Biosurgery Market Report by Product (Bone-Graft Substitutes, Soft-Tissue Attachments, Hemostatic Agents, Surgical Sealants and Adhesives, Adhesion Barriers, Staple Line Reinforcement), Source (Natural/Biologics Products, Synthetic Products), Application (Orthopedic Surgery, General Surgery, Neurological Surgery, Cardiovascular Surgery, Gynecological Surgery, and Others), End User (Hospitals, Clinics, and Others), and Region 2026-2034

Biosurgery Market Size:

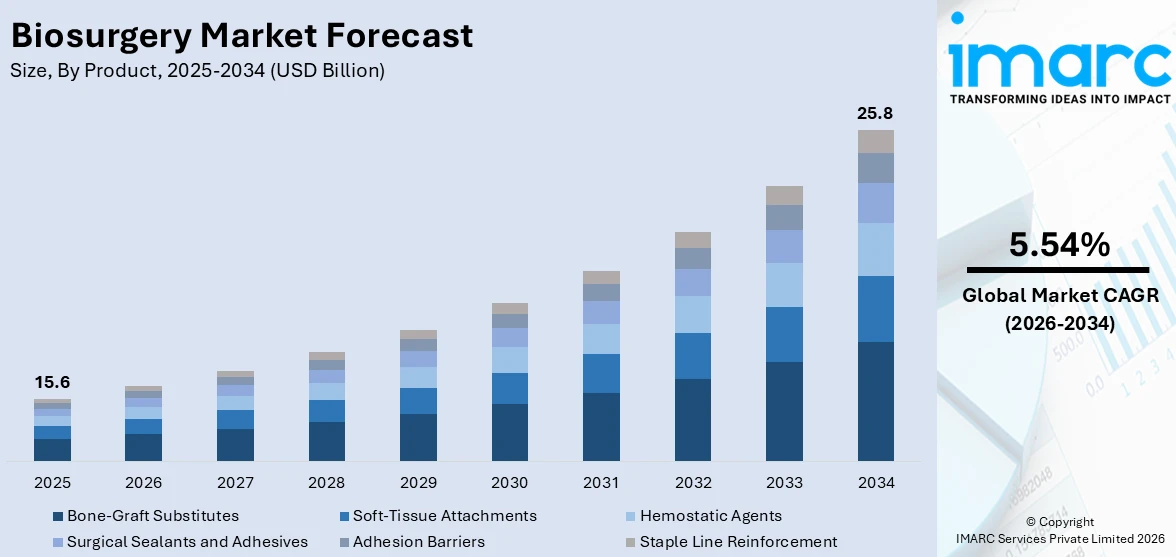

The global biosurgery market size reached USD 15.6 Billion in 2025. Looking forward, IMARC Group expects the market to reach USD 25.8 Billion by 2034, exhibiting a growth rate (CAGR) of 5.54% during 2026-2034. North America was the largest regional market for biosurgery owing to the advanced healthcare infrastructure, significant investments in research and development (R&D) activities, and the presence of leading players who drive innovation and expansion. Moreover, the increasing surgical procedures, technological advancements in medical devices, and growing demand for effective wound management in complex surgeries is enhancing surgical outcomes and recovery times for patients across the globe.

Market Size & Forecasts:

- Biosurgery market was valued at USD 15.6 Billion in 2025.

- The market is projected to reach USD 25.8 Billion by 2034, at a CAGR of 5.54% from 2026-2034.

Dominant Segments:

- Product: Bone-graft substitutes account for the majority of the market share as they play a critical role in many surgical operations, supporting bone regeneration and repair in orthopedics, trauma, spine surgery, and dentistry applications.

- Source: Natural/biologics products hold the largest share due to their effective healing properties and biocompatibility.

