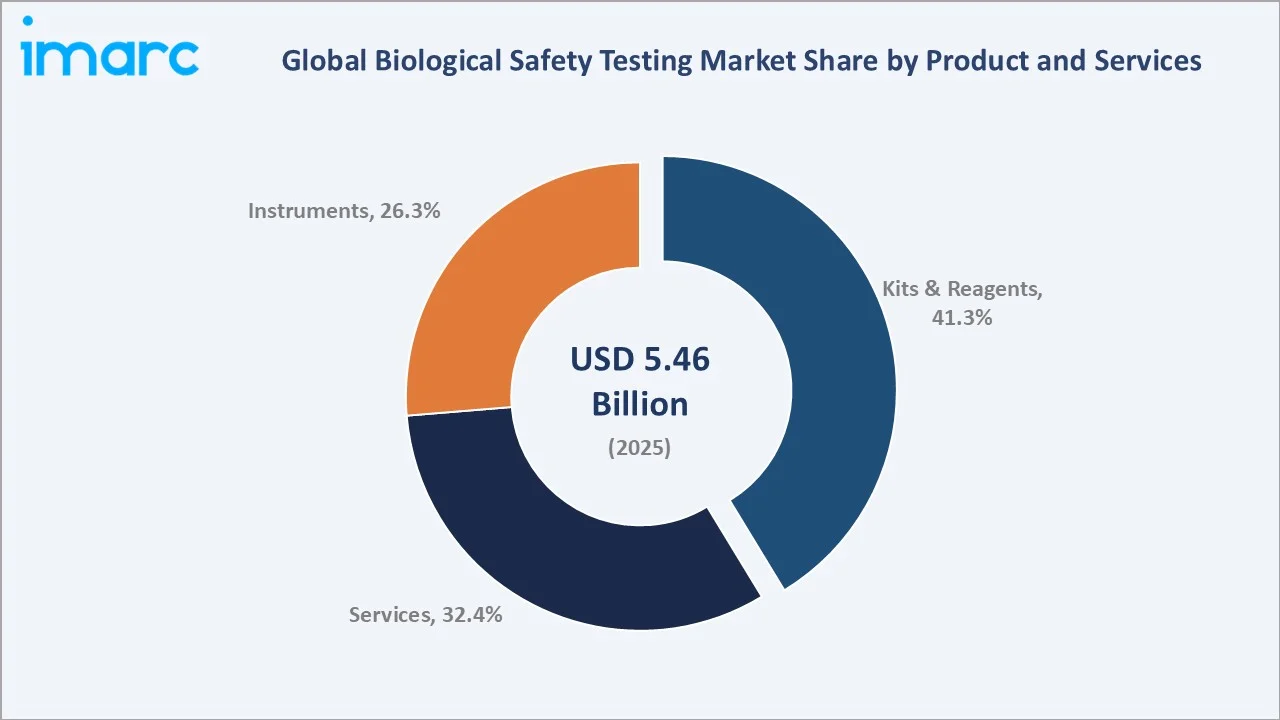

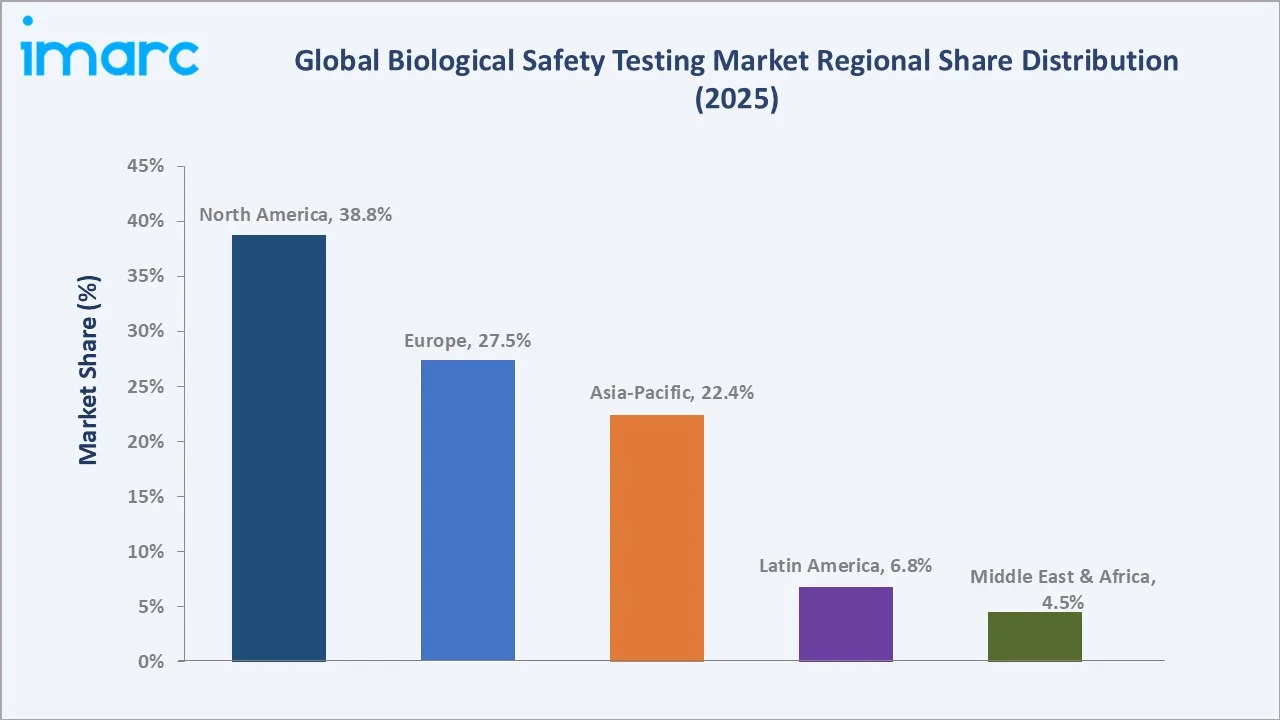

The global biological safety testing market size was valued at USD 5.46 Billion in 2025 and is projected to reach USD 14.62 Billion by 2034, at a CAGR of 9.97% during 2026-2034. Rapid expansion of biopharmaceutical pipelines, surging demand for cell and gene therapy products, increasing regulatory scrutiny, and heightened focus on pandemic preparedness are collectively propelling biological safety testing market growth. Kits and Reagents lead product segments with a 41.3% share in 2025, while Vaccine Development dominates application segments with 28.7%. North America commands regional demand at 38.8% share in 2025.

