Brazil 3PL Market Size, Share, Trends and Forecast by Services, End User, and Region, 2026-2034

Brazil 3PL Market Size & Forecast 2026-2034

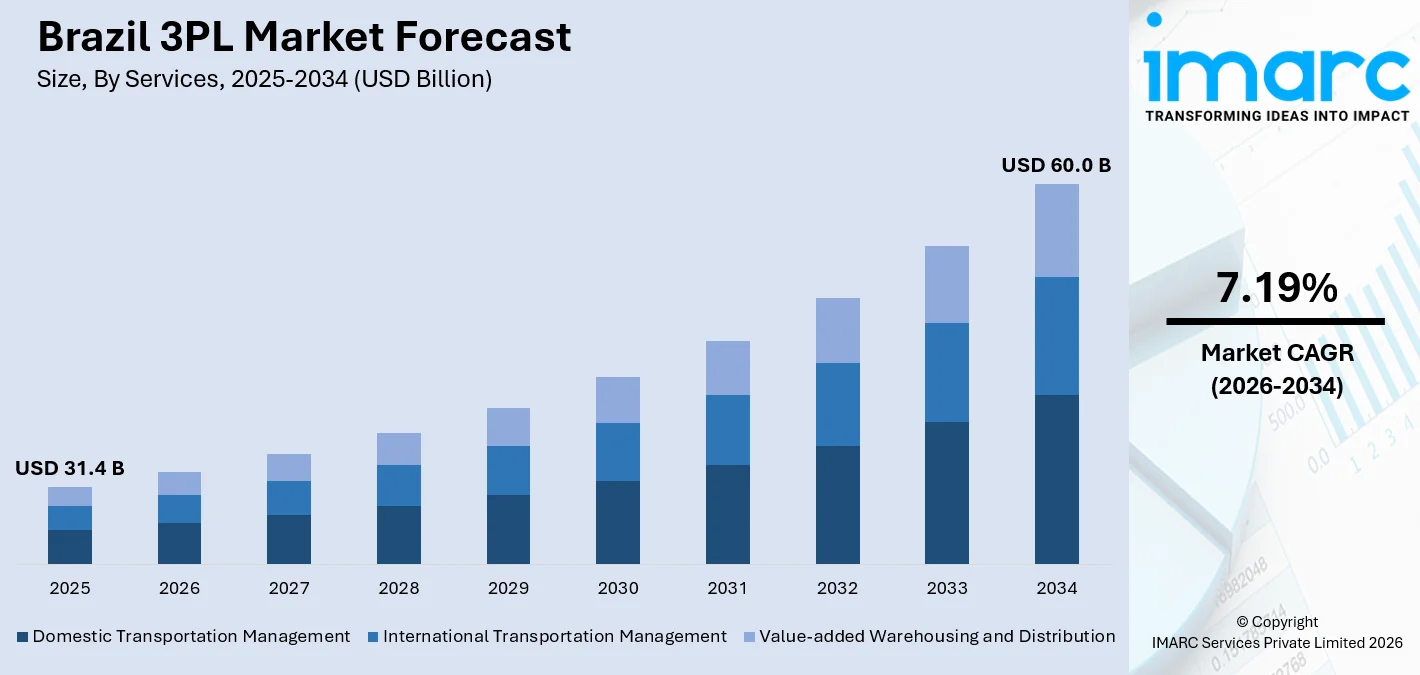

The Brazil 3PL market size, valued at USD 31.4 Billion in 2025, is projected to reach USD 60.0 Billion by 2034, growing at a CAGR of 7.19% from 2026-2034, propelled by rapid e-commerce expansion, rising domestic consumption from an urbanizing middle class, and government infrastructure investment programs reshaping road, rail, and port connectivity. Brazil's agribusiness sector generated USD 73.51 billion in 2024, structurally embedding 3PL demand into the country's agricultural supply chains and reinforcing the Brazil 3PL market share.

To get more information on this market Request Sample

Brazil 3PL Industry Analysis - Key Insights

- Domestic transportation management holds 38.2% of the services segment in 2025 - road freight accounts for approximately 65% in Brazil, making domestic routing, freight brokerage, and carrier management the foundational 3PL service layer across the country.