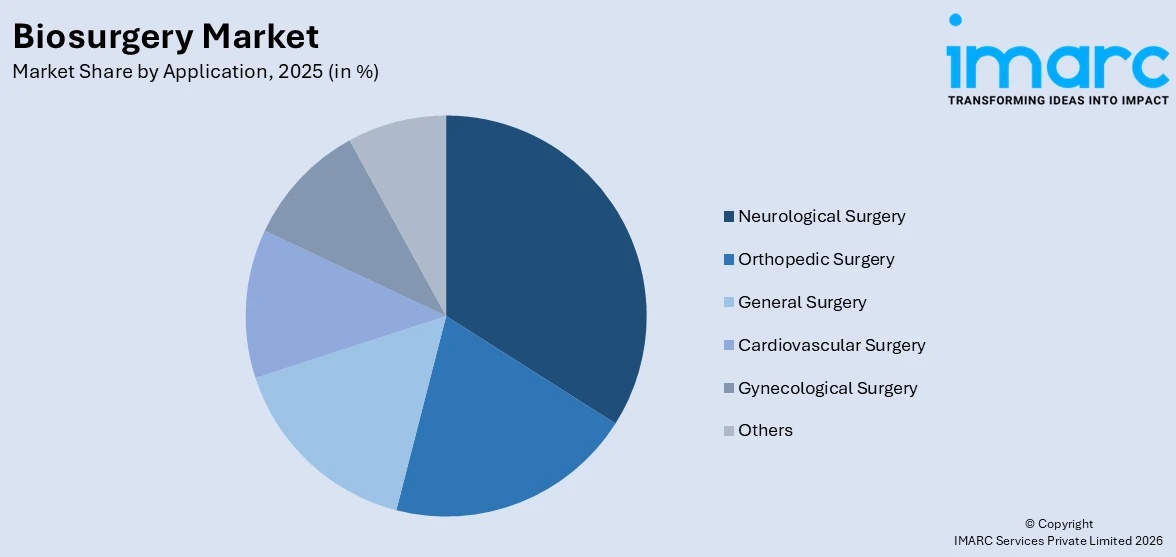

- Application: Neurological surgery represents the leading market segment as biosurgery products, such as sealants, hemostatic agents, and adhesion barriers, are extensively used in neurological procedures to manage bleeding, seal tissues, and reduce post-operative complications.

- End User: Hospital exhibits a clear dominance in the market as they offer a wide array of surgical procedures that frequently utilize biosurgical products.

- Region: North America leads the market because of the developed healthcare infrastructure, substantial funding in research and development (R&D) efforts, and the availability of major companies that promote innovation and growth.

Key Players:

- The leading companies in HFCV market include B. Braun Melsungen AG, Baxter International Inc., Becton Dickinson and Company, CryoLife Inc., CSL Limited, Hemostasis LLC, Integra Lifesciences Holdings Corporation, Johnson & Johnson, Medtronic plc, Pfizer Inc., Sanofi S.A., Smith & Nephew plc, Stryker Corporation, Surgalign Spine Technologies Inc., etc.

Key Market Growth Drivers:

- Growing Healthcare Requirements: Rising demand for sophisticated surgical solutions is driving the use of biosurgery products, as they provide superior healing and minimal recovery.

- Improvements in Technology: Continuous advancements in biologic material, like novel wound care products and tissue-engineered solutions, are enhancing the efficacy and usability of biosurgical methods.

- Aging Population: The growth in the global aging population is driving the need for intricate surgical procedures, thereby creating the demand for biosurgical products to achieve improved surgical recovery and faster recovery.

- Minimally Invasive Surgeries: The movement toward minimally invasive surgery (MIS) techniques is encouraging the uptake of biosurgery products since they help in quicker recovery and less risk of complications.

- Government Support and Regulation: Governments are actively promoting the development and approval of biosurgical products through the delivery of regulatory support and economic incentives to stimulate innovation in the industry.

Future Outlook:

- Sustained Market Growth: The biosurgery market is anticipated to continue growth, driven by continued technological advancements, a growing older population, and a quest for enhancing surgical outcomes and patient recovery.

- Expanding Application Base: The market is transforming with a broadening application base covering trauma care, wound healing, and tissue repair, which reflects a surge in demand in different surgical specialties and geographies.