Market Snapshot

|

Metric |

Value |

|

Market Size (2025) |

USD 5.46 Billion |

|

Forecast Market Size (2034) |

USD 14.62 Billion |

|

CAGR (2026-2034) |

9.97% |

|

Base Year |

2025 |

|

Historical Period |

2020-2025 |

|

Forecast Period |

2026-2034 |

|

Largest Region |

North America (38.8% share, 2025) |

|

Fastest Growing Region |

Asia-Pacific |

|

Leading Product Segment |

Kits and Reagents (41.3%, 2025) |

|

Leading Application Segment |

Vaccine Development (28.7%, 2025) |

The chart shows global biological safety testing market growth (2020–2034), with historical trends driven by post-COVID biologics investment and future growth supported by expanding cell and gene therapies.

To get more information on this market, Request Sample

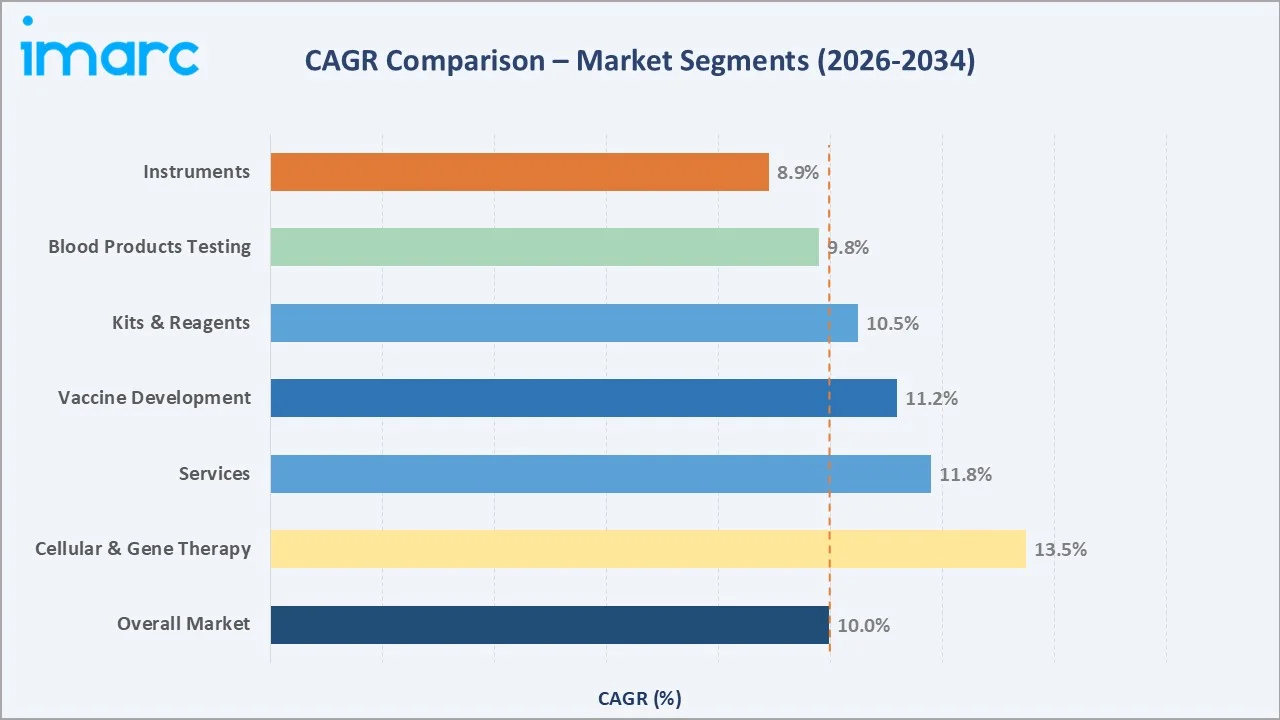

CAGR analysis identifies Cellular and Gene Therapy and Kits and Reagents as the fastest-growing segments, with the overall market sustaining a 9.97% CAGR through 2034.

Executive Summary

The global biological safety testing market is growing rapidly, driven by expanding biopharmaceutical pipelines, rising cell and gene therapies, and stricter regulatory requirements. Valued at USD 5.46 billion in 2025, the market is projected to reach USD 14.62 billion by 2034 at a CAGR of 9.97%, reflecting its critical role in ensuring biologics safety and regulatory approval worldwide.

Kits and reagents lead with a 41.3% share in 2025, driven by high-volume routine testing, while services hold 32.4% due to increased CRO outsourcing. Vaccine development dominates applications at 28.7%, with cellular and gene therapy (22.4%) emerging as the fastest-growing segment amid rising ATMP approvals and clinical trials.

North America leads the biological safety testing market with 38.8% in 2025, supported by strong biopharma presence and FDA oversight. Europe holds 27.5% driven by EMA regulations and CROs, while Asia-Pacific (22.4%) grows fastest due to expanding pharmaceutical, biosimilar, and ATMP production across China, India, Japan, and South Korea.