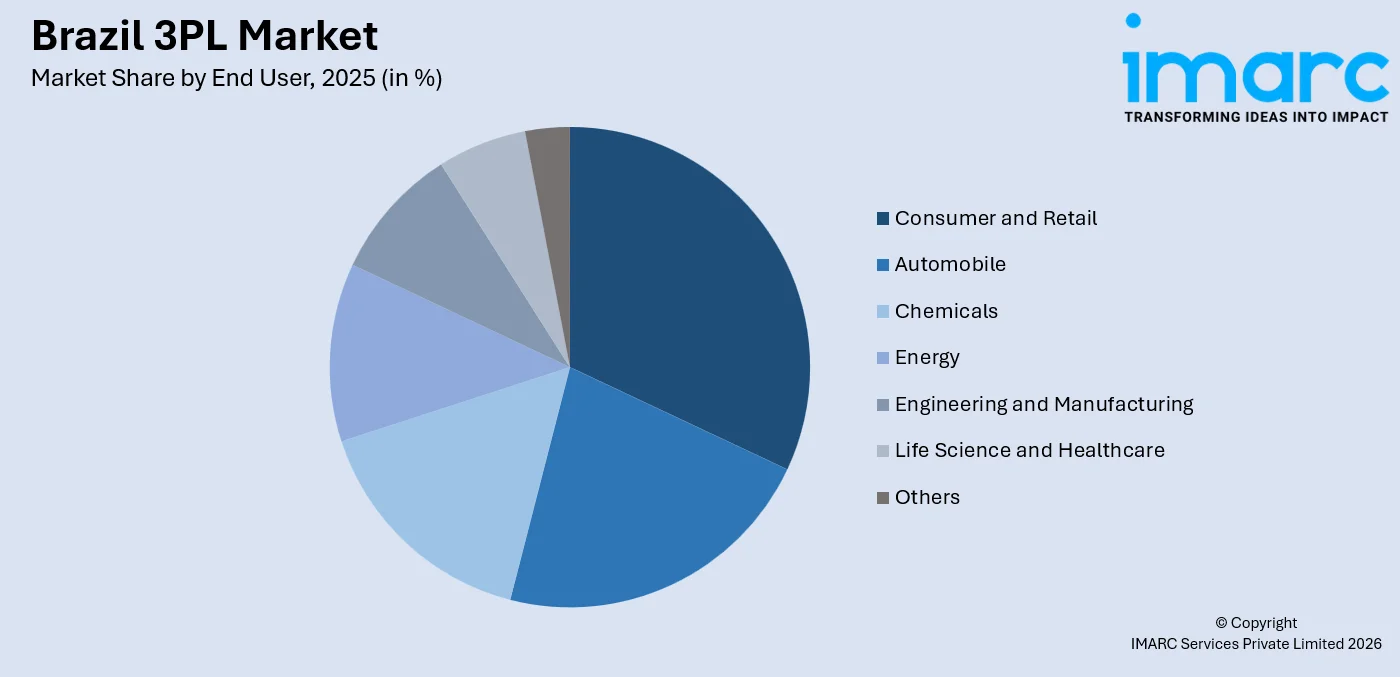

- Consumer and retail commands 30.4% of the end user segment in 2025 - e-commerce growth, modern retail distribution networks, and fast-moving consumer goods replenishment cycles are generating the single largest and fastest-growing demand category for 3PL services in Brazil.

- Southeast leads regionally at 52.6% in 2025 - this is the highest regional concentration across all segments, anchored by São Paulo and Rio de Janeiro's industrial density, Port of Santos container throughput, and the country's most advanced logistics park infrastructure.

Brazil 3PL Trends and Dynamics 2026

Market Trends

Infrastructure Development Accelerating Logistics Efficiency Across Brazil

Government investment in transport infrastructure is directly improving the operational conditions for 3PL providers across Brazil's vast territory. In February 2025, the Brazilian government announced a USD 11.9 billion investment in grain-harvest logistics, with major upgrades targeting road, rail, and port infrastructure, including key agricultural corridors and container terminal expansion at the Port of Santos. Projects under the Investment Partnerships Program are opening rail and road concessions to private participation, expanding multimodal capacity, and reducing transit delays that have historically constrained supply chain performance in hinterland regions.