The market for biosurgery is undergoing immense changes with the advancement of medical technologies and evolving healthcare requirements. The growing promise and complexity of biosurgical technologies are stimulating more interaction between the medical sector and academic centers. Academic institutions and research institutes are taking center stage in investigating new biologic materials, creating new surgical methods, and testing the efficacy of new products through clinical trials. This cooperative setting is developing the swift growth of innovative biosurgical solutions, as manufacturers and scientists collaborate to advance new products to market more quickly. In addition, academic centers play an active role in training future surgeons about the advantages and applications of biosurgery. With increasing numbers of healthcare professionals being trained in the handling of biologically derived products, the uptake and acceptance of these products in clinical practice is also growing. Collaborative research endeavors are also refining the understanding of complicated biological mechanisms, and useful insights are being utilized in developing improved biosurgical solutions that can benefit various patient groups.

To get more information on this market Request Sample

Biosurgery Market Trends:

Technological Progress in Biosurgical Products

Technological developments are contributing tremendously to the faster growth of the biosurgery market. Ongoing improvements in biologic materials are increasing the efficiency of products like hemostats, adhesives, and tissue-engineered products. Companies are targeting more efficient, biocompatible, and sustainable surgical products. For instance, advances in bioactive materials that promote faster wound healing and enhance tissue regeneration are revolutionizing the space. In addition, development in 3D printing technology is facilitating the production of personalized implants and surgical instruments, making way for more efficient and tailor-made surgical interventions. These developments not only enhance surgical performance but also make biosurgical products more accessible and affordable. With new technologies coming onto the scene, the scope of biosurgical solutions is increasing, treating more types of surgical requirements and facilitating improved patient care across a variety of medical specialties. 3D Systems revealed that, in partnership with University Hospital Basel (Switzerland), the Company’s exclusive point-of-care additive manufacturing solution is utilized to create the world’s first 3D-printed PEEK facial implant compliant with Medical Device Regulation (MDR). Prof. Florian Thieringer and Dr. Neha Sharma, along with their team of biomedical engineers, effectively created and produced a tailored device to meet a patient’s specific requirement utilizing 3D Systems technology and manufacturing knowledge. This implant was utilized in a successful operation finished at the hospital on March 18, 2025.

Increased Demand for Minimally Invasive Procedures

The heightened need for minimally invasive procedures is one of the fundamental growth drivers in the market. As medical practitioners and patients aim to minimize the recovery time and risks involved with conventional open surgeries, more minimally invasive procedures are being performed. These surgeries, in most cases, entail smaller cuts, less trauma to the tissues around them, and less blood loss, resulting in shorter recovery periods and fewer complications. Biosurgical items, including hemostats and biologic adhesives, are part of these procedures as they facilitate better tissue sealing and bleeding control with accuracy. Surgeons are also employing biologic materials for better wound healing and the prevention of chances of infection in minimally invasive procedures. With the trend toward minimally invasive procedures in all specialties, the need for biosurgical solutions that enable these procedures is increasing, further fueling the market growth. IMARC Group predicts that the global minimally invasive surgery market is anticipated to reach USD 94.9 Billion by 2033.

Aging Global Population

The aging world population is playing a huge role in driving the biosurgery market. As per an article published by the World Health Organization (WHO) in 2025, the number of people aged 60 and above is anticipated to increase to 1.4 billion by 2030. As individuals grow older, they tend to develop a variety of ailments that call for surgeries, including joint replacements, cardiovascular procedures, and orthopedic procedures. Elderly patients generally possess slower recovery mechanisms and are more prone to surgical and post-surgical complications. These issues are being dealt with by biosurgical devices like tissue-engineered grafts, wound healing products, and biologic adhesives that are facilitating quicker recovery, minimizing the risk of infection, and optimizing tissue regeneration. Second, as older patients have more chronic diseases that necessitate continuous medical care, the need for sophisticated biosurgical solutions is also on the increase. The elderly population worldwide is therefore fueling the market growth since healthcare systems are increasingly embracing advanced technologies to enhance surgical outcomes and reduce recovery periods for older patients.