Key Market Insights

|

Insight |

Data |

|

Largest Application Segment |

Vaccine Development – 28.7% share (2025) |

|

Fastest Growing Application |

Cellular & Gene Therapy – 22.4% share (2025); highest CAGR through 2034 |

|

Leading Product Segment |

Kits and Reagents – 41.3% share (2025) |

|

Leading Region |

North America – 38.8% revenue share (2025) |

|

Fastest Growing Region |

Asia-Pacific – 22.4% share (2025) |

|

Top Companies |

Charles River Laboratories International, Inc., Eurofins Scientific SE, Lonza Group AG, Sartorius AG, SGS Société Générale de Surveillance SA, WuXi Biologics, Maravai LifeSciences Holdings, Inc., and Pacific BioLabs, Inc. |

|

Market Opportunity |

Gene therapy expansion + Asia-Pacific biosimilar growth offer USD 5B+ incremental opportunity through 2034 |

Key Analytical Observations Supporting The Above Data:

- Vaccine Development’s 28.7% dominance in 2025: post-pandemic vaccine manufacturing, strict regulatory safety requirements, and continued next-generation mRNA development by Pfizer, Moderna, and BioNTech are all ongoing industry realities.

- Cellular and Gene Therapy’s 22.4% share in 2025: Growth is driven by expanding advanced therapies, with dozens of approved ATMPs, over 3,200 active cell and gene therapy trials, and a pipeline exceeding 4,000 therapies, all requiring extensive biological safety testing across development stages.

- Kits and Reagents’ 41.3% product share: reflects their essential role in routine in-house laboratory testing workflows, including endotoxin, sterility, and bioburden testing, offering cost-effective, high-throughput solutions adopted broadly across pharma quality control labs.

- North America’s 38.8% global leadership in 2025: is anchored by hundreds of FDA-regulated biopharmaceutical manufacturing facilities, a mature CRO ecosystem, and stringent 21 CFR Part 610 and USP Chapter based compliance requirements governing safety, sterility, and quality testing for licensed biologics.

- Asia-Pacific’s 22.4% share in 2025: is expanding rapidly, driven by China’s National Medical Products Administration (NMPA) mandating enhanced biosafety standards, India’s growing biologics export sector, and Japan’s leadership in regenerative medicine approvals.

- Market concentration at the top: Charles River Laboratories and Eurofins Scientific are leading biological safety testing providers, holding a high-single-digit combined share in 2025, supported by significant investments in ATMP-specific infrastructure and expanding cell and gene therapy testing capabilities.

Global Biological Safety Testing Market Overview

Biological safety testing (BST) includes analytical procedures to detect harmful biological contaminants in pharmaceutical and biopharmaceutical products, such as sterility, endotoxin, bioburden, and adventitious agent testing. The ecosystem covers suppliers, manufacturers, testing labs, regulators, and end users across vaccines, blood products, and advanced therapies.

Market growth is driven by expanding biologics approvals, stricter regulatory requirements, rising ATMP development, and continued investment in biologics testing infrastructure. Additional support comes from increasing healthcare expenditure, strong biopharma R&D spending, and government initiatives promoting biosimilars and domestic vaccine manufacturing globally.

Market Dynamics

To evaluate market opportunities, Request Sample

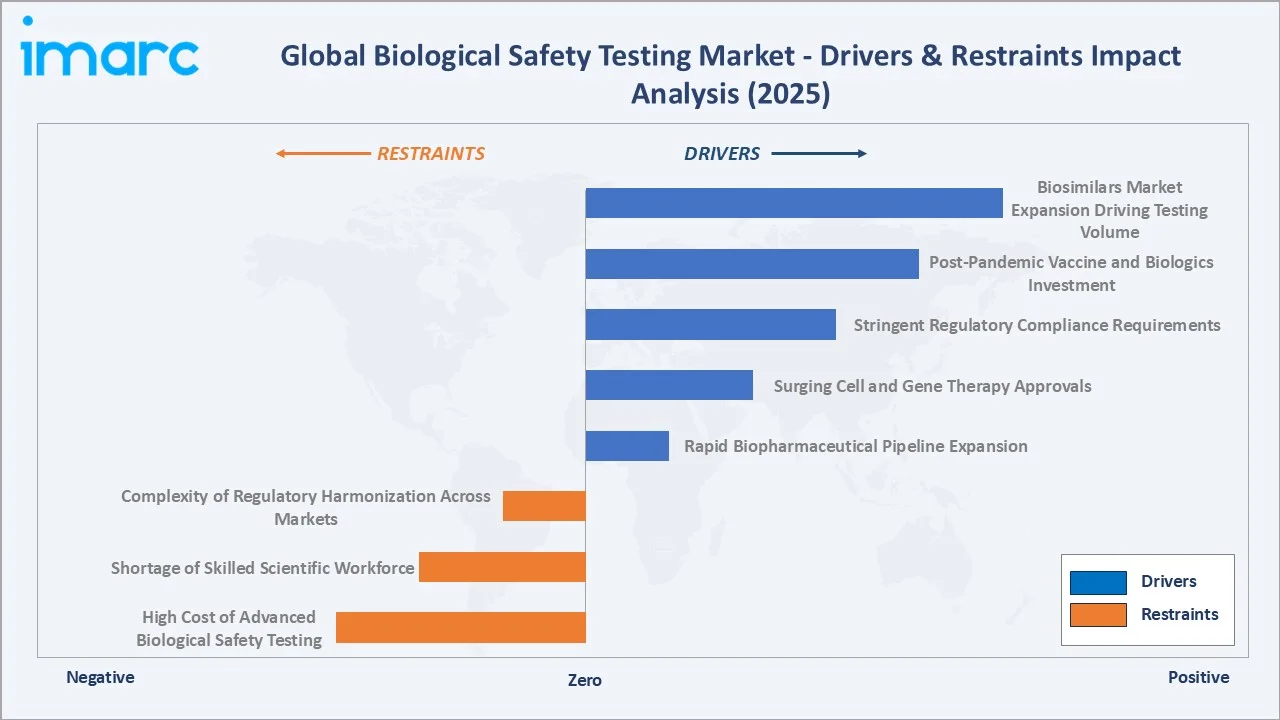

Market Drivers

- Rapid Biopharmaceutical Pipeline Expansion: Over 7,000 biologics and specialty therapies are currently in development globally, each requiring extensive safety evaluation under ICH Q5A, Q5B, and Q5D guidelines. These regulatory requirements drive sustained demand for biological safety testing products and services across all pipeline stages.