E-Commerce Expansion Driving Demand for Last-Mile and Fulfillment Solutions

The rapid proliferation of e-commerce is redefining 3PL service requirements across Brazil, particularly for last-mile delivery, urban warehousing, and same-day fulfillment capabilities. In 2025, the Brazilian e-commerce sector generated USD 513.3 Billion, driving significant demand for agile, high-frequency logistics solutions. Urban micro-fulfillment centers, dark stores, and AI-assisted route planning are emerging as core Brazil 3PL market trends as providers invest to serve omnichannel retailers and cross-border marketplaces.

Digital Transformation and AI Adoption Reshaping 3PL Operations

Advanced technologies, including artificial intelligence, IoT-enabled warehouse management, and real-time GPS tracking, are fundamentally transforming how 3PL providers operate and differentiate in Brazil. In July 2024, Brazil announced a USD 4 billion national AI development plan through to 2028, embedding AI investment across healthcare, agriculture, and logistics, the latter directly accelerating TMS and WMS platform capabilities for 3PL operators. The convergence of AI-driven route optimization, automated sortation, and predictive inventory management is compressing delivery windows while reducing fuel and labor costs for carriers.

- Green Logistics and Fleet Decarbonization: Growing shipper sustainability mandates and regulatory pressure are driving 3PL providers to adopt biofuel-powered trucks, electric vehicles, and carbon-tracking platforms across their Brazil operations.

- Cold Chain Expansion for Life Sciences and Food: Pharmaceutical sovereign stockpile requirements, GLP-1 therapy distribution, and fresh food export growth are expanding demand for validated temperature-controlled logistics corridors.

Growth Drivers

Urbanization and Rising Domestic Consumption Expanding Distribution Networks

By 2025, around 91.4% of the population lived in cities, which has structurally increased demand for efficient, widespread distribution networks spanning dense metropolitan areas and secondary urban centers alike. As the middle class grows and consumer spending on durable goods, food, and retail rises, companies are turning to 3PL providers to manage distribution complexity without absorbing fixed logistics costs. The shift toward outsourced supply chain management is reinforcing Brazil's 3PL market growth as manufacturers, retailers, and e-commerce platforms prioritize scalability over asset ownership.

E-Commerce Platform Investment Multiplying Warehouse and Fulfillment Demand

Major e-commerce operators are committing unprecedented capital to expand logistics infrastructure across Brazil, directly increasing 3PL subcontracting and fulfillment volumes. Mercado Libre increased its Brazilian distribution center count to 21 by 2025. This initiative forms part of a BRL 23 billion investment program focused on strengthening domestic operations and enhancing the country’s logistics infrastructure. These platform-driven investments are pulling specialist 3PL providers deeper into fulfillment, returns management, and cross-docking operations.

Life Sciences and Healthcare Sector Generating Premium Cold Chain Volumes

Brazil's pharmaceutical and healthcare sectors are generating sustained, high-value demand for temperature-controlled logistics, GxP-compliant warehousing, and last-mile pharmaceutical distribution across the country's sprawling public health network. Novo Nordisk invested BRL 1.09 billion to upgrade its Montes Claros manufacturing plant, adding capacity for nationwide GLP-1 therapy distribution. The convergence of sovereign stockpile mandates, expanding cancer care infrastructure, and biologics manufacturing growth is strongly favorable to the Brazil 3PL market forecast.

- Government Infrastructure Investment Catalyzing Freight Efficiency: Road, rail, and port upgrades through the Investment Partnerships Program and the National Logistics Plan are reducing transit times, lowering per-unit freight costs, and enabling multimodal connectivity.

- Manufacturing Sector Recovery and Export Demand: Brazil's manufacturing sector growth and agricultural commodity export expansion are intensifying demand for integrated supply chain services, particularly in engineering and auto-parts logistics.

Market Restraints

High Logistics Costs and Overdependence on Road Freight: Brazilian logistics expenses consume a greater portion of the national gross domestic product than developed markets because the country relies excessively on road transportation for its extensive land area and lacks affordable multimodal transport options, such as cabotage and rail systems in several inland routes. The shipping costs create financial limitations that prevent shippers from earning profits while restricting 3PL logistics providers from increasing their profit margins.

Complex Tax and Regulatory Environment: The tax system of Brazil, which operates at multiple levels together with its state-specific ICMS freight rules and its difficult customs processes, generates challenges for 3PL operators who need to handle their cross-state freight operations. The different regulations that exist between states make it harder to conduct business operations while increasing expenses for delivering uniform logistics services that operate across the entire country.