Biosurgery Market Growth Drivers:

Increasing Healthcare Costs and Sensitivity to Advanced Surgical Solutions

Health care spending is rising globally, and advanced surgical solutions, such as biosurgical products, are increasingly recognized as having advantages. Both healthcare professionals and patients are more aware today about the benefits that biologically engineered surgical products provide over conventional synthetic ones. These include lower healing times, fewer complications, and better biocompatibility, which are important for maximizing surgical outcomes. Healthcare systems, especially those in the developed world, are now investing heavily in such sophisticated solutions to enhance care quality and contain the costs of long-term recovery and complications. With more medical specialists adopting sophisticated surgical methods, biosurgical devices like bioactive dressings, tissue grafts, and biodegradable sutures are becoming part and parcel of a variety of procedures.

Increasing Incidence of Chronic Diseases and Surgical Surgeries

The increasing incidence of chronic diseases, including diabetes, cardiovascular disease, and obesity, is propelling the market growth. Most chronic diseases result in conditions that are likely to be treated with surgery, like diabetic ulcers, vascular surgeries, and joint replacements. As these conditions become more prevalent, the demand for novel surgical products that enhance faster recovery and lower complications is increasing. Biosurgical products like biologic solutions for wound care, tissue repair solutions, and hemostatics are finding growing use in surgeries to provide improved patient outcomes for chronic patients. For instance, biologic grafts and dressings play a crucial role in healing chronic, complicated wounds that are slow to heal in diabetic patients. With the growing global burden of chronic disease, the need for biosurgical products is spreading wide, making these products integral parts of contemporary surgical procedures.

Expanding Healthcare Access in Emerging Markets

Increased access to healthcare in emerging economies is bolstering the market growth. The developing world's improvement in healthcare infrastructure and access to sophisticated medical technology continues to catalyze the demand for biosurgical products. These nations are observing increased rates of surgeries in orthopedic, cardiovascular, and trauma care segments, which are driving the use of biosurgery products. As the populations become increasingly accessible to quality healthcare, biosurgical products with improved surgical outcomes are finding increased applications. Furthermore, numerous governments and healthcare systems are investing in projects aimed at enhancing surgical care and minimizing the incidence of medical complications, thus creating additional demand for biologically derived surgical solutions.

Biosurgery Market Segmentation:

IMARC Group provides an analysis of the key trends in each segment of the market, along with forecasts at the global, regional, and country levels for 2026-2034. Our report has categorized the market based on product, source, application and end user.

Breakup by Product:

- Bone-Graft Substitutes

- Soft-Tissue Attachments

- Hemostatic Agents

- Surgical Sealants and Adhesives

- Adhesion Barriers

- Staple Line Reinforcement

Bone-graft substitutes account for the majority of the market share

The report has provided a detailed breakup and analysis of the market based on the product. This includes bone-graft substitutes, soft-tissue attachments, hemostatic agents, surgical sealants and adhesives, adhesion barriers, and staple line reinforcement. According to the report, bone-graft substitutes represented the largest segment.

Bone-graft substitutes are crucial alternatives to bone grafting. These stand-ins play a critical role in many surgical operations, supporting bone regeneration and repair in orthopedics, trauma, spine surgery, and dentistry applications. They are intended to minimize the risk of donor site morbidity and infection by promoting bone development and replacing conventional autografts, which require removing bone from the patient's own body. Furthermore, the expansion is driven by the increasing frequency of bone and joint problems, the need for less intrusive operations, and developments in biomaterial technology. The growth of this market segment is also fueled by the creation of novel synthetic and composite grafts with improved osteoconductive and osteoinductive qualities. For instance, on 23 May 2023, Royal Biologics, Inc., a company focused on advanced cellular and autologous technologies for improved surgical outcomes, unveiled BIO-REIGN 3D. This innovative bone graft substitute is the first to use a natural hyper-crosslinked carbohydrate polymer. It is designed to enhance bone grafting procedures, and this proprietary technology is introduced alongside Royal Biologics' licensing agreement for Molecular Matrix's patented Osteo-P BGS technology.

Breakup by Source:

- Natural/Biologics Products

- Synthetic Products

Natural/biologics products hold the largest share of the industry

A detailed breakup and analysis of the market based on the source have also been provided in the report. This includes natural/biologics products and synthetic products. According to the report, natural/biologics products accounted for the largest market share.