- Surging Cell and Gene Therapy Approvals: Regulatory approvals of advanced therapy medicinal products and a rapidly expanding cell and gene therapy pipeline are driving demand for biological safety testing. These therapies require specialized safety protocols, including viral vector characterization and adventitious agent detection, creating recurring high-value testing demand.

- Stringent Regulatory Compliance Requirements: Regulatory agencies including the FDA (21 CFR Part 610), EMA (EU GMP Annex 2), and WHO technical guidelines mandate biological safety testing as a prerequisite for approval of biologics, vaccines, and blood products, creating a captive and non-discretionary demand for biological safety testing services.

- Post-Pandemic Vaccine and Biologics Investment: Post-COVID-19, global vaccine development has expanded across infectious diseases, oncology, and mRNA platforms. This growth is driving sustained demand for biological safety testing, including viral vector characterization and adventitious agent detection, resulting in recurring high-volume testing needs.

Market Restraints

- High Cost of Advanced Biological Safety Testing: Advanced biological safety testing, including adventitious agent detection and ATMP safety testing, involves complex requirements and specialized facilities, leading to high costs that create financial barriers for small biotech companies.

- Shortage of Skilled Scientific Workforce: Specialized BST laboratories require skilled experts in virology, microbiology, and molecular biology. A global shortage of qualified professionals’ limits capacity expansion, particularly in emerging Asian and Latin American markets.

- Complexity of Regulatory Harmonization Across Markets: Divergent safety testing standards across the US, EU, Japan, and China require manufacturers to conduct duplicate or modified testing protocols for multi-market registrations, increasing operational complexity and cost, particularly for global biosimilar developers.

Market Opportunities

- Biosimilars Market Expansion Driving Testing Volume: Growing biosimilar development requires comprehensive comparability testing, viral safety assessments, and bioburden analysis. These regulatory requirements generate substantial incremental biological safety testing demand throughout the forecast period.

- Emerging Markets Pharmaceutical Manufacturing Growth: India’s expanding biologics exports and China’s growing biosimilar approvals are increasing biological safety testing demand. Over 50 biosimilars approved by China’s NMPA require extensive safety testing, driving BST growth in both markets.

- Adoption of Rapid Microbiological Methods (RMMs): Regulatory acceptance of rapid microbiological methods under USP <1071> and EU Ph. Eur. 5.1.6 enables faster sterility testing, reducing timelines from 14 days to under 48 hours and accelerating ATMP product release.

Market Challenges

- Evolving Regulatory Landscape for ATMPs: Rapidly evolving FDA and EMA guidelines for advanced therapy products create compliance uncertainty. Manufacturers must continually update BST protocols to align with new guidance documents, increasing investment in regulatory affairs and testing infrastructure.

- Supply Chain Vulnerabilities for Critical Reagents: Certain biological reagents – such as Limulus Amoebocyte Lysate (LAL) for endotoxin testing – depend on limited natural sources (horseshoe crabs). Supply constraints and sustainability concerns are creating raw material availability risks for BST kit manufacturers.

- High Capital Investment in ATMP-Specific Testing Infrastructure: Viral vector and gene therapy testing facilities require BSL-2/3 containment, GMP cleanrooms, and specialized equipment, leading to high capital investments and creating barriers for new ATMP testing laboratories.