Infrastructure Bottlenecks and Port Congestion: Despite ongoing investment, critical freight infrastructure constraints remain at major ports and key highway corridors. Port congestion, limited intermodal terminal capacity in secondary cities, and inadequate cold chain infrastructure in remote regions restrict 3PL providers' ability to offer consistent, end-to-end service quality across all of Brazil's diverse geography.

Brazil 3PL Market Segmentation Analysis

| Segment Category | Leading Segment | Market Share | Year |

|---|---|---|---|

| Services | Domestic Transportation Management | 38.2% | 2025 |

| End User | Consumer and Retail | 30.4% | 2025 |

| Region | Southeast | 52.6% | 2025 |

Services Insights

Domestic Transportation Management - 38.2% Market Share (2025) | Leading Services

Brazil maintains over 1.7 million kilometers of federal roads, the fourth-largest highway network globally. This structural dependence on road freight makes domestic transportation management, including freight brokerage, carrier management, and route optimization, the core service provided by 3PL operators. According to the Brazilian Association of Highway Concessionaires (ABCR), truck traffic in Brazil increased by more than 60% over the past two decades, reflecting the sustained growth in domestic freight volumes that underpin this segment's leading position.

|

Segment Breakdown Domestic Transportation Management (38.2%) · International Transportation Management · Value-added Warehousing and Distribution |

End User Insights

Access the comprehensive market breakdown Request Sample

Consumer and Retail - 30.4% Market Share (2025) | Leading End User

Brazil's retail logistics requirements span high-frequency store replenishment, direct-to-consumer parcel fulfillment, and reverse logistics management, each demanding specialized 3PL capabilities. The Brazilian e-commerce sector's sustained double-digit growth is compelling consumer brands and retail platforms to outsource fulfillment, last-mile coordination, and inventory management to 3PL specialists. Retailers operating omnichannel models require logistics partners capable of managing inventory across physical stores, dark stores, and direct delivery, simultaneously driving deep, multi-service 3PL contracts.

|

Segment Breakdown Consumer and Retail (30.4%) · Automobile · Chemicals · Energy · Engineering and Manufacturing · Life Science and Healthcare · Others |

Regional Insights

Southeast - 52.6% Market Share (2025) | Leading Region

The Southeast region dominates Brazil's 3PL market by an overwhelming majority, anchored by São Paulo and Rio de Janeiro, the country's two largest economic centers, and the Port of Santos. The convergence of consumer demand, manufacturing output, and port-linked import-export flows makes the Southeast the structurally irreplaceable center of Brazil's 3PL ecosystem. Campinas, Guarulhos, and the Greater ABC industrial belt in São Paulo state are the most active 3PL operational zones, while Rio de Janeiro's port precinct and Rio de Janeiro-Santos corridor support heavy industrial and energy sector logistics.

|

Regional Breakdown Southeast (52.6%) · South · Northeast · North · Central-West |

South:

Brazil's South region is home to major automotive, food processing, and agro-industrial supply chains across Paraná, Santa Catarina, and Rio Grande do Sul. Paraná hosts Brazilian manufacturing facilities for Renault, Volkswagen, and Volvo Trucks, generating dense just-in-time automotive logistics demand that requires highly coordinated 3PL providers with specialized auto-parts sequencing and cross-docking capabilities. Moreover, logistics operators adopt biofuel-powered trucks to cut CO2 emissions, reflecting the South's early adoption of sustainable logistics practices driven by European-linked supply chain standards.

Northeast:

The Northeast is an emerging logistics growth corridor, with Fortaleza, Recife, and Salvador emerging as 3PL hubs serving the region's expanding industrial and consumer markets. In April 2025, DP World opened a dedicated freight forwarding office in Brazil to strengthen logistics connectivity for exporters and importers across Latin America, reflecting growing international operator confidence in Brazil's interior markets, including the Northeast. The Port of Suape in Pernambuco and the Port of Pecém in Ceará are expanding capacity to support both consumer goods imports and growing Northeast industrial output.