According to the biosurgery market overview, natural/biologics represent the largest segment due to their effective healing properties and biocompatibility. These products, derived from substances that are naturally present in the human body or other biological sources, include fibrin sealants, collagen-based matrices, and chitosan-based solutions. Additionally, natural/biologics product’s ability to mimic natural physiological processes significantly reduces the risk of rejection and adverse reactions, making them highly preferred in surgical procedures. Moreover, market dominance is further supported by advancements in biotechnology that enhance the safety and efficacy of these materials. Consequently, the increasing demand for minimally invasive surgeries, coupled with the growing prevalence of chronic diseases requiring complex surgeries, continues to drive the growth of natural/biologics products in the market.

Breakup by Application:

Access the comprehensive market breakdown Request Sample

- Orthopedic Surgery

- General Surgery

- Neurological Surgery

- Cardiovascular Surgery

- Gynecological Surgery

- Others

Neurological surgery represents the leading market segment

The report has provided a detailed breakup and analysis of the market based on the application. This includes orthopedic surgery, general surgery, neurological surgery, cardiovascular surgery, gynecological surgery, and others. According to the report, neurological surgery represented the largest segment.

Neurological surgeries are complex and require critical precision. Additionally, biosurgery products, such as sealants, hemostatic agents, and adhesion barriers, are extensively used in neurological procedures to manage bleeding, seal tissues, and reduce post-operative complications. Moreover, the rising prevalence of neurological disorders, such as brain tumors, epilepsy, and Parkinson's disease, coupled with advancements in neurosurgical techniques are escalating the demand in this segment. Besides, the widespread adoption of minimally invasive (MI) surgeries, which require highly effective biosurgical solutions to enhance patient outcomes is further driving the biosurgery market growth. This trend is supported by technological innovations in biosurgery products, aimed at improving surgical outcomes and reducing recovery times.

Breakup by End User:

- Hospitals

- Clinics

- Others

Hospital exhibits a clear dominance in the market

A detailed breakup and analysis of the market based on the end user have also been provided in the report. This includes hospitals, clinics, and others. According to the report, hospitals accounted for the largest market share.

Hospitals offer a wide array of surgical procedures that frequently utilize biosurgical products. These products, which include hemostatic agents, surgical sealants, and adhesives, are integral in managing intraoperative and postoperative bleeding and promoting tissue healing. Additionally, hospitals' capacity to handle high patient volumes and conduct complex surgeries increases biosurgery demand. Additionally, the constant advancements in surgical techniques and the increasing preference for minimally invasive surgeries further amplify the utilization of biosurgical solutions in hospital settings.

Breakup by Region:

- North America

- United States

- Canada

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Australia

- Indonesia

- Others

- Europe

- Germany

- France

- United Kingdom

- Italy

- Spain

- Russia

- Others

- Latin America

- Brazil

- Mexico

- Others

- Middle East and Africa

North America leads the market, accounting for the largest biosurgery market share

The report has also provided a comprehensive analysis of all the major regional markets, which include North America (the United States and Canada); Europe (Germany, France, the United Kingdom, Italy, Spain, Russia, and others); Asia Pacific (China, Japan, India, South Korea, Australia, Indonesia, and others); Latin America (Brazil, Mexico, and others); and the Middle East and Africa. According to the report, North America was the largest regional market for biosurgery.

North America is the leading region due to the advanced healthcare infrastructure, significant investments in research and development (R&D) activities, and the presence of leading players who drive innovation and expansion. Additionally, the increasing prevalence of chronic diseases and the growing elderly population in North America contribute to a higher demand for biosurgical products. According to the biosurgery market forecast, these factors, combined with favorable government policies and a strong trend toward minimally invasive surgeries, will continue to strengthen North America's leading position in the global biosurgery market.

Competitive Landscape:

- The biosurgery market research report has also provided a comprehensive analysis of the competitive landscape in the market. Detailed profiles of all major companies have also been provided. Some of the major market players in the industry include B. Braun Melsungen AG, Baxter International Inc., Becton Dickinson and Company, CryoLife Inc., CSL Limited, Hemostasis LLC, Integra Lifesciences Holdings Corporation, Johnson & Johnson, Medtronic plc, Pfizer Inc., Sanofi S.A., Smith & Nephew plc, Stryker Corporation and Surgalign Spine Technologies Inc.