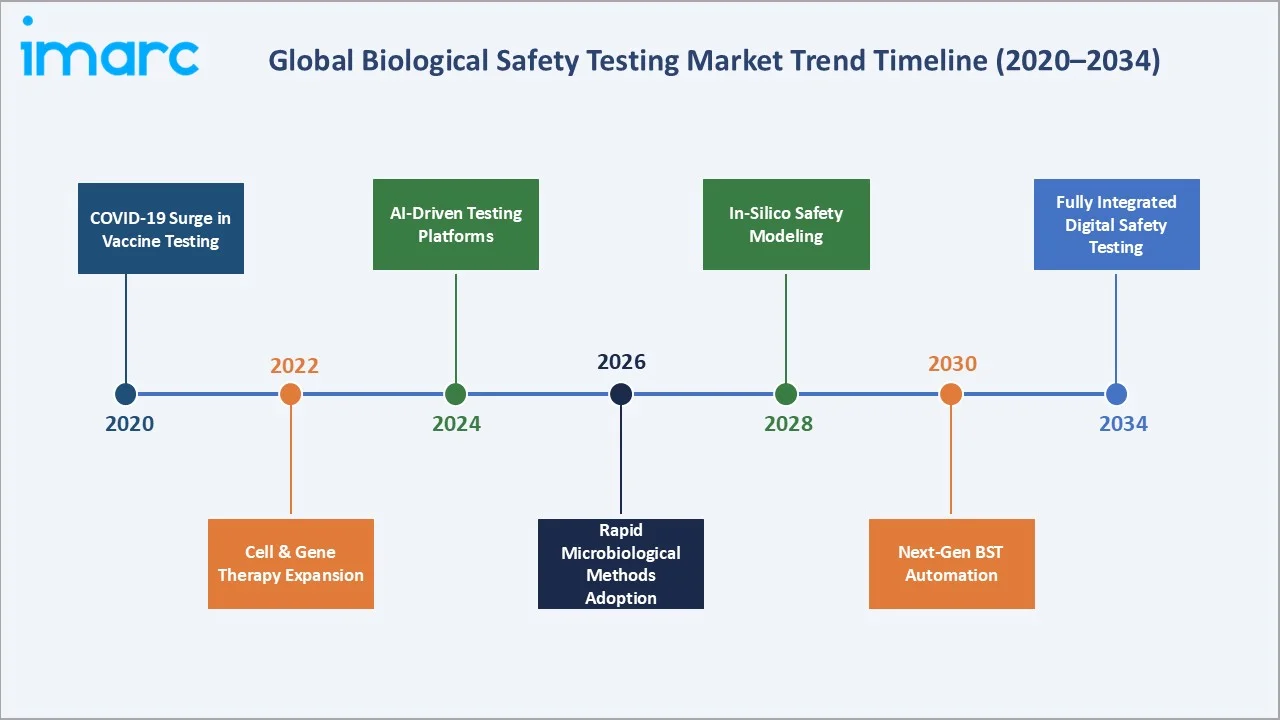

Emerging Market Trends

1. Adoption of Next-Generation Sequencing (NGS) in Safety Testing

NGS-based adventitious agent detection is gaining regulatory acceptance as an alternative to traditional cell-culture methods. Recent FDA-aligned guidance supports NGS for viral safety evaluation, enabling simultaneous detection of known and unknown contaminants and broader coverage than conventional assays.

2. Rise of Rapid Microbiological Methods (RMMs)

Automated RMM platforms, including ATP bioluminescence and flow cytometry systems, are replacing traditional sterility tests, with adoption rising in ATMP manufacturing due to short shelf-lives of autologous cell therapies.

3. Integration of AI and Machine Learning in BST Analysis

Artificial intelligence platforms are being deployed for data interpretation, anomaly detection, and predictive quality control in biological safety testing workflows. AI-driven analytics reduce manual review effort, improve assay interpretation, and enable real-time risk assessment across multi-site manufacturing operations.

4. Expansion of CRO-Based Outsourced Safety Testing

Global biopharmaceutical companies are increasingly outsourcing biological safety testing to specialist CROs to reduce capital expenditure, access specialized expertise, and accelerate regulatory timelines, driving faster adoption of outsourced testing services.

5. Synthetic Biology Alternatives to Animal-Derived Testing Materials

Recombinant Factor C (rFC), a synthetic alternative to LAL endotoxin testing, is gaining regulatory acceptance across major pharmacopoeias. European Pharmacopoeia adoption and recent USP/FDA-aligned guidance are accelerating transition away from horseshoe crab-derived reagents, transforming endotoxin testing supply chains.

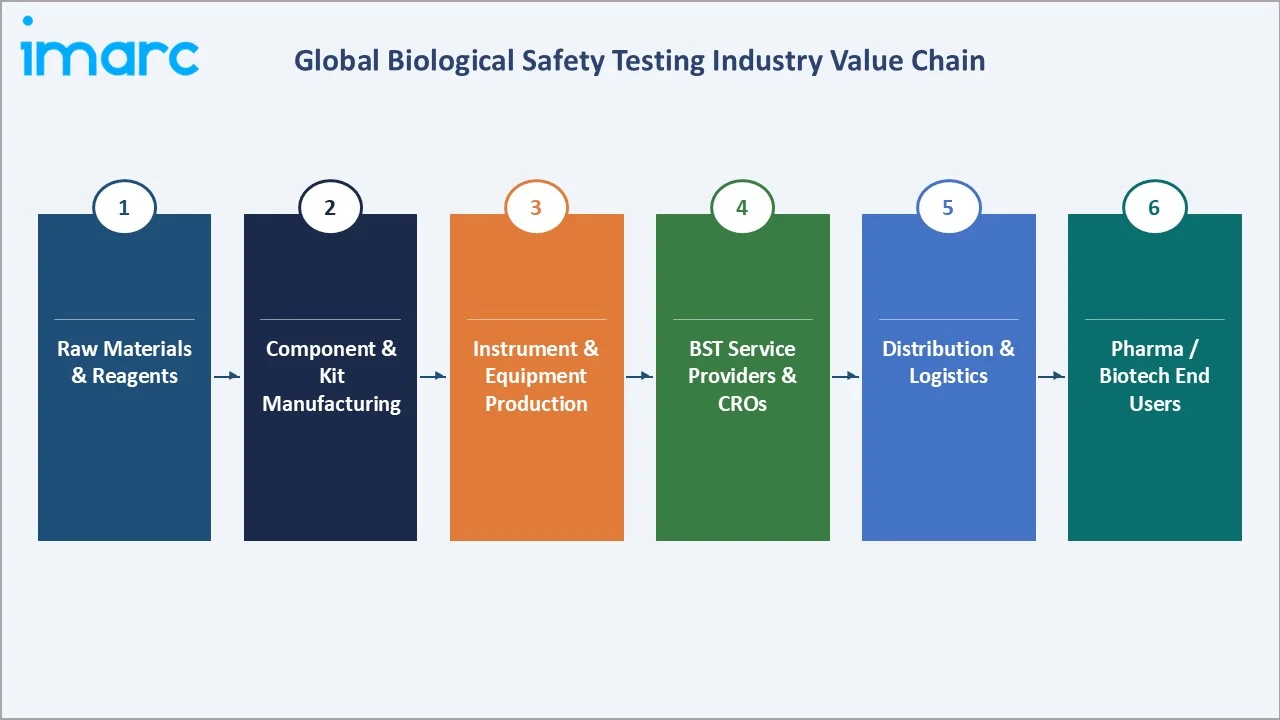

Industry Value Chain Analysis

The biological safety testing value chain spans six distinct stages, from raw biological materials to final end-user reporting, each presenting unique competitive dynamics and regulatory requirements.

|

Stage |

Key Players / Examples |

|

Raw Materials & Biological Reagents |

LAL suppliers (Associates of Cape Cod), rFC producers, cell culture media suppliers, microbial reference strains (ATCC, DSMZ) |

|

BST Kits & Reagent Manufacturing |

Lonza Group AG, Maravai LifeSciences |

|

Instrument & Equipment Production |

Sartorius AG, bioMerieux, Becton Dickinson |

|

Contract Research Organizations (BST Services) |

Eurofins Scientific, SGS SA, Pacific BioLabs, WuXi Biologics |

|

Distribution & Logistics |

Specialty life science distributors, cold chain logistics providers, VWR |

|

End Users |

Biopharmaceutical companies, vaccine manufacturers, blood banks, hospital compounding pharmacies, cell therapy developers |

Tier-1 CROs and kit manufacturers lead the value chain through strong scientific expertise, regulatory knowledge, and advanced platforms like NGS and rapid microbiology, creating competitive advantages over smaller regional laboratories.