North:

The North region's 3PL market is anchored by the Manaus Free Trade Zone, one of South America's most logistics-intensive manufacturing concentrations. Brazil's Suframa Industrial Park in Manaus generated BRL 174 billion in industrial output in 2023, producing electronics, two-wheelers, and chemical products that require specialist outbound distribution across Brazil's immense road and river freight network. The region's dependence on river logistics and limited road infrastructure creates specialized 3PL requirements distinct from those in Brazil's southern and southeastern corridors.

Central-West:

The Central-West is Brazil's agricultural powerhouse, with Mato Grosso, Mato Grosso do Sul, and Goiás accounting for Brazil's total soybean and grain output. Mato Grosso is the soy-producing state, generating enormous bulk grain and agricultural commodity freight volumes that feed export flows through the Port of Santos and northern Atlantic ports. The North-South Railway's expansion into the Central-West is transforming this region's logistics connectivity, enabling 3PL providers to build intermodal solutions that reduce freight costs for agri-commodity shippers.

Market Outlook 2026-2034

What is the future outlook of the Brazil 3PL market?

The Brazil 3PL market is expected to sustain steady revenue growth through 2034.

Brazil's 3PL sector is structurally positioned for durable above-average growth, supported by deepening e-commerce penetration, infrastructure modernization, pharmaceutical cold chain expansion, and sustained agricultural export volumes. Ongoing investment in digital logistics platforms, AI-driven routing, warehouse automation, and end-to-end supply chain visibility will progressively improve 3PL service quality and margin profiles. The convergence of urbanization, retail formalization, and manufacturing reshoring creates a compounding demand backdrop that solidifies the Brazil 3PL market outlook as one of Latin America's most resilient growth opportunities through the forecast period.

Brazil 3PL Market - Leading Key Players

The Brazil 3PL market features a competitive landscape of global logistics multinationals and domestic operators competing on service breadth, technology capabilities, geographic reach, and industry specialization. Leading players are investing in fleet decarbonization, warehouse automation, and digital supply chain integration to secure long-term contracts from automotive, consumer, healthcare, and agricultural clients across Brazil's diverse regional markets.

| Company | Leading Brands | Highlights |

|---|---|---|

| DHL Supply Chain (Deutsche Post AG) | DHL Supply Chain, DHL Global Forwarding | Announced EUR 500M investment in Latin America through 2028, focused on fleet decarbonization and real estate development; operates a fleet of 500 vehicles in Brazil with a strong life sciences and healthcare cold chain focus; invests in electric vehicles and Women at the Wheel sustainability program |

| A.P. Moller - Maersk | Maersk Logistics, Maersk Supply Chain | Expanding end-to-end supply chain capabilities in Brazil, combining ocean freight, inland logistics, and warehousing; strengthening cold chain and temperature-controlled distribution services for pharmaceutical and food clients. |

| BBM Logística SA | BBM Frota, BBM Supply Chain | Brazilian road freight and 3PL operator; extensive national trucking and distribution network; recognized strength in agricultural and consumer goods logistics across all Brazilian regions |

Some of the existing key players in the Brazil 3PL Market are JSL SA (Simpar Group), CEVA Logistics AG, Kuehne + Nagel International AG, etc.

Latest Development & News

- In April 2025, DP World opened a dedicated freight forwarding office in Campinas, São Paulo state, strengthening the company's logistics and freight forwarding capabilities across Latin America. The Campinas office positions DP World to serve exporters and importers in Brazil's most active inland logistics zone, connecting the São Paulo industrial belt to international shipping lanes through Santos and major Brazilian airports. The expansion reflects growing multinational confidence in Brazil's 3PL market potential during the 2026-2034 forecast period.

- In April 2025, Alonso Group, a specialist in global freight forwarding and customs brokerage, showcased its international 3PL capabilities at Intermodal South America 2025 in São Paulo, Latin America's largest logistics and transportation trade fair. The event highlighted the intensifying international dimension of Brazil's 3PL sector, with exhibitors emphasizing cross-border customs integration, multimodal freight coordination, and digital freight visibility platforms as differentiators in serving Brazil's expanding agribusiness and industrial export economy.

- In November 2024, Prumo, the Port of Açu, and Sarens signed a Memorandum of Understanding to develop specialist logistics solutions for Brazil's offshore wind energy industry, with a focus on heavy lifting and transportation of turbine components. The agreement positions the Port of Açu, located in Rio de Janeiro state, as a central hub for offshore wind logistics and manufacturing, directly supporting Brazil's renewable energy expansion and creating a new specialized 3PL vertical for energy transition infrastructure projects.