(Please note that this is only a partial list of the key players, and the complete list is provided in the report.)

- At present, biosurgery market players are actively enhancing market growth through a combination of strategic collaborations, innovative product launches, and expansions into new geographical markets. These companies invest heavily in research and development (R&D) to introduce advanced products that meet the increasing demands of minimally invasive surgeries and improved wound care. Additionally, market players are focusing on obtaining regulatory approvals across different regions, which helps in expanding their global footprint and accessing new markets. These strategies collectively contribute to the robust growth and resilience of the biosurgery market. For instance, in 2023, AROA Biosurgery Ltd. revealed the release of a new retrospective pilot case series that explores the use of Myriad Matrix and Myriad Morcells in the surgical treatment of contaminated volumetric soft tissue defects. It reviewed 13 complex traumatic wounds in 10 patients at a single facility. The study reported an average time of 23.4±9.2 days for achieving soft tissue coverage and fill, with a median of one product application and no complications among participants. Moreover, the research focused on injuries from motor vehicle accidents, abdominal dehiscence after hernia repair, Fournier’s Gangrene, compartment syndrome, and pressure injuries at a US Level 1 trauma center. It found that the Myriad products facilitated effective soft tissue formation with no reported complications, reinforcing the utility of AROA ECM products in trauma care.

Biosurgery Market News:

- June 2025: Dilon Technologies secured a $9 million growth capital investment from JGB Management to enhance its medical device offerings, featuring innovative technology for breast cancer surgery that greatly decreases the necessity for repeat operations.

- May 2025: Johnson & Johnson MedTech, a worldwide frontrunner in breast aesthetics and reconstruction, revealed the U.S. introduction of MENTOR™ MemoryGel™ Enhance Breast Implants, addressing a vital need in complete breast cancer treatment for women who have had a mastectomy.

- May 2025: Baxter's introduced the Hemopatch Sealing Hemostat, thereby signifying a major breakthrough in managing surgical bleeding. This advanced collagen-based pad features a dual-action system that merges a collagen matrix with a reactive NHS-PEG (N-hydroxysuccinimide polyethylene glycol) coating. When used on a bleeding area, this coating interacts with moisture to create a hydrogel that attaches to tissue and promptly seals it. The innovation is found in its enhanced hemostatic capabilities as well as the revised formulation that permits storage at room temperature and extends shelf life to three years, meeting essential logistical and clinical requirements.

- April 2025: Restor3D, a firm focused on 3D-printed, custom orthopedic implants, secured $38 million in growth funding to accelerate its expansion and introduce four new product lines over the next two years. The funding will support the commercialization of four entirely 3D-printed implant systems: the Veritas shoulder, iTotal Identity knee, Kinos ankle, and Velora hip cup.

- April 2025: After successfully finishing its first GMP (Good Manufacturing Practice) project, simAbs has opened a new GMP cleanroom facility in collaboration with Sealantium Medical, its latest neighbor and resident at Bioville. simAbs is a biotechnology firm based in Belgium, specializing in the research, development, and GMP manufacturing of antibodies. Sealantium Medical is a biosurgery enterprise dedicated to creating next-generation tissue sealants and hemostatic agents for surgical patients.

- March 2025: Olympus, an international medical expertise firm dedicated to improving people's health, safety, and quality of life, announced introduction of a new hemostasis clip to address the requirements of GI endoscopists. The Retentia™ HemoClip features 360° rotation and a user-friendly one-step deployment, allowing for controlled placement in three sizes to suit various closure needs.1 It is set to launch in the U.S. with intentions for broader global availability.

- January 2025: Aroa Biosurgery, a company focused on soft tissue regeneration and based in New Zealand, recently revealed the publication of additional robust clinical evidence supporting both the effectiveness and cost advantages of its AROA ECM™ technology in high-risk limb salvage surgery. Carried out from May 2022 to April 2023, the single-site prospective clinical study involved 130 complex lower limb defects from 120 patients. An astonishing 95% of participants in the research had at least one risk factor for lower limb amputation, while 55% had three or more predictive risk factors for amputation.