Technology Landscape in the Biological Safety Testing Industry

Next-Generation Sequencing and Metagenomic Analysis

NGS-based platforms are gaining regulatory acceptance as alternatives to conventional cell-culture methods for adventitious agent detection. Updated ICH Q5A(R2) guidance endorsed by FDA and EMA supports NGS for viral safety studies, accelerating adoption across biopharmaceutical manufacturers.

Rapid Microbiological Methods and Automation

Automated sterility and bioburden testing platforms, including ATP bioluminescence and flow cytometry, reduce traditional 14-day testing to 24–72 hours. These rapid systems are essential for short-shelf-life ATMPs and autologous cell therapies.

AI-Powered Data Analysis and Quality Management

Machine learning algorithms are increasingly integrated into BST laboratory information management systems to automate data review, detect anomalies, and predict contamination risks. AI-driven quality analytics reduce manual investigation time and improve regulatory compliance across manufacturing operations.

Digital PCR and Quantitative Molecular Methods

Digital PCR platforms provide absolute quantification of viral contamination and mycoplasma without calibration curves, offering higher sensitivity than conventional qPCR. Adoption is increasing for viral clearance validation and contamination testing in ATMP and vaccine manufacturing.

Market Segmentation Analysis

The report covers the following segments:

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Product and Services | Kits and Reagents | 41.3% | 2025 |

| Test Type | Endotoxin Tests | 24.9% | 2025 |

| Application | Vaccine Development | 28.7% | 2025 |

| Region | North America | 38.8% | 2025 |

By Application

Vaccine development leads the biological safety testing market with a 28.7% share in 2025, driven by mandatory viral safety, sterility, and potency testing under WHO guidelines and continued investment in next-generation vaccines. Cellular and gene therapy, holding 22.4% in 2025, is the fastest-growing segment due to expanding ATMP approvals and clinical pipeline growth.

To access detailed market analysis, Request Sample

Blood products testing holds 18.6% in 2025, driven by mandatory pathogen screening regulations. Tissue-related products testing accounts for 16.8%, while stem cell research at 13.5% is expanding due to growing adoption of regenerative medicine and tissue engineering globally.

By Product and Services

Kits and reagents lead with a 41.3% share in 2025, driven by cost-effective, standardized in-house testing compliant with global pharmacopeial standards. Services hold 32.4%, supported by increasing outsourcing of biological safety testing to specialized CROs.

Instruments account for 26.3% in 2025, including automated microbiology systems, endotoxin analyzers, flow cytometers, and PCR platforms. Adoption is increasing as manufacturers invest in automated BST infrastructure to enhance throughput, data integrity, and regulatory compliance.

Regional Market Insights

|

Region |

Share (2025) |

Key Growth Drivers |

|

North America |

38.8% |

Dense FDA-regulated biopharma manufacturing base; leading CRO ecosystem (Charles River, Pacific BioLabs); strong ATMP and vaccine development pipeline |

|

Europe |

27.5% |

EMA regulatory framework; established pharma clusters in Germany, Switzerland, UK; leadership of Eurofins Scientific and SGS SA in contract BST services |

|

Asia-Pacific |

22.4% |

Rapid biosimilar manufacturing expansion in China and India; NMPA and CDSCO regulatory tightening; Japan’s regenerative medicine sector growth |

|

Latin America |

6.8% |

Brazil and Mexico domestic vaccine manufacturing expansion; Fiocruz (Brazil) biosafety testing programs; growing biologics regulatory standards alignment |

|

Middle East & Africa |

4.5% |

Saudi Arabia and UAE pharmaceutical manufacturing investment; Africa CDC biologics quality initiative; WHO-supported national laboratory capacity building |

North America commands a 38.8% global revenue share in 2025, supported by a large base of FDA-licensed biologics manufacturers, leading CRO laboratories, and strong NIH and biopharma R&D investment. The U.S. dominates the regional market due to stringent biologics testing regulations.

Europe holds 27.5% in 2025, driven by Germany’s biopharma cluster, Swiss CROs like Lonza and SGS, and strong EMA compliance. Asia-Pacific at 22.4% is the fastest-growing region, supported by China’s “Made in China 2025” and India’s expanding vaccine manufacturing capacity.

Competitive Landscape

|

Company Name |

Key Brand / Platform |

Market Position |

Core Strength |

|

Charles River Laboratories International, Inc. |

Accugenix®, Endosafe® Testing |

Leader |

Broad BST portfolio; global CRO scale; ATMP & viral safety expertise |

|

Eurofins Scientific SE |

Eurofins BioPharma Product Testing |

Leader |

Largest testing network globally; integrated biopharma compliance services |

|

Lonza Group AG |

Lonza / Lonza Bioscience |

Leader |

Integrated biologics CDMO + BST; endotoxin & mycoplasma leadership |

|

Sartorius AG |

Microsart® |

Leader |

Instruments & filtration; lab automation; strong ATMP presence |

|

SGS Société Générale de Surveillance SA |

SGS Life Sciences (Biosafety Services) |

Challenger |

Global testing network; multi-sector pharma quality testing expertise |

|

WuXi Biologics |

WuXi Biologics Biosafety Testing |

Challenger |

Asia-Pacific leadership; integrated biologics CDMO-testing model |

|

Maravai LifeSciences Holdings, Inc. |

Cygnus Technologies |

Challenger |

mRNA & nucleic acid safety testing; high-growth ATMP focus |

|

Pacific BioLabs, Inc. |

Pacific BioLabs Testing Services |

Emerging |

GMP-compliant US regional BST services; NIH and FDA audit expertise |

The biological safety testing market is dominated by a concentrated group of global leaders along with specialized regional CROs. Charles River Laboratories and Eurofins Scientific together account for approximately 25–28% of global biological safety testing services revenue in 2025, supported by their broad testing capabilities, global lab networks, and strong regulatory expertise across FDA, EMA, and ICH frameworks.