Brazil 3PL Market Report Scope:

| Report Features | Details |

|---|---|

| Base Year of the Analysis | 2025 |

| Historical Period | 2020-2025 |

| Forecast Period | 2026-2034 |

| Units | Billion USD |

| Scope of the Report |

Exploration of Historical and Forecast Trends, Industry Catalysts and Challenges, Segment-Wise Historical and Predictive Market Assessment:

|

| Services Covered | Domestic Transportation Management, International Transportation Management, Value-added Warehousing and Distribution |

| End Users Covered | Automobile, Chemicals, Consumer and Retail, Energy, Engineering and Manufacturing, Life Science and Healthcare, Others |

| Regions Covered | Southeast, South, Northeast, North, Central-West |

| Customization Scope | 10% Free Customization |

| Post-Sale Analyst Support | 10-12 Weeks |

| Delivery Format | PDF and Excel through Email (We can also provide the editable version of the report in PPT/Word format on special request) |

Frequently Asked Questions About the Brazil 3PL Market Report

The Brazil 3PL market was valued at USD 31.4 Billion in 2025.

The Brazil 3PL market is anticipated to reach a value of USD 60.0 Billion by 2034.

Domestic transportation management dominates the market with a share of 38.2%, driven by Brazil's structural dependence on road freight, which carries approximately 90% of the country's ton-mile cargo across its vast road network - the fourth largest in the world at over 1.7 million km.

Consumer and retail commands the market with a share of 30.4%, driven by rapid e-commerce expansion, modern retail distribution requirements, and rising consumer demand for faster delivery services across Brazil's increasingly urban and digitally connected population.

Some of the major players in the Brazil 3PL market include DHL Supply Chain (Deutsche Post AG), A.P. Moller - Maersk, BBM Logística SA, JSL SA (Simpar Group), CEVA Logistics AG, Kuehne + Nagel International AG, etc.

Key trends include government infrastructure investment programs such as a USD 11.9 billion investment in grain harvest logistics, accelerating e-commerce demand for urban fulfillment and last-mile delivery, widespread AI and IoT adoption improving operational efficiency, fleet electrification and biofuel adoption driven by shipper sustainability mandates, and the rapid expansion of cold chain logistics for pharmaceutical and fresh food distribution.

Southeast currently leads the Brazil 3PL market, accounting for a share of 52.6%. The region's dominance is driven by São Paulo and Rio de Janeiro's industrial concentration, Port of Santos throughput as Latin America's largest container gateway, and the country's densest logistics park infrastructure supporting both domestic distribution and international trade.

Growth is driven by Brazil's high urbanization rate in 2025, around 91.4% of the population living in cities, creating concentrated distribution demand, e-commerce expansion with online sales, government infrastructure investment modernizing freight corridors, life sciences cold chain demand from pharmaceutical manufacturing expansion, and manufacturing sector recovery, increasing outsourced logistics requirements across automotive and industrial supply chains.

Key challenges include Brazil's elevated logistics costs absorbing a disproportionate share of GDP due to road overdependence and limited multimodal alternatives, the complex multi-state ICMS tax and customs regulatory environment creating compliance burdens for national 3PL operators, and persistent infrastructure bottlenecks at major ports and congested highway corridors that restrict consistent end-to-end service quality across Brazil's diverse regional geographies.

Need more help?

- Speak to our experienced analysts for insights on the current market scenarios.

- Include additional segments and countries to customize the report as per your requirement.

- Gain an unparalleled competitive advantage in your domain by understanding how to utilize the report and positively impacting your operations and revenue.

- For further assistance, please connect with our analysts.

Request Customization

Request Customization

Speak to an Analyst

Speak to an Analyst

Request Brochure

Request Brochure

Inquire Before Buying

Inquire Before Buying

Benefits of Customization

- Personalize this research

- Triangulate with your data

- Get data as per your format and definition

- Gain a deeper dive into a specific application, geography, customer, or competitor

- Any level of personalization

Get in Touch With Us

UNITED STATES

Phone: +1-201-971-6302

INDIA

Phone: +91-120-433-0800

UNITED KINGDOM

Phone: +44-753-714-6104

Email: [email protected]

Client Testimonials

.webp)