Biosurgery Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report | Exploration of Historical Trends and Market Outlook, Industry Catalysts and Challenges, Segment-Wise Historical and Future Market Assessment:

|

| Products Covered | Bone-Graft Substitutes, Soft-Tissue Attachments, Hemostatic Agents, Surgical Sealants and Adhesives, Adhesion Barriers, Staple Line Reinforcement |

| Sources Covered | Natural/Biologics Products, Synthetic Products |

| Applications Covered | Orthopedic Surgery, General Surgery, Neurological Surgery, Cardiovascular Surgery, Gynecological Surgery, Others |

| End Users Covered | Hospitals, Clinics, Others |

| Regions Covered | Asia Pacific, Europe, North America, Latin America, Middle East and Africa |

| Countries Covered | United States, Canada, Germany, France, United Kingdom, Italy, Spain, Russia, China, Japan, India, South Korea, Australia, Indonesia, Brazil, Mexico |

| Companies Covered | B. Braun Melsungen AG, Baxter International Inc., Becton Dickinson and Company, CryoLife Inc., CSL Limited, Hemostasis LLC, Integra Lifesciences Holdings Corporation, Johnson & Johnson, Medtronic plc, Pfizer Inc., Sanofi S.A., Smith & Nephew plc, Stryker Corporation, Surgalign Spine Technologies Inc., etc. |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Key Questions Answered in This Report:

- How has the global biosurgery market performed so far, and how will it perform in the coming years?

- What are the drivers, restraints, and opportunities in the global biosurgery market?

- What is the impact of each driver, restraint, and opportunity on the global biosurgery market?

- What are the key regional markets?

- Which countries represent the most attractive biosurgery market?

- What is the breakup of the market based on the product?

- Which is the most attractive product in the biosurgery market?

- What is the breakup of the market based on the source?

- Which is the most attractive source in the biosurgery market?

- What is the breakup of the market based on the application?

- Which is the most attractive application in the biosurgery market?

- What is the breakup of the market based on the end user?

- Which is the most attractive end user in the biosurgery market?

- What is the competitive structure of the market?

- Who are the key players/companies in the global biosurgery market?

Key Benefits for Stakeholders:

- IMARC’s industry report offers a comprehensive quantitative analysis of various market segments, historical and current market trends, market forecasts, and dynamics of the biosurgery market from 2020-2034.

- The research report provides the latest information on the market drivers, challenges, and opportunities in the global biosurgery market.

- The study maps the leading, as well as the fastest-growing, regional markets. It further enables stakeholders to identify the key country-level markets within each region.

- Porter's five forces analysis assists stakeholders in assessing the impact of new entrants, competitive rivalry, supplier power, buyer power, and the threat of substitution. It helps stakeholders to analyze the level of competition within the biosurgery industry and its attractiveness.

- The competitive landscape allows stakeholders to understand their competitive environment and provides insight into the current positions of key players in the market.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)

Related Reports

Choose your plan

*Please note that the prices mentioned below are starting prices for each bundle type. Kindly contact our team for further details.*

Single User License

- 1 User License, Access on 2 Devices

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- No Printing Rights

- 10% Free Report Customization

- 10–12 Weeks of Analyst Support

Five User License

- Access for 5 Users, 2 Devices per User

- PDF Report + Excel Dataset (Password Protected)

- Lifetime Access

- Dedicated Account Manager

- 12–14 Weeks of Analyst Support

- No Printing Rights

- 15% Free Report Customization

- 25% Discount on Your Next Purchase

Corporate User License

- Unlimited User Access (Within Your Organization)

- PDF Report + Excel Dataset

- Lifetime Access

- Dedicated Account Manager

- 14–20 Weeks of Analyst Support

- No Printing Rights

- 20% Free Report Customization

- 30% Discount on Your Next Purchase

Essential Insights

What's included:

3 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 2 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Professional Access

What's included:

5 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 8 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Business Advantage

What's included:

8 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 14 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade

Enterprise Intelligence

What's included:

10 reports

- Lifetime Access

- PDF Reports

- Excel Datasets

- 20 Weeks of Free Analyst Support

- 2 User Licenses

- Access on 2 Devices

- Printing Rights

- Complimentary PowerPoint (PPT) Version

- Complimentary License Upgrade