Key Company Profiles

Charles River Laboratories International, Inc.

Headquartered in Wilmington, Massachusetts, USA, Charles River Laboratories is a global CRO and biologics testing provider serving pharmaceutical, biotechnology, and government clients. The company reported USD 4.05 billion in FY 2024 revenue, with its Manufacturing Solutions segment offering biological safety testing, microbial solutions, viral safety testing, and cell banking services for biologics and advanced therapy developers.

- Product & Service Portfolio: Endotoxin testing (LAL/rFC), sterility testing, mycoplasma detection, viral safety testing, cell line authentication (Accugenix®), bioburden testing, microbial identification, adventitious agent detection, cell & viral banking, and lot release testing.

- Recent Developments: In 2025, Charles River expanded its Cell & Gene Therapy Incubator Program to support ATMP, gene therapy, and biologics developers by providing integrated testing, development, and manufacturing services, aimed at accelerating advanced therapy development. In 2024, company launched the Alternative Methods Advancement Project, focusing on non-animal testing, AI-based safety evaluation, and faster biologics safety testing to accelerate therapy development while maintaining regulatory compliance.

- Strategic Focus: Charles River focuses on ATMP safety testing leadership, NGS-based microbial detection, viral vector testing expansion, Asia-Pacific growth, and strengthening integrated CRO-to-BST service offerings for biopharmaceutical clients.

Eurofins Scientific SE

Eurofins Scientific, headquartered in Luxembourg, operates over 950 laboratories across 60 countries and reported EUR 6.95 billion revenue in 2024. Its BioPharma Product Testing division provides biological safety testing and pharmaceutical quality services to global pharmaceutical and biotechnology companies.

- Product & Service Portfolio: Sterility testing, endotoxin testing, mycoplasma detection, viral safety testing, cell line testing, bioburden testing, and pharmaceutical microbiology services through GMP-compliant laboratories.

- Recent Developments: In 2025, Eurofins expanded its global BioPharma testing infrastructure, adding approximately 46,000 m² of laboratory space across North America and Europe to support growing demand for biologics and advanced therapy safety testing services. In 2025, Eurofins Viracor BioPharma Services opened a new 8,800 m² state-of-the-art laboratory in Lenexa, Kansas (U.S.), strengthening capabilities in cell and gene therapy, biologics, biomarker, and infectious disease testing.

- Strategic Focus: Eurofins focuses on global laboratory expansion, ATMP testing services, digital laboratory systems, and strategic acquisitions to strengthen biological safety testing capabilities.

Lonza Group AG

Headquartered in Basel, Switzerland, Lonza Group AG is a leading global CDMO supporting pharmaceutical and biotechnology companies. The company reported CHF 6.6 billion revenue in 2024, with biologics and cell & gene technologies driving growth. Lonza provides QC testing technologies, endotoxin detection systems, and rapid microbiology solutions supporting biologics safety and manufacturing.

- Product & Service Portfolio: LAL and rFC endotoxin testing, rapid microbial detection, mycoplasma detection tools, bioburden testing solutions, contamination testing, and biologics QC testing technologies.

- Recent Developments: In 2025, Lonza announced the acquisition of Redberry SAS, a company specializing in rapid microbiology testing solutions, to strengthen its biological safety and contamination detection capabilities for pharmaceutical and biologics manufacturing. The acquisition adds the Red One™ platform, improving speed and sensitivity in microbial detection for QC laboratories.

- Strategic Focus: Lonza focuses on integrated biologics manufacturing, rFC endotoxin testing leadership, rapid microbial detection technologies, and expansion of cell and gene therapy manufacturing globally.

Market Concentration Analysis

The global biological safety testing market exhibits moderate-to-high concentration at the top tier, with the top five players – Charles River Laboratories, Eurofins Scientific, Lonza Group, Sartorius AG, and SGS SA – collectively accounting for approximately 45–50% of global market revenue in 2025. This concentration reflects the significant capital requirements for GMP-compliant BST laboratory infrastructure, regulatory expertise, and the breadth of testing portfolios required to serve large pharmaceutical clients.

Below the top tier, the market is highly fragmented, with regional CROs, national laboratories, and university-affiliated centres serving domestic pharmaceutical clients. This dual structure is typical in regulated testing markets, where global leaders handle multinational pharma companies, while regional players support domestic biotech and generic manufacturers.

Market consolidation is accelerating due to the need for global lab networks, ATMP testing capabilities, and digital platforms. Acquisitions by Charles River and Eurofins’ network expansion reflect this trend, while rising regulatory and technology requirements are expected to further pressure smaller BST providers through 2034.

Investment & Growth Opportunities

Fastest-Growing Segments

Cell and gene therapy safety testing represents a high-growth opportunity in the BST market through 2034. With over 3,000+ therapies and thousands of clinical trials globally, increasing approvals and complex regulatory requirements are driving demand for specialized infrastructure such as BSL-2/3 laboratories, viral vector testing, and advanced analytical capabilities—creating premium opportunities for specialized CRO providers.

RMM-based automated testing is a fast-growing segment driven by increasing regulatory acceptance and demand for rapid-release testing in ATMPs. Unlike traditional 14-day sterility tests, rapid methods deliver results within hours to days, enabling faster product release and supporting premium-margin opportunities despite higher costs.

Emerging Market Expansion

Asia-Pacific, currently at 22.4% of global market share in 2025, offers the strongest geographic growth opportunity through 2034. China’s NMPA alignment with ICH standards, India’s National Biopharma Mission expanding biologics capabilities, and South Korea’s K-BIO initiatives are collectively driving rapid biopharma expansion and increasing demand for biological safety testing capacity.

Venture & Strategic Investment Trends

Venture investment in rapid microbiology, NGS-based pathogen detection, and AI-driven BST platforms is accelerating, supported by growing demand for rapid biologics testing. Strategic acquisitions such as Charles River’s purchase of PathoQuest, Lonza’s acquisition of Redberry, and Eurofins’ ongoing lab expansion reflect strong investor confidence in ATMP testing’s high-margin, regulatory-driven growth opportunity.

Future Market Outlook (2026-2034)

The global biological safety testing market is projected to grow from USD 5.46 Billion in 2025 to USD 14.62 Billion by 2034, representing a CAGR of 9.97%, reflecting sustained high-growth expansion. Growth is driven by ATMP commercialization, expanding biosimilar pipelines, Asia-Pacific biopharma manufacturing growth, and increasingly stringent global biologics safety regulations.

Three transformational forces will reshape the BST market through 2034. First, NGS-based molecular diagnostics are increasingly replacing conventional cell-culture testing, improving sensitivity and reducing timelines. Second, AI-enabled LIMS and predictive quality platforms are automating compliance and data analysis, lowering per-test costs. Third, personalized medicine and autologous ATMP commercialization require individualized safety testing protocols, creating new premium-priced BST service segments.

By 2034, the biological safety testing industry is expected to become highly automated, technology-driven, and globally networked. CROs and kit manufacturers investing in NGS, rapid microbiological methods, and AI-enabled analytics are positioned to capture strong growth, driven by expanding cell and gene therapies, biosimilars, and next-generation biologics pipelines requiring advanced safety testing capabilities.

Research Methodology

Primary Research

Primary research included structured interviews and surveys conducted in 2024–2025 with biological safety testing stakeholders, including quality leaders at top biopharma companies, BST CRO laboratory directors, regulatory affairs professionals, and cell and gene therapy developers across North America, Europe, and Asia-Pacific.

Secondary Research

Secondary research included company reports (Charles River, Eurofins, Lonza, Sartorius, SGS), regulatory guidelines (FDA, EMA, ICH, WHO), peer-reviewed journals, industry association data (BIO, EFPIA, PhRMA), and government biopharma investment and approval databases.

Forecasting Models

Market estimates were developed using top-down and bottom-up models, incorporating biologics pipeline data, approval rates, testing frequency, outsourcing trends, regional manufacturing investments, and macroeconomic scenarios under base, optimistic, and conservative assumptions.

Biological Safety Testing Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products and Services Covered | Kits and Reagents, Instruments, Services |

| Test Types Covered | Endotoxin Tests, Sterility Tests, Cell Line Authentication and Characterization Tests, Bioburden Tests, Residual Host Contaminant Detection Tests, Adventitious Agent Detection Tests, Others |

| Applications Covered | Vaccine Development, Blood Products Testing, Cellular and Gene Therapy, Tissue and Tissue-related Products Testing, Stem Cell Research |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | Charles River Laboratories International, Inc., Eurofins Scientific SE, Lonza Group AG, Sartorius AG, SGS Société Générale de Surveillance SA, WuXi Biologics, Maravai LifeSciences Holdings, Inc., Pacific BioLabs, Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the biological safety testing market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global biological safety testing market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyse the level of competition within the biological safety testing industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Frequently Asked Questions About the Biological Safety Testing Market Report

The global biological safety testing market was valued at USD 5.46 Billion in 2025, driven by biopharmaceutical pipeline expansion, cell and gene therapy growth, and regulatory compliance requirements.

The market is projected to reach USD 14.62 Billion by 2034, at a CAGR of 9.97% during 2026-2034, driven by ATMP approvals, biosimilar expansion, and Asia-Pacific pharma manufacturing growth.

Vaccine Development leads with a 28.7% share in 2025, driven by mandatory viral safety, sterility, and potency testing requirements at each stage of vaccine manufacturing globally.

Kits and Reagents dominate with a 41.3% share in 2025, driven by widespread in-house laboratory adoption for routine endotoxin, sterility, and bioburden testing workflows.

North America leads with a 38.8% share in 2025, supported by a large FDA-regulated biopharmaceutical manufacturing base and a dense CRO laboratory ecosystem providing compliant biological safety testing services.

Key drivers include biopharmaceutical pipeline expansion, cell and gene therapy approvals, stringent FDA/EMA/ICH regulatory compliance, post-pandemic vaccine investment, and biosimilar market growth.

Asia-Pacific is the fastest-growing region at 22.4% share in 2025, driven by China’s biologics scale-up, India’s vaccine export ambitions, and South Korea’s biosimilar manufacturing expansion through 2034.

Leading companies include Charles River Laboratories International, Inc., Eurofins Scientific SE, Lonza Group AG, Sartorius AG, SGS Société Générale de Surveillance SA, WuXi Biologics, Maravai LifeSciences Holdings, Inc., and Pacific BioLabs, Inc.

NGS-based detection, rapid microbiological methods, AI-powered data analysis, and digital PCR are revolutionizing BST, reducing timelines from 14 days to 24–48 hours and improving detection sensitivity.

Key trends include NGS adoption, rapid microbiological methods, AI-integrated quality platforms, synthetic endotoxin testing materials, and Asia-Pacific BST laboratory capacity expansion through 2034.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)